Discount Schemes Analysis for BLC Limited

VerifiedAdded on 2020/05/28

|10

|1722

|78

AI Summary

This assignment analyzes the potential benefits and drawbacks of a new discount scheme offered by BLC Limited to customers. The analysis focuses on comparing the cost of offering discounts (interest incurred on overdrafts due to delayed payments) with the resulting savings from reduced bad debts. The report includes a detailed assessment of the current scheme's performance, the proposed discount scheme's potential impact, and a final recommendation for BLC Limited based on the cost-benefit analysis.

Contribute Materials

Your contribution can guide someone’s learning journey. Share your

documents today.

Running Head: ADVANCE FINANCIAL ACCOUNTING

Advance financial accounting

Name of the Student

Name of the University

Author Note

Advance financial accounting

Name of the Student

Name of the University

Author Note

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

1

ADVANCE FINANCIAL ACCOUNTING

Table of Contents

Introduction:..............................................................................................................................3

Case study assignment Part A:..................................................................................................3

Computing the net present value, internal rate of return and payback period:......................3

Evaluation of qualitative factors influencing the decisions:..................................................5

Case Study Assignment Part B:.................................................................................................5

Computation of approximate equivalent annual percentage cost:.........................................5

Computation of value of trade receivables:...........................................................................6

Evaluation of schemes of cost and benefits:..........................................................................6

Conclusions and Recommendation:......................................................................................7

References and Bibliography list:..............................................................................................8

ADVANCE FINANCIAL ACCOUNTING

Table of Contents

Introduction:..............................................................................................................................3

Case study assignment Part A:..................................................................................................3

Computing the net present value, internal rate of return and payback period:......................3

Evaluation of qualitative factors influencing the decisions:..................................................5

Case Study Assignment Part B:.................................................................................................5

Computation of approximate equivalent annual percentage cost:.........................................5

Computation of value of trade receivables:...........................................................................6

Evaluation of schemes of cost and benefits:..........................................................................6

Conclusions and Recommendation:......................................................................................7

References and Bibliography list:..............................................................................................8

2

ADVANCE FINANCIAL ACCOUNTING

ADVANCE FINANCIAL ACCOUNTING

3

ADVANCE FINANCIAL ACCOUNTING

Introduction:

In this particular assignment, there are two case study analyses. First part involves case

about BLC limited that is a medium sized company based in United Kingdom. Company seeks

to employ the technique of capital budgeting for evaluating its project of establishing office. Nest

case is about discussion of discount cost and its influence of business. Detailed analysis of both

the case study is done by explanations and calculations.

Case study assignment Part A:

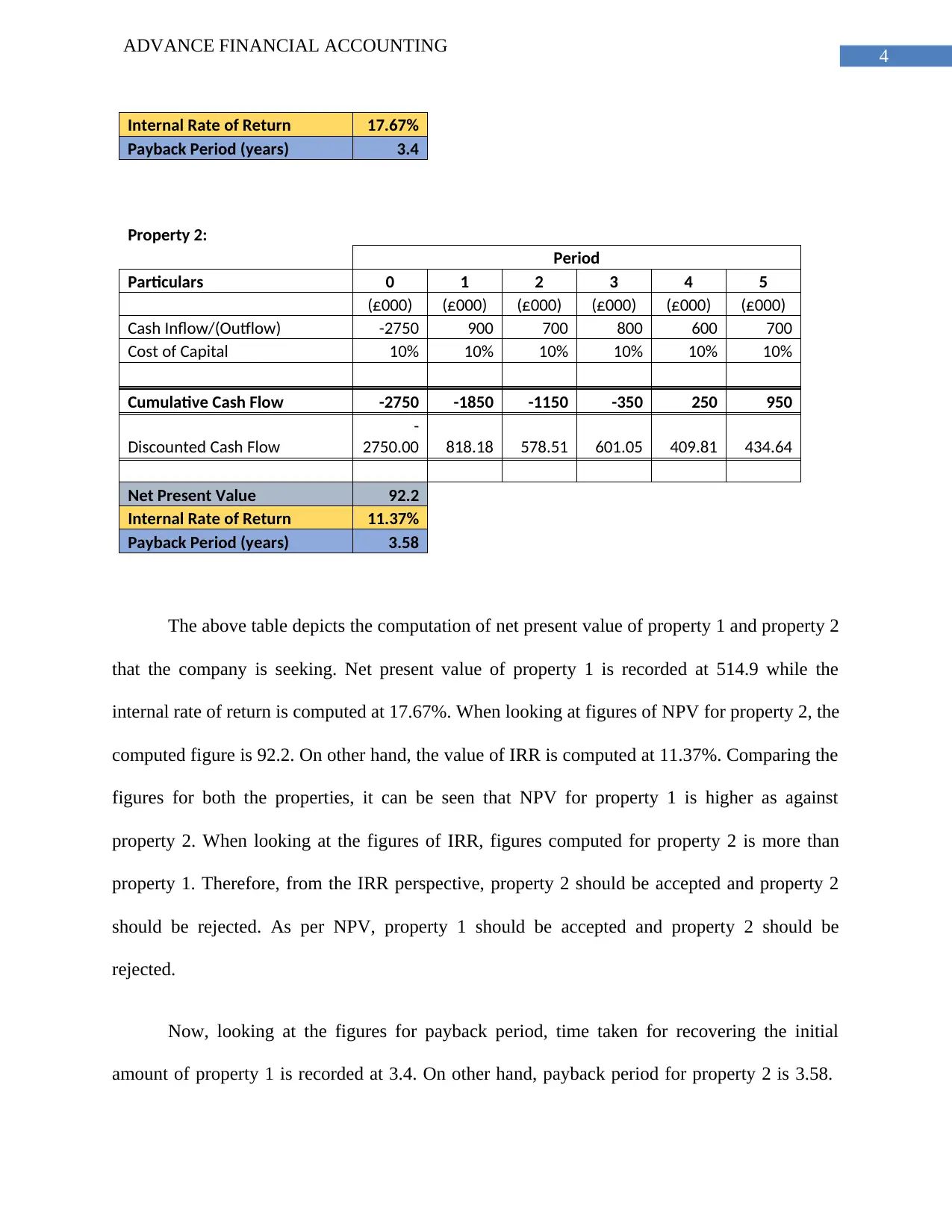

Computing the net present value, internal rate of return and payback period:

For the calculations of above these metrics, company has made the assumption of cost of

capital at the rate of 10%. As per the rule, project generating higher net present value should be

accepted compared to project generating lower net present value (Chittenden and Derregia

2015). Project evaluation based on IRR depicts that project generating IRR higher than cost of

capital will be accepted and vice versa. Project that has higher payback period should be rejected

as against lower payback (Andor et al. 2015).

Property 1:

Period

Particulars 0 1 2 3 4 5

(£000) (£000) (£000) (£000) (£000) (£000)

Cash Inflow/(Outflow) -2500 1000 500 600 1000 900

Cost of Capital 10% 10% 10% 10% 10% 10%

Cumulative Cash Flow -2500 -1500 -1000 -400 600 1500

Discounted Cash Flow

-

2500.00 909.09 413.22 450.79 683.01 558.83

Net Present Value 514.9

ADVANCE FINANCIAL ACCOUNTING

Introduction:

In this particular assignment, there are two case study analyses. First part involves case

about BLC limited that is a medium sized company based in United Kingdom. Company seeks

to employ the technique of capital budgeting for evaluating its project of establishing office. Nest

case is about discussion of discount cost and its influence of business. Detailed analysis of both

the case study is done by explanations and calculations.

Case study assignment Part A:

Computing the net present value, internal rate of return and payback period:

For the calculations of above these metrics, company has made the assumption of cost of

capital at the rate of 10%. As per the rule, project generating higher net present value should be

accepted compared to project generating lower net present value (Chittenden and Derregia

2015). Project evaluation based on IRR depicts that project generating IRR higher than cost of

capital will be accepted and vice versa. Project that has higher payback period should be rejected

as against lower payback (Andor et al. 2015).

Property 1:

Period

Particulars 0 1 2 3 4 5

(£000) (£000) (£000) (£000) (£000) (£000)

Cash Inflow/(Outflow) -2500 1000 500 600 1000 900

Cost of Capital 10% 10% 10% 10% 10% 10%

Cumulative Cash Flow -2500 -1500 -1000 -400 600 1500

Discounted Cash Flow

-

2500.00 909.09 413.22 450.79 683.01 558.83

Net Present Value 514.9

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

4

ADVANCE FINANCIAL ACCOUNTING

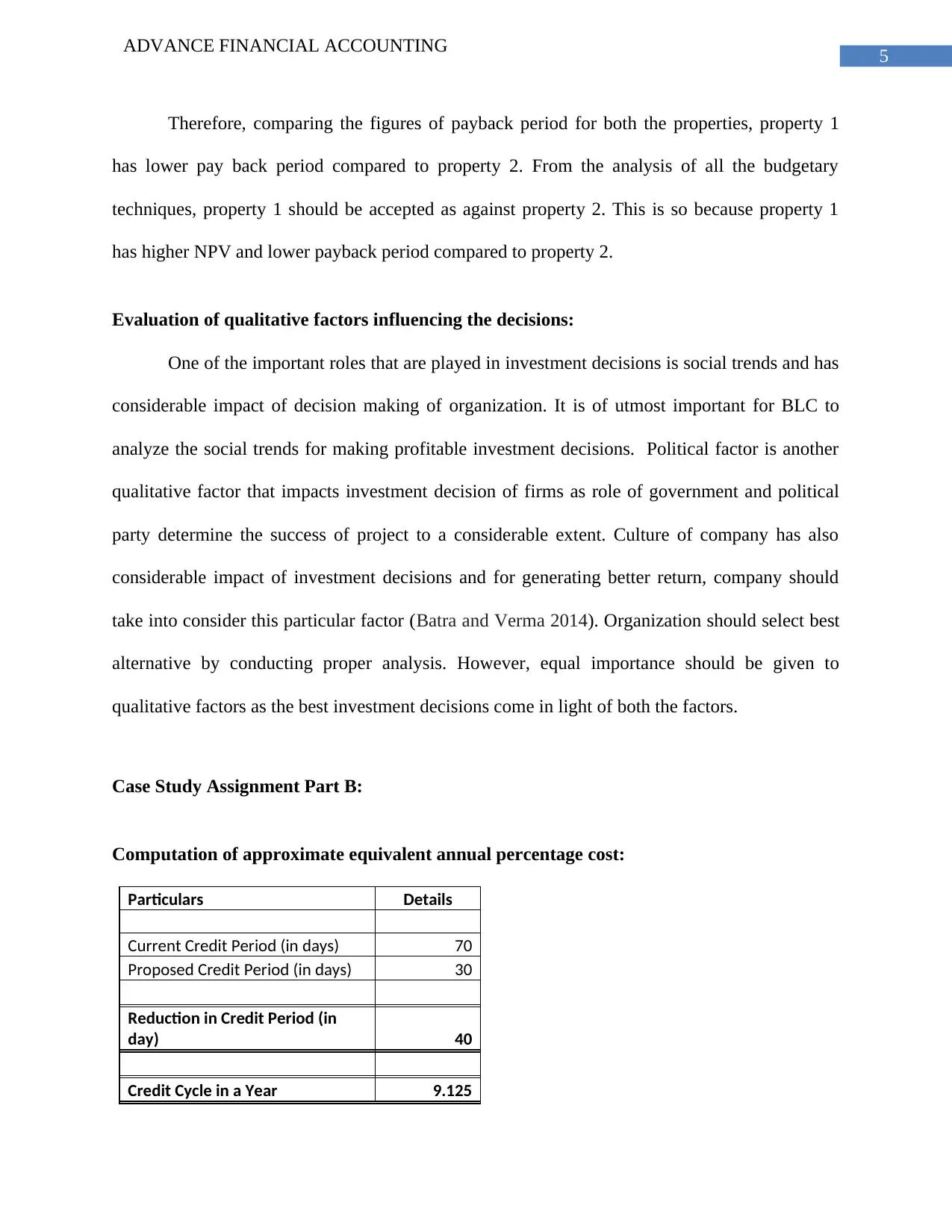

Internal Rate of Return 17.67%

Payback Period (years) 3.4

Property 2:

Period

Particulars 0 1 2 3 4 5

(£000) (£000) (£000) (£000) (£000) (£000)

Cash Inflow/(Outflow) -2750 900 700 800 600 700

Cost of Capital 10% 10% 10% 10% 10% 10%

Cumulative Cash Flow -2750 -1850 -1150 -350 250 950

Discounted Cash Flow

-

2750.00 818.18 578.51 601.05 409.81 434.64

Net Present Value 92.2

Internal Rate of Return 11.37%

Payback Period (years) 3.58

The above table depicts the computation of net present value of property 1 and property 2

that the company is seeking. Net present value of property 1 is recorded at 514.9 while the

internal rate of return is computed at 17.67%. When looking at figures of NPV for property 2, the

computed figure is 92.2. On other hand, the value of IRR is computed at 11.37%. Comparing the

figures for both the properties, it can be seen that NPV for property 1 is higher as against

property 2. When looking at the figures of IRR, figures computed for property 2 is more than

property 1. Therefore, from the IRR perspective, property 2 should be accepted and property 2

should be rejected. As per NPV, property 1 should be accepted and property 2 should be

rejected.

Now, looking at the figures for payback period, time taken for recovering the initial

amount of property 1 is recorded at 3.4. On other hand, payback period for property 2 is 3.58.

ADVANCE FINANCIAL ACCOUNTING

Internal Rate of Return 17.67%

Payback Period (years) 3.4

Property 2:

Period

Particulars 0 1 2 3 4 5

(£000) (£000) (£000) (£000) (£000) (£000)

Cash Inflow/(Outflow) -2750 900 700 800 600 700

Cost of Capital 10% 10% 10% 10% 10% 10%

Cumulative Cash Flow -2750 -1850 -1150 -350 250 950

Discounted Cash Flow

-

2750.00 818.18 578.51 601.05 409.81 434.64

Net Present Value 92.2

Internal Rate of Return 11.37%

Payback Period (years) 3.58

The above table depicts the computation of net present value of property 1 and property 2

that the company is seeking. Net present value of property 1 is recorded at 514.9 while the

internal rate of return is computed at 17.67%. When looking at figures of NPV for property 2, the

computed figure is 92.2. On other hand, the value of IRR is computed at 11.37%. Comparing the

figures for both the properties, it can be seen that NPV for property 1 is higher as against

property 2. When looking at the figures of IRR, figures computed for property 2 is more than

property 1. Therefore, from the IRR perspective, property 2 should be accepted and property 2

should be rejected. As per NPV, property 1 should be accepted and property 2 should be

rejected.

Now, looking at the figures for payback period, time taken for recovering the initial

amount of property 1 is recorded at 3.4. On other hand, payback period for property 2 is 3.58.

5

ADVANCE FINANCIAL ACCOUNTING

Therefore, comparing the figures of payback period for both the properties, property 1

has lower pay back period compared to property 2. From the analysis of all the budgetary

techniques, property 1 should be accepted as against property 2. This is so because property 1

has higher NPV and lower payback period compared to property 2.

Evaluation of qualitative factors influencing the decisions:

One of the important roles that are played in investment decisions is social trends and has

considerable impact of decision making of organization. It is of utmost important for BLC to

analyze the social trends for making profitable investment decisions. Political factor is another

qualitative factor that impacts investment decision of firms as role of government and political

party determine the success of project to a considerable extent. Culture of company has also

considerable impact of investment decisions and for generating better return, company should

take into consider this particular factor (Batra and Verma 2014). Organization should select best

alternative by conducting proper analysis. However, equal importance should be given to

qualitative factors as the best investment decisions come in light of both the factors.

Case Study Assignment Part B:

Computation of approximate equivalent annual percentage cost:

Particulars Details

Current Credit Period (in days) 70

Proposed Credit Period (in days) 30

Reduction in Credit Period (in

day) 40

Credit Cycle in a Year 9.125

ADVANCE FINANCIAL ACCOUNTING

Therefore, comparing the figures of payback period for both the properties, property 1

has lower pay back period compared to property 2. From the analysis of all the budgetary

techniques, property 1 should be accepted as against property 2. This is so because property 1

has higher NPV and lower payback period compared to property 2.

Evaluation of qualitative factors influencing the decisions:

One of the important roles that are played in investment decisions is social trends and has

considerable impact of decision making of organization. It is of utmost important for BLC to

analyze the social trends for making profitable investment decisions. Political factor is another

qualitative factor that impacts investment decision of firms as role of government and political

party determine the success of project to a considerable extent. Culture of company has also

considerable impact of investment decisions and for generating better return, company should

take into consider this particular factor (Batra and Verma 2014). Organization should select best

alternative by conducting proper analysis. However, equal importance should be given to

qualitative factors as the best investment decisions come in light of both the factors.

Case Study Assignment Part B:

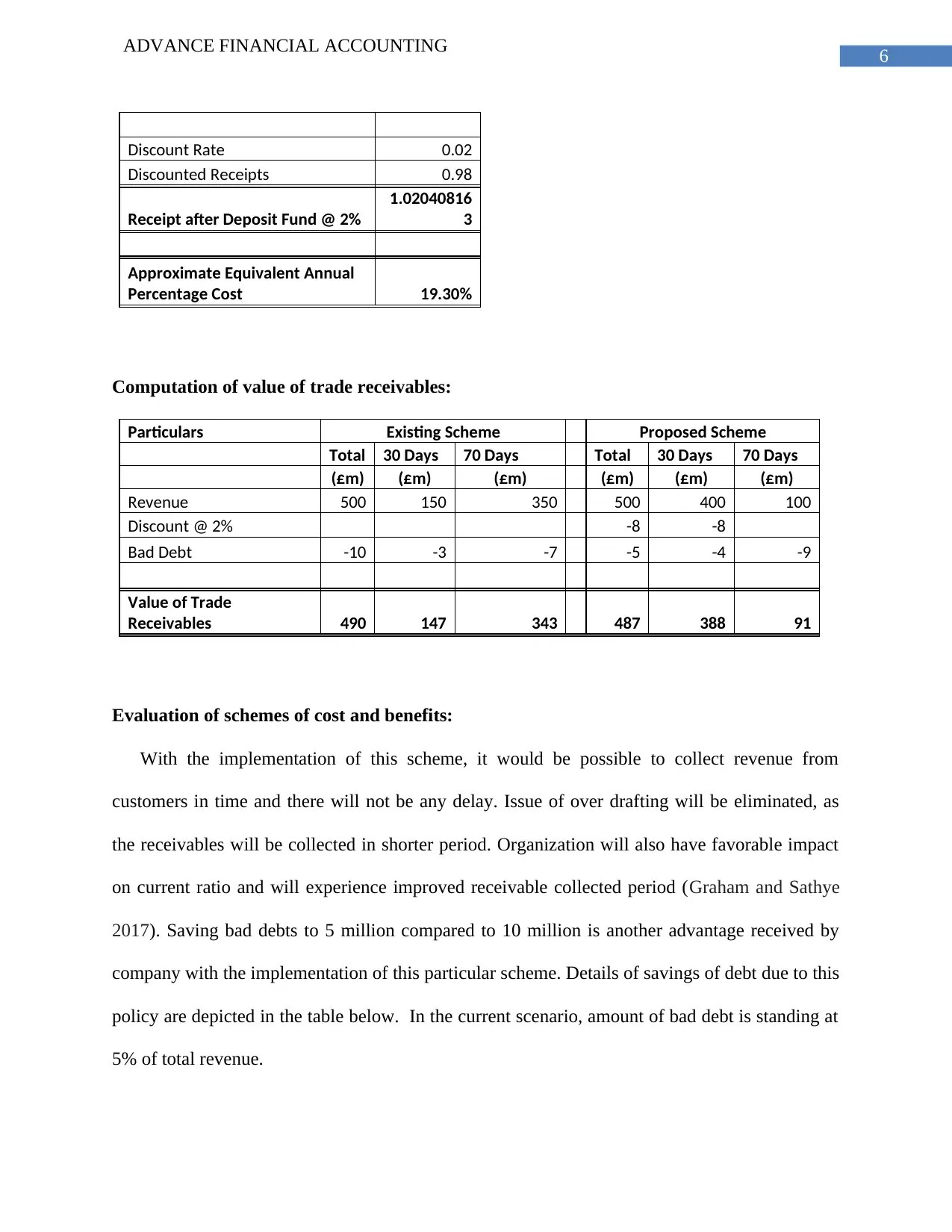

Computation of approximate equivalent annual percentage cost:

Particulars Details

Current Credit Period (in days) 70

Proposed Credit Period (in days) 30

Reduction in Credit Period (in

day) 40

Credit Cycle in a Year 9.125

6

ADVANCE FINANCIAL ACCOUNTING

Discount Rate 0.02

Discounted Receipts 0.98

Receipt after Deposit Fund @ 2%

1.02040816

3

Approximate Equivalent Annual

Percentage Cost 19.30%

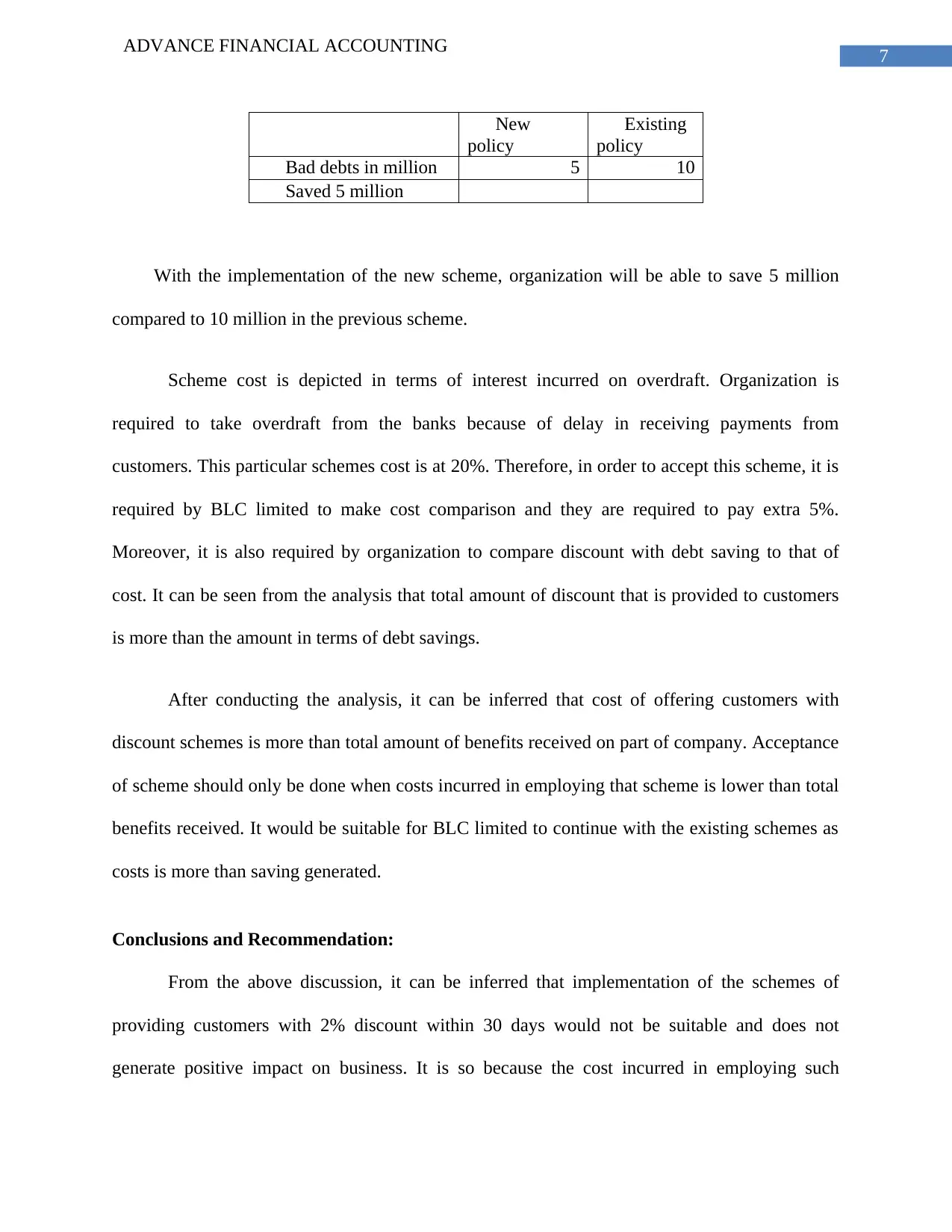

Computation of value of trade receivables:

Particulars Existing Scheme Proposed Scheme

Total 30 Days 70 Days Total 30 Days 70 Days

(£m) (£m) (£m) (£m) (£m) (£m)

Revenue 500 150 350 500 400 100

Discount @ 2% -8 -8

Bad Debt -10 -3 -7 -5 -4 -9

Value of Trade

Receivables 490 147 343 487 388 91

Evaluation of schemes of cost and benefits:

With the implementation of this scheme, it would be possible to collect revenue from

customers in time and there will not be any delay. Issue of over drafting will be eliminated, as

the receivables will be collected in shorter period. Organization will also have favorable impact

on current ratio and will experience improved receivable collected period (Graham and Sathye

2017). Saving bad debts to 5 million compared to 10 million is another advantage received by

company with the implementation of this particular scheme. Details of savings of debt due to this

policy are depicted in the table below. In the current scenario, amount of bad debt is standing at

5% of total revenue.

ADVANCE FINANCIAL ACCOUNTING

Discount Rate 0.02

Discounted Receipts 0.98

Receipt after Deposit Fund @ 2%

1.02040816

3

Approximate Equivalent Annual

Percentage Cost 19.30%

Computation of value of trade receivables:

Particulars Existing Scheme Proposed Scheme

Total 30 Days 70 Days Total 30 Days 70 Days

(£m) (£m) (£m) (£m) (£m) (£m)

Revenue 500 150 350 500 400 100

Discount @ 2% -8 -8

Bad Debt -10 -3 -7 -5 -4 -9

Value of Trade

Receivables 490 147 343 487 388 91

Evaluation of schemes of cost and benefits:

With the implementation of this scheme, it would be possible to collect revenue from

customers in time and there will not be any delay. Issue of over drafting will be eliminated, as

the receivables will be collected in shorter period. Organization will also have favorable impact

on current ratio and will experience improved receivable collected period (Graham and Sathye

2017). Saving bad debts to 5 million compared to 10 million is another advantage received by

company with the implementation of this particular scheme. Details of savings of debt due to this

policy are depicted in the table below. In the current scenario, amount of bad debt is standing at

5% of total revenue.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

7

ADVANCE FINANCIAL ACCOUNTING

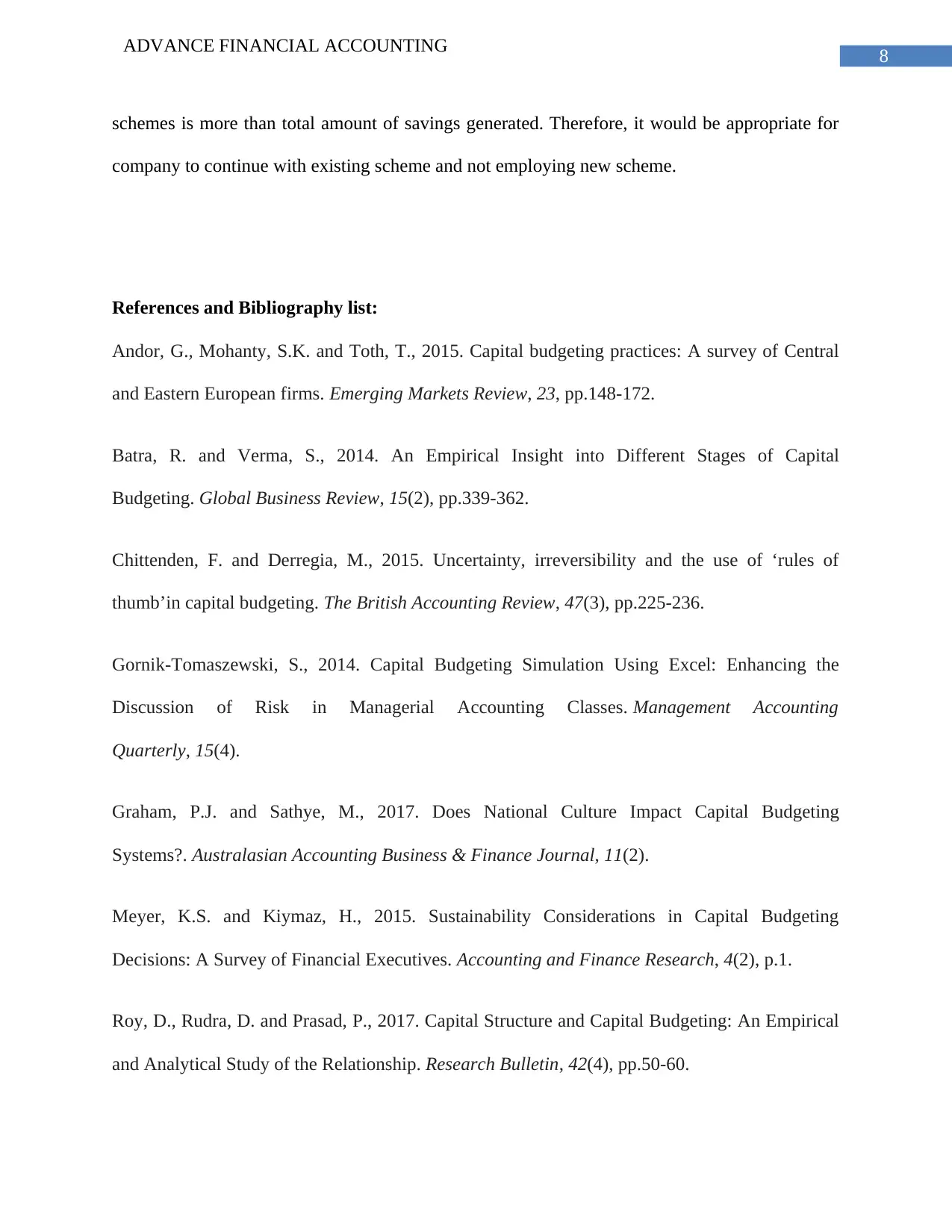

New

policy

Existing

policy

Bad debts in million 5 10

Saved 5 million

With the implementation of the new scheme, organization will be able to save 5 million

compared to 10 million in the previous scheme.

Scheme cost is depicted in terms of interest incurred on overdraft. Organization is

required to take overdraft from the banks because of delay in receiving payments from

customers. This particular schemes cost is at 20%. Therefore, in order to accept this scheme, it is

required by BLC limited to make cost comparison and they are required to pay extra 5%.

Moreover, it is also required by organization to compare discount with debt saving to that of

cost. It can be seen from the analysis that total amount of discount that is provided to customers

is more than the amount in terms of debt savings.

After conducting the analysis, it can be inferred that cost of offering customers with

discount schemes is more than total amount of benefits received on part of company. Acceptance

of scheme should only be done when costs incurred in employing that scheme is lower than total

benefits received. It would be suitable for BLC limited to continue with the existing schemes as

costs is more than saving generated.

Conclusions and Recommendation:

From the above discussion, it can be inferred that implementation of the schemes of

providing customers with 2% discount within 30 days would not be suitable and does not

generate positive impact on business. It is so because the cost incurred in employing such

ADVANCE FINANCIAL ACCOUNTING

New

policy

Existing

policy

Bad debts in million 5 10

Saved 5 million

With the implementation of the new scheme, organization will be able to save 5 million

compared to 10 million in the previous scheme.

Scheme cost is depicted in terms of interest incurred on overdraft. Organization is

required to take overdraft from the banks because of delay in receiving payments from

customers. This particular schemes cost is at 20%. Therefore, in order to accept this scheme, it is

required by BLC limited to make cost comparison and they are required to pay extra 5%.

Moreover, it is also required by organization to compare discount with debt saving to that of

cost. It can be seen from the analysis that total amount of discount that is provided to customers

is more than the amount in terms of debt savings.

After conducting the analysis, it can be inferred that cost of offering customers with

discount schemes is more than total amount of benefits received on part of company. Acceptance

of scheme should only be done when costs incurred in employing that scheme is lower than total

benefits received. It would be suitable for BLC limited to continue with the existing schemes as

costs is more than saving generated.

Conclusions and Recommendation:

From the above discussion, it can be inferred that implementation of the schemes of

providing customers with 2% discount within 30 days would not be suitable and does not

generate positive impact on business. It is so because the cost incurred in employing such

8

ADVANCE FINANCIAL ACCOUNTING

schemes is more than total amount of savings generated. Therefore, it would be appropriate for

company to continue with existing scheme and not employing new scheme.

References and Bibliography list:

Andor, G., Mohanty, S.K. and Toth, T., 2015. Capital budgeting practices: A survey of Central

and Eastern European firms. Emerging Markets Review, 23, pp.148-172.

Batra, R. and Verma, S., 2014. An Empirical Insight into Different Stages of Capital

Budgeting. Global Business Review, 15(2), pp.339-362.

Chittenden, F. and Derregia, M., 2015. Uncertainty, irreversibility and the use of ‘rules of

thumb’in capital budgeting. The British Accounting Review, 47(3), pp.225-236.

Gornik-Tomaszewski, S., 2014. Capital Budgeting Simulation Using Excel: Enhancing the

Discussion of Risk in Managerial Accounting Classes. Management Accounting

Quarterly, 15(4).

Graham, P.J. and Sathye, M., 2017. Does National Culture Impact Capital Budgeting

Systems?. Australasian Accounting Business & Finance Journal, 11(2).

Meyer, K.S. and Kiymaz, H., 2015. Sustainability Considerations in Capital Budgeting

Decisions: A Survey of Financial Executives. Accounting and Finance Research, 4(2), p.1.

Roy, D., Rudra, D. and Prasad, P., 2017. Capital Structure and Capital Budgeting: An Empirical

and Analytical Study of the Relationship. Research Bulletin, 42(4), pp.50-60.

ADVANCE FINANCIAL ACCOUNTING

schemes is more than total amount of savings generated. Therefore, it would be appropriate for

company to continue with existing scheme and not employing new scheme.

References and Bibliography list:

Andor, G., Mohanty, S.K. and Toth, T., 2015. Capital budgeting practices: A survey of Central

and Eastern European firms. Emerging Markets Review, 23, pp.148-172.

Batra, R. and Verma, S., 2014. An Empirical Insight into Different Stages of Capital

Budgeting. Global Business Review, 15(2), pp.339-362.

Chittenden, F. and Derregia, M., 2015. Uncertainty, irreversibility and the use of ‘rules of

thumb’in capital budgeting. The British Accounting Review, 47(3), pp.225-236.

Gornik-Tomaszewski, S., 2014. Capital Budgeting Simulation Using Excel: Enhancing the

Discussion of Risk in Managerial Accounting Classes. Management Accounting

Quarterly, 15(4).

Graham, P.J. and Sathye, M., 2017. Does National Culture Impact Capital Budgeting

Systems?. Australasian Accounting Business & Finance Journal, 11(2).

Meyer, K.S. and Kiymaz, H., 2015. Sustainability Considerations in Capital Budgeting

Decisions: A Survey of Financial Executives. Accounting and Finance Research, 4(2), p.1.

Roy, D., Rudra, D. and Prasad, P., 2017. Capital Structure and Capital Budgeting: An Empirical

and Analytical Study of the Relationship. Research Bulletin, 42(4), pp.50-60.

9

ADVANCE FINANCIAL ACCOUNTING

Shimizu, N. and Tamura, A., 2015. The Eff ects of Business Strategy on Economic Evaluation

Techniques of Capital Investment.

ADVANCE FINANCIAL ACCOUNTING

Shimizu, N. and Tamura, A., 2015. The Eff ects of Business Strategy on Economic Evaluation

Techniques of Capital Investment.

1 out of 10

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

© 2024 | Zucol Services PVT LTD | All rights reserved.