Vodafone PLC: A Financial Analysis of Gearing and Dividend Policies

VerifiedAdded on 2019/12/03

|18

|3073

|141

Report

AI Summary

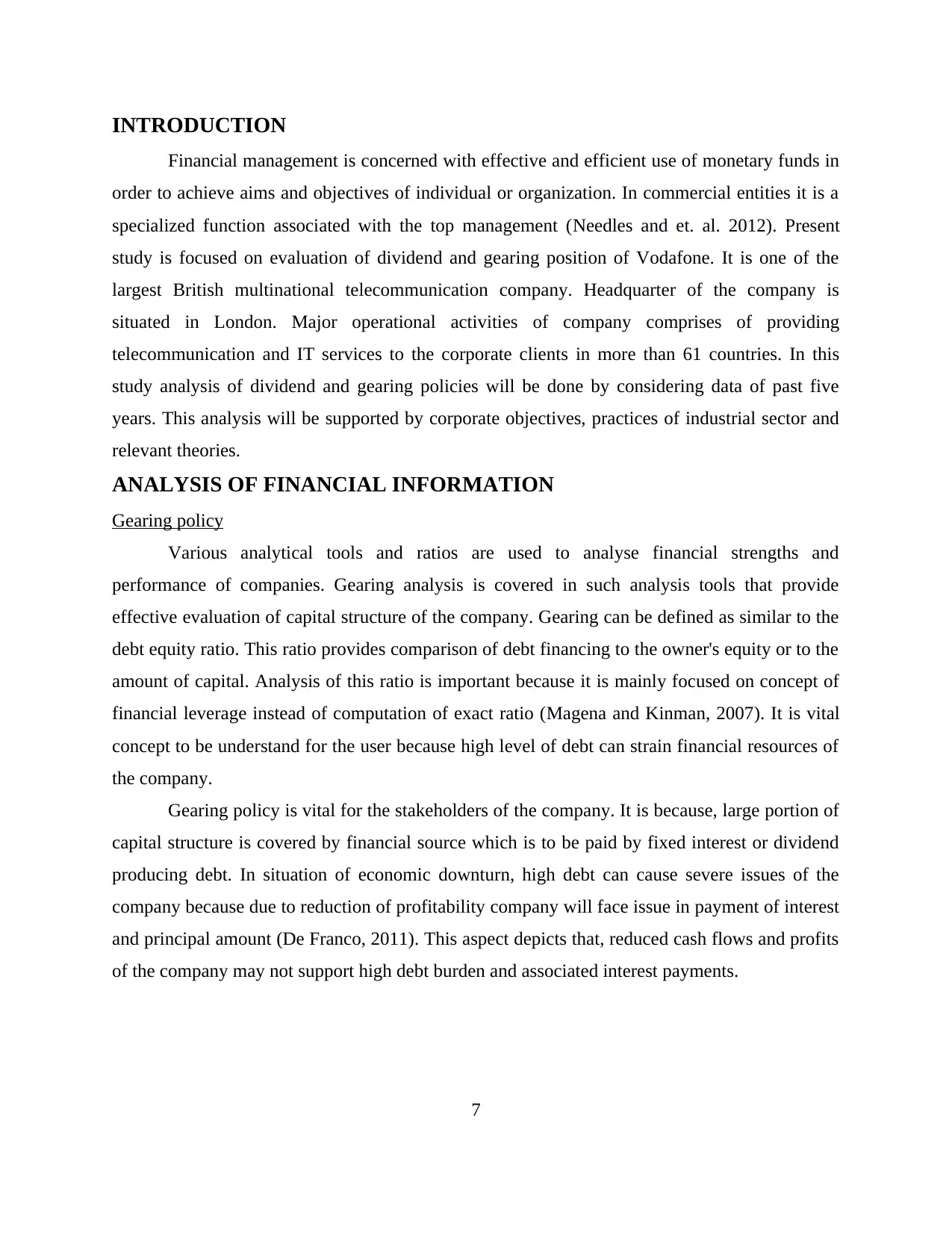

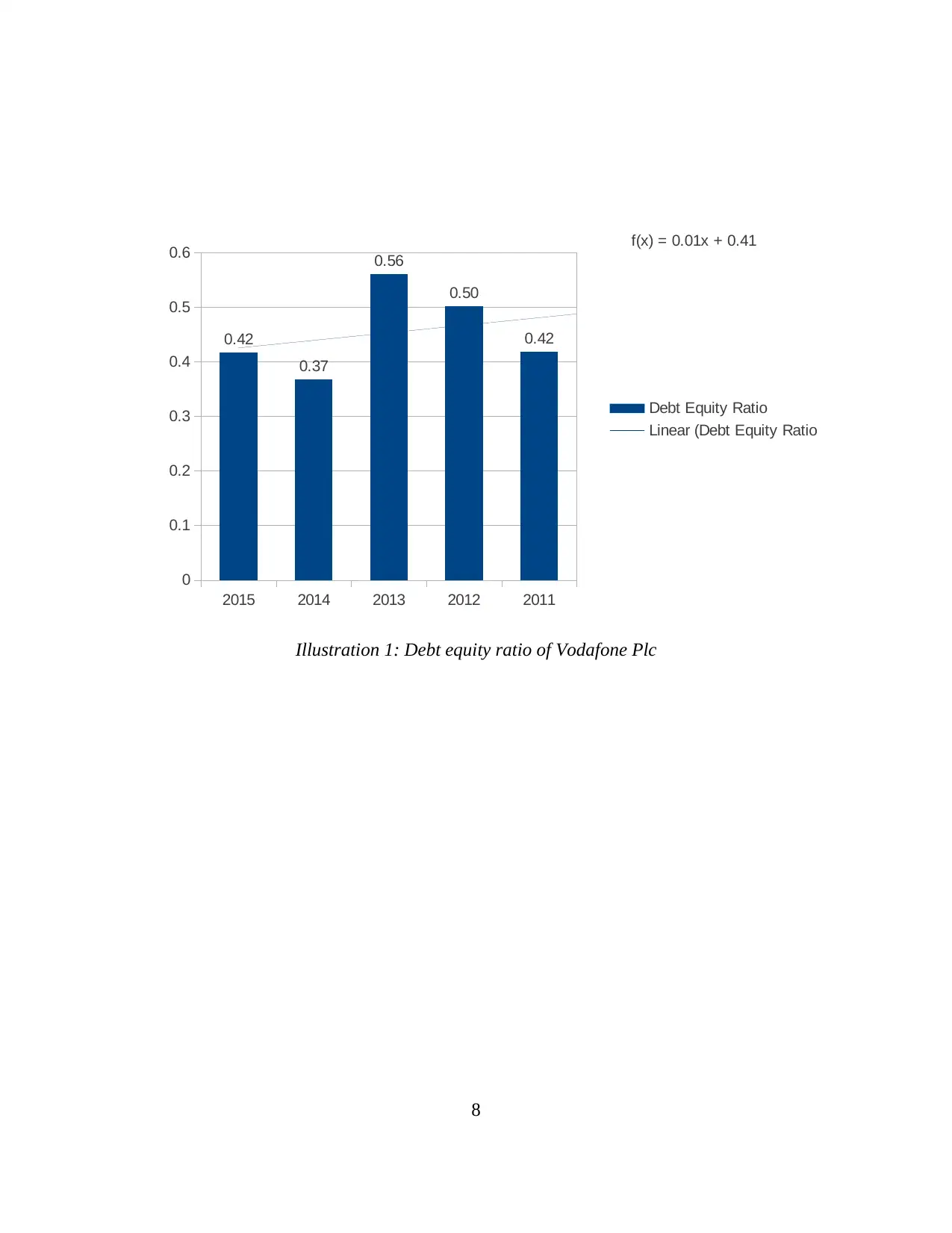

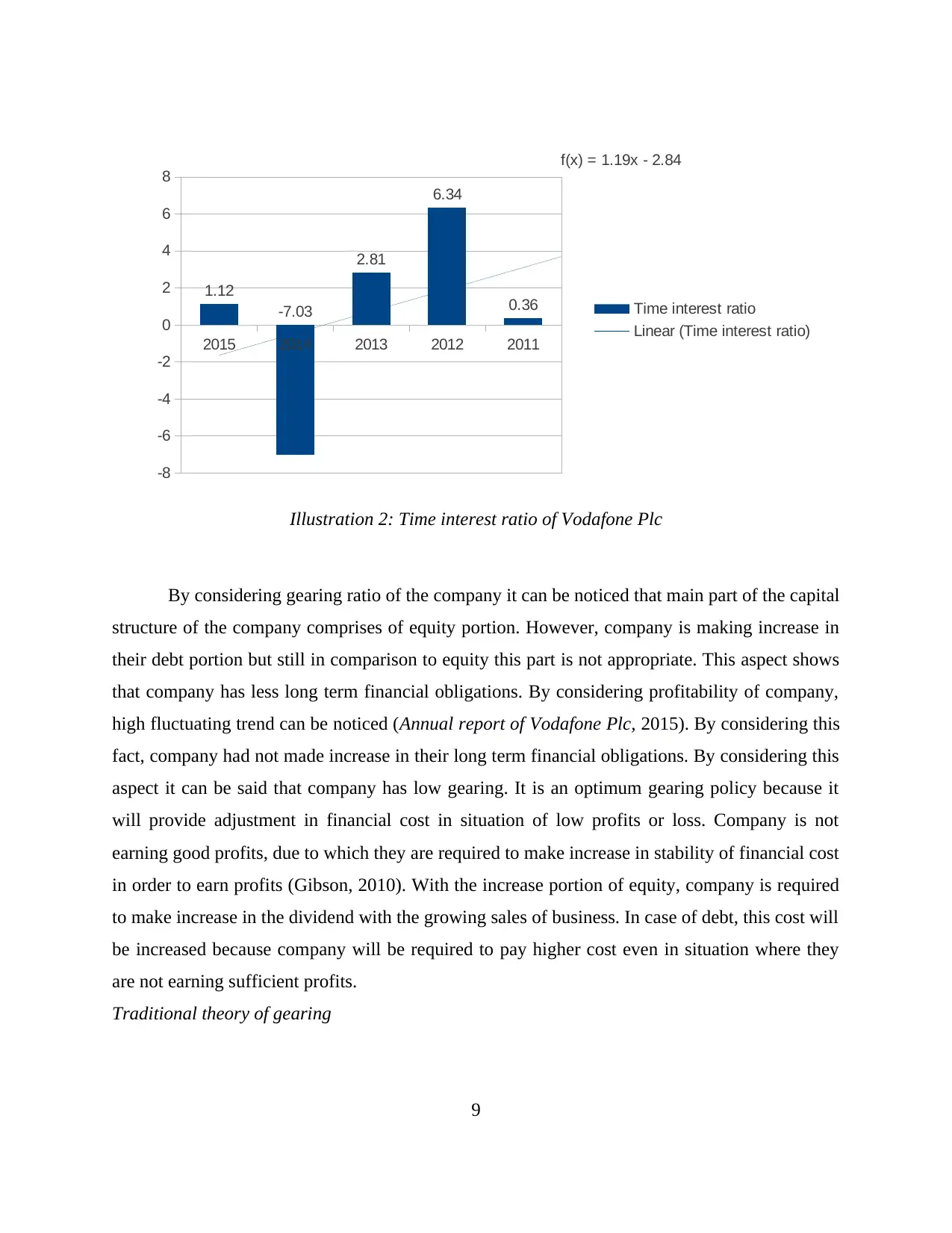

This report provides a financial analysis of Vodafone PLC, focusing on its gearing and dividend policies. The study examines the company's capital structure, utilizing gearing ratios to assess the proportion of debt and equity. It delves into Vodafone's dividend policy, evaluating payout ratios and their impact on shareholder returns. The analysis incorporates relevant financial theories, including traditional gearing theory, Modigliani and Miller's theories, and the static trade-off theory, to provide a comprehensive understanding of Vodafone's financial strategies. The report highlights fluctuations in profitability and their effect on dividend stability, ultimately recommending improvements in operational activities and dividend policies to enhance shareholder value and financial stability. The analysis is supported by data from annual reports and industry insights, offering practical recommendations for Vodafone PLC's financial management.

1 out of 18

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.