Machine Learning for Customer Retention in Banking

VerifiedAdded on 2023/04/07

|20

|5486

|199

AI Summary

This paper explores the role of consumer behavioral factors in influencing customer retention in the banking industry. It discusses the application of machine learning techniques to minimize customer churn and improve customer satisfaction. The study uses a descriptive research design and a questionnaire to gather data on customer retention in the banking industry. The findings highlight the importance of customer satisfaction and loyalty in long-term customer relationships.

Contribute Materials

Your contribution can guide someone’s learning journey. Share your

documents today.

0

Customer retention

Customer retention

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

Customer retention 1

Abstract

The customers have become more

interested in the service quality nowadays.

The service provided by the bank is not

highly distinguished which increases the

competition between the banks to maintain

and increase the quality of service. The

CRM is used to analyse competition

advantage by increasing customer

retention rate. This paper explains the role

of consumer behavioural factors in

influencing customer retention. The

application of machine learning techniques

has been explained. The machine learning

is enabling the fintech sector. It prevents

fraud, manages risk, improves chatbot

customer experience, network security and

more.

A descriptive research design is adapted to

fulfil the research objective; as it is

suitable for the study. A questionnaire is

intended to gather the data and find out the

most substantial aspect of customer

retention in the banking industry. The

secondary research is conducted to

implement the research. The structured

questionnaire is dispersed to the banking

customers based on the demographics like

gender, age, education, marital status,

occupation and income level.

Abstract

The customers have become more

interested in the service quality nowadays.

The service provided by the bank is not

highly distinguished which increases the

competition between the banks to maintain

and increase the quality of service. The

CRM is used to analyse competition

advantage by increasing customer

retention rate. This paper explains the role

of consumer behavioural factors in

influencing customer retention. The

application of machine learning techniques

has been explained. The machine learning

is enabling the fintech sector. It prevents

fraud, manages risk, improves chatbot

customer experience, network security and

more.

A descriptive research design is adapted to

fulfil the research objective; as it is

suitable for the study. A questionnaire is

intended to gather the data and find out the

most substantial aspect of customer

retention in the banking industry. The

secondary research is conducted to

implement the research. The structured

questionnaire is dispersed to the banking

customers based on the demographics like

gender, age, education, marital status,

occupation and income level.

Customer retention 2

Introduction

The role of the consumer behavioural

factors in influencing customer retention?

This question is chosen so that customer

churn can be minimized by using machine

learning techniques. Such techniques

enhance the retention of the customers in

banking. The main purpose is to study how

consumer behaviour influences the

customer retention.

The application of machine learning

techniques can minimise customer churn.

The customer churn is stated to the

condition when the existing customer stops

using services and buying products of an

organization. The churn is considered a

huge problem as it causes to a reduction in

the revenue of the organization. Acquiring

new customers can make up the lost

revenue. But the process of acquiring

customers is expensive and time-

consuming. The customer acquisition can

also put a dent to the overall income of the

company. The customer churn also has

some indirect effects as the customers

initiate a new relationship with the

competitors of the organization. Such

customers also take away the other loyal

customers with them. It has been

considered that the financial institution

will be losing 24% of the revenue in the

coming 4-5 years because of the customer

churn to new fintech companies. It is a key

business strategy to reduce customer churn

which can result in retaining customers in

a possible manner.

Related work

According to Agolla, Makara and

Monametsi, 2018, customer retention lead

to the actions and activities taken by the

organization to reduce the number of

customer defections. The aim of customer

retention is to help an organization in

retaining as many customers as possible.

The bank now days spend on the customer

acquisition as it is a quick way of

increasing revenue but customer retention

is faster and costs seven times less than the

customer acquisition (Agolla, Makara and

Monametsi, 2018). It is an effective way of

increasing revenue by selling to the

existing customers as the organization

does not have a need to attract customers

and guide.

As per Ennew Binks and Chiplin, 2015,

customer satisfaction keeps ahead of the

bank compared to the competitors. When

the customers are satisfied, it works as an

advantage to the bank. The customer

satisfaction promotes to customer

retention. The longer customers are

Introduction

The role of the consumer behavioural

factors in influencing customer retention?

This question is chosen so that customer

churn can be minimized by using machine

learning techniques. Such techniques

enhance the retention of the customers in

banking. The main purpose is to study how

consumer behaviour influences the

customer retention.

The application of machine learning

techniques can minimise customer churn.

The customer churn is stated to the

condition when the existing customer stops

using services and buying products of an

organization. The churn is considered a

huge problem as it causes to a reduction in

the revenue of the organization. Acquiring

new customers can make up the lost

revenue. But the process of acquiring

customers is expensive and time-

consuming. The customer acquisition can

also put a dent to the overall income of the

company. The customer churn also has

some indirect effects as the customers

initiate a new relationship with the

competitors of the organization. Such

customers also take away the other loyal

customers with them. It has been

considered that the financial institution

will be losing 24% of the revenue in the

coming 4-5 years because of the customer

churn to new fintech companies. It is a key

business strategy to reduce customer churn

which can result in retaining customers in

a possible manner.

Related work

According to Agolla, Makara and

Monametsi, 2018, customer retention lead

to the actions and activities taken by the

organization to reduce the number of

customer defections. The aim of customer

retention is to help an organization in

retaining as many customers as possible.

The bank now days spend on the customer

acquisition as it is a quick way of

increasing revenue but customer retention

is faster and costs seven times less than the

customer acquisition (Agolla, Makara and

Monametsi, 2018). It is an effective way of

increasing revenue by selling to the

existing customers as the organization

does not have a need to attract customers

and guide.

As per Ennew Binks and Chiplin, 2015,

customer satisfaction keeps ahead of the

bank compared to the competitors. When

the customers are satisfied, it works as an

advantage to the bank. The customer

satisfaction promotes to customer

retention. The longer customers are

Customer retention 3

satisfied; more are the chances of returning

customers in the future (Ennew Binks and

Chiplin, 2015). Customer retention is also

the base of maintaining loyalty. The loyal

customers are appreciated by the

organization and advocate the bran for the

lifetime. It also brings revenue to the

organization. The bank makes use of social

media marketing to engage customers and

provide a personal experience to them.

According to Bhat and Darzi, 2016, the

banking is identified as a competitive area

and the competition is increasing in the

banking sector on a daily basis. The

formulation of the new rules and

innovative technology is making banks to

be outstanding (Bhat and Darzi, 2016).

The CRM (Customer Relationship

Management) tools are also being

implemented to enhance customer

satisfaction and retention. The tools also

analyse the existing retention rates by

making use of predictive models.

The machine learning is becoming more

apparent day by day in order to improve

customer retention rate. The bank needs to

beef up with the security, streamline

process and customer satisfaction. The

machine learning creates opportunities for

the bank. The machine learning in the

fintech is a communal phrase. It enables a

new level of service for the financial

forecasting, customer service and data

safety. The machine learning is enabling

the fintech sector. It prevents fraud,

manages risk, improves chatbot customer

experience, network security and more

(Sayani, 2015). The prediction of the

customer churn works as a predictive

scoring model. It has a role in assessing

the probability of each customer staying or

not. The existing customers are used for

suggesting various models like SVM,

Random Forest or Naïve Bayes. It expands

the predictive performance and the

additional scoring outcome is also used to

evaluate who is a good and bad customer

(Magasi, 2015). The SVM is the

supervised learning model linked with

learning algorithms which analyse the data

utilised for classification and regression

analysis. This model performs the linear

classification along with the non-linear

classification. It is more of a supervised

machine learning algorithm used for both

classification and regression challenges. It

has a role in coordinating the individual

observation. The existing customers can be

observed in a better way by implementing

the SVM model (Harris, 2015). The

random forest is a collaborative learning

technique which supports both

classification and regression. It

encompasses the concept of a single

classification tree by increasing various

classification trees in the training phase

(Qasem, Abukhadijeh and Aladham,

satisfied; more are the chances of returning

customers in the future (Ennew Binks and

Chiplin, 2015). Customer retention is also

the base of maintaining loyalty. The loyal

customers are appreciated by the

organization and advocate the bran for the

lifetime. It also brings revenue to the

organization. The bank makes use of social

media marketing to engage customers and

provide a personal experience to them.

According to Bhat and Darzi, 2016, the

banking is identified as a competitive area

and the competition is increasing in the

banking sector on a daily basis. The

formulation of the new rules and

innovative technology is making banks to

be outstanding (Bhat and Darzi, 2016).

The CRM (Customer Relationship

Management) tools are also being

implemented to enhance customer

satisfaction and retention. The tools also

analyse the existing retention rates by

making use of predictive models.

The machine learning is becoming more

apparent day by day in order to improve

customer retention rate. The bank needs to

beef up with the security, streamline

process and customer satisfaction. The

machine learning creates opportunities for

the bank. The machine learning in the

fintech is a communal phrase. It enables a

new level of service for the financial

forecasting, customer service and data

safety. The machine learning is enabling

the fintech sector. It prevents fraud,

manages risk, improves chatbot customer

experience, network security and more

(Sayani, 2015). The prediction of the

customer churn works as a predictive

scoring model. It has a role in assessing

the probability of each customer staying or

not. The existing customers are used for

suggesting various models like SVM,

Random Forest or Naïve Bayes. It expands

the predictive performance and the

additional scoring outcome is also used to

evaluate who is a good and bad customer

(Magasi, 2015). The SVM is the

supervised learning model linked with

learning algorithms which analyse the data

utilised for classification and regression

analysis. This model performs the linear

classification along with the non-linear

classification. It is more of a supervised

machine learning algorithm used for both

classification and regression challenges. It

has a role in coordinating the individual

observation. The existing customers can be

observed in a better way by implementing

the SVM model (Harris, 2015). The

random forest is a collaborative learning

technique which supports both

classification and regression. It

encompasses the concept of a single

classification tree by increasing various

classification trees in the training phase

(Qasem, Abukhadijeh and Aladham,

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

Customer retention 4

2016). In order to classify, each tree

generates a response in the forest. The

class is chosen by the model which

attained the most votes over all the trees in

the forest. The foremost advantage of this

model over traditional decision trees is the

safeguard against overfitting (Belgiu and

Drăguţ, 2016). It enables the model to

provide high performance. On the other

side, Naive Bayes is a categorized

technique based on Bayer’s theorem. It

embraces the idea of complete variables

independence as the absence of one feature

can lead the absence of other feature. It

undertakes all the variables individually

contributed to the probability that the

instance associates to the certain class

(Keramati, Ghaneei and Mirmohammadi,

2016). It is a supervised learning technique

which centres its estimates for new

instances founded on the analysis of the

descendants. The probability score and

class membership are generally the

outcome of this model (Li, et al. 2018).

This model forecasts the prospect that a

customer will stay with the service

provider or switch to other one. It assists in

the churn problem.

A linear model is developed to analyse

customer retention. It was proposed that

customer relationship is a significant factor

in customer retention. It lies between the

customer satisfaction and retention. There

is a statistically proven relationship

between customer satisfaction and

customer retention (Stripling, et al. 2018).

The customer-centric culture centred on

the coordinated and integrated

organizational culture is critical for

successful customer retention. Predictably,

customer satisfaction is observed as one of

the critical element for long term customer

relationships. Higher the number of

satisfied customers higher will be

customer retention. The positive

customer's works create positive word of

mouth (Agolla, Makara and Monametsi,

2018).

The commercial and public banks have

started adopting the latest technologies in

order to outperform their competitors. The

banks have introduced innovative products

like mobile banking, core banking,

commercial banking, wealth management,

loyalty programmes and bank assurances.

Nowadays, the growth of the banks relies

on the way they offer structured quality

service and satisfaction to the customers.

The customer satisfaction plays a

significant role in the long term

commitment of the customers. Can Al-

driven analytics help to reduce customer

churn. It finds outs the need, analyse the

problem (Adam, 2018).

The banks are leading in announcing the

latest technologies to compete in the

2016). In order to classify, each tree

generates a response in the forest. The

class is chosen by the model which

attained the most votes over all the trees in

the forest. The foremost advantage of this

model over traditional decision trees is the

safeguard against overfitting (Belgiu and

Drăguţ, 2016). It enables the model to

provide high performance. On the other

side, Naive Bayes is a categorized

technique based on Bayer’s theorem. It

embraces the idea of complete variables

independence as the absence of one feature

can lead the absence of other feature. It

undertakes all the variables individually

contributed to the probability that the

instance associates to the certain class

(Keramati, Ghaneei and Mirmohammadi,

2016). It is a supervised learning technique

which centres its estimates for new

instances founded on the analysis of the

descendants. The probability score and

class membership are generally the

outcome of this model (Li, et al. 2018).

This model forecasts the prospect that a

customer will stay with the service

provider or switch to other one. It assists in

the churn problem.

A linear model is developed to analyse

customer retention. It was proposed that

customer relationship is a significant factor

in customer retention. It lies between the

customer satisfaction and retention. There

is a statistically proven relationship

between customer satisfaction and

customer retention (Stripling, et al. 2018).

The customer-centric culture centred on

the coordinated and integrated

organizational culture is critical for

successful customer retention. Predictably,

customer satisfaction is observed as one of

the critical element for long term customer

relationships. Higher the number of

satisfied customers higher will be

customer retention. The positive

customer's works create positive word of

mouth (Agolla, Makara and Monametsi,

2018).

The commercial and public banks have

started adopting the latest technologies in

order to outperform their competitors. The

banks have introduced innovative products

like mobile banking, core banking,

commercial banking, wealth management,

loyalty programmes and bank assurances.

Nowadays, the growth of the banks relies

on the way they offer structured quality

service and satisfaction to the customers.

The customer satisfaction plays a

significant role in the long term

commitment of the customers. Can Al-

driven analytics help to reduce customer

churn. It finds outs the need, analyse the

problem (Adam, 2018).

The banks are leading in announcing the

latest technologies to compete in the

Customer retention 5

current fintech domain (Pansari and

Kumar, 2017). Various verticals of fintech

domain have a role in the mobility

comprising big data analytics for

forecasting and evaluating customer’s

behaviour, digital payments, blockchain

technology in order to have an absolute

and safe distributed ledger where the

transaction details are decentralised. It also

comprises chatbots that have a role in the

investment domain of fintech. It provides

feedback and has a role in solving

customer queries. The biometric authentic

provides an extra layer of safety to the

personal account of the customers. It

benefits to the customers which solely

provides them with the satisfaction

(Puschmann, 2017).

It is a key business strategy to reduce

customer churn in banking. Reducing

customer churn is in the best interest of

banks in order to retain every possible

customer. The customer churn is needed to

be addressed with urgency. Here are some

approaches which can be used by the

banks to tackle customer behaviour

(Chahal and Bala, 2017). The tribal

knowledge and biased judgement are used

to categorize customers who are likely to

churn. In such a situation, it is expected to

end up targeting customers who are not

going to churn. Offering retention

incentives to such customers can add

unnecessary operational costs to the

organization (Alshurideh, 2016). It is also

a risk for the bank if it does not reach to

the customers who can actually churn. It

can result in losing the business. Data,

names, numbers and some other

information have been randomized to

safeguard private information. The banks

are losing customers to fintech startups.

The startups have implemented a data-

driven approach in order to acquire, serve

and retain customers. The banks are

required to innovate for retaining

customers. The banks are even

necessitated to reach out to the customers

who are likely to leave (Ennew, Binks and

Chiplin, 2015).

The leading multinational bank

concentrates on private banking. The

increased customer churn is faced by the

banks over the last years due to the

augmented competition in the market. The

bank possesses a large amount of customer

data but not capable of leveraging it

competently (Ngo and Nguyen, 2016). The

bank is required to identify the customer

who is intended to leave so that the

marketing department can also broadcast

targeted oriented advertisement in order to

retain customers. The bank is also likely to

comprehend the influencing factors for

churn. It can make bank proactive towards

addressing the issues instead of just

current fintech domain (Pansari and

Kumar, 2017). Various verticals of fintech

domain have a role in the mobility

comprising big data analytics for

forecasting and evaluating customer’s

behaviour, digital payments, blockchain

technology in order to have an absolute

and safe distributed ledger where the

transaction details are decentralised. It also

comprises chatbots that have a role in the

investment domain of fintech. It provides

feedback and has a role in solving

customer queries. The biometric authentic

provides an extra layer of safety to the

personal account of the customers. It

benefits to the customers which solely

provides them with the satisfaction

(Puschmann, 2017).

It is a key business strategy to reduce

customer churn in banking. Reducing

customer churn is in the best interest of

banks in order to retain every possible

customer. The customer churn is needed to

be addressed with urgency. Here are some

approaches which can be used by the

banks to tackle customer behaviour

(Chahal and Bala, 2017). The tribal

knowledge and biased judgement are used

to categorize customers who are likely to

churn. In such a situation, it is expected to

end up targeting customers who are not

going to churn. Offering retention

incentives to such customers can add

unnecessary operational costs to the

organization (Alshurideh, 2016). It is also

a risk for the bank if it does not reach to

the customers who can actually churn. It

can result in losing the business. Data,

names, numbers and some other

information have been randomized to

safeguard private information. The banks

are losing customers to fintech startups.

The startups have implemented a data-

driven approach in order to acquire, serve

and retain customers. The banks are

required to innovate for retaining

customers. The banks are even

necessitated to reach out to the customers

who are likely to leave (Ennew, Binks and

Chiplin, 2015).

The leading multinational bank

concentrates on private banking. The

increased customer churn is faced by the

banks over the last years due to the

augmented competition in the market. The

bank possesses a large amount of customer

data but not capable of leveraging it

competently (Ngo and Nguyen, 2016). The

bank is required to identify the customer

who is intended to leave so that the

marketing department can also broadcast

targeted oriented advertisement in order to

retain customers. The bank is also likely to

comprehend the influencing factors for

churn. It can make bank proactive towards

addressing the issues instead of just

Customer retention 6

reacting (Bhat and Darzi, 2016). The

problem identified is to reduce customers

churn, stabilize the business and augment

profits.

The machine learning measures customer

satisfaction and loyalty taken place in the

bank. It aids in the fintech sector by

increasing the customer base and

segmentation of the customers. It will

automatically encourage the development

of the new products and innovate more

verticals according to customer prospects

(Ayo, et al. 2016).

Tellius is the solution towards the

customer churn. It has made bank to

discover characteristics which caused

customer churn. Such patterns were

discovered repeatedly by fundamental

machine learning algorithms. Additionally,

the customer churn profile is also

identified as high worth risky customers.

The proactive campaigns are also run at

regular intervals to make sure that the bank

retains such customers before they leave

(Nataraj and Rajendran, 2018).

Use of machine learning techniques in

enhancing customer retention in the

BFSI industry

The machine learning has the biggest

impact on the banking industry. It even

illustrates the efficiency and helps in

exceeding customer’s expectations. The

machine learning is used from soring

emails by using Natural Language

processing (NLP). The records are

automatically updated through Customer

Relations Management (CRM). The

efficient assistance is provided through the

customer self-service portals whereas the

stock market trends are predicted for the

successful trading.

Objective

Targeting the right audience at the right

time and to eliminate the unwanted

customer: It is the objective of machine

learning language to targeting the right

audience at the right time. The bank should

be in the condition to determine the

audience along with the location. The

audience can be defined through any

variable. For instance, the bank wants to

offer its product to 25-year-old persons

living in suburban areas across the west

(Vieira and Sehgal, 2018). The bank is

required to know how many people are in

that area with similar attributes. On the

other side, how many people like that bank

have access to that profile? The targeting

helps in achieving that and constructing

different public segments. The potential of

each segment can be maximized by

understanding the scale of them. It can

help banks to give the best chance of

retaining customers at scale.

reacting (Bhat and Darzi, 2016). The

problem identified is to reduce customers

churn, stabilize the business and augment

profits.

The machine learning measures customer

satisfaction and loyalty taken place in the

bank. It aids in the fintech sector by

increasing the customer base and

segmentation of the customers. It will

automatically encourage the development

of the new products and innovate more

verticals according to customer prospects

(Ayo, et al. 2016).

Tellius is the solution towards the

customer churn. It has made bank to

discover characteristics which caused

customer churn. Such patterns were

discovered repeatedly by fundamental

machine learning algorithms. Additionally,

the customer churn profile is also

identified as high worth risky customers.

The proactive campaigns are also run at

regular intervals to make sure that the bank

retains such customers before they leave

(Nataraj and Rajendran, 2018).

Use of machine learning techniques in

enhancing customer retention in the

BFSI industry

The machine learning has the biggest

impact on the banking industry. It even

illustrates the efficiency and helps in

exceeding customer’s expectations. The

machine learning is used from soring

emails by using Natural Language

processing (NLP). The records are

automatically updated through Customer

Relations Management (CRM). The

efficient assistance is provided through the

customer self-service portals whereas the

stock market trends are predicted for the

successful trading.

Objective

Targeting the right audience at the right

time and to eliminate the unwanted

customer: It is the objective of machine

learning language to targeting the right

audience at the right time. The bank should

be in the condition to determine the

audience along with the location. The

audience can be defined through any

variable. For instance, the bank wants to

offer its product to 25-year-old persons

living in suburban areas across the west

(Vieira and Sehgal, 2018). The bank is

required to know how many people are in

that area with similar attributes. On the

other side, how many people like that bank

have access to that profile? The targeting

helps in achieving that and constructing

different public segments. The potential of

each segment can be maximized by

understanding the scale of them. It can

help banks to give the best chance of

retaining customers at scale.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Customer retention 7

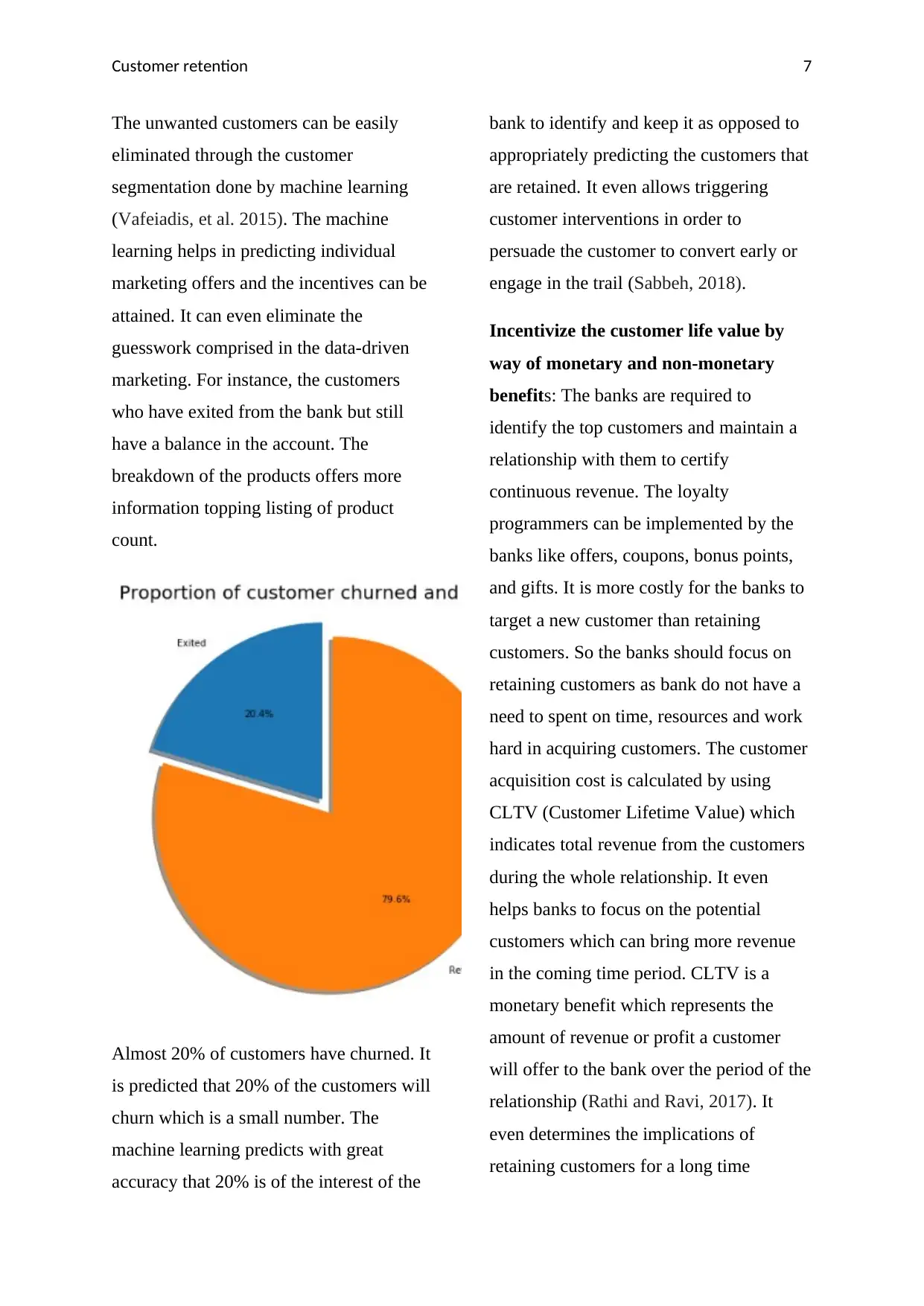

The unwanted customers can be easily

eliminated through the customer

segmentation done by machine learning

(Vafeiadis, et al. 2015). The machine

learning helps in predicting individual

marketing offers and the incentives can be

attained. It can even eliminate the

guesswork comprised in the data-driven

marketing. For instance, the customers

who have exited from the bank but still

have a balance in the account. The

breakdown of the products offers more

information topping listing of product

count.

Almost 20% of customers have churned. It

is predicted that 20% of the customers will

churn which is a small number. The

machine learning predicts with great

accuracy that 20% is of the interest of the

bank to identify and keep it as opposed to

appropriately predicting the customers that

are retained. It even allows triggering

customer interventions in order to

persuade the customer to convert early or

engage in the trail (Sabbeh, 2018).

Incentivize the customer life value by

way of monetary and non-monetary

benefits: The banks are required to

identify the top customers and maintain a

relationship with them to certify

continuous revenue. The loyalty

programmers can be implemented by the

banks like offers, coupons, bonus points,

and gifts. It is more costly for the banks to

target a new customer than retaining

customers. So the banks should focus on

retaining customers as bank do not have a

need to spent on time, resources and work

hard in acquiring customers. The customer

acquisition cost is calculated by using

CLTV (Customer Lifetime Value) which

indicates total revenue from the customers

during the whole relationship. It even

helps banks to focus on the potential

customers which can bring more revenue

in the coming time period. CLTV is a

monetary benefit which represents the

amount of revenue or profit a customer

will offer to the bank over the period of the

relationship (Rathi and Ravi, 2017). It

even determines the implications of

retaining customers for a long time

The unwanted customers can be easily

eliminated through the customer

segmentation done by machine learning

(Vafeiadis, et al. 2015). The machine

learning helps in predicting individual

marketing offers and the incentives can be

attained. It can even eliminate the

guesswork comprised in the data-driven

marketing. For instance, the customers

who have exited from the bank but still

have a balance in the account. The

breakdown of the products offers more

information topping listing of product

count.

Almost 20% of customers have churned. It

is predicted that 20% of the customers will

churn which is a small number. The

machine learning predicts with great

accuracy that 20% is of the interest of the

bank to identify and keep it as opposed to

appropriately predicting the customers that

are retained. It even allows triggering

customer interventions in order to

persuade the customer to convert early or

engage in the trail (Sabbeh, 2018).

Incentivize the customer life value by

way of monetary and non-monetary

benefits: The banks are required to

identify the top customers and maintain a

relationship with them to certify

continuous revenue. The loyalty

programmers can be implemented by the

banks like offers, coupons, bonus points,

and gifts. It is more costly for the banks to

target a new customer than retaining

customers. So the banks should focus on

retaining customers as bank do not have a

need to spent on time, resources and work

hard in acquiring customers. The customer

acquisition cost is calculated by using

CLTV (Customer Lifetime Value) which

indicates total revenue from the customers

during the whole relationship. It even

helps banks to focus on the potential

customers which can bring more revenue

in the coming time period. CLTV is a

monetary benefit which represents the

amount of revenue or profit a customer

will offer to the bank over the period of the

relationship (Rathi and Ravi, 2017). It

even determines the implications of

retaining customers for a long time

Customer retention 8

compared to the short term customers. The

approaches to calculate CLTV are:

Probabilistic models: The probabilistic

models operate by fitting a probability

distribution to the pragmatic

RFM(Recency, Frequency, and Monetary)

value for the customers (Alborzi and

Khanbabaei, 2016). Such models are

centered on the buying behavior which is

described by the transaction history of

each customer.

ML models: The ML models are broad and

mainly used a class of statistical models in

which parameters are fitted to the data by

training. This model uses more features

than probabilistic models. Deep neural

network (DNN) model is used in the

popular ML models.

Optimizing customer services through

emerging technologies: The customer

service can be optimized through the

emerging technologies. ML can solve the

problem of manual data entry. The ML

algorithms and predictive modeling

algorithms can substantially improve the

situation. The ML programs are effective

in improving the process as more

calculations can be made. The machines

can even learn to perform the time-

intensive documentation along with the

data entry tasks. The employees in the

bank also can perform time-intensive

documentation and data entry tasks. The

employees can also spend time on the

higher value problem-solving tasks (Patil

and Dharwadkar, 2017). The natural

language processing technology has been

also developed by AL which has a role in

scanning texts and determining the

relationship between concepts to write

reports.

The ML also solves the earliest problems

like spam detection. Earlier pre-existing

rule-based technology was used to remove

spam now the new rules have been created

by the spam filters through ML. The

neutral networks has made possible in the

spam filters and Google now boasts .1% of

spam rate. The junk mail can be

recognized in the spam filters. The ML can

even identify and filter abuse on social

media websites regarding bank

functioning. The ML enables banks to

identify the interested customers who are

likely to purchase the products. The

algorithm has a role in recognizing the

hidden pattern among the items and

concentrating on the grouping similar

products into the clusters. The ML has

been also helpful for the banks in enabling

product based recommendation system. It

offers purchase history to the customers

along with a large inventory of the

products. ML models identify the products

which are liked by the customers and

compared to the short term customers. The

approaches to calculate CLTV are:

Probabilistic models: The probabilistic

models operate by fitting a probability

distribution to the pragmatic

RFM(Recency, Frequency, and Monetary)

value for the customers (Alborzi and

Khanbabaei, 2016). Such models are

centered on the buying behavior which is

described by the transaction history of

each customer.

ML models: The ML models are broad and

mainly used a class of statistical models in

which parameters are fitted to the data by

training. This model uses more features

than probabilistic models. Deep neural

network (DNN) model is used in the

popular ML models.

Optimizing customer services through

emerging technologies: The customer

service can be optimized through the

emerging technologies. ML can solve the

problem of manual data entry. The ML

algorithms and predictive modeling

algorithms can substantially improve the

situation. The ML programs are effective

in improving the process as more

calculations can be made. The machines

can even learn to perform the time-

intensive documentation along with the

data entry tasks. The employees in the

bank also can perform time-intensive

documentation and data entry tasks. The

employees can also spend time on the

higher value problem-solving tasks (Patil

and Dharwadkar, 2017). The natural

language processing technology has been

also developed by AL which has a role in

scanning texts and determining the

relationship between concepts to write

reports.

The ML also solves the earliest problems

like spam detection. Earlier pre-existing

rule-based technology was used to remove

spam now the new rules have been created

by the spam filters through ML. The

neutral networks has made possible in the

spam filters and Google now boasts .1% of

spam rate. The junk mail can be

recognized in the spam filters. The ML can

even identify and filter abuse on social

media websites regarding bank

functioning. The ML enables banks to

identify the interested customers who are

likely to purchase the products. The

algorithm has a role in recognizing the

hidden pattern among the items and

concentrating on the grouping similar

products into the clusters. The ML has

been also helpful for the banks in enabling

product based recommendation system. It

offers purchase history to the customers

along with a large inventory of the

products. ML models identify the products

which are liked by the customers and

Customer retention 9

expected to be purchased (Katelaris and

Themistocleous, 2017). The algorithm has

a role in identifying the hidden patterns

among the items and concentrating on

grouping similar products into the clusters.

Motivation

Imbalances in risk and dynamics

analysis in customer retention: The

competition is continuously increasing

among the banks and has been a rapid shift

in the business process deliverance. The

Fintech and national banks are competing

for the same group of customers. The

banks are striving to improve the business

process through liaising with the

customers to endure and compete

successfully. The casual relationship exists

between the customer knowledge

management which can sometimes create

an imbalance in risk and dynamics analysis

in the customer retention. The challenge is

faced in comprehending the complete

customer lifecycle across channels and

products (Mohanty and Sree, 2018). The

imbalances in risk and dynamics analysis

in customer retention can be managed by

increasing customer loyalty and reducing

churn. It is also essential to understand the

requirement of the smart business

opportunities for innovation which can

drive growth. The customer insight should

be used to drive strategic planning across

the banks.

The gap in identifying the retention

campaigns: The proportion of the churned

customers is contrariwise related to the

population of the customers. The banks

can possibly have a problem in retaining

customers. The ratio of the female

customers churning is realized more than

the male customers (Maldonado, et al.

2015). The gap is identified in retaining

customers due to the more churned with

the credit cards. The inactive customers

have great churn and the banks need a

program to turn this group into the active

customers as it can result in a positive

impact on the customer churn. The gap

analysis offers the current situation

regarding banking products and services.

The bank can make a minimum gap after

getting the gap analysis report. The

understanding of customer retention

factors closes the gap between customer

retention and customer attrition. The

prediction of the industry trends can lessen

the gap in retaining campaigns. It can

utilize data analytics in order to predict the

forthcoming industry trends and customer

demands (Miguéis, Camanho, and Borges,

2017). It is a better way to indulge

customers and suggest them before

something is needed by them. It can

elevate the bank head and shoulder above

the competitors. The advantage of

predictive analytics can be used by banks

expected to be purchased (Katelaris and

Themistocleous, 2017). The algorithm has

a role in identifying the hidden patterns

among the items and concentrating on

grouping similar products into the clusters.

Motivation

Imbalances in risk and dynamics

analysis in customer retention: The

competition is continuously increasing

among the banks and has been a rapid shift

in the business process deliverance. The

Fintech and national banks are competing

for the same group of customers. The

banks are striving to improve the business

process through liaising with the

customers to endure and compete

successfully. The casual relationship exists

between the customer knowledge

management which can sometimes create

an imbalance in risk and dynamics analysis

in the customer retention. The challenge is

faced in comprehending the complete

customer lifecycle across channels and

products (Mohanty and Sree, 2018). The

imbalances in risk and dynamics analysis

in customer retention can be managed by

increasing customer loyalty and reducing

churn. It is also essential to understand the

requirement of the smart business

opportunities for innovation which can

drive growth. The customer insight should

be used to drive strategic planning across

the banks.

The gap in identifying the retention

campaigns: The proportion of the churned

customers is contrariwise related to the

population of the customers. The banks

can possibly have a problem in retaining

customers. The ratio of the female

customers churning is realized more than

the male customers (Maldonado, et al.

2015). The gap is identified in retaining

customers due to the more churned with

the credit cards. The inactive customers

have great churn and the banks need a

program to turn this group into the active

customers as it can result in a positive

impact on the customer churn. The gap

analysis offers the current situation

regarding banking products and services.

The bank can make a minimum gap after

getting the gap analysis report. The

understanding of customer retention

factors closes the gap between customer

retention and customer attrition. The

prediction of the industry trends can lessen

the gap in retaining campaigns. It can

utilize data analytics in order to predict the

forthcoming industry trends and customer

demands (Miguéis, Camanho, and Borges,

2017). It is a better way to indulge

customers and suggest them before

something is needed by them. It can

elevate the bank head and shoulder above

the competitors. The advantage of

predictive analytics can be used by banks

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

Customer retention 10

(Keramati, Ghaneei, and Mirmohammadi,

2016).

Divergence in fund allocations between

retention/acquisitions: The banks prefer

customer retention over acquiring the new

ones. The cost of acquiring a new

customer is almost five times more than

the cost of retaining a previous employee.

There are different parameters for

customer acquisition and customer

retention. The major involved here is ‘cost

factor’. It has been observed that 44% of

organizations prefer customer retention

and executing strategies for the same. Both

customer retention and acquisition are

important for shaping the future of an

organization. It helps businesses to grow

and prosper. Increasing customer retention

by 5% can result in increasing 25%-95%

profits. The succession rate of selling to an

existing customer is 60%-70% whereas

selling to a new customer is 5-20%. The

bank can increase customer retention rate

by building the customer loyalty rate as

loyal customers are likely to repurchase

the products and services five times (5x)

more. The 5x is anticipated to forgive, 4x

is anticipated to refer and 7x is anticipated

to try a new proposing. The 33% of

customers switch to other banks once poor

service is experienced. The customers can

be retained through loyalty programs,

offers, and memberships. It helps in

retaining customers for the long time and

saves the cost along with the cost to

acquire new customers.

Absent of earlier research towards

demographic aspects: The demographic

factors have become more important for

the banks. The demographic variables like

gender, age, occupation, education level,

monthly income and the type of accounts

held influences by the customer's influence

research of the banks. The quantitative

analysis is carried from the persons who

have a bank account. The five variables

like age, gender, education, monthly

income and type of account exemplify

significance towards using banking

services. The banks are required to connect

with customers by using internet

applications. The customers using bank

services are young and old aged and are

more affluent than average. The income

and gender are realized to put less impact

on consuming the services. The

demographics have more roles in

persuading the utilization of the banking

services along with the location of the

bank. The demographics play an important

role in comprehending the buying behavior

of the customers (Abdou, et al. 2017). The

banks develop products as per the

requirements, taste, and behavior of the

customers. But the research lacks

innovative technology as to suit the

(Keramati, Ghaneei, and Mirmohammadi,

2016).

Divergence in fund allocations between

retention/acquisitions: The banks prefer

customer retention over acquiring the new

ones. The cost of acquiring a new

customer is almost five times more than

the cost of retaining a previous employee.

There are different parameters for

customer acquisition and customer

retention. The major involved here is ‘cost

factor’. It has been observed that 44% of

organizations prefer customer retention

and executing strategies for the same. Both

customer retention and acquisition are

important for shaping the future of an

organization. It helps businesses to grow

and prosper. Increasing customer retention

by 5% can result in increasing 25%-95%

profits. The succession rate of selling to an

existing customer is 60%-70% whereas

selling to a new customer is 5-20%. The

bank can increase customer retention rate

by building the customer loyalty rate as

loyal customers are likely to repurchase

the products and services five times (5x)

more. The 5x is anticipated to forgive, 4x

is anticipated to refer and 7x is anticipated

to try a new proposing. The 33% of

customers switch to other banks once poor

service is experienced. The customers can

be retained through loyalty programs,

offers, and memberships. It helps in

retaining customers for the long time and

saves the cost along with the cost to

acquire new customers.

Absent of earlier research towards

demographic aspects: The demographic

factors have become more important for

the banks. The demographic variables like

gender, age, occupation, education level,

monthly income and the type of accounts

held influences by the customer's influence

research of the banks. The quantitative

analysis is carried from the persons who

have a bank account. The five variables

like age, gender, education, monthly

income and type of account exemplify

significance towards using banking

services. The banks are required to connect

with customers by using internet

applications. The customers using bank

services are young and old aged and are

more affluent than average. The income

and gender are realized to put less impact

on consuming the services. The

demographics have more roles in

persuading the utilization of the banking

services along with the location of the

bank. The demographics play an important

role in comprehending the buying behavior

of the customers (Abdou, et al. 2017). The

banks develop products as per the

requirements, taste, and behavior of the

customers. But the research lacks

innovative technology as to suit the

Customer retention 11

demographics like the sustainable level of

education. The customers are more

reactive to innovations. It has been also

observed that the younger customers have

a positive attitude than the old age

customers towards acceptance of the

technology.

Research methodology

To fulfil the research objective; a

descriptive research design is adopted as it

is suitable for the study. A questionnaire

has been taken from the article in order to

gather the data and find out the most

significant aspect of customer retention in

the banking industry (Mahapatra and

Parveen 2017). The secondary research is

conducted to implement the research. The

customer service has been redefined due to

the machine learning. It has even helped in

cutting front office and staffing costs. The

machine learning algorithms has helped

banks in performing sentiment analysis

and gives suggestions on what customers

think. The structured form was dispersed

to the banking customers based on the

demographics like gender, age, education,

marital status, occupation and income

level. The data was gathered successfully

from 500 respondents who have a saving

account or current account or both. The

opinion of the respondents on the twenty

items related to customer retention is

acquired. The features of customer

retention are characterised into four main

groups, tangible, reliability, responsiveness

and assurance and empathy factors

(Vafeiadis, et al. 2015). The customers

were requested to provide their opinion

concerning factors affecting customer

retention on Likert’s five-point scale. The

opinions were recorded from ‘strongly

disagree’ to ‘strongly agree’. The weight

one is allocated to the ‘strongly disagree’

and five to the ‘strongly agree’. The

questionnaires were circulated at the bank

premises and were face-to-face managed

in order to maximize the response rate and

solve the interrogations of the respondents.

demographics like the sustainable level of

education. The customers are more

reactive to innovations. It has been also

observed that the younger customers have

a positive attitude than the old age

customers towards acceptance of the

technology.

Research methodology

To fulfil the research objective; a

descriptive research design is adopted as it

is suitable for the study. A questionnaire

has been taken from the article in order to

gather the data and find out the most

significant aspect of customer retention in

the banking industry (Mahapatra and

Parveen 2017). The secondary research is

conducted to implement the research. The

customer service has been redefined due to

the machine learning. It has even helped in

cutting front office and staffing costs. The

machine learning algorithms has helped

banks in performing sentiment analysis

and gives suggestions on what customers

think. The structured form was dispersed

to the banking customers based on the

demographics like gender, age, education,

marital status, occupation and income

level. The data was gathered successfully

from 500 respondents who have a saving

account or current account or both. The

opinion of the respondents on the twenty

items related to customer retention is

acquired. The features of customer

retention are characterised into four main

groups, tangible, reliability, responsiveness

and assurance and empathy factors

(Vafeiadis, et al. 2015). The customers

were requested to provide their opinion

concerning factors affecting customer

retention on Likert’s five-point scale. The

opinions were recorded from ‘strongly

disagree’ to ‘strongly agree’. The weight

one is allocated to the ‘strongly disagree’

and five to the ‘strongly agree’. The

questionnaires were circulated at the bank

premises and were face-to-face managed

in order to maximize the response rate and

solve the interrogations of the respondents.

Customer retention 12

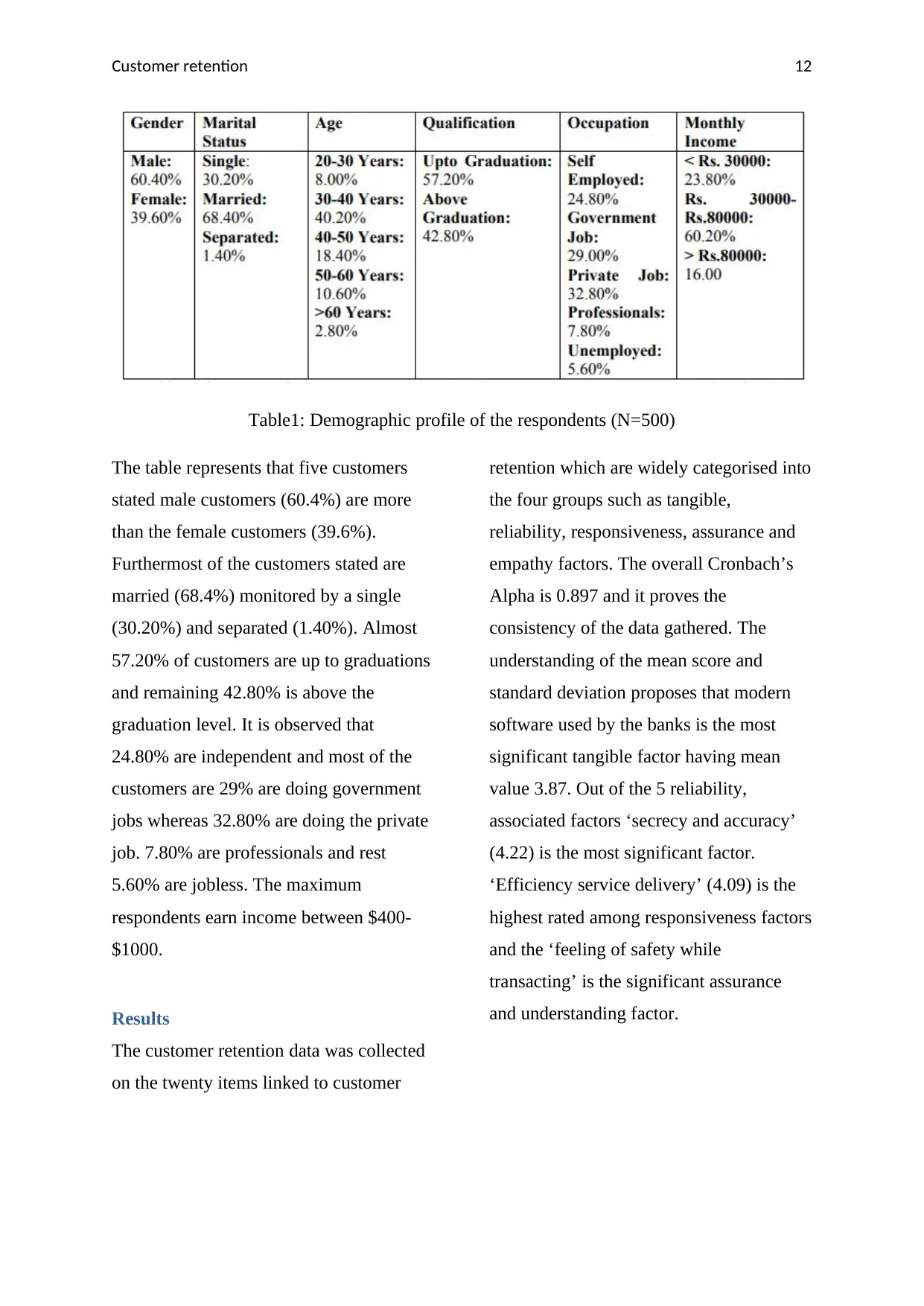

Table1: Demographic profile of the respondents (N=500)

The table represents that five customers

stated male customers (60.4%) are more

than the female customers (39.6%).

Furthermost of the customers stated are

married (68.4%) monitored by a single

(30.20%) and separated (1.40%). Almost

57.20% of customers are up to graduations

and remaining 42.80% is above the

graduation level. It is observed that

24.80% are independent and most of the

customers are 29% are doing government

jobs whereas 32.80% are doing the private

job. 7.80% are professionals and rest

5.60% are jobless. The maximum

respondents earn income between $400-

$1000.

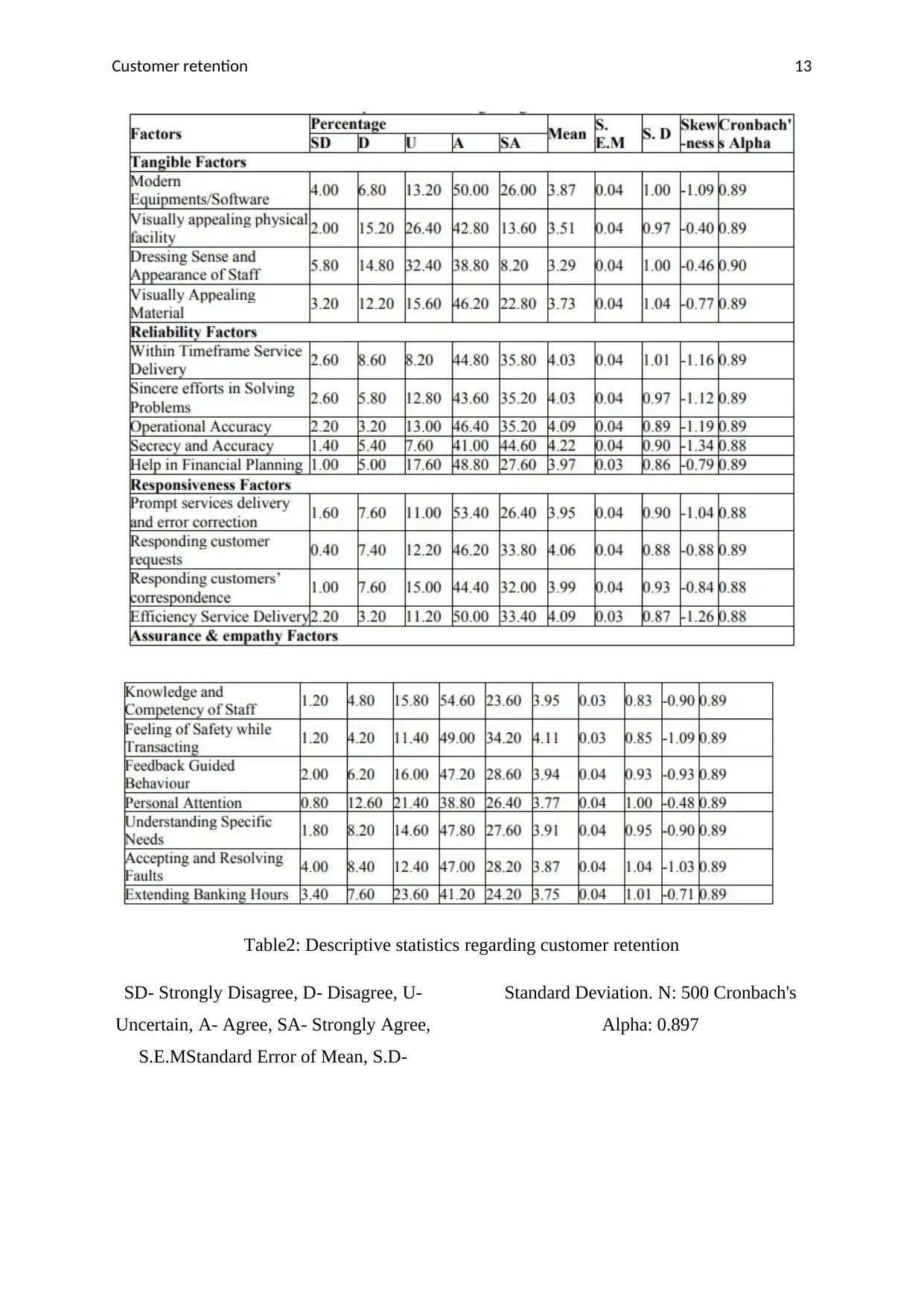

Results

The customer retention data was collected

on the twenty items linked to customer

retention which are widely categorised into

the four groups such as tangible,

reliability, responsiveness, assurance and

empathy factors. The overall Cronbach’s

Alpha is 0.897 and it proves the

consistency of the data gathered. The

understanding of the mean score and

standard deviation proposes that modern

software used by the banks is the most

significant tangible factor having mean

value 3.87. Out of the 5 reliability,

associated factors ‘secrecy and accuracy’

(4.22) is the most significant factor.

‘Efficiency service delivery’ (4.09) is the

highest rated among responsiveness factors

and the ‘feeling of safety while

transacting’ is the significant assurance

and understanding factor.

Table1: Demographic profile of the respondents (N=500)

The table represents that five customers

stated male customers (60.4%) are more

than the female customers (39.6%).

Furthermost of the customers stated are

married (68.4%) monitored by a single

(30.20%) and separated (1.40%). Almost

57.20% of customers are up to graduations

and remaining 42.80% is above the

graduation level. It is observed that

24.80% are independent and most of the

customers are 29% are doing government

jobs whereas 32.80% are doing the private

job. 7.80% are professionals and rest

5.60% are jobless. The maximum

respondents earn income between $400-

$1000.

Results

The customer retention data was collected

on the twenty items linked to customer

retention which are widely categorised into

the four groups such as tangible,

reliability, responsiveness, assurance and

empathy factors. The overall Cronbach’s

Alpha is 0.897 and it proves the

consistency of the data gathered. The

understanding of the mean score and

standard deviation proposes that modern

software used by the banks is the most

significant tangible factor having mean

value 3.87. Out of the 5 reliability,

associated factors ‘secrecy and accuracy’

(4.22) is the most significant factor.

‘Efficiency service delivery’ (4.09) is the

highest rated among responsiveness factors

and the ‘feeling of safety while

transacting’ is the significant assurance

and understanding factor.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Customer retention 13

Table2: Descriptive statistics regarding customer retention

SD- Strongly Disagree, D- Disagree, U-

Uncertain, A- Agree, SA- Strongly Agree,

S.E.MStandard Error of Mean, S.D-

Standard Deviation. N: 500 Cronbach's

Alpha: 0.897

Table2: Descriptive statistics regarding customer retention

SD- Strongly Disagree, D- Disagree, U-

Uncertain, A- Agree, SA- Strongly Agree,

S.E.MStandard Error of Mean, S.D-

Standard Deviation. N: 500 Cronbach's

Alpha: 0.897

Customer retention 14

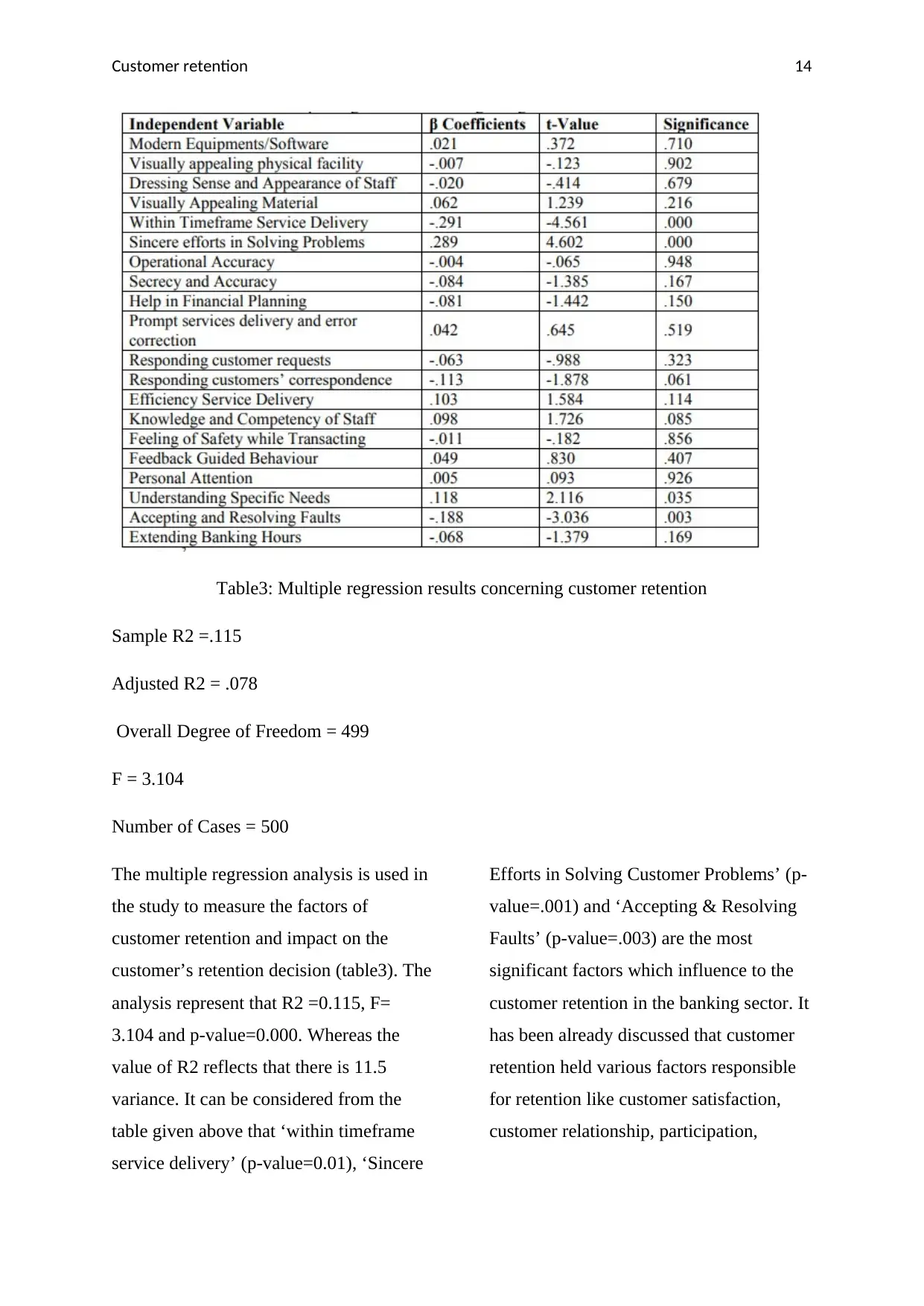

Table3: Multiple regression results concerning customer retention

Sample R2 =.115

Adjusted R2 = .078

Overall Degree of Freedom = 499

F = 3.104

Number of Cases = 500

The multiple regression analysis is used in

the study to measure the factors of

customer retention and impact on the

customer’s retention decision (table3). The

analysis represent that R2 =0.115, F=

3.104 and p-value=0.000. Whereas the

value of R2 reflects that there is 11.5

variance. It can be considered from the

table given above that ‘within timeframe

service delivery’ (p-value=0.01), ‘Sincere

Efforts in Solving Customer Problems’ (p-

value=.001) and ‘Accepting & Resolving

Faults’ (p-value=.003) are the most

significant factors which influence to the

customer retention in the banking sector. It

has been already discussed that customer

retention held various factors responsible

for retention like customer satisfaction,

customer relationship, participation,

Table3: Multiple regression results concerning customer retention

Sample R2 =.115

Adjusted R2 = .078

Overall Degree of Freedom = 499

F = 3.104

Number of Cases = 500

The multiple regression analysis is used in

the study to measure the factors of

customer retention and impact on the

customer’s retention decision (table3). The

analysis represent that R2 =0.115, F=

3.104 and p-value=0.000. Whereas the

value of R2 reflects that there is 11.5

variance. It can be considered from the

table given above that ‘within timeframe

service delivery’ (p-value=0.01), ‘Sincere

Efforts in Solving Customer Problems’ (p-

value=.001) and ‘Accepting & Resolving

Faults’ (p-value=.003) are the most

significant factors which influence to the

customer retention in the banking sector. It

has been already discussed that customer

retention held various factors responsible

for retention like customer satisfaction,

customer relationship, participation,

Customer retention 15

relationship quality, switching costs and

trust.

Conclusion and future work

The research conducted will help the banks

in retaining customers in an efficient

manner. It will also increase efficiency and

reduce customer acquisition cost. It will

automatically lead the organization to

increase revenue. It will also promote the

brand in the developing markets. The cut

throat competition has made essential to

retain the existing customers in order to

succeed in the market. The customer-

centric approach is required to retain

customers because it focuses on providing

quality services and delivers the services

within the time frame. The banks have to

build a quality relationship with the

customers so that the loyalty of the

customers can be attained as the emotional

cost is associated with it. The bank is also

required to concentrate on creating

switching barriers to reduce the defection

of the customer. The customer satisfaction

should be given supreme importance as it

is one of the critical variables impacting

customer retention. It is always considered

that the customer retention efforts cost less

to the organization as compared to the

customer acquisition efforts. The bank

should shift from potential customers to

retaining the existing customers through

CRM. Most importantly, the fintech

should be used by the bank to safeguard

the customer data. The problem of the

customers should be solved in the given

time frame so that customer satisfaction

can be maintained.

In the future in tech can advance

blockchain movement. The blockchain

technology is turning the financial world

into a better. Now days increasing number

of Asian companies concentrate on the

crypto currencies. The blockchain’s

potential will be increasing in the future.

The customers are also representing an

interest in the virtual currencies. The

chatbots are also given importance by the

bank in order to increase customer loyalty.

It also reduces the processing time and

cuts the administrative costs.

relationship quality, switching costs and

trust.

Conclusion and future work

The research conducted will help the banks

in retaining customers in an efficient

manner. It will also increase efficiency and

reduce customer acquisition cost. It will

automatically lead the organization to

increase revenue. It will also promote the

brand in the developing markets. The cut

throat competition has made essential to

retain the existing customers in order to

succeed in the market. The customer-

centric approach is required to retain

customers because it focuses on providing

quality services and delivers the services

within the time frame. The banks have to

build a quality relationship with the

customers so that the loyalty of the

customers can be attained as the emotional

cost is associated with it. The bank is also

required to concentrate on creating

switching barriers to reduce the defection

of the customer. The customer satisfaction

should be given supreme importance as it

is one of the critical variables impacting

customer retention. It is always considered

that the customer retention efforts cost less

to the organization as compared to the

customer acquisition efforts. The bank

should shift from potential customers to

retaining the existing customers through

CRM. Most importantly, the fintech

should be used by the bank to safeguard

the customer data. The problem of the

customers should be solved in the given

time frame so that customer satisfaction

can be maintained.

In the future in tech can advance

blockchain movement. The blockchain

technology is turning the financial world

into a better. Now days increasing number

of Asian companies concentrate on the

crypto currencies. The blockchain’s

potential will be increasing in the future.

The customers are also representing an

interest in the virtual currencies. The

chatbots are also given importance by the

bank in order to increase customer loyalty.

It also reduces the processing time and

cuts the administrative costs.

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

Customer retention 16

Bibliography

Abdou, H., Abd Allah, W., Mulkeen, J., Ntim, C.G. and Wang, Y., 2017. Prediction of

financial strength ratings using machine learning and conventional techniques. Abdou, HA,

Abdallah, WM, Mulkeen, J., Ntim, CG, & Wang, Y.(2017)‘Prediction of financial strength

ratings using machine learning and conventional techniques’, Investment Management and

Financial Innovation, 14(4), pp.194-211.

Adam, M.B., 2018. Improving complex sale cycles and performance by using machine

learning and predictive analytics to understand the customer journey (Doctoral dissertation,

Massachusetts Institute of Technology).

Agolla, J.E., Makara, T. and Monametsi, G., 2018. Impact of banking innovations on

customer attraction, satisfaction and retention: the case of commercial banks in

Botswana. International Journal of Electronic Banking, 1(2), pp.150-170.

Alborzi, M. and Khanbabaei, M., 2016. Using data mining and neural networks techniques to

propose a new hybrid customer behaviour analysis and credit scoring model in banking

services based on a developed RFM analysis method. International Journal of Business

Information Systems, 23(1), pp.1-22.

Alshurideh, M.T., 2016. Is customer retention beneficial for customers: A conceptual

background. Journal of Research in Marketing, 5(3), pp.382-389.

Ayo, C.K., Oni, A.A., Adewoye, O.J. and Eweoya, I.O., 2016. E-banking users’ behaviour: e-

service quality, attitude, and customer satisfaction. International Journal of Bank

Marketing, 34(3), pp.347-367.

Belgiu, M. and Drăguţ, L., 2016. Random forest in remote sensing: A review of applications

and future directions. ISPRS Journal of Photogrammetry and Remote Sensing, 114, pp.24-31.

Bhat, S.A. and Darzi, M.A., 2016. Customer relationship management: An approach to

competitive advantage in the banking sector by exploring the mediational role of

loyalty. International Journal of Bank Marketing, 34(3), pp.388-410.

Bibliography

Abdou, H., Abd Allah, W., Mulkeen, J., Ntim, C.G. and Wang, Y., 2017. Prediction of

financial strength ratings using machine learning and conventional techniques. Abdou, HA,

Abdallah, WM, Mulkeen, J., Ntim, CG, & Wang, Y.(2017)‘Prediction of financial strength

ratings using machine learning and conventional techniques’, Investment Management and

Financial Innovation, 14(4), pp.194-211.

Adam, M.B., 2018. Improving complex sale cycles and performance by using machine

learning and predictive analytics to understand the customer journey (Doctoral dissertation,

Massachusetts Institute of Technology).

Agolla, J.E., Makara, T. and Monametsi, G., 2018. Impact of banking innovations on

customer attraction, satisfaction and retention: the case of commercial banks in

Botswana. International Journal of Electronic Banking, 1(2), pp.150-170.

Alborzi, M. and Khanbabaei, M., 2016. Using data mining and neural networks techniques to

propose a new hybrid customer behaviour analysis and credit scoring model in banking

services based on a developed RFM analysis method. International Journal of Business

Information Systems, 23(1), pp.1-22.

Alshurideh, M.T., 2016. Is customer retention beneficial for customers: A conceptual

background. Journal of Research in Marketing, 5(3), pp.382-389.

Ayo, C.K., Oni, A.A., Adewoye, O.J. and Eweoya, I.O., 2016. E-banking users’ behaviour: e-

service quality, attitude, and customer satisfaction. International Journal of Bank

Marketing, 34(3), pp.347-367.

Belgiu, M. and Drăguţ, L., 2016. Random forest in remote sensing: A review of applications

and future directions. ISPRS Journal of Photogrammetry and Remote Sensing, 114, pp.24-31.

Bhat, S.A. and Darzi, M.A., 2016. Customer relationship management: An approach to

competitive advantage in the banking sector by exploring the mediational role of

loyalty. International Journal of Bank Marketing, 34(3), pp.388-410.

Customer retention 17

Chahal, H. and Bala, R., 2017. Role of customer retention equity in creating and developing

brand value. Journal of Relationship Marketing, 16(2), pp.119-142.

Ennew, C.T., Binks, M.R. and Chiplin, B., 2015. Customer satisfaction and customer

retention: An examination of small businesses and their banks in the UK. In Proceedings of

the 1994 Academy of Marketing Science (AMS) Annual Conference (pp. 188-192). Springer,

Cham.

Harris, T., 2015. Credit scoring using the clustered support vector machine. Expert Systems

with Applications, 42(2), pp.741-750.

Katelaris, L. and Themistocleous, M., 2017, September. Predicting Customer Churn:

Customer Behavior Forecasting for Subscription-Based Organizations. In European,

Mediterranean, and Middle Eastern Conference on Information Systems (pp. 128-135).

Springer, Cham.

Keramati, A., Ghaneei, H. and Mirmohammadi, S.M., 2016. Developing a prediction model

for customer churn from electronic banking services using data mining. Financial

Innovation, 2(1), p.10.

Li, T., Li, J., Liu, Z., Li, P. and Jia, C., 2018. Differentially private Naive Bayes learning over

multiple data sources. Information Sciences, 444, pp.89-104.

Magasi, C., 2015, October. Customer relationship marketing and its influence on customer

retention: a case of commercial banking industry in Tanzania. In Proceedings of the Third

Middle East Conference on Global Business, Economics, Finance and Banking (pp. 1-19).

Mahapatra, S.N. and Parveen K, 2017. Customer Retention: A Study On Indian Banks.

International Journal of Research Granthaalayah. Vol.5(Iss.7): July 2017.

Maldonado, S., Flores, Á., Verbraken, T., Baesens, B. and Weber, R., 2015. Profit-based

feature selection using support vector machines–General framework and an application for

customer retention. Applied Soft Computing, 35, pp.740-748.

Miguéis, V.L., Camanho, A.S. and Borges, J., 2017. Predicting direct marketing response in

banking: comparison of class imbalance methods. Service Business, 11(4), pp.831-849.

Mohanty, R. and Sree, C.N.R., 2018. Churn and Non-churn of Customers in Banking Sector

Using Extreme Learning Machine. In Proceedings of the Second International Conference on

Chahal, H. and Bala, R., 2017. Role of customer retention equity in creating and developing

brand value. Journal of Relationship Marketing, 16(2), pp.119-142.

Ennew, C.T., Binks, M.R. and Chiplin, B., 2015. Customer satisfaction and customer

retention: An examination of small businesses and their banks in the UK. In Proceedings of

the 1994 Academy of Marketing Science (AMS) Annual Conference (pp. 188-192). Springer,

Cham.

Harris, T., 2015. Credit scoring using the clustered support vector machine. Expert Systems

with Applications, 42(2), pp.741-750.

Katelaris, L. and Themistocleous, M., 2017, September. Predicting Customer Churn:

Customer Behavior Forecasting for Subscription-Based Organizations. In European,

Mediterranean, and Middle Eastern Conference on Information Systems (pp. 128-135).

Springer, Cham.

Keramati, A., Ghaneei, H. and Mirmohammadi, S.M., 2016. Developing a prediction model

for customer churn from electronic banking services using data mining. Financial

Innovation, 2(1), p.10.

Li, T., Li, J., Liu, Z., Li, P. and Jia, C., 2018. Differentially private Naive Bayes learning over

multiple data sources. Information Sciences, 444, pp.89-104.

Magasi, C., 2015, October. Customer relationship marketing and its influence on customer

retention: a case of commercial banking industry in Tanzania. In Proceedings of the Third

Middle East Conference on Global Business, Economics, Finance and Banking (pp. 1-19).

Mahapatra, S.N. and Parveen K, 2017. Customer Retention: A Study On Indian Banks.

International Journal of Research Granthaalayah. Vol.5(Iss.7): July 2017.

Maldonado, S., Flores, Á., Verbraken, T., Baesens, B. and Weber, R., 2015. Profit-based

feature selection using support vector machines–General framework and an application for

customer retention. Applied Soft Computing, 35, pp.740-748.

Miguéis, V.L., Camanho, A.S. and Borges, J., 2017. Predicting direct marketing response in

banking: comparison of class imbalance methods. Service Business, 11(4), pp.831-849.

Mohanty, R. and Sree, C.N.R., 2018. Churn and Non-churn of Customers in Banking Sector

Using Extreme Learning Machine. In Proceedings of the Second International Conference on

Customer retention 18

Computational Intelligence and Informatics(pp. 51-58). Springer, Singapore.

Nataraj, B. and Rajendran, R., 2018. Impact of Relationship Quality on Customer Retention–