ACFI7027 Quantitative Methods for Finance

VerifiedAdded on 2023/06/10

|16

|4211

|299

AI Summary

This document includes tasks related to multicollinearity, simple linear regression, improving the quality of the model, stationarity and its importance in time series analysis, calculation of present value of series of payments made to the bond holder, determination of the date of first coupon payment, purpose of discounting future cash flows and determination of appropriate discounting rate, and determination of a formula for total revenue from producing and selling quantities Q1 and Q2. The subject is ACFI7027 Quantitative Methods for Finance.

Contribute Materials

Your contribution can guide someone’s learning journey. Share your

documents today.

ACFI7027 QUANTITATIVE

METHODS FOR FINANCE

METHODS FOR FINANCE

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

Table of Contents

Task 1...............................................................................................................................................3

1. Check for multicollinearity, its explanation and interpretation...............................................3

2. Simple Linear Regression of EXR and PRI............................................................................4

3. Improving the quality of the model.........................................................................................5

4. Statement of Null hypothesis and alternative hypothesis........................................................6

5. Explanation for best model identified above...........................................................................6

6...................................................................................................................................................6

Task 2...............................................................................................................................................7

1. Concept of Stationarity and its importance in time series analysis.........................................7

Task 3...............................................................................................................................................8

1. Calculation of Present value of series of payments made to the bond holder.........................8

2. Determination of the date of first coupon payment.................................................................9

3. Purpose of discounting future cash flows and determination of appropriate discounting rate9

Task 4.............................................................................................................................................10

1. Determination of a formula for total revenue from producing and selling quantities Q1 and

Q2..............................................................................................................................................10

2. Obtaining a formula for the total annual cost of producing quantities Q1 and Q2...............11

3. Determination of the formula for the total annual profit of the firm.....................................11

REFERENCES..............................................................................................................................15

Task 1...............................................................................................................................................3

1. Check for multicollinearity, its explanation and interpretation...............................................3

2. Simple Linear Regression of EXR and PRI............................................................................4

3. Improving the quality of the model.........................................................................................5

4. Statement of Null hypothesis and alternative hypothesis........................................................6

5. Explanation for best model identified above...........................................................................6

6...................................................................................................................................................6

Task 2...............................................................................................................................................7

1. Concept of Stationarity and its importance in time series analysis.........................................7

Task 3...............................................................................................................................................8

1. Calculation of Present value of series of payments made to the bond holder.........................8

2. Determination of the date of first coupon payment.................................................................9

3. Purpose of discounting future cash flows and determination of appropriate discounting rate9

Task 4.............................................................................................................................................10

1. Determination of a formula for total revenue from producing and selling quantities Q1 and

Q2..............................................................................................................................................10

2. Obtaining a formula for the total annual cost of producing quantities Q1 and Q2...............11

3. Determination of the formula for the total annual profit of the firm.....................................11

REFERENCES..............................................................................................................................15

Task 1

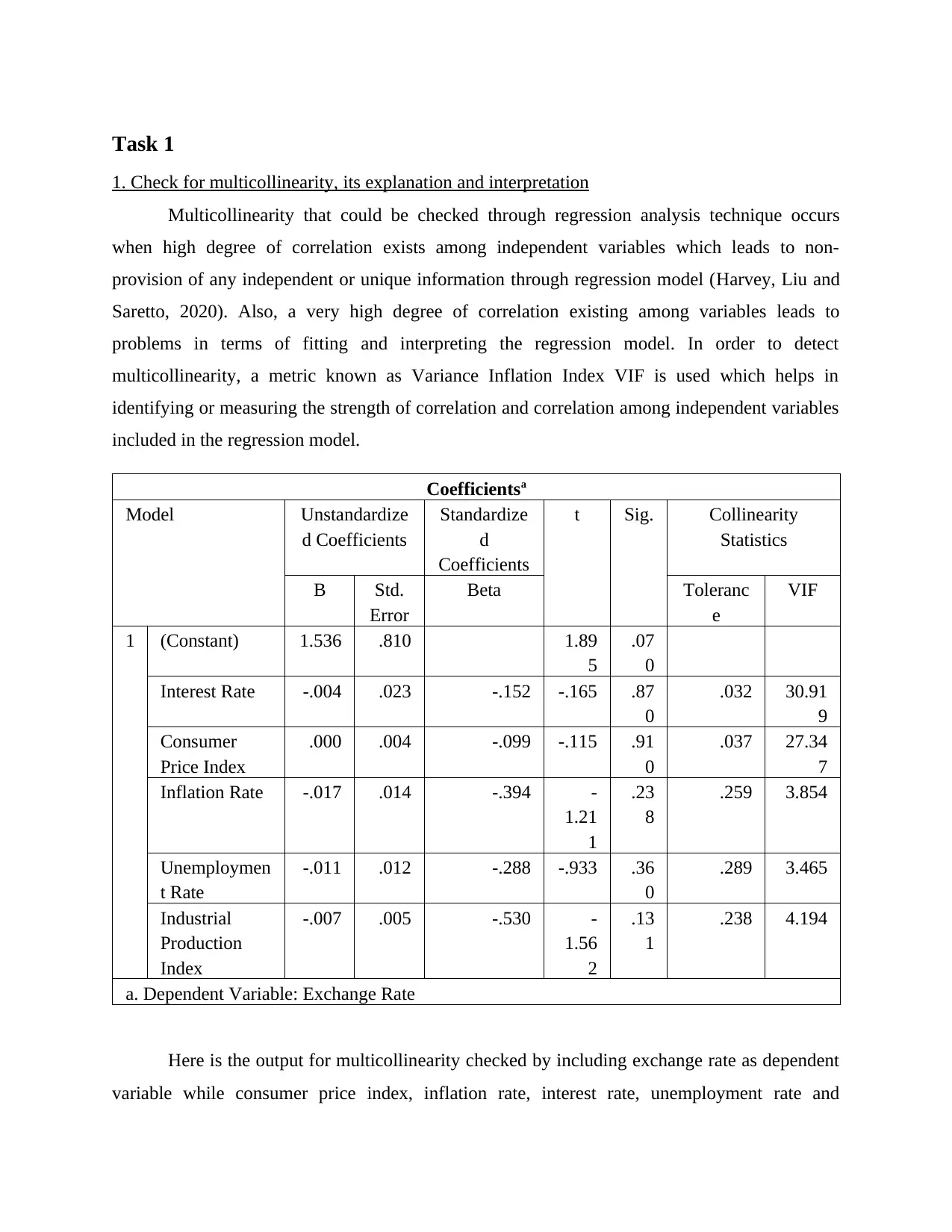

1. Check for multicollinearity, its explanation and interpretation

Multicollinearity that could be checked through regression analysis technique occurs

when high degree of correlation exists among independent variables which leads to non-

provision of any independent or unique information through regression model (Harvey, Liu and

Saretto, 2020). Also, a very high degree of correlation existing among variables leads to

problems in terms of fitting and interpreting the regression model. In order to detect

multicollinearity, a metric known as Variance Inflation Index VIF is used which helps in

identifying or measuring the strength of correlation and correlation among independent variables

included in the regression model.

Coefficientsa

Model Unstandardize

d Coefficients

Standardize

d

Coefficients

t Sig. Collinearity

Statistics

B Std.

Error

Beta Toleranc

e

VIF

1 (Constant) 1.536 .810 1.89

5

.07

0

Interest Rate -.004 .023 -.152 -.165 .87

0

.032 30.91

9

Consumer

Price Index

.000 .004 -.099 -.115 .91

0

.037 27.34

7

Inflation Rate -.017 .014 -.394 -

1.21

1

.23

8

.259 3.854

Unemploymen

t Rate

-.011 .012 -.288 -.933 .36

0

.289 3.465

Industrial

Production

Index

-.007 .005 -.530 -

1.56

2

.13

1

.238 4.194

a. Dependent Variable: Exchange Rate

Here is the output for multicollinearity checked by including exchange rate as dependent

variable while consumer price index, inflation rate, interest rate, unemployment rate and

1. Check for multicollinearity, its explanation and interpretation

Multicollinearity that could be checked through regression analysis technique occurs

when high degree of correlation exists among independent variables which leads to non-

provision of any independent or unique information through regression model (Harvey, Liu and

Saretto, 2020). Also, a very high degree of correlation existing among variables leads to

problems in terms of fitting and interpreting the regression model. In order to detect

multicollinearity, a metric known as Variance Inflation Index VIF is used which helps in

identifying or measuring the strength of correlation and correlation among independent variables

included in the regression model.

Coefficientsa

Model Unstandardize

d Coefficients

Standardize

d

Coefficients

t Sig. Collinearity

Statistics

B Std.

Error

Beta Toleranc

e

VIF

1 (Constant) 1.536 .810 1.89

5

.07

0

Interest Rate -.004 .023 -.152 -.165 .87

0

.032 30.91

9

Consumer

Price Index

.000 .004 -.099 -.115 .91

0

.037 27.34

7

Inflation Rate -.017 .014 -.394 -

1.21

1

.23

8

.259 3.854

Unemploymen

t Rate

-.011 .012 -.288 -.933 .36

0

.289 3.465

Industrial

Production

Index

-.007 .005 -.530 -

1.56

2

.13

1

.238 4.194

a. Dependent Variable: Exchange Rate

Here is the output for multicollinearity checked by including exchange rate as dependent

variable while consumer price index, inflation rate, interest rate, unemployment rate and

industrial production index are included as independent variables by ensuring that the five

independent variables are not highly correlated with each other. For this, VIF values for each of

the predictor variable has been obtained in order to determine the multicollinearity. The VIF

values have lower limit as 1 while having no upper limit Accordingly, the VIF values for each of

the predictor variable has been obtained as follows:

Interest rate = 30.919

Consumer Price Index = 27.347

Inflation rate = 3.854

Unemployment rate = 3.465

Industrial production index = 4.194

From the above results obtained in terms of VIF values, it can be found that none of the

predictor variable is having 1 as a VIF value while there are predictor variables that is, inflation

rate, unemployment rate and industrial production index where VIF values fall in the range of 1

and 5 which indicates presence of moderate correlation among one predictor variable to other

predictor variables involves in the model (James, 2020). However, a very high value of VIF for

interest rate and consumer price index shows there exists severe correlation between a particular

predictor variable and other predictor variables in the model. Accordingly, multicollinearity

would be a problem in this particular regression model and to avoid this problem such high

correlated independent variables should be removed from the model.

2. Simple Linear Regression of EXR and PRI

Model Summary

Mode

l

R R

Squar

e

Adjuste

d R

Square

Std.

Error of

the

Estimat

e

Change Statistics

R

Square

Chang

e

F

Chang

e

df

1

df

2

Sig. F

Chang

e

1 .559

a

.313 .289 .06207 .313 13.201 1 29 .001

a. Predictors: (Constant), Consumer Price Index

independent variables are not highly correlated with each other. For this, VIF values for each of

the predictor variable has been obtained in order to determine the multicollinearity. The VIF

values have lower limit as 1 while having no upper limit Accordingly, the VIF values for each of

the predictor variable has been obtained as follows:

Interest rate = 30.919

Consumer Price Index = 27.347

Inflation rate = 3.854

Unemployment rate = 3.465

Industrial production index = 4.194

From the above results obtained in terms of VIF values, it can be found that none of the

predictor variable is having 1 as a VIF value while there are predictor variables that is, inflation

rate, unemployment rate and industrial production index where VIF values fall in the range of 1

and 5 which indicates presence of moderate correlation among one predictor variable to other

predictor variables involves in the model (James, 2020). However, a very high value of VIF for

interest rate and consumer price index shows there exists severe correlation between a particular

predictor variable and other predictor variables in the model. Accordingly, multicollinearity

would be a problem in this particular regression model and to avoid this problem such high

correlated independent variables should be removed from the model.

2. Simple Linear Regression of EXR and PRI

Model Summary

Mode

l

R R

Squar

e

Adjuste

d R

Square

Std.

Error of

the

Estimat

e

Change Statistics

R

Square

Chang

e

F

Chang

e

df

1

df

2

Sig. F

Chang

e

1 .559

a

.313 .289 .06207 .313 13.201 1 29 .001

a. Predictors: (Constant), Consumer Price Index

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

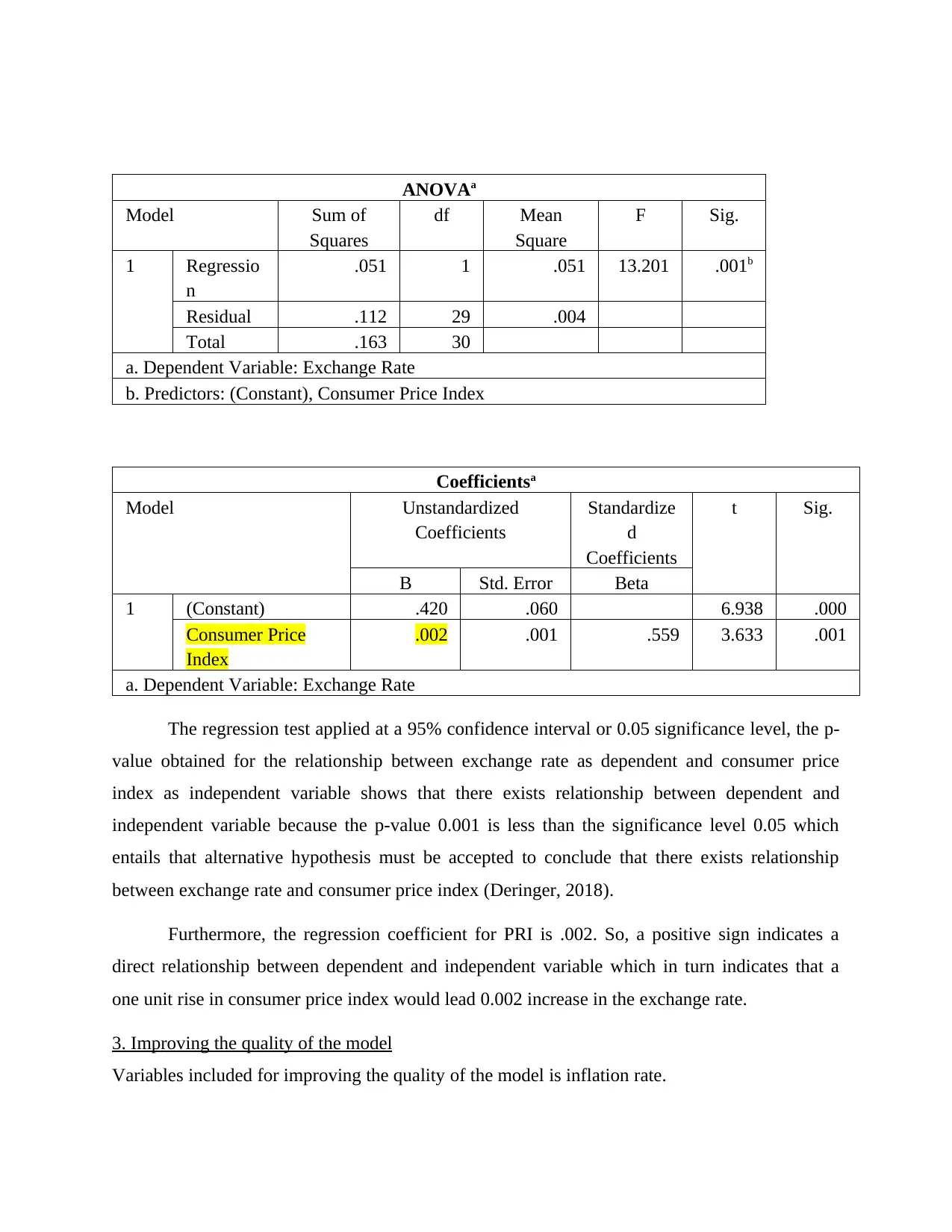

ANOVAa

Model Sum of

Squares

df Mean

Square

F Sig.

1 Regressio

n

.051 1 .051 13.201 .001b

Residual .112 29 .004

Total .163 30

a. Dependent Variable: Exchange Rate

b. Predictors: (Constant), Consumer Price Index

Coefficientsa

Model Unstandardized

Coefficients

Standardize

d

Coefficients

t Sig.

B Std. Error Beta

1 (Constant) .420 .060 6.938 .000

Consumer Price

Index

.002 .001 .559 3.633 .001

a. Dependent Variable: Exchange Rate

The regression test applied at a 95% confidence interval or 0.05 significance level, the p-

value obtained for the relationship between exchange rate as dependent and consumer price

index as independent variable shows that there exists relationship between dependent and

independent variable because the p-value 0.001 is less than the significance level 0.05 which

entails that alternative hypothesis must be accepted to conclude that there exists relationship

between exchange rate and consumer price index (Deringer, 2018).

Furthermore, the regression coefficient for PRI is .002. So, a positive sign indicates a

direct relationship between dependent and independent variable which in turn indicates that a

one unit rise in consumer price index would lead 0.002 increase in the exchange rate.

3. Improving the quality of the model

Variables included for improving the quality of the model is inflation rate.

Model Sum of

Squares

df Mean

Square

F Sig.

1 Regressio

n

.051 1 .051 13.201 .001b

Residual .112 29 .004

Total .163 30

a. Dependent Variable: Exchange Rate

b. Predictors: (Constant), Consumer Price Index

Coefficientsa

Model Unstandardized

Coefficients

Standardize

d

Coefficients

t Sig.

B Std. Error Beta

1 (Constant) .420 .060 6.938 .000

Consumer Price

Index

.002 .001 .559 3.633 .001

a. Dependent Variable: Exchange Rate

The regression test applied at a 95% confidence interval or 0.05 significance level, the p-

value obtained for the relationship between exchange rate as dependent and consumer price

index as independent variable shows that there exists relationship between dependent and

independent variable because the p-value 0.001 is less than the significance level 0.05 which

entails that alternative hypothesis must be accepted to conclude that there exists relationship

between exchange rate and consumer price index (Deringer, 2018).

Furthermore, the regression coefficient for PRI is .002. So, a positive sign indicates a

direct relationship between dependent and independent variable which in turn indicates that a

one unit rise in consumer price index would lead 0.002 increase in the exchange rate.

3. Improving the quality of the model

Variables included for improving the quality of the model is inflation rate.

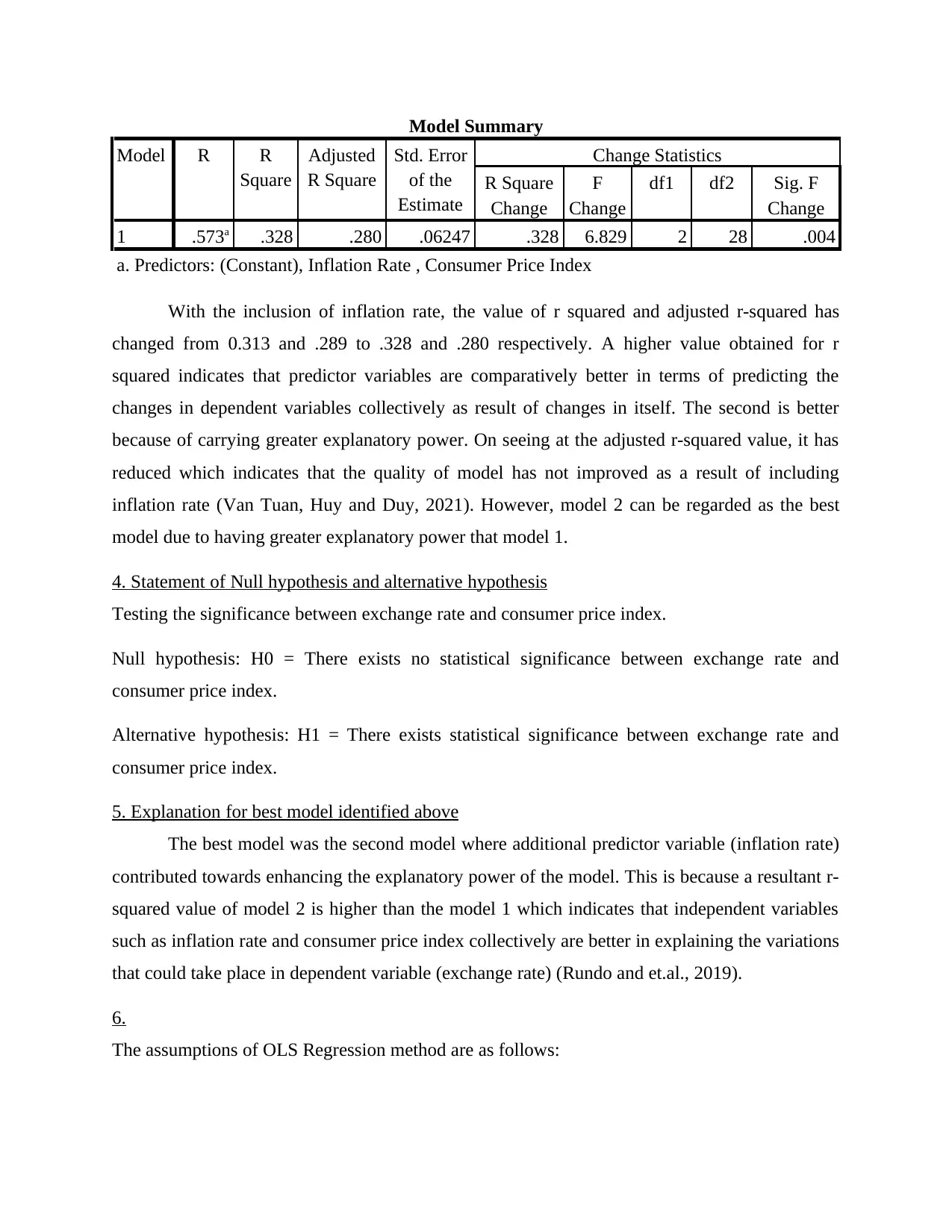

Model Summary

Model R R

Square

Adjusted

R Square

Std. Error

of the

Estimate

Change Statistics

R Square

Change

F

Change

df1 df2 Sig. F

Change

1 .573a .328 .280 .06247 .328 6.829 2 28 .004

a. Predictors: (Constant), Inflation Rate , Consumer Price Index

With the inclusion of inflation rate, the value of r squared and adjusted r-squared has

changed from 0.313 and .289 to .328 and .280 respectively. A higher value obtained for r

squared indicates that predictor variables are comparatively better in terms of predicting the

changes in dependent variables collectively as result of changes in itself. The second is better

because of carrying greater explanatory power. On seeing at the adjusted r-squared value, it has

reduced which indicates that the quality of model has not improved as a result of including

inflation rate (Van Tuan, Huy and Duy, 2021). However, model 2 can be regarded as the best

model due to having greater explanatory power that model 1.

4. Statement of Null hypothesis and alternative hypothesis

Testing the significance between exchange rate and consumer price index.

Null hypothesis: H0 = There exists no statistical significance between exchange rate and

consumer price index.

Alternative hypothesis: H1 = There exists statistical significance between exchange rate and

consumer price index.

5. Explanation for best model identified above

The best model was the second model where additional predictor variable (inflation rate)

contributed towards enhancing the explanatory power of the model. This is because a resultant r-

squared value of model 2 is higher than the model 1 which indicates that independent variables

such as inflation rate and consumer price index collectively are better in explaining the variations

that could take place in dependent variable (exchange rate) (Rundo and et.al., 2019).

6.

The assumptions of OLS Regression method are as follows:

Model R R

Square

Adjusted

R Square

Std. Error

of the

Estimate

Change Statistics

R Square

Change

F

Change

df1 df2 Sig. F

Change

1 .573a .328 .280 .06247 .328 6.829 2 28 .004

a. Predictors: (Constant), Inflation Rate , Consumer Price Index

With the inclusion of inflation rate, the value of r squared and adjusted r-squared has

changed from 0.313 and .289 to .328 and .280 respectively. A higher value obtained for r

squared indicates that predictor variables are comparatively better in terms of predicting the

changes in dependent variables collectively as result of changes in itself. The second is better

because of carrying greater explanatory power. On seeing at the adjusted r-squared value, it has

reduced which indicates that the quality of model has not improved as a result of including

inflation rate (Van Tuan, Huy and Duy, 2021). However, model 2 can be regarded as the best

model due to having greater explanatory power that model 1.

4. Statement of Null hypothesis and alternative hypothesis

Testing the significance between exchange rate and consumer price index.

Null hypothesis: H0 = There exists no statistical significance between exchange rate and

consumer price index.

Alternative hypothesis: H1 = There exists statistical significance between exchange rate and

consumer price index.

5. Explanation for best model identified above

The best model was the second model where additional predictor variable (inflation rate)

contributed towards enhancing the explanatory power of the model. This is because a resultant r-

squared value of model 2 is higher than the model 1 which indicates that independent variables

such as inflation rate and consumer price index collectively are better in explaining the variations

that could take place in dependent variable (exchange rate) (Rundo and et.al., 2019).

6.

The assumptions of OLS Regression method are as follows:

Errors are normally distributed: In order to check or test whether this particular

assumption is violated or not in the OLS regression model, the implicit factor need to be

check. It means if there is lack of independence within a sample and show apparent non-

normality by a few point indicate that the assumption of normality is violated. This affect

the p values which is used for significant testing (Bagheri Bodaghabadi, 2018). However,

this assumption violation does not contribute to bias and inefficiency in regression model

Homoscedasticity of errors: In case, if the graph shows the funnel shape to scattered plot

that this means that the assumption of homoscedasticity of errors are violated. The

homoscedasticity of error assumption indicates that across all the values of independent

variables, the variance of error term is similar. The impact of the violation of this

assumption on conclusion is that it makes coefficient less accurate. However, on the other

hand, this does not enhance the bias in the coefficient (Yang, Tu and Chen, 2019). The

assumption violation means the situation where assumption attached to specific statistical

procedure are not fulfilled. This affect the regression model with incorrect and

misleading results.

Errors are not serially correlated: This is another assumption of OLS regression method

which indicate that error term for different time periods are not correlated. In order to

check whether the errors are serially correlated or not, the Durbin Watson (DW) test need

to apply. This test is used for identifying the autocorrelation which value ranging between

1 to 4. With the help of this test, if the value of DW test come between 2 to 4 that it

means that the assumptions are not violated as it indicates no serially correlation (Das,

2019). But in case of value come below 2 to 0, this means the assumption of errors are

not serially correlated is violate. The impact of which misleading conclusion will be

drawn.

Task 2

1. Concept of Stationarity and its importance in time series analysis

Stationarity refers to the statistical properties of the time series that is deemed to be not changing

over the time. Accordingly, a time series is deemed to be having stationarity when the shifts or

changes in time doesn’t cause changes in the shape of distribution (Rundo and et.al., 2019). The

reason for which stationarity important in time series is its usefulness at the time of applying

assumption is violated or not in the OLS regression model, the implicit factor need to be

check. It means if there is lack of independence within a sample and show apparent non-

normality by a few point indicate that the assumption of normality is violated. This affect

the p values which is used for significant testing (Bagheri Bodaghabadi, 2018). However,

this assumption violation does not contribute to bias and inefficiency in regression model

Homoscedasticity of errors: In case, if the graph shows the funnel shape to scattered plot

that this means that the assumption of homoscedasticity of errors are violated. The

homoscedasticity of error assumption indicates that across all the values of independent

variables, the variance of error term is similar. The impact of the violation of this

assumption on conclusion is that it makes coefficient less accurate. However, on the other

hand, this does not enhance the bias in the coefficient (Yang, Tu and Chen, 2019). The

assumption violation means the situation where assumption attached to specific statistical

procedure are not fulfilled. This affect the regression model with incorrect and

misleading results.

Errors are not serially correlated: This is another assumption of OLS regression method

which indicate that error term for different time periods are not correlated. In order to

check whether the errors are serially correlated or not, the Durbin Watson (DW) test need

to apply. This test is used for identifying the autocorrelation which value ranging between

1 to 4. With the help of this test, if the value of DW test come between 2 to 4 that it

means that the assumptions are not violated as it indicates no serially correlation (Das,

2019). But in case of value come below 2 to 0, this means the assumption of errors are

not serially correlated is violate. The impact of which misleading conclusion will be

drawn.

Task 2

1. Concept of Stationarity and its importance in time series analysis

Stationarity refers to the statistical properties of the time series that is deemed to be not changing

over the time. Accordingly, a time series is deemed to be having stationarity when the shifts or

changes in time doesn’t cause changes in the shape of distribution (Rundo and et.al., 2019). The

reason for which stationarity important in time series is its usefulness at the time of applying

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

several analytical tools & models and tests in statistics which relies on it. Furthermore, it is

important because it helps in estimating parameters of a time series whose properties are not

going to change over the time in an easier and accurate manner. If the variance and mean of a

given time series keeps on changing over the time, there would be direct impact over the

accuracy of a time series over the time as well. Therefore, a time series that are affected by

trends or seasonality are not considered to be stationary as it affects the values with the series

over the time which in turn affects the value of its mean and variances.

2. In statistics, Dickey Fuller test is useful in testing the null hypothesis which indicates the

presence of unit root in an autoregressive model of time series. For the purpose of forecasting

and in order to ensure better prediction, stationary time series are used. To test the stationary,

Dicky Fuller test is being performed (Metu and Nwogwugwu, 2022). A unit root test is applied

to determine whether the time series is stationary or not which indicates the presence or absence

of unit root within the time series. When unit root is present, it defines that the null hypothesis

must be accepted for indicating the absence of stationarity while the alternative hypothesis is

meant for defining that the time series is stationary. In this way, Dicky Fuller test is useful in

determining whether the data series is stationary or not.

3. Augmented Dickey Fuller Test is known as the common statistical test meant for testing the

stationarity of time series which in turn gives results as the time series is stationary or not. Thus,

analysis of stationarity in time series is possible through Augmented Dickey Fuller Test. Dickey

Fuller test involves unit root testing for determining the presence or absence of stationarity with

the time series (Emerson and et.al., 2019). Unit roots are deemed to be causing unpredictable

results at the time of analyzing time series. However, Augmented Dickey Fuller test are used

with serial correlation meant for giving results indicating better prediction for the future.

Furthermore, Augmented Dickey Fuller Test is able to handle more complex models of time

series as compared to Dickey Fuller test, thus the former is considered to be more powerful than

the latter. In this way, ADF is utilized when the time series models are larger and complicated.

At last, the ADF statistic used in ADF test is a negative number and accordingly, when the

statistic is negative, there would be stronger rejection of the hypothesis that states that unit root is

present.

important because it helps in estimating parameters of a time series whose properties are not

going to change over the time in an easier and accurate manner. If the variance and mean of a

given time series keeps on changing over the time, there would be direct impact over the

accuracy of a time series over the time as well. Therefore, a time series that are affected by

trends or seasonality are not considered to be stationary as it affects the values with the series

over the time which in turn affects the value of its mean and variances.

2. In statistics, Dickey Fuller test is useful in testing the null hypothesis which indicates the

presence of unit root in an autoregressive model of time series. For the purpose of forecasting

and in order to ensure better prediction, stationary time series are used. To test the stationary,

Dicky Fuller test is being performed (Metu and Nwogwugwu, 2022). A unit root test is applied

to determine whether the time series is stationary or not which indicates the presence or absence

of unit root within the time series. When unit root is present, it defines that the null hypothesis

must be accepted for indicating the absence of stationarity while the alternative hypothesis is

meant for defining that the time series is stationary. In this way, Dicky Fuller test is useful in

determining whether the data series is stationary or not.

3. Augmented Dickey Fuller Test is known as the common statistical test meant for testing the

stationarity of time series which in turn gives results as the time series is stationary or not. Thus,

analysis of stationarity in time series is possible through Augmented Dickey Fuller Test. Dickey

Fuller test involves unit root testing for determining the presence or absence of stationarity with

the time series (Emerson and et.al., 2019). Unit roots are deemed to be causing unpredictable

results at the time of analyzing time series. However, Augmented Dickey Fuller test are used

with serial correlation meant for giving results indicating better prediction for the future.

Furthermore, Augmented Dickey Fuller Test is able to handle more complex models of time

series as compared to Dickey Fuller test, thus the former is considered to be more powerful than

the latter. In this way, ADF is utilized when the time series models are larger and complicated.

At last, the ADF statistic used in ADF test is a negative number and accordingly, when the

statistic is negative, there would be stronger rejection of the hypothesis that states that unit root is

present.

Task 3

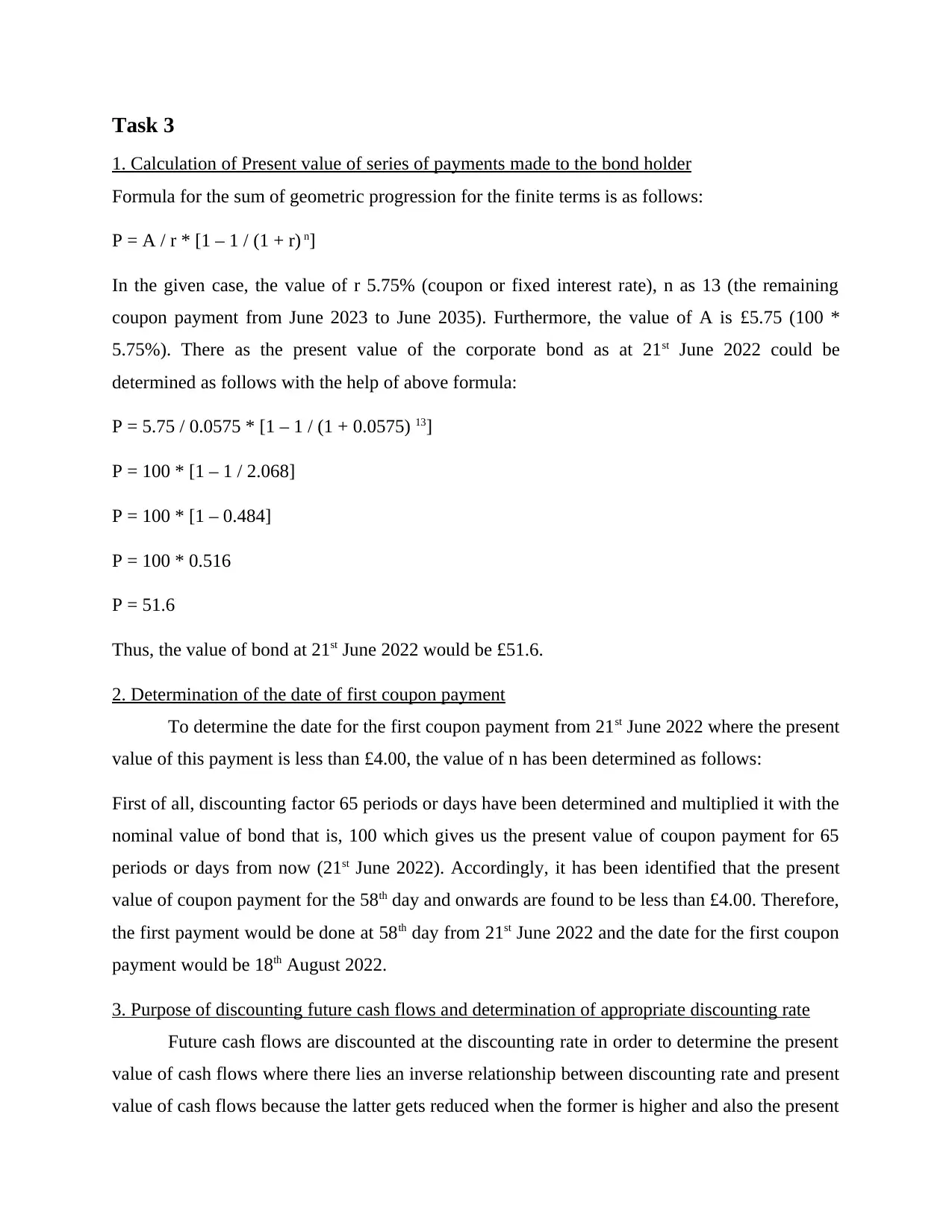

1. Calculation of Present value of series of payments made to the bond holder

Formula for the sum of geometric progression for the finite terms is as follows:

P = A / r * [1 – 1 / (1 + r) n]

In the given case, the value of r 5.75% (coupon or fixed interest rate), n as 13 (the remaining

coupon payment from June 2023 to June 2035). Furthermore, the value of A is £5.75 (100 *

5.75%). There as the present value of the corporate bond as at 21st June 2022 could be

determined as follows with the help of above formula:

P = 5.75 / 0.0575 * [1 – 1 / (1 + 0.0575) 13]

P = 100 * [1 – 1 / 2.068]

P = 100 * [1 – 0.484]

P = 100 * 0.516

P = 51.6

Thus, the value of bond at 21st June 2022 would be £51.6.

2. Determination of the date of first coupon payment

To determine the date for the first coupon payment from 21st June 2022 where the present

value of this payment is less than £4.00, the value of n has been determined as follows:

First of all, discounting factor 65 periods or days have been determined and multiplied it with the

nominal value of bond that is, 100 which gives us the present value of coupon payment for 65

periods or days from now (21st June 2022). Accordingly, it has been identified that the present

value of coupon payment for the 58th day and onwards are found to be less than £4.00. Therefore,

the first payment would be done at 58th day from 21st June 2022 and the date for the first coupon

payment would be 18th August 2022.

3. Purpose of discounting future cash flows and determination of appropriate discounting rate

Future cash flows are discounted at the discounting rate in order to determine the present

value of cash flows where there lies an inverse relationship between discounting rate and present

value of cash flows because the latter gets reduced when the former is higher and also the present

1. Calculation of Present value of series of payments made to the bond holder

Formula for the sum of geometric progression for the finite terms is as follows:

P = A / r * [1 – 1 / (1 + r) n]

In the given case, the value of r 5.75% (coupon or fixed interest rate), n as 13 (the remaining

coupon payment from June 2023 to June 2035). Furthermore, the value of A is £5.75 (100 *

5.75%). There as the present value of the corporate bond as at 21st June 2022 could be

determined as follows with the help of above formula:

P = 5.75 / 0.0575 * [1 – 1 / (1 + 0.0575) 13]

P = 100 * [1 – 1 / 2.068]

P = 100 * [1 – 0.484]

P = 100 * 0.516

P = 51.6

Thus, the value of bond at 21st June 2022 would be £51.6.

2. Determination of the date of first coupon payment

To determine the date for the first coupon payment from 21st June 2022 where the present

value of this payment is less than £4.00, the value of n has been determined as follows:

First of all, discounting factor 65 periods or days have been determined and multiplied it with the

nominal value of bond that is, 100 which gives us the present value of coupon payment for 65

periods or days from now (21st June 2022). Accordingly, it has been identified that the present

value of coupon payment for the 58th day and onwards are found to be less than £4.00. Therefore,

the first payment would be done at 58th day from 21st June 2022 and the date for the first coupon

payment would be 18th August 2022.

3. Purpose of discounting future cash flows and determination of appropriate discounting rate

Future cash flows are discounted at the discounting rate in order to determine the present

value of cash flows where there lies an inverse relationship between discounting rate and present

value of cash flows because the latter gets reduced when the former is higher and also the present

value of future cash flows increases with the reduction in the rate of discounting (Harvey, Liu

and Saretto, 2020). Accordingly, discounting refers to the process through which present value of

stream of payment or receipts that are going to take place in future is determined. This process

gives rise to the concept of time value of money which states that “the dollar is deemed to be

worth more as of today as company to what it would be worth tomorrow”. Discounting is known

as the price of stream of cash flows that are going to take place in the future. So, present value of

future cash flows is determined with the purpose to determine the current value of future cash

flow stream. Therefore, it is necessary to determine the appropriate rate for discounting future

cash flows. The discounting rate is the rate of return on investment which in alternative terms

known as the forgone rate of return for an investor while choosing to accept future receipts as

compared to the same amount today.

So, the purpose of discounting cash flows whether it is receipts or payments taking place in the

future is just to identify the equivalent value of the same amount if paid or received immediately.

Moreover, it is very important to appropriately determine the discounting rate for the purpose of

investing and reporting along with the assessment of viability of the financial project that the

company is going to undertake in the future (James, 2020). Accordingly, there are two methods

to for determining the rate for discounting future cash flows that is, weighted average cost of

capital and adjusted present value method. WACC in itself is used as the discounting rate which

can be determined with the help of following formula:

WACC = E/V x Ce + D/V x Cd x (1-T),

Where E is the equity value and D is the value of firm’s debt while V is the total value of the

business. Ce is the cost of equity while Cd is the cost of debt and T is the tax rate applicable on

the business.

Another method that is, adjusted present value where the cost of equity is used as the rate of

discounting and the formula is as follows:

APV = NPV + Present value of the impact of financing

and Saretto, 2020). Accordingly, discounting refers to the process through which present value of

stream of payment or receipts that are going to take place in future is determined. This process

gives rise to the concept of time value of money which states that “the dollar is deemed to be

worth more as of today as company to what it would be worth tomorrow”. Discounting is known

as the price of stream of cash flows that are going to take place in the future. So, present value of

future cash flows is determined with the purpose to determine the current value of future cash

flow stream. Therefore, it is necessary to determine the appropriate rate for discounting future

cash flows. The discounting rate is the rate of return on investment which in alternative terms

known as the forgone rate of return for an investor while choosing to accept future receipts as

compared to the same amount today.

So, the purpose of discounting cash flows whether it is receipts or payments taking place in the

future is just to identify the equivalent value of the same amount if paid or received immediately.

Moreover, it is very important to appropriately determine the discounting rate for the purpose of

investing and reporting along with the assessment of viability of the financial project that the

company is going to undertake in the future (James, 2020). Accordingly, there are two methods

to for determining the rate for discounting future cash flows that is, weighted average cost of

capital and adjusted present value method. WACC in itself is used as the discounting rate which

can be determined with the help of following formula:

WACC = E/V x Ce + D/V x Cd x (1-T),

Where E is the equity value and D is the value of firm’s debt while V is the total value of the

business. Ce is the cost of equity while Cd is the cost of debt and T is the tax rate applicable on

the business.

Another method that is, adjusted present value where the cost of equity is used as the rate of

discounting and the formula is as follows:

APV = NPV + Present value of the impact of financing

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

Task 4

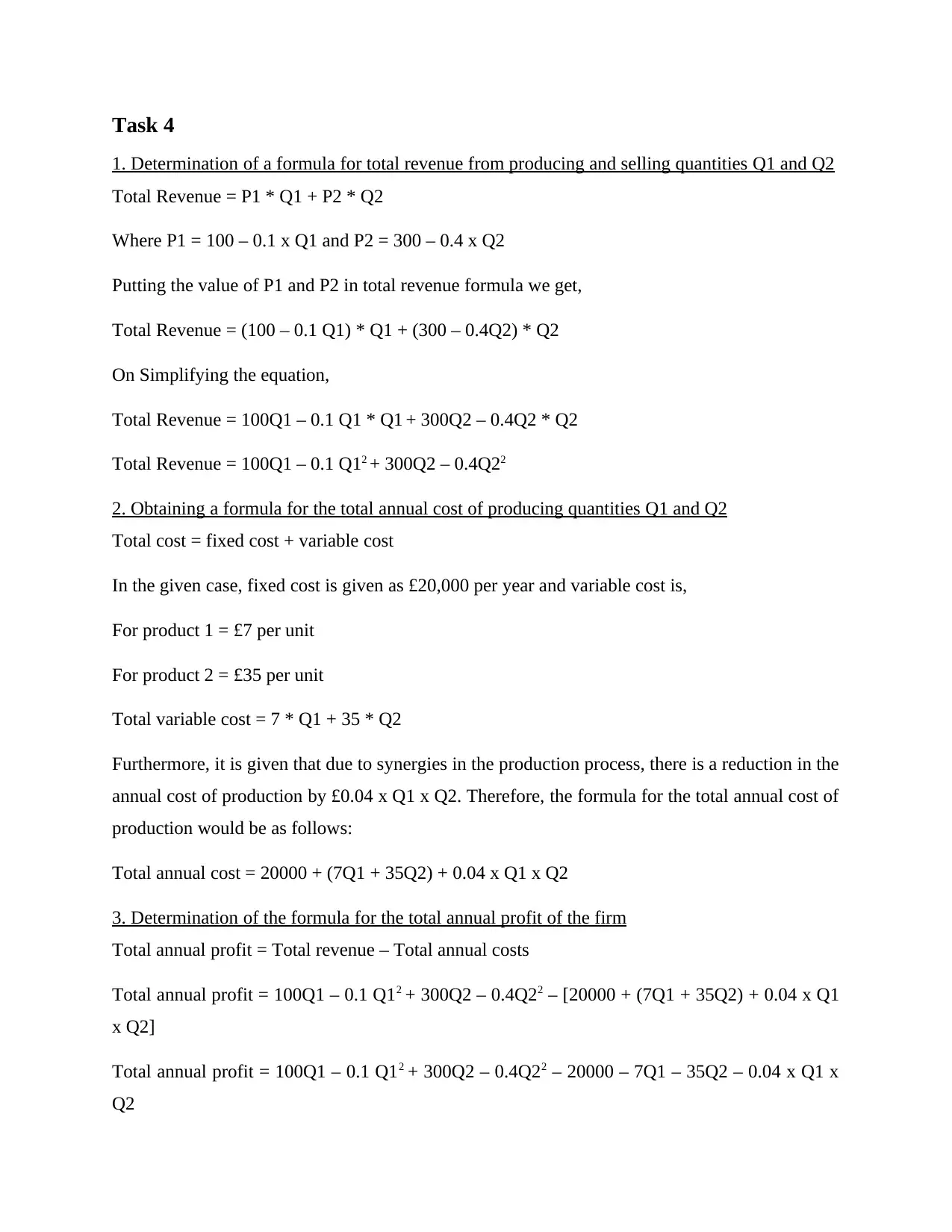

1. Determination of a formula for total revenue from producing and selling quantities Q1 and Q2

Total Revenue = P1 * Q1 + P2 * Q2

Where P1 = 100 – 0.1 x Q1 and P2 = 300 – 0.4 x Q2

Putting the value of P1 and P2 in total revenue formula we get,

Total Revenue = (100 – 0.1 Q1) * Q1 + (300 – 0.4Q2) * Q2

On Simplifying the equation,

Total Revenue = 100Q1 – 0.1 Q1 * Q1 + 300Q2 – 0.4Q2 * Q2

Total Revenue = 100Q1 – 0.1 Q12 + 300Q2 – 0.4Q22

2. Obtaining a formula for the total annual cost of producing quantities Q1 and Q2

Total cost = fixed cost + variable cost

In the given case, fixed cost is given as £20,000 per year and variable cost is,

For product 1 = £7 per unit

For product 2 = £35 per unit

Total variable cost = 7 * Q1 + 35 * Q2

Furthermore, it is given that due to synergies in the production process, there is a reduction in the

annual cost of production by £0.04 x Q1 x Q2. Therefore, the formula for the total annual cost of

production would be as follows:

Total annual cost = 20000 + (7Q1 + 35Q2) + 0.04 x Q1 x Q2

3. Determination of the formula for the total annual profit of the firm

Total annual profit = Total revenue – Total annual costs

Total annual profit = 100Q1 – 0.1 Q12 + 300Q2 – 0.4Q22 – [20000 + (7Q1 + 35Q2) + 0.04 x Q1

x Q2]

Total annual profit = 100Q1 – 0.1 Q12 + 300Q2 – 0.4Q22 – 20000 – 7Q1 – 35Q2 – 0.04 x Q1 x

Q2

1. Determination of a formula for total revenue from producing and selling quantities Q1 and Q2

Total Revenue = P1 * Q1 + P2 * Q2

Where P1 = 100 – 0.1 x Q1 and P2 = 300 – 0.4 x Q2

Putting the value of P1 and P2 in total revenue formula we get,

Total Revenue = (100 – 0.1 Q1) * Q1 + (300 – 0.4Q2) * Q2

On Simplifying the equation,

Total Revenue = 100Q1 – 0.1 Q1 * Q1 + 300Q2 – 0.4Q2 * Q2

Total Revenue = 100Q1 – 0.1 Q12 + 300Q2 – 0.4Q22

2. Obtaining a formula for the total annual cost of producing quantities Q1 and Q2

Total cost = fixed cost + variable cost

In the given case, fixed cost is given as £20,000 per year and variable cost is,

For product 1 = £7 per unit

For product 2 = £35 per unit

Total variable cost = 7 * Q1 + 35 * Q2

Furthermore, it is given that due to synergies in the production process, there is a reduction in the

annual cost of production by £0.04 x Q1 x Q2. Therefore, the formula for the total annual cost of

production would be as follows:

Total annual cost = 20000 + (7Q1 + 35Q2) + 0.04 x Q1 x Q2

3. Determination of the formula for the total annual profit of the firm

Total annual profit = Total revenue – Total annual costs

Total annual profit = 100Q1 – 0.1 Q12 + 300Q2 – 0.4Q22 – [20000 + (7Q1 + 35Q2) + 0.04 x Q1

x Q2]

Total annual profit = 100Q1 – 0.1 Q12 + 300Q2 – 0.4Q22 – 20000 – 7Q1 – 35Q2 – 0.04 x Q1 x

Q2

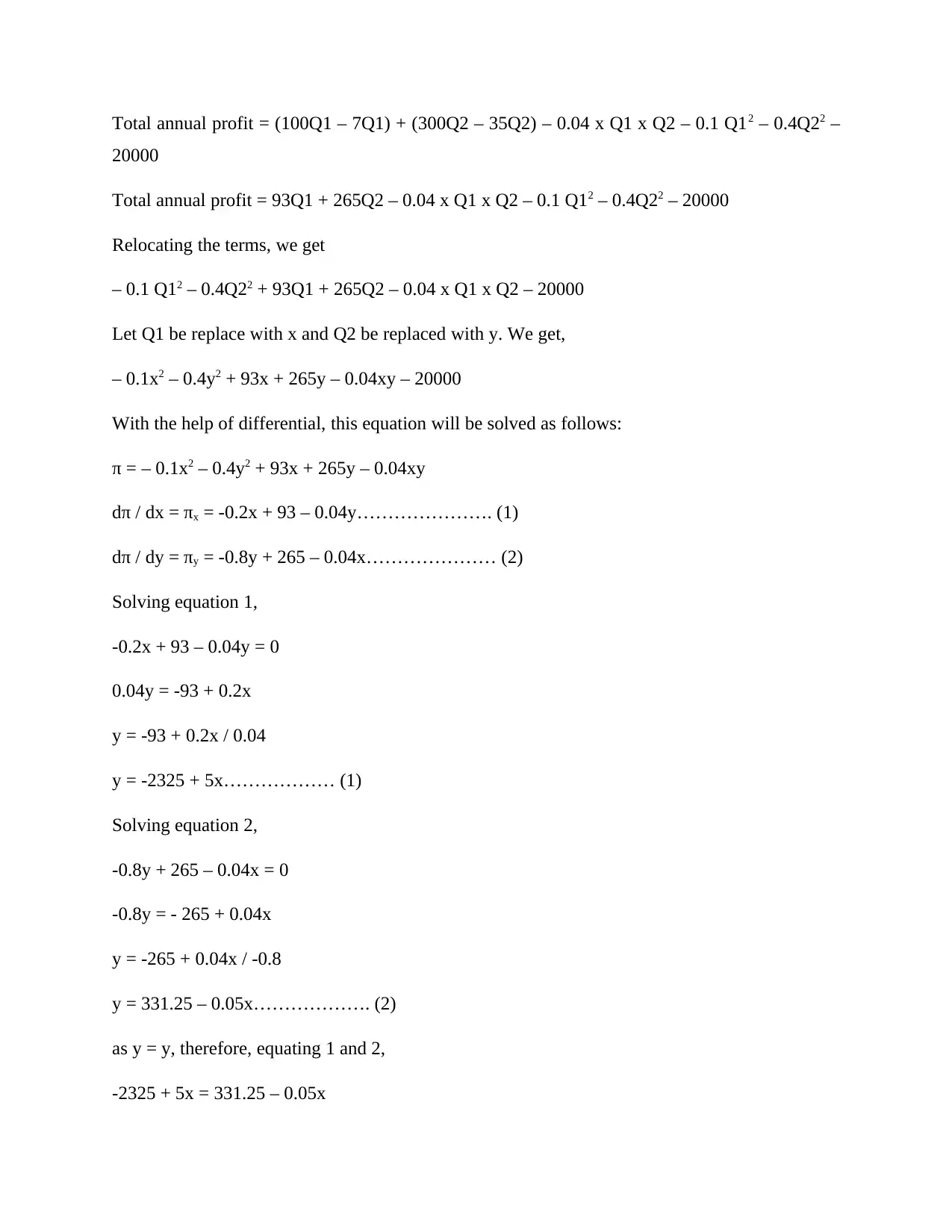

Total annual profit = (100Q1 – 7Q1) + (300Q2 – 35Q2) – 0.04 x Q1 x Q2 – 0.1 Q12 – 0.4Q22 –

20000

Total annual profit = 93Q1 + 265Q2 – 0.04 x Q1 x Q2 – 0.1 Q12 – 0.4Q22 – 20000

Relocating the terms, we get

– 0.1 Q12 – 0.4Q22 + 93Q1 + 265Q2 – 0.04 x Q1 x Q2 – 20000

Let Q1 be replace with x and Q2 be replaced with y. We get,

– 0.1x2 – 0.4y2 + 93x + 265y – 0.04xy – 20000

With the help of differential, this equation will be solved as follows:

π = – 0.1x2 – 0.4y2 + 93x + 265y – 0.04xy

dπ / dx = πx = -0.2x + 93 – 0.04y…………………. (1)

dπ / dy = πy = -0.8y + 265 – 0.04x………………… (2)

Solving equation 1,

-0.2x + 93 – 0.04y = 0

0.04y = -93 + 0.2x

y = -93 + 0.2x / 0.04

y = -2325 + 5x……………… (1)

Solving equation 2,

-0.8y + 265 – 0.04x = 0

-0.8y = - 265 + 0.04x

y = -265 + 0.04x / -0.8

y = 331.25 – 0.05x………………. (2)

as y = y, therefore, equating 1 and 2,

-2325 + 5x = 331.25 – 0.05x

20000

Total annual profit = 93Q1 + 265Q2 – 0.04 x Q1 x Q2 – 0.1 Q12 – 0.4Q22 – 20000

Relocating the terms, we get

– 0.1 Q12 – 0.4Q22 + 93Q1 + 265Q2 – 0.04 x Q1 x Q2 – 20000

Let Q1 be replace with x and Q2 be replaced with y. We get,

– 0.1x2 – 0.4y2 + 93x + 265y – 0.04xy – 20000

With the help of differential, this equation will be solved as follows:

π = – 0.1x2 – 0.4y2 + 93x + 265y – 0.04xy

dπ / dx = πx = -0.2x + 93 – 0.04y…………………. (1)

dπ / dy = πy = -0.8y + 265 – 0.04x………………… (2)

Solving equation 1,

-0.2x + 93 – 0.04y = 0

0.04y = -93 + 0.2x

y = -93 + 0.2x / 0.04

y = -2325 + 5x……………… (1)

Solving equation 2,

-0.8y + 265 – 0.04x = 0

-0.8y = - 265 + 0.04x

y = -265 + 0.04x / -0.8

y = 331.25 – 0.05x………………. (2)

as y = y, therefore, equating 1 and 2,

-2325 + 5x = 331.25 – 0.05x

5x + 0.05x = 331.25 + 2325

5.05x = 2656.25

x = 2656.25 / 5.05 = 525.99 or 526

y = 331.25 – 0.05 * 526

y = 331.25 – 26.3

y = 304.95 or 305

Therefore, Q1 and Q2 are 526 and 305 units respectively which are known as the profit

maximizing units.

Thus, by putting the values of Q1 and Q2 in the profit maximizing price equations that is, P1 and

P2 for product 1 and product 2 respectively, the price at which both the products would be sold

to generate maximum profits can be determined as follows:

P1 = 100 – 0.1 x Q1

P1 = 100 – 0.1 * 526

P1 = 100 – 52.6

P1 = £47.4

P2 = 300 – 0.4 x Q2

P2 = 300 – 0.4 * 305

P2 = 300 – 122

P2 = £178

Accordingly, with the maximum profit would be determined as follows:

Total revenue = P1 * Q1 + P2 * Q2

Total revenue = 47.4 * 526 + 178 * 305

Total revenue = 24932.4 + 54290

5.05x = 2656.25

x = 2656.25 / 5.05 = 525.99 or 526

y = 331.25 – 0.05 * 526

y = 331.25 – 26.3

y = 304.95 or 305

Therefore, Q1 and Q2 are 526 and 305 units respectively which are known as the profit

maximizing units.

Thus, by putting the values of Q1 and Q2 in the profit maximizing price equations that is, P1 and

P2 for product 1 and product 2 respectively, the price at which both the products would be sold

to generate maximum profits can be determined as follows:

P1 = 100 – 0.1 x Q1

P1 = 100 – 0.1 * 526

P1 = 100 – 52.6

P1 = £47.4

P2 = 300 – 0.4 x Q2

P2 = 300 – 0.4 * 305

P2 = 300 – 122

P2 = £178

Accordingly, with the maximum profit would be determined as follows:

Total revenue = P1 * Q1 + P2 * Q2

Total revenue = 47.4 * 526 + 178 * 305

Total revenue = 24932.4 + 54290

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Total revenue = £79222.4

Total annual cost = 20000 + (7Q1 + 35Q2) + 0.04 x Q1 x Q2

Total annual cost = 20000 + 7 * 526 + 35 * 305 + 0.04 * 526 * 305

Total annual cost = 20000 + 3682 + 10675 + 6417.2

Total annual cost = £40774.2

Maximum profit = £79222.4 - £40774.2

Maximum profit = £38448.2

Total annual cost = 20000 + (7Q1 + 35Q2) + 0.04 x Q1 x Q2

Total annual cost = 20000 + 7 * 526 + 35 * 305 + 0.04 * 526 * 305

Total annual cost = 20000 + 3682 + 10675 + 6417.2

Total annual cost = £40774.2

Maximum profit = £79222.4 - £40774.2

Maximum profit = £38448.2

REFERENCES

Bagheri Bodaghabadi, M., 2018. Is it necessarily a normally distributed data for kriging? A case

study: soil salinity map of Ghahab area, central Iran. Desert. 23(2). pp.284-293.

Yang, K., Tu, J. and Chen, T., 2019. Homoscedasticity: An overlooked critical assumption for

linear regression. General psychiatry. 32(5).

Das, P., 2019. Linear Regression Model: Relaxing the Classical Assumptions. In Econometrics

in Theory and Practice (pp. 109-135). Springer, Singapore.

James, R., 2020. Quantitative Methods in Empirical Finance: Insights into Economic

Forecasting, Designing Financial Market Surveillance Systems and Modeling Extreme

Returns (Doctoral dissertation).

Harvey, C. R., Liu, Y. and Saretto, A., 2020. An evaluation of alternative multiple testing

methods for finance applications. The Review of Asset Pricing Studies, 10(2), pp.199-

248.

Emerson, S., and et.al., 2019, May. Trends and applications of machine learning in quantitative

finance. In 8th international conference on economics and finance research (ICEFR

2019).

Metu, A. G. and Nwogwugwu, U. C., 2022. Challenging Factors Affecting Access to Finance by

Female Micro Entrepreneurs in Anambra State, Nigeria. Journal of African Business,

pp.1-13.

Rundo, F., and et.al., 2019. Machine learning for quantitative finance applications: A

survey. Applied Sciences, 9(24), p.5574.

Van Tuan, P., Huy, D. T. N. and Duy, P. K., 2021. Impacts of Competitor Selection Strategy on

Firm Risk-Case in Vietnam Investment and Finance Industry. Revista Geintec-Gestao

Inovacao E Tecnologias, 11(3), pp.127-135.

Deringer, W., 2018. Calculated values: Finance, politics, and the quantitative age. Harvard

University Press.

Bagheri Bodaghabadi, M., 2018. Is it necessarily a normally distributed data for kriging? A case

study: soil salinity map of Ghahab area, central Iran. Desert. 23(2). pp.284-293.

Yang, K., Tu, J. and Chen, T., 2019. Homoscedasticity: An overlooked critical assumption for

linear regression. General psychiatry. 32(5).

Das, P., 2019. Linear Regression Model: Relaxing the Classical Assumptions. In Econometrics

in Theory and Practice (pp. 109-135). Springer, Singapore.

James, R., 2020. Quantitative Methods in Empirical Finance: Insights into Economic

Forecasting, Designing Financial Market Surveillance Systems and Modeling Extreme

Returns (Doctoral dissertation).

Harvey, C. R., Liu, Y. and Saretto, A., 2020. An evaluation of alternative multiple testing

methods for finance applications. The Review of Asset Pricing Studies, 10(2), pp.199-

248.

Emerson, S., and et.al., 2019, May. Trends and applications of machine learning in quantitative

finance. In 8th international conference on economics and finance research (ICEFR

2019).

Metu, A. G. and Nwogwugwu, U. C., 2022. Challenging Factors Affecting Access to Finance by

Female Micro Entrepreneurs in Anambra State, Nigeria. Journal of African Business,

pp.1-13.

Rundo, F., and et.al., 2019. Machine learning for quantitative finance applications: A

survey. Applied Sciences, 9(24), p.5574.

Van Tuan, P., Huy, D. T. N. and Duy, P. K., 2021. Impacts of Competitor Selection Strategy on

Firm Risk-Case in Vietnam Investment and Finance Industry. Revista Geintec-Gestao

Inovacao E Tecnologias, 11(3), pp.127-135.

Deringer, W., 2018. Calculated values: Finance, politics, and the quantitative age. Harvard

University Press.

1 out of 16

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

© 2024 | Zucol Services PVT LTD | All rights reserved.