AUDIT ASSURANCE & COMPLIANCE Table of contents Question 1: Necesary Issue Audit-related decision towards the useful life of the assets

13 Pages2736 Words256 Views

Added on 2019-09-26

About This Document

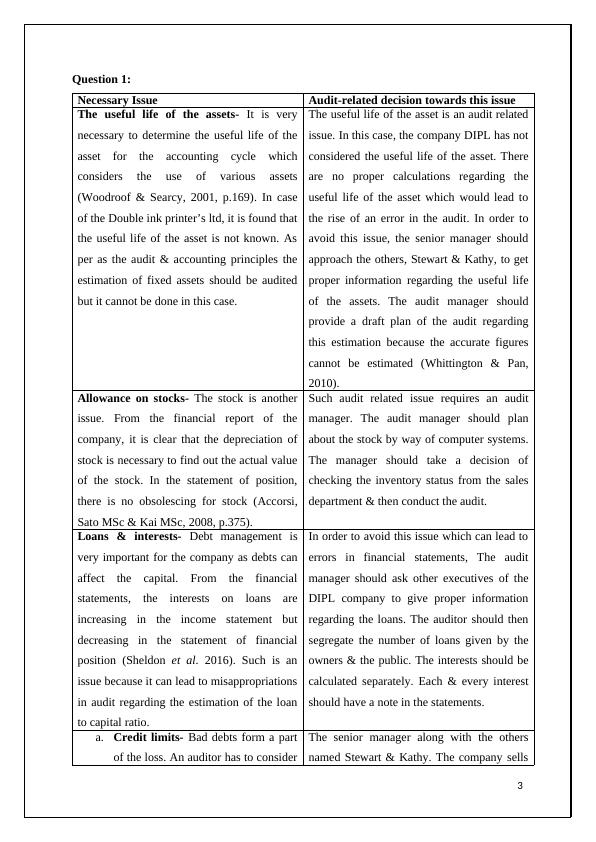

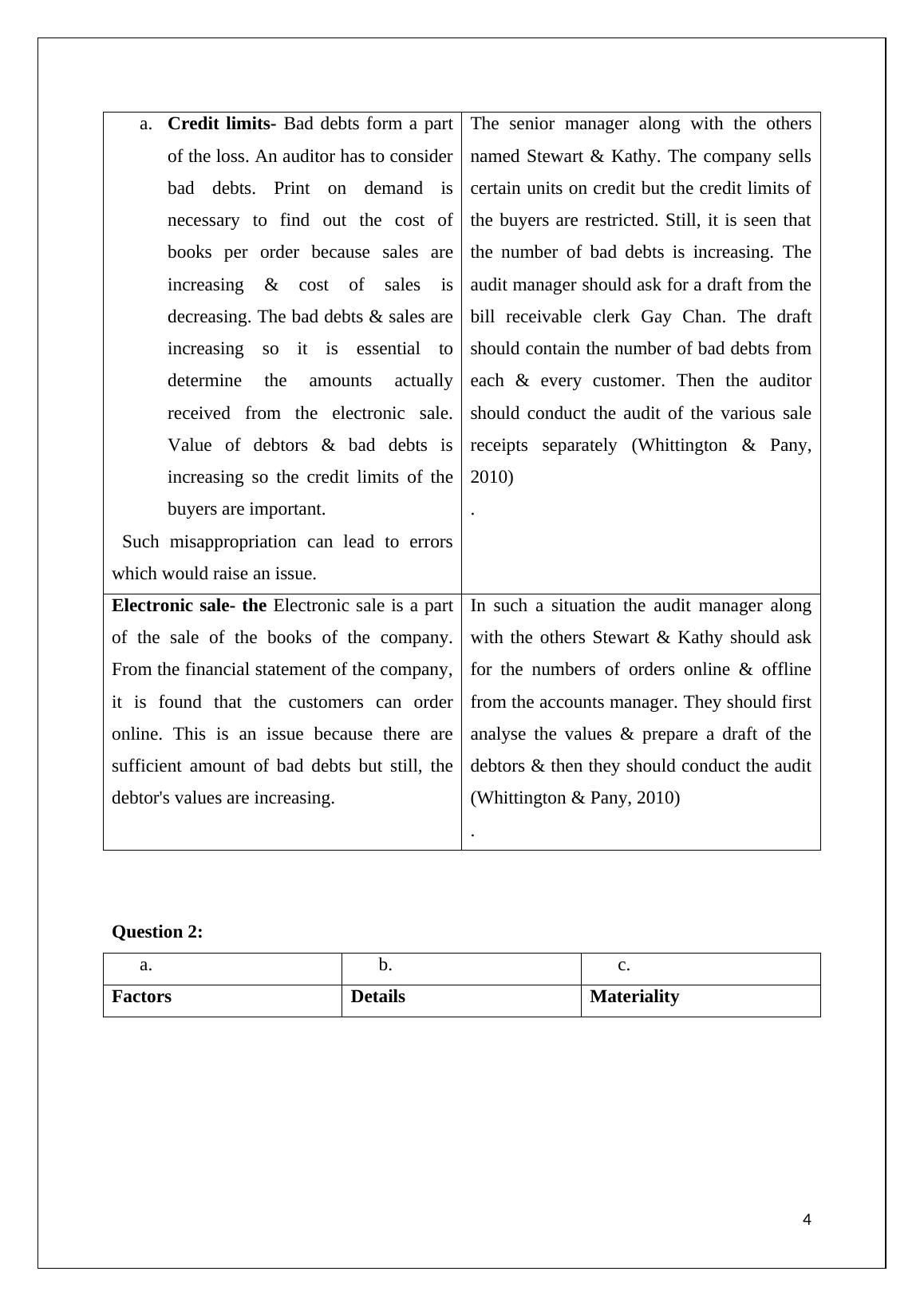

AUDIT ASSURANCE & COMPLIANCE Table of contents Question 1: 3 Question 2: 4 Reference list 9 Question 1: Necessary Issue Details Audit-related decision towards this issue The useful life of the assets- It is very necessary to determine the useful life of the asset for the accounting cycle which considers the use of various assets (Woodroof & Searcy, 2001, p.169). In order to avoid this issue, the senior manager should approach the others, Stewart & Kathy, to get proper

AUDIT ASSURANCE & COMPLIANCE Table of contents Question 1: Necesary Issue Audit-related decision towards the useful life of the assets

Added on 2019-09-26

ShareRelated Documents

End of preview

Want to access all the pages? Upload your documents or become a member.

Audit Assurance & Compliance: Issues and Factors

|13

|2736

|303

Assignment on Audit, Assurance and Compliance

|4

|498

|270

HI6026 Report | Audit, Assurance and Compliance

|9

|2366

|148

HI6026 | Audit and Assurance

|11

|2655

|53

HI6026 - Audit, Assurance and Compliance, Preliminary Analytical

|8

|2059

|214

HI6026 Audit, Assurance and Compliance Trimester 2

|9

|2209

|131