Tech (UK) Limited: Management Accounting, Budgeting & Analysis

VerifiedAdded on 2024/04/26

|16

|4120

|141

Report

AI Summary

This management accounting report for Tech (UK) Limited covers various aspects including the importance of management accounting in decision making, cost accounting systems, inventory management, and job costing. It differentiates between management and financial accounting, highlighting the role of managerial accounting reports and their understandable presentation. Marginal and absorption costing techniques are applied, presenting income statements and comparative analysis. The report also explores different types of budgets, their advantages, disadvantages, and the preparation process, emphasizing the strategic importance of budgeting. Furthermore, it discusses planning tools for tackling financial problems and introduces the balanced scorecard technique, comparing it with management accounting benchmarking. Desklib provides this and many other solved assignments for students.

Management accounting report for Tech

(UK) Limited

1

(UK) Limited

1

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of Contents

Introduction....................................................................................................................................3

Task 1..............................................................................................................................................4

Introduction................................................................................................................................4

a) (I–V) (M1, D1)........................................................................................................................4

b) (I-II)........................................................................................................................................5

Conclusion..................................................................................................................................6

Task 2..............................................................................................................................................7

a) (I –II) (M2, D2)......................................................................................................................7

Task 3..............................................................................................................................................9

a. (b, c) (M3, D3)........................................................................................................................9

Introduction................................................................................................................................9

Conclusion................................................................................................................................11

Task 4............................................................................................................................................12

a. (M4, D3)................................................................................................................................12

Conclusion....................................................................................................................................13

References.....................................................................................................................................14

2

Introduction....................................................................................................................................3

Task 1..............................................................................................................................................4

Introduction................................................................................................................................4

a) (I–V) (M1, D1)........................................................................................................................4

b) (I-II)........................................................................................................................................5

Conclusion..................................................................................................................................6

Task 2..............................................................................................................................................7

a) (I –II) (M2, D2)......................................................................................................................7

Task 3..............................................................................................................................................9

a. (b, c) (M3, D3)........................................................................................................................9

Introduction................................................................................................................................9

Conclusion................................................................................................................................11

Task 4............................................................................................................................................12

a. (M4, D3)................................................................................................................................12

Conclusion....................................................................................................................................13

References.....................................................................................................................................14

2

Introduction

The assignment consists of the report consisting of the management accounting importance along

with the cost accounting system, Inventory management system, job costing system. There is a

short description of the differentiation between the management and financial accounting along

with the managerial accounting report and presentation of the same in an understandable way.

Marginal and absorption costing are also being included in the assignment along with the income

statement and analysis. The various types of the budget along with their advantages and

disadvantages and the process for preparation is stated. The importance of budget in the

company as planning and the strategic tool is also included in the assignment. Various planning

tools and the use of them in tackling the financial problems are stated. There is also the inclusion

of the balanced scorecard technique and the comparison of the same with the management

accounting tool benchmarking.

3

The assignment consists of the report consisting of the management accounting importance along

with the cost accounting system, Inventory management system, job costing system. There is a

short description of the differentiation between the management and financial accounting along

with the managerial accounting report and presentation of the same in an understandable way.

Marginal and absorption costing are also being included in the assignment along with the income

statement and analysis. The various types of the budget along with their advantages and

disadvantages and the process for preparation is stated. The importance of budget in the

company as planning and the strategic tool is also included in the assignment. Various planning

tools and the use of them in tackling the financial problems are stated. There is also the inclusion

of the balanced scorecard technique and the comparison of the same with the management

accounting tool benchmarking.

3

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Task 1

Introduction

The report consists of the brief about the management accounting system and it's important in the

decision making of the company along with detail about the cost accounting system, Inventory

management system and Job Costing. There is also the inclusion of the types of managerial

accounting reports and importance of its presentation in an understandable way.

a) (I–V) (M1, D1)

Management accounting can be defined as the interpretation and recorded of the data in a way

that it helps the managers in the decision making of the company. Management accounting

consists of both the financial accounting and cost accounting depending upon which the

managers analyse the data available. Management accounting systems are the system established

by the company for the internal process and analyse the statements and data (Surum, 2018). The

Tech (UK) Limited can be benefitted with the help of the management accounting and systems

by reducing the cost and expenses through analysis of the quality of the resources. It can also

facilitate the decision making of the company by forecasting and analysis of various factors.

The difference between the financial Accounting is to provide the information and interpretation

of the transaction recorded for the external stakeholders of the company whereas the

management accounting is for the internal members of the company for an effective and efficient

use of the resources and working (Francis, 2018). The financial accounting of the company must

be prepared and presented depending upon the guidelines issued by governance bodies whereas

the Management accounting is a mere estimation or guess made for the decision making of the

company. The management accounting will help Tech (UK) Limited in better controlling and

coordination through plans.

The Management accounting follows various techniques and analysis on the basis of forecast and

historical data available to the management. It acts as a decision-making tool as depending on the

results and data available they make the plans and policies of the company (Freedman, 2018).

4

Introduction

The report consists of the brief about the management accounting system and it's important in the

decision making of the company along with detail about the cost accounting system, Inventory

management system and Job Costing. There is also the inclusion of the types of managerial

accounting reports and importance of its presentation in an understandable way.

a) (I–V) (M1, D1)

Management accounting can be defined as the interpretation and recorded of the data in a way

that it helps the managers in the decision making of the company. Management accounting

consists of both the financial accounting and cost accounting depending upon which the

managers analyse the data available. Management accounting systems are the system established

by the company for the internal process and analyse the statements and data (Surum, 2018). The

Tech (UK) Limited can be benefitted with the help of the management accounting and systems

by reducing the cost and expenses through analysis of the quality of the resources. It can also

facilitate the decision making of the company by forecasting and analysis of various factors.

The difference between the financial Accounting is to provide the information and interpretation

of the transaction recorded for the external stakeholders of the company whereas the

management accounting is for the internal members of the company for an effective and efficient

use of the resources and working (Francis, 2018). The financial accounting of the company must

be prepared and presented depending upon the guidelines issued by governance bodies whereas

the Management accounting is a mere estimation or guess made for the decision making of the

company. The management accounting will help Tech (UK) Limited in better controlling and

coordination through plans.

The Management accounting follows various techniques and analysis on the basis of forecast and

historical data available to the management. It acts as a decision-making tool as depending on the

results and data available they make the plans and policies of the company (Freedman, 2018).

4

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

The management accounting can help in deciding the Tech (UK) Limited about the decision

regarding the selling and production of the product in a way that can be best profitable to them.

There are various cost accounting systems for the analysis by the management. The cost

accounting system is used by the manager for the analysis of the cost and profitability of the

company. There are three types of costing Normal, Standard and Actual. In case of the Normal

costing, the cost is calculated on the basis of actual cost incurred which is based on the overhead

rate anticipated by the managers (Accounting Coach, 2018). In case of the standard costing, it is

based on the anticipated cost of the labour, material, and manufacturing. The actual cost values

the product on the basis of actual cost incurred on the product.

Inventory management system is the effective and efficient use of the available stock along with

a better allocation of the stock. It is important to maintain the cost of the stock as the money is

blocked in the inventory of the company. A high amount of stock in the warehouse can lead to

increase in the variable cost of the company. It will help Tech (UK) Limited in determining the

optimum stock level that can be best suitable in terms of profitability and the cost of the

company.

Job Costing system can help in assigning the cost that is incurred by the company to the

particular job or process that is carried on. It is important for any company irrespective of its

nature and size. Tech (UK) Limited can be benefitted as there are a lot of processes involved in

producing the special charger for mobile telephone etc. It will be helpful for them to analyse the

cost and apportion them to particular jobs and in reducing the cost of continuously (Ingram,

2017).

b) (I-II)

The different types of management accounting reports are as follows:-

i) Budget Report – There are various budgets that are prepared based on the forecasting and

different factors as well as on the basis of assumption for the decision making.

5

regarding the selling and production of the product in a way that can be best profitable to them.

There are various cost accounting systems for the analysis by the management. The cost

accounting system is used by the manager for the analysis of the cost and profitability of the

company. There are three types of costing Normal, Standard and Actual. In case of the Normal

costing, the cost is calculated on the basis of actual cost incurred which is based on the overhead

rate anticipated by the managers (Accounting Coach, 2018). In case of the standard costing, it is

based on the anticipated cost of the labour, material, and manufacturing. The actual cost values

the product on the basis of actual cost incurred on the product.

Inventory management system is the effective and efficient use of the available stock along with

a better allocation of the stock. It is important to maintain the cost of the stock as the money is

blocked in the inventory of the company. A high amount of stock in the warehouse can lead to

increase in the variable cost of the company. It will help Tech (UK) Limited in determining the

optimum stock level that can be best suitable in terms of profitability and the cost of the

company.

Job Costing system can help in assigning the cost that is incurred by the company to the

particular job or process that is carried on. It is important for any company irrespective of its

nature and size. Tech (UK) Limited can be benefitted as there are a lot of processes involved in

producing the special charger for mobile telephone etc. It will be helpful for them to analyse the

cost and apportion them to particular jobs and in reducing the cost of continuously (Ingram,

2017).

b) (I-II)

The different types of management accounting reports are as follows:-

i) Budget Report – There are various budgets that are prepared based on the forecasting and

different factors as well as on the basis of assumption for the decision making.

5

ii) Divisional, Departmental reports – The Divisional report consist of the cost report, revenue

report, investment report on the basis of the department. There is the various method adopted for

the preparation of these reports.

iii) Cost and Sales report – The cost and sale report consist of the price and volume that the

company has prepared along with the variances for the difference in the results

iv) Investment appraisal report – The Investment appraisal report includes various techniques

through which the profitability of the project can be judged and decision can be taken by the

management (Sartori, et. al., 2014).

It is important that the financial information must be relevant and the representation must be

made faithfully. It can be beneficial for the company as they will be easy to understand and

interpret by the managers. The relevance in the preparation of the statement and information will

result in determining the trend and comparison of the firm performance with the rival companies.

The Tech (UK) Limited will be benefited with the help of it as they will be able to formulate the

plans and policies of the company more effectively and efficiently (Vitez, 2018). The usefulness

will be increased with the better representation along with the reliability as they will be able to

understand the report that is being provided.

The management accounting system and reporting are integrated into the organisation process as

the transactions are recorded in the system based on which the reporting is being carried out. The

reporting helps in analysis of the information that is being recorded in the system. It can also be

stated that mere recording of the transaction is not enough it is important to analyse them and

take preventive steps to decrease the expenses and increase the profit of the company which can

be done only with the help of the Reporting.

Conclusion

It can be concluded with the help of the report that the management accounting is essential in the

system. It will help the Tech (UK) Limited in better controlling and decision-making process. It

will also lead to decrease in the cost of the company and better allocation of the process. The

6

report, investment report on the basis of the department. There is the various method adopted for

the preparation of these reports.

iii) Cost and Sales report – The cost and sale report consist of the price and volume that the

company has prepared along with the variances for the difference in the results

iv) Investment appraisal report – The Investment appraisal report includes various techniques

through which the profitability of the project can be judged and decision can be taken by the

management (Sartori, et. al., 2014).

It is important that the financial information must be relevant and the representation must be

made faithfully. It can be beneficial for the company as they will be easy to understand and

interpret by the managers. The relevance in the preparation of the statement and information will

result in determining the trend and comparison of the firm performance with the rival companies.

The Tech (UK) Limited will be benefited with the help of it as they will be able to formulate the

plans and policies of the company more effectively and efficiently (Vitez, 2018). The usefulness

will be increased with the better representation along with the reliability as they will be able to

understand the report that is being provided.

The management accounting system and reporting are integrated into the organisation process as

the transactions are recorded in the system based on which the reporting is being carried out. The

reporting helps in analysis of the information that is being recorded in the system. It can also be

stated that mere recording of the transaction is not enough it is important to analyse them and

take preventive steps to decrease the expenses and increase the profit of the company which can

be done only with the help of the Reporting.

Conclusion

It can be concluded with the help of the report that the management accounting is essential in the

system. It will help the Tech (UK) Limited in better controlling and decision-making process. It

will also lead to decrease in the cost of the company and better allocation of the process. The

6

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

conclusion can also be derived that the presentation of the information must be in a way that is

understandable to all for a better decision making.

7

understandable to all for a better decision making.

7

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Task 2

a) (I –II) (M2, D2)

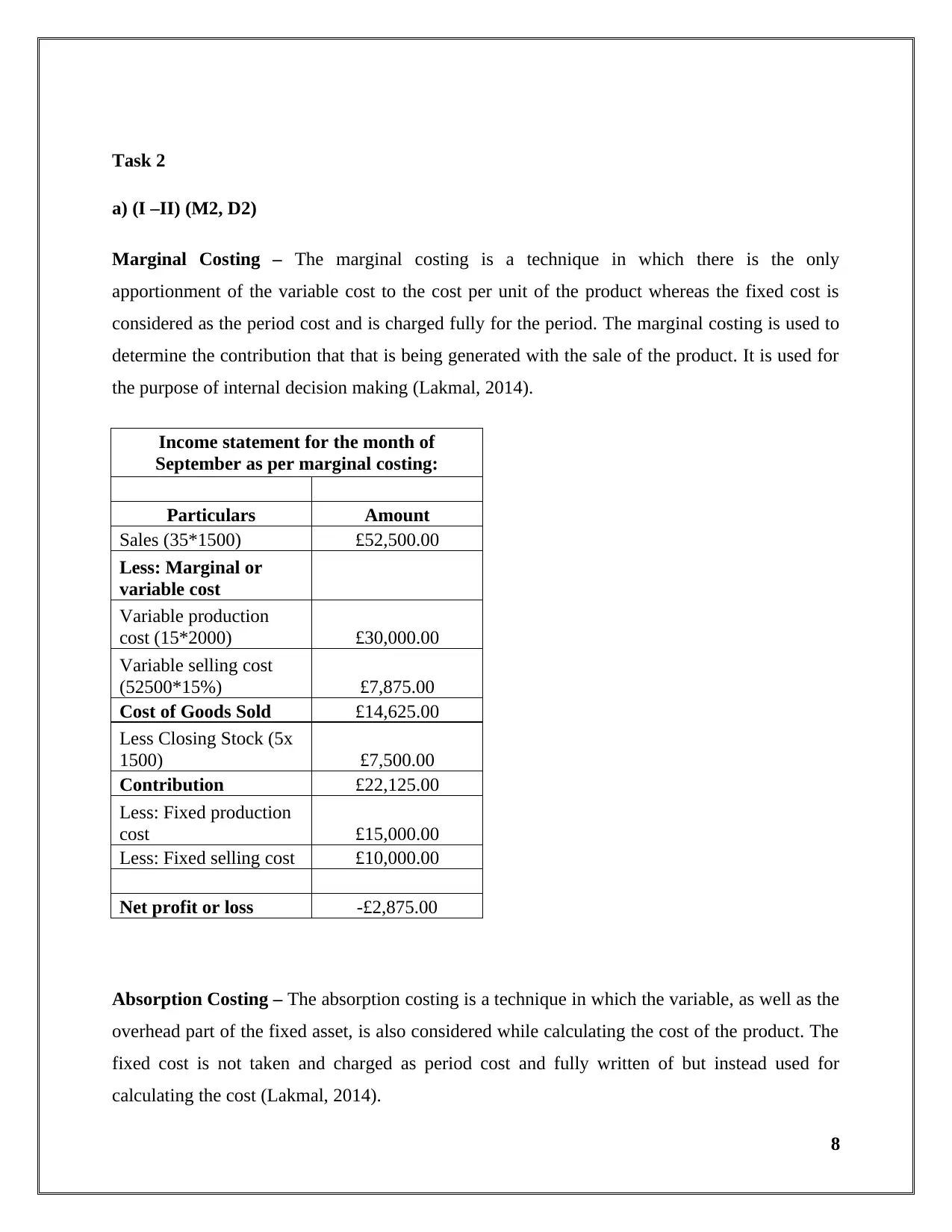

Marginal Costing – The marginal costing is a technique in which there is the only

apportionment of the variable cost to the cost per unit of the product whereas the fixed cost is

considered as the period cost and is charged fully for the period. The marginal costing is used to

determine the contribution that that is being generated with the sale of the product. It is used for

the purpose of internal decision making (Lakmal, 2014).

Income statement for the month of

September as per marginal costing:

Particulars Amount

Sales (35*1500) £52,500.00

Less: Marginal or

variable cost

Variable production

cost (15*2000) £30,000.00

Variable selling cost

(52500*15%) £7,875.00

Cost of Goods Sold £14,625.00

Less Closing Stock (5x

1500) £7,500.00

Contribution £22,125.00

Less: Fixed production

cost £15,000.00

Less: Fixed selling cost £10,000.00

Net profit or loss -£2,875.00

Absorption Costing – The absorption costing is a technique in which the variable, as well as the

overhead part of the fixed asset, is also considered while calculating the cost of the product. The

fixed cost is not taken and charged as period cost and fully written of but instead used for

calculating the cost (Lakmal, 2014).

8

a) (I –II) (M2, D2)

Marginal Costing – The marginal costing is a technique in which there is the only

apportionment of the variable cost to the cost per unit of the product whereas the fixed cost is

considered as the period cost and is charged fully for the period. The marginal costing is used to

determine the contribution that that is being generated with the sale of the product. It is used for

the purpose of internal decision making (Lakmal, 2014).

Income statement for the month of

September as per marginal costing:

Particulars Amount

Sales (35*1500) £52,500.00

Less: Marginal or

variable cost

Variable production

cost (15*2000) £30,000.00

Variable selling cost

(52500*15%) £7,875.00

Cost of Goods Sold £14,625.00

Less Closing Stock (5x

1500) £7,500.00

Contribution £22,125.00

Less: Fixed production

cost £15,000.00

Less: Fixed selling cost £10,000.00

Net profit or loss -£2,875.00

Absorption Costing – The absorption costing is a technique in which the variable, as well as the

overhead part of the fixed asset, is also considered while calculating the cost of the product. The

fixed cost is not taken and charged as period cost and fully written of but instead used for

calculating the cost (Lakmal, 2014).

8

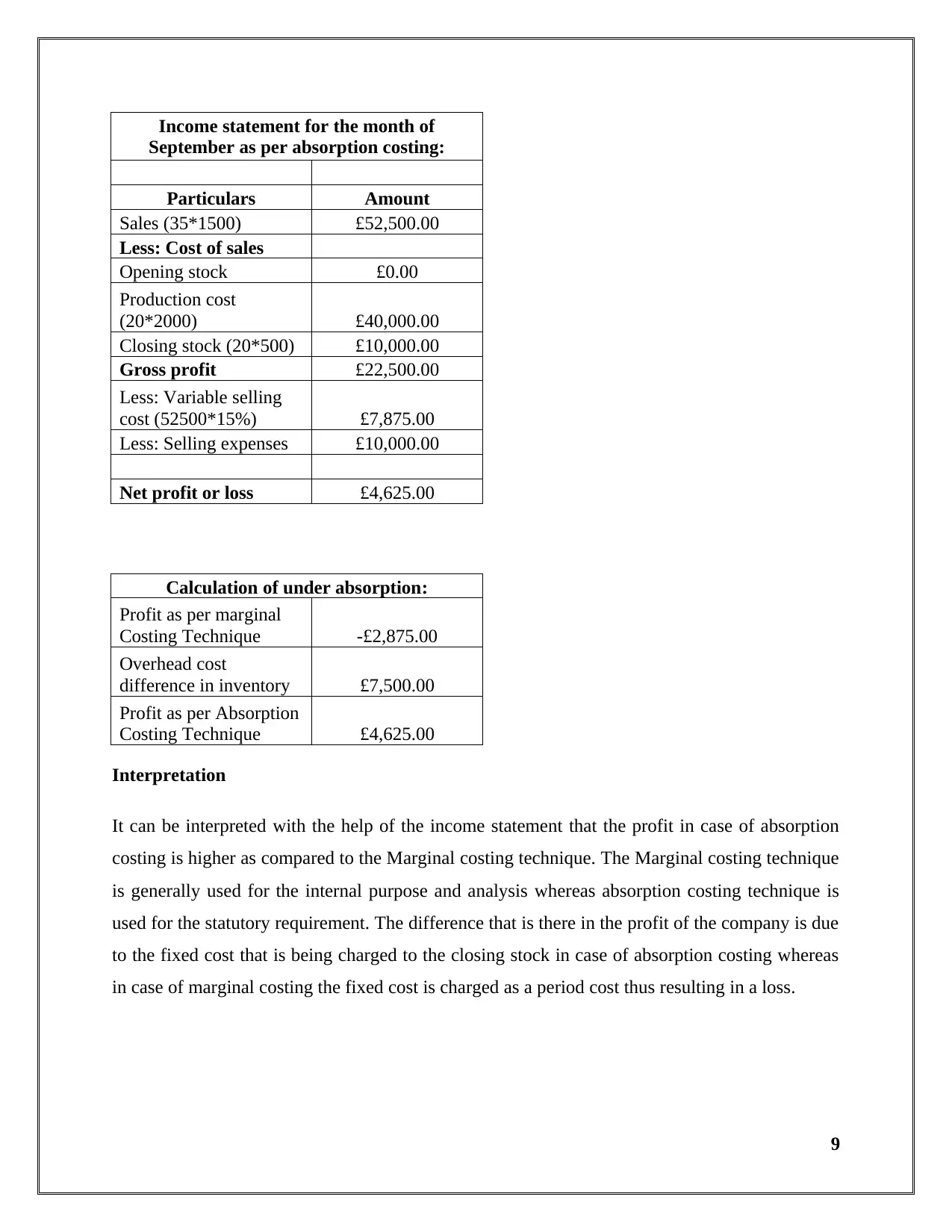

Income statement for the month of

September as per absorption costing:

Particulars Amount

Sales (35*1500) £52,500.00

Less: Cost of sales

Opening stock £0.00

Production cost

(20*2000) £40,000.00

Closing stock (20*500) £10,000.00

Gross profit £22,500.00

Less: Variable selling

cost (52500*15%) £7,875.00

Less: Selling expenses £10,000.00

Net profit or loss £4,625.00

Calculation of under absorption:

Profit as per marginal

Costing Technique -£2,875.00

Overhead cost

difference in inventory £7,500.00

Profit as per Absorption

Costing Technique £4,625.00

Interpretation

It can be interpreted with the help of the income statement that the profit in case of absorption

costing is higher as compared to the Marginal costing technique. The Marginal costing technique

is generally used for the internal purpose and analysis whereas absorption costing technique is

used for the statutory requirement. The difference that is there in the profit of the company is due

to the fixed cost that is being charged to the closing stock in case of absorption costing whereas

in case of marginal costing the fixed cost is charged as a period cost thus resulting in a loss.

9

September as per absorption costing:

Particulars Amount

Sales (35*1500) £52,500.00

Less: Cost of sales

Opening stock £0.00

Production cost

(20*2000) £40,000.00

Closing stock (20*500) £10,000.00

Gross profit £22,500.00

Less: Variable selling

cost (52500*15%) £7,875.00

Less: Selling expenses £10,000.00

Net profit or loss £4,625.00

Calculation of under absorption:

Profit as per marginal

Costing Technique -£2,875.00

Overhead cost

difference in inventory £7,500.00

Profit as per Absorption

Costing Technique £4,625.00

Interpretation

It can be interpreted with the help of the income statement that the profit in case of absorption

costing is higher as compared to the Marginal costing technique. The Marginal costing technique

is generally used for the internal purpose and analysis whereas absorption costing technique is

used for the statutory requirement. The difference that is there in the profit of the company is due

to the fixed cost that is being charged to the closing stock in case of absorption costing whereas

in case of marginal costing the fixed cost is charged as a period cost thus resulting in a loss.

9

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Task 3

a. (b, c) (M3, D3)

Introduction

The report consists of the various types of budgets that can be made within the company along

with the advantages and disadvantages. There is also the inclusion of the importance of budget

and the preparation process for an effective budget. The report also includes the various planning

tools that can be used for forecasting along with their use in overcome the financial problem that

can lead to sustainable success.

Content

The different kind of budget along with their advantages and disadvantages are as follows:-

Master Budget – The master budget is the accumulation of all the small budgets. The master

budget is prepared as a whole and for the organisation. It is an overall budget of the company. It

is useful in determining the problems that are faced by the department or any sector and plan

accordingly. It has a disadvantage also as it is difficult for the managers to analyse the same and

read it along with modifying it (Jane, 2017).

Operational Budgets – The operational budget is used to analyse the amount of cash required at

different sector along with the sustainable growth. It can be used for allocation of the resources

effectively and efficiently depending upon the need and preference of the company but it has

some disadvantage also as it is important to revise the budget as per the needs but if it is not done

it may lead to a shortage of cash due to the wrong allocation of resources (Lister, 2018).

Cash Flow Budget – The cash flow budget helps in determining the cash inflow and outflow

that the company may have in that particular time period. The cash flow budget can help in better

investment decision making along with the optimal utilisation of the cash. The cash flow budget

might show a possibility of cash crunch or negative cash balance due to the excessive payment

on the basis of cash flow budget but in actual, there was a delay in the cash flow resulting in

negative balance.

10

a. (b, c) (M3, D3)

Introduction

The report consists of the various types of budgets that can be made within the company along

with the advantages and disadvantages. There is also the inclusion of the importance of budget

and the preparation process for an effective budget. The report also includes the various planning

tools that can be used for forecasting along with their use in overcome the financial problem that

can lead to sustainable success.

Content

The different kind of budget along with their advantages and disadvantages are as follows:-

Master Budget – The master budget is the accumulation of all the small budgets. The master

budget is prepared as a whole and for the organisation. It is an overall budget of the company. It

is useful in determining the problems that are faced by the department or any sector and plan

accordingly. It has a disadvantage also as it is difficult for the managers to analyse the same and

read it along with modifying it (Jane, 2017).

Operational Budgets – The operational budget is used to analyse the amount of cash required at

different sector along with the sustainable growth. It can be used for allocation of the resources

effectively and efficiently depending upon the need and preference of the company but it has

some disadvantage also as it is important to revise the budget as per the needs but if it is not done

it may lead to a shortage of cash due to the wrong allocation of resources (Lister, 2018).

Cash Flow Budget – The cash flow budget helps in determining the cash inflow and outflow

that the company may have in that particular time period. The cash flow budget can help in better

investment decision making along with the optimal utilisation of the cash. The cash flow budget

might show a possibility of cash crunch or negative cash balance due to the excessive payment

on the basis of cash flow budget but in actual, there was a delay in the cash flow resulting in

negative balance.

10

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

The process that can be used for the preparation of budget is

Step 1 – Estimation – The managers need to analyse and forecast the future market condition

that can affect the business process.

Step 2 – Coordination of the Estimates – Based on the Estimation the best plans are chosen on

the basis of profitability and achievability.

Step 3 – Communication of the budget – The Budget is then passed on to different managers

and departments of the company along with the plans.

Step 4 – Implementation – The next plan of the Budget plan is to implement the same in the

small unit and then in a whole organisation effectively and efficiently.

Step 5 – Progress towards achievement – After the implementation of the budget is too

important to monitor the same. If the budget is not achieved or there is no growth in it then it is

necessary to revise the same or taken preventive measures to achieve them.

The budget helps in the planning process of the company as the managers are already aware of

the spending that they can be done. The budget is prepared after analysing the available data

along with the historic events and results that are being achieved by the organisation. The plans

and strategies are then made keeping in view the budget available (Henttu-Aho, and Järvinen,

2013). It is useful as a planning tool as it helps to identify the variance that is there between the

actual and budgeted results along with the reason for those variances. It acts as a planning tool as

it helps in overcome those variances and increase the efficiency and productivity.

There are various planning tool that can help in the development and forecasting of the

budget:-

PEST – The PEST (Political, social, economic and technological) helps in identification of the

factors along with their analysis which can affect the company profitability. It can help in

forecasting of the budget as with the help of technological, or political factor the investment can

be made on the new technology.

11

Step 1 – Estimation – The managers need to analyse and forecast the future market condition

that can affect the business process.

Step 2 – Coordination of the Estimates – Based on the Estimation the best plans are chosen on

the basis of profitability and achievability.

Step 3 – Communication of the budget – The Budget is then passed on to different managers

and departments of the company along with the plans.

Step 4 – Implementation – The next plan of the Budget plan is to implement the same in the

small unit and then in a whole organisation effectively and efficiently.

Step 5 – Progress towards achievement – After the implementation of the budget is too

important to monitor the same. If the budget is not achieved or there is no growth in it then it is

necessary to revise the same or taken preventive measures to achieve them.

The budget helps in the planning process of the company as the managers are already aware of

the spending that they can be done. The budget is prepared after analysing the available data

along with the historic events and results that are being achieved by the organisation. The plans

and strategies are then made keeping in view the budget available (Henttu-Aho, and Järvinen,

2013). It is useful as a planning tool as it helps to identify the variance that is there between the

actual and budgeted results along with the reason for those variances. It acts as a planning tool as

it helps in overcome those variances and increase the efficiency and productivity.

There are various planning tool that can help in the development and forecasting of the

budget:-

PEST – The PEST (Political, social, economic and technological) helps in identification of the

factors along with their analysis which can affect the company profitability. It can help in

forecasting of the budget as with the help of technological, or political factor the investment can

be made on the new technology.

11

Porter five forces – The porter five forces consist of the macro factors such as the new entrant,

Supplier power, Buyer power, Substitution and the competition in the market. It can be used for

the forecasting of the budget as the production policy or the cost and operational budget can be

made a bit tight in order to get am a competitive edge over the competitors.

Balance scorecard – The balance scorecard can be useful for the preparation of the budget as it

helps in determining the performance of the company based on financial as well as non-financial

indicators of the company (Perkins, et. al., 2014).

SWOT – It consists of an analysis of the Strength, Weakness, opportunity, and threat. It can be

beneficial for the company in preparation for the budget such as the sales budget will be on the

higher side if the opportunities are more than the threat. The budget can also be made keeping in

view the strength of the company (Bull, et. al., 2016)

These planning tools are not only useful for the development of the budget but also in solving the

financial problems of the company. It helps in reducing the cost of the company and minimising

it in the best possible way. They can forecast and save the overhead cost that can be attracted in

case there is no proper analysis of the available data. They are helpful in tackling the financial

cost by proper allocation of the available resources in the best suitable way.

Conclusion

It can be concluded with the help of the report that there is a different budget with the usefulness

in the company. They are useful in the preparation of the plans and policies depending on the

various factors. It can be concluded that planning tools can be beneficial for effective budget

making as they consider various macro factors that can affect company profitability. It also helps

in tackling the financial problem of the company by reducing the cost and better allocation of

resources.

12

Supplier power, Buyer power, Substitution and the competition in the market. It can be used for

the forecasting of the budget as the production policy or the cost and operational budget can be

made a bit tight in order to get am a competitive edge over the competitors.

Balance scorecard – The balance scorecard can be useful for the preparation of the budget as it

helps in determining the performance of the company based on financial as well as non-financial

indicators of the company (Perkins, et. al., 2014).

SWOT – It consists of an analysis of the Strength, Weakness, opportunity, and threat. It can be

beneficial for the company in preparation for the budget such as the sales budget will be on the

higher side if the opportunities are more than the threat. The budget can also be made keeping in

view the strength of the company (Bull, et. al., 2016)

These planning tools are not only useful for the development of the budget but also in solving the

financial problems of the company. It helps in reducing the cost of the company and minimising

it in the best possible way. They can forecast and save the overhead cost that can be attracted in

case there is no proper analysis of the available data. They are helpful in tackling the financial

cost by proper allocation of the available resources in the best suitable way.

Conclusion

It can be concluded with the help of the report that there is a different budget with the usefulness

in the company. They are useful in the preparation of the plans and policies depending on the

various factors. It can be concluded that planning tools can be beneficial for effective budget

making as they consider various macro factors that can affect company profitability. It also helps

in tackling the financial problem of the company by reducing the cost and better allocation of

resources.

12

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 16

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.