Calculating Fringe Benefits Tax Payable

VerifiedAdded on 2020/10/23

|8

|1986

|104

AI Summary

The provided document outlines the step-by-step process for calculating fringe benefits tax (FBT) payable by an employer in Australia. The calculation includes determining total fringe benefits, applying the gross-up rate to find the gross-up amount, and then multiplying this by the FBT rate to arrive at the FBT payable. The report takes into account specific details such as rent for an apartment being calculated after deducting the employee's contribution, and using the lower gross-up rate of 1.96608 as per Australian taxation authority for calculating the gross amount. This report follows relevant tax laws and regulations in Australia.

Contribute Materials

Your contribution can guide someone’s learning journey. Share your

documents today.

TAXATION LAW

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

Table of Contents

INTRODUCTION...........................................................................................................................1

Question 1 Calculation of net income for partnership firm.............................................................1

Question 2 Fringe benefits tax consequences for an employer.......................................................4

CONCLUSION................................................................................................................................5

REFERENCES................................................................................................................................6

INTRODUCTION...........................................................................................................................1

Question 1 Calculation of net income for partnership firm.............................................................1

Question 2 Fringe benefits tax consequences for an employer.......................................................4

CONCLUSION................................................................................................................................5

REFERENCES................................................................................................................................6

INTRODUCTION

In any company, there is a requirement to follow taxation law of the country in which it

operates business and revenue from that country. By the help of Taxation, a company can assess

its income and expenditure of the business and calculate the net income for the purpose of tax

payment. There are various Govt. Authorities which also mandatory to do the assessment

proceedings of the income of a company according to the provisions of taxation law. Taxation

law covers the Act, rules, regulations, notifications and circulars that assist the Govt ((Oats,

2012). authorities as well as companies to find out the correct income earned (taxable Income)

and accordingly income tax payable on this taxable income. This project includes two questions

and in each question, there is a different scenario is given, which need to be answered. First

question wants to calculate the net income for the year ended 30th June, 2017 of Daniel and

Olivia Smith operating business called Brekkie and Lunch and OZ Bottle Shop at 50 York

Street Sydney as a partnership firm. Second question contains the Fringe Benefits Tax

consequences for John who is senior executive at printing company and receiving various other

benefits like child's school fees, accommodation service along with his remuneration package. In

Australia all taxation related laws and related aspects are controlled and managed by the

Australian taxation authority (ATO).

Question 1 Calculation of net income for partnership firm

For calculation of net income for Daniel and Olivia Smith who are operated a mixed

business as Brekkie and Lunch and OZ Bottle Shop, trading and profit and loss account will

be required to calculate and this is prepared in a fixed format. The trading and Profit and loss

account for the partnership firm is as follows and it includes various working notes for easily

understanding the income calculation procedure:

Trading and P & L A/c for the Year ended 30th June, 2017

Particulars Amount ($) Particulars Amount ($)

To Opening Stock 9120

By Sales A/c ( working note

1) 182055

To Purchase ( working note 2) 160343

To Gross Profit (c/d) 22342 By Closing Stock 9750

1

In any company, there is a requirement to follow taxation law of the country in which it

operates business and revenue from that country. By the help of Taxation, a company can assess

its income and expenditure of the business and calculate the net income for the purpose of tax

payment. There are various Govt. Authorities which also mandatory to do the assessment

proceedings of the income of a company according to the provisions of taxation law. Taxation

law covers the Act, rules, regulations, notifications and circulars that assist the Govt ((Oats,

2012). authorities as well as companies to find out the correct income earned (taxable Income)

and accordingly income tax payable on this taxable income. This project includes two questions

and in each question, there is a different scenario is given, which need to be answered. First

question wants to calculate the net income for the year ended 30th June, 2017 of Daniel and

Olivia Smith operating business called Brekkie and Lunch and OZ Bottle Shop at 50 York

Street Sydney as a partnership firm. Second question contains the Fringe Benefits Tax

consequences for John who is senior executive at printing company and receiving various other

benefits like child's school fees, accommodation service along with his remuneration package. In

Australia all taxation related laws and related aspects are controlled and managed by the

Australian taxation authority (ATO).

Question 1 Calculation of net income for partnership firm

For calculation of net income for Daniel and Olivia Smith who are operated a mixed

business as Brekkie and Lunch and OZ Bottle Shop, trading and profit and loss account will

be required to calculate and this is prepared in a fixed format. The trading and Profit and loss

account for the partnership firm is as follows and it includes various working notes for easily

understanding the income calculation procedure:

Trading and P & L A/c for the Year ended 30th June, 2017

Particulars Amount ($) Particulars Amount ($)

To Opening Stock 9120

By Sales A/c ( working note

1) 182055

To Purchase ( working note 2) 160343

To Gross Profit (c/d) 22342 By Closing Stock 9750

1

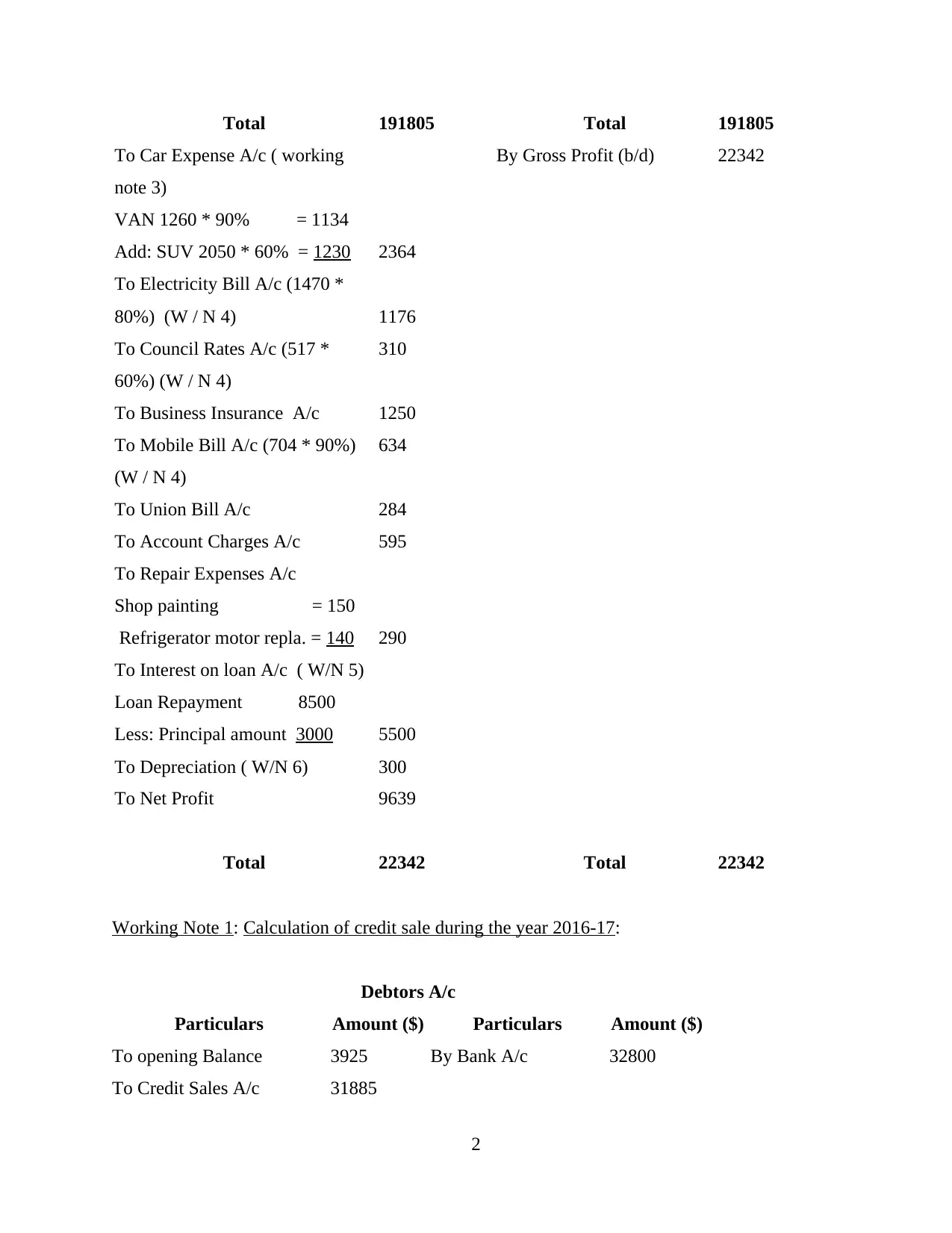

Total 191805 Total 191805

To Car Expense A/c ( working

note 3)

VAN 1260 * 90% = 1134

Add: SUV 2050 * 60% = 1230 2364

By Gross Profit (b/d) 22342

To Electricity Bill A/c (1470 *

80%) (W / N 4) 1176

To Council Rates A/c (517 *

60%) (W / N 4)

310

To Business Insurance A/c 1250

To Mobile Bill A/c (704 * 90%)

(W / N 4)

634

To Union Bill A/c 284

To Account Charges A/c 595

To Repair Expenses A/c

Shop painting = 150

Refrigerator motor repla. = 140 290

To Interest on loan A/c ( W/N 5)

Loan Repayment 8500

Less: Principal amount 3000 5500

To Depreciation ( W/N 6) 300

To Net Profit 9639

Total 22342 Total 22342

Working Note 1: Calculation of credit sale during the year 2016-17:

Debtors A/c

Particulars Amount ($) Particulars Amount ($)

To opening Balance 3925 By Bank A/c 32800

To Credit Sales A/c 31885

2

To Car Expense A/c ( working

note 3)

VAN 1260 * 90% = 1134

Add: SUV 2050 * 60% = 1230 2364

By Gross Profit (b/d) 22342

To Electricity Bill A/c (1470 *

80%) (W / N 4) 1176

To Council Rates A/c (517 *

60%) (W / N 4)

310

To Business Insurance A/c 1250

To Mobile Bill A/c (704 * 90%)

(W / N 4)

634

To Union Bill A/c 284

To Account Charges A/c 595

To Repair Expenses A/c

Shop painting = 150

Refrigerator motor repla. = 140 290

To Interest on loan A/c ( W/N 5)

Loan Repayment 8500

Less: Principal amount 3000 5500

To Depreciation ( W/N 6) 300

To Net Profit 9639

Total 22342 Total 22342

Working Note 1: Calculation of credit sale during the year 2016-17:

Debtors A/c

Particulars Amount ($) Particulars Amount ($)

To opening Balance 3925 By Bank A/c 32800

To Credit Sales A/c 31885

2

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

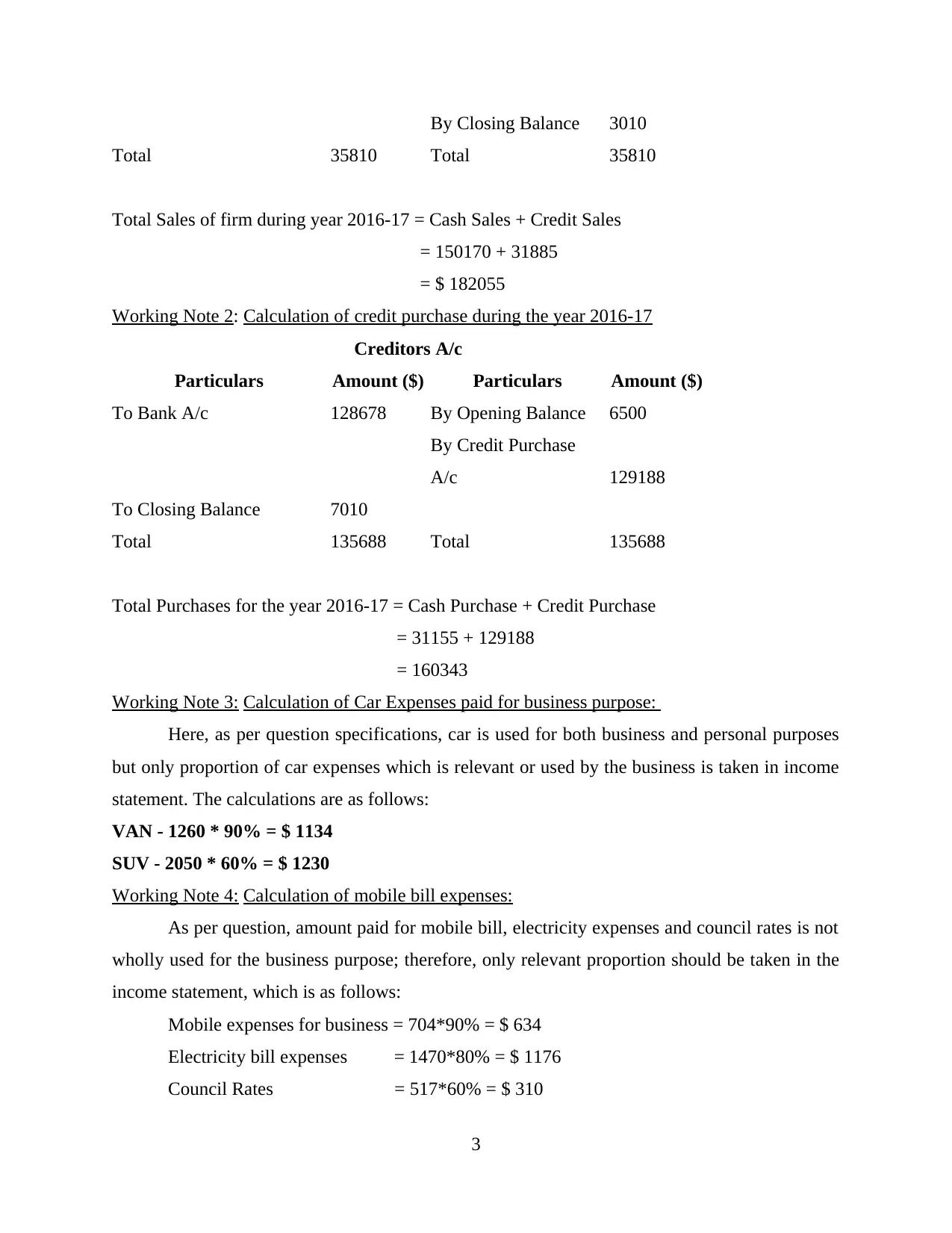

By Closing Balance 3010

Total 35810 Total 35810

Total Sales of firm during year 2016-17 = Cash Sales + Credit Sales

= 150170 + 31885

= $ 182055

Working Note 2: Calculation of credit purchase during the year 2016-17

Creditors A/c

Particulars Amount ($) Particulars Amount ($)

To Bank A/c 128678 By Opening Balance 6500

By Credit Purchase

A/c 129188

To Closing Balance 7010

Total 135688 Total 135688

Total Purchases for the year 2016-17 = Cash Purchase + Credit Purchase

= 31155 + 129188

= 160343

Working Note 3: Calculation of Car Expenses paid for business purpose:

Here, as per question specifications, car is used for both business and personal purposes

but only proportion of car expenses which is relevant or used by the business is taken in income

statement. The calculations are as follows:

VAN - 1260 * 90% = $ 1134

SUV - 2050 * 60% = $ 1230

Working Note 4: Calculation of mobile bill expenses:

As per question, amount paid for mobile bill, electricity expenses and council rates is not

wholly used for the business purpose; therefore, only relevant proportion should be taken in the

income statement, which is as follows:

Mobile expenses for business = 704*90% = $ 634

Electricity bill expenses = 1470*80% = $ 1176

Council Rates = 517*60% = $ 310

3

Total 35810 Total 35810

Total Sales of firm during year 2016-17 = Cash Sales + Credit Sales

= 150170 + 31885

= $ 182055

Working Note 2: Calculation of credit purchase during the year 2016-17

Creditors A/c

Particulars Amount ($) Particulars Amount ($)

To Bank A/c 128678 By Opening Balance 6500

By Credit Purchase

A/c 129188

To Closing Balance 7010

Total 135688 Total 135688

Total Purchases for the year 2016-17 = Cash Purchase + Credit Purchase

= 31155 + 129188

= 160343

Working Note 3: Calculation of Car Expenses paid for business purpose:

Here, as per question specifications, car is used for both business and personal purposes

but only proportion of car expenses which is relevant or used by the business is taken in income

statement. The calculations are as follows:

VAN - 1260 * 90% = $ 1134

SUV - 2050 * 60% = $ 1230

Working Note 4: Calculation of mobile bill expenses:

As per question, amount paid for mobile bill, electricity expenses and council rates is not

wholly used for the business purpose; therefore, only relevant proportion should be taken in the

income statement, which is as follows:

Mobile expenses for business = 704*90% = $ 634

Electricity bill expenses = 1470*80% = $ 1176

Council Rates = 517*60% = $ 310

3

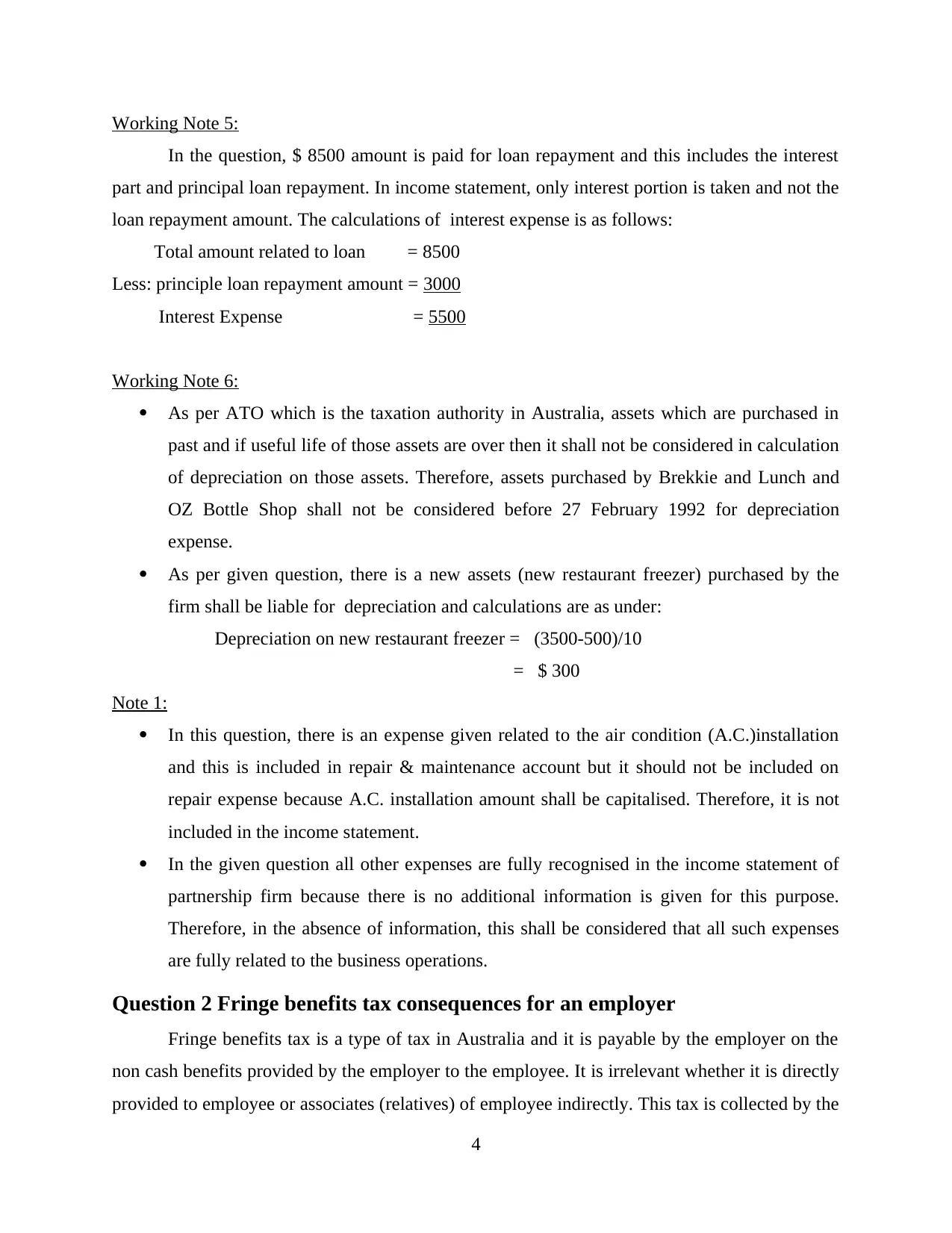

Working Note 5:

In the question, $ 8500 amount is paid for loan repayment and this includes the interest

part and principal loan repayment. In income statement, only interest portion is taken and not the

loan repayment amount. The calculations of interest expense is as follows:

Total amount related to loan = 8500

Less: principle loan repayment amount = 3000

Interest Expense = 5500

Working Note 6:

As per ATO which is the taxation authority in Australia, assets which are purchased in

past and if useful life of those assets are over then it shall not be considered in calculation

of depreciation on those assets. Therefore, assets purchased by Brekkie and Lunch and

OZ Bottle Shop shall not be considered before 27 February 1992 for depreciation

expense.

As per given question, there is a new assets (new restaurant freezer) purchased by the

firm shall be liable for depreciation and calculations are as under:

Depreciation on new restaurant freezer = (3500-500)/10

= $ 300

Note 1:

In this question, there is an expense given related to the air condition (A.C.)installation

and this is included in repair & maintenance account but it should not be included on

repair expense because A.C. installation amount shall be capitalised. Therefore, it is not

included in the income statement.

In the given question all other expenses are fully recognised in the income statement of

partnership firm because there is no additional information is given for this purpose.

Therefore, in the absence of information, this shall be considered that all such expenses

are fully related to the business operations.

Question 2 Fringe benefits tax consequences for an employer

Fringe benefits tax is a type of tax in Australia and it is payable by the employer on the

non cash benefits provided by the employer to the employee. It is irrelevant whether it is directly

provided to employee or associates (relatives) of employee indirectly. This tax is collected by the

4

In the question, $ 8500 amount is paid for loan repayment and this includes the interest

part and principal loan repayment. In income statement, only interest portion is taken and not the

loan repayment amount. The calculations of interest expense is as follows:

Total amount related to loan = 8500

Less: principle loan repayment amount = 3000

Interest Expense = 5500

Working Note 6:

As per ATO which is the taxation authority in Australia, assets which are purchased in

past and if useful life of those assets are over then it shall not be considered in calculation

of depreciation on those assets. Therefore, assets purchased by Brekkie and Lunch and

OZ Bottle Shop shall not be considered before 27 February 1992 for depreciation

expense.

As per given question, there is a new assets (new restaurant freezer) purchased by the

firm shall be liable for depreciation and calculations are as under:

Depreciation on new restaurant freezer = (3500-500)/10

= $ 300

Note 1:

In this question, there is an expense given related to the air condition (A.C.)installation

and this is included in repair & maintenance account but it should not be included on

repair expense because A.C. installation amount shall be capitalised. Therefore, it is not

included in the income statement.

In the given question all other expenses are fully recognised in the income statement of

partnership firm because there is no additional information is given for this purpose.

Therefore, in the absence of information, this shall be considered that all such expenses

are fully related to the business operations.

Question 2 Fringe benefits tax consequences for an employer

Fringe benefits tax is a type of tax in Australia and it is payable by the employer on the

non cash benefits provided by the employer to the employee. It is irrelevant whether it is directly

provided to employee or associates (relatives) of employee indirectly. This tax is collected by the

4

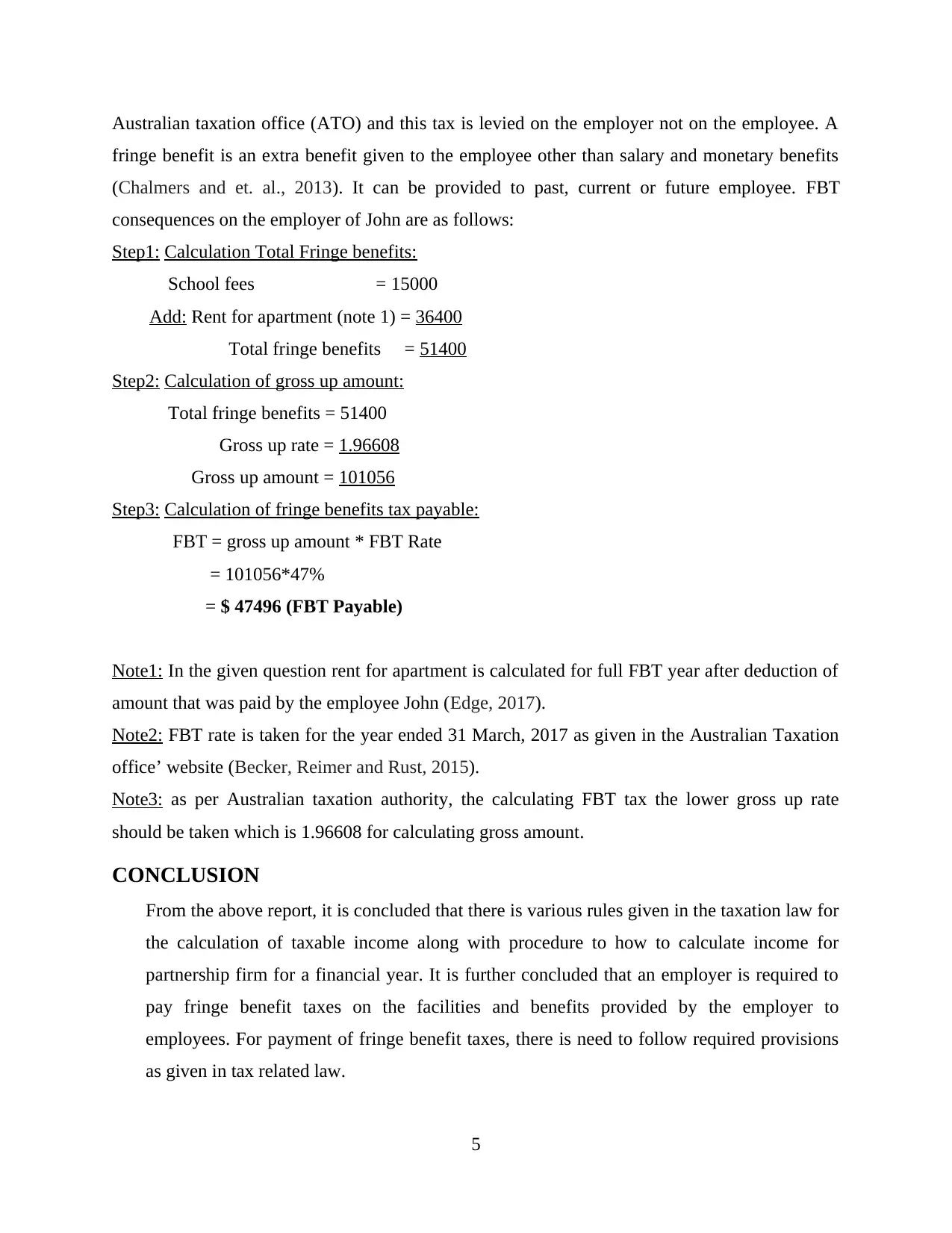

Australian taxation office (ATO) and this tax is levied on the employer not on the employee. A

fringe benefit is an extra benefit given to the employee other than salary and monetary benefits

(Chalmers and et. al., 2013). It can be provided to past, current or future employee. FBT

consequences on the employer of John are as follows:

Step1: Calculation Total Fringe benefits:

School fees = 15000

Add: Rent for apartment (note 1) = 36400

Total fringe benefits = 51400

Step2: Calculation of gross up amount:

Total fringe benefits = 51400

Gross up rate = 1.96608

Gross up amount = 101056

Step3: Calculation of fringe benefits tax payable:

FBT = gross up amount * FBT Rate

= 101056*47%

= $ 47496 (FBT Payable)

Note1: In the given question rent for apartment is calculated for full FBT year after deduction of

amount that was paid by the employee John (Edge, 2017).

Note2: FBT rate is taken for the year ended 31 March, 2017 as given in the Australian Taxation

office’ website (Becker, Reimer and Rust, 2015).

Note3: as per Australian taxation authority, the calculating FBT tax the lower gross up rate

should be taken which is 1.96608 for calculating gross amount.

CONCLUSION

From the above report, it is concluded that there is various rules given in the taxation law for

the calculation of taxable income along with procedure to how to calculate income for

partnership firm for a financial year. It is further concluded that an employer is required to

pay fringe benefit taxes on the facilities and benefits provided by the employer to

employees. For payment of fringe benefit taxes, there is need to follow required provisions

as given in tax related law.

5

fringe benefit is an extra benefit given to the employee other than salary and monetary benefits

(Chalmers and et. al., 2013). It can be provided to past, current or future employee. FBT

consequences on the employer of John are as follows:

Step1: Calculation Total Fringe benefits:

School fees = 15000

Add: Rent for apartment (note 1) = 36400

Total fringe benefits = 51400

Step2: Calculation of gross up amount:

Total fringe benefits = 51400

Gross up rate = 1.96608

Gross up amount = 101056

Step3: Calculation of fringe benefits tax payable:

FBT = gross up amount * FBT Rate

= 101056*47%

= $ 47496 (FBT Payable)

Note1: In the given question rent for apartment is calculated for full FBT year after deduction of

amount that was paid by the employee John (Edge, 2017).

Note2: FBT rate is taken for the year ended 31 March, 2017 as given in the Australian Taxation

office’ website (Becker, Reimer and Rust, 2015).

Note3: as per Australian taxation authority, the calculating FBT tax the lower gross up rate

should be taken which is 1.96608 for calculating gross amount.

CONCLUSION

From the above report, it is concluded that there is various rules given in the taxation law for

the calculation of taxable income along with procedure to how to calculate income for

partnership firm for a financial year. It is further concluded that an employer is required to

pay fringe benefit taxes on the facilities and benefits provided by the employer to

employees. For payment of fringe benefit taxes, there is need to follow required provisions

as given in tax related law.

5

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

REFERENCES

Oats, L. ed., 2012. Taxation: A fieldwork research handbook. Routledge.

Chalmers, J and et. Al., 2013. Real or perceived impediments to minimum pricing of alcohol in

Australia: public opinion, the industry and the law. International Journal of Drug

Policy. 24(6). pp.517-523.

Edge, P.W., 2017. Religion and law: An introduction. Routledge.

Becker, J., Reimer, E. and Rust, A., 2015. Klaus Vogel on Double Taxation Conventions. Kluwer

Law International.

Martin, N.J. and Rice, J.L., 2012. Developing renewable energy supply in Queensland, Australia:

A study of the barriers, targets, policies and actions. Renewable Energy. 44. pp.119-

127.

Lang, M., 2014. Introduction to the law of double taxation conventions. Linde Verlag GmbH.

Basu, S., 2016. Global perspectives on e-commerce taxation law. Routledge.

Berns, S., 2017. Women Going Backwards: Law and change in a family unfriendly society.

Routledge.

Endres, D. and Spengel, C. eds., 2015. International company taxation and tax planning. Alphen

aan Den Rijn: Kluwer Law International.

Sagaram, J.P.A. and Wickramanayake, J., 2012. Financial centers in the Asia-pacific region: an

empirical study on australia, Hong Kong, Japan and Singapore. PSL Quarterly

Review. 58(232.

6

Oats, L. ed., 2012. Taxation: A fieldwork research handbook. Routledge.

Chalmers, J and et. Al., 2013. Real or perceived impediments to minimum pricing of alcohol in

Australia: public opinion, the industry and the law. International Journal of Drug

Policy. 24(6). pp.517-523.

Edge, P.W., 2017. Religion and law: An introduction. Routledge.

Becker, J., Reimer, E. and Rust, A., 2015. Klaus Vogel on Double Taxation Conventions. Kluwer

Law International.

Martin, N.J. and Rice, J.L., 2012. Developing renewable energy supply in Queensland, Australia:

A study of the barriers, targets, policies and actions. Renewable Energy. 44. pp.119-

127.

Lang, M., 2014. Introduction to the law of double taxation conventions. Linde Verlag GmbH.

Basu, S., 2016. Global perspectives on e-commerce taxation law. Routledge.

Berns, S., 2017. Women Going Backwards: Law and change in a family unfriendly society.

Routledge.

Endres, D. and Spengel, C. eds., 2015. International company taxation and tax planning. Alphen

aan Den Rijn: Kluwer Law International.

Sagaram, J.P.A. and Wickramanayake, J., 2012. Financial centers in the Asia-pacific region: an

empirical study on australia, Hong Kong, Japan and Singapore. PSL Quarterly

Review. 58(232.

6

1 out of 8

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

© 2024 | Zucol Services PVT LTD | All rights reserved.