Management Accounting Report: Financial Analysis of Tech (UK) Ltd.

VerifiedAdded on 2023/02/03

|17

|6059

|64

Report

AI Summary

This report delves into the core principles of management accounting, examining its crucial role in organizations like Tech (UK) Ltd., a UK-based manufacturer. It explores various management accounting systems, including cost accounting, inventory management, and job costing, highlighting their importance in identifying costs, managing inventory, and assessing product profitability. The report also outlines different types of management accounting reports, such as cost accounting reports, inventory management reports, financial reports, accounts receivable and payable reports, and their significance in providing relevant financial information for decision-making. Furthermore, the report analyzes cost analysis techniques like marginal and absorption costing, and it covers planning tools for budgetary control and financial tools to resolve financial issues. It uses Tech (UK) Ltd. as a case study to illustrate these concepts, making recommendations for improved financial performance. The report concludes with a discussion of the importance of these tools in maintaining a strong financial position in a competitive market.

Management

Accounting

Accounting

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of Contents

INTRODUCTION...........................................................................................................................1

TASK 1............................................................................................................................................1

P1: Management accounting systems and its essential requirements to an organisation.......1

P2: Different types of management accounting reports.........................................................4

M1: Importance of different management system..................................................................5

D1: Various reporting method and accounting system integration........................................6

TASK 2............................................................................................................................................6

P3: Techniques used to analyse cost with marginal and absorption costs.............................6

M2: Various type of Accounting tool and techniques............................................................9

D2 Preparation of financial statements from collected data...................................................9

TASK 3............................................................................................................................................9

P4: Different planning tools used for budgetary control........................................................9

Planning tools for budgeting................................................................................................10

M3 Analysis of various planning tool and its application for forecasting...........................12

TASK 4..........................................................................................................................................12

P5: Financial issues and resolution of these problem and comparison with other company12

M4 Analysis of planning tool to deal with financial issue...................................................14

D3: Evaluation of planning tools for accounting respond appropriately to solving financial

problems...............................................................................................................................14

CONCLUSION..............................................................................................................................14

REFERENCES..............................................................................................................................15

INTRODUCTION...........................................................................................................................1

TASK 1............................................................................................................................................1

P1: Management accounting systems and its essential requirements to an organisation.......1

P2: Different types of management accounting reports.........................................................4

M1: Importance of different management system..................................................................5

D1: Various reporting method and accounting system integration........................................6

TASK 2............................................................................................................................................6

P3: Techniques used to analyse cost with marginal and absorption costs.............................6

M2: Various type of Accounting tool and techniques............................................................9

D2 Preparation of financial statements from collected data...................................................9

TASK 3............................................................................................................................................9

P4: Different planning tools used for budgetary control........................................................9

Planning tools for budgeting................................................................................................10

M3 Analysis of various planning tool and its application for forecasting...........................12

TASK 4..........................................................................................................................................12

P5: Financial issues and resolution of these problem and comparison with other company12

M4 Analysis of planning tool to deal with financial issue...................................................14

D3: Evaluation of planning tools for accounting respond appropriately to solving financial

problems...............................................................................................................................14

CONCLUSION..............................................................................................................................14

REFERENCES..............................................................................................................................15

INTRODUCTION

Management accounting is an essential requirement of an organisation to form who

perform several functions such as identifying, analysing, calculating and recording each

transaction and presenting the financial information to the internal management so as to assist

them in making an effective decision and plans for the betterment of an organisation. In business

organisation whether small, medium or large various kinds of reports are prepared which

contains different informations such as total receivables, availability of cash, total revenues and

cost incurred in execution of business operation. Therefore, management accounting play an

important role in leading business towards success. Tech (UK) Ltd. which deals in

manufacturing Tech (UK) Limited, who is producing special charger for mobile telephone and

other carry-on gadgets for retail outlets in the UK is selected for the purpose of preparing this

report. The project includes different types of management accounting systems and its essential

needs to an organisation. Along with this, various management accounting reporting system are

also discussed under this report in detailed manner. The project also describes the costing

methods along with calculation of net profitability, planning tools to control budget and financial

tools to resolving financial issues that facilitate organisation to maintain their financial position

among their rivals in competitive market (Callahan, Stetz and Brooks,2011).

TASK 1

P1: Management accounting systems and its essential requirements to an organisation

Accounting: It is a systematic recording of financial transactions made by an

organisation on daily basis. It help in measuring the results of an organisation's economic

activities and communicate it to their variety of users such as investor, creditors, management

etc. It mainly consists of two parts such as management accounting and financial accounting

which are explained as under:

Management accounting: It is the process of identifying, measuring, analysing and

communicating relevant and accurate information to managers so as to make easy for them to

make an effective decision to achieve organisational goals. It provides both monetary as well as

non-monetary information which is useful for internal management to make better policies. As it

is formed as per the needs and requirements of company thus not mandatory.

Financial accounting: It is the process of recording, summarizing and reporting the

myriad of transactions made during execution of business operations over a period of time. Such

1

Management accounting is an essential requirement of an organisation to form who

perform several functions such as identifying, analysing, calculating and recording each

transaction and presenting the financial information to the internal management so as to assist

them in making an effective decision and plans for the betterment of an organisation. In business

organisation whether small, medium or large various kinds of reports are prepared which

contains different informations such as total receivables, availability of cash, total revenues and

cost incurred in execution of business operation. Therefore, management accounting play an

important role in leading business towards success. Tech (UK) Ltd. which deals in

manufacturing Tech (UK) Limited, who is producing special charger for mobile telephone and

other carry-on gadgets for retail outlets in the UK is selected for the purpose of preparing this

report. The project includes different types of management accounting systems and its essential

needs to an organisation. Along with this, various management accounting reporting system are

also discussed under this report in detailed manner. The project also describes the costing

methods along with calculation of net profitability, planning tools to control budget and financial

tools to resolving financial issues that facilitate organisation to maintain their financial position

among their rivals in competitive market (Callahan, Stetz and Brooks,2011).

TASK 1

P1: Management accounting systems and its essential requirements to an organisation

Accounting: It is a systematic recording of financial transactions made by an

organisation on daily basis. It help in measuring the results of an organisation's economic

activities and communicate it to their variety of users such as investor, creditors, management

etc. It mainly consists of two parts such as management accounting and financial accounting

which are explained as under:

Management accounting: It is the process of identifying, measuring, analysing and

communicating relevant and accurate information to managers so as to make easy for them to

make an effective decision to achieve organisational goals. It provides both monetary as well as

non-monetary information which is useful for internal management to make better policies. As it

is formed as per the needs and requirements of company thus not mandatory.

Financial accounting: It is the process of recording, summarizing and reporting the

myriad of transactions made during execution of business operations over a period of time. Such

1

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

transactions are summarised in the preparation of financial statements such as Profit & Loss a/c,

Balance sheets, Cash flow statement etc. that shows the actual and true financial position of

company over a specified period. It is more useful for external parties as it allows them to make

decision regarding further investment in company.

Tech (UK) Ltd. is a small-sized company which is engaged in manufacturing electronic

gadgets such as special mobile chargers and other carry-on gadgets to retail outlets in UK

therefore it is more important for company to record each transactions made by each department

on daily basis so that the actual position of company at present time can be easily identified. It

assist management in identifying the deviations which causes differences in actual and standard

output. Preparing managerial reports is well supported by different management accounting

systems which are briefly discussed as under:

Types of management accounting systems:

Cost accounting systems: It is considered as an effective system which is adopted to

identify the total cost incurred in the execution of different business functions. It prepares

management to form an effective budget for future time period after analysing the cost incurred

in business activities in previous years (Dražić Lutilsky and Dragija, 2012). By using such

system, the management of Tech (UK) Ltd. is able to record, categorising, estimating the cost of

business functions in order to achieve high profitability. Cost accounting system is basically

classified into three methods which are define as under:

Normal costing: Normal costing uses indirect materials and labour costs to estimate

production costs. It provides a more consistent valuation of production costs which eliminates

month to month fluctuations. Tech (UK) Ltd. produced 10,000 mobile chargers. The actual

materials used totalled to be $50.00 per charger and direct costs were $20.00 per charger. The

manufacturing overhead determined per charger is $10.00. So the managers determines it costs

the company $80.00 to produce one mobile charger.

Actual costing: Actual costing uses the actual cost of materials and labour to calculate

production costs. This is beneficial when analysing a specific portion of the production process

and an exact accounting of costs is needed. For example, a Tech (UK) Ltd. may estimate that

production of charger will cost $700, but the actual cost may in fact be $800. One often is not

informed of the actual cost until it is incurred.

2

Balance sheets, Cash flow statement etc. that shows the actual and true financial position of

company over a specified period. It is more useful for external parties as it allows them to make

decision regarding further investment in company.

Tech (UK) Ltd. is a small-sized company which is engaged in manufacturing electronic

gadgets such as special mobile chargers and other carry-on gadgets to retail outlets in UK

therefore it is more important for company to record each transactions made by each department

on daily basis so that the actual position of company at present time can be easily identified. It

assist management in identifying the deviations which causes differences in actual and standard

output. Preparing managerial reports is well supported by different management accounting

systems which are briefly discussed as under:

Types of management accounting systems:

Cost accounting systems: It is considered as an effective system which is adopted to

identify the total cost incurred in the execution of different business functions. It prepares

management to form an effective budget for future time period after analysing the cost incurred

in business activities in previous years (Dražić Lutilsky and Dragija, 2012). By using such

system, the management of Tech (UK) Ltd. is able to record, categorising, estimating the cost of

business functions in order to achieve high profitability. Cost accounting system is basically

classified into three methods which are define as under:

Normal costing: Normal costing uses indirect materials and labour costs to estimate

production costs. It provides a more consistent valuation of production costs which eliminates

month to month fluctuations. Tech (UK) Ltd. produced 10,000 mobile chargers. The actual

materials used totalled to be $50.00 per charger and direct costs were $20.00 per charger. The

manufacturing overhead determined per charger is $10.00. So the managers determines it costs

the company $80.00 to produce one mobile charger.

Actual costing: Actual costing uses the actual cost of materials and labour to calculate

production costs. This is beneficial when analysing a specific portion of the production process

and an exact accounting of costs is needed. For example, a Tech (UK) Ltd. may estimate that

production of charger will cost $700, but the actual cost may in fact be $800. One often is not

informed of the actual cost until it is incurred.

2

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Standard costing: Standard costing is an effective accounting technique that some

manufacturers use to identify the differences or variances occurred in actual and standard results.

For an example, Based on historical data, a cost analyst determines that producing one widget

typically requires 1 pound of raw material costing $2 dollars and 1 hour of labour costing $20

dollars. These are the standard amounts and costs for material and labour.

Tech (UK) Ltd. is producing special mobile chargers for the UK retailers therefore using

such system help in tracking cost of producing product and prepare budget accordingly. It

enables in minimising the cost of production which makes positive impact on their profitability

as well (Granlund, 2011).

Inventory management system: It is a system which is concerned with supervision and

management of stock and non-capitalised assets of an organisation. It ensures organisation about

availability of inventory at present so that the management can take orders from their clients and

place order to the suppliers in order to avoid any interruptions in execution of business activities.

Using such accounting system, Tech (UK) Ltd. Is able to meet customers requirements on time

due to having sufficient amount of information about current level of inventory which indirectly

help in achieving loyalty and trust of their targeted clients. Inventory management system is

categories into different parts which are determined as under: FIFO: It is a method of valuation in which the assets produced or acquired first by

company are sold at first. For the purposes of taxation, FIFO has assumed that the stock

available in inventory are matched with the stock acquired or produced by company. LIFO: It is a method used to account for inventory where the goods produced fist will be

sold as first. For example, Tech (UK) Ltd. has produced special mobile chargers, then

using such method the cost of product produced first are the first to be expenses as cost of

goods sold that means the lower cost of older products will be reported as inventory. JIT: It is a management strategy that brings raw materials from the suppliers directly to

the production process in order to avoid any interruptions. It is used by companies such

as Tech (UK) Ltd. to increase efficiency and reducing wastage by receiving goods only

when the production process requires as it reduces inventory costs.

Job costing systems: It is concerned with identification of cost allocated to manufacture

product or bunch of products so as to examine the effectiveness of each product in the market.

Using such system, it enables management of Tech (UK) Ltd. to think whether to produce

3

manufacturers use to identify the differences or variances occurred in actual and standard results.

For an example, Based on historical data, a cost analyst determines that producing one widget

typically requires 1 pound of raw material costing $2 dollars and 1 hour of labour costing $20

dollars. These are the standard amounts and costs for material and labour.

Tech (UK) Ltd. is producing special mobile chargers for the UK retailers therefore using

such system help in tracking cost of producing product and prepare budget accordingly. It

enables in minimising the cost of production which makes positive impact on their profitability

as well (Granlund, 2011).

Inventory management system: It is a system which is concerned with supervision and

management of stock and non-capitalised assets of an organisation. It ensures organisation about

availability of inventory at present so that the management can take orders from their clients and

place order to the suppliers in order to avoid any interruptions in execution of business activities.

Using such accounting system, Tech (UK) Ltd. Is able to meet customers requirements on time

due to having sufficient amount of information about current level of inventory which indirectly

help in achieving loyalty and trust of their targeted clients. Inventory management system is

categories into different parts which are determined as under: FIFO: It is a method of valuation in which the assets produced or acquired first by

company are sold at first. For the purposes of taxation, FIFO has assumed that the stock

available in inventory are matched with the stock acquired or produced by company. LIFO: It is a method used to account for inventory where the goods produced fist will be

sold as first. For example, Tech (UK) Ltd. has produced special mobile chargers, then

using such method the cost of product produced first are the first to be expenses as cost of

goods sold that means the lower cost of older products will be reported as inventory. JIT: It is a management strategy that brings raw materials from the suppliers directly to

the production process in order to avoid any interruptions. It is used by companies such

as Tech (UK) Ltd. to increase efficiency and reducing wastage by receiving goods only

when the production process requires as it reduces inventory costs.

Job costing systems: It is concerned with identification of cost allocated to manufacture

product or bunch of products so as to examine the effectiveness of each product in the market.

Using such system, it enables management of Tech (UK) Ltd. to think whether to produce

3

individual product or group of products in order to achieve huge profitability through incurring

minimum cost in production process. For example, Tech (UK) Ltd. Is producing special mobile

chargers thus it is important for management to identify cost incurred in production process so

that it makes easy calculation and measurement of cost incurred in individual job associated with

manufacturing process.

P2: Different types of management accounting reports

Every organisation whether engaged in manufacturing sector or retail or construction

activities is required to maintain accounting reports on specified time period in order to have

adequate amount of relevant and accurate information about the position of company during

decision-making process (JOSHI and et. al., 2011). Such reports must include information

related with both monetary and non-monetary terms as it aid management in making an effective

decisions and suitable plans for the growth and expansion of business organisation. Therefore,

Tech (UK) Ltd. Must required to prepare various kinds of reports to expand its business on large

scale. Such reporting systems includes financial report, accounting receivable and payable report,

inventory management report etc. It describes the overview of company which become more

beneficial to outside party of an organisation such as investors, suppliers, creditors etc. as it

makes easy for them to decide whether to invest more in such company or should stop. It can be

further understood under the below:

Types of managerial accounting reports:

Cost accounting report: Such report contains the information about the cost invested in

execution of different business activities which enables management to prepare an effective

budget for future executed business activities. Tech (UK) Ltd. must required to prepare such kind

of report in order to reduce business cost through estimating the cost incurred in future period by

analysing the information obtain from such report regarding cost incurred in previous business

activities.

Inventory management report: It is a document which contains accurate and relevant

details about closing and opening stock with the company. It facilitate management to manage

inventory movement that are maintained by Tech (UK) Ltd. Therefore, it is more useful for Tech

(UK) Ltd. to prepare such kind of report in order to reviewing current status of company

inventory by location, time of arrival and departure of inventory etc. It reduces inventory storage

cost of company which directly makes positive impact on the profitability. Just-in-time, EOQ

4

minimum cost in production process. For example, Tech (UK) Ltd. Is producing special mobile

chargers thus it is important for management to identify cost incurred in production process so

that it makes easy calculation and measurement of cost incurred in individual job associated with

manufacturing process.

P2: Different types of management accounting reports

Every organisation whether engaged in manufacturing sector or retail or construction

activities is required to maintain accounting reports on specified time period in order to have

adequate amount of relevant and accurate information about the position of company during

decision-making process (JOSHI and et. al., 2011). Such reports must include information

related with both monetary and non-monetary terms as it aid management in making an effective

decisions and suitable plans for the growth and expansion of business organisation. Therefore,

Tech (UK) Ltd. Must required to prepare various kinds of reports to expand its business on large

scale. Such reporting systems includes financial report, accounting receivable and payable report,

inventory management report etc. It describes the overview of company which become more

beneficial to outside party of an organisation such as investors, suppliers, creditors etc. as it

makes easy for them to decide whether to invest more in such company or should stop. It can be

further understood under the below:

Types of managerial accounting reports:

Cost accounting report: Such report contains the information about the cost invested in

execution of different business activities which enables management to prepare an effective

budget for future executed business activities. Tech (UK) Ltd. must required to prepare such kind

of report in order to reduce business cost through estimating the cost incurred in future period by

analysing the information obtain from such report regarding cost incurred in previous business

activities.

Inventory management report: It is a document which contains accurate and relevant

details about closing and opening stock with the company. It facilitate management to manage

inventory movement that are maintained by Tech (UK) Ltd. Therefore, it is more useful for Tech

(UK) Ltd. to prepare such kind of report in order to reviewing current status of company

inventory by location, time of arrival and departure of inventory etc. It reduces inventory storage

cost of company which directly makes positive impact on the profitability. Just-in-time, EOQ

4

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

and Turnover ratio are some useful techniques which are required to be consider by Tech (UK)

Ltd. to maintain inventory position.

Financial report: It is a document containing actual and reliable financial information of

company at the end of accounting period which can be recorded from various financial reports

such as Profit & Loss a/c, Balance sheets and Cash flow statement etc. Such kinds of reports are

prepared on annual basis which determines the cash inflow and outflow of an organisation.

Therefore, it is essential for Tech (UK) Ltd. to prepare such report as it assist management

identify the deviation which causes differences between actual and desired financial performance

and accordingly make an effective decisions to maintain strong financial performance in future

period of time (Kuula, Putkiranta and Toivanen, 2012).

Accounting receivable report: It is the document which contains the actual information

about the list of debtors having unpaid amount to company for the product and services received

by them in previous period of time. It enables management to identify the unpaid amount and

accordingly make strategies to recover the same within specified time period. It increases the

cash availability of company thus must required to prepare such kind of report by Tech (UK)

Ltd. In order to recover the pending amount from debtors and make relevant changes in existing

credit policies so as to avoid any loss of funds.

Accounting payable report: It is the report which contains the accurate information about

the payment that yet to be paid by company to their suppliers. It helps in identifying the list of

suppliers to whom the company should required to pay in future for the product and services they

received in earlier time period. Making payment to suppliers on time increases their loyalty and

trust due to which the suppliers also deliver raw materials used in production process of

company on time. This will help company in meeting customers requirements in more effective

and efficient manner. Therefore, Tech (UK) Ltd. Must required to prepare such kind of report to

achieve loyalty and gain confidence of suppliers by making payments on due date.

M1: Importance of different management system

Importance of such management accounting systems:

Presenting accurate right information: Such systems help in providing accurate and

reliable information about the current position of company which makes easy for outside parties

such as investors to make decision regarding further investment.

5

Ltd. to maintain inventory position.

Financial report: It is a document containing actual and reliable financial information of

company at the end of accounting period which can be recorded from various financial reports

such as Profit & Loss a/c, Balance sheets and Cash flow statement etc. Such kinds of reports are

prepared on annual basis which determines the cash inflow and outflow of an organisation.

Therefore, it is essential for Tech (UK) Ltd. to prepare such report as it assist management

identify the deviation which causes differences between actual and desired financial performance

and accordingly make an effective decisions to maintain strong financial performance in future

period of time (Kuula, Putkiranta and Toivanen, 2012).

Accounting receivable report: It is the document which contains the actual information

about the list of debtors having unpaid amount to company for the product and services received

by them in previous period of time. It enables management to identify the unpaid amount and

accordingly make strategies to recover the same within specified time period. It increases the

cash availability of company thus must required to prepare such kind of report by Tech (UK)

Ltd. In order to recover the pending amount from debtors and make relevant changes in existing

credit policies so as to avoid any loss of funds.

Accounting payable report: It is the report which contains the accurate information about

the payment that yet to be paid by company to their suppliers. It helps in identifying the list of

suppliers to whom the company should required to pay in future for the product and services they

received in earlier time period. Making payment to suppliers on time increases their loyalty and

trust due to which the suppliers also deliver raw materials used in production process of

company on time. This will help company in meeting customers requirements in more effective

and efficient manner. Therefore, Tech (UK) Ltd. Must required to prepare such kind of report to

achieve loyalty and gain confidence of suppliers by making payments on due date.

M1: Importance of different management system

Importance of such management accounting systems:

Presenting accurate right information: Such systems help in providing accurate and

reliable information about the current position of company which makes easy for outside parties

such as investors to make decision regarding further investment.

5

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Aid in decision-making: It also assist management to make an effective decisions and

suitable policies to maximises the interest and satisfaction level of interested parties such as

customers, employees etc.

To speed up process: Using various systems such as inventory management system

which enables management to make decision regarding placing orders to suppliers so as to meet

customers demands on time.

D1: Various reporting method and accounting system integration.

As Tech (UK) Ltd. utilises various management accounting system and reporting that

communicates useful information about financial position and current status to the shareholder

and other investors. The link among report and system of management within as organisation

process is said to be integrated accounting system. Performance reports, inventory management

report, account receivable report etc. are more useful for Tech (UK) Ltd. to prepare to acquiring

information about the actual position of business at present time.

TASK 2

P3: Techniques used to analyse cost with marginal and absorption costs

Cost: It refers to the amount value which is sacrificed or paid to acquire something. In

other words, it the combination of various aspects such as effort, material, resources, time and

utilities invested, risk faced etc. The valuation of such aspects is known as cost.

In business organisation, all expenses are cost whereas all costs are not expenses due to

inclusion of some of the cost in income generating process. Tech (UK) Ltd. Is operating its

business activities at small-scale due to which they have limited funds to invest in execution of

different business functions. Therefore, it is important for company to prepare an effective

budget in which proper allocation of cost are required to be made in order to achieve desired

profitability (Moser, 2012). For this, the managers of Tech (UK) Ltd. Are required to use

different costing methods such as marginal and absorption costing which are further understood

under the below:

Absorption costing: It includes all those fixed and variable costs which are invested in

execution of different business activities which includes direct labour, material and fixed and

manufacturing overheads. It is considered as an effective costing method due to bringing out

actual cost incurred in business functions which enables management to make an effective

decisions for further business activities.

6

suitable policies to maximises the interest and satisfaction level of interested parties such as

customers, employees etc.

To speed up process: Using various systems such as inventory management system

which enables management to make decision regarding placing orders to suppliers so as to meet

customers demands on time.

D1: Various reporting method and accounting system integration.

As Tech (UK) Ltd. utilises various management accounting system and reporting that

communicates useful information about financial position and current status to the shareholder

and other investors. The link among report and system of management within as organisation

process is said to be integrated accounting system. Performance reports, inventory management

report, account receivable report etc. are more useful for Tech (UK) Ltd. to prepare to acquiring

information about the actual position of business at present time.

TASK 2

P3: Techniques used to analyse cost with marginal and absorption costs

Cost: It refers to the amount value which is sacrificed or paid to acquire something. In

other words, it the combination of various aspects such as effort, material, resources, time and

utilities invested, risk faced etc. The valuation of such aspects is known as cost.

In business organisation, all expenses are cost whereas all costs are not expenses due to

inclusion of some of the cost in income generating process. Tech (UK) Ltd. Is operating its

business activities at small-scale due to which they have limited funds to invest in execution of

different business functions. Therefore, it is important for company to prepare an effective

budget in which proper allocation of cost are required to be made in order to achieve desired

profitability (Moser, 2012). For this, the managers of Tech (UK) Ltd. Are required to use

different costing methods such as marginal and absorption costing which are further understood

under the below:

Absorption costing: It includes all those fixed and variable costs which are invested in

execution of different business activities which includes direct labour, material and fixed and

manufacturing overheads. It is considered as an effective costing method due to bringing out

actual cost incurred in business functions which enables management to make an effective

decisions for further business activities.

6

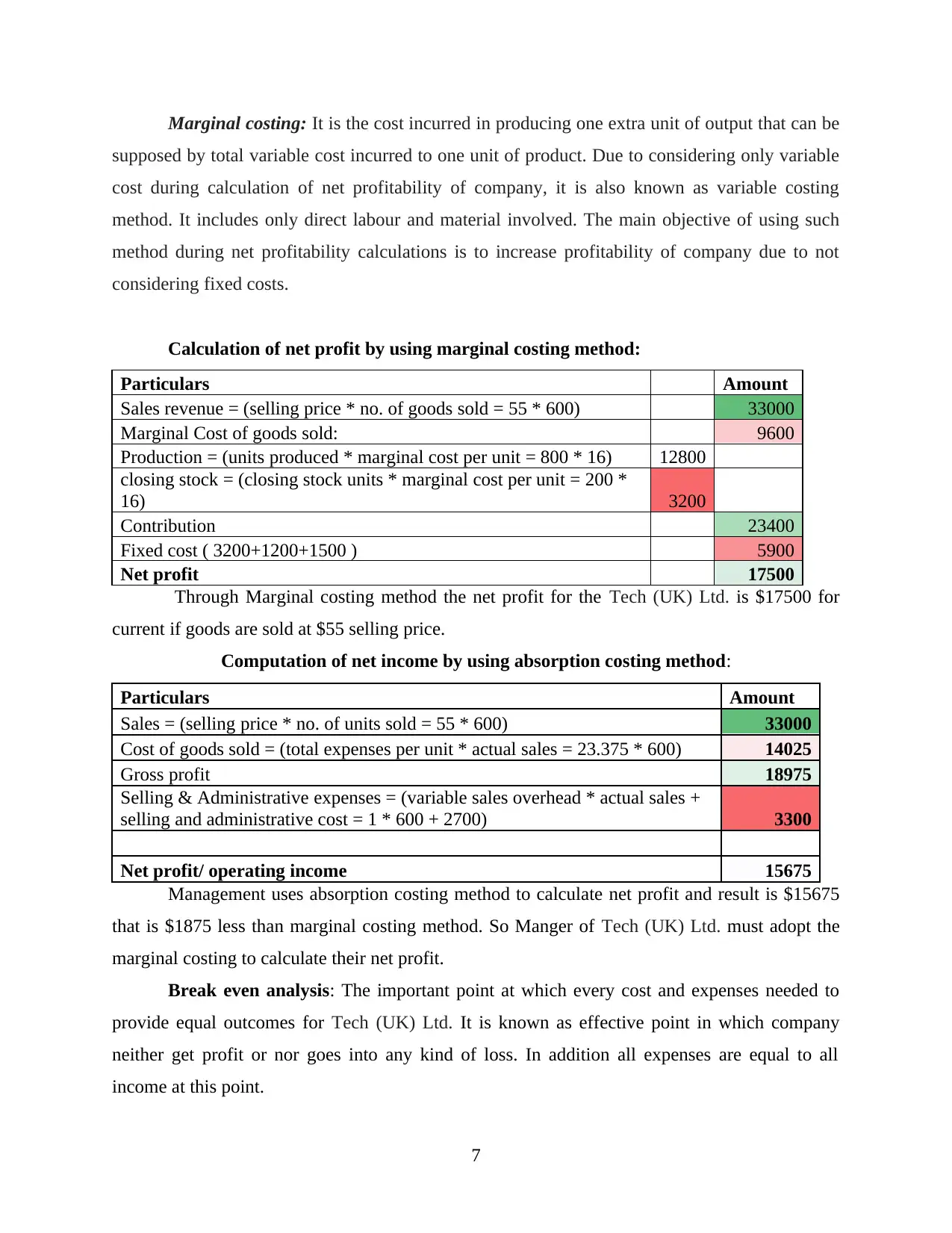

Marginal costing: It is the cost incurred in producing one extra unit of output that can be

supposed by total variable cost incurred to one unit of product. Due to considering only variable

cost during calculation of net profitability of company, it is also known as variable costing

method. It includes only direct labour and material involved. The main objective of using such

method during net profitability calculations is to increase profitability of company due to not

considering fixed costs.

Calculation of net profit by using marginal costing method:

Particulars Amount

Sales revenue = (selling price * no. of goods sold = 55 * 600) 33000

Marginal Cost of goods sold: 9600

Production = (units produced * marginal cost per unit = 800 * 16) 12800

closing stock = (closing stock units * marginal cost per unit = 200 *

16) 3200

Contribution 23400

Fixed cost ( 3200+1200+1500 ) 5900

Net profit 17500

Through Marginal costing method the net profit for the Tech (UK) Ltd. is $17500 for

current if goods are sold at $55 selling price.

Computation of net income by using absorption costing method:

Particulars Amount

Sales = (selling price * no. of units sold = 55 * 600) 33000

Cost of goods sold = (total expenses per unit * actual sales = 23.375 * 600) 14025

Gross profit 18975

Selling & Administrative expenses = (variable sales overhead * actual sales +

selling and administrative cost = 1 * 600 + 2700) 3300

Net profit/ operating income 15675

Management uses absorption costing method to calculate net profit and result is $15675

that is $1875 less than marginal costing method. So Manger of Tech (UK) Ltd. must adopt the

marginal costing to calculate their net profit.

Break even analysis: The important point at which every cost and expenses needed to

provide equal outcomes for Tech (UK) Ltd. It is known as effective point in which company

neither get profit or nor goes into any kind of loss. In addition all expenses are equal to all

income at this point.

7

supposed by total variable cost incurred to one unit of product. Due to considering only variable

cost during calculation of net profitability of company, it is also known as variable costing

method. It includes only direct labour and material involved. The main objective of using such

method during net profitability calculations is to increase profitability of company due to not

considering fixed costs.

Calculation of net profit by using marginal costing method:

Particulars Amount

Sales revenue = (selling price * no. of goods sold = 55 * 600) 33000

Marginal Cost of goods sold: 9600

Production = (units produced * marginal cost per unit = 800 * 16) 12800

closing stock = (closing stock units * marginal cost per unit = 200 *

16) 3200

Contribution 23400

Fixed cost ( 3200+1200+1500 ) 5900

Net profit 17500

Through Marginal costing method the net profit for the Tech (UK) Ltd. is $17500 for

current if goods are sold at $55 selling price.

Computation of net income by using absorption costing method:

Particulars Amount

Sales = (selling price * no. of units sold = 55 * 600) 33000

Cost of goods sold = (total expenses per unit * actual sales = 23.375 * 600) 14025

Gross profit 18975

Selling & Administrative expenses = (variable sales overhead * actual sales +

selling and administrative cost = 1 * 600 + 2700) 3300

Net profit/ operating income 15675

Management uses absorption costing method to calculate net profit and result is $15675

that is $1875 less than marginal costing method. So Manger of Tech (UK) Ltd. must adopt the

marginal costing to calculate their net profit.

Break even analysis: The important point at which every cost and expenses needed to

provide equal outcomes for Tech (UK) Ltd. It is known as effective point in which company

neither get profit or nor goes into any kind of loss. In addition all expenses are equal to all

income at this point.

7

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

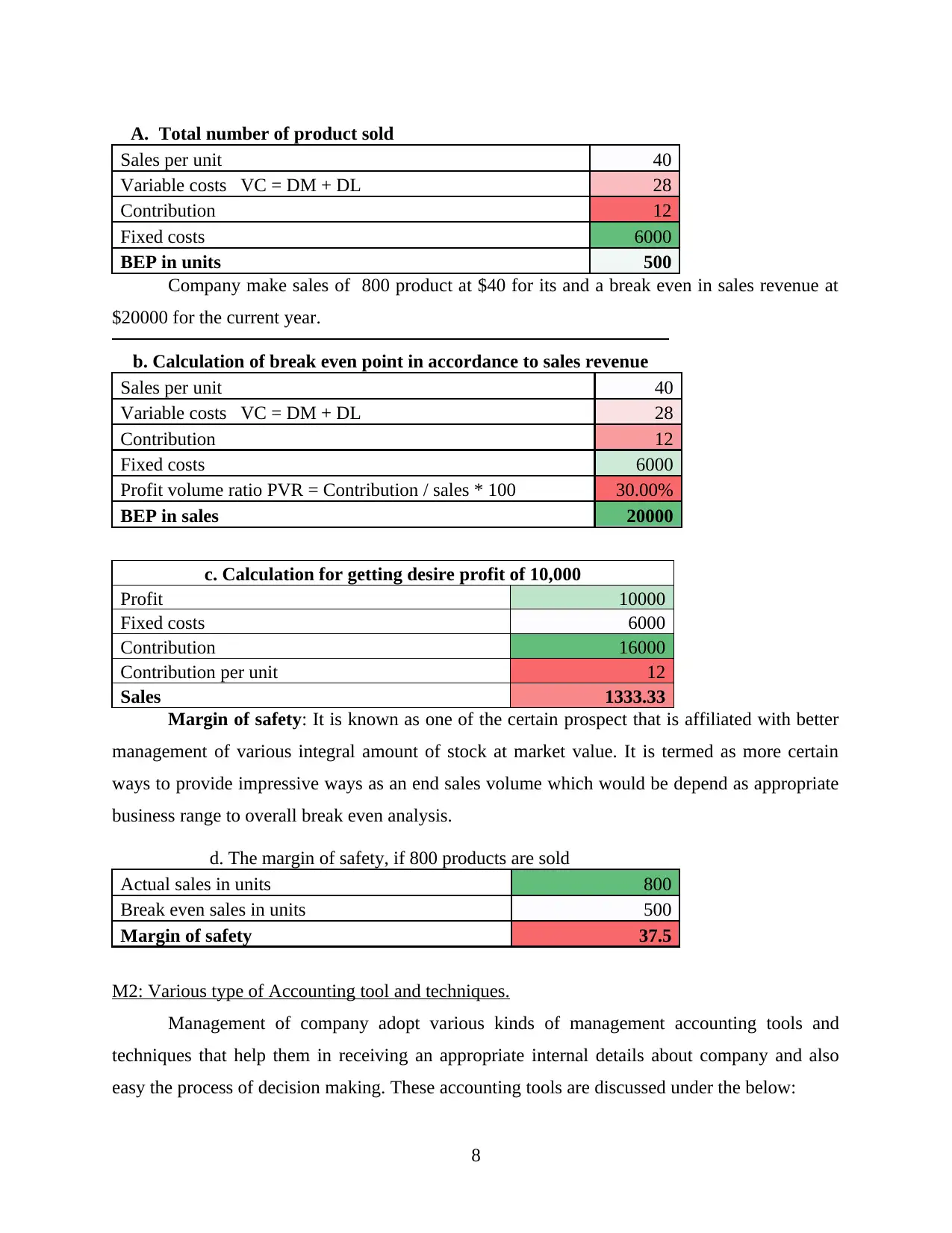

A. Total number of product sold

Sales per unit 40

Variable costs VC = DM + DL 28

Contribution 12

Fixed costs 6000

BEP in units 500

Company make sales of 800 product at $40 for its and a break even in sales revenue at

$20000 for the current year.

b. Calculation of break even point in accordance to sales revenue

Sales per unit 40

Variable costs VC = DM + DL 28

Contribution 12

Fixed costs 6000

Profit volume ratio PVR = Contribution / sales * 100 30.00%

BEP in sales 20000

c. Calculation for getting desire profit of 10,000

Profit 10000

Fixed costs 6000

Contribution 16000

Contribution per unit 12

Sales 1333.33

Margin of safety: It is known as one of the certain prospect that is affiliated with better

management of various integral amount of stock at market value. It is termed as more certain

ways to provide impressive ways as an end sales volume which would be depend as appropriate

business range to overall break even analysis.

d. The margin of safety, if 800 products are sold

Actual sales in units 800

Break even sales in units 500

Margin of safety 37.5

M2: Various type of Accounting tool and techniques.

Management of company adopt various kinds of management accounting tools and

techniques that help them in receiving an appropriate internal details about company and also

easy the process of decision making. These accounting tools are discussed under the below:

8

Sales per unit 40

Variable costs VC = DM + DL 28

Contribution 12

Fixed costs 6000

BEP in units 500

Company make sales of 800 product at $40 for its and a break even in sales revenue at

$20000 for the current year.

b. Calculation of break even point in accordance to sales revenue

Sales per unit 40

Variable costs VC = DM + DL 28

Contribution 12

Fixed costs 6000

Profit volume ratio PVR = Contribution / sales * 100 30.00%

BEP in sales 20000

c. Calculation for getting desire profit of 10,000

Profit 10000

Fixed costs 6000

Contribution 16000

Contribution per unit 12

Sales 1333.33

Margin of safety: It is known as one of the certain prospect that is affiliated with better

management of various integral amount of stock at market value. It is termed as more certain

ways to provide impressive ways as an end sales volume which would be depend as appropriate

business range to overall break even analysis.

d. The margin of safety, if 800 products are sold

Actual sales in units 800

Break even sales in units 500

Margin of safety 37.5

M2: Various type of Accounting tool and techniques.

Management of company adopt various kinds of management accounting tools and

techniques that help them in receiving an appropriate internal details about company and also

easy the process of decision making. These accounting tools are discussed under the below:

8

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Marginal costing tool: As this tool facilitate to determine the actual cost incurred in the

production of one additional unit of outcome. It also one of the best tool that aid in calculating

net profit of company of company charging variable units.

Historical cost: This process is related to the measurement of value of assets that is used

in accounting on the balance sheet depending on its actual cost when acquired by the company.

D2 Preparation of financial statements from collected data.

Management of Tech (UK) Ltd. uses different costing method in order to increase its net

profit and resolve various issues that might arise in company. This will help manager to make

effective decision making. In Tech (UK) Ltd., marginal and absorption costing method are used

to calculate net profit for the present year. The total amount of net profit generated from

absorption method is $15675 whereas from marginal costing amount of profit is $17500. These

result are being calculated by using total fixed cost incurred in production process. So,

management of Tech (UK) Ltd. must adopt marginal costing system to make sufficient amount

of profit.

TASK 3

P4: Different planning tools used for budgetary control

Budgeting: It is the process of establishing a plan to spend money in execution of future

business activities thus spending plan is called as budget. It helps management to determine in

advance whether to have sufficient amount of funds to execute future business activities or

should arrange funds from different sources. The main objective of budgeting is to prevent any

shortage of resources during execution of future activities and also minimising the wastage so

that desired result can be achieved within pre-determined time period.

According to ACCA, budgeting is an essential component of management control

systems as it helps in providing a system of planning, coordination and control for management.

It is an arduous process and often strikes dread in the hearts of those involved in budget

preparation (Quinn, 2011).

According to CIMA, budgeting is a plan quantified in monetary term prepare and

approved before defining period of time usual showing the planned income to be achieved and

expenditure that to be incurred.

Different planning tools for budgetary control:

9

production of one additional unit of outcome. It also one of the best tool that aid in calculating

net profit of company of company charging variable units.

Historical cost: This process is related to the measurement of value of assets that is used

in accounting on the balance sheet depending on its actual cost when acquired by the company.

D2 Preparation of financial statements from collected data.

Management of Tech (UK) Ltd. uses different costing method in order to increase its net

profit and resolve various issues that might arise in company. This will help manager to make

effective decision making. In Tech (UK) Ltd., marginal and absorption costing method are used

to calculate net profit for the present year. The total amount of net profit generated from

absorption method is $15675 whereas from marginal costing amount of profit is $17500. These

result are being calculated by using total fixed cost incurred in production process. So,

management of Tech (UK) Ltd. must adopt marginal costing system to make sufficient amount

of profit.

TASK 3

P4: Different planning tools used for budgetary control

Budgeting: It is the process of establishing a plan to spend money in execution of future

business activities thus spending plan is called as budget. It helps management to determine in

advance whether to have sufficient amount of funds to execute future business activities or

should arrange funds from different sources. The main objective of budgeting is to prevent any

shortage of resources during execution of future activities and also minimising the wastage so

that desired result can be achieved within pre-determined time period.

According to ACCA, budgeting is an essential component of management control

systems as it helps in providing a system of planning, coordination and control for management.

It is an arduous process and often strikes dread in the hearts of those involved in budget

preparation (Quinn, 2011).

According to CIMA, budgeting is a plan quantified in monetary term prepare and

approved before defining period of time usual showing the planned income to be achieved and

expenditure that to be incurred.

Different planning tools for budgetary control:

9

Planning tools for budgeting

Cash budget: Cash budget is one of the forecasting method for estimating cash payments

and cash receipts. It is also used for forecasting cash position for a particular time frame. Cash

budgeting is usually done on a short time frame in compare to other financial statements. This is

framed month by month or on week by week basis to find out accurate cash position. Cash

budgeting enable Tech UK to find out cash shortages and take major actions to overcome this

shortage. There are two types of cash budgeting namely:

(a) Cash receipts: Cash receipts is simple way to identify an keep track on sales of goods and

services when cash is gained by crediting sales and debiting transaction (b) Cash payment: Cash

payment is used in accounting to record and maintain those transaction that are already paid in

the form of cash.

Advantages of Cash Budget

Firstly, it enables Tech UK to find and predict those areas where there is shortage of cash

and take action against it to overcome cash crisis.

Secondly, it allows Tech UK to identify those areas excess cash are lying idle and can be

utilized in better areas for profit making.

Disadvantage of Cash Budget

Firstly, there is always an issue with cash budget regarding danger of theft.

Secondly, its lower down the ability to create a credit profile.

Variance Analysis: Variance analysis deals with estimating the difference between a

planned cost and the actual cost that is incurred. Tech UK use variance analysis as key of

planned costing system to maintain their costs and revenues. Variance analysis is accounting

method that refers to identify the deviations that is found in financial operation from planned

budgets defined by organization. Advantage of Variance analysis: It helps in analysis and computation of both costs as

well as revenues.

Disadvantage: It adversely affects the working behavior of employees due to continuous

analyzing their performance.

Master Budgets: Master budgeting act as central nerves planning technique which

enables management to guideline the responsibility and activities of an organization. Master

budgets allows to handle various function which includes financial statements, financial planning

10

Cash budget: Cash budget is one of the forecasting method for estimating cash payments

and cash receipts. It is also used for forecasting cash position for a particular time frame. Cash

budgeting is usually done on a short time frame in compare to other financial statements. This is

framed month by month or on week by week basis to find out accurate cash position. Cash

budgeting enable Tech UK to find out cash shortages and take major actions to overcome this

shortage. There are two types of cash budgeting namely:

(a) Cash receipts: Cash receipts is simple way to identify an keep track on sales of goods and

services when cash is gained by crediting sales and debiting transaction (b) Cash payment: Cash

payment is used in accounting to record and maintain those transaction that are already paid in

the form of cash.

Advantages of Cash Budget

Firstly, it enables Tech UK to find and predict those areas where there is shortage of cash

and take action against it to overcome cash crisis.

Secondly, it allows Tech UK to identify those areas excess cash are lying idle and can be

utilized in better areas for profit making.

Disadvantage of Cash Budget

Firstly, there is always an issue with cash budget regarding danger of theft.

Secondly, its lower down the ability to create a credit profile.

Variance Analysis: Variance analysis deals with estimating the difference between a

planned cost and the actual cost that is incurred. Tech UK use variance analysis as key of

planned costing system to maintain their costs and revenues. Variance analysis is accounting

method that refers to identify the deviations that is found in financial operation from planned

budgets defined by organization. Advantage of Variance analysis: It helps in analysis and computation of both costs as

well as revenues.

Disadvantage: It adversely affects the working behavior of employees due to continuous

analyzing their performance.

Master Budgets: Master budgeting act as central nerves planning technique which

enables management to guideline the responsibility and activities of an organization. Master

budgets allows to handle various function which includes financial statements, financial planning

10

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 17

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.