Taxation Law 2022 Question Answer

VerifiedAdded on 2022/09/26

|18

|3538

|24

AI Summary

Contribute Materials

Your contribution can guide someone’s learning journey. Share your

documents today.

Running head: TAXATION LAW

Taxation Law

Name of the Student:

Name of the University:

Author Note

Taxation Law

Name of the Student:

Name of the University:

Author Note

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

1TAXATION LAW

Table of Contents

Answer to Question 1:................................................................................................................3

Answer to part A:...................................................................................................................3

Answer to part B:...................................................................................................................3

Answer to part C:...................................................................................................................3

Answer to part D:...................................................................................................................4

Answer to part E:...................................................................................................................4

Answer to part F:....................................................................................................................4

Answer to part G:...................................................................................................................4

Answer to part H:...................................................................................................................5

Answer to part I:.....................................................................................................................6

Answer to Question 2-...............................................................................................................7

Answer to Question 3:................................................................................................................9

Answer to Question 4:..............................................................................................................13

Answer to part A:.................................................................................................................13

Answer to part B:.................................................................................................................14

Answer to part C:.................................................................................................................14

Answer to part D:.................................................................................................................15

Answer to Question 5-.............................................................................................................15

Answer to part A:.................................................................................................................15

Answer to part B:.................................................................................................................16

Table of Contents

Answer to Question 1:................................................................................................................3

Answer to part A:...................................................................................................................3

Answer to part B:...................................................................................................................3

Answer to part C:...................................................................................................................3

Answer to part D:...................................................................................................................4

Answer to part E:...................................................................................................................4

Answer to part F:....................................................................................................................4

Answer to part G:...................................................................................................................4

Answer to part H:...................................................................................................................5

Answer to part I:.....................................................................................................................6

Answer to Question 2-...............................................................................................................7

Answer to Question 3:................................................................................................................9

Answer to Question 4:..............................................................................................................13

Answer to part A:.................................................................................................................13

Answer to part B:.................................................................................................................14

Answer to part C:.................................................................................................................14

Answer to part D:.................................................................................................................15

Answer to Question 5-.............................................................................................................15

Answer to part A:.................................................................................................................15

Answer to part B:.................................................................................................................16

2TAXATION LAW

Answer to part C:.................................................................................................................16

Answer to part D:.................................................................................................................17

Answer to part E:.................................................................................................................17

References:...............................................................................................................................18

Answer to part C:.................................................................................................................16

Answer to part D:.................................................................................................................17

Answer to part E:.................................................................................................................17

References:...............................................................................................................................18

3TAXATION LAW

Answer to Question 1:

Answer to part A:

Generally an organization which perform its business operation as a small business

entity followed the viewpoints of a tax commissioner under “Sec-23 of the Income Tax Rates

Act 1986”, which is allocable from the FY 2015-16 and 2016-17 or followed the “sec-328-

110, ITAA 1997”1.

Answer to part B:

Gift or any contribution made by relatives allowed for deduction in order such gift or

contributing must be consider as donation followed “Division 30, ITAA 1997”.

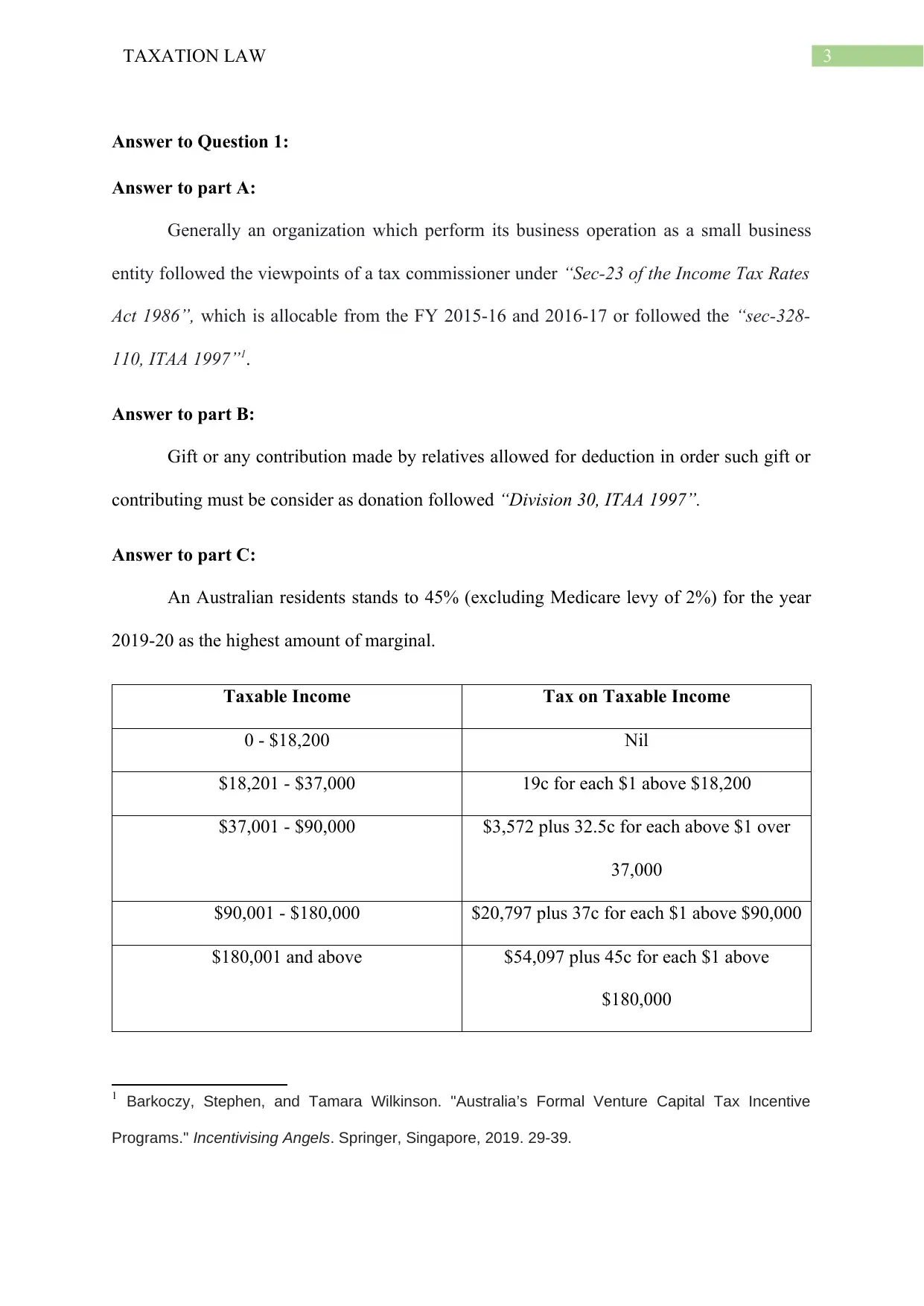

Answer to part C:

An Australian residents stands to 45% (excluding Medicare levy of 2%) for the year

2019-20 as the highest amount of marginal.

Taxable Income Tax on Taxable Income

0 - $18,200 Nil

$18,201 - $37,000 19c for each $1 above $18,200

$37,001 - $90,000 $3,572 plus 32.5c for each above $1 over

37,000

$90,001 - $180,000 $20,797 plus 37c for each $1 above $90,000

$180,001 and above $54,097 plus 45c for each $1 above

$180,000

1 Barkoczy, Stephen, and Tamara Wilkinson. "Australia’s Formal Venture Capital Tax Incentive

Programs." Incentivising Angels. Springer, Singapore, 2019. 29-39.

Answer to Question 1:

Answer to part A:

Generally an organization which perform its business operation as a small business

entity followed the viewpoints of a tax commissioner under “Sec-23 of the Income Tax Rates

Act 1986”, which is allocable from the FY 2015-16 and 2016-17 or followed the “sec-328-

110, ITAA 1997”1.

Answer to part B:

Gift or any contribution made by relatives allowed for deduction in order such gift or

contributing must be consider as donation followed “Division 30, ITAA 1997”.

Answer to part C:

An Australian residents stands to 45% (excluding Medicare levy of 2%) for the year

2019-20 as the highest amount of marginal.

Taxable Income Tax on Taxable Income

0 - $18,200 Nil

$18,201 - $37,000 19c for each $1 above $18,200

$37,001 - $90,000 $3,572 plus 32.5c for each above $1 over

37,000

$90,001 - $180,000 $20,797 plus 37c for each $1 above $90,000

$180,001 and above $54,097 plus 45c for each $1 above

$180,000

1 Barkoczy, Stephen, and Tamara Wilkinson. "Australia’s Formal Venture Capital Tax Incentive

Programs." Incentivising Angels. Springer, Singapore, 2019. 29-39.

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

4TAXATION LAW

Answer to part D:

Motorcycle or car use for personal purpose considered as personal assets followed

under the “sec-108-20 of the ITAA 1997”, however for the computation of capital gain tax,

those consider as taxable elements and no exemptions or deduction are allowed for such

assets.

Answer to part E:

Event C1 generally occurred while the Computation of capital gain tax followed

under “sec-104-20 of the ITAA 1997”,When a taxable assets, which is charged under capital

gain taxability held by the taxpayer is either destroyed or lost2. The capital gain event

occurred, while C1 is normally applied for particular portion of capital gain assets on which

no payment is generated by the taxpayer for considering any loss or damages of such assets3.

Answer to part F:

At present the tax-free threshold limit for a residential individual is $18,200 in the

financial year 2019-20.

Answer to part G:

The law court issued a discernment on behalf of a fact that while a other than private

company was founded by a previous employer and for contribution he has received a

preferable amount of shares from such company in case of providing free service relating to

provide advices to such company in “Hayes vs. FCT (1956)”. For providing such advices a

normal amount paid by an accountant to such employer and such payment is paid out of

2 Kenny, Paul. "Small business capital allowances." (2018).

3

Answer to part D:

Motorcycle or car use for personal purpose considered as personal assets followed

under the “sec-108-20 of the ITAA 1997”, however for the computation of capital gain tax,

those consider as taxable elements and no exemptions or deduction are allowed for such

assets.

Answer to part E:

Event C1 generally occurred while the Computation of capital gain tax followed

under “sec-104-20 of the ITAA 1997”,When a taxable assets, which is charged under capital

gain taxability held by the taxpayer is either destroyed or lost2. The capital gain event

occurred, while C1 is normally applied for particular portion of capital gain assets on which

no payment is generated by the taxpayer for considering any loss or damages of such assets3.

Answer to part F:

At present the tax-free threshold limit for a residential individual is $18,200 in the

financial year 2019-20.

Answer to part G:

The law court issued a discernment on behalf of a fact that while a other than private

company was founded by a previous employer and for contribution he has received a

preferable amount of shares from such company in case of providing free service relating to

provide advices to such company in “Hayes vs. FCT (1956)”. For providing such advices a

normal amount paid by an accountant to such employer and such payment is paid out of

2 Kenny, Paul. "Small business capital allowances." (2018).

3

5TAXATION LAW

customary friendship between them not because of professional reasons4. Followed the

judgement the law court draws an attentions through providing a judgement that in case of

any gift received from relatives and if no revenues are generating from there than such

amount of gift will not consider as income and not chargeable to tax as per Income tax act.

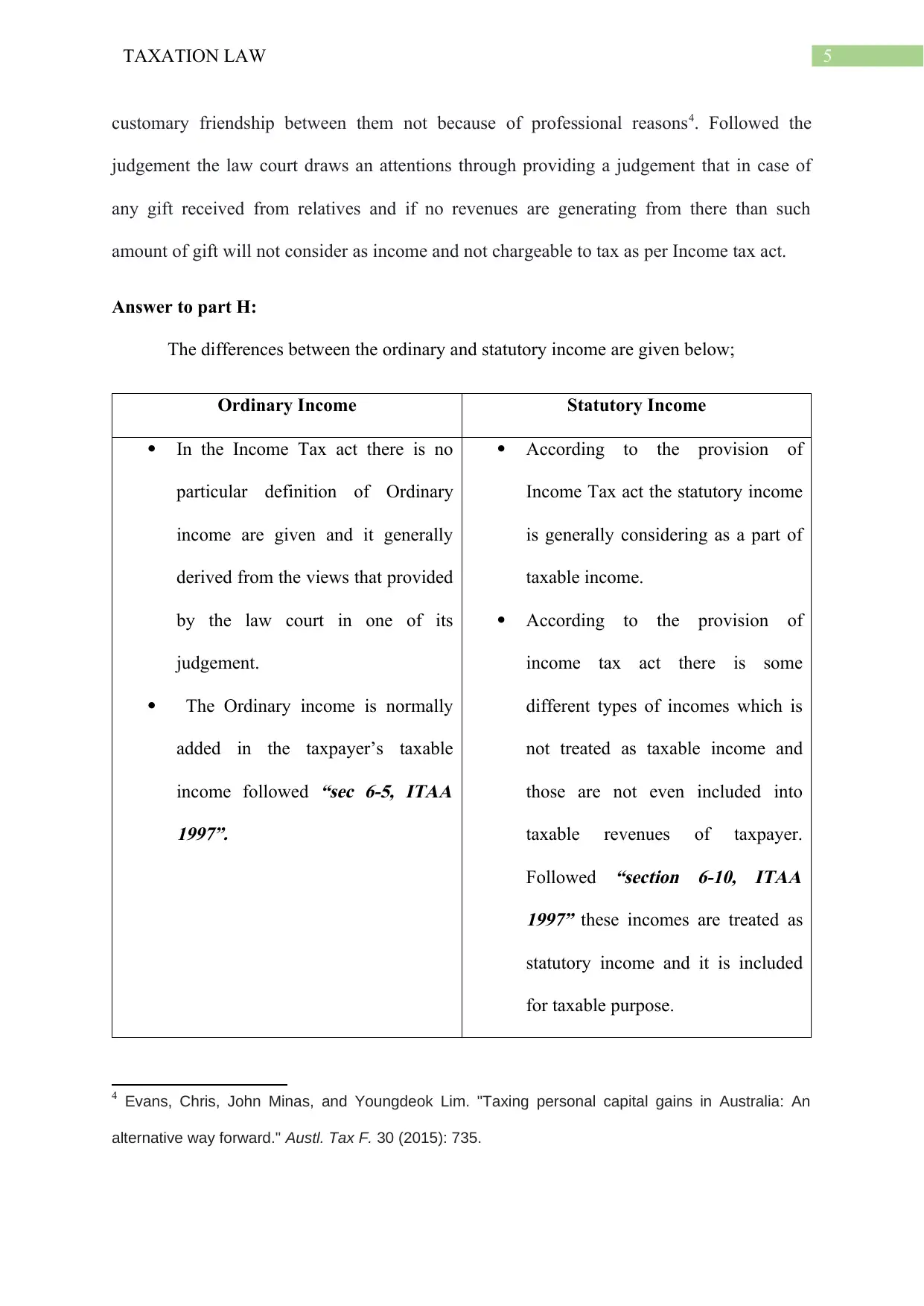

Answer to part H:

The differences between the ordinary and statutory income are given below;

Ordinary Income Statutory Income

In the Income Tax act there is no

particular definition of Ordinary

income are given and it generally

derived from the views that provided

by the law court in one of its

judgement.

The Ordinary income is normally

added in the taxpayer’s taxable

income followed

“sec 6-5, ITAA

1997”.

According to the provision of

Income Tax act the statutory income

is generally considering as a part of

taxable income.

According to the provision of

income tax act there is some

different types of incomes which is

not treated as taxable income and

those are not even included into

taxable revenues of taxpayer.

Followed

“section 6-10, ITAA

1997” these incomes are treated as

statutory income and it is included

for taxable purpose.

4 Evans, Chris, John Minas, and Youngdeok Lim. "Taxing personal capital gains in Australia: An

alternative way forward." Austl. Tax F. 30 (2015): 735.

customary friendship between them not because of professional reasons4. Followed the

judgement the law court draws an attentions through providing a judgement that in case of

any gift received from relatives and if no revenues are generating from there than such

amount of gift will not consider as income and not chargeable to tax as per Income tax act.

Answer to part H:

The differences between the ordinary and statutory income are given below;

Ordinary Income Statutory Income

In the Income Tax act there is no

particular definition of Ordinary

income are given and it generally

derived from the views that provided

by the law court in one of its

judgement.

The Ordinary income is normally

added in the taxpayer’s taxable

income followed

“sec 6-5, ITAA

1997”.

According to the provision of

Income Tax act the statutory income

is generally considering as a part of

taxable income.

According to the provision of

income tax act there is some

different types of incomes which is

not treated as taxable income and

those are not even included into

taxable revenues of taxpayer.

Followed

“section 6-10, ITAA

1997” these incomes are treated as

statutory income and it is included

for taxable purpose.

4 Evans, Chris, John Minas, and Youngdeok Lim. "Taxing personal capital gains in Australia: An

alternative way forward." Austl. Tax F. 30 (2015): 735.

6TAXATION LAW

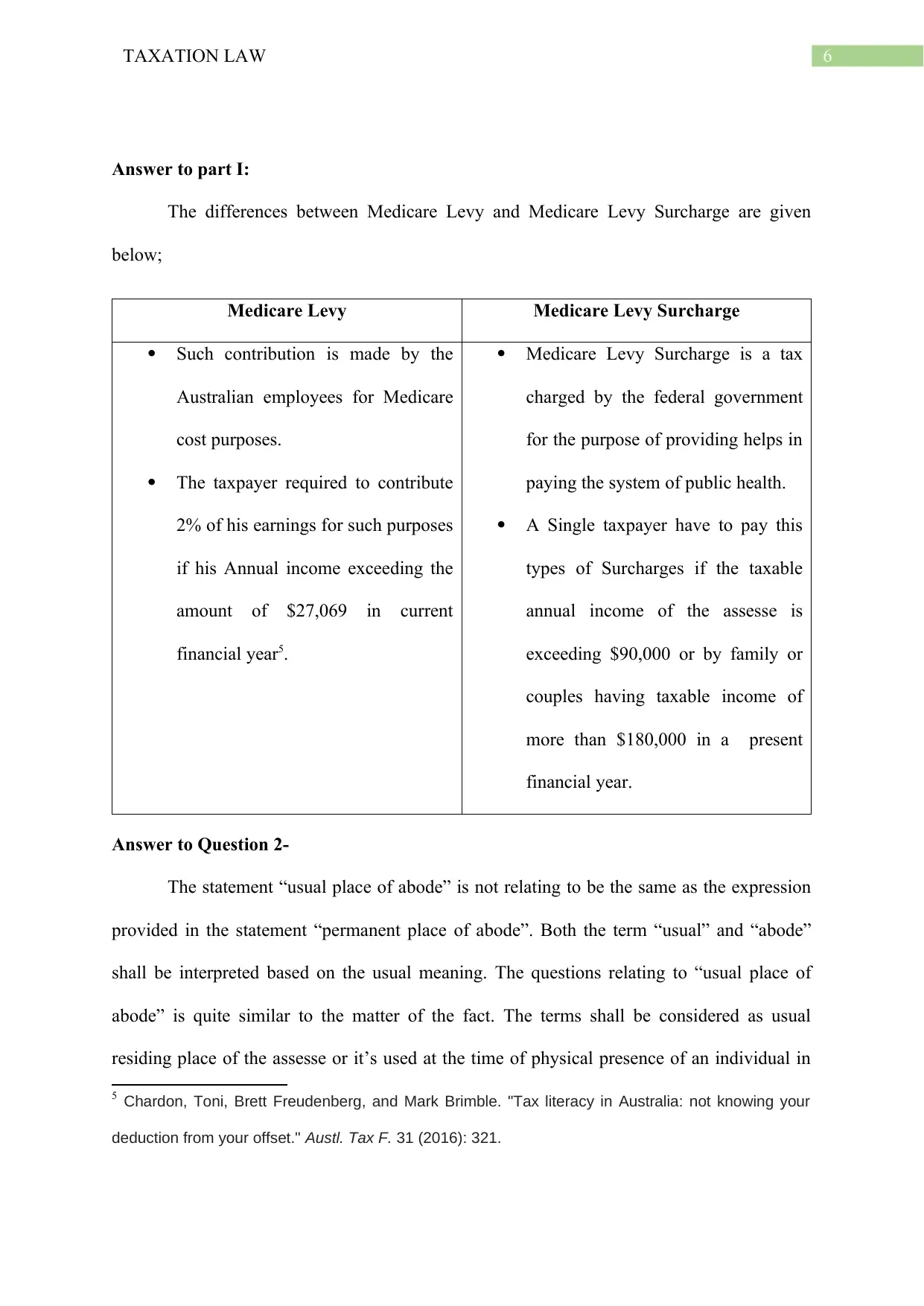

Answer to part I:

The differences between Medicare Levy and Medicare Levy Surcharge are given

below;

Medicare Levy Medicare Levy Surcharge

Such contribution is made by the

Australian employees for Medicare

cost purposes.

The taxpayer required to contribute

2% of his earnings for such purposes

if his Annual income exceeding the

amount of $27,069 in current

financial year5.

Medicare Levy Surcharge is a tax

charged by the federal government

for the purpose of providing helps in

paying the system of public health.

A Single taxpayer have to pay this

types of Surcharges if the taxable

annual income of the assesse is

exceeding $90,000 or by family or

couples having taxable income of

more than $180,000 in a present

financial year.

Answer to Question 2-

The statement “usual place of abode” is not relating to be the same as the expression

provided in the statement “permanent place of abode”. Both the term “usual” and “abode”

shall be interpreted based on the usual meaning. The questions relating to “usual place of

abode” is quite similar to the matter of the fact. The terms shall be considered as usual

residing place of the assesse or it’s used at the time of physical presence of an individual in

5 Chardon, Toni, Brett Freudenberg, and Mark Brimble. "Tax literacy in Australia: not knowing your

deduction from your offset." Austl. Tax F. 31 (2016): 321.

Answer to part I:

The differences between Medicare Levy and Medicare Levy Surcharge are given

below;

Medicare Levy Medicare Levy Surcharge

Such contribution is made by the

Australian employees for Medicare

cost purposes.

The taxpayer required to contribute

2% of his earnings for such purposes

if his Annual income exceeding the

amount of $27,069 in current

financial year5.

Medicare Levy Surcharge is a tax

charged by the federal government

for the purpose of providing helps in

paying the system of public health.

A Single taxpayer have to pay this

types of Surcharges if the taxable

annual income of the assesse is

exceeding $90,000 or by family or

couples having taxable income of

more than $180,000 in a present

financial year.

Answer to Question 2-

The statement “usual place of abode” is not relating to be the same as the expression

provided in the statement “permanent place of abode”. Both the term “usual” and “abode”

shall be interpreted based on the usual meaning. The questions relating to “usual place of

abode” is quite similar to the matter of the fact. The terms shall be considered as usual

residing place of the assesse or it’s used at the time of physical presence of an individual in

5 Chardon, Toni, Brett Freudenberg, and Mark Brimble. "Tax literacy in Australia: not knowing your

deduction from your offset." Austl. Tax F. 31 (2016): 321.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

7TAXATION LAW

that country. An individual’s “usual place of abode” should be perpetual but it should show

the dwelling quality in comparison to monthly, weekly basis or overnight place of housing

for a traveller6. It comprises a relation, which is long-term in nature with the payer of tax

having a place of residence over those who generally have been dwelling or have their “usual

place of abode” inside Australia.

However if an assesse has an “usual place of abode” inside Australia and also doesn’t

have any fixed place of residence in other countries and who is intends to move from one

country to another or relocates constantly in the domestic country or has relation with

particular overseas place, then the living will not be consider as the permanent place of his

living. In such situations, the payer of tax will not be accepted to have taken other living

place of their option or “permanent place of abode” external to Australia.

The concept “permanent place of abode” means the assesse has their residence in

Australia. According to the “subparagraph (a) (i)’’, the concept of “resident” is deriving that

it needs to satisfy the tax commissioner that the assessment must have “permanent place of

abode” is within Australia. The concept of “place of abode” means that an individual must

have a dwelling where he and his family stay together. Even in “Levene v IRC (1928)” the

law court is providing that same concept relates to the home of an assessed7.

In case of “FCT v Applegate (1979)” it was an Australian residence that understood

by the taxpayers, as well as it travelled the New Hebrides to establish an office branch the tax

6 Jones, Daryl. "Complexity of tax residency attracts review." Taxation in Australia 53.6 (2018): 296.

7

that country. An individual’s “usual place of abode” should be perpetual but it should show

the dwelling quality in comparison to monthly, weekly basis or overnight place of housing

for a traveller6. It comprises a relation, which is long-term in nature with the payer of tax

having a place of residence over those who generally have been dwelling or have their “usual

place of abode” inside Australia.

However if an assesse has an “usual place of abode” inside Australia and also doesn’t

have any fixed place of residence in other countries and who is intends to move from one

country to another or relocates constantly in the domestic country or has relation with

particular overseas place, then the living will not be consider as the permanent place of his

living. In such situations, the payer of tax will not be accepted to have taken other living

place of their option or “permanent place of abode” external to Australia.

The concept “permanent place of abode” means the assesse has their residence in

Australia. According to the “subparagraph (a) (i)’’, the concept of “resident” is deriving that

it needs to satisfy the tax commissioner that the assessment must have “permanent place of

abode” is within Australia. The concept of “place of abode” means that an individual must

have a dwelling where he and his family stay together. Even in “Levene v IRC (1928)” the

law court is providing that same concept relates to the home of an assessed7.

In case of “FCT v Applegate (1979)” it was an Australian residence that understood

by the taxpayers, as well as it travelled the New Hebrides to establish an office branch the tax

6 Jones, Daryl. "Complexity of tax residency attracts review." Taxation in Australia 53.6 (2018): 296.

7

8TAXATION LAW

payer for that relevant year was considered non-resident as held by the commissioner using

the principle of permanent place of abode8.

Alternatively, while in “FCT v Jenkins (1982)” the taxpayer was considered as bank

officer who shifted to New Hebrides for the duration of 3 years and he had come back to

Australia after the completion of 18 months only due to sickness9. The court further explained

about the taxpayers that it was the permanent “place for the abode” was not at all in Australia

all the year and he had not spent any time for living in place of New Hebrides. Both the cases

explained about permanent place of abode and it cannot be judged through implementation of

hard as well as fast rules.

On behalf of the above discussion providing the clear idea about that the taxpayer

need to made satisfied about usual place of abode which is outside the place of Australia on

the other hand the test makes necessary for a person to get satisfied about permanent place for

abode which is not existed in place of Australia.

8 Norbury, Michael. "Mr Harding's residence reconsidered." Taxation in Australia 53.9 (2019): 497.

9 Idris, Nuhu Musa. "Some comparisons between the Nigerian and South African fiscal regimes

regarding an individual’s tax residence." Obiter 39.1 (2018): 76-84.

payer for that relevant year was considered non-resident as held by the commissioner using

the principle of permanent place of abode8.

Alternatively, while in “FCT v Jenkins (1982)” the taxpayer was considered as bank

officer who shifted to New Hebrides for the duration of 3 years and he had come back to

Australia after the completion of 18 months only due to sickness9. The court further explained

about the taxpayers that it was the permanent “place for the abode” was not at all in Australia

all the year and he had not spent any time for living in place of New Hebrides. Both the cases

explained about permanent place of abode and it cannot be judged through implementation of

hard as well as fast rules.

On behalf of the above discussion providing the clear idea about that the taxpayer

need to made satisfied about usual place of abode which is outside the place of Australia on

the other hand the test makes necessary for a person to get satisfied about permanent place for

abode which is not existed in place of Australia.

8 Norbury, Michael. "Mr Harding's residence reconsidered." Taxation in Australia 53.9 (2019): 497.

9 Idris, Nuhu Musa. "Some comparisons between the Nigerian and South African fiscal regimes

regarding an individual’s tax residence." Obiter 39.1 (2018): 76-84.

9TAXATION LAW

Answer to Question 3:

HECS HELP: $850

As per ATO, taxpayer is permissible for deduction of allowable income tax for

outgoings of self-education in case of all the expenses are under taxpayer’s assessable

earnings. As per ATO, the expenses being incurred by the individual for self-education as

well as if the eligibility is satisfied in that case Free-Help or VET or loan that is provided to

the student under HECS-HELP shall not be considerable for deduction purpose. Again,

within HECS-HELP expenses for $850 is considerable for expenditure for being non-

deductible.

Travel-work in University $110:

Expenditure being deductible includes maintenance and increase in the skills of

taxpayer for service is presently engaged for outgoings in case of improvement in income for

future period for possibility provision to taxpayer.

Under “Finn v FCT (1961)” income tax deduction is permitted and is allowable for

architect who has been employed as per WA Government for expenditure purpose with

respect to travelling related to overseas travelling for the assessment year for studying

architecture10. The court held that the tour was connected to nature and was acquainted to

taxpayer’s employment.

In current case of travel with respect to work as per University will be considered for

deduction under “section 8-1, ITTA 1997” as expenditure with respect to travel was

happening one in terms of nature and was acquainted to the employment of taxpayer.

10 Lee, Joanne. "The Effectiveness of Part IVA of the Income Tax Assessment Act 1936 (CTH): Time

for a Not Merely Incidental'Purpose Test." J. Austl. Tax'n 20 (2018): 1.

Answer to Question 3:

HECS HELP: $850

As per ATO, taxpayer is permissible for deduction of allowable income tax for

outgoings of self-education in case of all the expenses are under taxpayer’s assessable

earnings. As per ATO, the expenses being incurred by the individual for self-education as

well as if the eligibility is satisfied in that case Free-Help or VET or loan that is provided to

the student under HECS-HELP shall not be considerable for deduction purpose. Again,

within HECS-HELP expenses for $850 is considerable for expenditure for being non-

deductible.

Travel-work in University $110:

Expenditure being deductible includes maintenance and increase in the skills of

taxpayer for service is presently engaged for outgoings in case of improvement in income for

future period for possibility provision to taxpayer.

Under “Finn v FCT (1961)” income tax deduction is permitted and is allowable for

architect who has been employed as per WA Government for expenditure purpose with

respect to travelling related to overseas travelling for the assessment year for studying

architecture10. The court held that the tour was connected to nature and was acquainted to

taxpayer’s employment.

In current case of travel with respect to work as per University will be considered for

deduction under “section 8-1, ITTA 1997” as expenditure with respect to travel was

happening one in terms of nature and was acquainted to the employment of taxpayer.

10 Lee, Joanne. "The Effectiveness of Part IVA of the Income Tax Assessment Act 1936 (CTH): Time

for a Not Merely Incidental'Purpose Test." J. Austl. Tax'n 20 (2018): 1.

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

10TAXATION LAW

Books of $200:

Expenses for self-education in terms of cost for study-materials such as-calculators,

textbooks and stationary as well for improving promotion and earning capacities of taxpayers

are considerable for deduction as per “section 8-1,ITTA 1997”. Under “FCT v Highfield

(1982)” general practice carried by the dentist is considerable for deduction that is

permissible for outgoings closely related to fees and accommodation for self-education

undertaking expenses.

In current case of expenses with respect to books that is considerable will be accepted

for further deduction under “section 8-1, ITAA 1997” as expenses were considerable for

improvement in case of promotion for future time and earning capacities of taxpayer11.

Childcare for evening classes$80:

As per “section 8-1(2)(b), ITAA 1997” expenses considerable for domestic and

private in nature are not considerable for deduction as criteria is not meeting positivity and

also non-deductible for norms of negativity. Under “FCT v Lodge (1972)” court does not

held for deduction of taxpayer for expenses in case of child care for her child to be as minded

and also be present for her work. In case, court expenses does not remain acquainted to

income activities of the taxpayer12.

11 Castelyn, Donovan, Helen Hodgson, and Lisa Marriott. "Income equalisation: is all fair in primary

production and tax law?." Australian Tax Forum. Vol. 34. No. 2. 2019.

Books of $200:

Expenses for self-education in terms of cost for study-materials such as-calculators,

textbooks and stationary as well for improving promotion and earning capacities of taxpayers

are considerable for deduction as per “section 8-1,ITTA 1997”. Under “FCT v Highfield

(1982)” general practice carried by the dentist is considerable for deduction that is

permissible for outgoings closely related to fees and accommodation for self-education

undertaking expenses.

In current case of expenses with respect to books that is considerable will be accepted

for further deduction under “section 8-1, ITAA 1997” as expenses were considerable for

improvement in case of promotion for future time and earning capacities of taxpayer11.

Childcare for evening classes$80:

As per “section 8-1(2)(b), ITAA 1997” expenses considerable for domestic and

private in nature are not considerable for deduction as criteria is not meeting positivity and

also non-deductible for norms of negativity. Under “FCT v Lodge (1972)” court does not

held for deduction of taxpayer for expenses in case of child care for her child to be as minded

and also be present for her work. In case, court expenses does not remain acquainted to

income activities of the taxpayer12.

11 Castelyn, Donovan, Helen Hodgson, and Lisa Marriott. "Income equalisation: is all fair in primary

production and tax law?." Australian Tax Forum. Vol. 34. No. 2. 2019.

11TAXATION LAW

In case of current situation of the expenditure that is connected to childcare of $80

which is paid by the taxpayer in case of remaining present in evening classes were not

connected for income related activities of the taxpayer.

Repair of fridge at home for approximately $250:

An individual who is a taxpayer is not permissible for claim of deduction under

“section 8-1(2) (b), ITAA 1997” such that the outgoings are not considerable for being

private and domestic in terms of nature. Under court held “Lunney v FCT (1958)” it is

necessary to analyse the loss and outgoings for being considerable as an important

prerequisite for sourcing of taxable returns. In the same way , repairs in terms of fringe at

home for near about $250 is not considerable for future deduction under “section 8-1(2)

(b),ITAA 1997” as expenses are considerable for private as well as to be domestic in nature

and it also cannot be as such important prerequisite for sourcing of taxable earning.

Black trousers and shirt is essential to be worn at office for $145

Answer to Question 4:

Answer to part A:

Normally the capital gain tax relating to F1 takes place when an assesse allowed to

make a contract with some another party or expanding the contract, which was already owned

by such assesse13. Under the circumstances of F1 there is no 50% capital gains tax are

allowed even in case of the event F1 happen when the john enables his property as a

12 Long, Brendan, Jon Campbell, and Carolyn Kelshaw. "The justice lens on taxation policy in

Australia." St Mark's Review235 (2016): 94.

13 Campbell, Sam. "Personal liability of a trustee to tax on trust income: Part 1." Taxation in

Australia 53.5 (2018): 263.

In case of current situation of the expenditure that is connected to childcare of $80

which is paid by the taxpayer in case of remaining present in evening classes were not

connected for income related activities of the taxpayer.

Repair of fridge at home for approximately $250:

An individual who is a taxpayer is not permissible for claim of deduction under

“section 8-1(2) (b), ITAA 1997” such that the outgoings are not considerable for being

private and domestic in terms of nature. Under court held “Lunney v FCT (1958)” it is

necessary to analyse the loss and outgoings for being considerable as an important

prerequisite for sourcing of taxable returns. In the same way , repairs in terms of fringe at

home for near about $250 is not considerable for future deduction under “section 8-1(2)

(b),ITAA 1997” as expenses are considerable for private as well as to be domestic in nature

and it also cannot be as such important prerequisite for sourcing of taxable earning.

Black trousers and shirt is essential to be worn at office for $145

Answer to Question 4:

Answer to part A:

Normally the capital gain tax relating to F1 takes place when an assesse allowed to

make a contract with some another party or expanding the contract, which was already owned

by such assesse13. Under the circumstances of F1 there is no 50% capital gains tax are

allowed even in case of the event F1 happen when the john enables his property as a

12 Long, Brendan, Jon Campbell, and Carolyn Kelshaw. "The justice lens on taxation policy in

Australia." St Mark's Review235 (2016): 94.

13 Campbell, Sam. "Personal liability of a trustee to tax on trust income: Part 1." Taxation in

Australia 53.5 (2018): 263.

12TAXATION LAW

premium of $ 7,000 after the completion of seven years. As well as john cannot get 50%

capital gains tax discount from the capital gains tax F1 events.

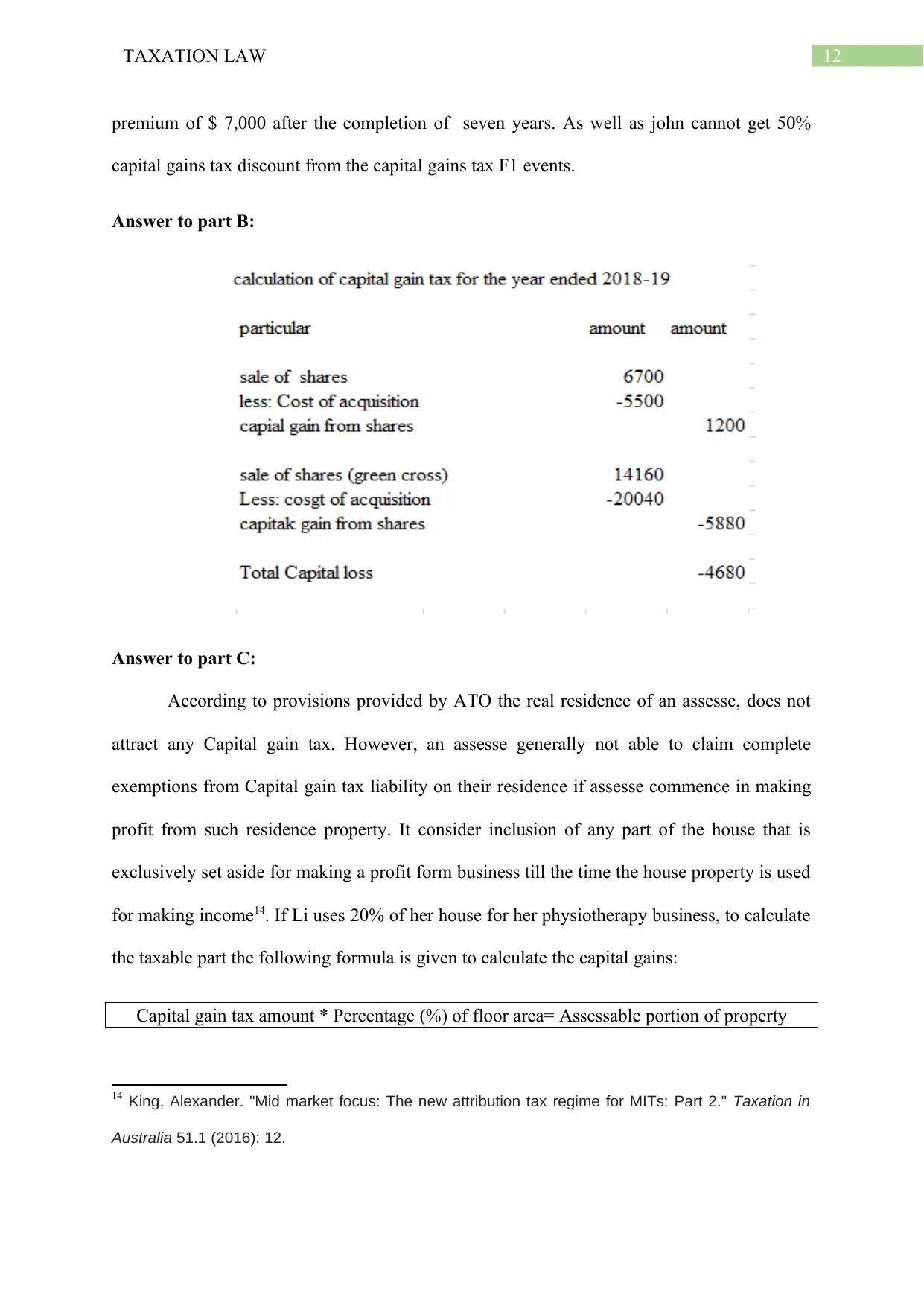

Answer to part B:

Answer to part C:

According to provisions provided by ATO the real residence of an assesse, does not

attract any Capital gain tax. However, an assesse generally not able to claim complete

exemptions from Capital gain tax liability on their residence if assesse commence in making

profit from such residence property. It consider inclusion of any part of the house that is

exclusively set aside for making a profit form business till the time the house property is used

for making income14. If Li uses 20% of her house for her physiotherapy business, to calculate

the taxable part the following formula is given to calculate the capital gains:

Capital gain tax amount * Percentage (%) of floor area= Assessable portion of property

14 King, Alexander. "Mid market focus: The new attribution tax regime for MITs: Part 2." Taxation in

Australia 51.1 (2016): 12.

premium of $ 7,000 after the completion of seven years. As well as john cannot get 50%

capital gains tax discount from the capital gains tax F1 events.

Answer to part B:

Answer to part C:

According to provisions provided by ATO the real residence of an assesse, does not

attract any Capital gain tax. However, an assesse generally not able to claim complete

exemptions from Capital gain tax liability on their residence if assesse commence in making

profit from such residence property. It consider inclusion of any part of the house that is

exclusively set aside for making a profit form business till the time the house property is used

for making income14. If Li uses 20% of her house for her physiotherapy business, to calculate

the taxable part the following formula is given to calculate the capital gains:

Capital gain tax amount * Percentage (%) of floor area= Assessable portion of property

14 King, Alexander. "Mid market focus: The new attribution tax regime for MITs: Part 2." Taxation in

Australia 51.1 (2016): 12.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

13TAXATION LAW

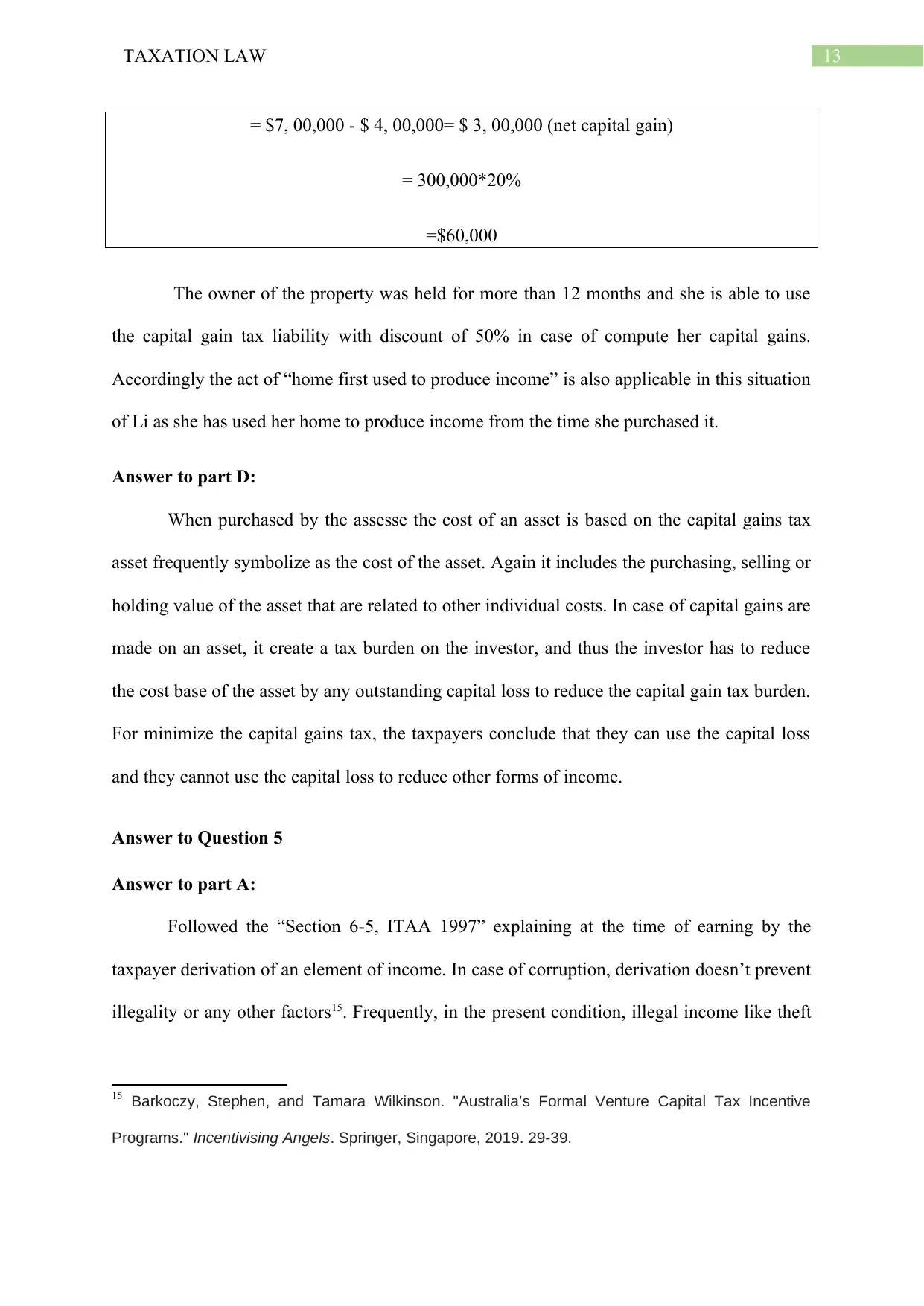

= $7, 00,000 - $ 4, 00,000= $ 3, 00,000 (net capital gain)

= 300,000*20%

=$60,000

The owner of the property was held for more than 12 months and she is able to use

the capital gain tax liability with discount of 50% in case of compute her capital gains.

Accordingly the act of “home first used to produce income” is also applicable in this situation

of Li as she has used her home to produce income from the time she purchased it.

Answer to part D:

When purchased by the assesse the cost of an asset is based on the capital gains tax

asset frequently symbolize as the cost of the asset. Again it includes the purchasing, selling or

holding value of the asset that are related to other individual costs. In case of capital gains are

made on an asset, it create a tax burden on the investor, and thus the investor has to reduce

the cost base of the asset by any outstanding capital loss to reduce the capital gain tax burden.

For minimize the capital gains tax, the taxpayers conclude that they can use the capital loss

and they cannot use the capital loss to reduce other forms of income.

Answer to Question 5

Answer to part A:

Followed the “Section 6-5, ITAA 1997” explaining at the time of earning by the

taxpayer derivation of an element of income. In case of corruption, derivation doesn’t prevent

illegality or any other factors15. Frequently, in the present condition, illegal income like theft

15 Barkoczy, Stephen, and Tamara Wilkinson. "Australia’s Formal Venture Capital Tax Incentive

Programs." Incentivising Angels. Springer, Singapore, 2019. 29-39.

= $7, 00,000 - $ 4, 00,000= $ 3, 00,000 (net capital gain)

= 300,000*20%

=$60,000

The owner of the property was held for more than 12 months and she is able to use

the capital gain tax liability with discount of 50% in case of compute her capital gains.

Accordingly the act of “home first used to produce income” is also applicable in this situation

of Li as she has used her home to produce income from the time she purchased it.

Answer to part D:

When purchased by the assesse the cost of an asset is based on the capital gains tax

asset frequently symbolize as the cost of the asset. Again it includes the purchasing, selling or

holding value of the asset that are related to other individual costs. In case of capital gains are

made on an asset, it create a tax burden on the investor, and thus the investor has to reduce

the cost base of the asset by any outstanding capital loss to reduce the capital gain tax burden.

For minimize the capital gains tax, the taxpayers conclude that they can use the capital loss

and they cannot use the capital loss to reduce other forms of income.

Answer to Question 5

Answer to part A:

Followed the “Section 6-5, ITAA 1997” explaining at the time of earning by the

taxpayer derivation of an element of income. In case of corruption, derivation doesn’t prevent

illegality or any other factors15. Frequently, in the present condition, illegal income like theft

15 Barkoczy, Stephen, and Tamara Wilkinson. "Australia’s Formal Venture Capital Tax Incentive

Programs." Incentivising Angels. Springer, Singapore, 2019. 29-39.

14TAXATION LAW

or drug-dealing would be consider as the income that is taxable as per “Section 6-5, ITAA

1997” under general meaning.

Answer to part B:

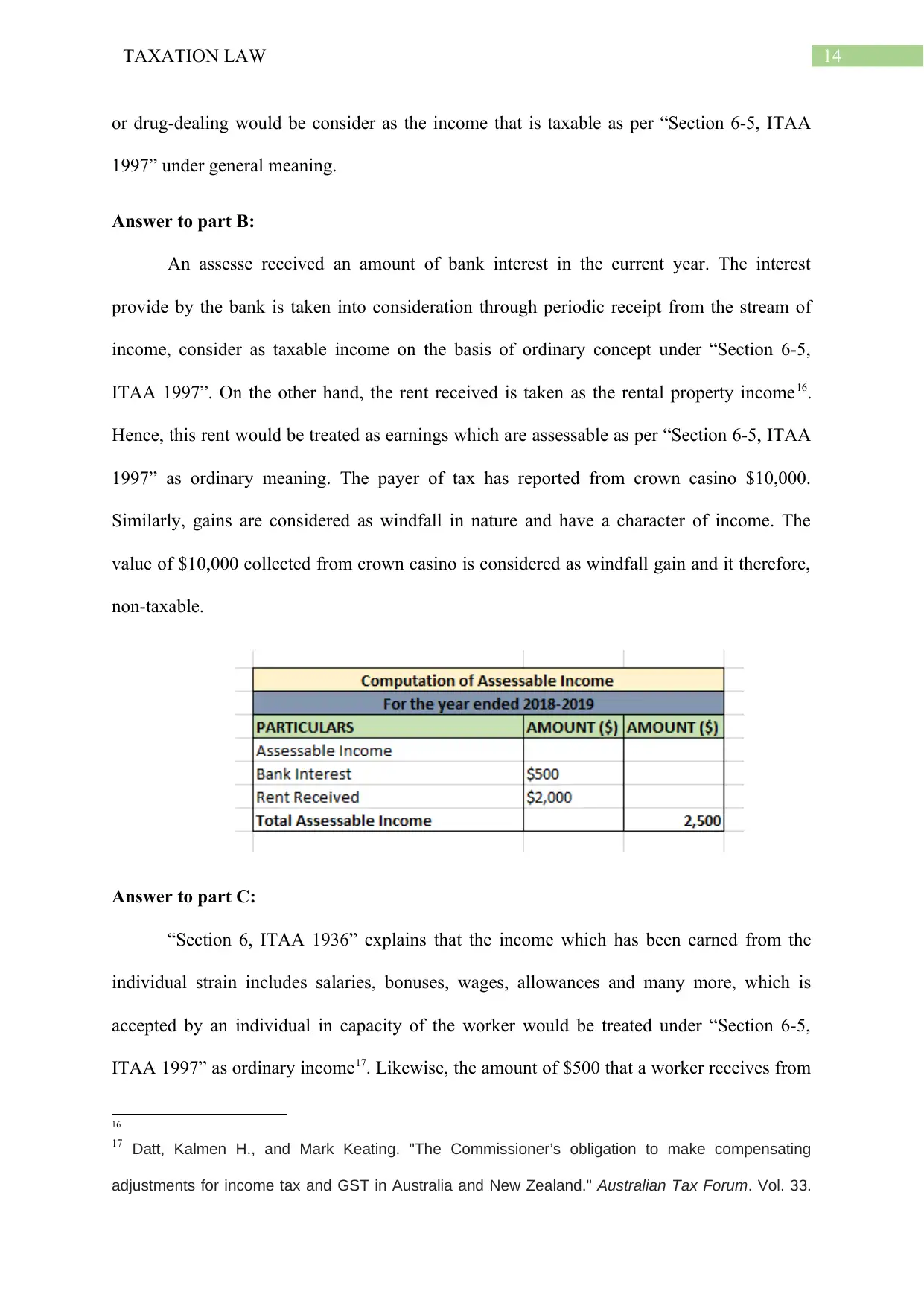

An assesse received an amount of bank interest in the current year. The interest

provide by the bank is taken into consideration through periodic receipt from the stream of

income, consider as taxable income on the basis of ordinary concept under “Section 6-5,

ITAA 1997”. On the other hand, the rent received is taken as the rental property income16.

Hence, this rent would be treated as earnings which are assessable as per “Section 6-5, ITAA

1997” as ordinary meaning. The payer of tax has reported from crown casino $10,000.

Similarly, gains are considered as windfall in nature and have a character of income. The

value of $10,000 collected from crown casino is considered as windfall gain and it therefore,

non-taxable.

Answer to part C:

“Section 6, ITAA 1936” explains that the income which has been earned from the

individual strain includes salaries, bonuses, wages, allowances and many more, which is

accepted by an individual in capacity of the worker would be treated under “Section 6-5,

ITAA 1997” as ordinary income17. Likewise, the amount of $500 that a worker receives from

16

17 Datt, Kalmen H., and Mark Keating. "The Commissioner’s obligation to make compensating

adjustments for income tax and GST in Australia and New Zealand." Australian Tax Forum. Vol. 33.

or drug-dealing would be consider as the income that is taxable as per “Section 6-5, ITAA

1997” under general meaning.

Answer to part B:

An assesse received an amount of bank interest in the current year. The interest

provide by the bank is taken into consideration through periodic receipt from the stream of

income, consider as taxable income on the basis of ordinary concept under “Section 6-5,

ITAA 1997”. On the other hand, the rent received is taken as the rental property income16.

Hence, this rent would be treated as earnings which are assessable as per “Section 6-5, ITAA

1997” as ordinary meaning. The payer of tax has reported from crown casino $10,000.

Similarly, gains are considered as windfall in nature and have a character of income. The

value of $10,000 collected from crown casino is considered as windfall gain and it therefore,

non-taxable.

Answer to part C:

“Section 6, ITAA 1936” explains that the income which has been earned from the

individual strain includes salaries, bonuses, wages, allowances and many more, which is

accepted by an individual in capacity of the worker would be treated under “Section 6-5,

ITAA 1997” as ordinary income17. Likewise, the amount of $500 that a worker receives from

16

17 Datt, Kalmen H., and Mark Keating. "The Commissioner’s obligation to make compensating

adjustments for income tax and GST in Australia and New Zealand." Australian Tax Forum. Vol. 33.

15TAXATION LAW

his employee would be treated as income from individual strain. Hence, it would be taxable

under “Section 6-5, ITAA 1997”.

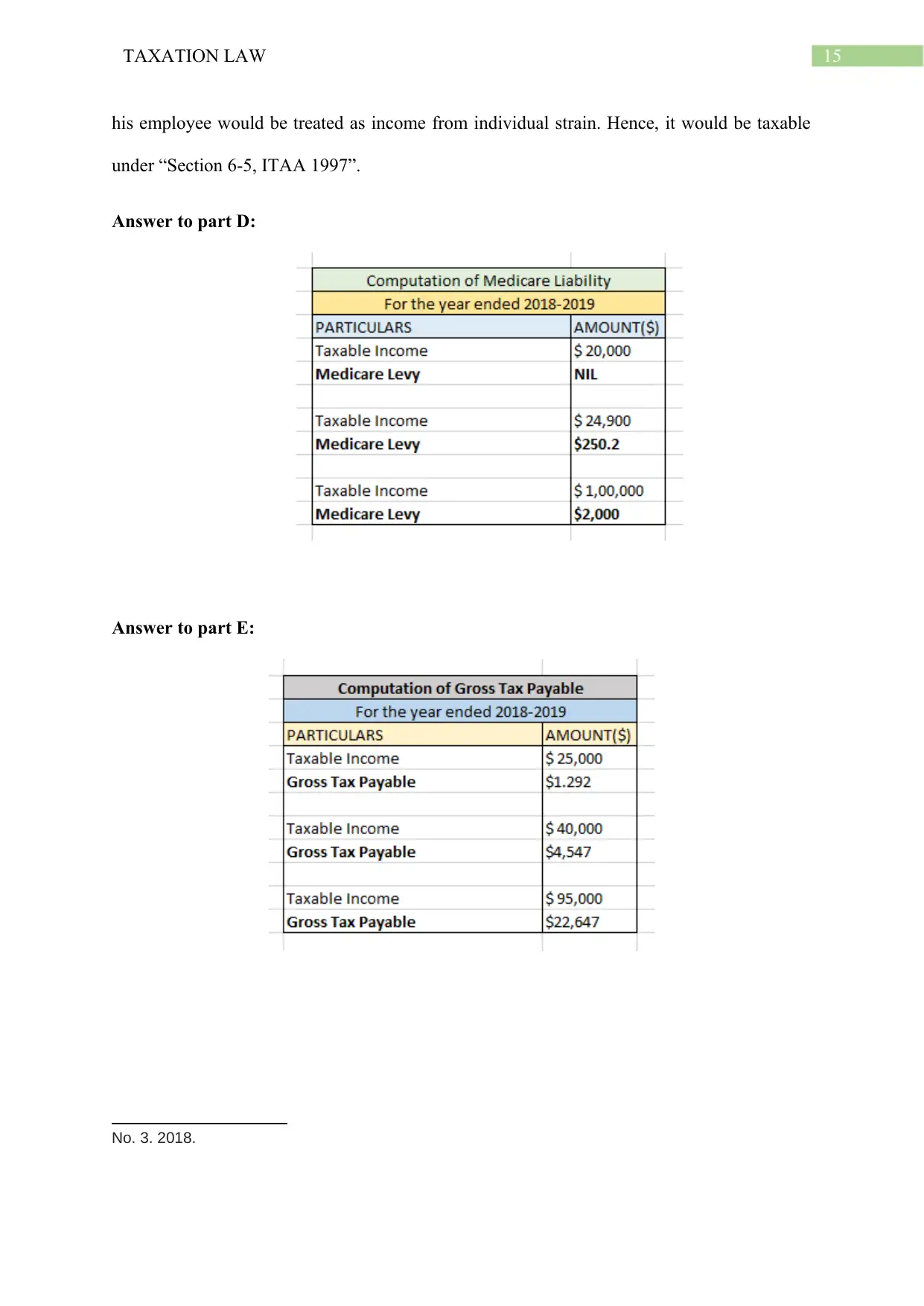

Answer to part D:

Answer to part E:

No. 3. 2018.

his employee would be treated as income from individual strain. Hence, it would be taxable

under “Section 6-5, ITAA 1997”.

Answer to part D:

Answer to part E:

No. 3. 2018.

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

16TAXATION LAW

References:

Barkoczy, Stephen, and Tamara Wilkinson. "Australia’s Formal Venture Capital Tax

Incentive Programs." Incentivising Angels. Springer, Singapore, 2019. 29-39.

Barkoczy, Stephen, and Tamara Wilkinson. "Australia’s Formal Venture Capital Tax

Incentive Programs." Incentivising Angels. Springer, Singapore, 2019. 29-39.

Campbell, Sam. "Personal liability of a trustee to tax on trust income: Part 1." Taxation in

Australia 53.5 (2018): 263.

Castelyn, Donovan, Helen Hodgson, and Lisa Marriott. "Income equalisation: is all fair in

primary production and tax law?." Australian Tax Forum. Vol. 34. No. 2. 2019.

Chardon, Toni, Brett Freudenberg, and Mark Brimble. "Tax literacy in Australia: not

knowing your deduction from your offset." Austl. Tax F. 31 (2016): 321.

Datt, Kalmen H., and Mark Keating. "The Commissioner’s obligation to make compensating

adjustments for income tax and GST in Australia and New Zealand." Australian Tax Forum.

Vol. 33. No. 3. 2018.

Evans, Chris, John Minas, and Youngdeok Lim. "Taxing personal capital gains in Australia:

An alternative way forward." Austl. Tax F. 30 (2015): 735.

Idris, Nuhu Musa. "Some comparisons between the Nigerian and South African fiscal

regimes regarding an individual’s tax residence." Obiter 39.1 (2018): 76-84.

Jones, Daryl. "Complexity of tax residency attracts review." Taxation in Australia 53.6

(2018): 296.

Kenny, Paul. "Small business capital allowances." (2018).

References:

Barkoczy, Stephen, and Tamara Wilkinson. "Australia’s Formal Venture Capital Tax

Incentive Programs." Incentivising Angels. Springer, Singapore, 2019. 29-39.

Barkoczy, Stephen, and Tamara Wilkinson. "Australia’s Formal Venture Capital Tax

Incentive Programs." Incentivising Angels. Springer, Singapore, 2019. 29-39.

Campbell, Sam. "Personal liability of a trustee to tax on trust income: Part 1." Taxation in

Australia 53.5 (2018): 263.

Castelyn, Donovan, Helen Hodgson, and Lisa Marriott. "Income equalisation: is all fair in

primary production and tax law?." Australian Tax Forum. Vol. 34. No. 2. 2019.

Chardon, Toni, Brett Freudenberg, and Mark Brimble. "Tax literacy in Australia: not

knowing your deduction from your offset." Austl. Tax F. 31 (2016): 321.

Datt, Kalmen H., and Mark Keating. "The Commissioner’s obligation to make compensating

adjustments for income tax and GST in Australia and New Zealand." Australian Tax Forum.

Vol. 33. No. 3. 2018.

Evans, Chris, John Minas, and Youngdeok Lim. "Taxing personal capital gains in Australia:

An alternative way forward." Austl. Tax F. 30 (2015): 735.

Idris, Nuhu Musa. "Some comparisons between the Nigerian and South African fiscal

regimes regarding an individual’s tax residence." Obiter 39.1 (2018): 76-84.

Jones, Daryl. "Complexity of tax residency attracts review." Taxation in Australia 53.6

(2018): 296.

Kenny, Paul. "Small business capital allowances." (2018).

17TAXATION LAW

King, Alexander. "Mid market focus: The new attribution tax regime for MITs: Part

2." Taxation in Australia 51.1 (2016): 12.

Lee, Joanne. "The Effectiveness of Part IVA of the Income Tax Assessment Act 1936 (CTH):

Time for a Not Merely Incidental'Purpose Test." J. Austl. Tax'n 20 (2018): 1.

Long, Brendan, Jon Campbell, and Carolyn Kelshaw. "The justice lens on taxation policy in

Australia." St Mark's Review235 (2016): 94.

Norbury, Michael. "Mr Harding's residence reconsidered." Taxation in Australia 53.9 (2019):

497.

King, Alexander. "Mid market focus: The new attribution tax regime for MITs: Part

2." Taxation in Australia 51.1 (2016): 12.

Lee, Joanne. "The Effectiveness of Part IVA of the Income Tax Assessment Act 1936 (CTH):

Time for a Not Merely Incidental'Purpose Test." J. Austl. Tax'n 20 (2018): 1.

Long, Brendan, Jon Campbell, and Carolyn Kelshaw. "The justice lens on taxation policy in

Australia." St Mark's Review235 (2016): 94.

Norbury, Michael. "Mr Harding's residence reconsidered." Taxation in Australia 53.9 (2019):

497.

1 out of 18

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

© 2024 | Zucol Services PVT LTD | All rights reserved.