Limitations of Relying on Financial Ratios

VerifiedAdded on 2022/09/08

|22

|4277

|21

AI Summary

Contribute Materials

Your contribution can guide someone’s learning journey. Share your

documents today.

Running head: FINANCE PORTFOLIO MANAGEMENT

Finance Portfolio Management

Name of the Student

Name of the University

Author’s Note

Finance Portfolio Management

Name of the Student

Name of the University

Author’s Note

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

1FINANCE PORTFOLIO MANAGEMENT

Table of Contents

Portfolio 1...................................................................................................................................2

Introduction............................................................................................................................2

a) Calculation of Ratios..........................................................................................................2

b) Analysis of Performance, Financial Position and Investment Potential............................4

Analysis of Ratios..............................................................................................................4

Analysis of Audited Financial Statements.......................................................................10

c) Recommendations............................................................................................................11

d) Limitations of Relying on Financial Ratios to Interpret Company’s Performance.........12

Conclusion............................................................................................................................13

Portfolio 2.................................................................................................................................15

a) Advise to the Senior Management on the Selection of Project........................................15

b) Limitations of Investment Appraisal Techniques in Long-Term Decision Making........17

References................................................................................................................................19

Table of Contents

Portfolio 1...................................................................................................................................2

Introduction............................................................................................................................2

a) Calculation of Ratios..........................................................................................................2

b) Analysis of Performance, Financial Position and Investment Potential............................4

Analysis of Ratios..............................................................................................................4

Analysis of Audited Financial Statements.......................................................................10

c) Recommendations............................................................................................................11

d) Limitations of Relying on Financial Ratios to Interpret Company’s Performance.........12

Conclusion............................................................................................................................13

Portfolio 2.................................................................................................................................15

a) Advise to the Senior Management on the Selection of Project........................................15

b) Limitations of Investment Appraisal Techniques in Long-Term Decision Making........17

References................................................................................................................................19

2FINANCE PORTFOLIO MANAGEMENT

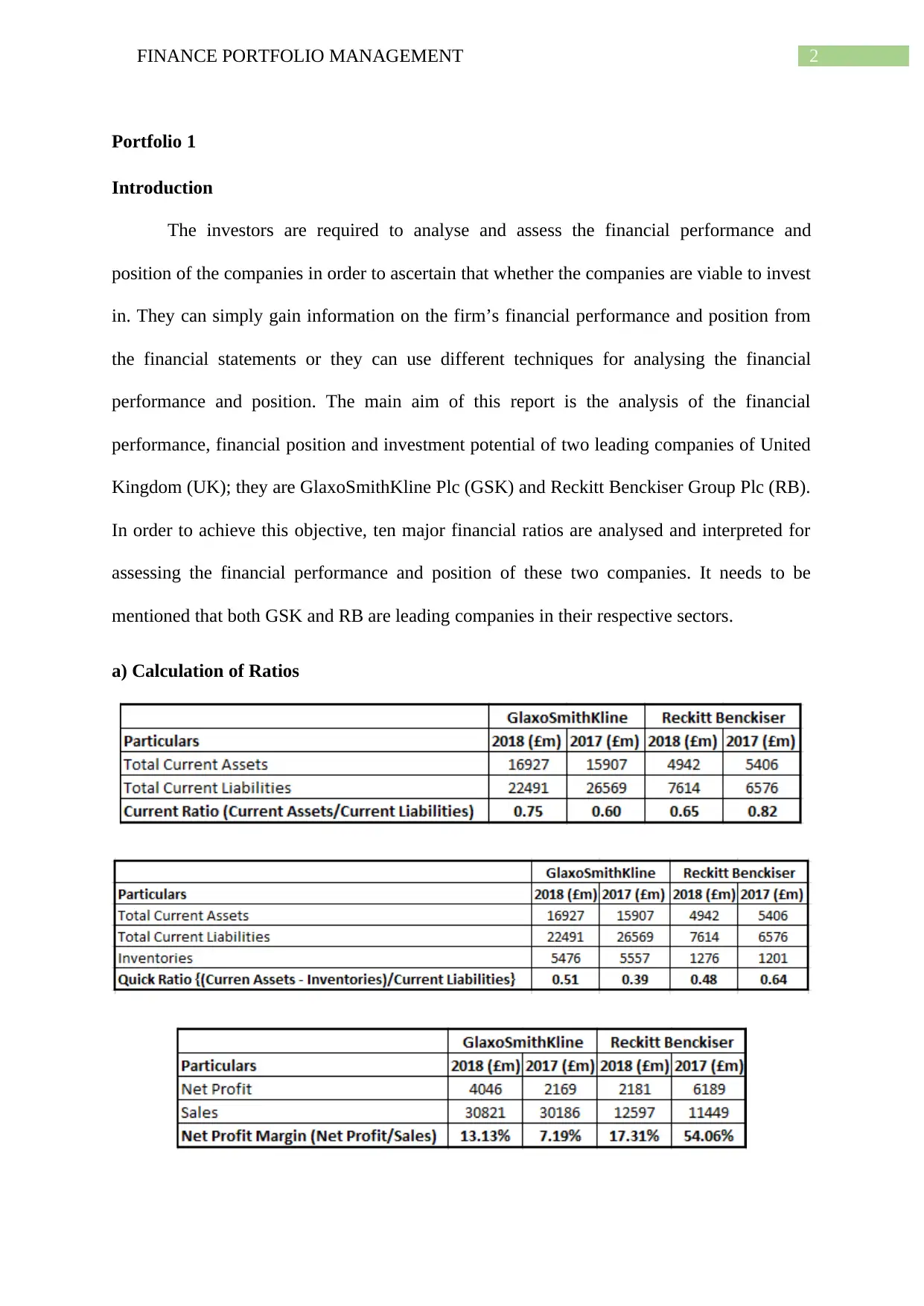

Portfolio 1

Introduction

The investors are required to analyse and assess the financial performance and

position of the companies in order to ascertain that whether the companies are viable to invest

in. They can simply gain information on the firm’s financial performance and position from

the financial statements or they can use different techniques for analysing the financial

performance and position. The main aim of this report is the analysis of the financial

performance, financial position and investment potential of two leading companies of United

Kingdom (UK); they are GlaxoSmithKline Plc (GSK) and Reckitt Benckiser Group Plc (RB).

In order to achieve this objective, ten major financial ratios are analysed and interpreted for

assessing the financial performance and position of these two companies. It needs to be

mentioned that both GSK and RB are leading companies in their respective sectors.

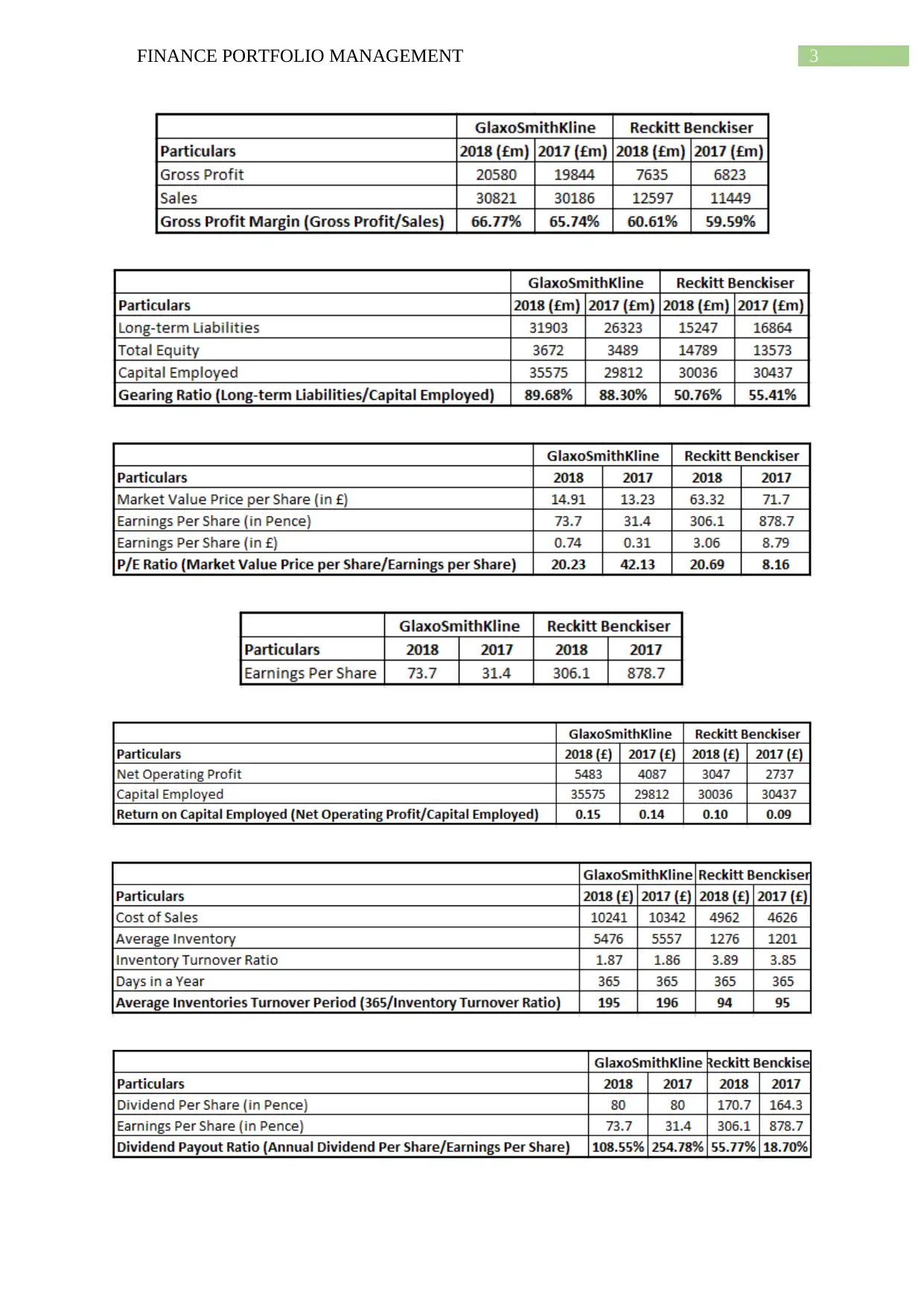

a) Calculation of Ratios

Portfolio 1

Introduction

The investors are required to analyse and assess the financial performance and

position of the companies in order to ascertain that whether the companies are viable to invest

in. They can simply gain information on the firm’s financial performance and position from

the financial statements or they can use different techniques for analysing the financial

performance and position. The main aim of this report is the analysis of the financial

performance, financial position and investment potential of two leading companies of United

Kingdom (UK); they are GlaxoSmithKline Plc (GSK) and Reckitt Benckiser Group Plc (RB).

In order to achieve this objective, ten major financial ratios are analysed and interpreted for

assessing the financial performance and position of these two companies. It needs to be

mentioned that both GSK and RB are leading companies in their respective sectors.

a) Calculation of Ratios

3FINANCE PORTFOLIO MANAGEMENT

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

4FINANCE PORTFOLIO MANAGEMENT

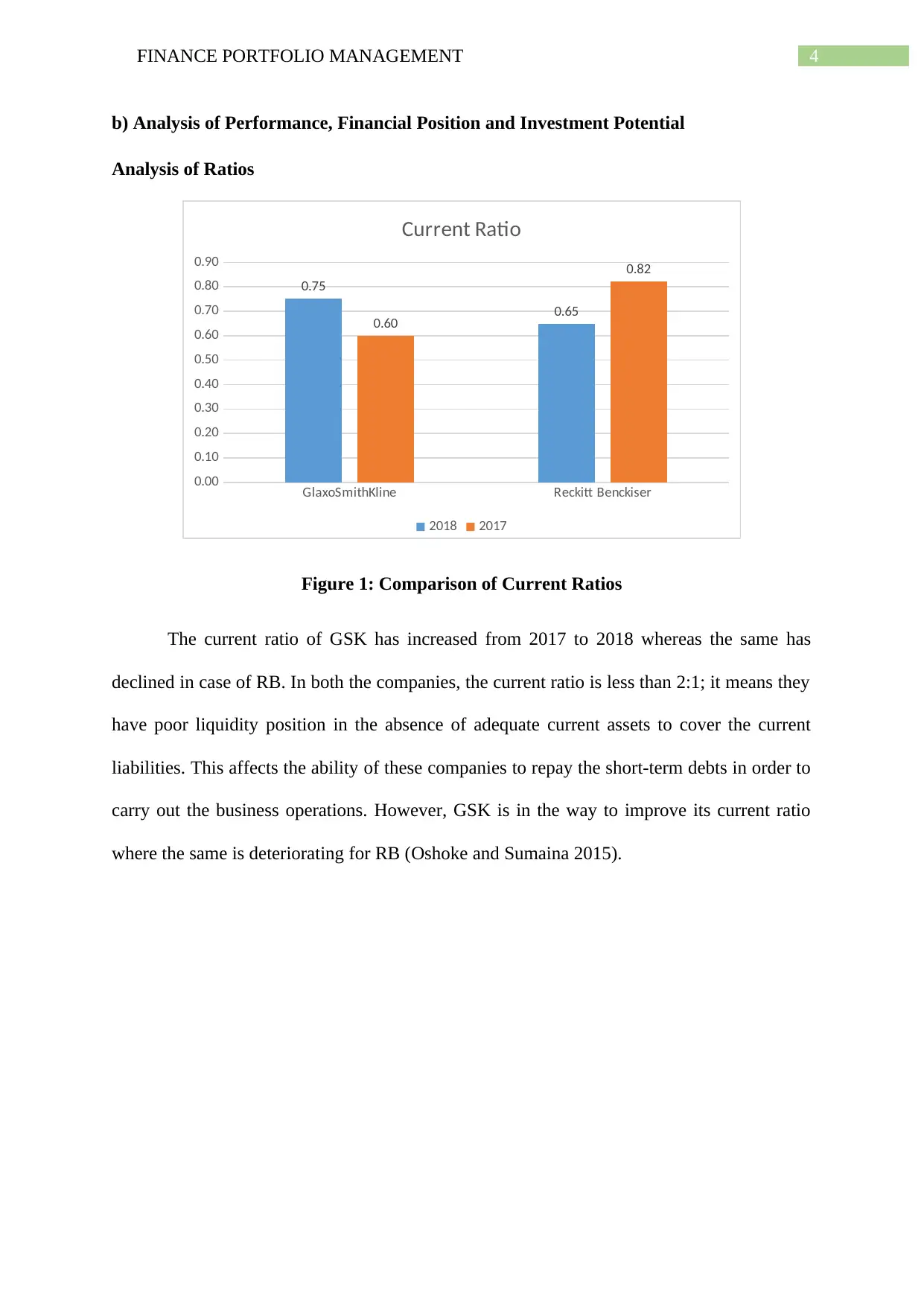

b) Analysis of Performance, Financial Position and Investment Potential

Analysis of Ratios

GlaxoSmithKline Reckitt Benckiser

0.00

0.10

0.20

0.30

0.40

0.50

0.60

0.70

0.80

0.90

0.75

0.65

0.60

0.82

Current Ratio

2018 2017

Figure 1: Comparison of Current Ratios

The current ratio of GSK has increased from 2017 to 2018 whereas the same has

declined in case of RB. In both the companies, the current ratio is less than 2:1; it means they

have poor liquidity position in the absence of adequate current assets to cover the current

liabilities. This affects the ability of these companies to repay the short-term debts in order to

carry out the business operations. However, GSK is in the way to improve its current ratio

where the same is deteriorating for RB (Oshoke and Sumaina 2015).

b) Analysis of Performance, Financial Position and Investment Potential

Analysis of Ratios

GlaxoSmithKline Reckitt Benckiser

0.00

0.10

0.20

0.30

0.40

0.50

0.60

0.70

0.80

0.90

0.75

0.65

0.60

0.82

Current Ratio

2018 2017

Figure 1: Comparison of Current Ratios

The current ratio of GSK has increased from 2017 to 2018 whereas the same has

declined in case of RB. In both the companies, the current ratio is less than 2:1; it means they

have poor liquidity position in the absence of adequate current assets to cover the current

liabilities. This affects the ability of these companies to repay the short-term debts in order to

carry out the business operations. However, GSK is in the way to improve its current ratio

where the same is deteriorating for RB (Oshoke and Sumaina 2015).

5FINANCE PORTFOLIO MANAGEMENT

GlaxoSmithKline Reckitt Benckiser

0.00

0.10

0.20

0.30

0.40

0.50

0.60

0.70

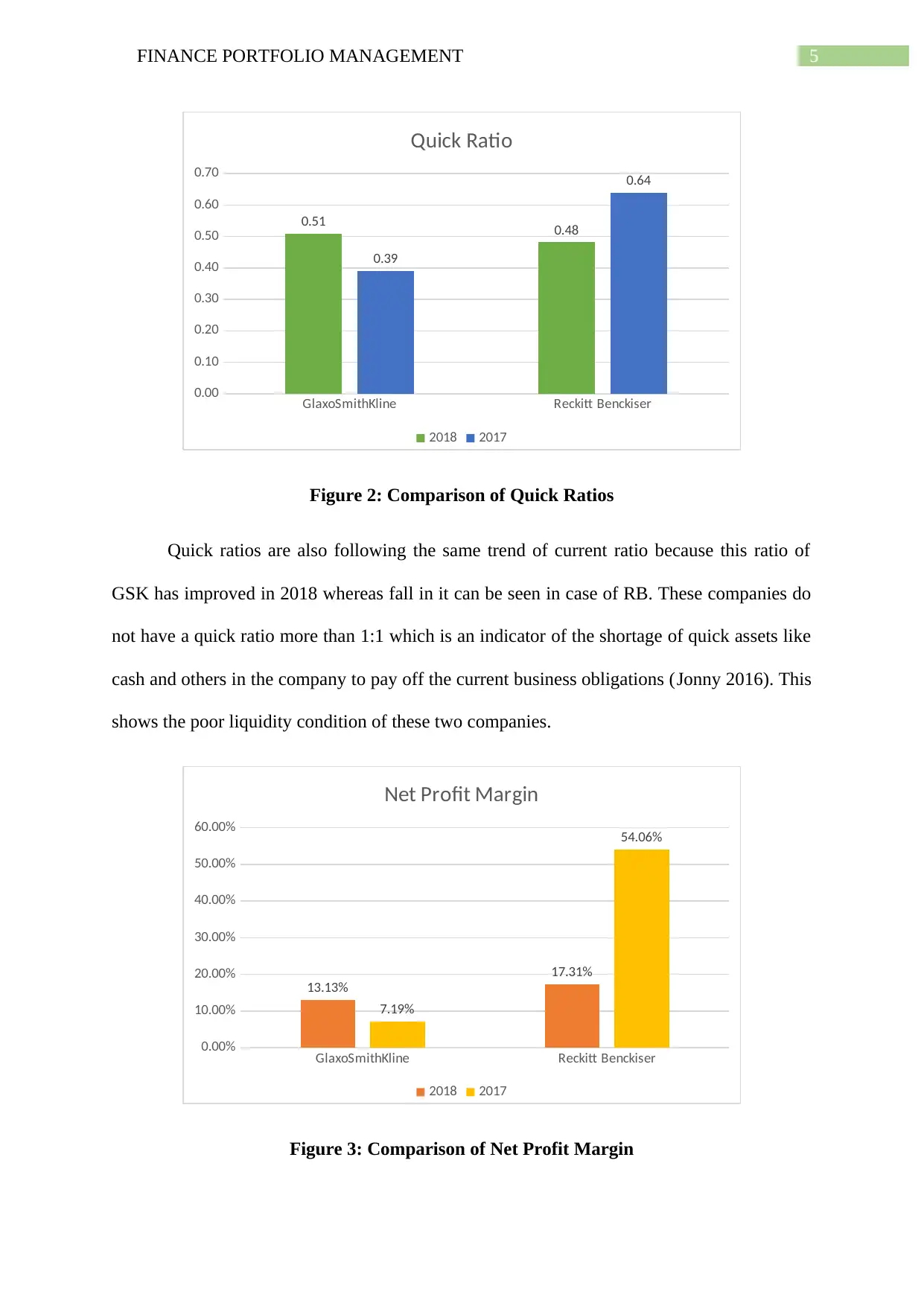

0.51 0.48

0.39

0.64

Quick Ratio

2018 2017

Figure 2: Comparison of Quick Ratios

Quick ratios are also following the same trend of current ratio because this ratio of

GSK has improved in 2018 whereas fall in it can be seen in case of RB. These companies do

not have a quick ratio more than 1:1 which is an indicator of the shortage of quick assets like

cash and others in the company to pay off the current business obligations (Jonny 2016). This

shows the poor liquidity condition of these two companies.

GlaxoSmithKline Reckitt Benckiser

0.00%

10.00%

20.00%

30.00%

40.00%

50.00%

60.00%

13.13%

17.31%

7.19%

54.06%

Net Profit Margin

2018 2017

Figure 3: Comparison of Net Profit Margin

GlaxoSmithKline Reckitt Benckiser

0.00

0.10

0.20

0.30

0.40

0.50

0.60

0.70

0.51 0.48

0.39

0.64

Quick Ratio

2018 2017

Figure 2: Comparison of Quick Ratios

Quick ratios are also following the same trend of current ratio because this ratio of

GSK has improved in 2018 whereas fall in it can be seen in case of RB. These companies do

not have a quick ratio more than 1:1 which is an indicator of the shortage of quick assets like

cash and others in the company to pay off the current business obligations (Jonny 2016). This

shows the poor liquidity condition of these two companies.

GlaxoSmithKline Reckitt Benckiser

0.00%

10.00%

20.00%

30.00%

40.00%

50.00%

60.00%

13.13%

17.31%

7.19%

54.06%

Net Profit Margin

2018 2017

Figure 3: Comparison of Net Profit Margin

6FINANCE PORTFOLIO MANAGEMENT

There is a growth in the net profit margin of GSK, but a large fall in this ratio can be

seen in case of RB. This shows effective financial performance of GSK as the company has

increased its sales while decreased its overall direct and indirect expenses. In case of RB, the

main reason for this large fall in this ratio can be the increase in direct and indirect expenses

(Reynolds et al.2013).

GlaxoSmithKline Reckitt Benckiser

56.00%

58.00%

60.00%

62.00%

64.00%

66.00%

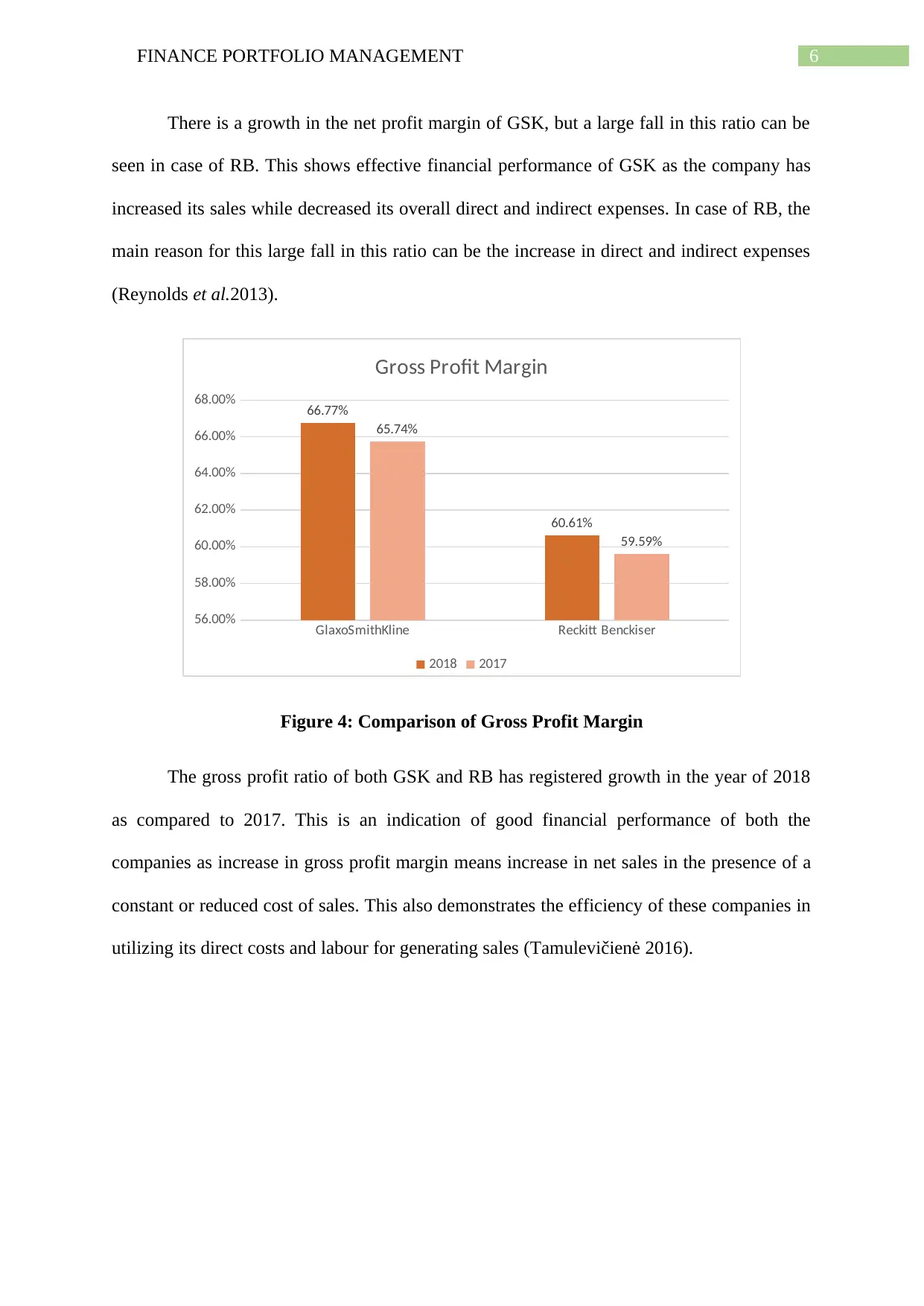

68.00% 66.77%

60.61%

65.74%

59.59%

Gross Profit Margin

2018 2017

Figure 4: Comparison of Gross Profit Margin

The gross profit ratio of both GSK and RB has registered growth in the year of 2018

as compared to 2017. This is an indication of good financial performance of both the

companies as increase in gross profit margin means increase in net sales in the presence of a

constant or reduced cost of sales. This also demonstrates the efficiency of these companies in

utilizing its direct costs and labour for generating sales (Tamulevičienė 2016).

There is a growth in the net profit margin of GSK, but a large fall in this ratio can be

seen in case of RB. This shows effective financial performance of GSK as the company has

increased its sales while decreased its overall direct and indirect expenses. In case of RB, the

main reason for this large fall in this ratio can be the increase in direct and indirect expenses

(Reynolds et al.2013).

GlaxoSmithKline Reckitt Benckiser

56.00%

58.00%

60.00%

62.00%

64.00%

66.00%

68.00% 66.77%

60.61%

65.74%

59.59%

Gross Profit Margin

2018 2017

Figure 4: Comparison of Gross Profit Margin

The gross profit ratio of both GSK and RB has registered growth in the year of 2018

as compared to 2017. This is an indication of good financial performance of both the

companies as increase in gross profit margin means increase in net sales in the presence of a

constant or reduced cost of sales. This also demonstrates the efficiency of these companies in

utilizing its direct costs and labour for generating sales (Tamulevičienė 2016).

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

7FINANCE PORTFOLIO MANAGEMENT

GlaxoSmithKline Reckitt Benckiser

0.00%

10.00%

20.00%

30.00%

40.00%

50.00%

60.00%

70.00%

80.00%

90.00%

100.00% 89.68%

50.76%

88.30%

55.41%

Gearing Ratio

2018 2017

Figure 5: Comparison of Gearing Ratios

There is a minor increase in the gearing ratio of GSK in 2018, but the same ratio of

RB has witnessed a fall in 2018 as compared to 2017. In both these companies, this ratio is

more than 50% that makes these companies highly geared. It means the proportion of finance

provided by debt is higher than that of equity which exposed these companies to higher risks

as the payment of interest and repayment of debt are mandatory unlike payment of dividends

(Yapa Abeywardhana 2015).

GlaxoSmithKline Reckitt Benckiser

-

5.00

10.00

15.00

20.00

25.00

30.00

35.00

40.00

45.00

20.23 20.69

42.13

8.16

P/E Ratio

2018 2017

GlaxoSmithKline Reckitt Benckiser

0.00%

10.00%

20.00%

30.00%

40.00%

50.00%

60.00%

70.00%

80.00%

90.00%

100.00% 89.68%

50.76%

88.30%

55.41%

Gearing Ratio

2018 2017

Figure 5: Comparison of Gearing Ratios

There is a minor increase in the gearing ratio of GSK in 2018, but the same ratio of

RB has witnessed a fall in 2018 as compared to 2017. In both these companies, this ratio is

more than 50% that makes these companies highly geared. It means the proportion of finance

provided by debt is higher than that of equity which exposed these companies to higher risks

as the payment of interest and repayment of debt are mandatory unlike payment of dividends

(Yapa Abeywardhana 2015).

GlaxoSmithKline Reckitt Benckiser

-

5.00

10.00

15.00

20.00

25.00

30.00

35.00

40.00

45.00

20.23 20.69

42.13

8.16

P/E Ratio

2018 2017

8FINANCE PORTFOLIO MANAGEMENT

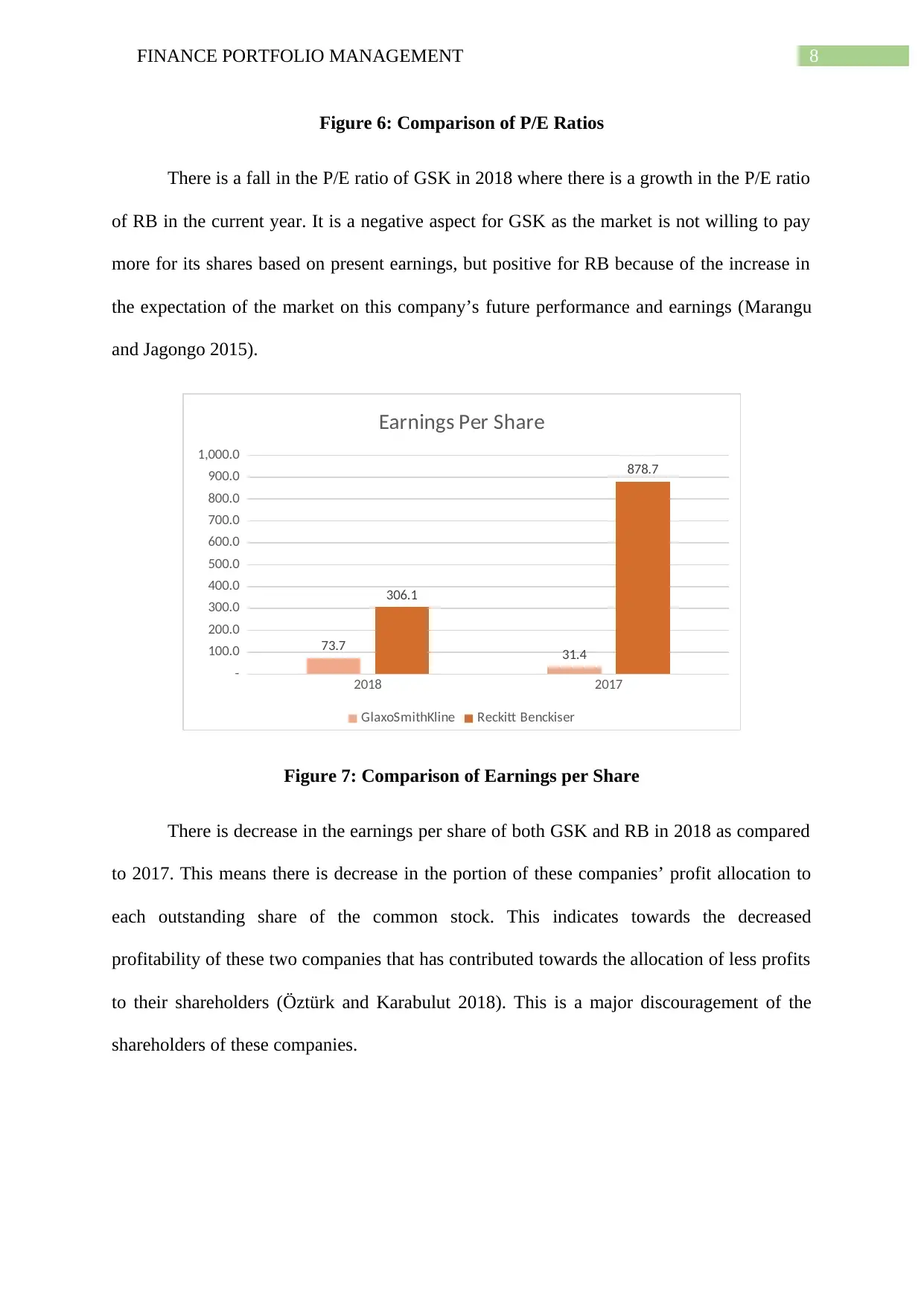

Figure 6: Comparison of P/E Ratios

There is a fall in the P/E ratio of GSK in 2018 where there is a growth in the P/E ratio

of RB in the current year. It is a negative aspect for GSK as the market is not willing to pay

more for its shares based on present earnings, but positive for RB because of the increase in

the expectation of the market on this company’s future performance and earnings (Marangu

and Jagongo 2015).

2018 2017

-

100.0

200.0

300.0

400.0

500.0

600.0

700.0

800.0

900.0

1,000.0

73.7 31.4

306.1

878.7

Earnings Per Share

GlaxoSmithKline Reckitt Benckiser

Figure 7: Comparison of Earnings per Share

There is decrease in the earnings per share of both GSK and RB in 2018 as compared

to 2017. This means there is decrease in the portion of these companies’ profit allocation to

each outstanding share of the common stock. This indicates towards the decreased

profitability of these two companies that has contributed towards the allocation of less profits

to their shareholders (Öztürk and Karabulut 2018). This is a major discouragement of the

shareholders of these companies.

Figure 6: Comparison of P/E Ratios

There is a fall in the P/E ratio of GSK in 2018 where there is a growth in the P/E ratio

of RB in the current year. It is a negative aspect for GSK as the market is not willing to pay

more for its shares based on present earnings, but positive for RB because of the increase in

the expectation of the market on this company’s future performance and earnings (Marangu

and Jagongo 2015).

2018 2017

-

100.0

200.0

300.0

400.0

500.0

600.0

700.0

800.0

900.0

1,000.0

73.7 31.4

306.1

878.7

Earnings Per Share

GlaxoSmithKline Reckitt Benckiser

Figure 7: Comparison of Earnings per Share

There is decrease in the earnings per share of both GSK and RB in 2018 as compared

to 2017. This means there is decrease in the portion of these companies’ profit allocation to

each outstanding share of the common stock. This indicates towards the decreased

profitability of these two companies that has contributed towards the allocation of less profits

to their shareholders (Öztürk and Karabulut 2018). This is a major discouragement of the

shareholders of these companies.

9FINANCE PORTFOLIO MANAGEMENT

GlaxoSmithKline Reckitt Benckiser

-

0.02

0.04

0.06

0.08

0.10

0.12

0.14

0.16

0.18

0.15

0.10

0.14

0.09

Return on Capital Employed

2018 2017

Figure 8: Comparison of Return on Capital Employed

There is increase in the return on capital employed in GSK and RB in 2018 from 2017

and this indicates effective performance of these two companies in terms of effectively using

the employed capital for generating profit. It implies that both GSK and RB are using its

capital in efficient manner in order to generate profit. It makes both of these companies

suitable candidates to the investors to invest in them (Ojeka, Iyoha and Obigbemi 2014).

GlaxoSmithKline Reckitt Benckiser

-

50

100

150

200

250

195

94

196

95

Average Inventories Turnover Period

2018 2017

Figure 9: Comparison of Average Inventories Turnover Period

GlaxoSmithKline Reckitt Benckiser

-

0.02

0.04

0.06

0.08

0.10

0.12

0.14

0.16

0.18

0.15

0.10

0.14

0.09

Return on Capital Employed

2018 2017

Figure 8: Comparison of Return on Capital Employed

There is increase in the return on capital employed in GSK and RB in 2018 from 2017

and this indicates effective performance of these two companies in terms of effectively using

the employed capital for generating profit. It implies that both GSK and RB are using its

capital in efficient manner in order to generate profit. It makes both of these companies

suitable candidates to the investors to invest in them (Ojeka, Iyoha and Obigbemi 2014).

GlaxoSmithKline Reckitt Benckiser

-

50

100

150

200

250

195

94

196

95

Average Inventories Turnover Period

2018 2017

Figure 9: Comparison of Average Inventories Turnover Period

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

10FINANCE PORTFOLIO MANAGEMENT

Minor decrease in the average inventories turnover period can be seen in GSK and RB in

2018 as compared to 2017. However, the average inventories turnover period of RB is less

than that of GSK. This is a good indicator for RB because this means RB takes less time to

clear its inventory averagely in a year as compared to GSK (Grubor, Milicevic and Mijic

2013). This indicates towards the potential issues in the inventory management mechanism in

GSK.

GlaxoSmithKline Reckitt Benckiser

0.00%

50.00%

100.00%

150.00%

200.00%

250.00%

300.00%

108.55%

55.77%

254.78%

18.70%

Dividend Payout Ratio

2018 2017

Figure 10: Comparison of Dividend Pay-out Ratios

The dividend pay-out ratio of GSK has decreased in 2018 from 2017; but the same

has increased has increased in case of RB in the current year. In case of GSK, this fall in this

ratio is an alarming sign for the investors as this signifies that the company cannot afford to

pay such dividend. However, growth in this ratio is a positive aspect for the performance of

RB as this indicates the increase in dividend payment by the company (Ahmed 2015).

Analysis of Audited Financial Statements

The examination of the audited financial statements of both GSK and RB shows the

increase in sales of these two companies and decrease in cost of sales which contributes to the

increase in gross profit for both the companies. However, GSK has almost doubled its net

Minor decrease in the average inventories turnover period can be seen in GSK and RB in

2018 as compared to 2017. However, the average inventories turnover period of RB is less

than that of GSK. This is a good indicator for RB because this means RB takes less time to

clear its inventory averagely in a year as compared to GSK (Grubor, Milicevic and Mijic

2013). This indicates towards the potential issues in the inventory management mechanism in

GSK.

GlaxoSmithKline Reckitt Benckiser

0.00%

50.00%

100.00%

150.00%

200.00%

250.00%

300.00%

108.55%

55.77%

254.78%

18.70%

Dividend Payout Ratio

2018 2017

Figure 10: Comparison of Dividend Pay-out Ratios

The dividend pay-out ratio of GSK has decreased in 2018 from 2017; but the same

has increased has increased in case of RB in the current year. In case of GSK, this fall in this

ratio is an alarming sign for the investors as this signifies that the company cannot afford to

pay such dividend. However, growth in this ratio is a positive aspect for the performance of

RB as this indicates the increase in dividend payment by the company (Ahmed 2015).

Analysis of Audited Financial Statements

The examination of the audited financial statements of both GSK and RB shows the

increase in sales of these two companies and decrease in cost of sales which contributes to the

increase in gross profit for both the companies. However, GSK has almost doubled its net

11FINANCE PORTFOLIO MANAGEMENT

profit in 2018 where there is more than double decrease in the net profit of RB (gsk.com

2019). This is mainly because of the increase in direct and indirect expenses of RB.

Moreover, asset position of both of these companies have increased where there is increase in

GSK’s total current assets and non-current assets along with RB’s total non-current assets.

However, total current assets of RB have decreased in the current year. Total liabilities of

GSK have increased in 2018 there the total liabilities of RB has fallen in the current year.

Total equity of both GSK and RB has increased in the current year (rb.com 2019).

c) Recommendations

It can be seen from the above analysis that both GSK and RB have certain financial

areas where they have performed poorly and appropriate recommendations are required to

improve the situation. The recommendations are provided below:

Both GSK and RB has major liquidity issues. This can be improved through cutting

the unnecessary overhead expenses along with getting rid of the unproductive assets.

In addition, both accounts receivables and accounts payables should be managed

monitored in order to ensure their speedy collection and payment respectively

(Oshoke and Sumaina 2015).

RB has issues in net profit margin and there are two major ways to improve this

situation; they are increase in sales revenue and decrease in operational costs. Net

products and service can be introduced that would boost the sales. Unnecessary

operational costs should also be cut.

Both GSK and RB has high gearing ratio that needs to be reduce. The recommended

ways to reduce gearing ate sell of shares for pay down the debts, conversion of loans

through negotiating with the lenders to the company’s shares and increase in the

company’s profit. Moreover, there should be increase in the accounts receivable

profit in 2018 where there is more than double decrease in the net profit of RB (gsk.com

2019). This is mainly because of the increase in direct and indirect expenses of RB.

Moreover, asset position of both of these companies have increased where there is increase in

GSK’s total current assets and non-current assets along with RB’s total non-current assets.

However, total current assets of RB have decreased in the current year. Total liabilities of

GSK have increased in 2018 there the total liabilities of RB has fallen in the current year.

Total equity of both GSK and RB has increased in the current year (rb.com 2019).

c) Recommendations

It can be seen from the above analysis that both GSK and RB have certain financial

areas where they have performed poorly and appropriate recommendations are required to

improve the situation. The recommendations are provided below:

Both GSK and RB has major liquidity issues. This can be improved through cutting

the unnecessary overhead expenses along with getting rid of the unproductive assets.

In addition, both accounts receivables and accounts payables should be managed

monitored in order to ensure their speedy collection and payment respectively

(Oshoke and Sumaina 2015).

RB has issues in net profit margin and there are two major ways to improve this

situation; they are increase in sales revenue and decrease in operational costs. Net

products and service can be introduced that would boost the sales. Unnecessary

operational costs should also be cut.

Both GSK and RB has high gearing ratio that needs to be reduce. The recommended

ways to reduce gearing ate sell of shares for pay down the debts, conversion of loans

through negotiating with the lenders to the company’s shares and increase in the

company’s profit. Moreover, there should be increase in the accounts receivable

12FINANCE PORTFOLIO MANAGEMENT

collection, reduction in the level of inventory, increase in the days for paying the trade

payable and others (Yapa Abeywardhana 2015).

GSK has problem in price earnings ratio. This can be improved through reinvesting

the earnings, developing new production plants and expanding the business

operations. These need to be done because most of the investors are enthusiastic to

buy the stock at higher share price out of the expectation of a high future payoff from

the investment in the company.

RB has major issues with the Earnings per share. This can be improved through the

increase in revenue that will enable flowing down more pounds to the earnings. It is

also recommended to decrease the costs as this enables the flow down of greater

portion of revenue to the earnings. Lastly, share count needs to be decreased that will

split the total earnings in less shares.

Both GSK and RB has witnessed decrease in average inventory days. The

recommendation to the company is to turn to automated inventory management

system with the aim to keep track of the inventories in effective manner. Moreover,

the pricing strategy of the companies needs to be reviewed as the current price many

not be working for the companies to increase the demand. Most importantly, the

overall costs associated with the inventories need to be reduced (Ahmed 2015).

d) Limitations of Relying on Financial Ratios to Interpret Company’s Performance

Followings are the limitations of depending in financial ratios for understanding the

financial performance of the companies:

The financial information used in ratio analysis is based on the past results published

by the firm; the metrics in ratio analysis do not essentially represent the future

performance of the firm (Faello 2015).

collection, reduction in the level of inventory, increase in the days for paying the trade

payable and others (Yapa Abeywardhana 2015).

GSK has problem in price earnings ratio. This can be improved through reinvesting

the earnings, developing new production plants and expanding the business

operations. These need to be done because most of the investors are enthusiastic to

buy the stock at higher share price out of the expectation of a high future payoff from

the investment in the company.

RB has major issues with the Earnings per share. This can be improved through the

increase in revenue that will enable flowing down more pounds to the earnings. It is

also recommended to decrease the costs as this enables the flow down of greater

portion of revenue to the earnings. Lastly, share count needs to be decreased that will

split the total earnings in less shares.

Both GSK and RB has witnessed decrease in average inventory days. The

recommendation to the company is to turn to automated inventory management

system with the aim to keep track of the inventories in effective manner. Moreover,

the pricing strategy of the companies needs to be reviewed as the current price many

not be working for the companies to increase the demand. Most importantly, the

overall costs associated with the inventories need to be reduced (Ahmed 2015).

d) Limitations of Relying on Financial Ratios to Interpret Company’s Performance

Followings are the limitations of depending in financial ratios for understanding the

financial performance of the companies:

The financial information used in ratio analysis is based on the past results published

by the firm; the metrics in ratio analysis do not essentially represent the future

performance of the firm (Faello 2015).

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

13FINANCE PORTFOLIO MANAGEMENT

There are differences in time in the financial statements as they are published

periodically. In case there is occurrence of inflation in the time lag, the information

presented in the financial statements fails to reflect the same. Therefore, it become

impossible to obtain the real price. Thus, the numbers across different financial period

are not comparable until there is adjustment of inflation (Faello 2015).

Changes in accounting policies of a firm create major impact on financial reporting of

the firms. Different companies tend to have different accounting policies. In this

situation, it is not possible in comparing the ratios of two companies having different

accounting policies since ratio analysis does not consider the changes in accounting

policies.

Financial analysts need to be aware of the seasonal factors that can possibly lead to

the limitation of the ratio analysis. Ratio analysis is unable in adjusting the seasonality

effects which can contribute to false interpretation of financial results (Faello 2015).

Conclusion

As per the above discussion, both the companies have positive and negative aspects

associated with the financial performance and position; but the positives of GSK are stronger

than RB. Both the companies have liquidity issues, but GSK is showing the sigh of

improving where the liquidity of RB is deteriorating. Both the companies have high gearing

ratio and this can be to accommodate any business expansion plan or introduction of new

product line. Significant improvement in the earnings per share of GSK is evident from the

analysis which is a major positive for the investors as GSK is allocating more profit to the

investors. GSK has also improved its efficiency in using its employed capital for generating

sales and profit. Decrease in the dividend pay-out ratio is an indicator that the company is

paying less dividend to the investors and undertaking any new expansion plan could be the

possible reason and this increases the scope of future profitability of GSK. Most importantly,

There are differences in time in the financial statements as they are published

periodically. In case there is occurrence of inflation in the time lag, the information

presented in the financial statements fails to reflect the same. Therefore, it become

impossible to obtain the real price. Thus, the numbers across different financial period

are not comparable until there is adjustment of inflation (Faello 2015).

Changes in accounting policies of a firm create major impact on financial reporting of

the firms. Different companies tend to have different accounting policies. In this

situation, it is not possible in comparing the ratios of two companies having different

accounting policies since ratio analysis does not consider the changes in accounting

policies.

Financial analysts need to be aware of the seasonal factors that can possibly lead to

the limitation of the ratio analysis. Ratio analysis is unable in adjusting the seasonality

effects which can contribute to false interpretation of financial results (Faello 2015).

Conclusion

As per the above discussion, both the companies have positive and negative aspects

associated with the financial performance and position; but the positives of GSK are stronger

than RB. Both the companies have liquidity issues, but GSK is showing the sigh of

improving where the liquidity of RB is deteriorating. Both the companies have high gearing

ratio and this can be to accommodate any business expansion plan or introduction of new

product line. Significant improvement in the earnings per share of GSK is evident from the

analysis which is a major positive for the investors as GSK is allocating more profit to the

investors. GSK has also improved its efficiency in using its employed capital for generating

sales and profit. Decrease in the dividend pay-out ratio is an indicator that the company is

paying less dividend to the investors and undertaking any new expansion plan could be the

possible reason and this increases the scope of future profitability of GSK. Most importantly,

14FINANCE PORTFOLIO MANAGEMENT

GSK has been able in increasing its profitability in terms of both net profit and gross profit

where the same has deteriorated for RB and this is the most important indicator of the

company’s good financial performance. It means the company is adequately profitable to

provide the investors with healthy return. Therefore, based on the whole analysis, it is

recommended to invest in GSK as this is a more viable option to invest in.

GSK has been able in increasing its profitability in terms of both net profit and gross profit

where the same has deteriorated for RB and this is the most important indicator of the

company’s good financial performance. It means the company is adequately profitable to

provide the investors with healthy return. Therefore, based on the whole analysis, it is

recommended to invest in GSK as this is a more viable option to invest in.

15FINANCE PORTFOLIO MANAGEMENT

Portfolio 2

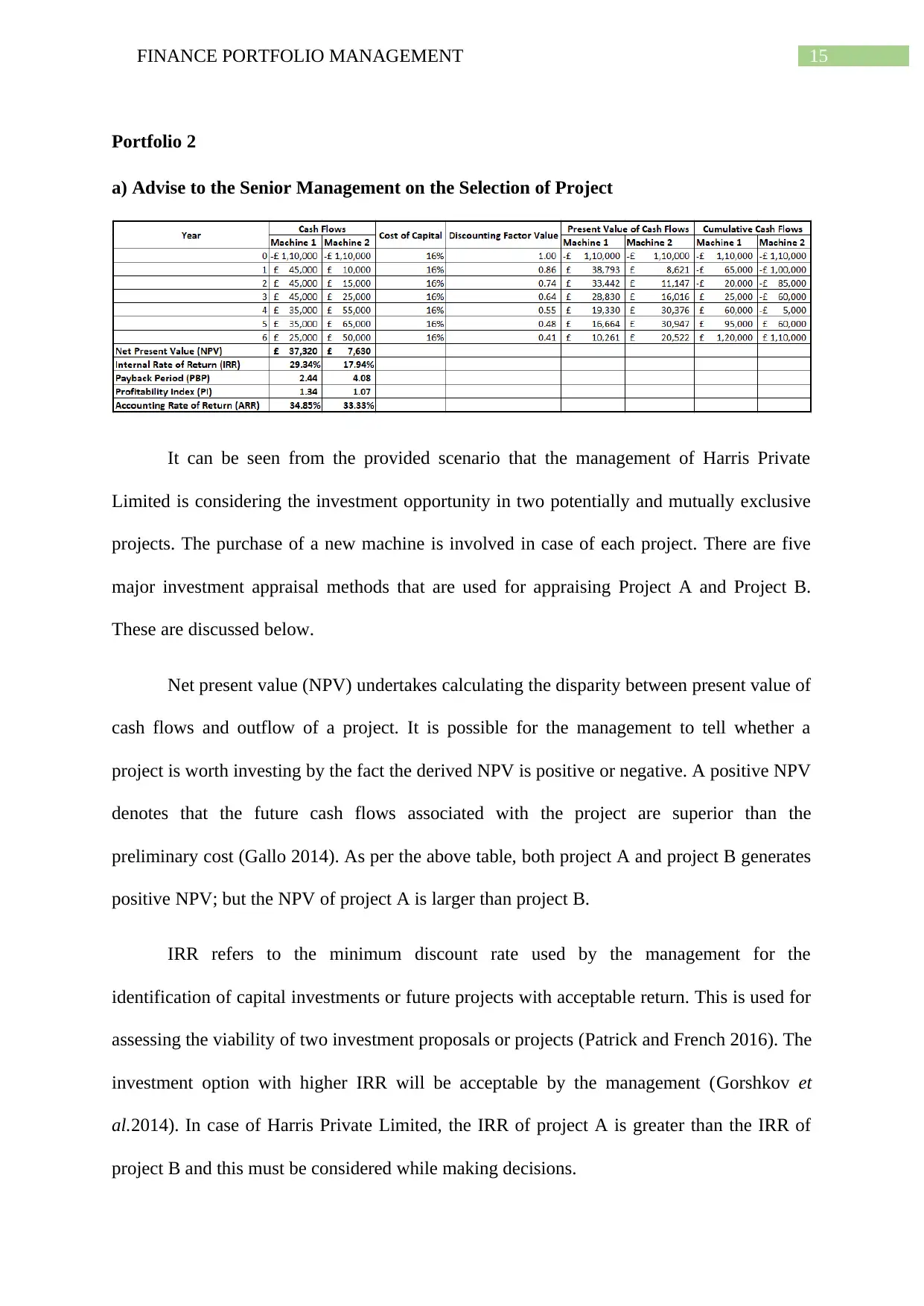

a) Advise to the Senior Management on the Selection of Project

It can be seen from the provided scenario that the management of Harris Private

Limited is considering the investment opportunity in two potentially and mutually exclusive

projects. The purchase of a new machine is involved in case of each project. There are five

major investment appraisal methods that are used for appraising Project A and Project B.

These are discussed below.

Net present value (NPV) undertakes calculating the disparity between present value of

cash flows and outflow of a project. It is possible for the management to tell whether a

project is worth investing by the fact the derived NPV is positive or negative. A positive NPV

denotes that the future cash flows associated with the project are superior than the

preliminary cost (Gallo 2014). As per the above table, both project A and project B generates

positive NPV; but the NPV of project A is larger than project B.

IRR refers to the minimum discount rate used by the management for the

identification of capital investments or future projects with acceptable return. This is used for

assessing the viability of two investment proposals or projects (Patrick and French 2016). The

investment option with higher IRR will be acceptable by the management (Gorshkov et

al.2014). In case of Harris Private Limited, the IRR of project A is greater than the IRR of

project B and this must be considered while making decisions.

Portfolio 2

a) Advise to the Senior Management on the Selection of Project

It can be seen from the provided scenario that the management of Harris Private

Limited is considering the investment opportunity in two potentially and mutually exclusive

projects. The purchase of a new machine is involved in case of each project. There are five

major investment appraisal methods that are used for appraising Project A and Project B.

These are discussed below.

Net present value (NPV) undertakes calculating the disparity between present value of

cash flows and outflow of a project. It is possible for the management to tell whether a

project is worth investing by the fact the derived NPV is positive or negative. A positive NPV

denotes that the future cash flows associated with the project are superior than the

preliminary cost (Gallo 2014). As per the above table, both project A and project B generates

positive NPV; but the NPV of project A is larger than project B.

IRR refers to the minimum discount rate used by the management for the

identification of capital investments or future projects with acceptable return. This is used for

assessing the viability of two investment proposals or projects (Patrick and French 2016). The

investment option with higher IRR will be acceptable by the management (Gorshkov et

al.2014). In case of Harris Private Limited, the IRR of project A is greater than the IRR of

project B and this must be considered while making decisions.

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

16FINANCE PORTFOLIO MANAGEMENT

Payback period is a key capital budgeting method used for calculating the required

number of days for an investment project for generating cash flows equal to the actual

investment cost. The management of Harris Private Limited needs to use payback period

calculation for assessing how speedily the money can be got back on the investment, the

faster the better. As per the above table, project A provides the money back in fewer years as

compared to project B.

PI involves in computing the present value of the expected cash flow that can be

generated by the investment. In case PI is larger than 1, management should undertake the

project. In case PI is less than 1, the project should not be undertaken. In case the PI is equal

to 1, the project is indifferent which accepting the project will not make any difference

(Nekrasova, Leventsov and Axionova 2016). The above table shows that both the projects

have PI of more than 1.

ARR is used for calculating the amount of return that would be made by the investors

from an investment. Therefore, projects with higher ARR are acceptable. It can be seen in the

case of Harris Private Limited that Project A has higher ARR as compared to project B

(Brdulak and Zakrzewski 2013).

It can be seen from the above discussion that Project A is superior in every aspect as

compared to the project B. First, despite of NPV of both the projects as positive, Project A

has more NPV than Project b. Second, the IRR of Project A is superior to Project B. Third;

the payback period of Project A is lesser than Project B which means this will take less time

to recover the investment money. Fourth, despite of PI of both the projects is greater than 1,

Project A has greater PI than Project B. Lastly, the ARR of Project A is greater than Project

B. Therefore, the management is advised to select Project A.

Payback period is a key capital budgeting method used for calculating the required

number of days for an investment project for generating cash flows equal to the actual

investment cost. The management of Harris Private Limited needs to use payback period

calculation for assessing how speedily the money can be got back on the investment, the

faster the better. As per the above table, project A provides the money back in fewer years as

compared to project B.

PI involves in computing the present value of the expected cash flow that can be

generated by the investment. In case PI is larger than 1, management should undertake the

project. In case PI is less than 1, the project should not be undertaken. In case the PI is equal

to 1, the project is indifferent which accepting the project will not make any difference

(Nekrasova, Leventsov and Axionova 2016). The above table shows that both the projects

have PI of more than 1.

ARR is used for calculating the amount of return that would be made by the investors

from an investment. Therefore, projects with higher ARR are acceptable. It can be seen in the

case of Harris Private Limited that Project A has higher ARR as compared to project B

(Brdulak and Zakrzewski 2013).

It can be seen from the above discussion that Project A is superior in every aspect as

compared to the project B. First, despite of NPV of both the projects as positive, Project A

has more NPV than Project b. Second, the IRR of Project A is superior to Project B. Third;

the payback period of Project A is lesser than Project B which means this will take less time

to recover the investment money. Fourth, despite of PI of both the projects is greater than 1,

Project A has greater PI than Project B. Lastly, the ARR of Project A is greater than Project

B. Therefore, the management is advised to select Project A.

17FINANCE PORTFOLIO MANAGEMENT

b) Limitations ofInvestment Appraisal Techniques in Long-Term Decision Making

The above-used five investment appraisal techniques have certain limitations in

helping in the long-term decision making process and these are discussed below:

NPV – The main limitation associated with NPV method is the requirement to guess about

the future cash flows along with the estimation of the cost of capital of the firm. This method

cannot be applied at the time of comparing investment projects with dissimilar investment

amount. In addition, it is hard to apply NPV method at the time to compare two investment

projects having different life durations (San Ong and Thum 2013).

IRR – The major limitation of IRR is that it assumes that there is reinvestment of earnings at

the IRR for the project’s outstanding duration. In case the average rate of return earned by the

company is not close to the IRR, there is no reasonableness in the profitability of that

particular project. This method does not take into account economies of scale and the

presence of impractical implicit assumptions associated with reinvestment can be seen in this

(El Tahir and El Otaibi 2014).

PBP – The greatest limitation of PBP in long-term decision making is its failure in taking

into consideration the time value of money in order to adjust the cash flows consequently. At

the same time, this method also fails to consider the cash inflows take place further than the

payback period which leads to the failure in comparing one project’s overall profitability to

another (Kim, Shim and Reinschmidt 2013).

PI – One main limitation of PI is that the generated information is based on estimations rather

than facts. The use of best-guess estimation in PI fails to provide any guarantee. One crucial

aspect that is sunk cost is ignored under this method. Sunk costs are the costs that are

incurred before the commencement of the projects which form a crucial part of the capital

investment appraisal decision. At the same time, the managements have to face major

b) Limitations ofInvestment Appraisal Techniques in Long-Term Decision Making

The above-used five investment appraisal techniques have certain limitations in

helping in the long-term decision making process and these are discussed below:

NPV – The main limitation associated with NPV method is the requirement to guess about

the future cash flows along with the estimation of the cost of capital of the firm. This method

cannot be applied at the time of comparing investment projects with dissimilar investment

amount. In addition, it is hard to apply NPV method at the time to compare two investment

projects having different life durations (San Ong and Thum 2013).

IRR – The major limitation of IRR is that it assumes that there is reinvestment of earnings at

the IRR for the project’s outstanding duration. In case the average rate of return earned by the

company is not close to the IRR, there is no reasonableness in the profitability of that

particular project. This method does not take into account economies of scale and the

presence of impractical implicit assumptions associated with reinvestment can be seen in this

(El Tahir and El Otaibi 2014).

PBP – The greatest limitation of PBP in long-term decision making is its failure in taking

into consideration the time value of money in order to adjust the cash flows consequently. At

the same time, this method also fails to consider the cash inflows take place further than the

payback period which leads to the failure in comparing one project’s overall profitability to

another (Kim, Shim and Reinschmidt 2013).

PI – One main limitation of PI is that the generated information is based on estimations rather

than facts. The use of best-guess estimation in PI fails to provide any guarantee. One crucial

aspect that is sunk cost is ignored under this method. Sunk costs are the costs that are

incurred before the commencement of the projects which form a crucial part of the capital

investment appraisal decision. At the same time, the managements have to face major

18FINANCE PORTFOLIO MANAGEMENT

difficulties in the estimation of opportunity cost under PI technique (Daunfeldt and Hartwig

2014).

ARR – One greatest limitation of ARR is that this does not consider the time factor that

causes problems in the selection of alternative use of the funds. In case return on investment

(ROI) is different from ARR, major problem is created in the long-term decision making.

Different external factors are not considered under this method while making long-term

decisions (Beck, Raj and Britzelmaier 2013).

difficulties in the estimation of opportunity cost under PI technique (Daunfeldt and Hartwig

2014).

ARR – One greatest limitation of ARR is that this does not consider the time factor that

causes problems in the selection of alternative use of the funds. In case return on investment

(ROI) is different from ARR, major problem is created in the long-term decision making.

Different external factors are not considered under this method while making long-term

decisions (Beck, Raj and Britzelmaier 2013).

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

19FINANCE PORTFOLIO MANAGEMENT

References

Ahmed, I.E., 2015. Liquidity, profitability and the dividends payout policy. World Review of

Business Research, 5(2), pp.73-85.

Beck, V., Raj, R. and Britzelmaier, B., 2013. The effects of capital investment appraisal

methods in automotive companies. International Journal of Sales, Retailing and

Marketing, 2, pp.3-12.

Brdulak, J. and Zakrzewski, B., 2013. Methods for calculating the efficiency of logistics

centres. Archives of Transport, 27(28, iss. 3-4), pp.25-43.

Daunfeldt, S.O. and Hartwig, F., 2014. What determines the use of capital budgeting

methods?: Evidence from Swedish listed companies. Journal of Finance and

Economics, 2(4), pp.101-112.

El Tahir, Y. and El Otaibi, D., 2014. Internal Rate of Return: A suggested alternative formula

and its macroeconomics implications. J Am Sci, 10(11), pp.216-221.

Faello, J., 2015. Understanding the limitations of financial ratios. Academy of Accounting and

Financial Studies Journal, 19(3), p.75.

Gallo, A., 2014. A refresher on net present value. Harvard Business Review, 19.

Gorshkov, A.S., Rymkevich, P.P., Nemova, D.V. and Vatin, N.I., 2014. Method of

calculating the payback period of investment for renovation of building facades. Stroitel'stvo

Unikal'nyh Zdanij i Sooruzenij, (2), p.82.

Grubor, A., Milicevic, N. and Mijic, K., 2013. Empirical Analysis of Inventory Turnover

Ratio in FMCG Retail Sector-Evidence from the Republic of Serbia. Engineering

Economics, 24(5), pp.401-407.

References

Ahmed, I.E., 2015. Liquidity, profitability and the dividends payout policy. World Review of

Business Research, 5(2), pp.73-85.

Beck, V., Raj, R. and Britzelmaier, B., 2013. The effects of capital investment appraisal

methods in automotive companies. International Journal of Sales, Retailing and

Marketing, 2, pp.3-12.

Brdulak, J. and Zakrzewski, B., 2013. Methods for calculating the efficiency of logistics

centres. Archives of Transport, 27(28, iss. 3-4), pp.25-43.

Daunfeldt, S.O. and Hartwig, F., 2014. What determines the use of capital budgeting

methods?: Evidence from Swedish listed companies. Journal of Finance and

Economics, 2(4), pp.101-112.

El Tahir, Y. and El Otaibi, D., 2014. Internal Rate of Return: A suggested alternative formula

and its macroeconomics implications. J Am Sci, 10(11), pp.216-221.

Faello, J., 2015. Understanding the limitations of financial ratios. Academy of Accounting and

Financial Studies Journal, 19(3), p.75.

Gallo, A., 2014. A refresher on net present value. Harvard Business Review, 19.

Gorshkov, A.S., Rymkevich, P.P., Nemova, D.V. and Vatin, N.I., 2014. Method of

calculating the payback period of investment for renovation of building facades. Stroitel'stvo

Unikal'nyh Zdanij i Sooruzenij, (2), p.82.

Grubor, A., Milicevic, N. and Mijic, K., 2013. Empirical Analysis of Inventory Turnover

Ratio in FMCG Retail Sector-Evidence from the Republic of Serbia. Engineering

Economics, 24(5), pp.401-407.

20FINANCE PORTFOLIO MANAGEMENT

Gsk.com. 2019. Annual Report 2018. [online] Available at:

https://www.gsk.com/media/5349/annual-report-2018.pdf [Accessed 19 Dec. 2019].

Jonny, J., 2016. Efficiency Analysis of Financial Management Administration of ABC

Hospital using Financial Ratio Analysis Method. Binus Business Review, 7(1), pp.65-69.

Kim, B.C., Shim, E. and Reinschmidt, K.F., 2013. Probability distribution of the project

payback period using the equivalent cash flow decomposition. The Engineering

Economist, 58(2), pp.112-136.

Marangu, K. and Jagongo, A., 2015. Price to Book Value Ratio and Financial Statement

Variables: A Study of Companies Quoted at Nairobi Securities Exchange,

Kenya. International Journal of Finance & Policy Analysis, 7.

Nekrasova, T., Leventsov, V. and Axionova, E., 2016. Evaluating the efficiency of

investments in mobile telecommunication systems development. In Internet of Things, Smart

Spaces, and Next Generation Networks and Systems (pp. 741-751). Springer, Cham.

Ojeka, S., Iyoha, F.O. and Obigbemi, I.F., 2014. Effectiveness of audit committee and firm

financial performance in Nigeria: an empirical analysis. Journal of Accounting and Auditing:

Research & Practice.

Oshoke, A.S. and Sumaina, J., 2015. Performance evaluation through ratio analysis. Journal

of Accounting and Financial Management, 1, pp.1-10.

Öztürk, H. and Karabulut, T.A., 2018. The Relationship between Earnings-to-Price, Current

Ratio, Profit Margin and Return: An Empirical Analysis on Istanbul Stock

Exchange. Accounting and Finance Research, 7(1), pp.109-115.

Patrick, M. and French, N., 2016. The internal rate of return (IRR): projections, benchmarks

and pitfalls. Journal of Property Investment & Finance, 34(6), pp.664-669.

Gsk.com. 2019. Annual Report 2018. [online] Available at:

https://www.gsk.com/media/5349/annual-report-2018.pdf [Accessed 19 Dec. 2019].

Jonny, J., 2016. Efficiency Analysis of Financial Management Administration of ABC

Hospital using Financial Ratio Analysis Method. Binus Business Review, 7(1), pp.65-69.

Kim, B.C., Shim, E. and Reinschmidt, K.F., 2013. Probability distribution of the project

payback period using the equivalent cash flow decomposition. The Engineering

Economist, 58(2), pp.112-136.

Marangu, K. and Jagongo, A., 2015. Price to Book Value Ratio and Financial Statement

Variables: A Study of Companies Quoted at Nairobi Securities Exchange,

Kenya. International Journal of Finance & Policy Analysis, 7.

Nekrasova, T., Leventsov, V. and Axionova, E., 2016. Evaluating the efficiency of

investments in mobile telecommunication systems development. In Internet of Things, Smart

Spaces, and Next Generation Networks and Systems (pp. 741-751). Springer, Cham.

Ojeka, S., Iyoha, F.O. and Obigbemi, I.F., 2014. Effectiveness of audit committee and firm

financial performance in Nigeria: an empirical analysis. Journal of Accounting and Auditing:

Research & Practice.

Oshoke, A.S. and Sumaina, J., 2015. Performance evaluation through ratio analysis. Journal

of Accounting and Financial Management, 1, pp.1-10.

Öztürk, H. and Karabulut, T.A., 2018. The Relationship between Earnings-to-Price, Current

Ratio, Profit Margin and Return: An Empirical Analysis on Istanbul Stock

Exchange. Accounting and Finance Research, 7(1), pp.109-115.

Patrick, M. and French, N., 2016. The internal rate of return (IRR): projections, benchmarks

and pitfalls. Journal of Property Investment & Finance, 34(6), pp.664-669.

21FINANCE PORTFOLIO MANAGEMENT

Rb.com. 2019. Reckitt Benckiser Group plc: Annual Report and Financial Statements 2018.

[online] Available at: https://www.rb.com/media/4116/rb-ar2018.pdf [Accessed 19 Dec.

2019].

Reynolds, D., Davenport, D.L., Korosec, R.L. and Roth, J.S., 2013. Financial implications of

ventral hernia repair: a hospital cost analysis. Journal of gastrointestinal surgery, 17(1),

pp.159-167.

San Ong, T. and Thum, C.H., 2013. Net present value and payback period for building

integrated photovoltaic projects in Malaysia. International Journal of Academic Research in

Business and Social Sciences, 3(2), p.153.

Tamulevičienė, D., 2016. Methodology of complex analysis of companies’

profitability. Entrepreneurship and sustainability issues, 4, pp.53-63.

Yapa Abeywardhana, D., 2015. Capital structure and profitability: An empirical analysis of

SMEs in the UK. Journal of Emerging Issues in Economics, Finance and Banking

(JEIEFB), 4(2), pp.1661-1675.

Rb.com. 2019. Reckitt Benckiser Group plc: Annual Report and Financial Statements 2018.

[online] Available at: https://www.rb.com/media/4116/rb-ar2018.pdf [Accessed 19 Dec.

2019].

Reynolds, D., Davenport, D.L., Korosec, R.L. and Roth, J.S., 2013. Financial implications of

ventral hernia repair: a hospital cost analysis. Journal of gastrointestinal surgery, 17(1),

pp.159-167.

San Ong, T. and Thum, C.H., 2013. Net present value and payback period for building

integrated photovoltaic projects in Malaysia. International Journal of Academic Research in

Business and Social Sciences, 3(2), p.153.

Tamulevičienė, D., 2016. Methodology of complex analysis of companies’

profitability. Entrepreneurship and sustainability issues, 4, pp.53-63.

Yapa Abeywardhana, D., 2015. Capital structure and profitability: An empirical analysis of

SMEs in the UK. Journal of Emerging Issues in Economics, Finance and Banking

(JEIEFB), 4(2), pp.1661-1675.

1 out of 22

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

© 2024 | Zucol Services PVT LTD | All rights reserved.