Management Accounting Report: Unilever and Costing Methods

VerifiedAdded on 2020/10/05

|22

|5808

|188

Report

AI Summary

This report provides a comprehensive analysis of management accounting practices within Unilever. It begins with an introduction to management accounting, its role, and different systems, including cost accounting and inventory management. The report then delves into various methods such as financial accounting, financial statement analysis, fund flow analysis, cash flow analysis, marginal costing, budgetary control, ratio analysis, and management reporting, explaining their applications within the company. The benefits of management accounting systems, including planning, controlling, and organizing, are also discussed. Furthermore, the report addresses the preparation of income statements using both absorption and marginal costing. Finally, it compares Unilever's management accounting methods with those of other organizations, evaluating the role of budgets in resolving financial problems, and concludes with a summary of findings and references.

Management Accounting

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of Contents

INTRODUCTION...........................................................................................................................1

LO 1.................................................................................................................................................1

Role of management accounting and different management accounting system ......................1

Different methods used in management accounting system ......................................................3

Benefits of management accounting systems in select company ...............................................5

LO 2.................................................................................................................................................6

Prepare income statement using both absorption and marginal costing ....................................6

Produce management accounting reports that apply in range of different business activities ...7

LO 3.................................................................................................................................................8

Advantages and disadvantages of planning tools used in budgetary control..............................8

Analysis of different planning tools and its application in preparing budgets............................9

LO 4...............................................................................................................................................10

Comparing the management accounting methods of Unilever with other organisation...........10

Analysis of management accounting method...........................................................................12

Evaluating the role of budget for resolving financial problem.................................................13

CONCLUSION..............................................................................................................................13

REFERENCES..............................................................................................................................15

.......................................................................................................................................................16

APPENDIX....................................................................................................................................17

INTRODUCTION...........................................................................................................................1

LO 1.................................................................................................................................................1

Role of management accounting and different management accounting system ......................1

Different methods used in management accounting system ......................................................3

Benefits of management accounting systems in select company ...............................................5

LO 2.................................................................................................................................................6

Prepare income statement using both absorption and marginal costing ....................................6

Produce management accounting reports that apply in range of different business activities ...7

LO 3.................................................................................................................................................8

Advantages and disadvantages of planning tools used in budgetary control..............................8

Analysis of different planning tools and its application in preparing budgets............................9

LO 4...............................................................................................................................................10

Comparing the management accounting methods of Unilever with other organisation...........10

Analysis of management accounting method...........................................................................12

Evaluating the role of budget for resolving financial problem.................................................13

CONCLUSION..............................................................................................................................13

REFERENCES..............................................................................................................................15

.......................................................................................................................................................16

APPENDIX....................................................................................................................................17

INTRODUCTION

Management accounting is the display of analysis of business activities to the internal

management to facilitate decisions making. The procedure of making management reports and

accounts which provides accurate and timely financial and statistical data required by managers

to prepare daily and short terms decisions. Management accounting generates monthly and

weekly reports for inside audiences with the company (Elsukova, 2015). These reports show

amount of available cash, generating sales revenues outstanding debts and also includes trends

charts, variance analysis and other applied mathematics. It is the also called as cost accounting

which is procedure of recognizing, measuring, explanation and communicating info to managers

for the movement of objectives of organization. This study is based on Unilever. It is the British

Dutch transnational consumer goods organization in the UK. The products involve food and

drinks, beauty goods and personal care goods.

Furthermore, this report will explain role of management accounting and different

management system in the company. It will state the different methods utilised in management

accounting system. It will prepare income statement using both absorption and marginal costing

in the firm. It will explain use of planning tools utilised in management accounting in the firm. It

will compare different ways of management accounting system by different companies.

LO 1

Role of management accounting and different management accounting system

Management Accounting:

Managers utilise provisions of accounting data in relation to better inform themselves

before they decide matters within their companies like Unilever that helps their management and

execution of control operations. Management accounting is the profession which includes

partnering in administration in management decision making, making planning and performance

management systems (Beattie, 2014). It is the giving expertise in financial reporting and control

to help administration in the formulation and apply of strategy of company which is called as

management accounting. The aim of management accounting is to help managers for making

decisions within the organization. It manages margin analysis to assess profits when weighed

against varying kinds of costs.

Role of management Accounting:

1

Management accounting is the display of analysis of business activities to the internal

management to facilitate decisions making. The procedure of making management reports and

accounts which provides accurate and timely financial and statistical data required by managers

to prepare daily and short terms decisions. Management accounting generates monthly and

weekly reports for inside audiences with the company (Elsukova, 2015). These reports show

amount of available cash, generating sales revenues outstanding debts and also includes trends

charts, variance analysis and other applied mathematics. It is the also called as cost accounting

which is procedure of recognizing, measuring, explanation and communicating info to managers

for the movement of objectives of organization. This study is based on Unilever. It is the British

Dutch transnational consumer goods organization in the UK. The products involve food and

drinks, beauty goods and personal care goods.

Furthermore, this report will explain role of management accounting and different

management system in the company. It will state the different methods utilised in management

accounting system. It will prepare income statement using both absorption and marginal costing

in the firm. It will explain use of planning tools utilised in management accounting in the firm. It

will compare different ways of management accounting system by different companies.

LO 1

Role of management accounting and different management accounting system

Management Accounting:

Managers utilise provisions of accounting data in relation to better inform themselves

before they decide matters within their companies like Unilever that helps their management and

execution of control operations. Management accounting is the profession which includes

partnering in administration in management decision making, making planning and performance

management systems (Beattie, 2014). It is the giving expertise in financial reporting and control

to help administration in the formulation and apply of strategy of company which is called as

management accounting. The aim of management accounting is to help managers for making

decisions within the organization. It manages margin analysis to assess profits when weighed

against varying kinds of costs.

Role of management Accounting:

1

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Managerial accounting plays an essential role in helping managers to lead the

organization in effective manner.

Make financial strategies:

It is the necessary to formulate financial strategies utilising sales forecasts, budgets and

job costing tool between other managerial accounting methods. It also can integrate information

from financial statement of Unilever to develop strategies which increase gross income, net

profits and earning per share.

Monitor expenditure:

It can create static, flexible, rolling budgets along with another kind of reports which

enable senior leaders and departmental heads to monitor expenditure within Unilever. It is the

essential because operation expenditure have direct effect on bottom line profits.

Communicating:

Managerial accounting plays important role in establishment and maintenance of

communication and reporting system. The report about performance equipped by accountants

communicate essential info to manager (Mihăilă, 2014). It shows them different ways well

manages their actions and highlighting those issues which requires more thorough enquiry by

management by exception action.

Motivating:

Managerial accounting plays essential role in relation to budget and performance reports

which are prepared by accountants have an essential effect in motivating staff of organization

like Unilever. The budgets are targeted intending to motivate managers to accomplish objectives

of company. The performance reports plan to motivate individual execution by communicating

information linked to the targets.

Fewer number of situation:

Managerial accounting does not have to follow norms and principles of financial

accounting within the Unilever. Still, it needs to be accurate, but accountants can present

information, so that non-accountant can easily compass what is going on in the organization.

This aids take the financial information and utilization it to create future plans for operating the

firm ( Luft, Shields and Thomas, 2016).

Looking to future:

2

organization in effective manner.

Make financial strategies:

It is the necessary to formulate financial strategies utilising sales forecasts, budgets and

job costing tool between other managerial accounting methods. It also can integrate information

from financial statement of Unilever to develop strategies which increase gross income, net

profits and earning per share.

Monitor expenditure:

It can create static, flexible, rolling budgets along with another kind of reports which

enable senior leaders and departmental heads to monitor expenditure within Unilever. It is the

essential because operation expenditure have direct effect on bottom line profits.

Communicating:

Managerial accounting plays important role in establishment and maintenance of

communication and reporting system. The report about performance equipped by accountants

communicate essential info to manager (Mihăilă, 2014). It shows them different ways well

manages their actions and highlighting those issues which requires more thorough enquiry by

management by exception action.

Motivating:

Managerial accounting plays essential role in relation to budget and performance reports

which are prepared by accountants have an essential effect in motivating staff of organization

like Unilever. The budgets are targeted intending to motivate managers to accomplish objectives

of company. The performance reports plan to motivate individual execution by communicating

information linked to the targets.

Fewer number of situation:

Managerial accounting does not have to follow norms and principles of financial

accounting within the Unilever. Still, it needs to be accurate, but accountants can present

information, so that non-accountant can easily compass what is going on in the organization.

This aids take the financial information and utilization it to create future plans for operating the

firm ( Luft, Shields and Thomas, 2016).

Looking to future:

2

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Managerial accounting focus more on what is to come. Through this, trying to figure out

budget for coming financial year. Management accountant present with predictions of revenue or

list of expected expenditures. Unilever can utilise that info to work put the budget or make other

decisions for the future.

Different methods used in management accounting system

There are different management accounting system like cots accounting, inventory

management system and so on. The aim of management accounting is to help the managers of

company in recognizing and evaluating the outcomes of their judgements. It is also called as cost

accounting which includes preparation of financial reports and statistical data that can assist in

taking long-term and short term management decisions with the organization like Unilever

(Elsukova, 2015). The managerial accounting reports contains all the compulsory details about

cash flow, generating the revenue, detail of stock, payable accounts, debts and other related

statistics. In relation to, there are many methods, tools and techniques used in management

accounting. Also, there are different management accounting system like cots accounting,

inventory management system and so on.

Cost accounting system:

It is also called as costing system which is framework utilised by companies to estimate

the cost of their products for profitability analysis and inventory valuation and controlling of cost

within the Unilever.

Inventory management system:

Inventory management means to the procedure of ordering, storing, and utilising the

stock of firm. These involve management of raw material, elements and finished goods and

warehousing and processing the such items by Unilever.

Methods for management accounting system:

Financial Accounting:

It is the tool which is used in management accounting within the firm. The main objective

of any of business organization is maximising of profits. This aim is accomplished by making

proper financial planning with in Unilever. Therefore, financial planning is considered as the

best technique or method for accomplishing the objectives of company.

Financial statement analysis:

3

budget for coming financial year. Management accountant present with predictions of revenue or

list of expected expenditures. Unilever can utilise that info to work put the budget or make other

decisions for the future.

Different methods used in management accounting system

There are different management accounting system like cots accounting, inventory

management system and so on. The aim of management accounting is to help the managers of

company in recognizing and evaluating the outcomes of their judgements. It is also called as cost

accounting which includes preparation of financial reports and statistical data that can assist in

taking long-term and short term management decisions with the organization like Unilever

(Elsukova, 2015). The managerial accounting reports contains all the compulsory details about

cash flow, generating the revenue, detail of stock, payable accounts, debts and other related

statistics. In relation to, there are many methods, tools and techniques used in management

accounting. Also, there are different management accounting system like cots accounting,

inventory management system and so on.

Cost accounting system:

It is also called as costing system which is framework utilised by companies to estimate

the cost of their products for profitability analysis and inventory valuation and controlling of cost

within the Unilever.

Inventory management system:

Inventory management means to the procedure of ordering, storing, and utilising the

stock of firm. These involve management of raw material, elements and finished goods and

warehousing and processing the such items by Unilever.

Methods for management accounting system:

Financial Accounting:

It is the tool which is used in management accounting within the firm. The main objective

of any of business organization is maximising of profits. This aim is accomplished by making

proper financial planning with in Unilever. Therefore, financial planning is considered as the

best technique or method for accomplishing the objectives of company.

Financial statement analysis:

3

It is the tool which is used in management accounting within the firm. Profits & loss and

balance sheet are essential financial statements. These statements are examined for different

period (Beattie, 2014). This kind of investigation aids the management to know the rate of

growth of business concern. This examination is done through comparative financial statement,

common size statement and ratio analysis. This kind of technique help to achieve the objective of

Unilever.

Fund flow analysis:

It is the tool which is used in management accounting within the firm. This analysis

discovers the movement of fund from one period to another. Furthermore, fund flow analysis is

very useful to know whether the fund is properly utilised or not in year when compared to the

past year. The working capital modification and funds from operation are also discovered out

through fund flow analysis. This kind of technique help to achieve the objective of Unilever.

Cash flow analysis:

It is the tool which is used in management accounting within the firm. The change of

cash from one period to another can be discover through cash flow analysis (Mihăilă, 2014).

Also, the reason for cash balance and modification among two periods are also found out. It

studies the cash from operation and movement of cash in period. This kind of technique help to

achieve the objective of Unilever.

Marginal costing:

It is the tool which is used in management accounting within the firm. This technique or

method is utilised to fix selling price, selection of the best sale mix, utilization of rare raw

material or resources for making the decisions, acceptance or rejection of majority order and

international order. It is the based on fixed, variable cost and contribution. This kind of technique

help to achieve the objective of Unilever.

Budgetary control:

It is the tool which is used in management accounting within the firm. Future financial

requirements are estimated and managed according to an orderly basis under budgetary control

method ( Luft, Shields and Thomas, 2016.). It is utilised to control the fiscal execution of

business concern. Business operations are managed in desired direction. This kind of technique

help to achieve the objective of Unilever.

Ratio Analysis:

4

balance sheet are essential financial statements. These statements are examined for different

period (Beattie, 2014). This kind of investigation aids the management to know the rate of

growth of business concern. This examination is done through comparative financial statement,

common size statement and ratio analysis. This kind of technique help to achieve the objective of

Unilever.

Fund flow analysis:

It is the tool which is used in management accounting within the firm. This analysis

discovers the movement of fund from one period to another. Furthermore, fund flow analysis is

very useful to know whether the fund is properly utilised or not in year when compared to the

past year. The working capital modification and funds from operation are also discovered out

through fund flow analysis. This kind of technique help to achieve the objective of Unilever.

Cash flow analysis:

It is the tool which is used in management accounting within the firm. The change of

cash from one period to another can be discover through cash flow analysis (Mihăilă, 2014).

Also, the reason for cash balance and modification among two periods are also found out. It

studies the cash from operation and movement of cash in period. This kind of technique help to

achieve the objective of Unilever.

Marginal costing:

It is the tool which is used in management accounting within the firm. This technique or

method is utilised to fix selling price, selection of the best sale mix, utilization of rare raw

material or resources for making the decisions, acceptance or rejection of majority order and

international order. It is the based on fixed, variable cost and contribution. This kind of technique

help to achieve the objective of Unilever.

Budgetary control:

It is the tool which is used in management accounting within the firm. Future financial

requirements are estimated and managed according to an orderly basis under budgetary control

method ( Luft, Shields and Thomas, 2016.). It is utilised to control the fiscal execution of

business concern. Business operations are managed in desired direction. This kind of technique

help to achieve the objective of Unilever.

Ratio Analysis:

4

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

It is the tool which is used in management accounting within the firm. Ratio analysis is

utilised to management in the discharge of basic operations of forecasting, planning,

coordination, communication and control. It is setting the way for effective control of operations

of business by undertaking an appraisal of both physical and monetary targets. This kind of

technique help to achieve the objective of Unilever.

Management reporting:

It is the tool which is used in management accounting within the firm. It is preparing the

report on the basis of contents of profits & loss account and balance sheet as well as submit the

same before the top management. Therefore, prepared reports disclose the strength and weakness

indifferent areas of operating and financial actions (Drake, Roulstone and Thornock, 2016).

These recognitions are highly useful to management for workout control and decision making.

This kind of technique help to achieve the objective of the Unilever.

Benefits of management accounting systems in select company

Management accounting is very advantageous which is being utilised broadly. The

benefits are as follows:

Cost accounting system:

It is the tool which is used in management accounting within the firm. It presents cost

data in according to product, department, branch etc. These cost information re compared with

planned one. This comparison of two costs allows the management to decide the cause

responsible for the difference among these costs. This kind of technique help to achieve the

objective of Unilever. The management can take decisions about continuing product or changing

the sale strategy. Management accounting is not regulated by any law, the management can

decide areas which requires more analysis, investigation and accordingly draw up strategies.

Planning:

Management accounting play role in planning in which aids set future plan, accounting

information utilised in the procedure of decisions making. It plays crucial role in short terms

planning procedure within the Unilever. With this, company establish budget process and

prepares schedules and coordinates short terms plans on all business department (Lavia López

and Hiebl, 2014).

Controlling:

5

utilised to management in the discharge of basic operations of forecasting, planning,

coordination, communication and control. It is setting the way for effective control of operations

of business by undertaking an appraisal of both physical and monetary targets. This kind of

technique help to achieve the objective of Unilever.

Management reporting:

It is the tool which is used in management accounting within the firm. It is preparing the

report on the basis of contents of profits & loss account and balance sheet as well as submit the

same before the top management. Therefore, prepared reports disclose the strength and weakness

indifferent areas of operating and financial actions (Drake, Roulstone and Thornock, 2016).

These recognitions are highly useful to management for workout control and decision making.

This kind of technique help to achieve the objective of the Unilever.

Benefits of management accounting systems in select company

Management accounting is very advantageous which is being utilised broadly. The

benefits are as follows:

Cost accounting system:

It is the tool which is used in management accounting within the firm. It presents cost

data in according to product, department, branch etc. These cost information re compared with

planned one. This comparison of two costs allows the management to decide the cause

responsible for the difference among these costs. This kind of technique help to achieve the

objective of Unilever. The management can take decisions about continuing product or changing

the sale strategy. Management accounting is not regulated by any law, the management can

decide areas which requires more analysis, investigation and accordingly draw up strategies.

Planning:

Management accounting play role in planning in which aids set future plan, accounting

information utilised in the procedure of decisions making. It plays crucial role in short terms

planning procedure within the Unilever. With this, company establish budget process and

prepares schedules and coordinates short terms plans on all business department (Lavia López

and Hiebl, 2014).

Controlling:

5

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Management accounting is useful for the control procedure because it draws up

performance reports which compare the actual to budgeted revenue for each responsibility

center. It helps the control function giving immediate activities measures and recognizing

problems (Management Accounting – Meaning, Advantages & Functions, 2018). Managers are

warned about those specific actions which are not according to the plan as management

accounting.

Organizing:

It is identifying components of organizational structure more relevant and important for

proper functioning of the management accounting system which enables the preparation of

internal reporting system for this structure and suggest more appropriate organizational structure

of the Unilever. The organizational structure is handling with authority, accountability and

expertise to ensure real performance of firm (Maas, Schaltegger and Crutzen, 2016). For that,

managerial accounting is designing and applying accounting system to better define and modify

these connections.

LO 2

Prepare income statement using both absorption and marginal costing

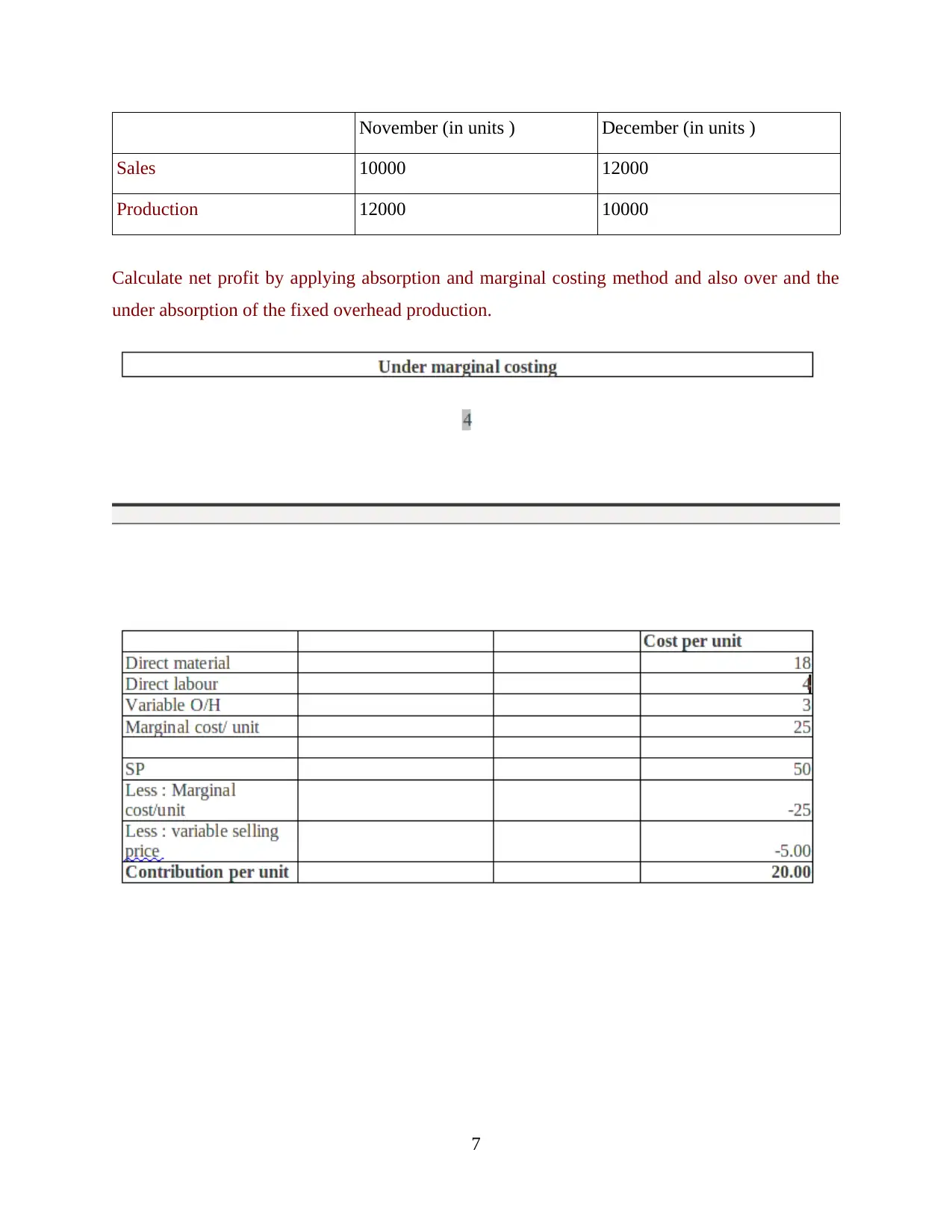

In the given scenarios, the following figures are been stated as follows-

Per unit- (£)

Sales price: 50

Direct cost of material: 18

Direct wages: 4

Variable overhead production: 3

In addition to this company incurs fixed overheads' production for each month amounting to-

Fixed overhead production: 99000

Fixed overhead in terms of selling: 14000

Fixed overhead relating to administration: 26000

The variable overheads selling was 10% of the volume of sales. Furthermore, an entity normally

produce 11000 units of the per month production and the value of production and the sales for

the month of November and December equated as follows-

6

performance reports which compare the actual to budgeted revenue for each responsibility

center. It helps the control function giving immediate activities measures and recognizing

problems (Management Accounting – Meaning, Advantages & Functions, 2018). Managers are

warned about those specific actions which are not according to the plan as management

accounting.

Organizing:

It is identifying components of organizational structure more relevant and important for

proper functioning of the management accounting system which enables the preparation of

internal reporting system for this structure and suggest more appropriate organizational structure

of the Unilever. The organizational structure is handling with authority, accountability and

expertise to ensure real performance of firm (Maas, Schaltegger and Crutzen, 2016). For that,

managerial accounting is designing and applying accounting system to better define and modify

these connections.

LO 2

Prepare income statement using both absorption and marginal costing

In the given scenarios, the following figures are been stated as follows-

Per unit- (£)

Sales price: 50

Direct cost of material: 18

Direct wages: 4

Variable overhead production: 3

In addition to this company incurs fixed overheads' production for each month amounting to-

Fixed overhead production: 99000

Fixed overhead in terms of selling: 14000

Fixed overhead relating to administration: 26000

The variable overheads selling was 10% of the volume of sales. Furthermore, an entity normally

produce 11000 units of the per month production and the value of production and the sales for

the month of November and December equated as follows-

6

November (in units ) December (in units )

Sales 10000 12000

Production 12000 10000

Calculate net profit by applying absorption and marginal costing method and also over and the

under absorption of the fixed overhead production.

7

Sales 10000 12000

Production 12000 10000

Calculate net profit by applying absorption and marginal costing method and also over and the

under absorption of the fixed overhead production.

7

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

8

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

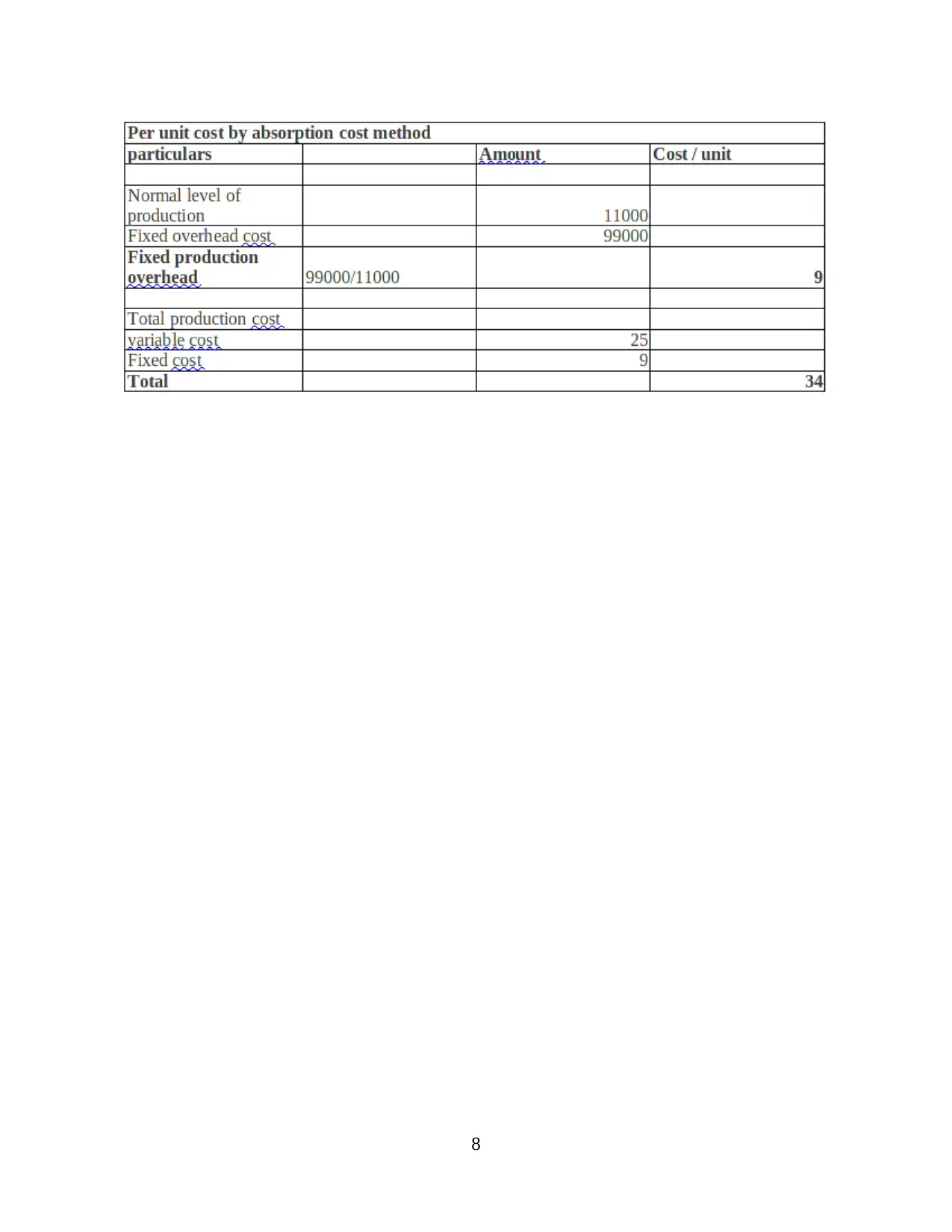

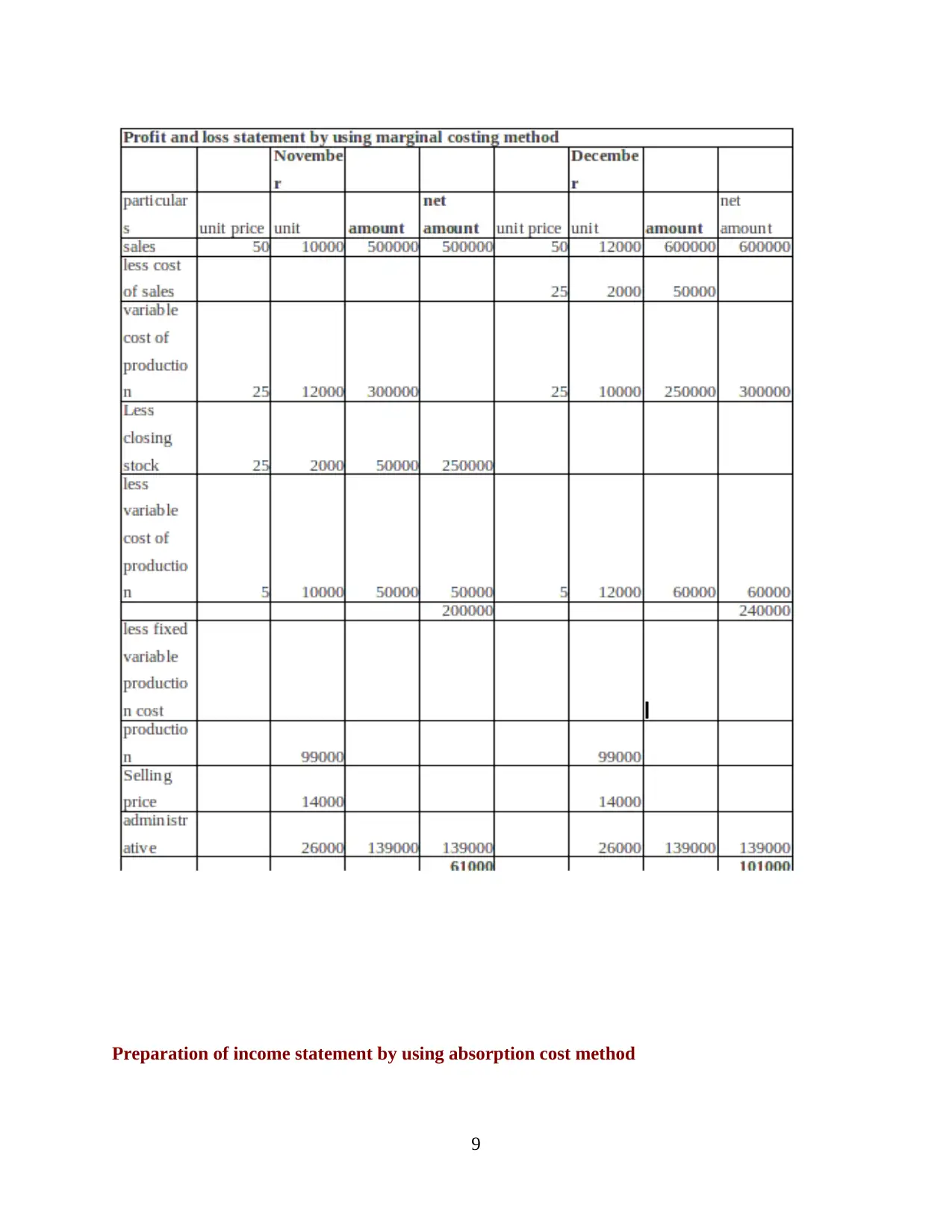

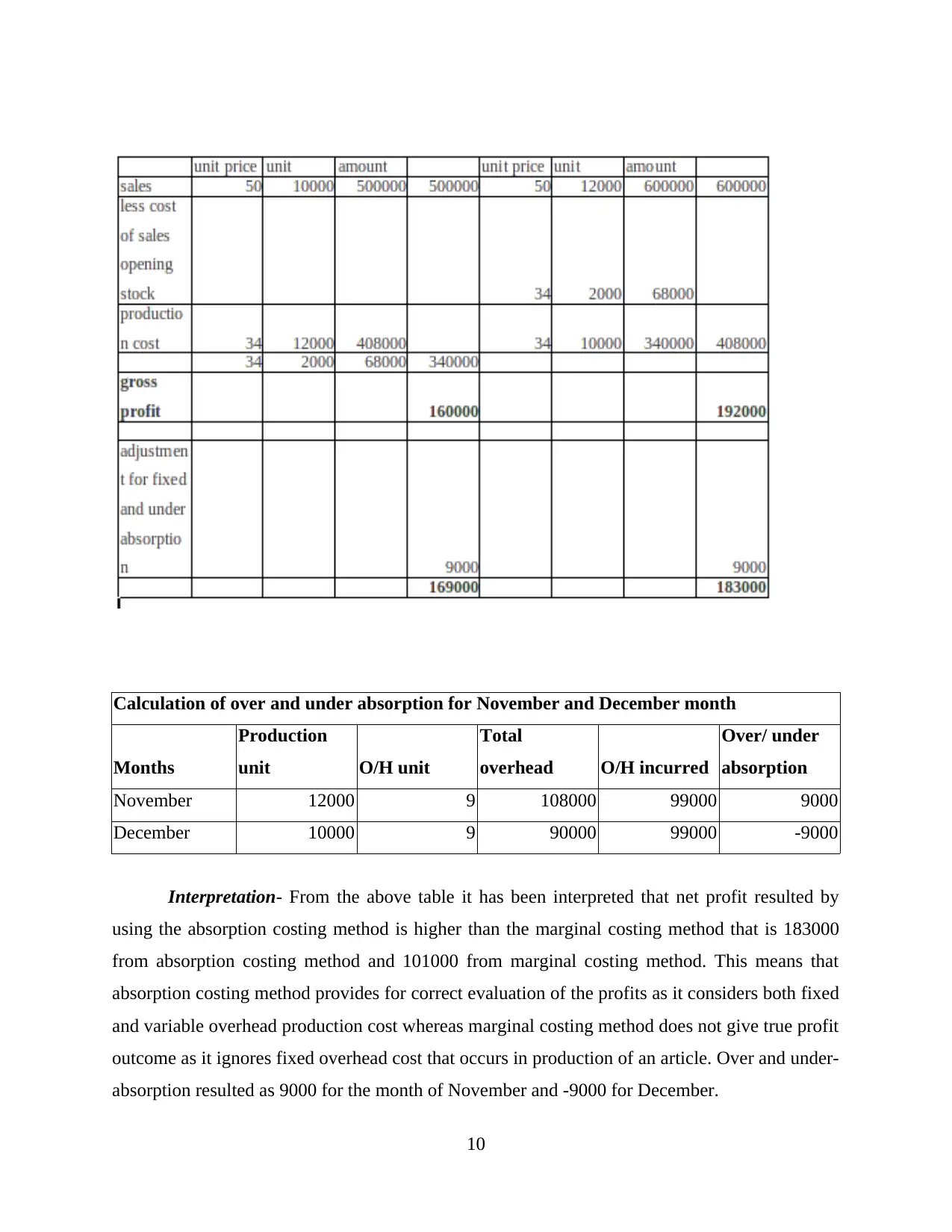

Preparation of income statement by using absorption cost method

9

9

Calculation of over and under absorption for November and December month

Months

Production

unit O/H unit

Total

overhead O/H incurred

Over/ under

absorption

November 12000 9 108000 99000 9000

December 10000 9 90000 99000 -9000

Interpretation- From the above table it has been interpreted that net profit resulted by

using the absorption costing method is higher than the marginal costing method that is 183000

from absorption costing method and 101000 from marginal costing method. This means that

absorption costing method provides for correct evaluation of the profits as it considers both fixed

and variable overhead production cost whereas marginal costing method does not give true profit

outcome as it ignores fixed overhead cost that occurs in production of an article. Over and under-

absorption resulted as 9000 for the month of November and -9000 for December.

10

Months

Production

unit O/H unit

Total

overhead O/H incurred

Over/ under

absorption

November 12000 9 108000 99000 9000

December 10000 9 90000 99000 -9000

Interpretation- From the above table it has been interpreted that net profit resulted by

using the absorption costing method is higher than the marginal costing method that is 183000

from absorption costing method and 101000 from marginal costing method. This means that

absorption costing method provides for correct evaluation of the profits as it considers both fixed

and variable overhead production cost whereas marginal costing method does not give true profit

outcome as it ignores fixed overhead cost that occurs in production of an article. Over and under-

absorption resulted as 9000 for the month of November and -9000 for December.

10

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 22

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.