HI3042 Taxation Law T2 2017 Individual Assignment Case Studies

VerifiedAdded on 2020/04/07

|10

|1678

|497

Homework Assignment

AI Summary

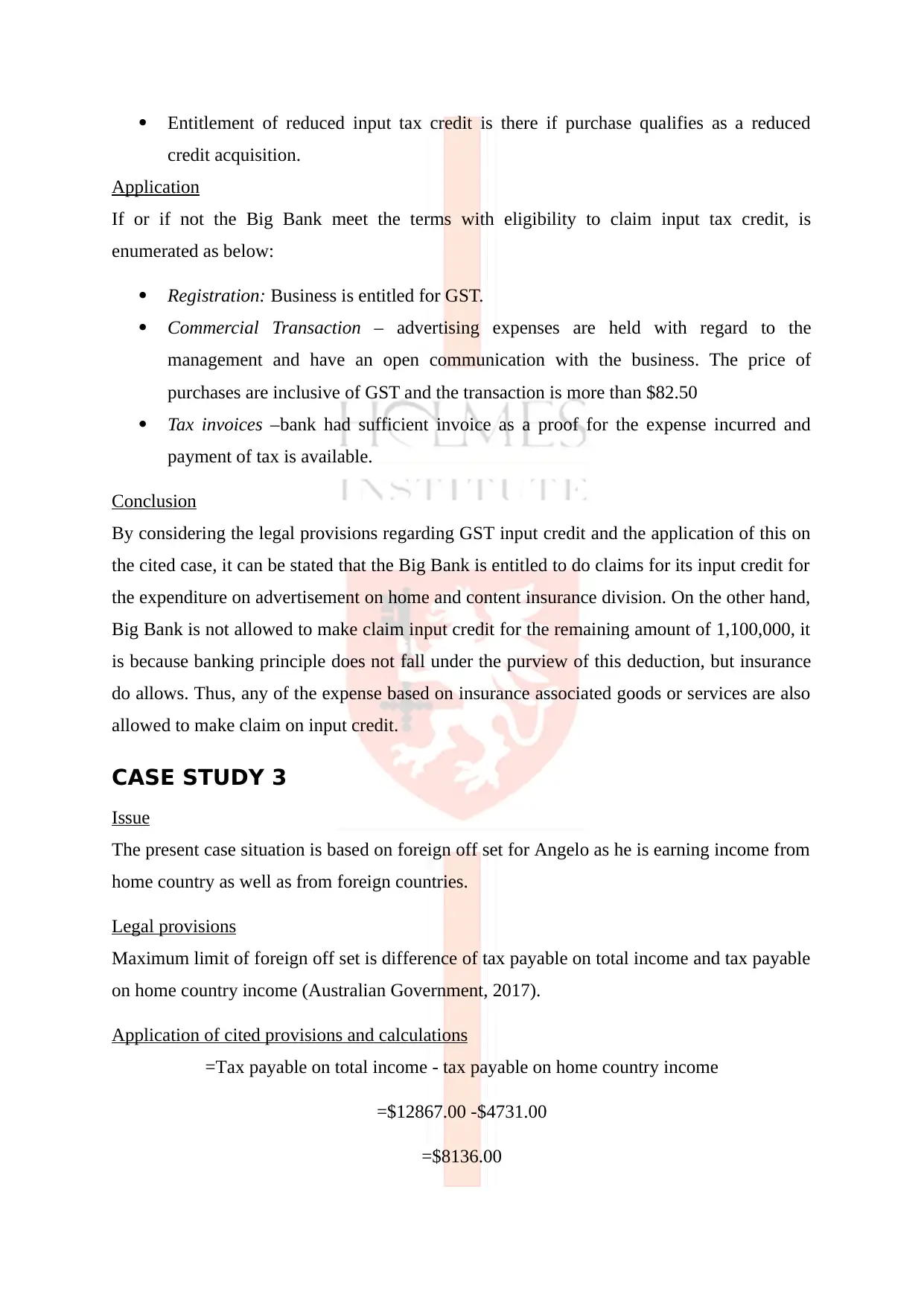

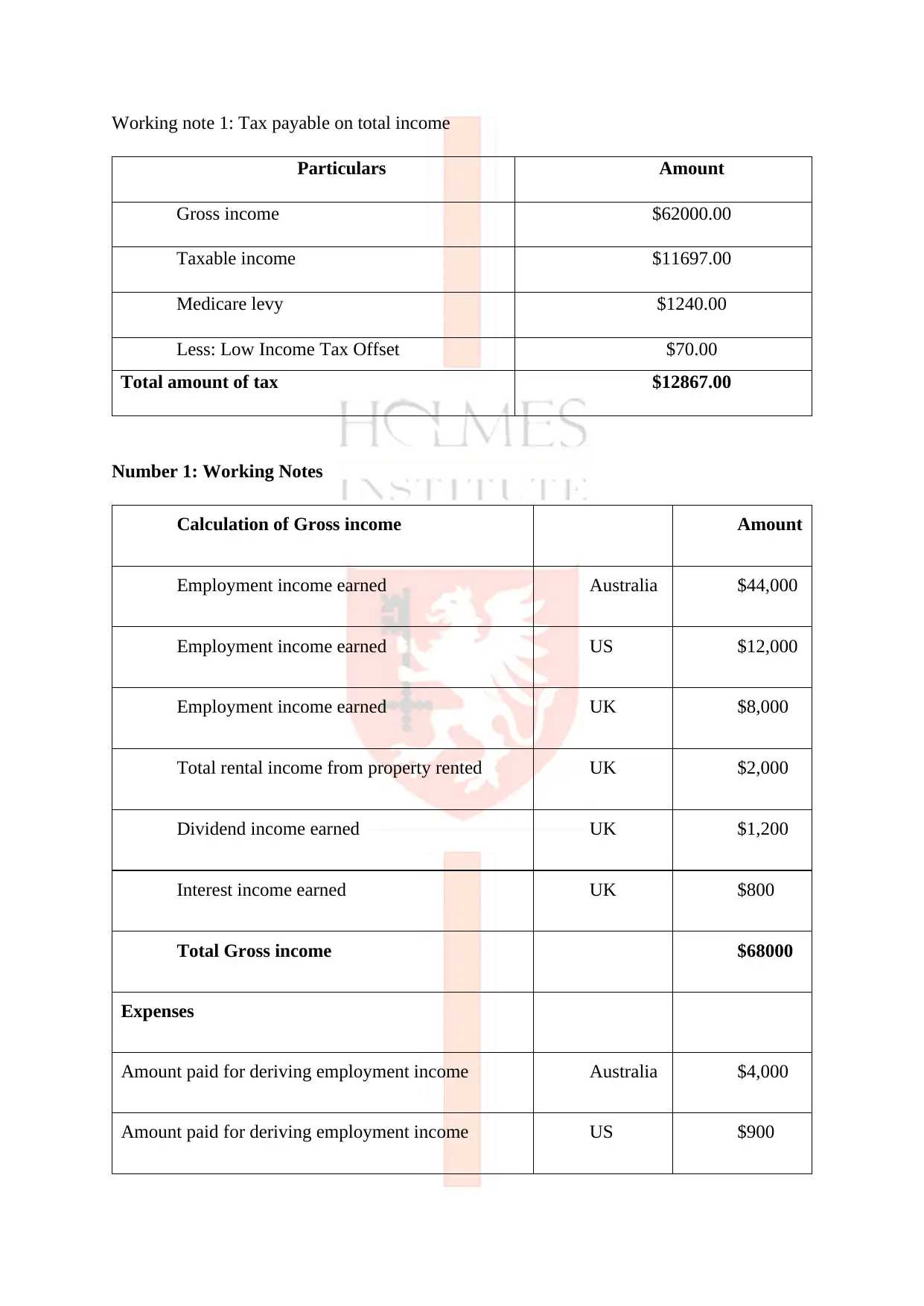

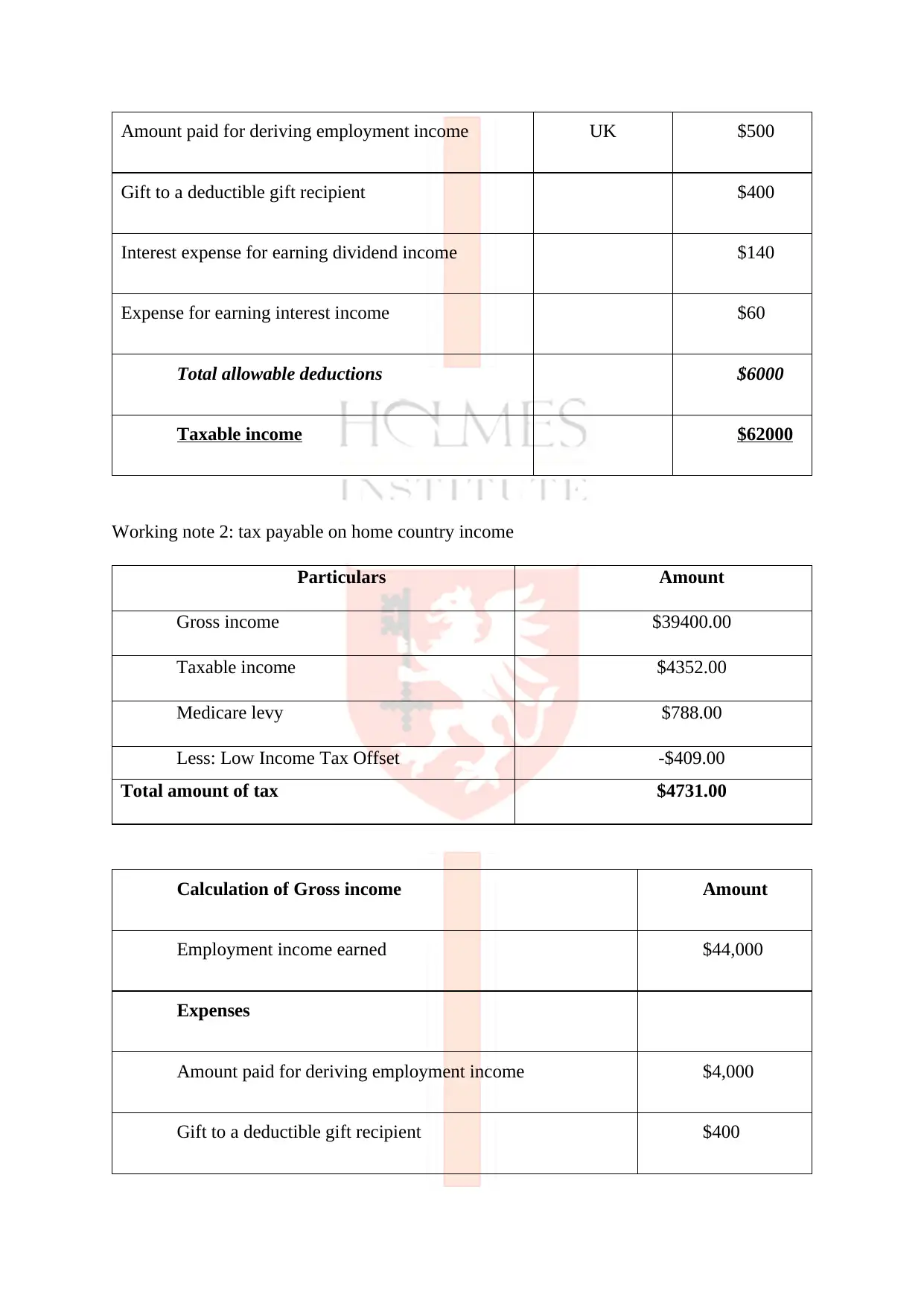

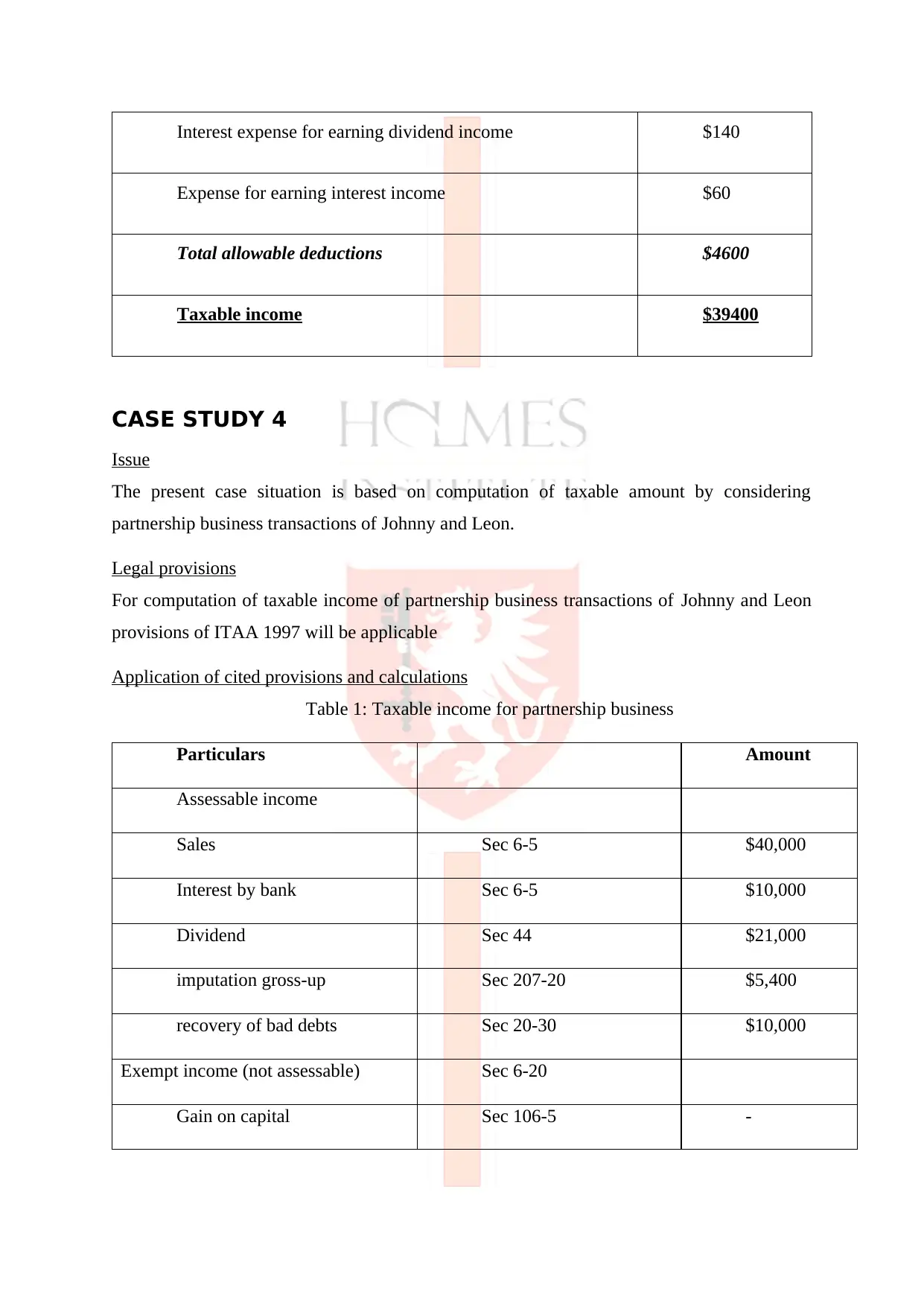

This document presents a comprehensive taxation law assignment, meticulously analyzing four case studies. The first case study assesses the deductibility of various expenses under section 8(1) of the ITAA 1997, covering capital and revenue expenditures. Case study two examines the entitlement of Big Bank to input tax credits for advertising expenses, considering GST provisions related to financial supplies. The third case study focuses on calculating a foreign offset for an individual with income from multiple countries, detailing the application of foreign income tax offset rules. The final case study involves computing the taxable income of a partnership, incorporating assessable income, deductions, and relevant legal provisions, including considerations for salaries, fringe benefits tax, and various business expenses. Each case study includes a detailed analysis of the issues, relevant legal provisions, and their application, complete with calculations and conclusions.

1 out of 10

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.