FNS40811 Certificate IV in Finance and Mortgage Broking Assessment

VerifiedAdded on 2020/10/22

|48

|20179

|30

Homework Assignment

AI Summary

This document presents a completed assessment task for the Certificate IV in Finance and Mortgage Broking (FNS40811). The assignment focuses on identifying and interpreting compliance requirements within the finance industry, particularly for mortgage brokers. It covers key aspects such as the NCCP Act, responsible lending obligations (including the unsuitability test), credit guides, and the roles of regulatory bodies like APRA. The assessment requires the student to demonstrate understanding of compliance requirements, relevant legislation, and the importance of staying up-to-date with industry changes. The task also explores how organizations monitor compliance and the implications of non-compliance for both brokers and clients. The document offers insights into various compliance-related topics, including codes of conduct, training registers, and the impact of APRA's policies on bank lending for investment properties. It provides detailed answers to the assessment questions, covering topics such as client requirements, compliance monitoring, and the relevant legislation.

Certificate IV in Finance and Mortgage Broking

Assessment Task

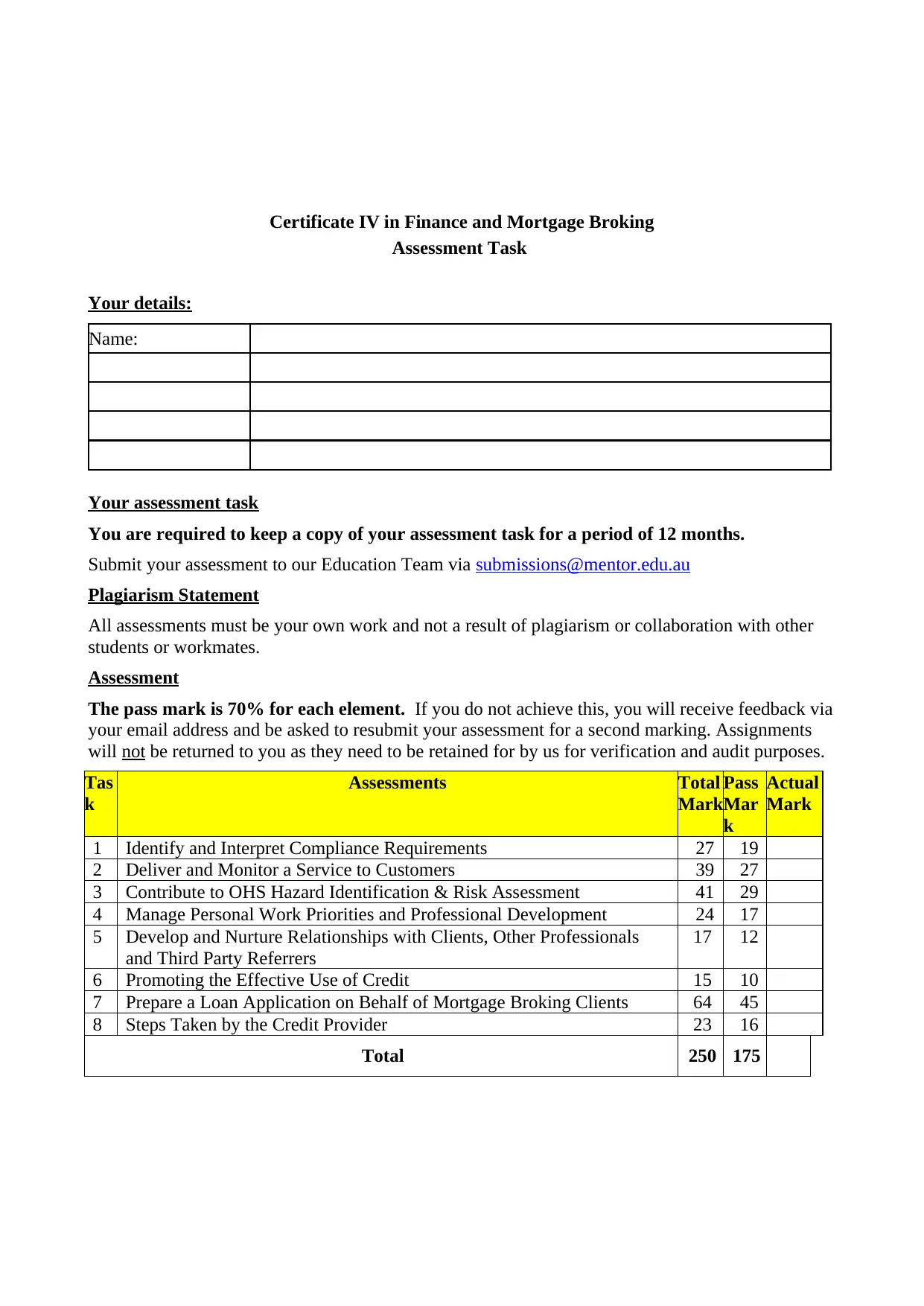

Your details:

Name:

Your assessment task

You are required to keep a copy of your assessment task for a period of 12 months.

Submit your assessment to our Education Team via submissions@mentor.edu.au

Plagiarism Statement

All assessments must be your own work and not a result of plagiarism or collaboration with other

students or workmates.

Assessment

The pass mark is 70% for each element. If you do not achieve this, you will receive feedback via

your email address and be asked to resubmit your assessment for a second marking. Assignments

will not be returned to you as they need to be retained for by us for verification and audit purposes.

Tas

k

Assessments Total

Mark

Pass

Mar

k

Actual

Mark

1 Identify and Interpret Compliance Requirements 27 19

2 Deliver and Monitor a Service to Customers 39 27

3 Contribute to OHS Hazard Identification & Risk Assessment 41 29

4 Manage Personal Work Priorities and Professional Development 24 17

5 Develop and Nurture Relationships with Clients, Other Professionals

and Third Party Referrers

17 12

6 Promoting the Effective Use of Credit 15 10

7 Prepare a Loan Application on Behalf of Mortgage Broking Clients 64 45

8 Steps Taken by the Credit Provider 23 16

Total 250 175

Assessment Task

Your details:

Name:

Your assessment task

You are required to keep a copy of your assessment task for a period of 12 months.

Submit your assessment to our Education Team via submissions@mentor.edu.au

Plagiarism Statement

All assessments must be your own work and not a result of plagiarism or collaboration with other

students or workmates.

Assessment

The pass mark is 70% for each element. If you do not achieve this, you will receive feedback via

your email address and be asked to resubmit your assessment for a second marking. Assignments

will not be returned to you as they need to be retained for by us for verification and audit purposes.

Tas

k

Assessments Total

Mark

Pass

Mar

k

Actual

Mark

1 Identify and Interpret Compliance Requirements 27 19

2 Deliver and Monitor a Service to Customers 39 27

3 Contribute to OHS Hazard Identification & Risk Assessment 41 29

4 Manage Personal Work Priorities and Professional Development 24 17

5 Develop and Nurture Relationships with Clients, Other Professionals

and Third Party Referrers

17 12

6 Promoting the Effective Use of Credit 15 10

7 Prepare a Loan Application on Behalf of Mortgage Broking Clients 64 45

8 Steps Taken by the Credit Provider 23 16

Total 250 175

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Assessor’s Initials: ____________________

Assessment Date: ____________________

Assessment Date: ____________________

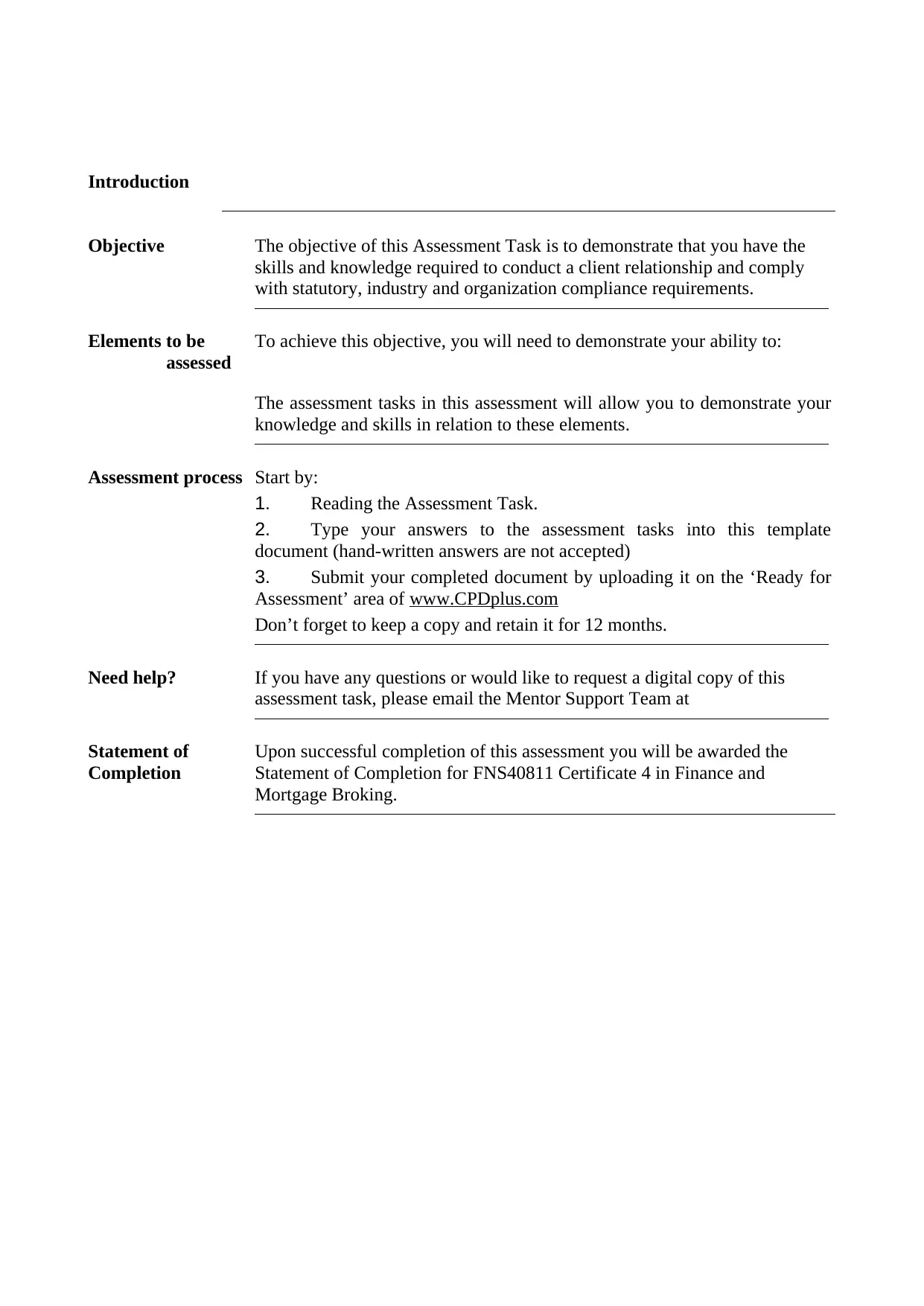

Introduction

Objective The objective of this Assessment Task is to demonstrate that you have the

skills and knowledge required to conduct a client relationship and comply

with statutory, industry and organization compliance requirements.

Elements to be

assessed

To achieve this objective, you will need to demonstrate your ability to:

The assessment tasks in this assessment will allow you to demonstrate your

knowledge and skills in relation to these elements.

Assessment process Start by:

1. Reading the Assessment Task.

2. Type your answers to the assessment tasks into this template

document (hand-written answers are not accepted)

3. Submit your completed document by uploading it on the ‘Ready for

Assessment’ area of www.CPDplus.com

Don’t forget to keep a copy and retain it for 12 months.

Need help? If you have any questions or would like to request a digital copy of this

assessment task, please email the Mentor Support Team at

Statement of

Completion

Upon successful completion of this assessment you will be awarded the

Statement of Completion for FNS40811 Certificate 4 in Finance and

Mortgage Broking.

Objective The objective of this Assessment Task is to demonstrate that you have the

skills and knowledge required to conduct a client relationship and comply

with statutory, industry and organization compliance requirements.

Elements to be

assessed

To achieve this objective, you will need to demonstrate your ability to:

The assessment tasks in this assessment will allow you to demonstrate your

knowledge and skills in relation to these elements.

Assessment process Start by:

1. Reading the Assessment Task.

2. Type your answers to the assessment tasks into this template

document (hand-written answers are not accepted)

3. Submit your completed document by uploading it on the ‘Ready for

Assessment’ area of www.CPDplus.com

Don’t forget to keep a copy and retain it for 12 months.

Need help? If you have any questions or would like to request a digital copy of this

assessment task, please email the Mentor Support Team at

Statement of

Completion

Upon successful completion of this assessment you will be awarded the

Statement of Completion for FNS40811 Certificate 4 in Finance and

Mortgage Broking.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

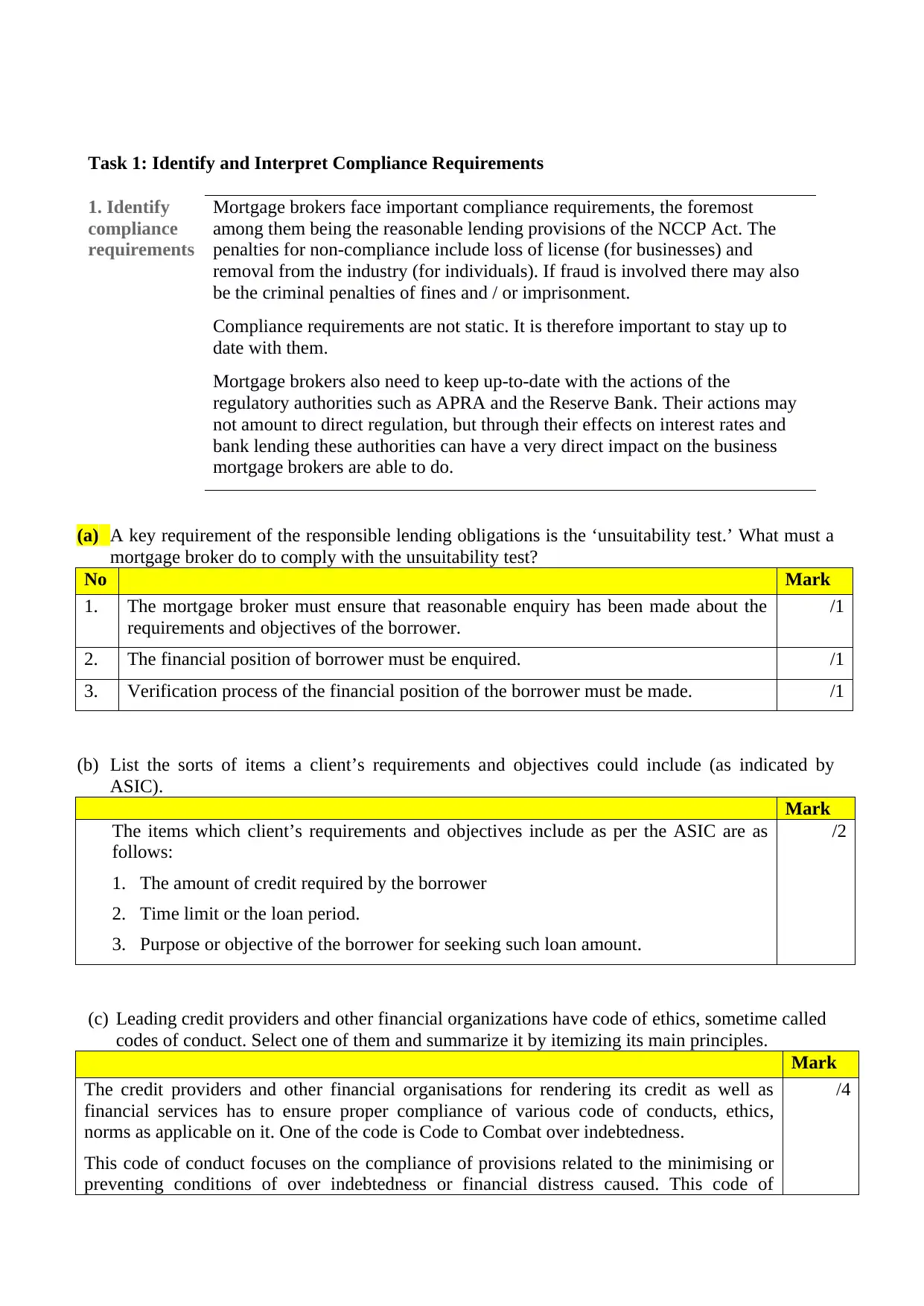

Task 1: Identify and Interpret Compliance Requirements

1. Identify

compliance

requirements

Mortgage brokers face important compliance requirements, the foremost

among them being the reasonable lending provisions of the NCCP Act. The

penalties for non-compliance include loss of license (for businesses) and

removal from the industry (for individuals). If fraud is involved there may also

be the criminal penalties of fines and / or imprisonment.

Compliance requirements are not static. It is therefore important to stay up to

date with them.

Mortgage brokers also need to keep up-to-date with the actions of the

regulatory authorities such as APRA and the Reserve Bank. Their actions may

not amount to direct regulation, but through their effects on interest rates and

bank lending these authorities can have a very direct impact on the business

mortgage brokers are able to do.

(a) A key requirement of the responsible lending obligations is the ‘unsuitability test.’ What must a

mortgage broker do to comply with the unsuitability test?

No Mark

1. The mortgage broker must ensure that reasonable enquiry has been made about the

requirements and objectives of the borrower.

/1

2. The financial position of borrower must be enquired. /1

3. Verification process of the financial position of the borrower must be made. /1

(b) List the sorts of items a client’s requirements and objectives could include (as indicated by

ASIC).

Mark

The items which client’s requirements and objectives include as per the ASIC are as

follows:

1. The amount of credit required by the borrower

2. Time limit or the loan period.

3. Purpose or objective of the borrower for seeking such loan amount.

/2

(c) Leading credit providers and other financial organizations have code of ethics, sometime called

codes of conduct. Select one of them and summarize it by itemizing its main principles.

Mark

The credit providers and other financial organisations for rendering its credit as well as

financial services has to ensure proper compliance of various code of conducts, ethics,

norms as applicable on it. One of the code is Code to Combat over indebtedness.

This code of conduct focuses on the compliance of provisions related to the minimising or

preventing conditions of over indebtedness or financial distress caused. This code of

/4

1. Identify

compliance

requirements

Mortgage brokers face important compliance requirements, the foremost

among them being the reasonable lending provisions of the NCCP Act. The

penalties for non-compliance include loss of license (for businesses) and

removal from the industry (for individuals). If fraud is involved there may also

be the criminal penalties of fines and / or imprisonment.

Compliance requirements are not static. It is therefore important to stay up to

date with them.

Mortgage brokers also need to keep up-to-date with the actions of the

regulatory authorities such as APRA and the Reserve Bank. Their actions may

not amount to direct regulation, but through their effects on interest rates and

bank lending these authorities can have a very direct impact on the business

mortgage brokers are able to do.

(a) A key requirement of the responsible lending obligations is the ‘unsuitability test.’ What must a

mortgage broker do to comply with the unsuitability test?

No Mark

1. The mortgage broker must ensure that reasonable enquiry has been made about the

requirements and objectives of the borrower.

/1

2. The financial position of borrower must be enquired. /1

3. Verification process of the financial position of the borrower must be made. /1

(b) List the sorts of items a client’s requirements and objectives could include (as indicated by

ASIC).

Mark

The items which client’s requirements and objectives include as per the ASIC are as

follows:

1. The amount of credit required by the borrower

2. Time limit or the loan period.

3. Purpose or objective of the borrower for seeking such loan amount.

/2

(c) Leading credit providers and other financial organizations have code of ethics, sometime called

codes of conduct. Select one of them and summarize it by itemizing its main principles.

Mark

The credit providers and other financial organisations for rendering its credit as well as

financial services has to ensure proper compliance of various code of conducts, ethics,

norms as applicable on it. One of the code is Code to Combat over indebtedness.

This code of conduct focuses on the compliance of provisions related to the minimising or

preventing conditions of over indebtedness or financial distress caused. This code of

/4

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

conduct provides relief and safeguarding measures in respect of financial difficulties, loss or

risk to the consumers who are seeking services from this credit and financial organisation.

Sub-total /9

Continued

(d) In point form, list the key information that the NCCP Act requires to be contained in a Credit

Guide.

Mark

The credit guide should contain following key information as per the NCCP Act:

1. Name and contact details of Licensee

2. Australian credit license number of Licensee

3. Details and methods for working out any amount of fees payable to the

Licensee by the consumer

4. Details of top 6 lenders which has been introduced to consumers by the

Licensee and Credit Rep

5. Commission which an individual is likely to receive

6. IDRS and EDRS details of the Licensee

7. The Credit Rep's CR number and contact details.

8. Name of CR's top 6 licensees

9. Information related to the CR's IDRS.

/3

(e) It is important to keep up to date with compliance requirements so that the required changes

can be made to organization procedures and product offerings. Suggest three sources that you

can use.

Mark

1) Professional associations such as The Mortgage and Finance Association of

Australia and The Finance Brokers Association of Australia inform their

members of changes to requirements before they happen.

2) The professional associations code of practice can also be used as a sound

guidance for compliance requirements.

3) Large mortgage broking business organisations have compliance officers

assisting practitioners to meet compliance standards.

/3

(f) Explain the requirement for Australian Credit Licensees to keep a training register.

Mark

As per the requirement for Australian Credit Licensees to keep a training register, it

helps the business organisation in tracking the record of training which has been

imparted to the employees by maintaining the training register. The training of

employees is considered as one of the obligations on credit licensees.

/2

risk to the consumers who are seeking services from this credit and financial organisation.

Sub-total /9

Continued

(d) In point form, list the key information that the NCCP Act requires to be contained in a Credit

Guide.

Mark

The credit guide should contain following key information as per the NCCP Act:

1. Name and contact details of Licensee

2. Australian credit license number of Licensee

3. Details and methods for working out any amount of fees payable to the

Licensee by the consumer

4. Details of top 6 lenders which has been introduced to consumers by the

Licensee and Credit Rep

5. Commission which an individual is likely to receive

6. IDRS and EDRS details of the Licensee

7. The Credit Rep's CR number and contact details.

8. Name of CR's top 6 licensees

9. Information related to the CR's IDRS.

/3

(e) It is important to keep up to date with compliance requirements so that the required changes

can be made to organization procedures and product offerings. Suggest three sources that you

can use.

Mark

1) Professional associations such as The Mortgage and Finance Association of

Australia and The Finance Brokers Association of Australia inform their

members of changes to requirements before they happen.

2) The professional associations code of practice can also be used as a sound

guidance for compliance requirements.

3) Large mortgage broking business organisations have compliance officers

assisting practitioners to meet compliance standards.

/3

(f) Explain the requirement for Australian Credit Licensees to keep a training register.

Mark

As per the requirement for Australian Credit Licensees to keep a training register, it

helps the business organisation in tracking the record of training which has been

imparted to the employees by maintaining the training register. The training of

employees is considered as one of the obligations on credit licensees.

/2

(g) Explain APRA’s current attitude towards bank lending for investment properties.

Mark

The Australian Prudential Regulation Authority has introduced restrictions which has

created impact on the bank lending for investment purposes. The banks attitude to the

APRA changes includes

1. changing in the serviceability requirements for the investor loans.

2. Creating difficultly for investors in seeking financial assistance.

3. The borrowing capacity has been downsized, charges high interest rates and

repayments of existing debt are assessed at higher rate.

/2

Sub-total /

10

Continued

Task 1: Identify and Interpret Compliance Requirements Continued

1.2

Interpret,

analyse

and

prioritise

identified

complian

ce

requirem

ents

Some of the compliance requirements are difficult to meet. Unfortunately, also there

have been some ‘rogue’ mortgage brokers who have failed to comply – to the

disadvantage of their clients.

The finance planning industry has been plagued by non-compliance in the largest

planning groups, with the image of the industry being substantially tarnished as a

result. It may not suffer greatly because of the absence of an alternative source of

financial advice.

This is not so with mortgage brokers. They are just establishing their reputation and

consumers always have alternative of going to the lenders directly.

(a) Select three tasks you perform on a regular basis that are subject to compliance requirements.

No Mark

1. Finding lender institution. /1

2. Completing the loan application. /1

3. Submission of the loan application to the bank & getting approval of it. /1

(b) Identify the compliance requirements that are relevant to the three tasks selected, indicating the

name of the relevant legislation, regulation or code of conduct.

No

1. Australian Consumer Law /1

2. ASIC /1

3. The National Consumer Credit Protection Act 2009 /1

Mark

The Australian Prudential Regulation Authority has introduced restrictions which has

created impact on the bank lending for investment purposes. The banks attitude to the

APRA changes includes

1. changing in the serviceability requirements for the investor loans.

2. Creating difficultly for investors in seeking financial assistance.

3. The borrowing capacity has been downsized, charges high interest rates and

repayments of existing debt are assessed at higher rate.

/2

Sub-total /

10

Continued

Task 1: Identify and Interpret Compliance Requirements Continued

1.2

Interpret,

analyse

and

prioritise

identified

complian

ce

requirem

ents

Some of the compliance requirements are difficult to meet. Unfortunately, also there

have been some ‘rogue’ mortgage brokers who have failed to comply – to the

disadvantage of their clients.

The finance planning industry has been plagued by non-compliance in the largest

planning groups, with the image of the industry being substantially tarnished as a

result. It may not suffer greatly because of the absence of an alternative source of

financial advice.

This is not so with mortgage brokers. They are just establishing their reputation and

consumers always have alternative of going to the lenders directly.

(a) Select three tasks you perform on a regular basis that are subject to compliance requirements.

No Mark

1. Finding lender institution. /1

2. Completing the loan application. /1

3. Submission of the loan application to the bank & getting approval of it. /1

(b) Identify the compliance requirements that are relevant to the three tasks selected, indicating the

name of the relevant legislation, regulation or code of conduct.

No

1. Australian Consumer Law /1

2. ASIC /1

3. The National Consumer Credit Protection Act 2009 /1

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

(c) How does your organisation monitor your compliance?

Mark

The business organisation should always ensures the compliance of its applicable rules and

regulations in the following manner:

1. By monitoring the pre activity approvals lists or transaction checklist with capturing

of data or relevant information. For effective monitoring of business operations'

compliance, company should gather or collect data and evaluates the factors which

is leading to non compliance.

2. Company should have a proper and effective internal control system which can

rapidly provide solutions and remedies to those risk or issues which have been

identified related to the breach of laws or leading to non compliance of rules and

regulations.

3. Company should make sound and effective plan and strategies to monitor and

evaluate whether the company is complying with its applicable norms or not.

/2

Sub-total /8

Total /27

Task 2: Deliver and Monitor a Service to Customers

2.

Identify

customer

needs

The relationship with a client is generally described as beginning with the

establishment of empathy. In other words, it is first necessary for a mortgage broker

to establish that he / she is truly interested in the client and the client’s needs. It is

only after that that the mortgage broker has established the right to interview a

client.

(a) Use the internet or any other source to find a definition of empathy.

Mark

The word Empathy basically means the ability or skill of understanding, identifying as

well as sharing the feelings of another. Empathy is considered as the ability of sensing or

determining the emotions and feelings of the other people. This process is coupled with

the ability to imagine what other might be thinking or feeling. Thus, empathy is the

capacity to understand, determine or feel what another person is experiencing from a

given frame of reference by placing oneself into the another position. The types of

empathy include cognitive empathy, emotional empathy and somatic empathy.

/1

(b) List three open-ended questions that assist in developing empathy with a client? How do such

questions indicate empathy?

No. Mark

1. How do you deal or overcome with the negative emotions arising?

2. Where do you experience more positivity or feel most present ? And what

other understands about you ?

3. What things in other motivates or encourages you the most ?

/2

Mark

The business organisation should always ensures the compliance of its applicable rules and

regulations in the following manner:

1. By monitoring the pre activity approvals lists or transaction checklist with capturing

of data or relevant information. For effective monitoring of business operations'

compliance, company should gather or collect data and evaluates the factors which

is leading to non compliance.

2. Company should have a proper and effective internal control system which can

rapidly provide solutions and remedies to those risk or issues which have been

identified related to the breach of laws or leading to non compliance of rules and

regulations.

3. Company should make sound and effective plan and strategies to monitor and

evaluate whether the company is complying with its applicable norms or not.

/2

Sub-total /8

Total /27

Task 2: Deliver and Monitor a Service to Customers

2.

Identify

customer

needs

The relationship with a client is generally described as beginning with the

establishment of empathy. In other words, it is first necessary for a mortgage broker

to establish that he / she is truly interested in the client and the client’s needs. It is

only after that that the mortgage broker has established the right to interview a

client.

(a) Use the internet or any other source to find a definition of empathy.

Mark

The word Empathy basically means the ability or skill of understanding, identifying as

well as sharing the feelings of another. Empathy is considered as the ability of sensing or

determining the emotions and feelings of the other people. This process is coupled with

the ability to imagine what other might be thinking or feeling. Thus, empathy is the

capacity to understand, determine or feel what another person is experiencing from a

given frame of reference by placing oneself into the another position. The types of

empathy include cognitive empathy, emotional empathy and somatic empathy.

/1

(b) List three open-ended questions that assist in developing empathy with a client? How do such

questions indicate empathy?

No. Mark

1. How do you deal or overcome with the negative emotions arising?

2. Where do you experience more positivity or feel most present ? And what

other understands about you ?

3. What things in other motivates or encourages you the most ?

/2

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

The above questionnaire is designed in the open ended form so as to encourage the

full as well as meaningful answer by making use of the own knowledge related to

the subject matter and feelings.

/1

(c) List and explain the steps involved in an ‘active listening approach’.

Mark

A Good listener is a person who is interested in the listening about what is going in

the lives of other people, their hobbies or any other life related activities to them.

The attention of person goes there who says or do something in an attentive

manner.

1

The steps involved in an active listening approach are as follows:

1. Hearing - At this stage listener always pays attention by making eye contact to

make sure proper hearing of the words being said by other.

2. Interpretation – What words has been heard, always make sure correct and

relevant interpretation is done so as to ensure that there is no misunderstanding or

confusion related to basic meanings.

/1

3. Evaluation – After making interpretation, the evaluation has to be made by deciding

what to do with the available information and data on receiving it.

4. Respond - The final stage of listening is to give either a verbal or visual response to the

speaker so as to confirm that information has been understood which has been said by

them.

/1

(d) How is client service commonly monitored in your organisation? What are the two possible

outcomes?

No

.

Mark

1. The client service in a business organisation can be monitored with the help of

following mechanisms:

By capturing customer feedback channels and scheduling meetings on weekly basis

with the customer service staff.

/1

2. BY conducting such process, company is able to assess its service quality and

demand for its product among customer and in the market as well. It will help

company in measuring its performance as well as profitability level and measures it

any, to required to be taken for improving the business operations. This will help in

framing budget and different business strategies and plans which will work towards

attainment of organizational goals and objectives.

/2

Sub-total /10

Continued

Task 2: Deliver and Monitor a Service to Customers Continued

full as well as meaningful answer by making use of the own knowledge related to

the subject matter and feelings.

/1

(c) List and explain the steps involved in an ‘active listening approach’.

Mark

A Good listener is a person who is interested in the listening about what is going in

the lives of other people, their hobbies or any other life related activities to them.

The attention of person goes there who says or do something in an attentive

manner.

1

The steps involved in an active listening approach are as follows:

1. Hearing - At this stage listener always pays attention by making eye contact to

make sure proper hearing of the words being said by other.

2. Interpretation – What words has been heard, always make sure correct and

relevant interpretation is done so as to ensure that there is no misunderstanding or

confusion related to basic meanings.

/1

3. Evaluation – After making interpretation, the evaluation has to be made by deciding

what to do with the available information and data on receiving it.

4. Respond - The final stage of listening is to give either a verbal or visual response to the

speaker so as to confirm that information has been understood which has been said by

them.

/1

(d) How is client service commonly monitored in your organisation? What are the two possible

outcomes?

No

.

Mark

1. The client service in a business organisation can be monitored with the help of

following mechanisms:

By capturing customer feedback channels and scheduling meetings on weekly basis

with the customer service staff.

/1

2. BY conducting such process, company is able to assess its service quality and

demand for its product among customer and in the market as well. It will help

company in measuring its performance as well as profitability level and measures it

any, to required to be taken for improving the business operations. This will help in

framing budget and different business strategies and plans which will work towards

attainment of organizational goals and objectives.

/2

Sub-total /10

Continued

Task 2: Deliver and Monitor a Service to Customers Continued

2.1

Deliver a

service to

customer

s

In a survey on the reasons for referrals conducted by David Maister, only 10%

were due to the quality of technical work. The remaining 90% of referrals were due

to the quality of service.

This indicates that the key to maintaining client relationships and gaining referrals

is the provision of outstanding service. This has been described by Maister as

‘over-servicing’.

(a) Describe three ways in which a mortgage broking organisation can attempt to ‘overservice’

clients?

No. Mark

1. Asking the clients for more often time an on the situation of scope creep, the cost

of project is required to be renegotiated.

/1

2. Investing in the business tools and automation like job management solutions,

benchmarks etc. which will help in tracking and monitoring the results.

/1

3. On opportunity showcasing work efforts, then it is better to invest time by

entering into the industry awards.

/1

(b) How would you keep a client informed about the progress of an application as it passed through

a creditor provider’s hands? What approximate timing might be involved?

No. Mark

1. After submission of the Loan application to lender, the mortgage broker is once

again involved for ensuring the product being offered by the lender is complying

with all the requirements of the clients. Mortgage brokers should have contact

with the client and are responsible for breaches of lending provisions of the

NCCP Act.

Mortgage broker is also required to prepare the client or borrowers with the

contract so that they can understand their obligations relating to repayments and

conditions of late repayment, redraw facilities and all late fees and brokerage that

will be applied.

/2

2. The time period between client assessment and forwarding of the loan application

to the credit provider should not be longer than two days. It is important that the

information should be passed on to the credit provider in a timely manner.

/2

(c) Describe how you might attempt to resolve conflicts with clients.

Mark

Conflicts with clients is one of the factor which can leads to deterioration of the business

operations. The first most step in resolving conflict is to ascertain or having a deep

knowledge of the basic reason of conflict taking place. Once the reason is determined,

measures related to how to handle and resolve conflict are

made. This measures helps business organisation in making an ideal place for client to

work with. By having sound business strategies and plans related to conflict reduction

/2

Deliver a

service to

customer

s

In a survey on the reasons for referrals conducted by David Maister, only 10%

were due to the quality of technical work. The remaining 90% of referrals were due

to the quality of service.

This indicates that the key to maintaining client relationships and gaining referrals

is the provision of outstanding service. This has been described by Maister as

‘over-servicing’.

(a) Describe three ways in which a mortgage broking organisation can attempt to ‘overservice’

clients?

No. Mark

1. Asking the clients for more often time an on the situation of scope creep, the cost

of project is required to be renegotiated.

/1

2. Investing in the business tools and automation like job management solutions,

benchmarks etc. which will help in tracking and monitoring the results.

/1

3. On opportunity showcasing work efforts, then it is better to invest time by

entering into the industry awards.

/1

(b) How would you keep a client informed about the progress of an application as it passed through

a creditor provider’s hands? What approximate timing might be involved?

No. Mark

1. After submission of the Loan application to lender, the mortgage broker is once

again involved for ensuring the product being offered by the lender is complying

with all the requirements of the clients. Mortgage brokers should have contact

with the client and are responsible for breaches of lending provisions of the

NCCP Act.

Mortgage broker is also required to prepare the client or borrowers with the

contract so that they can understand their obligations relating to repayments and

conditions of late repayment, redraw facilities and all late fees and brokerage that

will be applied.

/2

2. The time period between client assessment and forwarding of the loan application

to the credit provider should not be longer than two days. It is important that the

information should be passed on to the credit provider in a timely manner.

/2

(c) Describe how you might attempt to resolve conflicts with clients.

Mark

Conflicts with clients is one of the factor which can leads to deterioration of the business

operations. The first most step in resolving conflict is to ascertain or having a deep

knowledge of the basic reason of conflict taking place. Once the reason is determined,

measures related to how to handle and resolve conflict are

made. This measures helps business organisation in making an ideal place for client to

work with. By having sound business strategies and plans related to conflict reduction

/2

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

will produce greater satisfaction among clients and employees. It will also lead to

improvement in performance and increase in profitability level.

(d) How do you can prepare clients for the hiccups that can happen while their credit application is

being processed.

Mark

Clients can be prepared by providing details of interim updates. Do not ask the borrower

to provide unnecessary information which is not strictly relevant or which the lender

already has in its possession.

/2

Sub-total /11

Continued

(e) The chapter on Operating a Mortgage Broking Business contains an example suggesting that a

mortgage broker acting in the best interests of clients should act as a Protector rather than an

Expert. What are the implications for this in regard to (i) advice given to clients and (ii)

recommending the most suitable loan products?.

No. Mark

1. New products can be introduced from time to time, changes in the existing

products features can be made. Mortgage brokers should be aware of information

regarding change from product providers with information being shared by

conducting team meetings, seminars etc.

/2

2. The mortgage brokers should also be prepared to discuss the different products

with their clients and point out their different features so that an informed choice

can be made.

/2

(f) How could you prepare yourself to deal with client concerns?

Mark

For dealing with the concern or issues of client, one should adopt following ways for

overcoming these issues and making client satisfied:

1. Understanding the scope of client project and defining the time frames for

completion of such projects.

2. Meeting clients expectations by rendering of quality services as per the budgeted

amount and resources.

3. Making clear about the cost associated with the project and its schedule and

deciding the time period for making payment.

4. Assessing the problem which is causing the project conflicts and hampering the

interest of client. After making assessment of the problem, professional response in

form of clear and proper course of action should be given for overcoming such

/2

improvement in performance and increase in profitability level.

(d) How do you can prepare clients for the hiccups that can happen while their credit application is

being processed.

Mark

Clients can be prepared by providing details of interim updates. Do not ask the borrower

to provide unnecessary information which is not strictly relevant or which the lender

already has in its possession.

/2

Sub-total /11

Continued

(e) The chapter on Operating a Mortgage Broking Business contains an example suggesting that a

mortgage broker acting in the best interests of clients should act as a Protector rather than an

Expert. What are the implications for this in regard to (i) advice given to clients and (ii)

recommending the most suitable loan products?.

No. Mark

1. New products can be introduced from time to time, changes in the existing

products features can be made. Mortgage brokers should be aware of information

regarding change from product providers with information being shared by

conducting team meetings, seminars etc.

/2

2. The mortgage brokers should also be prepared to discuss the different products

with their clients and point out their different features so that an informed choice

can be made.

/2

(f) How could you prepare yourself to deal with client concerns?

Mark

For dealing with the concern or issues of client, one should adopt following ways for

overcoming these issues and making client satisfied:

1. Understanding the scope of client project and defining the time frames for

completion of such projects.

2. Meeting clients expectations by rendering of quality services as per the budgeted

amount and resources.

3. Making clear about the cost associated with the project and its schedule and

deciding the time period for making payment.

4. Assessing the problem which is causing the project conflicts and hampering the

interest of client. After making assessment of the problem, professional response in

form of clear and proper course of action should be given for overcoming such

/2

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

problem and making client satisfied.

(g) Give examples of the following legal breaches: breach of the duty of care, false and misleading

conduct, unconscionable conduct & conflict of interest without disclosure.

No. Mark

1. Breach of duty of care example - THE COMMONWEALTH v. VERWAYEN.

In this case, where the Commonwealth had been in breach of its duty of

care as a result the ship sunk due to negligence. The Commonwealth was

liable for the accident.

/1

2. Breach of duty of false and misleading conduct - In Barnes v Forty Two

International Pty Ltd. In this case, the respondents claim for the false, misleading

and deceptive conduct which was based solely on the fact that the appellants had

made two specific false representations.

/1

3. Breach of duty of unconscionable conduct - Harsh Loan Contract

In the James v. National Financial, LLC, C.A. case, a woman was given the loan

with the interest of 800%. She sued the lender on the grounds that the loan contract

was unconscionable. In its 2016 ruling, the Delaware Court of Chancery assessed

that the loan contract was null and void because it was unconscionable.

/1

4. Breach of duty of conflict of interest without disclosure - In Duke Group Ltd v

Pilmer, the Full Court of the South Australian Supreme Court has attempted to

identify in analogous situations the recurring underlying features of fiduciary

relationships. Among all the issues, one of the issue in the case was whether a firm

of chartered accountants owed fiduciary obligations against their client in some

dealings that the parties had.

/1

(h) Once a desirable market segment has been identified, a mortgage broking business can put its

mind on developing suitable marketing strategies. List examples of different strategies that

might be used.

Mark

Some of the marketing strategies that can help a mortgage broking business are as follows:

1. Make use of social media platform, as it provides the opportunity to connect with

new potential clients. It is a great way to show knowledge as a mortgage broker,

building brand awareness, answer client questions etc.

2. By making mortgage broker services different from other will increase

mortgage broker sales. One way to grab positive attention towards business and

attract new clients is to get referrals.

3. Creating personalised mortgage broker campaigns for each clients will helps in

building clients loyalty and engagement. By using marketing automation, emails

automatically go to each client as per their own needs and preferences this saves

time.

/2

(g) Give examples of the following legal breaches: breach of the duty of care, false and misleading

conduct, unconscionable conduct & conflict of interest without disclosure.

No. Mark

1. Breach of duty of care example - THE COMMONWEALTH v. VERWAYEN.

In this case, where the Commonwealth had been in breach of its duty of

care as a result the ship sunk due to negligence. The Commonwealth was

liable for the accident.

/1

2. Breach of duty of false and misleading conduct - In Barnes v Forty Two

International Pty Ltd. In this case, the respondents claim for the false, misleading

and deceptive conduct which was based solely on the fact that the appellants had

made two specific false representations.

/1

3. Breach of duty of unconscionable conduct - Harsh Loan Contract

In the James v. National Financial, LLC, C.A. case, a woman was given the loan

with the interest of 800%. She sued the lender on the grounds that the loan contract

was unconscionable. In its 2016 ruling, the Delaware Court of Chancery assessed

that the loan contract was null and void because it was unconscionable.

/1

4. Breach of duty of conflict of interest without disclosure - In Duke Group Ltd v

Pilmer, the Full Court of the South Australian Supreme Court has attempted to

identify in analogous situations the recurring underlying features of fiduciary

relationships. Among all the issues, one of the issue in the case was whether a firm

of chartered accountants owed fiduciary obligations against their client in some

dealings that the parties had.

/1

(h) Once a desirable market segment has been identified, a mortgage broking business can put its

mind on developing suitable marketing strategies. List examples of different strategies that

might be used.

Mark

Some of the marketing strategies that can help a mortgage broking business are as follows:

1. Make use of social media platform, as it provides the opportunity to connect with

new potential clients. It is a great way to show knowledge as a mortgage broker,

building brand awareness, answer client questions etc.

2. By making mortgage broker services different from other will increase

mortgage broker sales. One way to grab positive attention towards business and

attract new clients is to get referrals.

3. Creating personalised mortgage broker campaigns for each clients will helps in

building clients loyalty and engagement. By using marketing automation, emails

automatically go to each client as per their own needs and preferences this saves

time.

/2

Sub-total /12

Continued

(i) What steps can be taken to keep up to date with product changes and ensure that this knowledge

is properly disseminated?

Mark

Company should make proper business strategies and plans related to the promotion and

advertisement of their newly launched products ad services in the market so as to grab the

attention of its customers towards it. Company should indulge itself in publicity campaign,

hoardings, make use of social media platforms, advertisement in newspaper, articles

related to changes made in product. With the helps of this, customers will be aware about

changes made I products. Also, company should focus on the labelling, designing and

packaging process of its product as this helps in seeking more customer attraction.

/2

(j) What are the procedures for dealing with client complaints in your organisation?

Mark

Every company or business organization should pay attention towards the customer needs

and preferences for making them satisfied. As customer or clients are considered as one of

the most important key for business success. Resolving clients problems timely will help in

customer retention with the company. The procedures for dealing with clients complaints in

business organization are as follows:

1. Listen and understand compliant or grievance by inviting it - Always listen to

the customer or client by taking time and understanding their concern as they are

concerned about services.

2. Empathize – After listening empathize with client position so as to create bond &

let them know that their concern & issue are going to resolve soon.

3. Offer a solution – Solution as per the client issues and complaints is drive

accordingly in a very cost effective manner and timely

4. Execution of Solution and Follow up – Once the solution is made to their problem

as per their need, execute t for checking accuracy. After executing timely follow up

should be taken to assess any error face.

/2

(k) What normal protocols should for protecting the confidentiality of client files?

Mark

The protocol used by company for protecting the confidentiality of client files are as

follows:

1. Document Security – Because of technological advancements document security

has becomes big issue nowadays. Technology has come up with some benefits and

drawbacks as well. Keeping clients’ files in safe cabinet, making use of the

shredding machine etc helps in document security.

2. Data Security - Client’s data is at risk during normal business time especially when

/2

Continued

(i) What steps can be taken to keep up to date with product changes and ensure that this knowledge

is properly disseminated?

Mark

Company should make proper business strategies and plans related to the promotion and

advertisement of their newly launched products ad services in the market so as to grab the

attention of its customers towards it. Company should indulge itself in publicity campaign,

hoardings, make use of social media platforms, advertisement in newspaper, articles

related to changes made in product. With the helps of this, customers will be aware about

changes made I products. Also, company should focus on the labelling, designing and

packaging process of its product as this helps in seeking more customer attraction.

/2

(j) What are the procedures for dealing with client complaints in your organisation?

Mark

Every company or business organization should pay attention towards the customer needs

and preferences for making them satisfied. As customer or clients are considered as one of

the most important key for business success. Resolving clients problems timely will help in

customer retention with the company. The procedures for dealing with clients complaints in

business organization are as follows:

1. Listen and understand compliant or grievance by inviting it - Always listen to

the customer or client by taking time and understanding their concern as they are

concerned about services.

2. Empathize – After listening empathize with client position so as to create bond &

let them know that their concern & issue are going to resolve soon.

3. Offer a solution – Solution as per the client issues and complaints is drive

accordingly in a very cost effective manner and timely

4. Execution of Solution and Follow up – Once the solution is made to their problem

as per their need, execute t for checking accuracy. After executing timely follow up

should be taken to assess any error face.

/2

(k) What normal protocols should for protecting the confidentiality of client files?

Mark

The protocol used by company for protecting the confidentiality of client files are as

follows:

1. Document Security – Because of technological advancements document security

has becomes big issue nowadays. Technology has come up with some benefits and

drawbacks as well. Keeping clients’ files in safe cabinet, making use of the

shredding machine etc helps in document security.

2. Data Security - Client’s data is at risk during normal business time especially when

/2

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 48

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.