Taxation Law Homework: Assessment of Tax Scenarios and Income

VerifiedAdded on 2020/02/18

|11

|2555

|39

Homework Assignment

AI Summary

This assignment delves into various aspects of Australian taxation law, providing detailed answers to two key questions. Question 1 analyzes ten different tax scenarios, determining whether specific incomes are taxable or deductible based on established tax rulings. The analysis covers fringe benefit tax, damage payments, gifts, club funds, income from sports performance, building apprentice expenditures, education expenses, artist expenditures, travel expenses, and official travel expenses. Question 2 focuses on calculating the assessable income, taxable income, and tax payable for an individual named Manpreet, considering gross salary, foreign income, and deductions. The solution includes a comprehensive table outlining the financial calculations and a discussion on the deductibility of certain expenses, referencing relevant sections of the Income Tax Assessment Act and supporting case laws like Lunney v. FC of T and Ronpibon Tin NL v. FC of T.

Running head: TAXATION LAW

Taxation Law

Name of the Student:

Name of the University:

Author’s Note:

Course ID:

Taxation Law

Name of the Student:

Name of the University:

Author’s Note:

Course ID:

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

1TAXATION LAW

Table of Contents

Answer to Question 1:.....................................................................................................................2

Answer to Part i:..........................................................................................................................2

Answer to Part ii:.........................................................................................................................2

Answer to Part iii:........................................................................................................................3

Answer to Part iv:........................................................................................................................3

Answer to Part v:.........................................................................................................................4

Answer to Part vi:........................................................................................................................4

Answer to Part vii:.......................................................................................................................5

Answer to Part viii:......................................................................................................................5

Answer to Part ix:........................................................................................................................6

Answer to Part x:.........................................................................................................................6

Answer to Question 2:.....................................................................................................................7

References:......................................................................................................................................9

Table of Contents

Answer to Question 1:.....................................................................................................................2

Answer to Part i:..........................................................................................................................2

Answer to Part ii:.........................................................................................................................2

Answer to Part iii:........................................................................................................................3

Answer to Part iv:........................................................................................................................3

Answer to Part v:.........................................................................................................................4

Answer to Part vi:........................................................................................................................4

Answer to Part vii:.......................................................................................................................5

Answer to Part viii:......................................................................................................................5

Answer to Part ix:........................................................................................................................6

Answer to Part x:.........................................................................................................................6

Answer to Question 2:.....................................................................................................................7

References:......................................................................................................................................9

2TAXATION LAW

Answer to Question 1:

Answer to Part i:

The pertinent point provided on the part of the airline organisation does not fall under

taxation ruling. This is a direct indication that this kind of income could not be adjudged as

income. However, there is absence of specific rules regarding the organisational benefits to the

staffs, which fall under the fringe benefit tax directly. Various scenarios are inherent, in which

the reward points could be taken into account under fringe benefit tax. For example, if a staff

receives a reward point that the employer has offered as benefits, it could be adjudged as taxable

amount falling under the fringe benefit tax. The second example is primarily at the time the

reward points are offered to the staffs in a specific arrangement with the organisation. However,

in this specific case, there is absence of any identified circumstance that signifies directly the

absence of taxation on the reward points provided on the part of the airline organisation

(Barkoczy, 2016).

Answer to Part ii:

The provided case primarily signifies that damage payment has been carried out on the

part of the service receiver. This signifies directly that the service receiver is required to carry the

burden of the overall tax amount. The conducted damage to the capital asset does not fall under

the taxable amount related to the receiver of payment. This has direct indication that the service

receiver is required to incur the entire tax amount for the capital damage, which is carried out.

However, some assets need to be taken into consideration before the identification of the taxable

asset. This need to be taken into account as capital and the organisation could make thorough

utilisation of the same. Along with this, the asset needs to be depreciated as well under the clause

Answer to Question 1:

Answer to Part i:

The pertinent point provided on the part of the airline organisation does not fall under

taxation ruling. This is a direct indication that this kind of income could not be adjudged as

income. However, there is absence of specific rules regarding the organisational benefits to the

staffs, which fall under the fringe benefit tax directly. Various scenarios are inherent, in which

the reward points could be taken into account under fringe benefit tax. For example, if a staff

receives a reward point that the employer has offered as benefits, it could be adjudged as taxable

amount falling under the fringe benefit tax. The second example is primarily at the time the

reward points are offered to the staffs in a specific arrangement with the organisation. However,

in this specific case, there is absence of any identified circumstance that signifies directly the

absence of taxation on the reward points provided on the part of the airline organisation

(Barkoczy, 2016).

Answer to Part ii:

The provided case primarily signifies that damage payment has been carried out on the

part of the service receiver. This signifies directly that the service receiver is required to carry the

burden of the overall tax amount. The conducted damage to the capital asset does not fall under

the taxable amount related to the receiver of payment. This has direct indication that the service

receiver is required to incur the entire tax amount for the capital damage, which is carried out.

However, some assets need to be taken into consideration before the identification of the taxable

asset. This need to be taken into account as capital and the organisation could make thorough

utilisation of the same. Along with this, the asset needs to be depreciated as well under the clause

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

3TAXATION LAW

of depreciation, which needs to be depicted in the annual report. Hence, the payment of

compensation related to crane is not taken into account under taxable income (Braithwaite,

2017).

Answer to Part iii:

The provided case study primarily depicts the presence of pertinent gift, which the

supplier has provided to the owner of the nightclub. However, in accordance with the taxation

law of Australia for the individuals, small kind gifts are not taken into account pertinently.

Conversely, the big-sized gifts and expensive gifts are considered as well for the overall taxable

income. Moreover, the big-sized gifts, which could be converted into amounts of greater cash

value or cash, could be taken into account under the receiver’s taxable income. Hence, based on

the case scenario, it has been observed that the nightclub manager has obtained the entire

package for the overseas holidays having pertinent monetary benefits received on the part of the

manager. This primarily denotes that the individual taxation of the manager would comprise of

the entire overseas packages provided on the part of the supplier (Cao et al., 2015).

Answer to Part iv:

The whole scenario primarily denotes that the additional funds have been accumulated

from the members of the club in order to buy canoe. This has primarily enabled in obtaining an

overview that the individuals utilising the donated funds to the canoe club is not deductible under

the taxation rule. Hence, any return provided from the club could not be adjudged as excess

income. The entire income for the individual members has induced the entire funds, which are

paid to the club. Hence, the total income of the individual members would have no influence on

the monetary returns provided on the part of the club as excess income and the depiction would

be made in the form of taxable income (Davis et al., 2015).

of depreciation, which needs to be depicted in the annual report. Hence, the payment of

compensation related to crane is not taken into account under taxable income (Braithwaite,

2017).

Answer to Part iii:

The provided case study primarily depicts the presence of pertinent gift, which the

supplier has provided to the owner of the nightclub. However, in accordance with the taxation

law of Australia for the individuals, small kind gifts are not taken into account pertinently.

Conversely, the big-sized gifts and expensive gifts are considered as well for the overall taxable

income. Moreover, the big-sized gifts, which could be converted into amounts of greater cash

value or cash, could be taken into account under the receiver’s taxable income. Hence, based on

the case scenario, it has been observed that the nightclub manager has obtained the entire

package for the overseas holidays having pertinent monetary benefits received on the part of the

manager. This primarily denotes that the individual taxation of the manager would comprise of

the entire overseas packages provided on the part of the supplier (Cao et al., 2015).

Answer to Part iv:

The whole scenario primarily denotes that the additional funds have been accumulated

from the members of the club in order to buy canoe. This has primarily enabled in obtaining an

overview that the individuals utilising the donated funds to the canoe club is not deductible under

the taxation rule. Hence, any return provided from the club could not be adjudged as excess

income. The entire income for the individual members has induced the entire funds, which are

paid to the club. Hence, the total income of the individual members would have no influence on

the monetary returns provided on the part of the club as excess income and the depiction would

be made in the form of taxable income (Davis et al., 2015).

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

4TAXATION LAW

Answer to Part v:

The entire case scenario primarily denotes that the pertinent payment has been carried out

to a football player on the part of a television organisation. In accordance with the “Taxation

ruling in Australian TR 1999/17”, it primarily signifies that any sports personality making

income from the individuals related to the sports performance need to be taken into account

under taxable income. Moreover, this has direct indication that the pertinent income generated on

the part of the football player from the television organisation would be taken into account like

the taxable income. Henceforth, the individual taxation law denotes that the pertinent taxes are

required to be incurred on the part of the football player, since the amount provided on the part

of the television organisation is considered directly in the form of taxable income. Such taxable

income is required to be taken into account under the “Rulings TR 1999/17”, in which the

pertinent taxes are required to be incurred on the part of the sports person (Douglas et al., 2014).

Answer to Part vi:

The provided case study primarily depicts that the expenditures pertaining to building

qualification for the apprentice of the building has been carried out. In compliance with the “TR

95.22”, pertinent consideration for the allowance deduction to the staffs of the construction

organisation could be detected. This signifies mainly that the pertinent expenditures carried out

on the building apprentice is subtracted pertinently for the construction organisation. Hence, the

total expenditures carried out on the part of the construction organisation could be utilised as

deductible expenditures, which minimise the entire taxable amount of the organisation.

According to “TR 95/22”, some pertinent abbreviations are used, which are summarised briefly

as follows:

Answer to Part v:

The entire case scenario primarily denotes that the pertinent payment has been carried out

to a football player on the part of a television organisation. In accordance with the “Taxation

ruling in Australian TR 1999/17”, it primarily signifies that any sports personality making

income from the individuals related to the sports performance need to be taken into account

under taxable income. Moreover, this has direct indication that the pertinent income generated on

the part of the football player from the television organisation would be taken into account like

the taxable income. Henceforth, the individual taxation law denotes that the pertinent taxes are

required to be incurred on the part of the football player, since the amount provided on the part

of the television organisation is considered directly in the form of taxable income. Such taxable

income is required to be taken into account under the “Rulings TR 1999/17”, in which the

pertinent taxes are required to be incurred on the part of the sports person (Douglas et al., 2014).

Answer to Part vi:

The provided case study primarily depicts that the expenditures pertaining to building

qualification for the apprentice of the building has been carried out. In compliance with the “TR

95.22”, pertinent consideration for the allowance deduction to the staffs of the construction

organisation could be detected. This signifies mainly that the pertinent expenditures carried out

on the building apprentice is subtracted pertinently for the construction organisation. Hence, the

total expenditures carried out on the part of the construction organisation could be utilised as

deductible expenditures, which minimise the entire taxable amount of the organisation.

According to “TR 95/22”, some pertinent abbreviations are used, which are summarised briefly

as follows:

5TAXATION LAW

The trainees, labours, apprentices and carpenters utilised for building are considered

primarily under the ruling.

The work of the supervisors conducted for building purpose and work of the project

manager is taken into account under this ruling.

Hence, the total expenditures identified from the assessment of the case study majorly

signifies that expenditure carried out on the apprentice of the building is stated directly in the

form of compensation, which is deductible under the Australian taxation law (Lang, 2014).

Answer to Part vii:

The pertinent condition primarily signifies that the pertinent expenditures are carried out

majorly for a short course in art management for becoming an art director. This has direct

indication that the total expenditures are carried out for enhancing the overall individual career.

This falls under the Australian taxation law and it is deductible from the overall amount of

taxation. However, various criteria are inherent that is required to be assessed before the

expenses are detected as deductible from the taxable income. Moreover, pertinent criteria are

needed to be followed like the module of education and software conducted on the part of the

individual, which is required to enhance its overall future income. Moreover, the course related

to short-term fees is allowed primarily as deduction, while ignoring the other education facilities.

Answer to Part viii:

The situation indicates that the pertinent expenditures related to dresses and make-up are

carried out on the part of the individual. There is deduction of pertinent taxation for the

expenditures carried out on the artist about to perform. Such tax deductions are restricted

primarily to the subsequent or specific individuals (artists) and this could be provided as the

The trainees, labours, apprentices and carpenters utilised for building are considered

primarily under the ruling.

The work of the supervisors conducted for building purpose and work of the project

manager is taken into account under this ruling.

Hence, the total expenditures identified from the assessment of the case study majorly

signifies that expenditure carried out on the apprentice of the building is stated directly in the

form of compensation, which is deductible under the Australian taxation law (Lang, 2014).

Answer to Part vii:

The pertinent condition primarily signifies that the pertinent expenditures are carried out

majorly for a short course in art management for becoming an art director. This has direct

indication that the total expenditures are carried out for enhancing the overall individual career.

This falls under the Australian taxation law and it is deductible from the overall amount of

taxation. However, various criteria are inherent that is required to be assessed before the

expenses are detected as deductible from the taxable income. Moreover, pertinent criteria are

needed to be followed like the module of education and software conducted on the part of the

individual, which is required to enhance its overall future income. Moreover, the course related

to short-term fees is allowed primarily as deduction, while ignoring the other education facilities.

Answer to Part viii:

The situation indicates that the pertinent expenditures related to dresses and make-up are

carried out on the part of the individual. There is deduction of pertinent taxation for the

expenditures carried out on the artist about to perform. Such tax deductions are restricted

primarily to the subsequent or specific individuals (artists) and this could be provided as the

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

6TAXATION LAW

pertinent exemptions. The performing artist depicted in the rule of taxation could be singer,

actor, musician, artist, dancer and circus performer. Hence, any type of expenditures carried out

on the performing artist is allowed in the form of a deduction on the taxable amount. Therefore,

the expenditures carried out on the dresses and makeup that are associated with work are

deductible from the overall taxable income (Novikov, Ling & Kordzakhia, 2014).

Answer to Part ix:

The situation denotes that the total expenditures are carried out on the part of an

individual travelling from house to the workplace. This solely represents that the pertinent

deductions could be possible under the law of taxation, in which the travelling for work purpose

could be subtracted from the amount of taxation. However, any type of non-official expenditure

carried out on travelling could not be detected in the form of deductible expenditures from the

taxable income. In addition, it has been assumed that the expenditures related to travelling from

home to office are for office work, the nature of which is deductible in accordance with the

taxation law of Australia. However, on a various assumption, if the travelling expenses are for

personal use, it could be deducted in compliance with the taxation law of Australia. Hence, the

ascertainment of expenditure is crucial to identify the total measure to be carried out on taxable

income (Saad, 2014).

Answer to Part x:

The provided case study primarily denotes that the total travelling expenses are mainly

carried out on the part of the individual for official purposes. The total expenditures carried out

on travel is mainly productive in nature in conformance to the taxation law of Australia. In

accordance with this taxation law of the nation, any type of expenditure carried out for official

purposes are deductible in nature, which could be utilised directly to minimise the taxable

pertinent exemptions. The performing artist depicted in the rule of taxation could be singer,

actor, musician, artist, dancer and circus performer. Hence, any type of expenditures carried out

on the performing artist is allowed in the form of a deduction on the taxable amount. Therefore,

the expenditures carried out on the dresses and makeup that are associated with work are

deductible from the overall taxable income (Novikov, Ling & Kordzakhia, 2014).

Answer to Part ix:

The situation denotes that the total expenditures are carried out on the part of an

individual travelling from house to the workplace. This solely represents that the pertinent

deductions could be possible under the law of taxation, in which the travelling for work purpose

could be subtracted from the amount of taxation. However, any type of non-official expenditure

carried out on travelling could not be detected in the form of deductible expenditures from the

taxable income. In addition, it has been assumed that the expenditures related to travelling from

home to office are for office work, the nature of which is deductible in accordance with the

taxation law of Australia. However, on a various assumption, if the travelling expenses are for

personal use, it could be deducted in compliance with the taxation law of Australia. Hence, the

ascertainment of expenditure is crucial to identify the total measure to be carried out on taxable

income (Saad, 2014).

Answer to Part x:

The provided case study primarily denotes that the total travelling expenses are mainly

carried out on the part of the individual for official purposes. The total expenditures carried out

on travel is mainly productive in nature in conformance to the taxation law of Australia. In

accordance with this taxation law of the nation, any type of expenditure carried out for official

purposes are deductible in nature, which could be utilised directly to minimise the taxable

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

7TAXATION LAW

income. In accordance with the scenario, the total expenditures have been carried out from one

place to another. In this case, it could be utilised as a deduction amount for the overall taxable

income. Hence, the total expenditures could be subtracted on the part of the employer from its

taxable income.

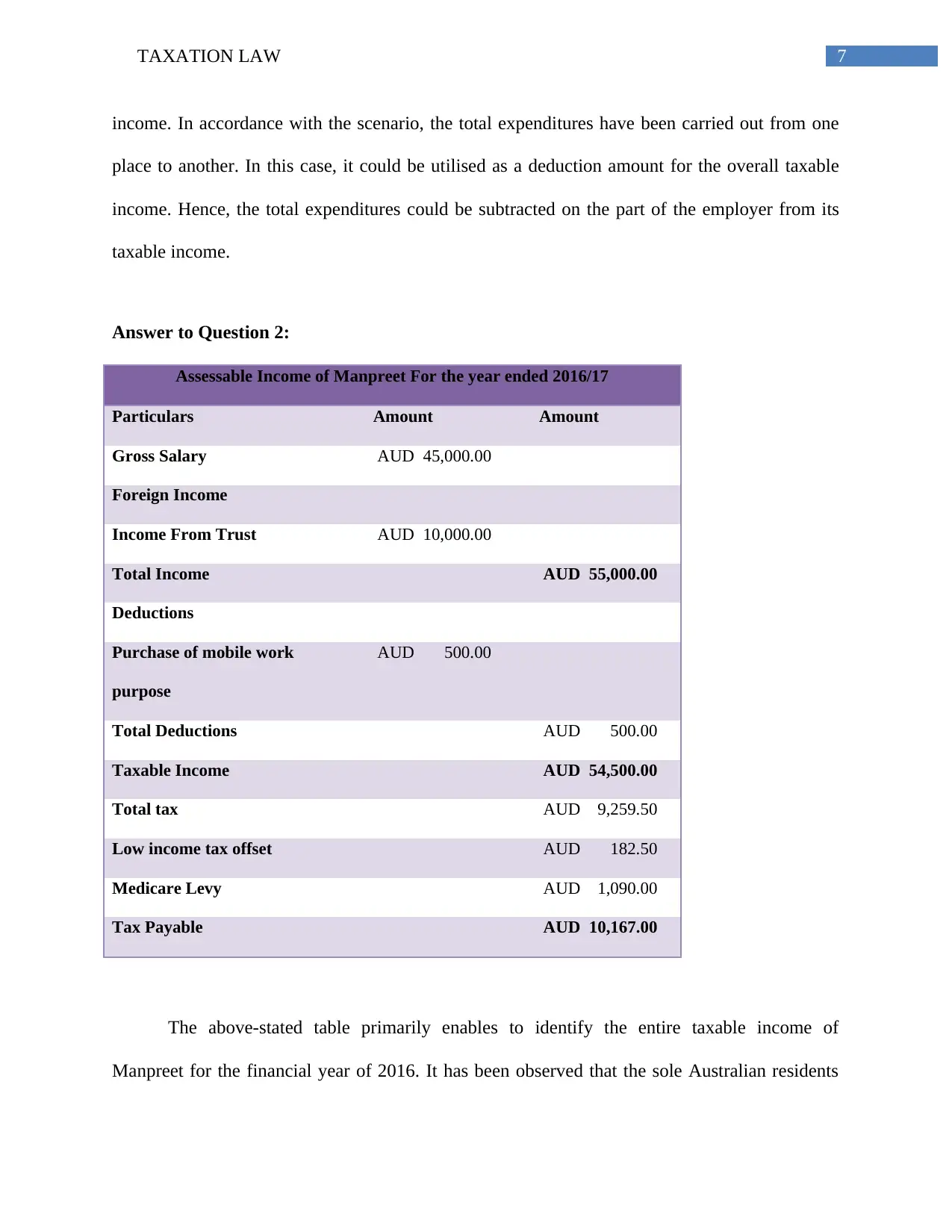

Answer to Question 2:

Assessable Income of Manpreet For the year ended 2016/17

Particulars Amount Amount

Gross Salary AUD 45,000.00

Foreign Income

Income From Trust AUD 10,000.00

Total Income AUD 55,000.00

Deductions

Purchase of mobile work

purpose

AUD 500.00

Total Deductions AUD 500.00

Taxable Income AUD 54,500.00

Total tax AUD 9,259.50

Low income tax offset AUD 182.50

Medicare Levy AUD 1,090.00

Tax Payable AUD 10,167.00

The above-stated table primarily enables to identify the entire taxable income of

Manpreet for the financial year of 2016. It has been observed that the sole Australian residents

income. In accordance with the scenario, the total expenditures have been carried out from one

place to another. In this case, it could be utilised as a deduction amount for the overall taxable

income. Hence, the total expenditures could be subtracted on the part of the employer from its

taxable income.

Answer to Question 2:

Assessable Income of Manpreet For the year ended 2016/17

Particulars Amount Amount

Gross Salary AUD 45,000.00

Foreign Income

Income From Trust AUD 10,000.00

Total Income AUD 55,000.00

Deductions

Purchase of mobile work

purpose

AUD 500.00

Total Deductions AUD 500.00

Taxable Income AUD 54,500.00

Total tax AUD 9,259.50

Low income tax offset AUD 182.50

Medicare Levy AUD 1,090.00

Tax Payable AUD 10,167.00

The above-stated table primarily enables to identify the entire taxable income of

Manpreet for the financial year of 2016. It has been observed that the sole Australian residents

8TAXATION LAW

are responsible for providing pertinent taxes to the government, which would be decided with the

help of considerable residential method in ascertaining the requirement for taxation. Based on the

case study, it has been found that Manpreet has been residing in Australia for above six months

and as a result; such duration of stay has helped the person in becoming the resident of Australia.

In this case, there is need for payment of pertinent taxes. Manpreet earns nearly $45,000 from the

part time job that directly assures that the person is required to incur the pertinent individual tax

(Taylor & Richardson, 2013).

Manpreet has incurred various kinds of expenditures for education purposes, which does

not signify any type of improvement in income from part time work. Hence, both computer

expenditures and educational expenditures could not be deducted from the overall amount of

taxation. In accordance with “Section 8-1 of the Income Tax Assessment Act”, the expense

having domestic ort\ private nature could not be subtracted under this act. Therefore, both the

expenditures incurred for education and computer could not be deducted under the taxation law

of Australia. However, any type of expenditure carried out for improving the income or career of

the individual is deductible under the taxation law of Australia. There are certain case laws that

could be utilised to support the individual taxation law of Australia (Tran-Nam, Evans & Lignier,

2014). These laws include “Lunney v. FC of T; Hayley v. FC of T (1958) 100 CLR 478”,

“Ronpibon Tin NL v. FC of T (1949)” and “FC of T v. M I Roberts 92 ATC 4787”.

are responsible for providing pertinent taxes to the government, which would be decided with the

help of considerable residential method in ascertaining the requirement for taxation. Based on the

case study, it has been found that Manpreet has been residing in Australia for above six months

and as a result; such duration of stay has helped the person in becoming the resident of Australia.

In this case, there is need for payment of pertinent taxes. Manpreet earns nearly $45,000 from the

part time job that directly assures that the person is required to incur the pertinent individual tax

(Taylor & Richardson, 2013).

Manpreet has incurred various kinds of expenditures for education purposes, which does

not signify any type of improvement in income from part time work. Hence, both computer

expenditures and educational expenditures could not be deducted from the overall amount of

taxation. In accordance with “Section 8-1 of the Income Tax Assessment Act”, the expense

having domestic ort\ private nature could not be subtracted under this act. Therefore, both the

expenditures incurred for education and computer could not be deducted under the taxation law

of Australia. However, any type of expenditure carried out for improving the income or career of

the individual is deductible under the taxation law of Australia. There are certain case laws that

could be utilised to support the individual taxation law of Australia (Tran-Nam, Evans & Lignier,

2014). These laws include “Lunney v. FC of T; Hayley v. FC of T (1958) 100 CLR 478”,

“Ronpibon Tin NL v. FC of T (1949)” and “FC of T v. M I Roberts 92 ATC 4787”.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

9TAXATION LAW

References:

Barkoczy, S. (2016). Foundations of Taxation Law 2016. OUP Catalogue.

Braithwaite, V. (Ed.). (2017). Taxing democracy: Understanding tax avoidance and evasion.

Routledge.

Cao, L., Hosking, A., Kouparitsas, M., Mullaly, D., Rimmer, X., Shi, Q., ... & Wende, S. (2015).

Understanding the economy-wide efficiency and incidence of major Australian

taxes. Treasury WP, 1.

Davis, A. K., Guenther, D. A., Krull, L. K., & Williams, B. M. (2015). Do socially responsible

firms pay more taxes?. The Accounting Review, 91(1), 47-68.

Douglas, H., Bartlett, F., Luker, T., & Hunter, R. (Eds.). (2014). Australian feminist judgments:

Righting and rewriting law. Bloomsbury Publishing.

Lang, M. (2014). Introduction to the law of double taxation conventions. Linde Verlag GmbH.

Novikov, A. A., Ling, T. G., & Kordzakhia, N. (2014). Pricing of volume-weighted average

options: Analytical approximations and numerical results. In Inspired by Finance (pp.

461-474). Springer International Publishing.

Saad, N. (2014). Tax knowledge, tax complexity and tax compliance: Taxpayers’

view. Procedia-Social and Behavioral Sciences, 109, 1069-1075.

Taylor, G., & Richardson, G. (2013). The determinants of thinly capitalized tax avoidance

structures: Evidence from Australian firms. Journal of International Accounting,

Auditing and Taxation, 22(1), 12-25.

References:

Barkoczy, S. (2016). Foundations of Taxation Law 2016. OUP Catalogue.

Braithwaite, V. (Ed.). (2017). Taxing democracy: Understanding tax avoidance and evasion.

Routledge.

Cao, L., Hosking, A., Kouparitsas, M., Mullaly, D., Rimmer, X., Shi, Q., ... & Wende, S. (2015).

Understanding the economy-wide efficiency and incidence of major Australian

taxes. Treasury WP, 1.

Davis, A. K., Guenther, D. A., Krull, L. K., & Williams, B. M. (2015). Do socially responsible

firms pay more taxes?. The Accounting Review, 91(1), 47-68.

Douglas, H., Bartlett, F., Luker, T., & Hunter, R. (Eds.). (2014). Australian feminist judgments:

Righting and rewriting law. Bloomsbury Publishing.

Lang, M. (2014). Introduction to the law of double taxation conventions. Linde Verlag GmbH.

Novikov, A. A., Ling, T. G., & Kordzakhia, N. (2014). Pricing of volume-weighted average

options: Analytical approximations and numerical results. In Inspired by Finance (pp.

461-474). Springer International Publishing.

Saad, N. (2014). Tax knowledge, tax complexity and tax compliance: Taxpayers’

view. Procedia-Social and Behavioral Sciences, 109, 1069-1075.

Taylor, G., & Richardson, G. (2013). The determinants of thinly capitalized tax avoidance

structures: Evidence from Australian firms. Journal of International Accounting,

Auditing and Taxation, 22(1), 12-25.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

10TAXATION LAW

Tran-Nam, B., Evans, C., & Lignier, P. (2014). Personal taxpayer compliance costs: Recent

evidence from Australia. Austl. Tax F., 29, 137.

Tran-Nam, B., Evans, C., & Lignier, P. (2014). Personal taxpayer compliance costs: Recent

evidence from Australia. Austl. Tax F., 29, 137.

1 out of 11

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.