Project Appraisal Techniques

VerifiedAdded on 2019/09/13

|5

|784

|499

Homework Assignment

AI Summary

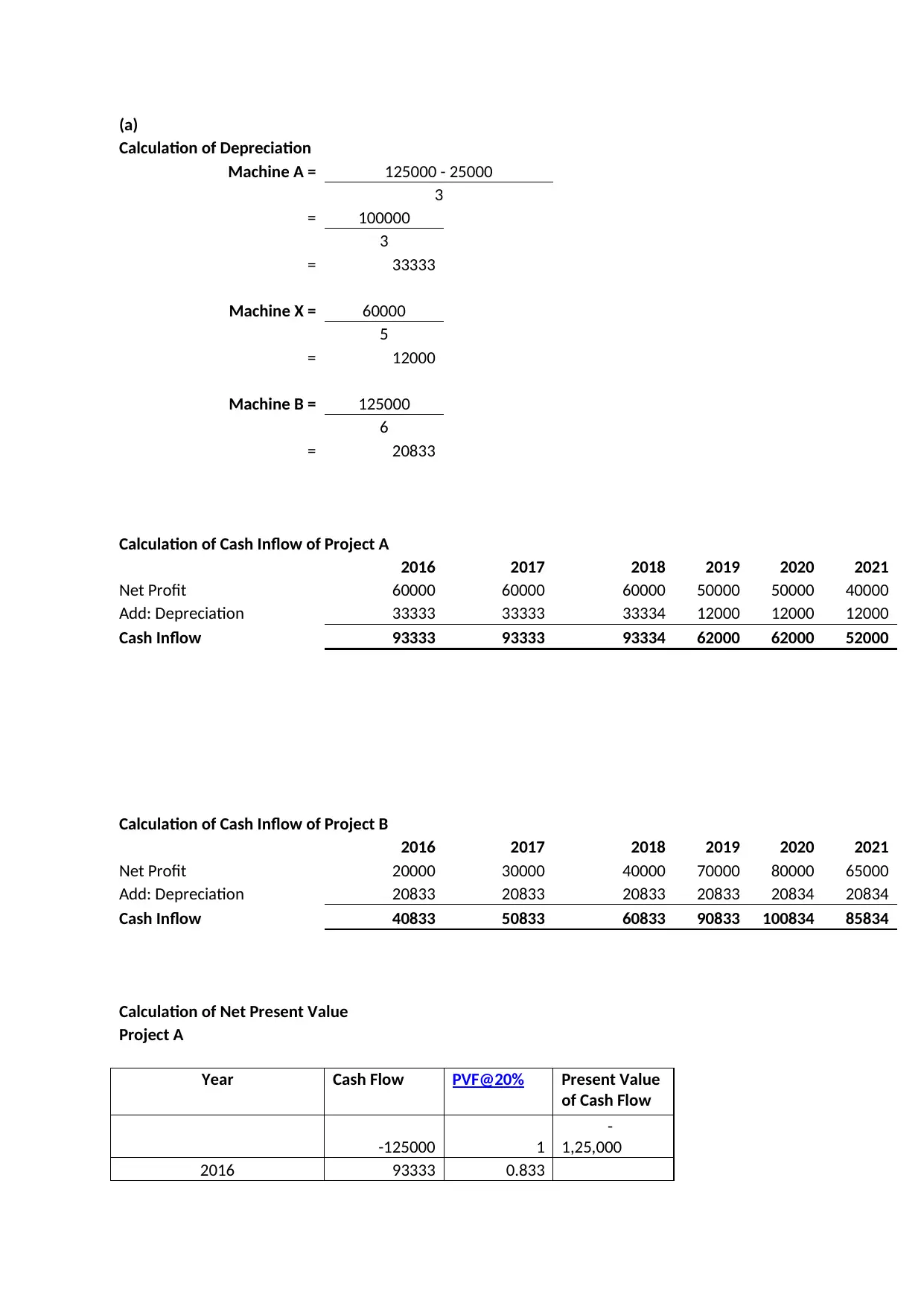

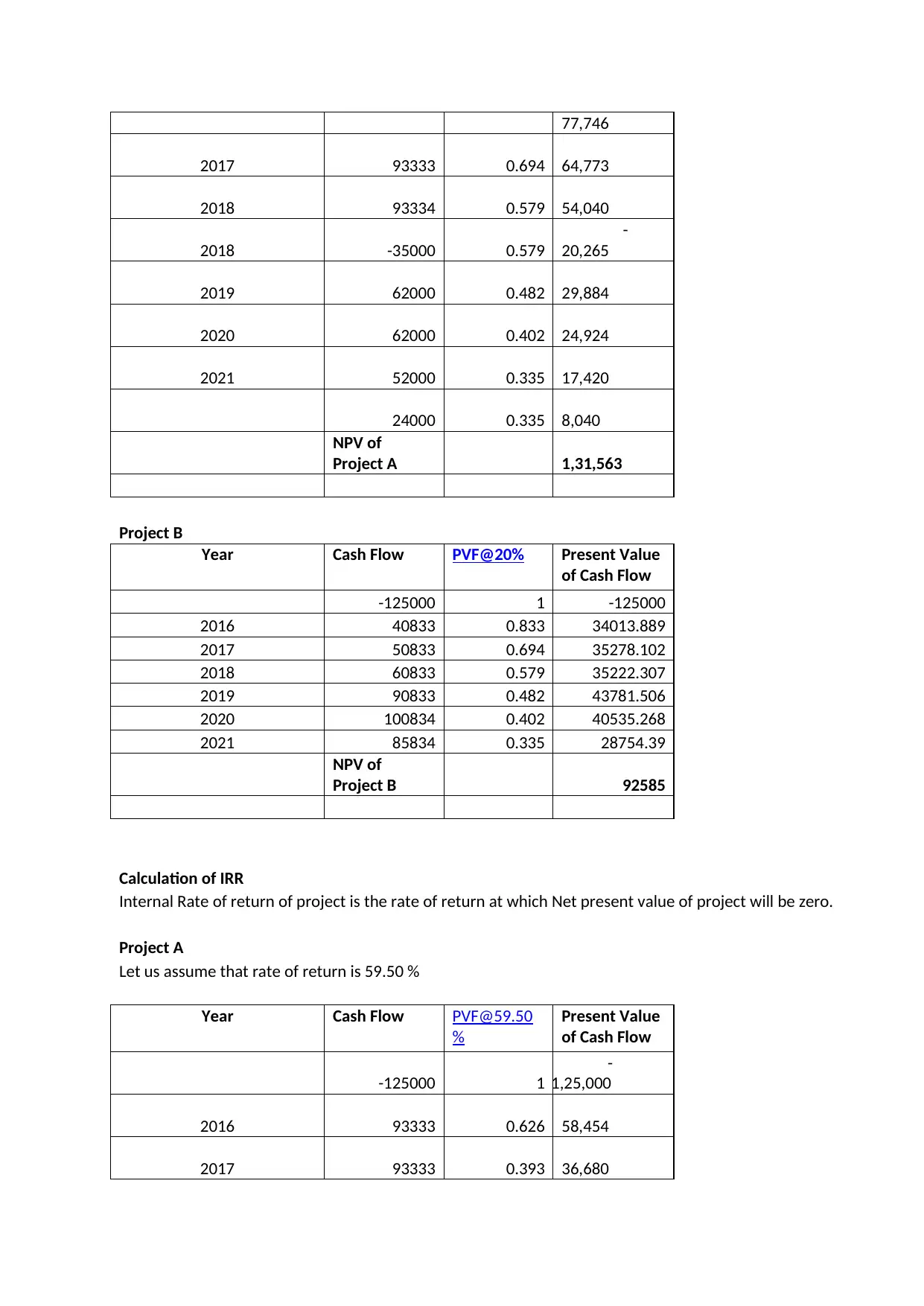

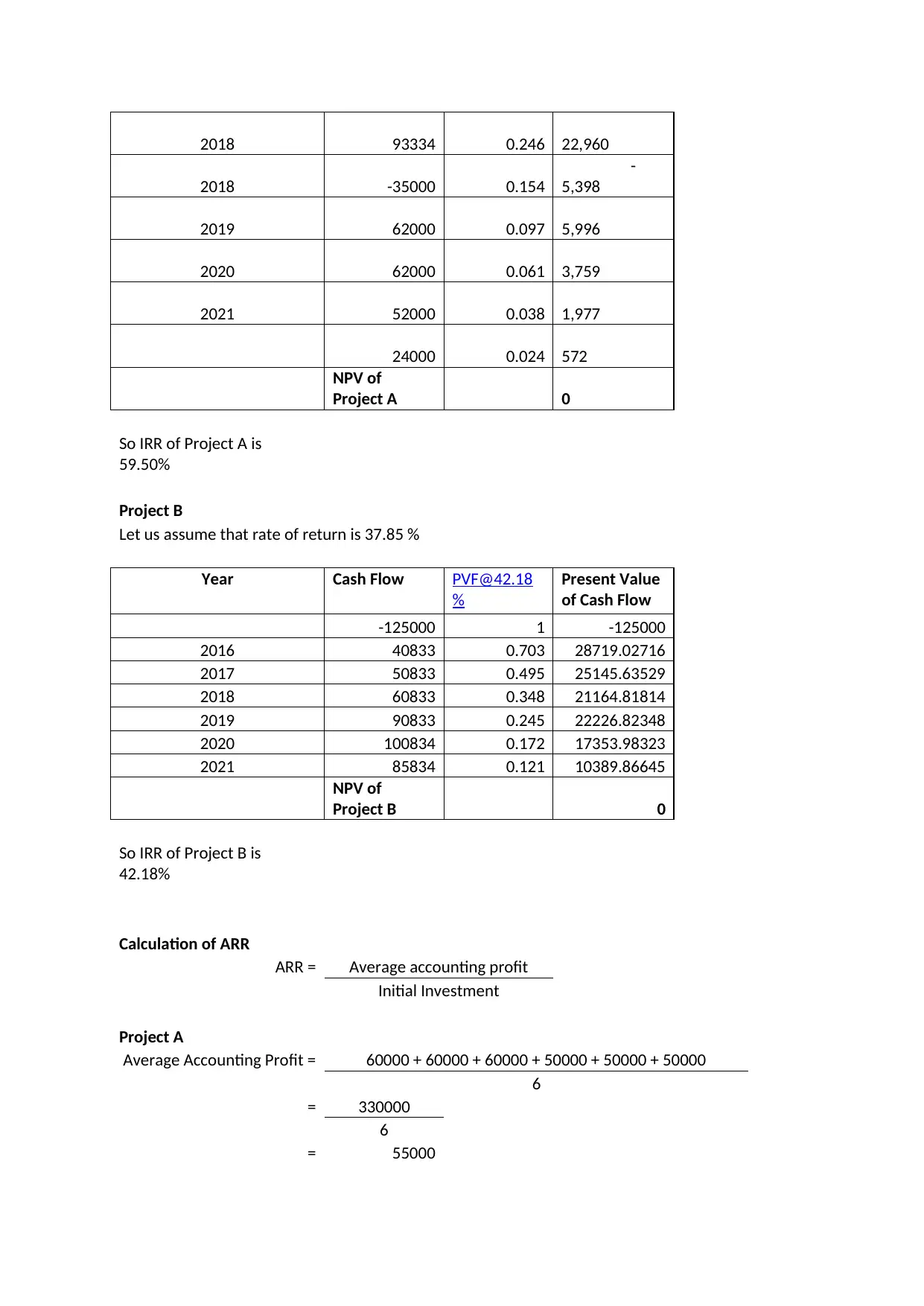

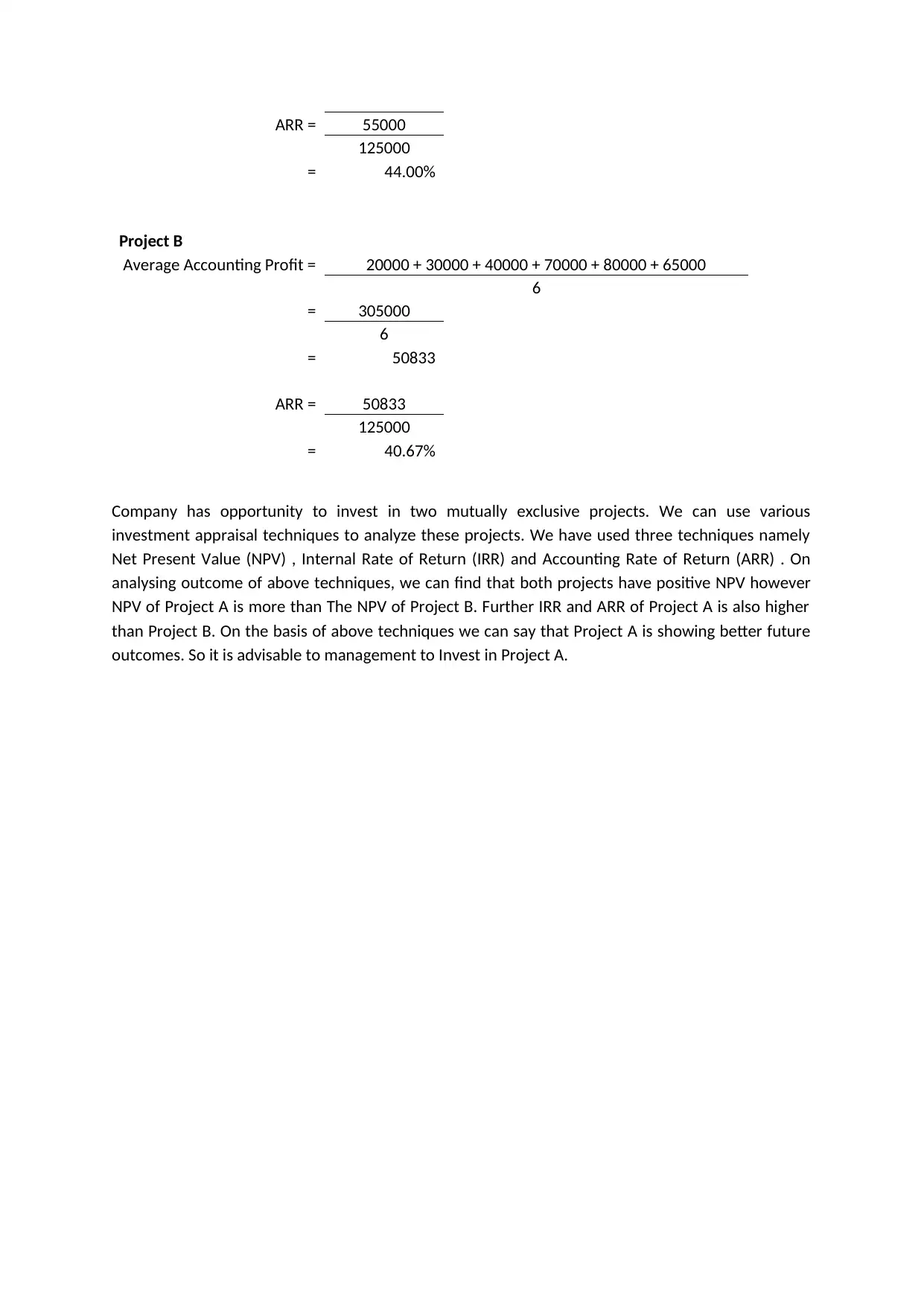

This assignment presents a detailed solution for evaluating two mutually exclusive projects (A and B) using three investment appraisal techniques: Net Present Value (NPV), Internal Rate of Return (IRR), and Accounting Rate of Return (ARR). The solution begins by calculating depreciation for each project's assets. Then, it meticulously calculates the cash inflow for each project over a six-year period, incorporating net profit and depreciation. The core of the solution lies in the NPV calculation for both projects, using a discount rate of 20%. Following this, the IRR is determined for each project through iterative calculations, finding the discount rate that results in a zero NPV. Finally, the ARR is calculated for both projects using average accounting profit and initial investment. The analysis concludes that Project A is superior based on higher NPV, IRR, and ARR values. The assignment also briefly discusses the limitations of investment appraisal techniques, highlighting challenges in accurately estimating future cash flows, project durations, and the potential for conflicting results from different techniques. It also mentions the limitations of using a fixed cost of capital and the exclusion of unexpected events.

1 out of 5

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2025 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.