Corporate Accounting: Wesfarmers Ltd. Financial Statement Analysis

VerifiedAdded on 2024/05/29

|14

|3296

|333

Report

AI Summary

This report provides a detailed analysis of Wesfarmers Ltd., an ASX-listed company, focusing on its financial statements. It examines the company's cash flow statement, breaking down cash flows from operating, investing, and financing activities, and provides a comparative analysis over three years. The report also analyzes Wesfarmers Ltd.'s other comprehensive income statement, explaining the various items reported, such as exchange differences and cash flow hedges, and why these are not included in the profit and loss statement. Furthermore, the report delves into the company's corporate income tax, discussing tax expenses, deferred tax assets and liabilities, and the relationship between income tax payable and income tax expense. The analysis utilizes information from Wesfarmers Ltd.'s financial statements to provide a comprehensive overview of the company's financial performance and accounting practices.

Corporate Accounting

1

1

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of Contents

Introduction......................................................................................................................................3

1. CASH FLOWS STATEMENT...................................................................................................3

2. OTHER COMPREHENSIVE INCOME STATEMENT............................................................5

3. ACCOUNTING FOR CROPORATE INCOME TAX...............................................................8

Conclusion.....................................................................................................................................11

References......................................................................................................................................12

2

Introduction......................................................................................................................................3

1. CASH FLOWS STATEMENT...................................................................................................3

2. OTHER COMPREHENSIVE INCOME STATEMENT............................................................5

3. ACCOUNTING FOR CROPORATE INCOME TAX...............................................................8

Conclusion.....................................................................................................................................11

References......................................................................................................................................12

2

Introduction

Evaluation of financial statements of a firm helps in analyzing its performance, assessing its

accounting treatments, evaluating its taxes paid, etc. This report consists of a discussion of

Wesfarmers Ltd., an ASX listed company with largest turnovers in the country of Australia

(Wesfarmers.com.au, 2018). In this report, the cash flow statement of the company is going to be

analyzed along with analyzing Wesfarmers Ltd.’s corporate taxes and other comprehensive

income statement.

1. CASH FLOWS STATEMENT

(i) List of each item in cash flows statement and the understanding of each item

As stated by Reid & Myddelton (2017), a cash flow statement of a company determines the net

cash position of a company through categorizing the cash inflows and outflows as per their

respective activities. The following are the items contained in the cash flows statement of

Wesfarmers Ltd. -

Cash flows from operating activities - Gordon et al. (2017) stated the net changes taking

place in a company’s cash due to operating such as cash received from sales, etc. is called

cash flow from operating activities. The cash flows of Wesfarmers Ltd. from operating

activities changed from $3365 million in 2016 to $4226 million in 2017

(Wesfarmers.com.au, 2018). This change has possibly taken place due to the increase in

the receipts from customers, reduction in borrowing costs, increase in payment to

employees and suppliers, net movements in financing loans and advance, decrease in

dividends and interest received and reduction in income taxes paid.

Cash flows from investing activities - Warren and Jones (2018) stated the net changes

taking place in a company’s cash due to investing such as investment in fixed assets is

called cash flow from investing. The cash flows of Wesfarmers Ltd. from investing

activities changed from $2132 million in 2016 decreased to $53 million in 2017

(Wesfarmers.com.au, 2018). These changes have taken place due to the reduction of the

company’s payment on fixed assets, increase in sales of fixed assets, increase in sales of

3

Evaluation of financial statements of a firm helps in analyzing its performance, assessing its

accounting treatments, evaluating its taxes paid, etc. This report consists of a discussion of

Wesfarmers Ltd., an ASX listed company with largest turnovers in the country of Australia

(Wesfarmers.com.au, 2018). In this report, the cash flow statement of the company is going to be

analyzed along with analyzing Wesfarmers Ltd.’s corporate taxes and other comprehensive

income statement.

1. CASH FLOWS STATEMENT

(i) List of each item in cash flows statement and the understanding of each item

As stated by Reid & Myddelton (2017), a cash flow statement of a company determines the net

cash position of a company through categorizing the cash inflows and outflows as per their

respective activities. The following are the items contained in the cash flows statement of

Wesfarmers Ltd. -

Cash flows from operating activities - Gordon et al. (2017) stated the net changes taking

place in a company’s cash due to operating such as cash received from sales, etc. is called

cash flow from operating activities. The cash flows of Wesfarmers Ltd. from operating

activities changed from $3365 million in 2016 to $4226 million in 2017

(Wesfarmers.com.au, 2018). This change has possibly taken place due to the increase in

the receipts from customers, reduction in borrowing costs, increase in payment to

employees and suppliers, net movements in financing loans and advance, decrease in

dividends and interest received and reduction in income taxes paid.

Cash flows from investing activities - Warren and Jones (2018) stated the net changes

taking place in a company’s cash due to investing such as investment in fixed assets is

called cash flow from investing. The cash flows of Wesfarmers Ltd. from investing

activities changed from $2132 million in 2016 decreased to $53 million in 2017

(Wesfarmers.com.au, 2018). These changes have taken place due to the reduction of the

company’s payment on fixed assets, increase in sales of fixed assets, increase in sales of

3

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

associates and businesses, decrease in acquisition of subsidiaries and increase in net

redemption.

Cash flows from financing activities - As stated by Stevanovic et al. (2017), the net

changes taking place in a company’s cash due to financing such as purchase of equity

capital is called cash flow from financing activities. The cash outflows of Wesfarmers

Ltd. from financing activities have further increased from $1333million in 2016 to

$3771million in 2017 (Wesfarmers.com.au, 2018). This change has taken place due to the

decreased in proceed from borrowings, increase in repayment of debts and decreased in

payment of equity dividends.

(ii) Comparative analysis of your company’s three broad categories of cash flows and

comparative evaluation for three years

The comparative analysis of the company Wesfarmers Ltd.’s three main categories of cash flows

during the past three financial years has been done in the table below -

Particulars 2017 (in $) 2016 (in $) 2015 (in $)

Net cash balance as per operating activities 4226 million 3365 million 3791 million

Net cash balance as per investing activities - 53 million - 2132

million

- 1898

million

Net cash balance as per financing activities - 3771

million

- 1333

million

- 3249

million

(Source: Wesfarmers.com.au, 2018)

As shown in the table above, it can be noticed that the cash flows of the company from operating

activities show a decrease from $3791 million in 2015 to $3365 million to 2016, followed by an

increase again in 2017 to $4226 million (Wesfarmers.com.au, 2018). This indicates that the cash

position of the company has improved from the year 2015 to the year 2017. The comparison of

the cash flows of Wesfarmers Ltd. from investing activities show a net outflow of $1898 million

in 2015, which increased to $2132 million in 2016 and again decreased to $53 million in 2017

(Wesfarmers.com.au, 2018). An improvement can also be noticed in Wesfarmers Ltd.’s cash

flows from investing activities as the net outflow of cash from the company has decreased during

the three past years. However, the cash outflows of the company Wesfarmers Ltd. show an

4

redemption.

Cash flows from financing activities - As stated by Stevanovic et al. (2017), the net

changes taking place in a company’s cash due to financing such as purchase of equity

capital is called cash flow from financing activities. The cash outflows of Wesfarmers

Ltd. from financing activities have further increased from $1333million in 2016 to

$3771million in 2017 (Wesfarmers.com.au, 2018). This change has taken place due to the

decreased in proceed from borrowings, increase in repayment of debts and decreased in

payment of equity dividends.

(ii) Comparative analysis of your company’s three broad categories of cash flows and

comparative evaluation for three years

The comparative analysis of the company Wesfarmers Ltd.’s three main categories of cash flows

during the past three financial years has been done in the table below -

Particulars 2017 (in $) 2016 (in $) 2015 (in $)

Net cash balance as per operating activities 4226 million 3365 million 3791 million

Net cash balance as per investing activities - 53 million - 2132

million

- 1898

million

Net cash balance as per financing activities - 3771

million

- 1333

million

- 3249

million

(Source: Wesfarmers.com.au, 2018)

As shown in the table above, it can be noticed that the cash flows of the company from operating

activities show a decrease from $3791 million in 2015 to $3365 million to 2016, followed by an

increase again in 2017 to $4226 million (Wesfarmers.com.au, 2018). This indicates that the cash

position of the company has improved from the year 2015 to the year 2017. The comparison of

the cash flows of Wesfarmers Ltd. from investing activities show a net outflow of $1898 million

in 2015, which increased to $2132 million in 2016 and again decreased to $53 million in 2017

(Wesfarmers.com.au, 2018). An improvement can also be noticed in Wesfarmers Ltd.’s cash

flows from investing activities as the net outflow of cash from the company has decreased during

the three past years. However, the cash outflows of the company Wesfarmers Ltd. show an

4

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

increase over the three past years from $3249 million in 2015 to $3771 million in 2017, which is

not a good sign for the cash position of the company (Wesfarmers.com.au, 2018).

5

not a good sign for the cash position of the company (Wesfarmers.com.au, 2018).

5

2. OTHER COMPREHENSIVE INCOME STATEMENT

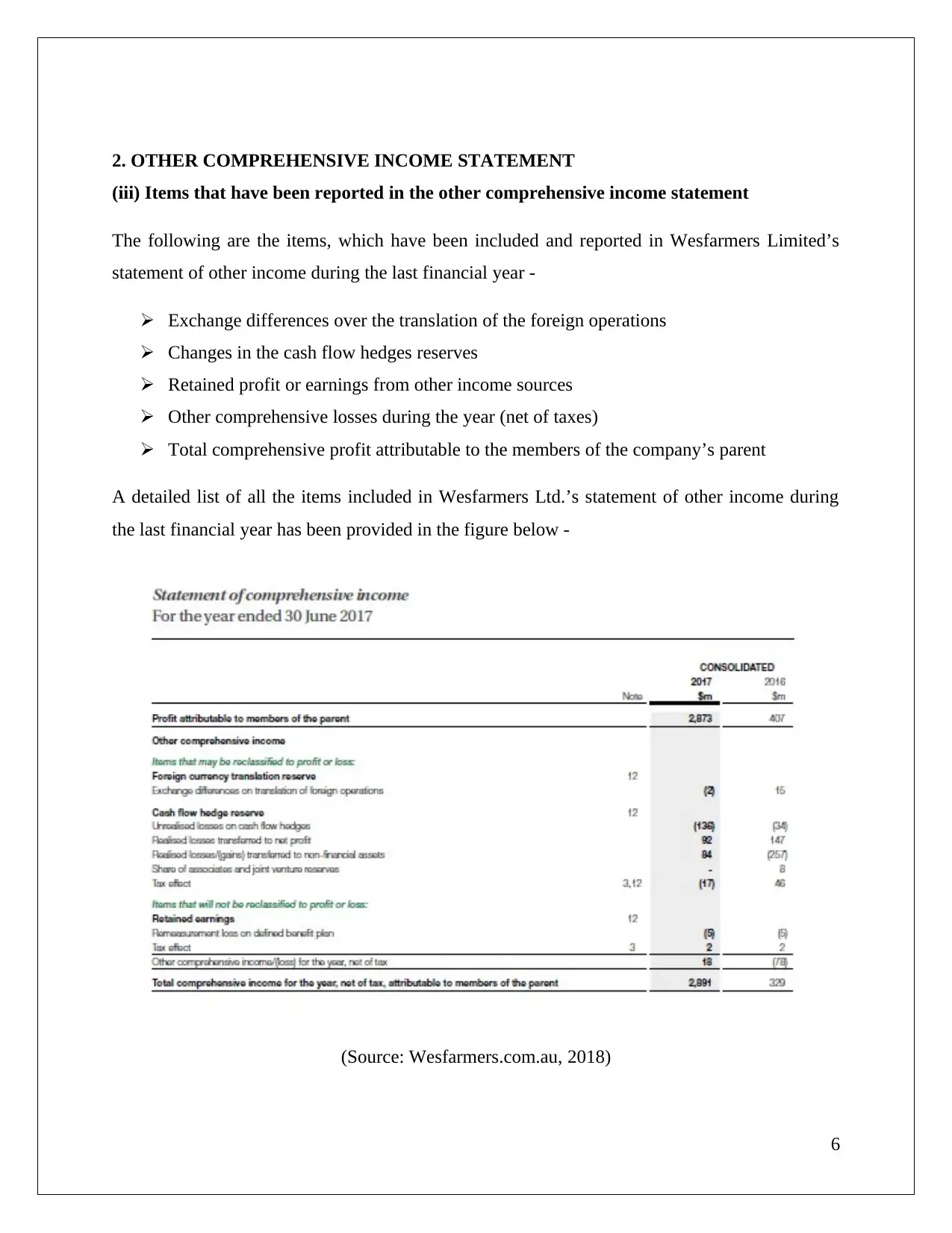

(iii) Items that have been reported in the other comprehensive income statement

The following are the items, which have been included and reported in Wesfarmers Limited’s

statement of other income during the last financial year -

Exchange differences over the translation of the foreign operations

Changes in the cash flow hedges reserves

Retained profit or earnings from other income sources

Other comprehensive losses during the year (net of taxes)

Total comprehensive profit attributable to the members of the company’s parent

A detailed list of all the items included in Wesfarmers Ltd.’s statement of other income during

the last financial year has been provided in the figure below -

(Source: Wesfarmers.com.au, 2018)

6

(iii) Items that have been reported in the other comprehensive income statement

The following are the items, which have been included and reported in Wesfarmers Limited’s

statement of other income during the last financial year -

Exchange differences over the translation of the foreign operations

Changes in the cash flow hedges reserves

Retained profit or earnings from other income sources

Other comprehensive losses during the year (net of taxes)

Total comprehensive profit attributable to the members of the company’s parent

A detailed list of all the items included in Wesfarmers Ltd.’s statement of other income during

the last financial year has been provided in the figure below -

(Source: Wesfarmers.com.au, 2018)

6

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

(iv) Understanding of each item reported in the other comprehensive income statement

The following points can be helping in developing an understanding of all the items included in

Wesfarmers Ltd.’s statement of other income during the last financial year -

The difference that results from translation of a given volume of units of a certain

currency to another currency of dissimilar exchange rates is the exchange differences

over the translation of the foreign operations. A change can be noticed in Wesfarmers

Ltd.’s foreign currency translation reserve from $15 million in 2016 to -$2 million in

2017 (Wesfarmers.com.au, 2018).

Cash flow hedges are used in companies for the elimination or minimization of the

exposure, which arises from the changes in cash flows of any financial liability or asset

because of various risks. It can be noticed from Wesfarmers Ltd.’s other income

statement that the company has a reserve for cash flow hedges, which contains several

items. Various changes can be noticed in the items under the cash flow hedge reserves of

the company Wesfarmers Ltd. from the year 2016 to the year 2017.

Another item under Wesfarmers Ltd.’s other income statement is retained earnings.

Retained earnings refer to the earnings that are retained in a company after paying off

dividends to shareholders. Changes can be noticed in the retained profits of Wesfarmers

Ltd. as well, which will not be reclassified to profit and loss.

The last item listed under the Wesfarmers Ltd.’s other income statement is other

comprehensive income or loss for the year net of taxes. It can be noticed that the

company faced a net loss of $78 million during 2016, which increased to $18 million

during the year 2017 (Wesfarmers.com.au, 2018).

(v) Why these items have not been reported in Profit and Loss Statement / Income

statement

The OCI, which stands for the other income statement, refers to a specific type of financial

statement prepared in a company for recording the income and expenses of a company for other

operations except for the normal course of operations. The items recorded in the OCI consist of

transactions that have an effect over the balance amount of a firm (Nejad & Ahmad, 2017).

However, such items are not recorded in the profit and loss account of an organization but

7

The following points can be helping in developing an understanding of all the items included in

Wesfarmers Ltd.’s statement of other income during the last financial year -

The difference that results from translation of a given volume of units of a certain

currency to another currency of dissimilar exchange rates is the exchange differences

over the translation of the foreign operations. A change can be noticed in Wesfarmers

Ltd.’s foreign currency translation reserve from $15 million in 2016 to -$2 million in

2017 (Wesfarmers.com.au, 2018).

Cash flow hedges are used in companies for the elimination or minimization of the

exposure, which arises from the changes in cash flows of any financial liability or asset

because of various risks. It can be noticed from Wesfarmers Ltd.’s other income

statement that the company has a reserve for cash flow hedges, which contains several

items. Various changes can be noticed in the items under the cash flow hedge reserves of

the company Wesfarmers Ltd. from the year 2016 to the year 2017.

Another item under Wesfarmers Ltd.’s other income statement is retained earnings.

Retained earnings refer to the earnings that are retained in a company after paying off

dividends to shareholders. Changes can be noticed in the retained profits of Wesfarmers

Ltd. as well, which will not be reclassified to profit and loss.

The last item listed under the Wesfarmers Ltd.’s other income statement is other

comprehensive income or loss for the year net of taxes. It can be noticed that the

company faced a net loss of $78 million during 2016, which increased to $18 million

during the year 2017 (Wesfarmers.com.au, 2018).

(v) Why these items have not been reported in Profit and Loss Statement / Income

statement

The OCI, which stands for the other income statement, refers to a specific type of financial

statement prepared in a company for recording the income and expenses of a company for other

operations except for the normal course of operations. The items recorded in the OCI consist of

transactions that have an effect over the balance amount of a firm (Nejad & Ahmad, 2017).

However, such items are not recorded in the profit and loss account of an organization but

7

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

entered into the OCI that is prepared by it. The list of the items that are recorded in the other

income statement of Wesfarmers Ltd. such as cash flow hedges reserves, etc. do not have an

impact on the net income of the company. Such items also do not have an impact on the retained

earnings of the company. Hence, as there are no impacts on the retained earnings and net profits

of the company, the company Wesfarmers Ltd. does not record them in its profit and loss or

income statement.

8

income statement of Wesfarmers Ltd. such as cash flow hedges reserves, etc. do not have an

impact on the net income of the company. Such items also do not have an impact on the retained

earnings of the company. Hence, as there are no impacts on the retained earnings and net profits

of the company, the company Wesfarmers Ltd. does not record them in its profit and loss or

income statement.

8

3. ACCOUNTING FOR CROPORATE INCOME TAX

(vi) Firm’s tax expense in its latest financial statements

The tax expenses that a company pays to the government as a part of its net income is recorded

and presented in the profit and loss statement of a company (Lee et al., 2017). The tax expenses

of the company Wesfarmers Ltd. is also recorded in the company’s financial statements. The

analysis of the income statement of the company Wesfarmers Ltd. shows that the tax expense

made by the company Wesfarmers Ltd. amounted to $1266 million during the last financial year

2016 (Wesfarmers.com.au, 2018).

(vii) Is this figure the same as the company tax rate times your firm’s accounting income?

Explain why this is, or is not, the case for your firm

Evaluation of the financial accounts of the company Wesfarmers Ltd. shows that the figure of the

tax expense of the company is same as the company’s tax rate times of its total accounting profit

or income. The tax rate payable to Australian Government is usually 30% (Burkhauser, Hahn &

Wilkins, 2015). As per the accounting treatment of taxes made in Wesfarmers Ltd., it can be

identified that the effective rate of taxes paid by the company for its global operations is 30.6%

(Wesfarmers.com.au, 2018). The multiplication of this rate with the net income of the company

shows that the figure is same as the company’s tax rate times of its total accounting income.

(viii) Comment on deferred tax assets / liabilities that are reported in the balance sheet

articulating the possible reasons why they have been recorded

According to Wang, Butterfield & Campbell (2016), the deferred tax assets of a company can be

referred to as the assets, which can be held in an organization for minimizing its taxable income.

On the other hand, the deferred tax liabilities of a company can be referred to as the liabilities,

which can be mentioned in the balance sheet of an organization for increasing its taxable income

(Mullinova & Simonyants, 2016). Evaluation of the financial accounts of the company

Wesfarmers Ltd. shows that the balance sheet of the company consists of deferred tax assets. The

company had a total amount of $1042 million deferred tax assets during the year 2016, which

can be noticed to be decreasing to $971 million during the year 2016 (Wesfarmers.com.au,

2018). However, the deferred tax liabilities of the company are nil. The possible reasons for

9

(vi) Firm’s tax expense in its latest financial statements

The tax expenses that a company pays to the government as a part of its net income is recorded

and presented in the profit and loss statement of a company (Lee et al., 2017). The tax expenses

of the company Wesfarmers Ltd. is also recorded in the company’s financial statements. The

analysis of the income statement of the company Wesfarmers Ltd. shows that the tax expense

made by the company Wesfarmers Ltd. amounted to $1266 million during the last financial year

2016 (Wesfarmers.com.au, 2018).

(vii) Is this figure the same as the company tax rate times your firm’s accounting income?

Explain why this is, or is not, the case for your firm

Evaluation of the financial accounts of the company Wesfarmers Ltd. shows that the figure of the

tax expense of the company is same as the company’s tax rate times of its total accounting profit

or income. The tax rate payable to Australian Government is usually 30% (Burkhauser, Hahn &

Wilkins, 2015). As per the accounting treatment of taxes made in Wesfarmers Ltd., it can be

identified that the effective rate of taxes paid by the company for its global operations is 30.6%

(Wesfarmers.com.au, 2018). The multiplication of this rate with the net income of the company

shows that the figure is same as the company’s tax rate times of its total accounting income.

(viii) Comment on deferred tax assets / liabilities that are reported in the balance sheet

articulating the possible reasons why they have been recorded

According to Wang, Butterfield & Campbell (2016), the deferred tax assets of a company can be

referred to as the assets, which can be held in an organization for minimizing its taxable income.

On the other hand, the deferred tax liabilities of a company can be referred to as the liabilities,

which can be mentioned in the balance sheet of an organization for increasing its taxable income

(Mullinova & Simonyants, 2016). Evaluation of the financial accounts of the company

Wesfarmers Ltd. shows that the balance sheet of the company consists of deferred tax assets. The

company had a total amount of $1042 million deferred tax assets during the year 2016, which

can be noticed to be decreasing to $971 million during the year 2016 (Wesfarmers.com.au,

2018). However, the deferred tax liabilities of the company are nil. The possible reasons for

9

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

which the company has recorded its deferred tax assets in its balance sheet is that the deferred

tax assets are the prepaid income of the company and helps in reducing its tax expenses.

(ix) Is there any current tax assets or income tax payable recorded by your company? Why

is the income tax payable not the same as income tax expense?

As stated by Morris (2017), a current tax asset refers to the prepaid taxes of a company. On the

other hand, a current tax liability, also known as income tax payable is the outstanding taxes of a

company, which it is liable to pay within a year (Balakrishnan Blouin & Guay, 2018). Evaluation

of the financial accounts of the company Wesfarmers Ltd. shows that there are no current tax

assets of the company. However, there is income tax payable by the company. The income tax

payable of Wesfarmers Ltd. amounted to $29 million during the financial year 2016, which can

be noticed to increase to $292 million during the year 2017 (Wesfarmers.com.au, 2018).

However, the income tax payable of the company is not the same as its income tax expense. The

income tax expense is the amount that is paid to the government as a part of the company’s net

income while the income tax payable is the amount that the company is still liable to pay to the

government within the period of one financial year (Gitman, Juchau & Flanagan, 2015). This is

reason for which Wesfarmers Ltd.’s income tax expense and income tax payable are not the

same.

(x) Is the income tax expense shown in the income statement same as the income tax paid

shown in the cash flow statement?

Evaluation of the financial accounts of the company Wesfarmers Ltd. shows that the figure of the

tax expense of the company shown in its income statement differs from the income tax paid

shown in its cash flow statement. According to Gao, Givoly & Laux (2015), the income

statement of a company contains the income tax expense attributable to a company from its net

income while the cash flow statement of a company records the amount that has been paid in

cash to the government as income tax during a specific period. Due to this reason, there can be

noticed a difference in the income tax paid of Wesfarmers Ltd. and the income tax expense that

has been recorded in its income statement.

10

tax assets are the prepaid income of the company and helps in reducing its tax expenses.

(ix) Is there any current tax assets or income tax payable recorded by your company? Why

is the income tax payable not the same as income tax expense?

As stated by Morris (2017), a current tax asset refers to the prepaid taxes of a company. On the

other hand, a current tax liability, also known as income tax payable is the outstanding taxes of a

company, which it is liable to pay within a year (Balakrishnan Blouin & Guay, 2018). Evaluation

of the financial accounts of the company Wesfarmers Ltd. shows that there are no current tax

assets of the company. However, there is income tax payable by the company. The income tax

payable of Wesfarmers Ltd. amounted to $29 million during the financial year 2016, which can

be noticed to increase to $292 million during the year 2017 (Wesfarmers.com.au, 2018).

However, the income tax payable of the company is not the same as its income tax expense. The

income tax expense is the amount that is paid to the government as a part of the company’s net

income while the income tax payable is the amount that the company is still liable to pay to the

government within the period of one financial year (Gitman, Juchau & Flanagan, 2015). This is

reason for which Wesfarmers Ltd.’s income tax expense and income tax payable are not the

same.

(x) Is the income tax expense shown in the income statement same as the income tax paid

shown in the cash flow statement?

Evaluation of the financial accounts of the company Wesfarmers Ltd. shows that the figure of the

tax expense of the company shown in its income statement differs from the income tax paid

shown in its cash flow statement. According to Gao, Givoly & Laux (2015), the income

statement of a company contains the income tax expense attributable to a company from its net

income while the cash flow statement of a company records the amount that has been paid in

cash to the government as income tax during a specific period. Due to this reason, there can be

noticed a difference in the income tax paid of Wesfarmers Ltd. and the income tax expense that

has been recorded in its income statement.

10

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

(xi) What do you find interesting, confusing, surprising or difficult to understand about the

treatment of tax in your firm’s financial statements?

After conducting an in-depth analysis of the financial accounts and statements of Wesfarmers

Ltd., it can be said that the most interesting factor in the treatment of taxes in the financial

statements of the company is the way in which the company has accounted for income tax has

been completely disclosed in the notes to financial accounts of the company. The notes to

financial statements of the company where the taxes of the company have been recorded indicate

the notes to financial statements, which contain the breakdown of the treatment of taxes. There is

tax transparency disclosures of the company specified in all the financial reports of Wesfarmers

Ltd., which has made it easier to interpret and understand the financial statements of the

company and understanding the treatment of taxes in the company.

11

treatment of tax in your firm’s financial statements?

After conducting an in-depth analysis of the financial accounts and statements of Wesfarmers

Ltd., it can be said that the most interesting factor in the treatment of taxes in the financial

statements of the company is the way in which the company has accounted for income tax has

been completely disclosed in the notes to financial accounts of the company. The notes to

financial statements of the company where the taxes of the company have been recorded indicate

the notes to financial statements, which contain the breakdown of the treatment of taxes. There is

tax transparency disclosures of the company specified in all the financial reports of Wesfarmers

Ltd., which has made it easier to interpret and understand the financial statements of the

company and understanding the treatment of taxes in the company.

11

Conclusion

Therefore, from the detailed analysis of the financial statements and corporate accounting details

of the company Wesfarmers Ltd., it can be determined that the company’s financial statements

have been prepared in a way such that it has been easy to interpret them. The analysis of the cash

flows statement of the company indicates that there has been changes in the company’s cash

flows from different activities while the analysis of its other comprehensive income statement

shows the different other sources such as cash flow hedges reserves from which the company has

earned sources. Lastly, the analysis of the company’s corporate taxes show that the treatment of

the taxes of the company has been done in an effective manner.

12

Therefore, from the detailed analysis of the financial statements and corporate accounting details

of the company Wesfarmers Ltd., it can be determined that the company’s financial statements

have been prepared in a way such that it has been easy to interpret them. The analysis of the cash

flows statement of the company indicates that there has been changes in the company’s cash

flows from different activities while the analysis of its other comprehensive income statement

shows the different other sources such as cash flow hedges reserves from which the company has

earned sources. Lastly, the analysis of the company’s corporate taxes show that the treatment of

the taxes of the company has been done in an effective manner.

12

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 14

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.