Principles of Taxation Law Assignment - University of XYZ

VerifiedAdded on 2020/02/19

|13

|2601

|730

Homework Assignment

AI Summary

This document presents a comprehensive solution to a taxation law assignment, addressing various aspects of Australian taxation. The solution explores diverse scenarios including fringe benefits, compensation for damages, gifts, additional funds, and gains for sports individuals. It provides detailed explanations of tax implications for construction employees, artists, and travel expenses. The assignment also analyzes a case study involving an overseas student, Manpreet, and his tax liabilities. It covers topics like self-education expenses, deductible expenses, and the application of relevant tax laws and rulings, offering a thorough understanding of taxation principles and their practical application.

Running head: PRINCIPLES OF TAXATION LAW

Principles of Taxation law

University Name

Student Name

Authors’ Note

Principles of Taxation law

University Name

Student Name

Authors’ Note

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

2PRINCIPLES OF TAXATION LAW

Table of Contents

Solution to Question 1:...............................................................................................................2

Solution to Question (i):............................................................................................................2

Solution to Question 1(ii):..........................................................................................................3

Solution to Question 1(iii):.........................................................................................................3

Solution to Question 1(iv):.........................................................................................................4

Solution to Question 1(v):..........................................................................................................4

Solution to Question 1(vi):.........................................................................................................6

Solution to Question Vii.............................................................................................................6

Solution to Question viii............................................................................................................7

Solution to Question ix...............................................................................................................8

Solution to Question x................................................................................................................8

Solution to Question 2................................................................................................................8

References................................................................................................................................11

Table of Contents

Solution to Question 1:...............................................................................................................2

Solution to Question (i):............................................................................................................2

Solution to Question 1(ii):..........................................................................................................3

Solution to Question 1(iii):.........................................................................................................3

Solution to Question 1(iv):.........................................................................................................4

Solution to Question 1(v):..........................................................................................................4

Solution to Question 1(vi):.........................................................................................................6

Solution to Question Vii.............................................................................................................6

Solution to Question viii............................................................................................................7

Solution to Question ix...............................................................................................................8

Solution to Question x................................................................................................................8

Solution to Question 2................................................................................................................8

References................................................................................................................................11

3PRINCIPLES OF TAXATION LAW

Solution to Question 1:

Solution to Question (i):

The trustworthy client of airline is rewarded with Flight Point and Reward by aviation

corporations that is necessarily covered under the directives stipulated under the Taxation

Ruling of TR 1999/6. In essence, taxation ruling as mentioned under TR 1999/6 states that

points or incentives that are received by diverse clients from corporations operating in the

airline industry are generally not considered under taxation as type of income (Braithwaite,

2017). Nevertheless, fringe benefits might possibly be executed on specific points and

incentives in case if the following situations occur:-

- There is a specific association between the employer and the workers. Again, the

points or incentive from the flight are in actual fact accepted by employees taking into

consideration employment provision.

- The flight points otherwise rewards are offered to the worker for a certain specific

deal (McGuire et al., 2014).

The firm Web jet’s recurrent flier compensation received by the employee for work

associated travel shall be taxed neither as the Fringe Benefits nor as taxable earning.

Solution to Question 1(ii):

The individual from among the customer gets a payment for damage caused to the capital

asset during the period of delivering service to the customer. Then in that case, the amount

received as compensation for different damages caused cannot be evaluated under taxation.

However, this is taxable under the recipient (McGuire et al., 2014). The significant points that

can be taken into account include the following:

Solution to Question 1:

Solution to Question (i):

The trustworthy client of airline is rewarded with Flight Point and Reward by aviation

corporations that is necessarily covered under the directives stipulated under the Taxation

Ruling of TR 1999/6. In essence, taxation ruling as mentioned under TR 1999/6 states that

points or incentives that are received by diverse clients from corporations operating in the

airline industry are generally not considered under taxation as type of income (Braithwaite,

2017). Nevertheless, fringe benefits might possibly be executed on specific points and

incentives in case if the following situations occur:-

- There is a specific association between the employer and the workers. Again, the

points or incentive from the flight are in actual fact accepted by employees taking into

consideration employment provision.

- The flight points otherwise rewards are offered to the worker for a certain specific

deal (McGuire et al., 2014).

The firm Web jet’s recurrent flier compensation received by the employee for work

associated travel shall be taxed neither as the Fringe Benefits nor as taxable earning.

Solution to Question 1(ii):

The individual from among the customer gets a payment for damage caused to the capital

asset during the period of delivering service to the customer. Then in that case, the amount

received as compensation for different damages caused cannot be evaluated under taxation.

However, this is taxable under the recipient (McGuire et al., 2014). The significant points that

can be taken into account include the following:

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

4PRINCIPLES OF TAXATION LAW

- The assets/resources can be treated as a capital need to be vigorously used in the

business process of the recipient.

- The resources also need to be an asset that is essentially depreciable and anticipated

depreciation can be examined for the resources presented in the records (Dowling,

2014).

- The compensation amount accepted can be used for refurbishing parts of the resources

that are damaged

A certain amount of money is accepted for the caused damage by the Crane Hire

Company from the clientele. In essence, this is not to be regarded under cases of taxation

that is essentially not a taxable earning of the corporation provided that the above

mentioned conditions are satisfied (Austin & Wilson, 2015).

Solution to Question 1(iii):

According to the Australian Taxation Office, gifts received in kind else wise in cash can be

accepted by a particular individual but cannot be treated as an element of earning. This

particular element of earning accepted is neither a part of non-exempted earning nor non-

assessable earning. Essentially, small gift can be considered to be a certain category of a gift

that is eliminated during the period of enumeration of income tax of the individual (Austin &

Wilson, 2015). Nevertheless, in case of receipt of huge quantity of gifts that can transform

into money, then that particular sum can be taken into account in the process of analysis by

the recipient.

In this case, the supplier of alcohol has delivered the package of overseas holiday for free and

that is received by the executive of the night club. However, this can be taken into account in

the process of enumeration of income tax of the executive of the night club.

- The assets/resources can be treated as a capital need to be vigorously used in the

business process of the recipient.

- The resources also need to be an asset that is essentially depreciable and anticipated

depreciation can be examined for the resources presented in the records (Dowling,

2014).

- The compensation amount accepted can be used for refurbishing parts of the resources

that are damaged

A certain amount of money is accepted for the caused damage by the Crane Hire

Company from the clientele. In essence, this is not to be regarded under cases of taxation

that is essentially not a taxable earning of the corporation provided that the above

mentioned conditions are satisfied (Austin & Wilson, 2015).

Solution to Question 1(iii):

According to the Australian Taxation Office, gifts received in kind else wise in cash can be

accepted by a particular individual but cannot be treated as an element of earning. This

particular element of earning accepted is neither a part of non-exempted earning nor non-

assessable earning. Essentially, small gift can be considered to be a certain category of a gift

that is eliminated during the period of enumeration of income tax of the individual (Austin &

Wilson, 2015). Nevertheless, in case of receipt of huge quantity of gifts that can transform

into money, then that particular sum can be taken into account in the process of analysis by

the recipient.

In this case, the supplier of alcohol has delivered the package of overseas holiday for free and

that is received by the executive of the night club. However, this can be taken into account in

the process of enumeration of income tax of the executive of the night club.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

5PRINCIPLES OF TAXATION LAW

Solution to Question 1(iv):

The amount of money acquired by the Canoe Club for purchasing supplementary canoes was

discovered to be an additional fund raised. However, this was necessarily returned to all the

members of the Canoe Club. However, the additional fund that was acquired cannot be taken

into account at the time of enumeration of the income tax. As such, this cannot be considered

whilst recording of earnings. This is because this finance cannot be necessarily reflected as

the earning in the alternative additional fund that is delivered by different members (Guenther

et al., 2016).

Solution to Question 1(v):

Gains that are accepted by different sports individuals can be covered Taxation Stipulations

TR 1999/171. However, according to the directives mentioned under this rule, any kind of

gains or else sums accepted by sports individuals can be considered as an earning that is

subject to taxation. Again, receipts cumulatively also becomes a part of total earnings

(Guenther et al., 2016). However, in the present situation, the total amount accepted by the

Australian football player from the television selling company can be considered as an

income that is taxable according to the general notion.

1

Solution to Question 1(iv):

The amount of money acquired by the Canoe Club for purchasing supplementary canoes was

discovered to be an additional fund raised. However, this was necessarily returned to all the

members of the Canoe Club. However, the additional fund that was acquired cannot be taken

into account at the time of enumeration of the income tax. As such, this cannot be considered

whilst recording of earnings. This is because this finance cannot be necessarily reflected as

the earning in the alternative additional fund that is delivered by different members (Guenther

et al., 2016).

Solution to Question 1(v):

Gains that are accepted by different sports individuals can be covered Taxation Stipulations

TR 1999/171. However, according to the directives mentioned under this rule, any kind of

gains or else sums accepted by sports individuals can be considered as an earning that is

subject to taxation. Again, receipts cumulatively also becomes a part of total earnings

(Guenther et al., 2016). However, in the present situation, the total amount accepted by the

Australian football player from the television selling company can be considered as an

income that is taxable according to the general notion.

1

6PRINCIPLES OF TAXATION LAW

Solution to Question 1(vi):

Fundamentally, reimbursement as well as allowance for construction employees can be

mentioned under the Taxation directives as mentioned under TR 95/22 (Badertscher et al.,

2013). According to the Taxation ruling mentioned under TR 95/22, employees working for

the construction along with building business are necessarily composed of the below

mentioned factors:

- Labours who are employed for building development

- Project Manager is engaged for the purpose of construction and development of

building in addition to many other things

- Apprentice, carpenter as well as trainee (Armstrong et al., 2016).

- place such as construction sites where different supervisors operate

The expenditure is incurred with respect to aptitude for building of the workers is clearly

illustrated as the compensation of the construction as well as building labourers along

with different allowance (Bauer, 2016).

Solution to Question Vii

During the period of enumeration of income tax, consequential expenditure incurred for short

time period considered from the context of an artiste can be sanctioned with deductions such

as:-

-Education of modules as well as software

-Course fee for the particular term that is necessarily of short term period for the arts

subject

-Recommended meals for a specific expense amount

Solution to Question 1(vi):

Fundamentally, reimbursement as well as allowance for construction employees can be

mentioned under the Taxation directives as mentioned under TR 95/22 (Badertscher et al.,

2013). According to the Taxation ruling mentioned under TR 95/22, employees working for

the construction along with building business are necessarily composed of the below

mentioned factors:

- Labours who are employed for building development

- Project Manager is engaged for the purpose of construction and development of

building in addition to many other things

- Apprentice, carpenter as well as trainee (Armstrong et al., 2016).

- place such as construction sites where different supervisors operate

The expenditure is incurred with respect to aptitude for building of the workers is clearly

illustrated as the compensation of the construction as well as building labourers along

with different allowance (Bauer, 2016).

Solution to Question Vii

During the period of enumeration of income tax, consequential expenditure incurred for short

time period considered from the context of an artiste can be sanctioned with deductions such

as:-

-Education of modules as well as software

-Course fee for the particular term that is necessarily of short term period for the arts

subject

-Recommended meals for a specific expense amount

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

7PRINCIPLES OF TAXATION LAW

-Cost of travelling that is drawn in for the specific course (Braithwaite, 2017).

However, the expenses specified above can be considered for deductions. However, this can

be allowed in case if the expends are associated to the course of art administration and that

too necessarily for a short period of time. Again, expends that occur but does not associate

proportionately to the art management cannot be permitted for deduction for taxation

(McGuire et al., 2014). Therefore, expends in the present state of affairs can be set for the

deductions taking into consideration art management course that is a short term period course

and expends carried out remains within the above specified range (Dowling, 2014).

Solution to Question viii

According to the laws of taxation, expenditure for dresses offered by the employer is not

considered under the system of taxation. According to the Taxation Office of Australia art

execution by artists can be considered as permissible deduction under the laws of the taxation

(Austin & Wilson, 2015). As per the directives of taxation and grant permissible by

particularly Taxation Office of Australia, performing artists are the ones as mentioned

below:-

-Performing artist refers to musicians

-Performing artist refers to an actor

-Performing artist refers to a singer

-Performing artist refers to many other categories of artists

-Performing artists also refers to performers at circus as well as dancers (Bauer, 2016).

-Cost of travelling that is drawn in for the specific course (Braithwaite, 2017).

However, the expenses specified above can be considered for deductions. However, this can

be allowed in case if the expends are associated to the course of art administration and that

too necessarily for a short period of time. Again, expends that occur but does not associate

proportionately to the art management cannot be permitted for deduction for taxation

(McGuire et al., 2014). Therefore, expends in the present state of affairs can be set for the

deductions taking into consideration art management course that is a short term period course

and expends carried out remains within the above specified range (Dowling, 2014).

Solution to Question viii

According to the laws of taxation, expenditure for dresses offered by the employer is not

considered under the system of taxation. According to the Taxation Office of Australia art

execution by artists can be considered as permissible deduction under the laws of the taxation

(Austin & Wilson, 2015). As per the directives of taxation and grant permissible by

particularly Taxation Office of Australia, performing artists are the ones as mentioned

below:-

-Performing artist refers to musicians

-Performing artist refers to an actor

-Performing artist refers to a singer

-Performing artist refers to many other categories of artists

-Performing artists also refers to performers at circus as well as dancers (Bauer, 2016).

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

8PRINCIPLES OF TAXATION LAW

However, in the present circumstances, expends can be related to dresses and make up of

different performing artists. Then that particular expends can be permitted as a deduction in

shaping the earnings that are taxable for performing artist (Armstrong et al., 2016).

Solution to Question ix

In general, travelling between home and place of work can be considered as travel for private

causes. Nevertheless, there are particular provisions for deductions and the ones that are

permissible assert for travelling expends. Again, in case if travelling is carried out only for

official purpose and in case of partly for private and partly for official reasons, then

expenditure components can be considered as travel only for official purpose. In this case,

deductions that are permissible can be properly mentioned. However, in the present

condition, it might better be comprehended that the travelling was carried out only for work

purpose (Badertscher et al., 2013). Again, the expenditure that was incurred can be

mentioned for deductions of tax determination.

Solution to Question x

In essence expends related to travelling between yet another employer and the particular

employer. Nonetheless, in the current state of affairs, costs borne for the purpose of travelling

between the two different employers can be taken into account else wise considered as

permissible deduction (McGuire et al., 2014). However, this is mainly because claims for

deductions cannot be claimed for travelling between diverse employers.

Solution to Question 2

In a bid to verify the liability of tax of a specific individual, it is essential to settle on whether

the specific individual is a resident or else a foreign resident for taxation purpose. Essentially,

the provision of the law mentions that a particular overseas student who has enrolled in

However, in the present circumstances, expends can be related to dresses and make up of

different performing artists. Then that particular expends can be permitted as a deduction in

shaping the earnings that are taxable for performing artist (Armstrong et al., 2016).

Solution to Question ix

In general, travelling between home and place of work can be considered as travel for private

causes. Nevertheless, there are particular provisions for deductions and the ones that are

permissible assert for travelling expends. Again, in case if travelling is carried out only for

official purpose and in case of partly for private and partly for official reasons, then

expenditure components can be considered as travel only for official purpose. In this case,

deductions that are permissible can be properly mentioned. However, in the present

condition, it might better be comprehended that the travelling was carried out only for work

purpose (Badertscher et al., 2013). Again, the expenditure that was incurred can be

mentioned for deductions of tax determination.

Solution to Question x

In essence expends related to travelling between yet another employer and the particular

employer. Nonetheless, in the current state of affairs, costs borne for the purpose of travelling

between the two different employers can be taken into account else wise considered as

permissible deduction (McGuire et al., 2014). However, this is mainly because claims for

deductions cannot be claimed for travelling between diverse employers.

Solution to Question 2

In a bid to verify the liability of tax of a specific individual, it is essential to settle on whether

the specific individual is a resident or else a foreign resident for taxation purpose. Essentially,

the provision of the law mentions that a particular overseas student who has enrolled in

9PRINCIPLES OF TAXATION LAW

Australia for a period of over and above six months can be regarded as a resident for taxation

purpose. Particularly, in the present scenario, it can be observed that Manpreet can be

considered as an Australian resident for taxation purpose since the student is registered for a

particular course in excess of six months in any Australian University. Additionally, this

individual also operates in a specific office on a part time basis and receives a compensation

of around $45000. This individual also had to acquire expenses for educational purpose and

this is necessarily not permissible as deduction. Again, expends for self-education that is

around $18000 cannot be permitted as deduction. Particularly, the law mentions that a

particular individual can claim expends associated to self-education only in case if the study

is associated to work otherwise if the individual has accepted scholarship of bond that is

taxable as per law (Gallemore & Labro, 2015). Essentially, the course adopted for the

purpose of self education need to have favourable interest with the present employment. In

this case, it can be mentioned that the course need to satisfy the following conditions:-

- Enhance the requisite skills that is required by a specific individual in the present

place of work

- The course can assist in the process of augmenting the overall earnings from the

present employment (Dowling, 2014).

Thus, it can be hereby mentioned that a particular individual need not claim for different

expends associated to self-education that does not have any association with present state of

employment.

As per the section 8-1 mentioned particularly under Income Tax Assessment presents that an

expenditure is permitted as deduction in case if there is ample association between expends

and income generating actions. Again, expends that are private or domestic in nature is not

permitted as deduction. Furthermore, a case presented on Ronpibon Tin NL v. FC of

Australia for a period of over and above six months can be regarded as a resident for taxation

purpose. Particularly, in the present scenario, it can be observed that Manpreet can be

considered as an Australian resident for taxation purpose since the student is registered for a

particular course in excess of six months in any Australian University. Additionally, this

individual also operates in a specific office on a part time basis and receives a compensation

of around $45000. This individual also had to acquire expenses for educational purpose and

this is necessarily not permissible as deduction. Again, expends for self-education that is

around $18000 cannot be permitted as deduction. Particularly, the law mentions that a

particular individual can claim expends associated to self-education only in case if the study

is associated to work otherwise if the individual has accepted scholarship of bond that is

taxable as per law (Gallemore & Labro, 2015). Essentially, the course adopted for the

purpose of self education need to have favourable interest with the present employment. In

this case, it can be mentioned that the course need to satisfy the following conditions:-

- Enhance the requisite skills that is required by a specific individual in the present

place of work

- The course can assist in the process of augmenting the overall earnings from the

present employment (Dowling, 2014).

Thus, it can be hereby mentioned that a particular individual need not claim for different

expends associated to self-education that does not have any association with present state of

employment.

As per the section 8-1 mentioned particularly under Income Tax Assessment presents that an

expenditure is permitted as deduction in case if there is ample association between expends

and income generating actions. Again, expends that are private or domestic in nature is not

permitted as deduction. Furthermore, a case presented on Ronpibon Tin NL v. FC of

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

10PRINCIPLES OF TAXATION LAW

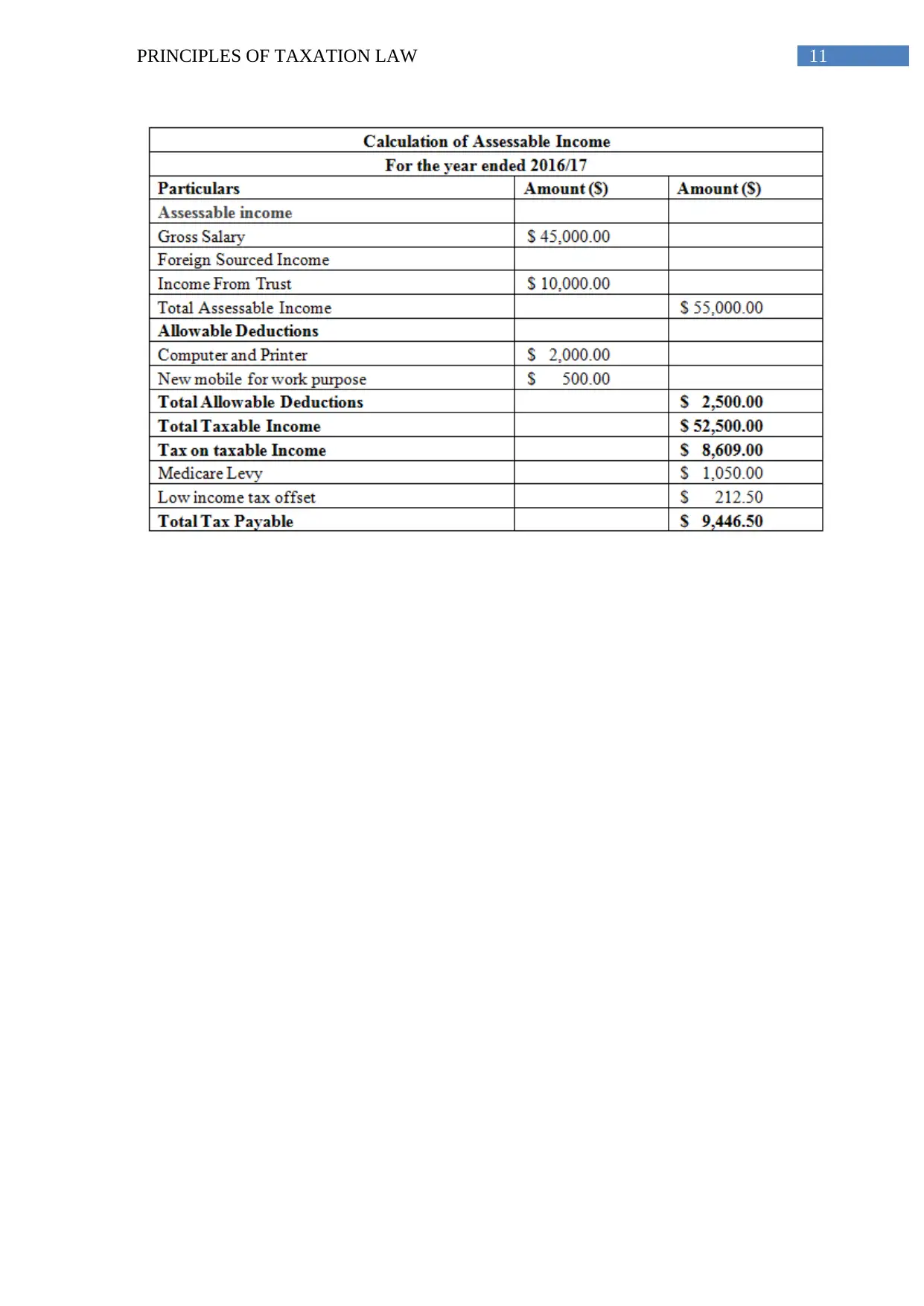

T (1949) backs the specific standpoint. This necessarily mentions that a particular outgoing

can only be permitted as deduction of tax in case if the outgoing results in producing taxable

earning (Braithwaite, 2017). However, there expends that are incurred for the purpose of self-

education and cannot be permitted as a deduction.

In essence, there are also expends that are sustained by Manpreet on particularly computers

as well as printers. Again, there are expends that are incurred for mobile phones that are in

turn utilized for work associated purposes. Expends are normally deductible in case if there is

adequate nexus between expends and income earning capability (McGuire et al., 2014).

Again, obligatory character of expend is that it need not be associated to work but for

domestic purposes. Again, the expenditure also can be incidental or else pertinent for

generation of earnings. In addition to this, case of FC of T v. M I Roberts 92 ATC 4787

asserts that the court has permitted nine managers to subtract expends associated to MBA

according to the standard mentioned in (Maddlena Braithwaite, 2017). Thus, it can be said

that he can aver permissible deduction for principally the mobile phone. The enumeration is

hereby mentioned below:

T (1949) backs the specific standpoint. This necessarily mentions that a particular outgoing

can only be permitted as deduction of tax in case if the outgoing results in producing taxable

earning (Braithwaite, 2017). However, there expends that are incurred for the purpose of self-

education and cannot be permitted as a deduction.

In essence, there are also expends that are sustained by Manpreet on particularly computers

as well as printers. Again, there are expends that are incurred for mobile phones that are in

turn utilized for work associated purposes. Expends are normally deductible in case if there is

adequate nexus between expends and income earning capability (McGuire et al., 2014).

Again, obligatory character of expend is that it need not be associated to work but for

domestic purposes. Again, the expenditure also can be incidental or else pertinent for

generation of earnings. In addition to this, case of FC of T v. M I Roberts 92 ATC 4787

asserts that the court has permitted nine managers to subtract expends associated to MBA

according to the standard mentioned in (Maddlena Braithwaite, 2017). Thus, it can be said

that he can aver permissible deduction for principally the mobile phone. The enumeration is

hereby mentioned below:

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

11PRINCIPLES OF TAXATION LAW

12PRINCIPLES OF TAXATION LAW

References

Armstrong, C., Glaeser, S., & Kepler, J. D. (2016). Strategic reactions in corporate tax

avoidance.

Austin, C. R., & Wilson, R. J. (2015). Are Reputational Costs a Determinant of Tax

Avoidance?.

Badertscher, B. A., Katz, S. P., & Rego, S. O. (2013). The separation of ownership and

control and corporate tax avoidance. Journal of Accounting and Economics, 56(2), 228-250.

Bauer, A. M. (2016). Tax avoidance and the implications of weak internal

controls. Contemporary Accounting Research, 33(2), 449-486.

Braithwaite, V. (Ed.). (2017). Taxing democracy: Understanding tax avoidance and evasion.

Routledge.

Dowling, G. R. (2014). The curious case of corporate tax avoidance: Is it socially

irresponsible?. Journal of Business Ethics, 124(1), 173-184.

Gallemore, J., & Labro, E. (2015). The importance of the internal information environment

for tax avoidance. Journal of Accounting and Economics, 60(1), 149-167.

Guenther, D. A., Matsunaga, S. R., & Williams, B. M. (2016). Is tax avoidance related to

firm risk?. The Accounting Review, 92(1), 115-136.

McGuire, S. T., Wang, D., & Wilson, R. J. (2014). Dual class ownership and tax

avoidance. The Accounting Review, 89(4), 1487-1516.

References

Armstrong, C., Glaeser, S., & Kepler, J. D. (2016). Strategic reactions in corporate tax

avoidance.

Austin, C. R., & Wilson, R. J. (2015). Are Reputational Costs a Determinant of Tax

Avoidance?.

Badertscher, B. A., Katz, S. P., & Rego, S. O. (2013). The separation of ownership and

control and corporate tax avoidance. Journal of Accounting and Economics, 56(2), 228-250.

Bauer, A. M. (2016). Tax avoidance and the implications of weak internal

controls. Contemporary Accounting Research, 33(2), 449-486.

Braithwaite, V. (Ed.). (2017). Taxing democracy: Understanding tax avoidance and evasion.

Routledge.

Dowling, G. R. (2014). The curious case of corporate tax avoidance: Is it socially

irresponsible?. Journal of Business Ethics, 124(1), 173-184.

Gallemore, J., & Labro, E. (2015). The importance of the internal information environment

for tax avoidance. Journal of Accounting and Economics, 60(1), 149-167.

Guenther, D. A., Matsunaga, S. R., & Williams, B. M. (2016). Is tax avoidance related to

firm risk?. The Accounting Review, 92(1), 115-136.

McGuire, S. T., Wang, D., & Wilson, R. J. (2014). Dual class ownership and tax

avoidance. The Accounting Review, 89(4), 1487-1516.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 13

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.