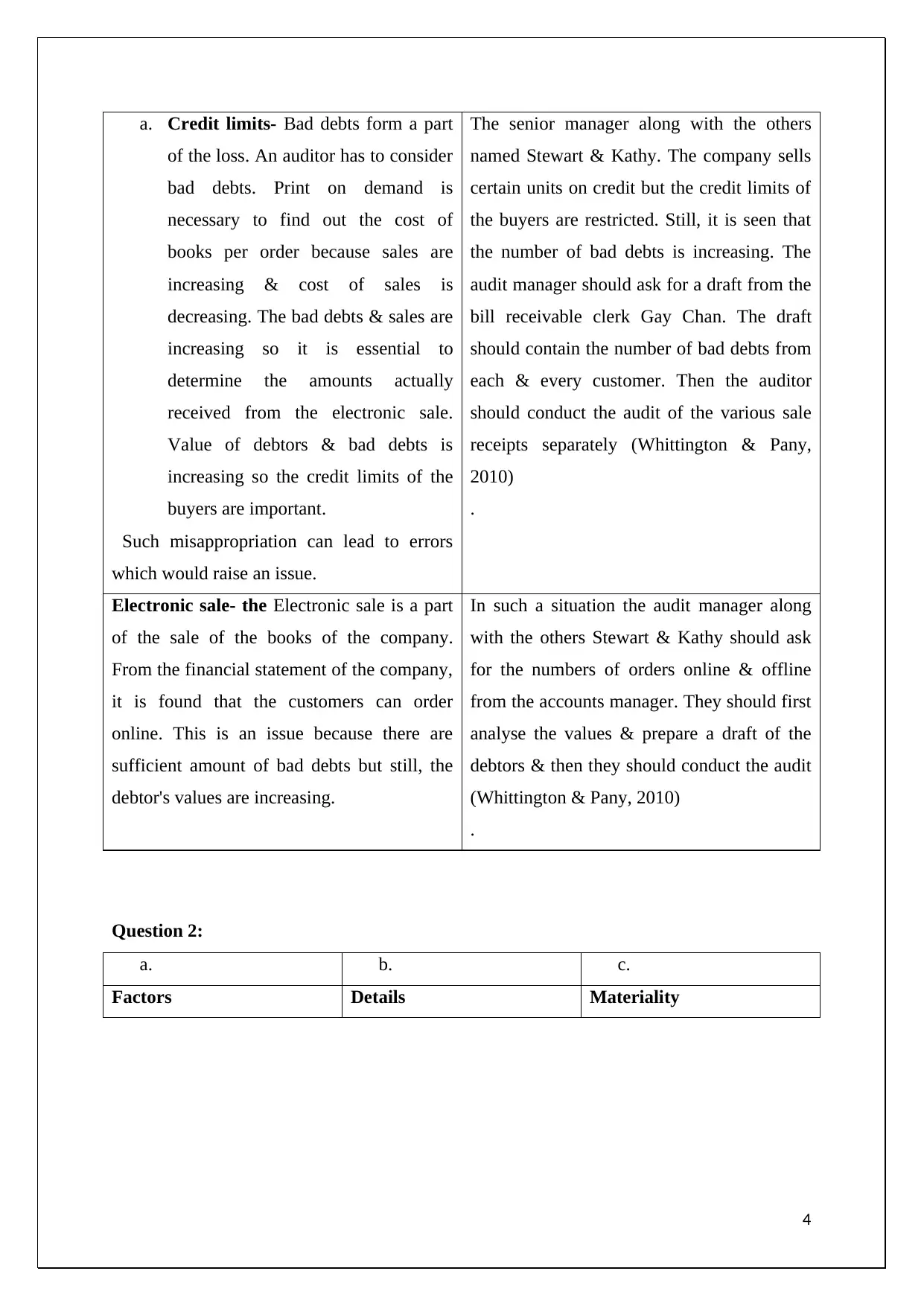

The assignment content discusses the factors that affect the preliminary figure for materiality in the context of Double Ink Printers Ltd (DIPL) company. The three main factors identified are accounting factors, operational factors, and technological factors. Accounting factors include proper treatment of revenues and expenses to avoid errors in audit results. Operational factors refer to the business policies and methods adopted by DIPL, such as print-on-demand, which can affect the financial statements and audit results. Technological factors involve the adoption of new and better methods of accounting and auditing, which can provide accurate material evidence without loopholes.

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)