Australian Dairy Industry Analysis

VerifiedAdded on 2020/03/01

|20

|3321

|40

AI Summary

The assignment requires an analysis of the Australian dairy industry, taking into account its social, economic, and environmental impacts. Students are to utilize provided research articles focusing on various aspects of the industry including sustainability, deregulation, innovation, farm management practices, and gender dynamics within the sector. The analysis should draw upon these sources to provide a comprehensive understanding of the current state and challenges facing the Australian dairy industry.

Contribute Materials

Your contribution can guide someone’s learning journey. Share your

documents today.

Running head: THE AUSTRALIAN DAIRY INDUSTRY

Australian Dairy Industry analysis

Name of the Student:

Name of the University:

Author note:

Australian Dairy Industry analysis

Name of the Student:

Name of the University:

Author note:

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

1

THE AUSTRALIAN DAIRY INDUSTRY

Executive summary

The text in the report analyses the charts that are gathered on Australian Dairy Industry. The

internal and external factors that affects the industry. The global position of the industry and

what are the strategic and innovative steps that they have taken to remain one of the largest

competitors in the world.

THE AUSTRALIAN DAIRY INDUSTRY

Executive summary

The text in the report analyses the charts that are gathered on Australian Dairy Industry. The

internal and external factors that affects the industry. The global position of the industry and

what are the strategic and innovative steps that they have taken to remain one of the largest

competitors in the world.

2

THE AUSTRALIAN DAIRY INDUSTRY

Table of Contents

Introduction......................................................................................................................................4

Domestic market..............................................................................................................................4

International market.........................................................................................................................5

International trade scenario..............................................................................................................6

Export share of trade........................................................................................................................7

Milk and it’s derivative products life cycle.....................................................................................8

Australia export by region...............................................................................................................9

Industry analysis............................................................................................................................10

Internal value chain analysis.........................................................................................................11

Industry structure and regional strength........................................................................................12

External..........................................................................................................................................13

Issues and challenges faced by the industry in global competition...............................................13

Strengths and weakness Opportunities and threats of the industry...............................................13

Strategic analysis...........................................................................................................................15

Porter’s values chain analysis........................................................................................................15

Conclusion.....................................................................................................................................16

Reference.......................................................................................................................................17

THE AUSTRALIAN DAIRY INDUSTRY

Table of Contents

Introduction......................................................................................................................................4

Domestic market..............................................................................................................................4

International market.........................................................................................................................5

International trade scenario..............................................................................................................6

Export share of trade........................................................................................................................7

Milk and it’s derivative products life cycle.....................................................................................8

Australia export by region...............................................................................................................9

Industry analysis............................................................................................................................10

Internal value chain analysis.........................................................................................................11

Industry structure and regional strength........................................................................................12

External..........................................................................................................................................13

Issues and challenges faced by the industry in global competition...............................................13

Strengths and weakness Opportunities and threats of the industry...............................................13

Strategic analysis...........................................................................................................................15

Porter’s values chain analysis........................................................................................................15

Conclusion.....................................................................................................................................16

Reference.......................................................................................................................................17

3

THE AUSTRALIAN DAIRY INDUSTRY

THE AUSTRALIAN DAIRY INDUSTRY

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

4

THE AUSTRALIAN DAIRY INDUSTRY

Introduction

Australian industry is one of the most agriculture intensive industries comparing with the

global agriculture market. Victoria is dominant in dairy and herd production. The evolution o f

technology has served them well and their productivity has increased since last three decades

(Klerkx and Nettle, 2013). The small farmers were able to generate the derivative products of

milk and supported to the revenue that every individual state made in the following years.

According to the dairy situation and outlook report on 2017 the farmers have produced 700

million fewer litters of milk due to a huge crisis that have hit the whole Australia in the last year

(Sorensen, 2011). However, the consumption of the branded products has not lessened. Victoria

being the centre of production has seen 9% growth in the full cream milk production (Klerkx and

Nettle, 2013). Whereas Australia accounts for an approximate 2% of the world’s milk

production, it is a noteworthy exporter of dairy merchandise (Regulations, 2013). The Australian

dairy industry was significantly challenged by deregulation, droughts and the financial crisis.

However, the industry has also been seen to to adapt to difficult situations through sharing its

view of the challenges and opportunities and with collective action. One crucial feature for their

success now would be the policy control of the environmental factors, which is an important role

in accordance with the industry to adapt in the future and further develop.

Domestic market

The Australian Dairy industry is a fully established industry and some subtropical areas

of Australia is also rich in giving supply to its customers. Even though most of the country’s

milk production takes place in south‐east seaboard parts states, all states have separate dairy

farms that supply fresh drinking milk to close by cities and towns.

THE AUSTRALIAN DAIRY INDUSTRY

Introduction

Australian industry is one of the most agriculture intensive industries comparing with the

global agriculture market. Victoria is dominant in dairy and herd production. The evolution o f

technology has served them well and their productivity has increased since last three decades

(Klerkx and Nettle, 2013). The small farmers were able to generate the derivative products of

milk and supported to the revenue that every individual state made in the following years.

According to the dairy situation and outlook report on 2017 the farmers have produced 700

million fewer litters of milk due to a huge crisis that have hit the whole Australia in the last year

(Sorensen, 2011). However, the consumption of the branded products has not lessened. Victoria

being the centre of production has seen 9% growth in the full cream milk production (Klerkx and

Nettle, 2013). Whereas Australia accounts for an approximate 2% of the world’s milk

production, it is a noteworthy exporter of dairy merchandise (Regulations, 2013). The Australian

dairy industry was significantly challenged by deregulation, droughts and the financial crisis.

However, the industry has also been seen to to adapt to difficult situations through sharing its

view of the challenges and opportunities and with collective action. One crucial feature for their

success now would be the policy control of the environmental factors, which is an important role

in accordance with the industry to adapt in the future and further develop.

Domestic market

The Australian Dairy industry is a fully established industry and some subtropical areas

of Australia is also rich in giving supply to its customers. Even though most of the country’s

milk production takes place in south‐east seaboard parts states, all states have separate dairy

farms that supply fresh drinking milk to close by cities and towns.

5

THE AUSTRALIAN DAIRY INDUSTRY

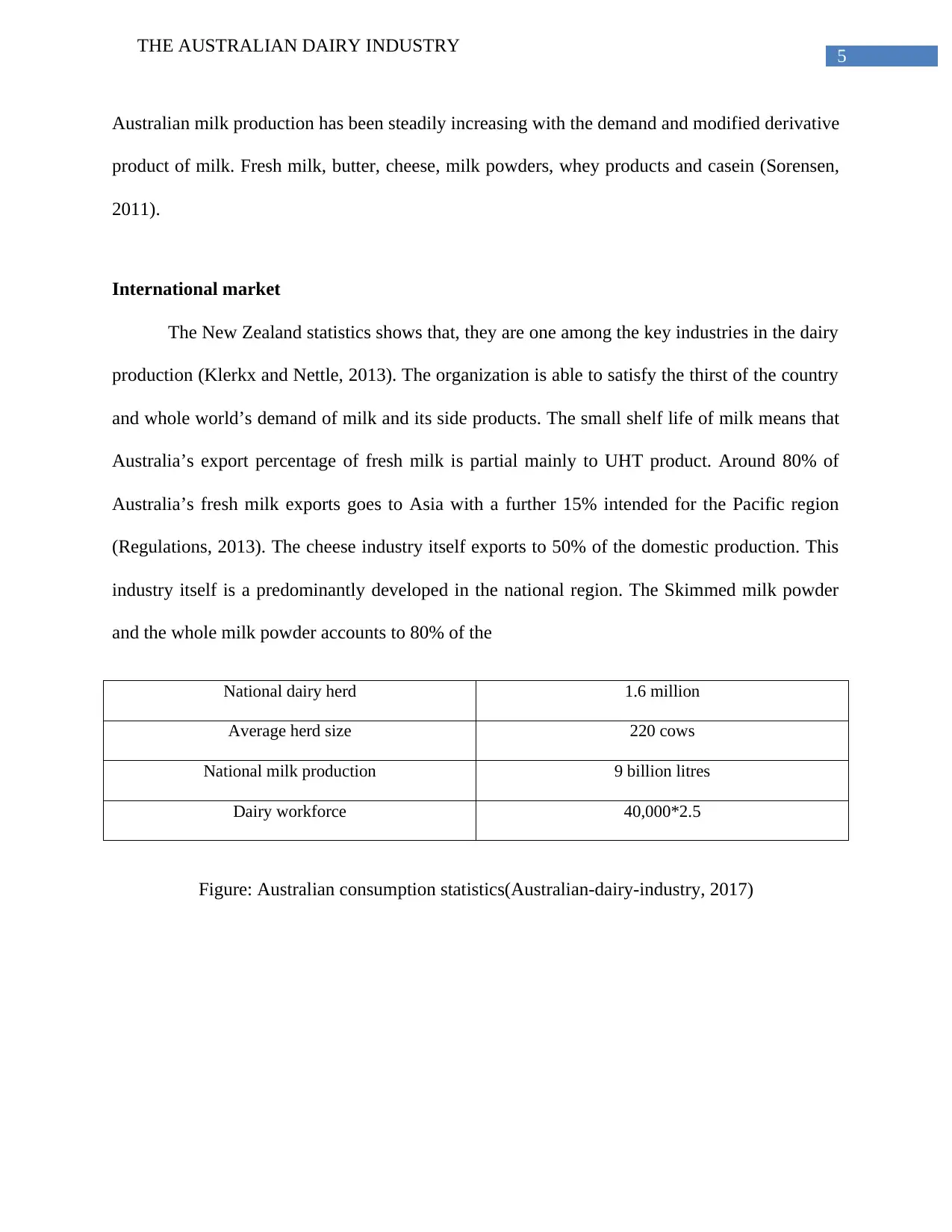

Australian milk production has been steadily increasing with the demand and modified derivative

product of milk. Fresh milk, butter, cheese, milk powders, whey products and casein (Sorensen,

2011).

International market

The New Zealand statistics shows that, they are one among the key industries in the dairy

production (Klerkx and Nettle, 2013). The organization is able to satisfy the thirst of the country

and whole world’s demand of milk and its side products. The small shelf life of milk means that

Australia’s export percentage of fresh milk is partial mainly to UHT product. Around 80% of

Australia’s fresh milk exports goes to Asia with a further 15% intended for the Pacific region

(Regulations, 2013). The cheese industry itself exports to 50% of the domestic production. This

industry itself is a predominantly developed in the national region. The Skimmed milk powder

and the whole milk powder accounts to 80% of the

National dairy herd 1.6 million

Average herd size 220 cows

National milk production 9 billion litres

Dairy workforce 40,000*2.5

Figure: Australian consumption statistics(Australian-dairy-industry, 2017)

THE AUSTRALIAN DAIRY INDUSTRY

Australian milk production has been steadily increasing with the demand and modified derivative

product of milk. Fresh milk, butter, cheese, milk powders, whey products and casein (Sorensen,

2011).

International market

The New Zealand statistics shows that, they are one among the key industries in the dairy

production (Klerkx and Nettle, 2013). The organization is able to satisfy the thirst of the country

and whole world’s demand of milk and its side products. The small shelf life of milk means that

Australia’s export percentage of fresh milk is partial mainly to UHT product. Around 80% of

Australia’s fresh milk exports goes to Asia with a further 15% intended for the Pacific region

(Regulations, 2013). The cheese industry itself exports to 50% of the domestic production. This

industry itself is a predominantly developed in the national region. The Skimmed milk powder

and the whole milk powder accounts to 80% of the

National dairy herd 1.6 million

Average herd size 220 cows

National milk production 9 billion litres

Dairy workforce 40,000*2.5

Figure: Australian consumption statistics(Australian-dairy-industry, 2017)

6

THE AUSTRALIAN DAIRY INDUSTRY

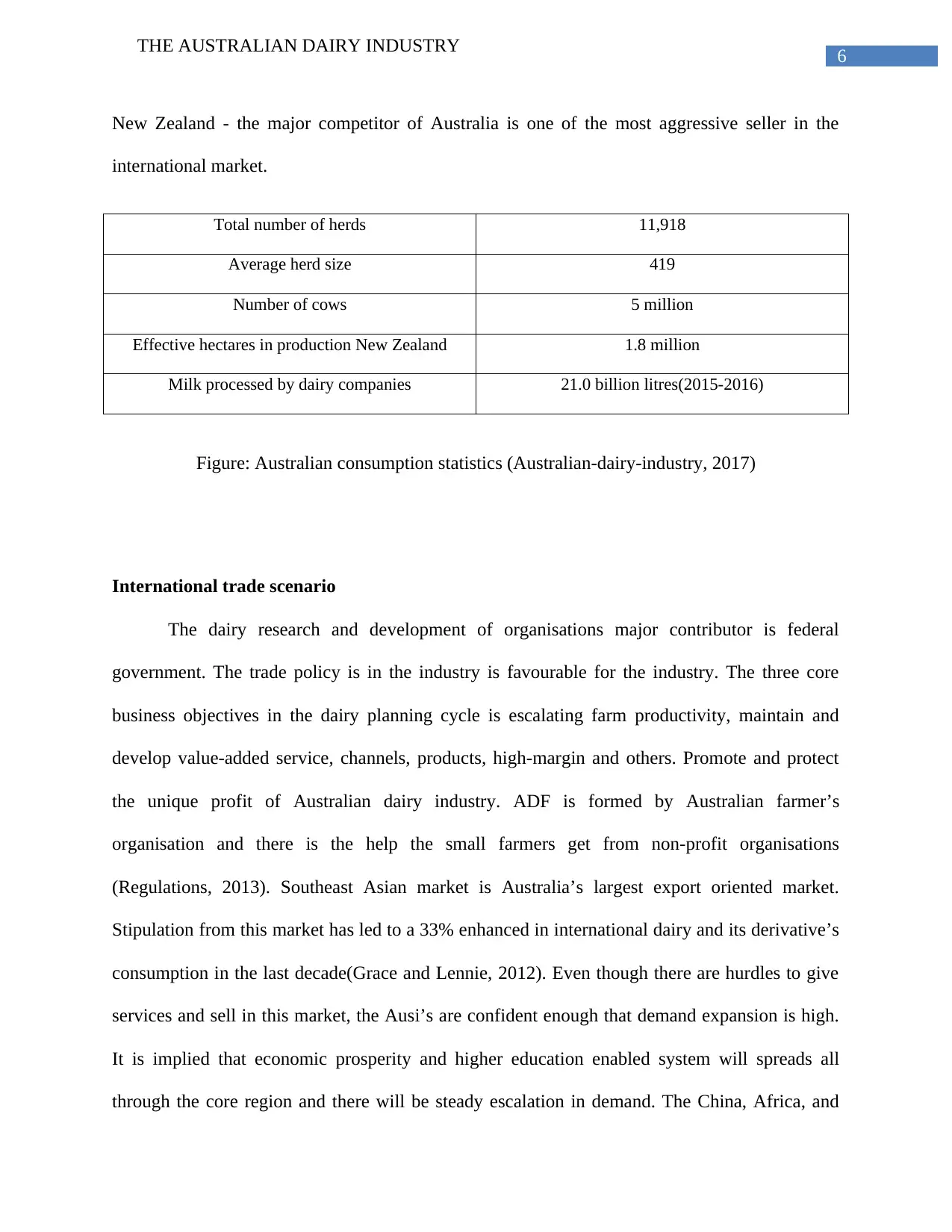

New Zealand - the major competitor of Australia is one of the most aggressive seller in the

international market.

Total number of herds 11,918

Average herd size 419

Number of cows 5 million

Effective hectares in production New Zealand 1.8 million

Milk processed by dairy companies 21.0 billion litres(2015-2016)

Figure: Australian consumption statistics (Australian-dairy-industry, 2017)

International trade scenario

The dairy research and development of organisations major contributor is federal

government. The trade policy is in the industry is favourable for the industry. The three core

business objectives in the dairy planning cycle is escalating farm productivity, maintain and

develop value-added service, channels, products, high-margin and others. Promote and protect

the unique profit of Australian dairy industry. ADF is formed by Australian farmer’s

organisation and there is the help the small farmers get from non-profit organisations

(Regulations, 2013). Southeast Asian market is Australia’s largest export oriented market.

Stipulation from this market has led to a 33% enhanced in international dairy and its derivative’s

consumption in the last decade(Grace and Lennie, 2012). Even though there are hurdles to give

services and sell in this market, the Ausi’s are confident enough that demand expansion is high.

It is implied that economic prosperity and higher education enabled system will spreads all

through the core region and there will be steady escalation in demand. The China, Africa, and

THE AUSTRALIAN DAIRY INDUSTRY

New Zealand - the major competitor of Australia is one of the most aggressive seller in the

international market.

Total number of herds 11,918

Average herd size 419

Number of cows 5 million

Effective hectares in production New Zealand 1.8 million

Milk processed by dairy companies 21.0 billion litres(2015-2016)

Figure: Australian consumption statistics (Australian-dairy-industry, 2017)

International trade scenario

The dairy research and development of organisations major contributor is federal

government. The trade policy is in the industry is favourable for the industry. The three core

business objectives in the dairy planning cycle is escalating farm productivity, maintain and

develop value-added service, channels, products, high-margin and others. Promote and protect

the unique profit of Australian dairy industry. ADF is formed by Australian farmer’s

organisation and there is the help the small farmers get from non-profit organisations

(Regulations, 2013). Southeast Asian market is Australia’s largest export oriented market.

Stipulation from this market has led to a 33% enhanced in international dairy and its derivative’s

consumption in the last decade(Grace and Lennie, 2012). Even though there are hurdles to give

services and sell in this market, the Ausi’s are confident enough that demand expansion is high.

It is implied that economic prosperity and higher education enabled system will spreads all

through the core region and there will be steady escalation in demand. The China, Africa, and

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

7

THE AUSTRALIAN DAIRY INDUSTRY

Middle East are the one among the major exporters of the dairy products and consume the major

percentage of the products (Grace and Lennie, 2012).

The Australian market has strength in the domestic market and furthermore, they are

milk’s multinational value increment (Sorensen, 2011). The derivatives of the main product are

also capturing the completely international market competing with the value-addition and

prospective consumption market percentage (Nettle, Paine and Penry, 2010).

However, the trade regulations of the industry have to face some highly contingency

factors. This includes the China and Middle East’s production and expansion in the regarding

instruction (Nettle, Paine and Penry, 2010). The Neighbouring countries production and their

strong economic condition can be highly competitive in the recent years inferred from the above

table. European’s balance and protectionist has long since given headache to the trade enablers in

the international market. Their products are facing headed competition with the former dairy

market leaders (Grace and Lennie, 2012). The prices of the products are also volatile because of

dynamic supply-demand ration working in the industry.

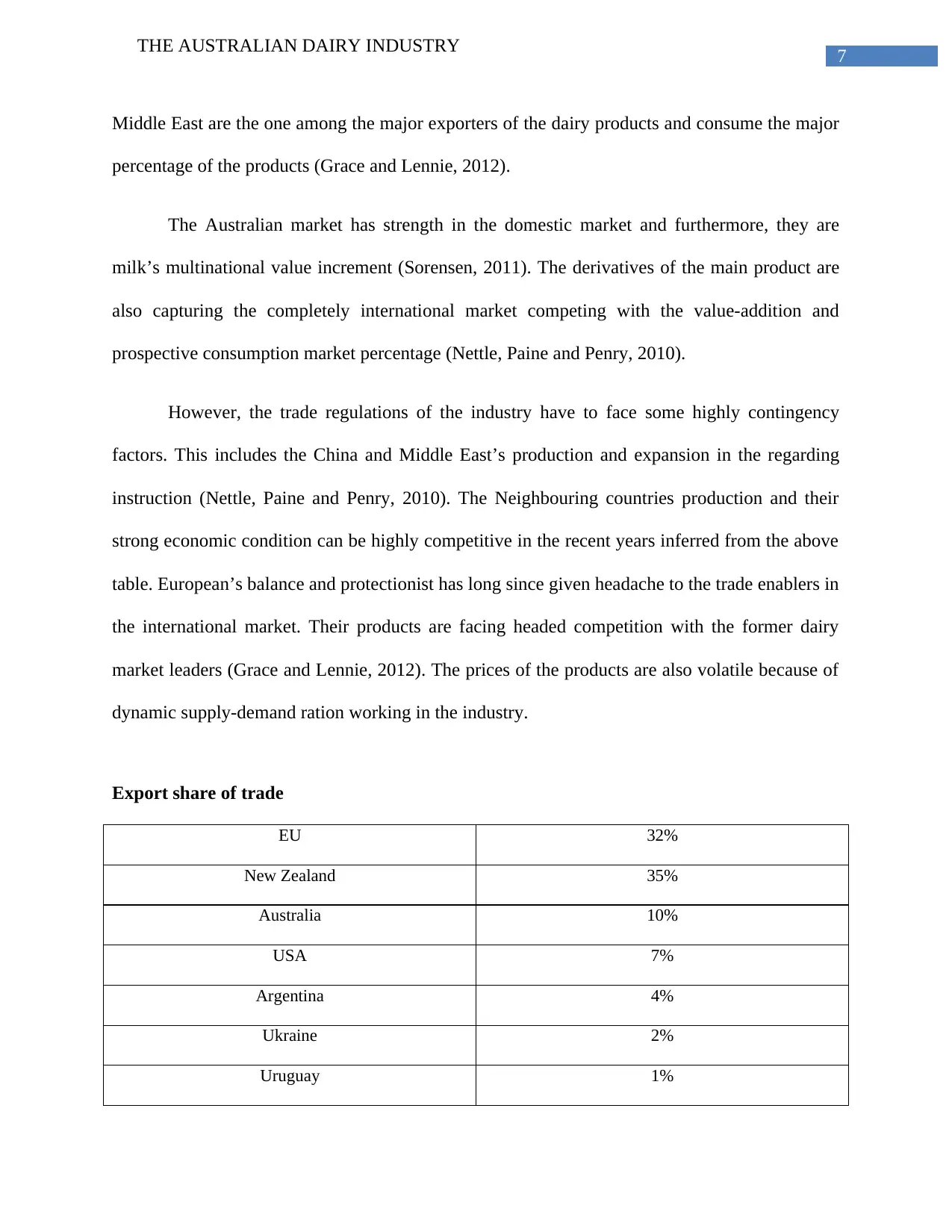

Export share of trade

EU 32%

New Zealand 35%

Australia 10%

USA 7%

Argentina 4%

Ukraine 2%

Uruguay 1%

THE AUSTRALIAN DAIRY INDUSTRY

Middle East are the one among the major exporters of the dairy products and consume the major

percentage of the products (Grace and Lennie, 2012).

The Australian market has strength in the domestic market and furthermore, they are

milk’s multinational value increment (Sorensen, 2011). The derivatives of the main product are

also capturing the completely international market competing with the value-addition and

prospective consumption market percentage (Nettle, Paine and Penry, 2010).

However, the trade regulations of the industry have to face some highly contingency

factors. This includes the China and Middle East’s production and expansion in the regarding

instruction (Nettle, Paine and Penry, 2010). The Neighbouring countries production and their

strong economic condition can be highly competitive in the recent years inferred from the above

table. European’s balance and protectionist has long since given headache to the trade enablers in

the international market. Their products are facing headed competition with the former dairy

market leaders (Grace and Lennie, 2012). The prices of the products are also volatile because of

dynamic supply-demand ration working in the industry.

Export share of trade

EU 32%

New Zealand 35%

Australia 10%

USA 7%

Argentina 4%

Ukraine 2%

Uruguay 1%

8

THE AUSTRALIAN DAIRY INDUSTRY

Other 9%

32%

35%

10%

7%

4%

2%1% 9%

EU

New Zealand

Australia

USA

Argentina

Ukraine

Uruguay

Other

Figure: Australian consumption statistics (Australian-dairy-industry, 2017)

Milk and it’s derivative products life cycle

The most consumption is in the fresh milk sector and the stage is by drinking (Nettle,

Brightling and Hope, 2013). The drinking milk, butter, cheese, yogurt are the majorly consumed

product among the country the statistics of per capita is given below.

Commodity Consumption(per capita/annum)

Milk 102 litres

Cheese 13kg

Butter 4 kg

Yogurt 7 kg

THE AUSTRALIAN DAIRY INDUSTRY

Other 9%

32%

35%

10%

7%

4%

2%1% 9%

EU

New Zealand

Australia

USA

Argentina

Ukraine

Uruguay

Other

Figure: Australian consumption statistics (Australian-dairy-industry, 2017)

Milk and it’s derivative products life cycle

The most consumption is in the fresh milk sector and the stage is by drinking (Nettle,

Brightling and Hope, 2013). The drinking milk, butter, cheese, yogurt are the majorly consumed

product among the country the statistics of per capita is given below.

Commodity Consumption(per capita/annum)

Milk 102 litres

Cheese 13kg

Butter 4 kg

Yogurt 7 kg

9

THE AUSTRALIAN DAIRY INDUSTRY

Figure: Australian consumption statistics(Australian-dairy-industry, 2017)

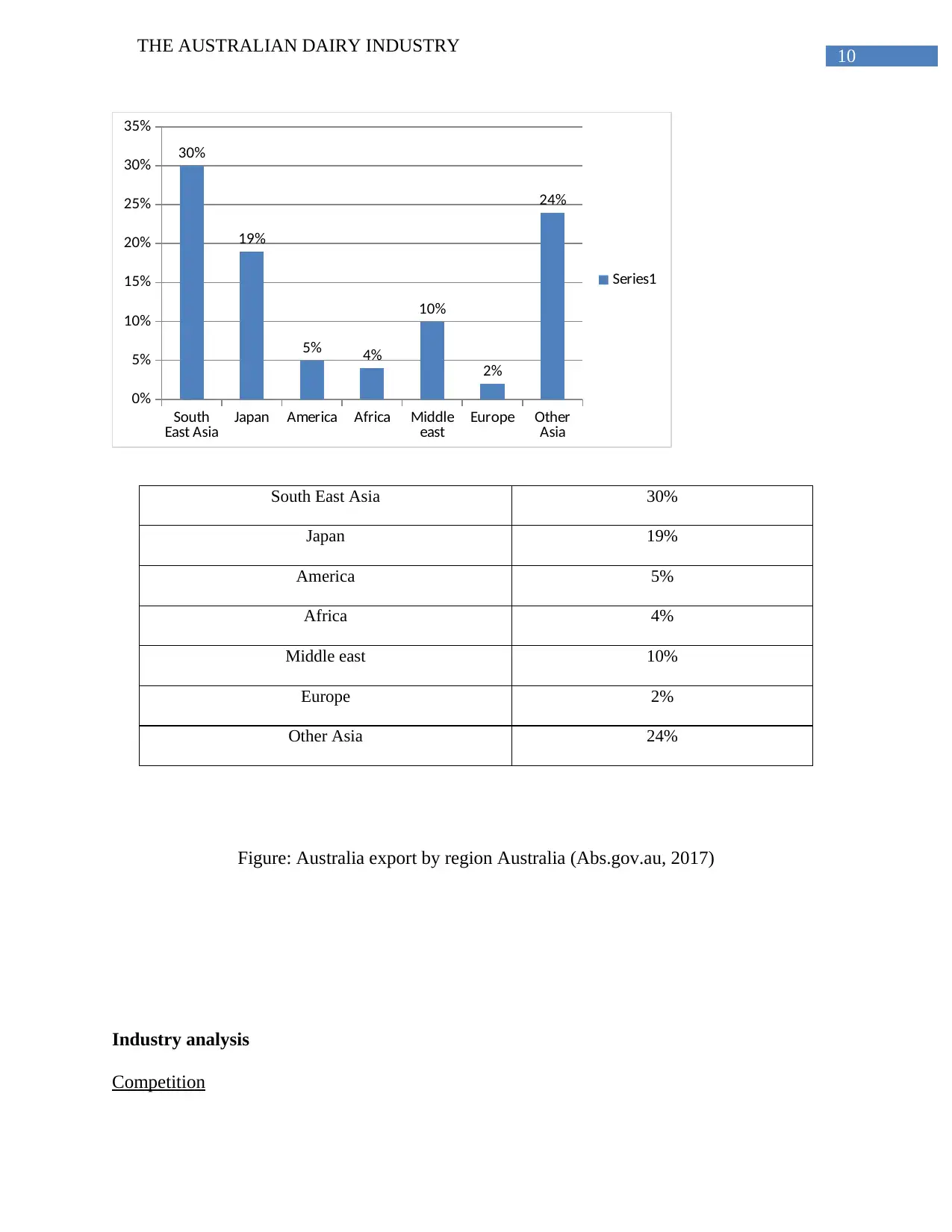

Australia export by region

THE AUSTRALIAN DAIRY INDUSTRY

Figure: Australian consumption statistics(Australian-dairy-industry, 2017)

Australia export by region

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

10

THE AUSTRALIAN DAIRY INDUSTRY

South

East Asia Japan America Africa Middle

east Europe Other

Asia

0%

5%

10%

15%

20%

25%

30%

35%

30%

19%

5% 4%

10%

2%

24%

Series1

South East Asia 30%

Japan 19%

America 5%

Africa 4%

Middle east 10%

Europe 2%

Other Asia 24%

Figure: Australia export by region Australia (Abs.gov.au, 2017)

Industry analysis

Competition

THE AUSTRALIAN DAIRY INDUSTRY

South

East Asia Japan America Africa Middle

east Europe Other

Asia

0%

5%

10%

15%

20%

25%

30%

35%

30%

19%

5% 4%

10%

2%

24%

Series1

South East Asia 30%

Japan 19%

America 5%

Africa 4%

Middle east 10%

Europe 2%

Other Asia 24%

Figure: Australia export by region Australia (Abs.gov.au, 2017)

Industry analysis

Competition

11

THE AUSTRALIAN DAIRY INDUSTRY

Internal value chain analysis– Australian dairy industry’s largest producer was Victoria

accounting for supplying 60% of the national milk consumption (Backus, Eidman and

Dijkhuizen, 2012). The Southern, Central, Coastal NSW Dairy industry produces diverse milk

production as they have land grass and fodder growing areas (Edwards, 2003). The market

influences are one among the major factor for fresh milk production. The processor authority

prefers local and reliably produced milk, which helps them in cost reduction and logistics

handling. This region produces among the 741 million litres of milk and 8% of Australia’s

production milk (Nettle, Brightling and Hope, 2013). The level of risk for adaptation and

investment may affect production of milk. Second, major reformation is likely to be made at

milk production stage in some challenging regions, which will in turn will affect on the current

system and structure (Buys et al.2014). Third, the Emission Trading Scheme of the country,

paired with a limited growth of production and increased ethical standards, everything have the

potential headed for raising costs above competitors, and this may affect the competitiveness and

price of Australian products (Von et al., 2013).

THE AUSTRALIAN DAIRY INDUSTRY

Internal value chain analysis– Australian dairy industry’s largest producer was Victoria

accounting for supplying 60% of the national milk consumption (Backus, Eidman and

Dijkhuizen, 2012). The Southern, Central, Coastal NSW Dairy industry produces diverse milk

production as they have land grass and fodder growing areas (Edwards, 2003). The market

influences are one among the major factor for fresh milk production. The processor authority

prefers local and reliably produced milk, which helps them in cost reduction and logistics

handling. This region produces among the 741 million litres of milk and 8% of Australia’s

production milk (Nettle, Brightling and Hope, 2013). The level of risk for adaptation and

investment may affect production of milk. Second, major reformation is likely to be made at

milk production stage in some challenging regions, which will in turn will affect on the current

system and structure (Buys et al.2014). Third, the Emission Trading Scheme of the country,

paired with a limited growth of production and increased ethical standards, everything have the

potential headed for raising costs above competitors, and this may affect the competitiveness and

price of Australian products (Von et al., 2013).

12

THE AUSTRALIAN DAIRY INDUSTRY

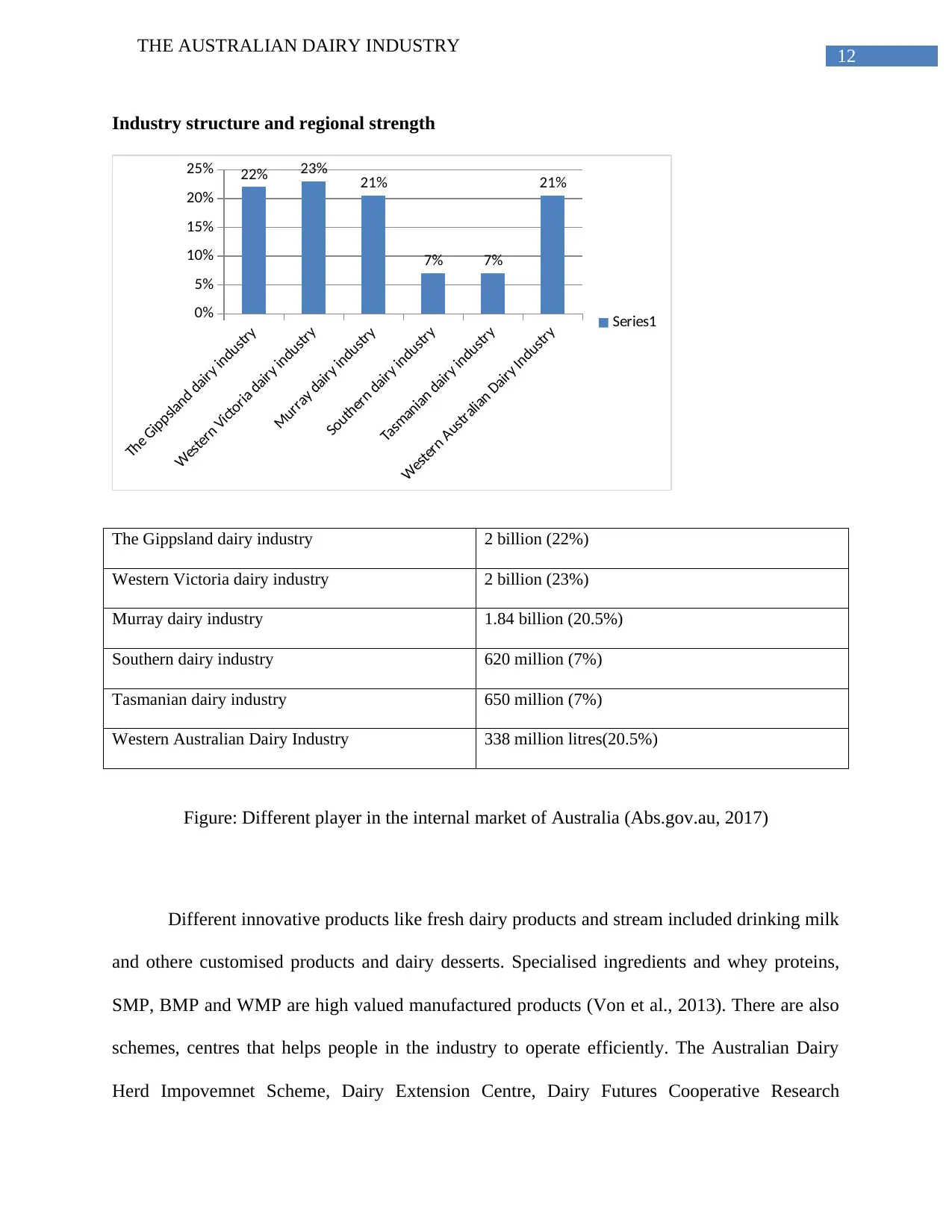

Industry structure and regional strength

The Gippsland dairy industry

Western Victoria dairy industry

Murray dairy industry

Southern dairy industry

Tasmanian dairy industry

Western Australian Dairy Industry

0%

5%

10%

15%

20%

25% 22% 23% 21%

7% 7%

21%

Series1

The Gippsland dairy industry 2 billion (22%)

Western Victoria dairy industry 2 billion (23%)

Murray dairy industry 1.84 billion (20.5%)

Southern dairy industry 620 million (7%)

Tasmanian dairy industry 650 million (7%)

Western Australian Dairy Industry 338 million litres(20.5%)

Figure: Different player in the internal market of Australia (Abs.gov.au, 2017)

Different innovative products like fresh dairy products and stream included drinking milk

and othere customised products and dairy desserts. Specialised ingredients and whey proteins,

SMP, BMP and WMP are high valued manufactured products (Von et al., 2013). There are also

schemes, centres that helps people in the industry to operate efficiently. The Australian Dairy

Herd Impovemnet Scheme, Dairy Extension Centre, Dairy Futures Cooperative Research

THE AUSTRALIAN DAIRY INDUSTRY

Industry structure and regional strength

The Gippsland dairy industry

Western Victoria dairy industry

Murray dairy industry

Southern dairy industry

Tasmanian dairy industry

Western Australian Dairy Industry

0%

5%

10%

15%

20%

25% 22% 23% 21%

7% 7%

21%

Series1

The Gippsland dairy industry 2 billion (22%)

Western Victoria dairy industry 2 billion (23%)

Murray dairy industry 1.84 billion (20.5%)

Southern dairy industry 620 million (7%)

Tasmanian dairy industry 650 million (7%)

Western Australian Dairy Industry 338 million litres(20.5%)

Figure: Different player in the internal market of Australia (Abs.gov.au, 2017)

Different innovative products like fresh dairy products and stream included drinking milk

and othere customised products and dairy desserts. Specialised ingredients and whey proteins,

SMP, BMP and WMP are high valued manufactured products (Von et al., 2013). There are also

schemes, centres that helps people in the industry to operate efficiently. The Australian Dairy

Herd Impovemnet Scheme, Dairy Extension Centre, Dairy Futures Cooperative Research

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

13

THE AUSTRALIAN DAIRY INDUSTRY

Centre(CRC), Dairy Innovation Australia Limited, Department of primary history Victoria

(Backus, Eidman and Dijkhuizen, 2012). The national bodies which helps in this are National

Heritage trust, National landscape program, NSW department and primary Industries, Tasmanian

Institute and Heritage trust are one of the major investor in the innovation program and dynamic

strategy faces challenges in the regarding Industry(Gourley et al., 2012).

External

Issues and challenges faced by the industry in global competition.

There are many challenges that the manufacturing industry faces in the production

procedure. The volatility of the supply and demand market and customer’s preference in the

different products. The global crisis on 2008-2009 has been the most difficult period for the

Industry (Bethune et al. 2004). However, the prices of the products have come down due to the

consumption pattern changes and outlook of retail stages have gone down due to the

competitiveness of the food safety (Edwards, 2003). In addition there is a decline in inflationary

pressure, that additionally benefits the selling of dairy products.

Strengths and weakness Opportunities and threats of the industry

Strengths

As the historical data suggest that the dairy industry have grown in the last three decades

they have incorporated efficient production methods

The position of this industry is strong in the export market and have seen steady growth

of 9% (Gourley et al., 2012).

THE AUSTRALIAN DAIRY INDUSTRY

Centre(CRC), Dairy Innovation Australia Limited, Department of primary history Victoria

(Backus, Eidman and Dijkhuizen, 2012). The national bodies which helps in this are National

Heritage trust, National landscape program, NSW department and primary Industries, Tasmanian

Institute and Heritage trust are one of the major investor in the innovation program and dynamic

strategy faces challenges in the regarding Industry(Gourley et al., 2012).

External

Issues and challenges faced by the industry in global competition.

There are many challenges that the manufacturing industry faces in the production

procedure. The volatility of the supply and demand market and customer’s preference in the

different products. The global crisis on 2008-2009 has been the most difficult period for the

Industry (Bethune et al. 2004). However, the prices of the products have come down due to the

consumption pattern changes and outlook of retail stages have gone down due to the

competitiveness of the food safety (Edwards, 2003). In addition there is a decline in inflationary

pressure, that additionally benefits the selling of dairy products.

Strengths and weakness Opportunities and threats of the industry

Strengths

As the historical data suggest that the dairy industry have grown in the last three decades

they have incorporated efficient production methods

The position of this industry is strong in the export market and have seen steady growth

of 9% (Gourley et al., 2012).

14

THE AUSTRALIAN DAIRY INDUSTRY

The Australian industry is one of the major exporters, as in third largest exporter on milk

and its derivative products.

The industry also have a backup of investors willing to contribute in the research and

development in dairy manufacturing and value added products, as well as the packaging and

customising the products (Bethune et al. 2004).

Weakness

The weakness is seen to be in the demand factor. The domestic market of the industry

faces the volatility of climate. The agricultural sector has always been prone to volatility

of climate change factors.

The retail sell and wholesale industry of milk faces a major problem of having shelf life

of the products.

Policy uncertainty of the trade practises has been one of the major weaknesses of the

industry.

Opportunity

Management of production risk less

Demand of all Australian milk products in Asia

Greater efficiency scale of the industry

Threats

The production cost

Climate change in agricultural business

THE AUSTRALIAN DAIRY INDUSTRY

The Australian industry is one of the major exporters, as in third largest exporter on milk

and its derivative products.

The industry also have a backup of investors willing to contribute in the research and

development in dairy manufacturing and value added products, as well as the packaging and

customising the products (Bethune et al. 2004).

Weakness

The weakness is seen to be in the demand factor. The domestic market of the industry

faces the volatility of climate. The agricultural sector has always been prone to volatility

of climate change factors.

The retail sell and wholesale industry of milk faces a major problem of having shelf life

of the products.

Policy uncertainty of the trade practises has been one of the major weaknesses of the

industry.

Opportunity

Management of production risk less

Demand of all Australian milk products in Asia

Greater efficiency scale of the industry

Threats

The production cost

Climate change in agricultural business

15

THE AUSTRALIAN DAIRY INDUSTRY

Strategic analysis

Porter’s values chain analysis

Barriers to entry – the Australian diary industry has been strong since 1989 revolution in the

industry (Soliman, 2000). However, the recent crisis in the milk production of the industry and

shortage in the production has lead to crisis in the international market reputation. The domestic

industry factors are strong to retaliate against (Gourley et al., 2012). Therefore, the risk to entry

of global competitors is less.

Threat of rival - the major threat in the industry is the water availability in the agro-cultivated

land but the industry is facing certain policy related problem on the state of Victoria. The other

industries are there to give competition to this industry in this matter. The deregulation of this

industry has left some uncertainty in the boar (Buys et l.2014). The rationalisation of this

industry has left the core efficient producers weak to international competitors vulnerable and

heavily subsided. The main competitors of this industry are China and Africa.

Threat of substitute – the products itself does not have good substitute. However, the competitors

pose a challenge in building the good substitute brand for the company.

Threat of supplier – The supplier market is dominative in this particular industry. The suppliers

have different board of co-operation and back up of having investments from the government

subsidiary bodies (Grace and Lennie, 2012). The total industry is private and deregulated in

Australia.

Threat of customers -the risk in threat of customers is less than any other industry. The

customers are less prone to go to other products than the fresh produce of the domestic

THE AUSTRALIAN DAIRY INDUSTRY

Strategic analysis

Porter’s values chain analysis

Barriers to entry – the Australian diary industry has been strong since 1989 revolution in the

industry (Soliman, 2000). However, the recent crisis in the milk production of the industry and

shortage in the production has lead to crisis in the international market reputation. The domestic

industry factors are strong to retaliate against (Gourley et al., 2012). Therefore, the risk to entry

of global competitors is less.

Threat of rival - the major threat in the industry is the water availability in the agro-cultivated

land but the industry is facing certain policy related problem on the state of Victoria. The other

industries are there to give competition to this industry in this matter. The deregulation of this

industry has left some uncertainty in the boar (Buys et l.2014). The rationalisation of this

industry has left the core efficient producers weak to international competitors vulnerable and

heavily subsided. The main competitors of this industry are China and Africa.

Threat of substitute – the products itself does not have good substitute. However, the competitors

pose a challenge in building the good substitute brand for the company.

Threat of supplier – The supplier market is dominative in this particular industry. The suppliers

have different board of co-operation and back up of having investments from the government

subsidiary bodies (Grace and Lennie, 2012). The total industry is private and deregulated in

Australia.

Threat of customers -the risk in threat of customers is less than any other industry. The

customers are less prone to go to other products than the fresh produce of the domestic

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

16

THE AUSTRALIAN DAIRY INDUSTRY

companies (Nettle, Brightling and Hope, 2013). However, the global competitor’s dairy products

and their innovative products may inherit a threat to competitors.

Conclusion

The Australian dairy industry is certainly a self-sufficient and competitive enough in the

global context. There is direct employment in the region of Australia for around 40,000 people

and additional downstream processing. This industry is one of Australia’s major industries that

contribute to the economic development. Australia ranks third in terms of global dairy trade with

10% share of world dairy export followed by New Zealand and the European Union. In response

to these discussed challenges, a variety of strategies well as actions and plan have been

redirected or executed by the industry in respect to the industry’s production systems, response

to environmental change and natural resource management, and market access. In a nutshell, the

Australian dairy industry has faced significant challenges like deregulation, droughts and the

financial crisis. However, the industry has also demonstrated its ability to adapt to difficult

situations through sharing its view of the challenges and opportunities and addressing these

challenges with collective action.

THE AUSTRALIAN DAIRY INDUSTRY

companies (Nettle, Brightling and Hope, 2013). However, the global competitor’s dairy products

and their innovative products may inherit a threat to competitors.

Conclusion

The Australian dairy industry is certainly a self-sufficient and competitive enough in the

global context. There is direct employment in the region of Australia for around 40,000 people

and additional downstream processing. This industry is one of Australia’s major industries that

contribute to the economic development. Australia ranks third in terms of global dairy trade with

10% share of world dairy export followed by New Zealand and the European Union. In response

to these discussed challenges, a variety of strategies well as actions and plan have been

redirected or executed by the industry in respect to the industry’s production systems, response

to environmental change and natural resource management, and market access. In a nutshell, the

Australian dairy industry has faced significant challenges like deregulation, droughts and the

financial crisis. However, the industry has also demonstrated its ability to adapt to difficult

situations through sharing its view of the challenges and opportunities and addressing these

challenges with collective action.

17

THE AUSTRALIAN DAIRY INDUSTRY

Reference

Abs.gov.au. 2017. 1301.0 - Year Book Australia, 2004. [online] Available at:

http://www.abs.gov.au/Ausstats/abs@.nsf/0/B006A83A9127B0F5CA256DEA00053965?Open

[Accessed 29 Aug. 2017].

http://www.pwc.com.au/industry/agribusiness/assets/australian-dairy-industry-nov11.pdf

[Accessed 29 Aug. 2017].

Backus, G.B.C., Eidman, V.R. and Dijkhuizen, A.A., 2012. Farm decision making under risk and

uncertainty. NJAS wageningen journal of life sciences, 45(2), pp.307-328.

Bethune, M. and Armstrong, D.P., 2004. Overview of the irrigated dairy industry in

Australia. Australian Journal of Experimental Agriculture, 44(2), pp.127-129.

Buys, L., Mengersen, K., Johnson, S., van Buuren, N. and Chauvin, A., 2014. Creating a

Sustainability Scorecard as a predictive tool for measuring the complex social, economic and

environmental impacts of industries, a case study: Assessing the viability and sustainability of

the dairy industry. Journal of environmental management, 133, pp.184-192.

Edwards, G., 2003. The story of deregulation in the dairy industry. Australian Journal of

Agricultural and Resource Economics, 47(1), pp.75-98.

Gourley, C.J., Dougherty, W.J., Weaver, D.M., Aarons, S.R., Awty, I.M., Gibson, D.M.,

Hannah, M.C., Smith, A.P. and Peverill, K.I., 2012. Farm-scale nitrogen, phosphorus, potassium

and sulfur balances and use efficiencies on Australian dairy farms. Animal Production

Science, 52(10), pp.929-944.

THE AUSTRALIAN DAIRY INDUSTRY

Reference

Abs.gov.au. 2017. 1301.0 - Year Book Australia, 2004. [online] Available at:

http://www.abs.gov.au/Ausstats/abs@.nsf/0/B006A83A9127B0F5CA256DEA00053965?Open

[Accessed 29 Aug. 2017].

http://www.pwc.com.au/industry/agribusiness/assets/australian-dairy-industry-nov11.pdf

[Accessed 29 Aug. 2017].

Backus, G.B.C., Eidman, V.R. and Dijkhuizen, A.A., 2012. Farm decision making under risk and

uncertainty. NJAS wageningen journal of life sciences, 45(2), pp.307-328.

Bethune, M. and Armstrong, D.P., 2004. Overview of the irrigated dairy industry in

Australia. Australian Journal of Experimental Agriculture, 44(2), pp.127-129.

Buys, L., Mengersen, K., Johnson, S., van Buuren, N. and Chauvin, A., 2014. Creating a

Sustainability Scorecard as a predictive tool for measuring the complex social, economic and

environmental impacts of industries, a case study: Assessing the viability and sustainability of

the dairy industry. Journal of environmental management, 133, pp.184-192.

Edwards, G., 2003. The story of deregulation in the dairy industry. Australian Journal of

Agricultural and Resource Economics, 47(1), pp.75-98.

Gourley, C.J., Dougherty, W.J., Weaver, D.M., Aarons, S.R., Awty, I.M., Gibson, D.M.,

Hannah, M.C., Smith, A.P. and Peverill, K.I., 2012. Farm-scale nitrogen, phosphorus, potassium

and sulfur balances and use efficiencies on Australian dairy farms. Animal Production

Science, 52(10), pp.929-944.

18

THE AUSTRALIAN DAIRY INDUSTRY

Grace, M. and Lennie, J., 2012. Constructing and reconstructing rural women in Australia: The

politics of change, diversity and identity. Sociologia Ruralis, 38(3), pp.351-370.

Klerkx, L. and Nettle, R., 2013. Achievements and challenges of innovation co-production

support initiatives in the Australian and Dutch dairy sectors: a comparative study. Food

Policy, 40, pp.74-89.

Klerkx, L. and Nettle, R., 2013. Achievements and challenges of innovation co-production

support initiatives in the Australian and Dutch dairy sectors: a comparative study. Food

Policy, 40, pp.74-89.

Nettle, R., Brightling, P. and Hope, A., 2013. How programme teams progress agricultural

innovation in the Australian dairy industry. The Journal of Agricultural Education and

Extension, 19(3), pp.271-290.

Nettle, R., Brightling, P. and Hope, A., 2013. How programme teams progress agricultural

innovation in the Australian dairy industry. The Journal of Agricultural Education and

Extension, 19(3), pp.271-290.

Nettle, R., Paine, M. and Penry, J., 2010. Aligning farm decision making and genetic information

systems to improve animal production: methodology and findings from the Australian dairy

industry. Animal Production Science, 50(6), pp.429-434.

Regulations, P., 2013. Australian Dairy Industry.

Soliman, F., 2000. Application of knowledge management for hazard analysis in the Australian

dairy industry. Journal of Knowledge Management, 4(4), pp.287-294.

THE AUSTRALIAN DAIRY INDUSTRY

Grace, M. and Lennie, J., 2012. Constructing and reconstructing rural women in Australia: The

politics of change, diversity and identity. Sociologia Ruralis, 38(3), pp.351-370.

Klerkx, L. and Nettle, R., 2013. Achievements and challenges of innovation co-production

support initiatives in the Australian and Dutch dairy sectors: a comparative study. Food

Policy, 40, pp.74-89.

Klerkx, L. and Nettle, R., 2013. Achievements and challenges of innovation co-production

support initiatives in the Australian and Dutch dairy sectors: a comparative study. Food

Policy, 40, pp.74-89.

Nettle, R., Brightling, P. and Hope, A., 2013. How programme teams progress agricultural

innovation in the Australian dairy industry. The Journal of Agricultural Education and

Extension, 19(3), pp.271-290.

Nettle, R., Brightling, P. and Hope, A., 2013. How programme teams progress agricultural

innovation in the Australian dairy industry. The Journal of Agricultural Education and

Extension, 19(3), pp.271-290.

Nettle, R., Paine, M. and Penry, J., 2010. Aligning farm decision making and genetic information

systems to improve animal production: methodology and findings from the Australian dairy

industry. Animal Production Science, 50(6), pp.429-434.

Regulations, P., 2013. Australian Dairy Industry.

Soliman, F., 2000. Application of knowledge management for hazard analysis in the Australian

dairy industry. Journal of Knowledge Management, 4(4), pp.287-294.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

19

THE AUSTRALIAN DAIRY INDUSTRY

Sorensen, T., 2011. Australian agricultural R&D and innovation systems. International Journal

of Foresight and Innovation Policy, 7(1-3), pp.192-212.

Von Keyserlingk, M.A.G., Martin, N.P., Kebreab, E., Knowlton, K.F., Grant, R.J., Stephenson,

M., Sniffen, C.J., Harner, J.P., Wright, A.D. and Smith, S.I., 2013. Invited review: Sustainability

of the US dairy industry. Journal of dairy science, 96(9), pp.5405-5425.

THE AUSTRALIAN DAIRY INDUSTRY

Sorensen, T., 2011. Australian agricultural R&D and innovation systems. International Journal

of Foresight and Innovation Policy, 7(1-3), pp.192-212.

Von Keyserlingk, M.A.G., Martin, N.P., Kebreab, E., Knowlton, K.F., Grant, R.J., Stephenson,

M., Sniffen, C.J., Harner, J.P., Wright, A.D. and Smith, S.I., 2013. Invited review: Sustainability

of the US dairy industry. Journal of dairy science, 96(9), pp.5405-5425.

1 out of 20

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

© 2024 | Zucol Services PVT LTD | All rights reserved.