Airline Revenue Management: EasyJet vs British Airways Analysis

VerifiedAdded on 2023/06/17

|7

|1674

|185

Report

AI Summary

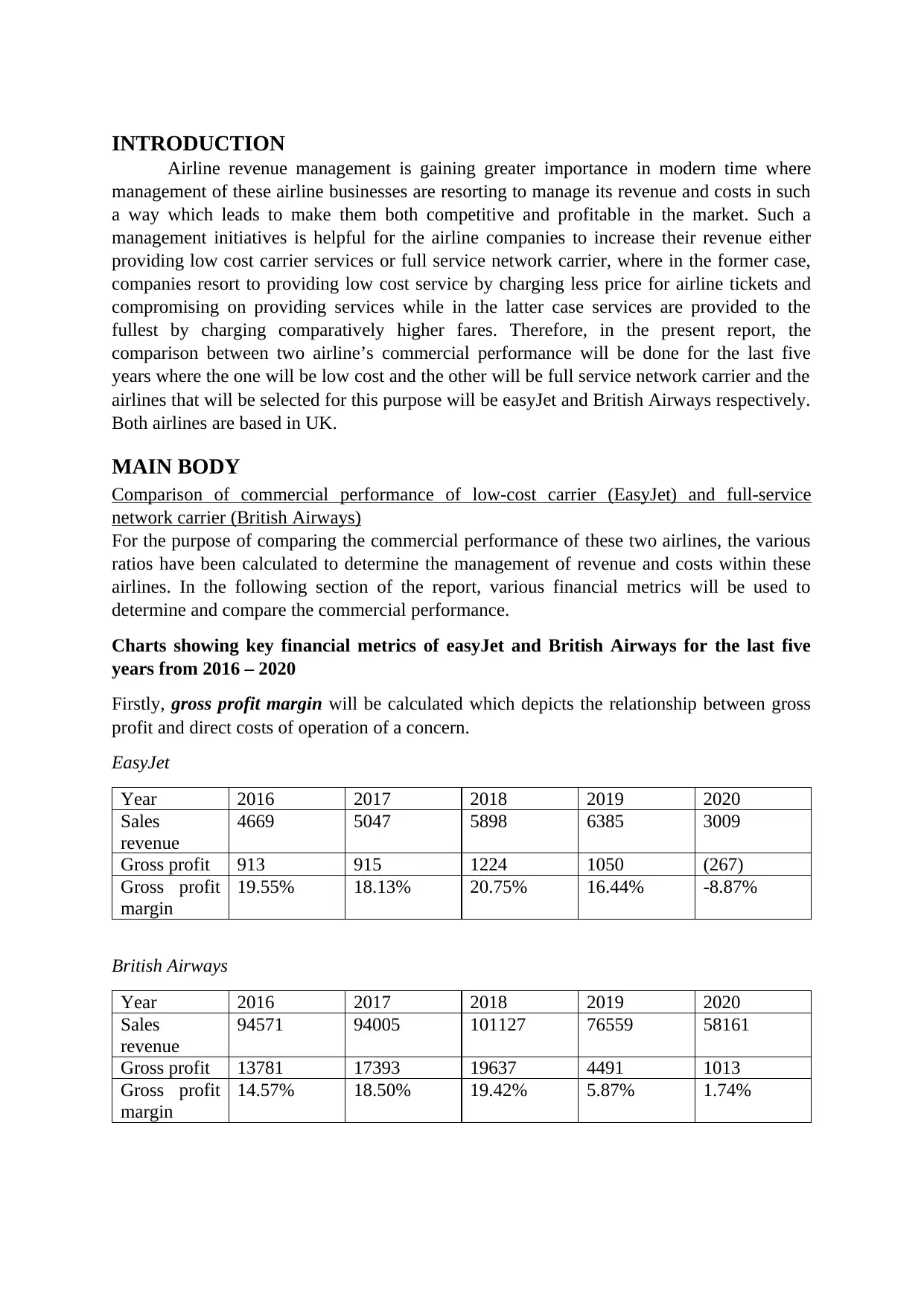

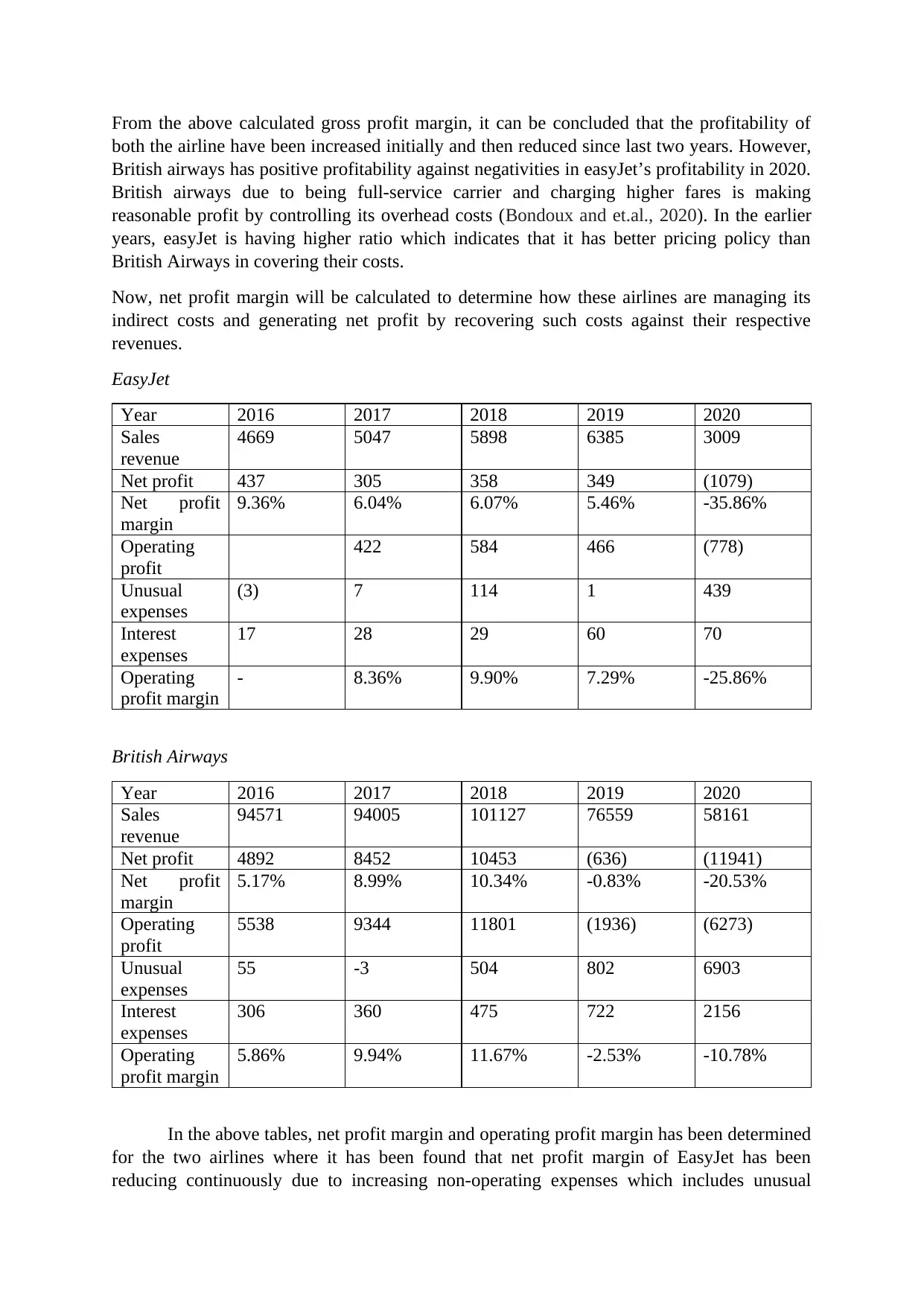

This report provides a comparative analysis of the commercial performance of EasyJet (a low-cost carrier) and British Airways (a full-service network carrier) over the last five years (2016-2020). It uses key financial metrics such as gross profit margin, net profit margin, and operating profit margin to evaluate and contrast the revenue and cost management strategies of the two airlines. The report highlights the impact of the COVID-19 pandemic on both airlines, noting the challenges faced by low-cost carriers due to lower margins. The analysis concludes with recommendations for improving the commercial performance of both types of airlines, including cost reduction strategies for British Airways and focusing on customer satisfaction for both.

1 out of 7

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.