Corporate Finance Project: WACC and Valuation of Bega Cheese

VerifiedAdded on 2023/06/05

|4

|674

|351

Project

AI Summary

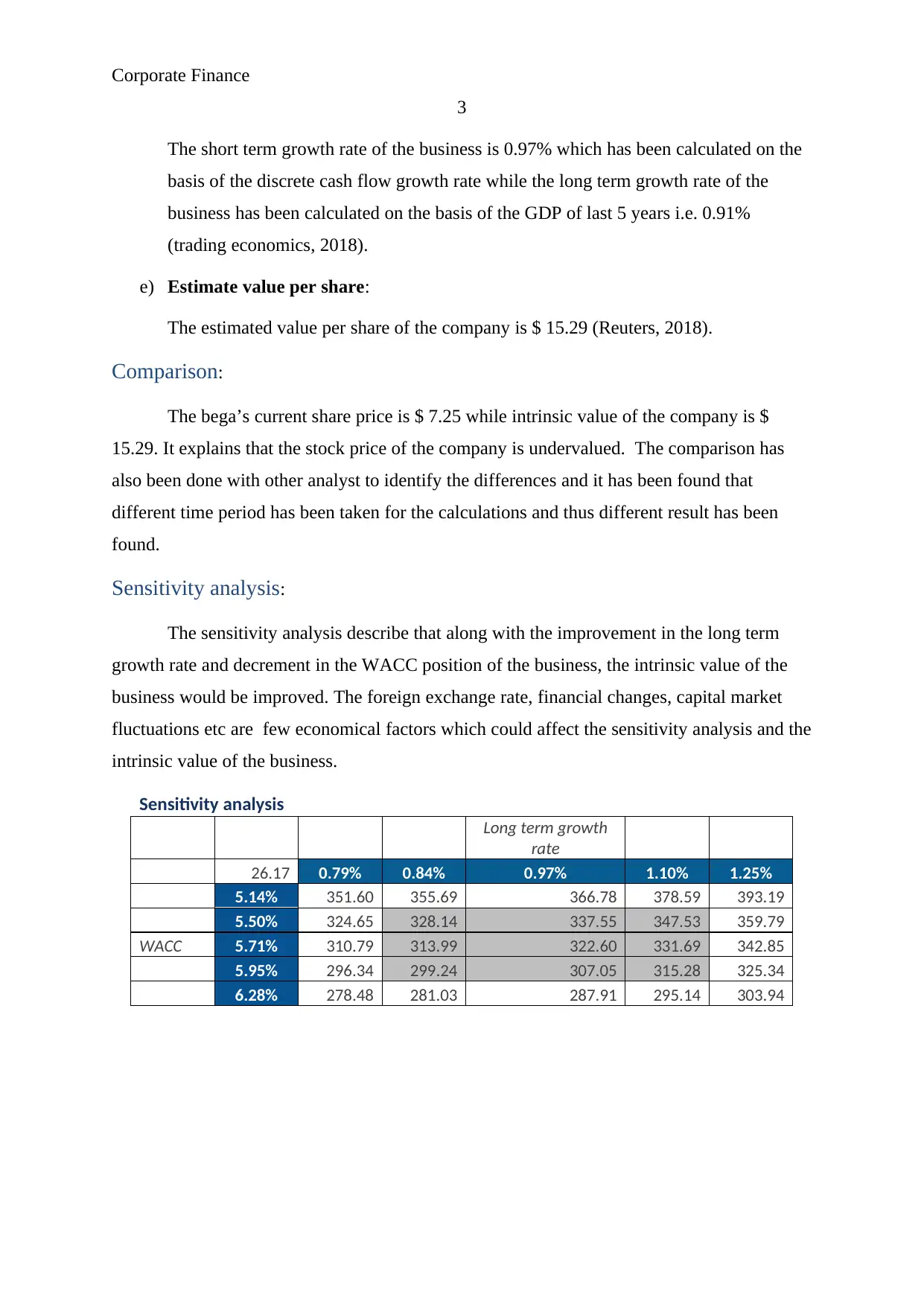

This corporate finance project report focuses on the valuation of Bega Cheese, calculating its Weighted Average Cost of Capital (WACC) and intrinsic value. The WACC is determined to be 5.71%, with a cost of equity of 7.29% and a cost of debt of 2.45%. The project utilizes a three-year period (2015-2018) to assess the intrinsic value, highlighting 2018 as a high-growth year. Pro forma financial statements reveal an average free cash flow of $12,860.47, with a terminal value of $2,604,450.08. Short-term and long-term growth rates are estimated at 0.97% and 0.91%, respectively, leading to an estimated value per share of $15.29, which suggests the company is undervalued compared to its current share price of $7.25. Sensitivity analysis indicates that improvements in long-term growth and reductions in WACC would enhance the intrinsic value. The analysis also acknowledges the impact of economic factors like foreign exchange rates and capital market fluctuations. The report concludes by referencing data from Trading Economics, Morningstar, Reuters and Market risk premia.

1 out of 4

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.