Managerial Finance Report: Financial Analysis of M&S and Next

VerifiedAdded on 2020/10/22

|14

|3200

|208

Report

AI Summary

This report presents a comprehensive analysis of managerial finance, focusing on the financial performance of Marks and Spencer (M&S) and Next Plc. It begins with an introduction to managerial finance and its significance in optimizing financial strategies and mitigating potential losses. The core of the report involves a detailed examination of financial statements, including the calculation and interpretation of ten key financial ratios for both companies from 2017 to 2018. These ratios are used to evaluate the companies' liquidity, profitability, gearing, and investment potential. The analysis highlights the strengths and weaknesses of each company, offering insights into their financial positions and investment prospects. Furthermore, the report provides recommendations for improving the financial performance of M&S, which is identified as the underperforming entity. It also discusses the limitations of relying solely on financial ratios for performance interpretation. Finally, the report delves into capital investment appraisal techniques, comparing the Alpha and Beta projects using payback period and net present value methods, and discusses the limitations of these techniques in long-term decision-making.

Assessment Brief 2

Managerial Finance

Managerial Finance

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Contents

INTRODUCTION.......................................................................................................................................4

5.1 Task.......................................................................................................................................................4

Portfolio 1................................................................................................................................................4

5.1.1 Task 1:............................................................................................................................................4

a) Calculation of 10 financial ratios as given below for two years (2017 - 2018):.......................................4

b) Analysis of the performance of two selected companies and analysis of their financial position and

investment potential.................................................................................................................................5

c) Recommendations of how the financial performance of the poorly performing business can be

improved..................................................................................................................................................9

d) Discuss the limitations of relying on financial ratios to interpret companies performance..................9

Portfolio 2:.............................................................................................................................................10

5.1.2 Task 2: Capital Investment Appraisal...........................................................................................10

a) Using appropriate investment appraisal techniques, advise senior management on whether they

should opt for Alpha project or Beta project......................................................................................10

Payback period (PBP)........................................................................................................................10

Net Present value method (NPV).......................................................................................................11

b) Discuss the limitations of using investment appraisal techniques to help in long term decision

making...............................................................................................................................................12

CONCLUSION.........................................................................................................................................12

REFERENCES..........................................................................................................................................14

INTRODUCTION.......................................................................................................................................4

5.1 Task.......................................................................................................................................................4

Portfolio 1................................................................................................................................................4

5.1.1 Task 1:............................................................................................................................................4

a) Calculation of 10 financial ratios as given below for two years (2017 - 2018):.......................................4

b) Analysis of the performance of two selected companies and analysis of their financial position and

investment potential.................................................................................................................................5

c) Recommendations of how the financial performance of the poorly performing business can be

improved..................................................................................................................................................9

d) Discuss the limitations of relying on financial ratios to interpret companies performance..................9

Portfolio 2:.............................................................................................................................................10

5.1.2 Task 2: Capital Investment Appraisal...........................................................................................10

a) Using appropriate investment appraisal techniques, advise senior management on whether they

should opt for Alpha project or Beta project......................................................................................10

Payback period (PBP)........................................................................................................................10

Net Present value method (NPV).......................................................................................................11

b) Discuss the limitations of using investment appraisal techniques to help in long term decision

making...............................................................................................................................................12

CONCLUSION.........................................................................................................................................12

REFERENCES..........................................................................................................................................14

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

INTRODUCTION

Managerial finance refers to a branch of finance that is associated with the managerial

importance of techniques used in finance. It also highlights the most optimum way in which

money can be utilized in order to enhance futuristic opportunities related to money making. Also,

this helps in significantly reducing the consequences of financial losses and unfavourable

situations (Combs, Samy and Cengiz, 2017). This report includes the financial analysis of Marks

and Spencer and Next Plc. Also, this explores the various recommending by adopting which the

financial performance of poorly performing entities can be improved in an effective manner.

Furthermore, the limitations of relying upon financial ratios for analyzing a company’s

performance have been discussed. Also, capital appraisal techniques have been highlighted along

with their limitations in long term decision making.

5.1 Task

Portfolio 1

5.1.1 Task 1:

The analysis of the financial statements of Marks and spencer and Next plc. has yielded the

followings:

a) Calculation of 10 financial ratios as given below for two years (2017 -

2018):

M&S NEXT PLC

Formulae 2017 2018 2017 2018

Current ratios CA/CL 0.728 0.722 2.290 1.964

Quick ratios QA/CL 0.407 0.294 1.668 1.429

Net Profit Margin Net profit /net revenue 1.09% 0.27%

15.67

% 14.44%

Gross Profit margin Gross Profit/ net revenue 24.29% 23.22%

34.19

% 33.10%

Gearing ratios Total long-term debts/Equity 0.881 0.938 2.290 2.412

P/E ratio MPS/EPS 9.814 10.172 11.335 8.681

Managerial finance refers to a branch of finance that is associated with the managerial

importance of techniques used in finance. It also highlights the most optimum way in which

money can be utilized in order to enhance futuristic opportunities related to money making. Also,

this helps in significantly reducing the consequences of financial losses and unfavourable

situations (Combs, Samy and Cengiz, 2017). This report includes the financial analysis of Marks

and Spencer and Next Plc. Also, this explores the various recommending by adopting which the

financial performance of poorly performing entities can be improved in an effective manner.

Furthermore, the limitations of relying upon financial ratios for analyzing a company’s

performance have been discussed. Also, capital appraisal techniques have been highlighted along

with their limitations in long term decision making.

5.1 Task

Portfolio 1

5.1.1 Task 1:

The analysis of the financial statements of Marks and spencer and Next plc. has yielded the

followings:

a) Calculation of 10 financial ratios as given below for two years (2017 -

2018):

M&S NEXT PLC

Formulae 2017 2018 2017 2018

Current ratios CA/CL 0.728 0.722 2.290 1.964

Quick ratios QA/CL 0.407 0.294 1.668 1.429

Net Profit Margin Net profit /net revenue 1.09% 0.27%

15.67

% 14.44%

Gross Profit margin Gross Profit/ net revenue 24.29% 23.22%

34.19

% 33.10%

Gearing ratios Total long-term debts/Equity 0.881 0.938 2.290 2.412

P/E ratio MPS/EPS 9.814 10.172 11.335 8.681

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Earnings per share PAT/n 30.4 27.8 441.3 416.7

Return on capital employed Operating Profits/CE 4.27% 2.73%

49.27

% 46.15%

Average inventories turnover

period 365/Inventory Turnover 27.23 27.53 60.74 66.27

Dividend payout ratio DPS/EPS 58.22% 63.67%

23.79

% 12.72%

b) Analysis of the performance of two selected companies and analysis of their financial

position and investment potential.

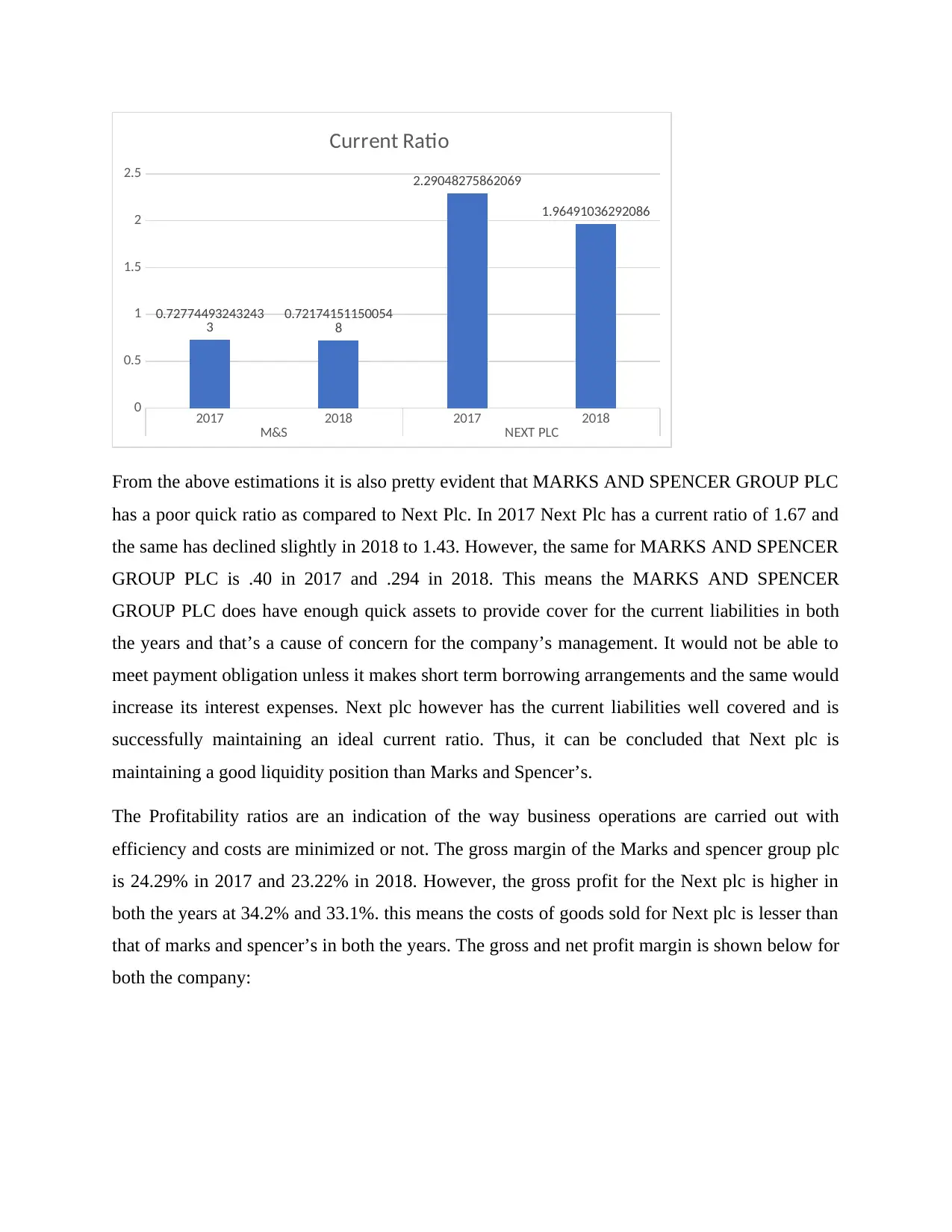

From the above estimations it is apparent that MARKS AND SPENCER GROUP PLC has a

poor liquidity position as compared to Next Plc. In 2017 Next Plc has a current ratio of 2.29 and

the same has declined slightly in 2018 to 1.97. However, the same for MARKS AND SPENCER

GROUP PLC is .728 in 2017 and .722 in 2018. This means the MARKS AND SPENCER

GROUP PLC does have enough current assets to provide cover for the current liabilities in both

the years and that’s a cause of concern for the company’s management. It would not be able to

meet payment obligation unless it makes short term borrowing arrangements and the same would

increase its interest expenses. Next plc however has the current liabilities well covered and is

successfully maintaining an ideal current ratio.

The same is shown as follows:

Return on capital employed Operating Profits/CE 4.27% 2.73%

49.27

% 46.15%

Average inventories turnover

period 365/Inventory Turnover 27.23 27.53 60.74 66.27

Dividend payout ratio DPS/EPS 58.22% 63.67%

23.79

% 12.72%

b) Analysis of the performance of two selected companies and analysis of their financial

position and investment potential.

From the above estimations it is apparent that MARKS AND SPENCER GROUP PLC has a

poor liquidity position as compared to Next Plc. In 2017 Next Plc has a current ratio of 2.29 and

the same has declined slightly in 2018 to 1.97. However, the same for MARKS AND SPENCER

GROUP PLC is .728 in 2017 and .722 in 2018. This means the MARKS AND SPENCER

GROUP PLC does have enough current assets to provide cover for the current liabilities in both

the years and that’s a cause of concern for the company’s management. It would not be able to

meet payment obligation unless it makes short term borrowing arrangements and the same would

increase its interest expenses. Next plc however has the current liabilities well covered and is

successfully maintaining an ideal current ratio.

The same is shown as follows:

2017 2018 2017 2018

M&S NEXT PLC

0

0.5

1

1.5

2

2.5

0.72774493243243

3 0.72174151150054

8

2.29048275862069

1.96491036292086

Current Ratio

From the above estimations it is also pretty evident that MARKS AND SPENCER GROUP PLC

has a poor quick ratio as compared to Next Plc. In 2017 Next Plc has a current ratio of 1.67 and

the same has declined slightly in 2018 to 1.43. However, the same for MARKS AND SPENCER

GROUP PLC is .40 in 2017 and .294 in 2018. This means the MARKS AND SPENCER

GROUP PLC does have enough quick assets to provide cover for the current liabilities in both

the years and that’s a cause of concern for the company’s management. It would not be able to

meet payment obligation unless it makes short term borrowing arrangements and the same would

increase its interest expenses. Next plc however has the current liabilities well covered and is

successfully maintaining an ideal current ratio. Thus, it can be concluded that Next plc is

maintaining a good liquidity position than Marks and Spencer’s.

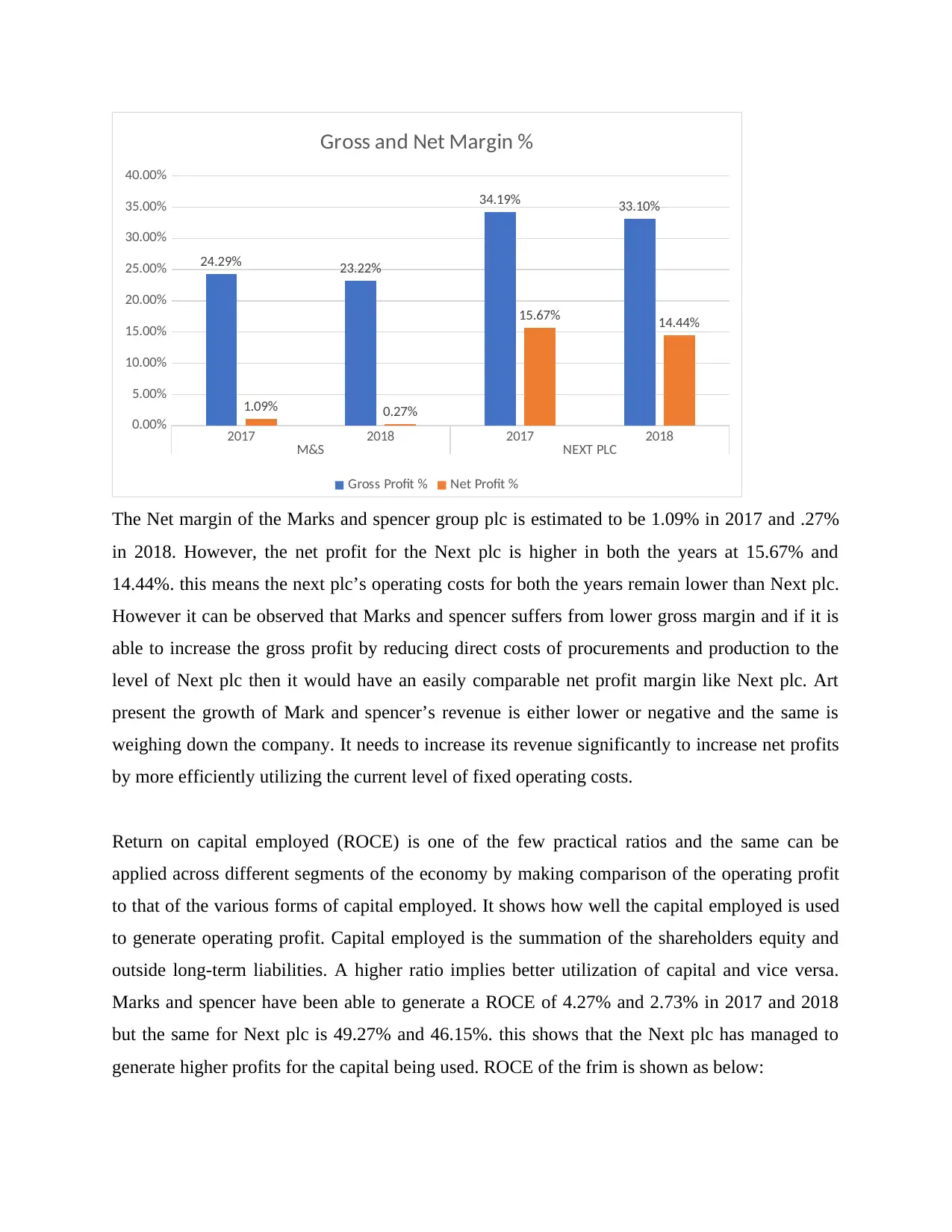

The Profitability ratios are an indication of the way business operations are carried out with

efficiency and costs are minimized or not. The gross margin of the Marks and spencer group plc

is 24.29% in 2017 and 23.22% in 2018. However, the gross profit for the Next plc is higher in

both the years at 34.2% and 33.1%. this means the costs of goods sold for Next plc is lesser than

that of marks and spencer’s in both the years. The gross and net profit margin is shown below for

both the company:

M&S NEXT PLC

0

0.5

1

1.5

2

2.5

0.72774493243243

3 0.72174151150054

8

2.29048275862069

1.96491036292086

Current Ratio

From the above estimations it is also pretty evident that MARKS AND SPENCER GROUP PLC

has a poor quick ratio as compared to Next Plc. In 2017 Next Plc has a current ratio of 1.67 and

the same has declined slightly in 2018 to 1.43. However, the same for MARKS AND SPENCER

GROUP PLC is .40 in 2017 and .294 in 2018. This means the MARKS AND SPENCER

GROUP PLC does have enough quick assets to provide cover for the current liabilities in both

the years and that’s a cause of concern for the company’s management. It would not be able to

meet payment obligation unless it makes short term borrowing arrangements and the same would

increase its interest expenses. Next plc however has the current liabilities well covered and is

successfully maintaining an ideal current ratio. Thus, it can be concluded that Next plc is

maintaining a good liquidity position than Marks and Spencer’s.

The Profitability ratios are an indication of the way business operations are carried out with

efficiency and costs are minimized or not. The gross margin of the Marks and spencer group plc

is 24.29% in 2017 and 23.22% in 2018. However, the gross profit for the Next plc is higher in

both the years at 34.2% and 33.1%. this means the costs of goods sold for Next plc is lesser than

that of marks and spencer’s in both the years. The gross and net profit margin is shown below for

both the company:

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

2017 2018 2017 2018

M&S NEXT PLC

0.00%

5.00%

10.00%

15.00%

20.00%

25.00%

30.00%

35.00%

40.00%

24.29% 23.22%

34.19% 33.10%

1.09% 0.27%

15.67% 14.44%

Gross and Net Margin %

Gross Profit % Net Profit %

The Net margin of the Marks and spencer group plc is estimated to be 1.09% in 2017 and .27%

in 2018. However, the net profit for the Next plc is higher in both the years at 15.67% and

14.44%. this means the next plc’s operating costs for both the years remain lower than Next plc.

However it can be observed that Marks and spencer suffers from lower gross margin and if it is

able to increase the gross profit by reducing direct costs of procurements and production to the

level of Next plc then it would have an easily comparable net profit margin like Next plc. Art

present the growth of Mark and spencer’s revenue is either lower or negative and the same is

weighing down the company. It needs to increase its revenue significantly to increase net profits

by more efficiently utilizing the current level of fixed operating costs.

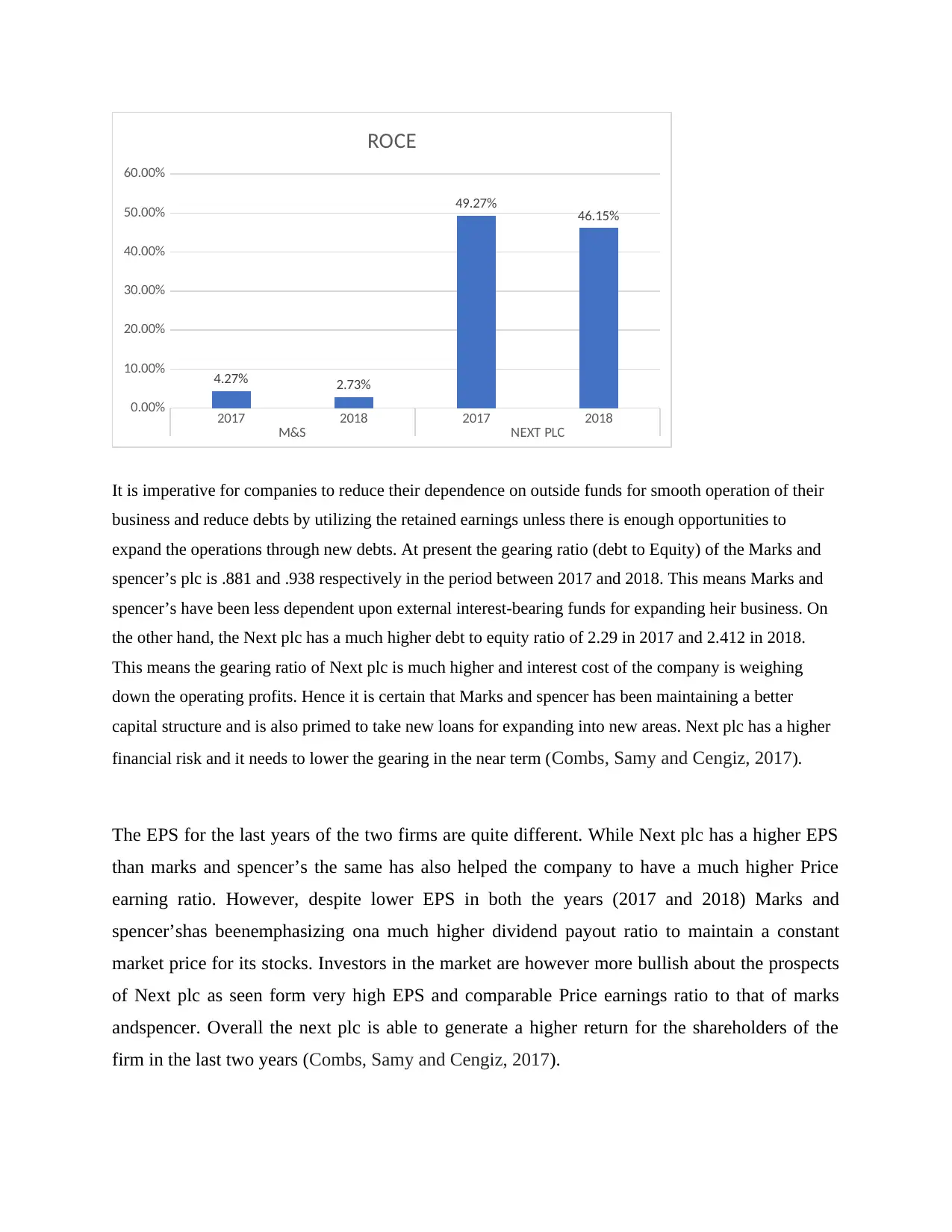

Return on capital employed (ROCE) is one of the few practical ratios and the same can be

applied across different segments of the economy by making comparison of the operating profit

to that of the various forms of capital employed. It shows how well the capital employed is used

to generate operating profit. Capital employed is the summation of the shareholders equity and

outside long-term liabilities. A higher ratio implies better utilization of capital and vice versa.

Marks and spencer have been able to generate a ROCE of 4.27% and 2.73% in 2017 and 2018

but the same for Next plc is 49.27% and 46.15%. this shows that the Next plc has managed to

generate higher profits for the capital being used. ROCE of the frim is shown as below:

M&S NEXT PLC

0.00%

5.00%

10.00%

15.00%

20.00%

25.00%

30.00%

35.00%

40.00%

24.29% 23.22%

34.19% 33.10%

1.09% 0.27%

15.67% 14.44%

Gross and Net Margin %

Gross Profit % Net Profit %

The Net margin of the Marks and spencer group plc is estimated to be 1.09% in 2017 and .27%

in 2018. However, the net profit for the Next plc is higher in both the years at 15.67% and

14.44%. this means the next plc’s operating costs for both the years remain lower than Next plc.

However it can be observed that Marks and spencer suffers from lower gross margin and if it is

able to increase the gross profit by reducing direct costs of procurements and production to the

level of Next plc then it would have an easily comparable net profit margin like Next plc. Art

present the growth of Mark and spencer’s revenue is either lower or negative and the same is

weighing down the company. It needs to increase its revenue significantly to increase net profits

by more efficiently utilizing the current level of fixed operating costs.

Return on capital employed (ROCE) is one of the few practical ratios and the same can be

applied across different segments of the economy by making comparison of the operating profit

to that of the various forms of capital employed. It shows how well the capital employed is used

to generate operating profit. Capital employed is the summation of the shareholders equity and

outside long-term liabilities. A higher ratio implies better utilization of capital and vice versa.

Marks and spencer have been able to generate a ROCE of 4.27% and 2.73% in 2017 and 2018

but the same for Next plc is 49.27% and 46.15%. this shows that the Next plc has managed to

generate higher profits for the capital being used. ROCE of the frim is shown as below:

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

2017 2018 2017 2018

M&S NEXT PLC

0.00%

10.00%

20.00%

30.00%

40.00%

50.00%

60.00%

4.27% 2.73%

49.27% 46.15%

ROCE

It is imperative for companies to reduce their dependence on outside funds for smooth operation of their

business and reduce debts by utilizing the retained earnings unless there is enough opportunities to

expand the operations through new debts. At present the gearing ratio (debt to Equity) of the Marks and

spencer’s plc is .881 and .938 respectively in the period between 2017 and 2018. This means Marks and

spencer’s have been less dependent upon external interest-bearing funds for expanding heir business. On

the other hand, the Next plc has a much higher debt to equity ratio of 2.29 in 2017 and 2.412 in 2018.

This means the gearing ratio of Next plc is much higher and interest cost of the company is weighing

down the operating profits. Hence it is certain that Marks and spencer has been maintaining a better

capital structure and is also primed to take new loans for expanding into new areas. Next plc has a higher

financial risk and it needs to lower the gearing in the near term (Combs, Samy and Cengiz, 2017).

The EPS for the last years of the two firms are quite different. While Next plc has a higher EPS

than marks and spencer’s the same has also helped the company to have a much higher Price

earning ratio. However, despite lower EPS in both the years (2017 and 2018) Marks and

spencer’shas beenemphasizing ona much higher dividend payout ratio to maintain a constant

market price for its stocks. Investors in the market are however more bullish about the prospects

of Next plc as seen form very high EPS and comparable Price earnings ratio to that of marks

andspencer. Overall the next plc is able to generate a higher return for the shareholders of the

firm in the last two years (Combs, Samy and Cengiz, 2017).

M&S NEXT PLC

0.00%

10.00%

20.00%

30.00%

40.00%

50.00%

60.00%

4.27% 2.73%

49.27% 46.15%

ROCE

It is imperative for companies to reduce their dependence on outside funds for smooth operation of their

business and reduce debts by utilizing the retained earnings unless there is enough opportunities to

expand the operations through new debts. At present the gearing ratio (debt to Equity) of the Marks and

spencer’s plc is .881 and .938 respectively in the period between 2017 and 2018. This means Marks and

spencer’s have been less dependent upon external interest-bearing funds for expanding heir business. On

the other hand, the Next plc has a much higher debt to equity ratio of 2.29 in 2017 and 2.412 in 2018.

This means the gearing ratio of Next plc is much higher and interest cost of the company is weighing

down the operating profits. Hence it is certain that Marks and spencer has been maintaining a better

capital structure and is also primed to take new loans for expanding into new areas. Next plc has a higher

financial risk and it needs to lower the gearing in the near term (Combs, Samy and Cengiz, 2017).

The EPS for the last years of the two firms are quite different. While Next plc has a higher EPS

than marks and spencer’s the same has also helped the company to have a much higher Price

earning ratio. However, despite lower EPS in both the years (2017 and 2018) Marks and

spencer’shas beenemphasizing ona much higher dividend payout ratio to maintain a constant

market price for its stocks. Investors in the market are however more bullish about the prospects

of Next plc as seen form very high EPS and comparable Price earnings ratio to that of marks

andspencer. Overall the next plc is able to generate a higher return for the shareholders of the

firm in the last two years (Combs, Samy and Cengiz, 2017).

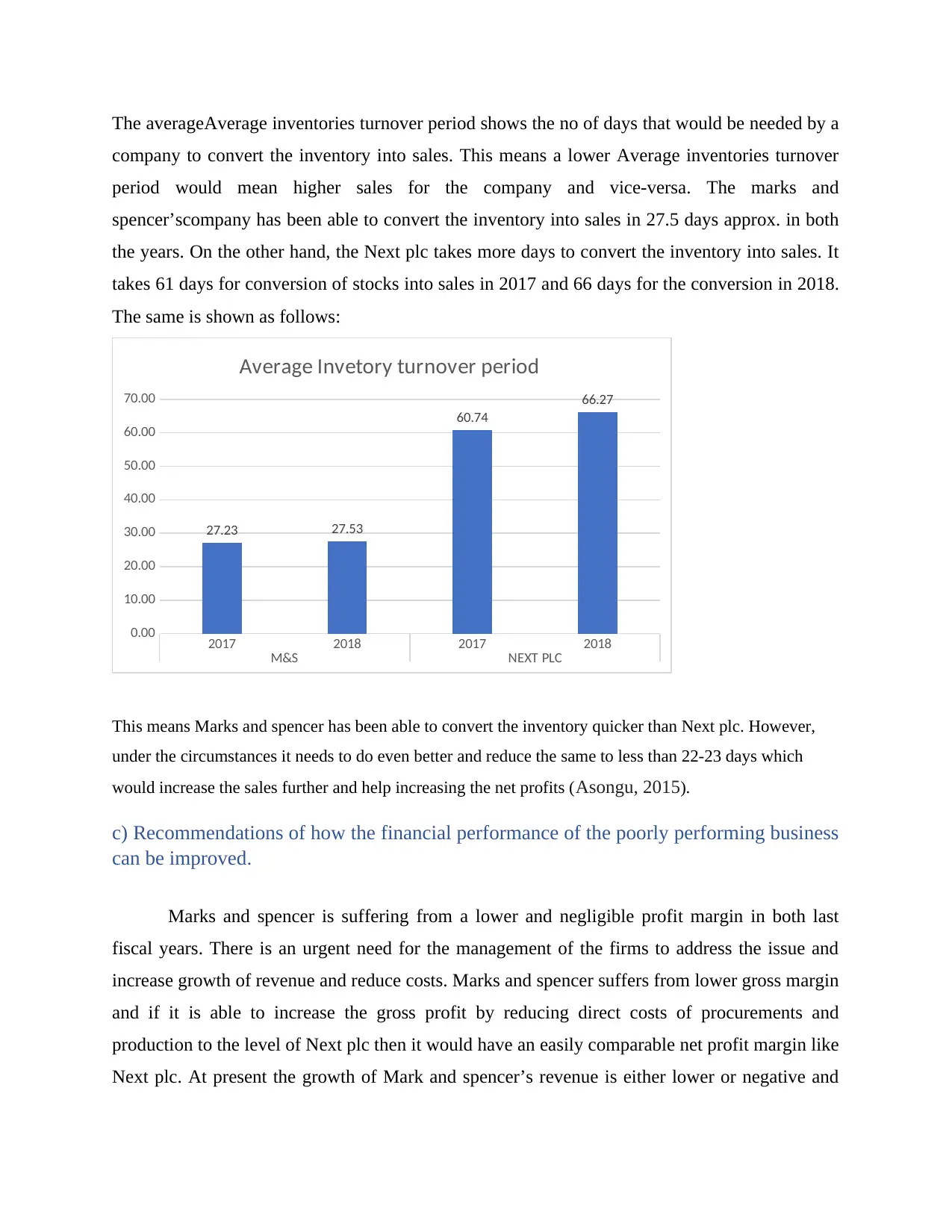

The averageAverage inventories turnover period shows the no of days that would be needed by a

company to convert the inventory into sales. This means a lower Average inventories turnover

period would mean higher sales for the company and vice-versa. The marks and

spencer’scompany has been able to convert the inventory into sales in 27.5 days approx. in both

the years. On the other hand, the Next plc takes more days to convert the inventory into sales. It

takes 61 days for conversion of stocks into sales in 2017 and 66 days for the conversion in 2018.

The same is shown as follows:

2017 2018 2017 2018

M&S NEXT PLC

0.00

10.00

20.00

30.00

40.00

50.00

60.00

70.00

27.23 27.53

60.74

66.27

Average Invetory turnover period

This means Marks and spencer has been able to convert the inventory quicker than Next plc. However,

under the circumstances it needs to do even better and reduce the same to less than 22-23 days which

would increase the sales further and help increasing the net profits (Asongu, 2015).

c) Recommendations of how the financial performance of the poorly performing business

can be improved.

Marks and spencer is suffering from a lower and negligible profit margin in both last

fiscal years. There is an urgent need for the management of the firms to address the issue and

increase growth of revenue and reduce costs. Marks and spencer suffers from lower gross margin

and if it is able to increase the gross profit by reducing direct costs of procurements and

production to the level of Next plc then it would have an easily comparable net profit margin like

Next plc. At present the growth of Mark and spencer’s revenue is either lower or negative and

company to convert the inventory into sales. This means a lower Average inventories turnover

period would mean higher sales for the company and vice-versa. The marks and

spencer’scompany has been able to convert the inventory into sales in 27.5 days approx. in both

the years. On the other hand, the Next plc takes more days to convert the inventory into sales. It

takes 61 days for conversion of stocks into sales in 2017 and 66 days for the conversion in 2018.

The same is shown as follows:

2017 2018 2017 2018

M&S NEXT PLC

0.00

10.00

20.00

30.00

40.00

50.00

60.00

70.00

27.23 27.53

60.74

66.27

Average Invetory turnover period

This means Marks and spencer has been able to convert the inventory quicker than Next plc. However,

under the circumstances it needs to do even better and reduce the same to less than 22-23 days which

would increase the sales further and help increasing the net profits (Asongu, 2015).

c) Recommendations of how the financial performance of the poorly performing business

can be improved.

Marks and spencer is suffering from a lower and negligible profit margin in both last

fiscal years. There is an urgent need for the management of the firms to address the issue and

increase growth of revenue and reduce costs. Marks and spencer suffers from lower gross margin

and if it is able to increase the gross profit by reducing direct costs of procurements and

production to the level of Next plc then it would have an easily comparable net profit margin like

Next plc. At present the growth of Mark and spencer’s revenue is either lower or negative and

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

the same is weighing down the company. It needs to increase its revenue significantly to increase

net profits by more efficiently utilizing the current level of fixed operating costs.

Marks and spencer is a bigger firm than that of Next plc and is thus more used to see

fluctuations in profits due to uneven business environment. It can correct the lower profitability

issue through the following measures:

a) It needs to address the gross margin through long term supply agreements with

experienced and reliable suppliers and keep costs down and constant in the long term.

b) It also needs to pare the fixed costs which are underutilized and save huge operating

costs. Selling and general administration costs needs to be lowered (Vesty, Brooks and

Oliver, 2015).

c) More objective selling and advertising campaigns can be prepared to increase sales

growth which has remained stagnant in the last three years. Higher sales growth would

mean higher contributions and bigger net margins.

d) Discuss the limitations of relying on financial ratios to interpret companies

performance.

While ratio analysis is a good tool for performance evaluation oflisted firms the same suffers

from several limitations which must be considered during ratio analysis:

a) The ratios which are calculated for evaluating performance is related to the last fiscal

years and it is not highly probable that the same performance would be separated by the

company in the future as well. Using historical data might backfire.

b) The rates of inflation are different in different years and which affects the costs incurred.

Thus, comparison across periods suffer from lack of knowledge about inflationary

conditions.

c) Different companies which are being analyzed during a period might be using different

accounting policies regarding depreciationetc. and which might make it impossible for

the accounting figures to be compared and judge correctly. Results under different

accountingpolicies would be highly subjective and would lead to difference of opinion

(Penman, 2015)

net profits by more efficiently utilizing the current level of fixed operating costs.

Marks and spencer is a bigger firm than that of Next plc and is thus more used to see

fluctuations in profits due to uneven business environment. It can correct the lower profitability

issue through the following measures:

a) It needs to address the gross margin through long term supply agreements with

experienced and reliable suppliers and keep costs down and constant in the long term.

b) It also needs to pare the fixed costs which are underutilized and save huge operating

costs. Selling and general administration costs needs to be lowered (Vesty, Brooks and

Oliver, 2015).

c) More objective selling and advertising campaigns can be prepared to increase sales

growth which has remained stagnant in the last three years. Higher sales growth would

mean higher contributions and bigger net margins.

d) Discuss the limitations of relying on financial ratios to interpret companies

performance.

While ratio analysis is a good tool for performance evaluation oflisted firms the same suffers

from several limitations which must be considered during ratio analysis:

a) The ratios which are calculated for evaluating performance is related to the last fiscal

years and it is not highly probable that the same performance would be separated by the

company in the future as well. Using historical data might backfire.

b) The rates of inflation are different in different years and which affects the costs incurred.

Thus, comparison across periods suffer from lack of knowledge about inflationary

conditions.

c) Different companies which are being analyzed during a period might be using different

accounting policies regarding depreciationetc. and which might make it impossible for

the accounting figures to be compared and judge correctly. Results under different

accountingpolicies would be highly subjective and would lead to difference of opinion

(Penman, 2015)

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

d) It would also be impractical for business operations to be compared if the two businesses

are in different segments of the industry. Like one company is in retail business and while

the other is a producing concern.

Portfolio 2:

5.1.2 Task 2: Capital Investment Appraisal

Required:

a) Using appropriate investment appraisal techniques, advise senior management on whether

they should opt for Alpha project or Beta project.

The following investing appraisal techniques are being used to evaluate the projects Alpha and

Beta.

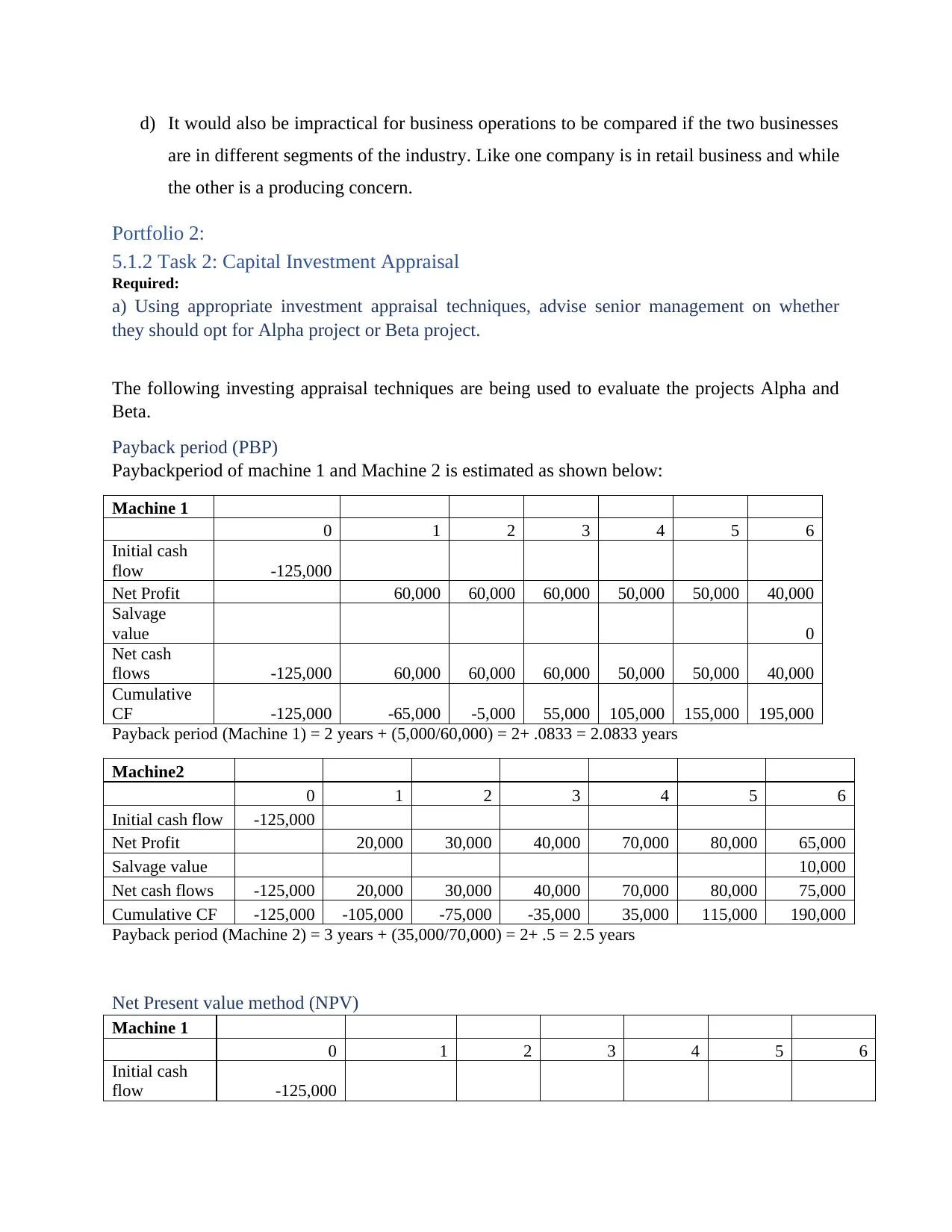

Payback period (PBP)

Paybackperiod of machine 1 and Machine 2 is estimated as shown below:

Machine 1

0 1 2 3 4 5 6

Initial cash

flow -125,000

Net Profit 60,000 60,000 60,000 50,000 50,000 40,000

Salvage

value 0

Net cash

flows -125,000 60,000 60,000 60,000 50,000 50,000 40,000

Cumulative

CF -125,000 -65,000 -5,000 55,000 105,000 155,000 195,000

Payback period (Machine 1) = 2 years + (5,000/60,000) = 2+ .0833 = 2.0833 years

Machine2

0 1 2 3 4 5 6

Initial cash flow -125,000

Net Profit 20,000 30,000 40,000 70,000 80,000 65,000

Salvage value 10,000

Net cash flows -125,000 20,000 30,000 40,000 70,000 80,000 75,000

Cumulative CF -125,000 -105,000 -75,000 -35,000 35,000 115,000 190,000

Payback period (Machine 2) = 3 years + (35,000/70,000) = 2+ .5 = 2.5 years

Net Present value method (NPV)

Machine 1

0 1 2 3 4 5 6

Initial cash

flow -125,000

are in different segments of the industry. Like one company is in retail business and while

the other is a producing concern.

Portfolio 2:

5.1.2 Task 2: Capital Investment Appraisal

Required:

a) Using appropriate investment appraisal techniques, advise senior management on whether

they should opt for Alpha project or Beta project.

The following investing appraisal techniques are being used to evaluate the projects Alpha and

Beta.

Payback period (PBP)

Paybackperiod of machine 1 and Machine 2 is estimated as shown below:

Machine 1

0 1 2 3 4 5 6

Initial cash

flow -125,000

Net Profit 60,000 60,000 60,000 50,000 50,000 40,000

Salvage

value 0

Net cash

flows -125,000 60,000 60,000 60,000 50,000 50,000 40,000

Cumulative

CF -125,000 -65,000 -5,000 55,000 105,000 155,000 195,000

Payback period (Machine 1) = 2 years + (5,000/60,000) = 2+ .0833 = 2.0833 years

Machine2

0 1 2 3 4 5 6

Initial cash flow -125,000

Net Profit 20,000 30,000 40,000 70,000 80,000 65,000

Salvage value 10,000

Net cash flows -125,000 20,000 30,000 40,000 70,000 80,000 75,000

Cumulative CF -125,000 -105,000 -75,000 -35,000 35,000 115,000 190,000

Payback period (Machine 2) = 3 years + (35,000/70,000) = 2+ .5 = 2.5 years

Net Present value method (NPV)

Machine 1

0 1 2 3 4 5 6

Initial cash

flow -125,000

Net Profit 60,000 60,000 60,000 50,000 50,000 40,000

Salvage value 0

Net cash

flows -125,000 60,000 60,000 60,000 50,000 50,000 40,000

PVF @ 20% 1.000 0.833 0.694 0.579 0.482 0.402 0.335

PV -125000.00 50000.00 41666.67 34722.22 24112.65 20093.88 13395.92

NPV 58,991.34

NPV of the Machine 1 is £58,991.34 approx.

Machine 2

0 1 2 3 4 5 6

Initial cash

flow -125,000

20,000 30,000 40,000 70,000 80,000 65,000

Salvage value 10000

Net cash flows -125,000 20,000 30,000 40,000 70,000 80,000 75,000

PVF @ 20% 1.000 0.833 0.694 0.579 0.482 0.402 0.335

PV -125,000 16,666.67 20,833.33 23,148.15 33,757.72 32,150.21 25,117.35

NPV 26,673.42

NPV of the Machine 2 is £26,673.42 approx.

Note:

As there is no corporate tax the estimation of depreciation won’t have any effect on the

estimation of the cash flows and this is why the same is ignored.

Recommendations:

a) as per the payback period estimation of both Alpha and Beta projects, the Project1 or

Alpha has a lower payback period of 2.0833 years and hence the same is recommended to

be invested. This is because while Alpha project would be able to recover the initial cash

investments in 2.0833 years the Beta Project or Beta Machine would take slightly higher

time frame of 2.5 years to recover the initial cash outflows. Thus Alpha (machine 1 is

recommended for investment) (Bender & Ward, 2012).

b) The NPV of the projects are estimated as £58,991.34 and £26,673.42 respectively. As

the Alpha project has a higher NPV of £58,991.34 the same is recommended for

Salvage value 0

Net cash

flows -125,000 60,000 60,000 60,000 50,000 50,000 40,000

PVF @ 20% 1.000 0.833 0.694 0.579 0.482 0.402 0.335

PV -125000.00 50000.00 41666.67 34722.22 24112.65 20093.88 13395.92

NPV 58,991.34

NPV of the Machine 1 is £58,991.34 approx.

Machine 2

0 1 2 3 4 5 6

Initial cash

flow -125,000

20,000 30,000 40,000 70,000 80,000 65,000

Salvage value 10000

Net cash flows -125,000 20,000 30,000 40,000 70,000 80,000 75,000

PVF @ 20% 1.000 0.833 0.694 0.579 0.482 0.402 0.335

PV -125,000 16,666.67 20,833.33 23,148.15 33,757.72 32,150.21 25,117.35

NPV 26,673.42

NPV of the Machine 2 is £26,673.42 approx.

Note:

As there is no corporate tax the estimation of depreciation won’t have any effect on the

estimation of the cash flows and this is why the same is ignored.

Recommendations:

a) as per the payback period estimation of both Alpha and Beta projects, the Project1 or

Alpha has a lower payback period of 2.0833 years and hence the same is recommended to

be invested. This is because while Alpha project would be able to recover the initial cash

investments in 2.0833 years the Beta Project or Beta Machine would take slightly higher

time frame of 2.5 years to recover the initial cash outflows. Thus Alpha (machine 1 is

recommended for investment) (Bender & Ward, 2012).

b) The NPV of the projects are estimated as £58,991.34 and £26,673.42 respectively. As

the Alpha project has a higher NPV of £58,991.34 the same is recommended for

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 14

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2025 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.