BUS708: Data Analysis of Tax Lodgement Methods for Australia

VerifiedAdded on 2020/05/16

|13

|2322

|237

Report

AI Summary

This report, prepared for BUS708 Statistics and Data Analysis, examines tax lodgement preferences in Australia, utilizing data from the Australian Taxation Office (ATO) and a survey of international students. The analysis compares the use of tax agents versus self-preparation for tax returns. Key findings include that a significant majority of both the general Australian population and international students prefer using tax agents. The study investigates the relationship between age range and lodgement method, finding a preference for tax agents across all age groups. Furthermore, the report analyzes the correlation between total income, total deductions, and the chosen lodgement method, revealing that individuals using tax agents tend to have higher average incomes. Regression analysis is performed to assess the relationship between income and deductions for both tax agent users and self-preparers, showing a weak positive correlation for tax agents and a moderate positive correlation for self-preparers. The study concludes that the preference for tax agents is consistent across both datasets, highlighting the importance of professional assistance in tax filing.

Running Head: BUS708 STATISTICS AND DATA ANALYSIS

BUS708 Statistics and Data Analysis

Name of the Student

Name of the University

Author Note

BUS708 Statistics and Data Analysis

Name of the Student

Name of the University

Author Note

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

1BUS708 STATISTICS AND DATA ANALYSIS

Table of Contents

1.0 Introduction...........................................................................................................................................2

2.0 Analysis of Lodgement Method of ATO Data.........................................................................................2

3.0 Analysis of Lodgement Method of Students Data.................................................................................3

4.0 Age Range and Lodgement Method......................................................................................................5

5.0 Lodgement Method and Total Income..................................................................................................6

6.0 Total Income and Total Deduction based on Lodgement Methods.......................................................9

7.0 Conclusion...........................................................................................................................................10

References.................................................................................................................................................11

Table of Contents

1.0 Introduction...........................................................................................................................................2

2.0 Analysis of Lodgement Method of ATO Data.........................................................................................2

3.0 Analysis of Lodgement Method of Students Data.................................................................................3

4.0 Age Range and Lodgement Method......................................................................................................5

5.0 Lodgement Method and Total Income..................................................................................................6

6.0 Total Income and Total Deduction based on Lodgement Methods.......................................................9

7.0 Conclusion...........................................................................................................................................10

References.................................................................................................................................................11

2BUS708 STATISTICS AND DATA ANALYSIS

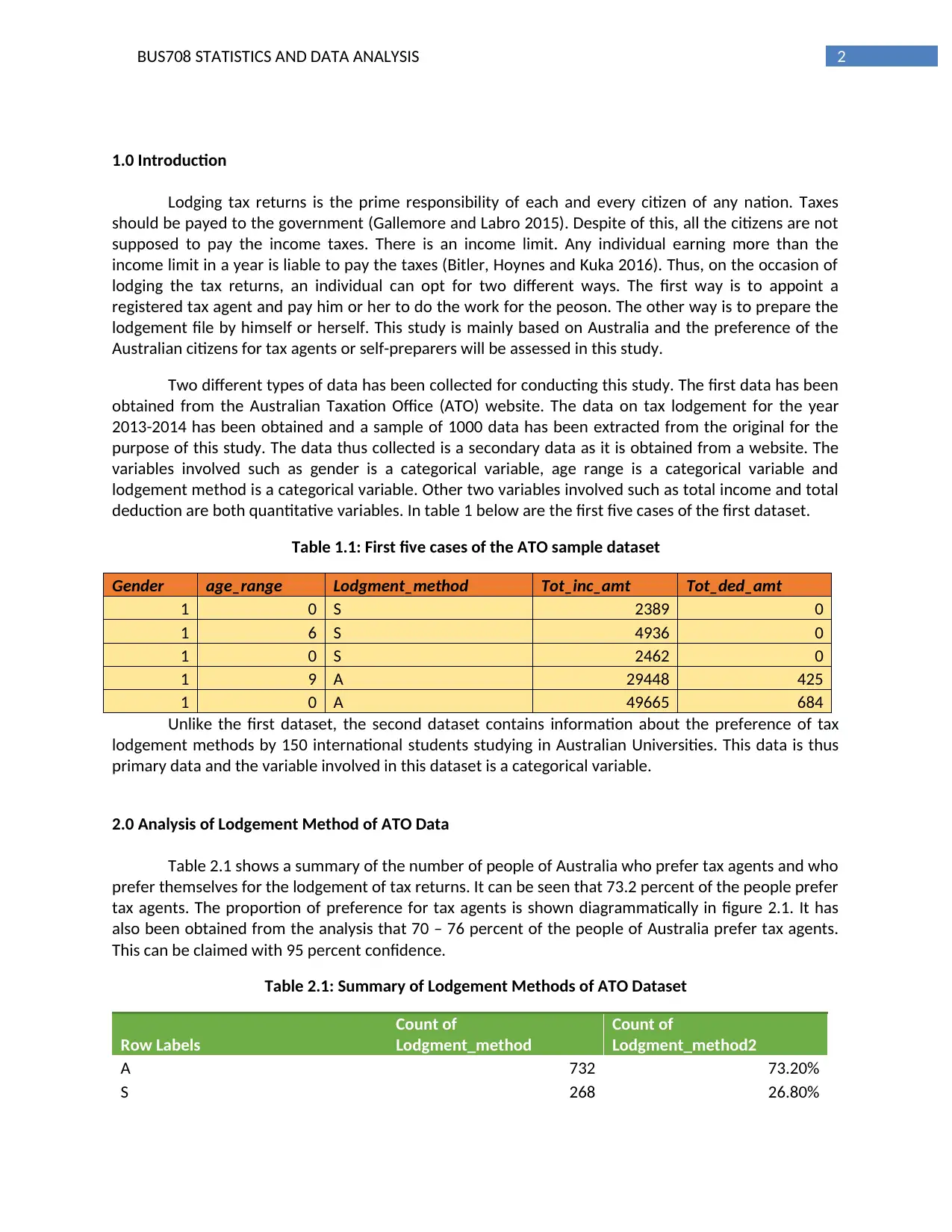

1.0 Introduction

Lodging tax returns is the prime responsibility of each and every citizen of any nation. Taxes

should be payed to the government (Gallemore and Labro 2015). Despite of this, all the citizens are not

supposed to pay the income taxes. There is an income limit. Any individual earning more than the

income limit in a year is liable to pay the taxes (Bitler, Hoynes and Kuka 2016). Thus, on the occasion of

lodging the tax returns, an individual can opt for two different ways. The first way is to appoint a

registered tax agent and pay him or her to do the work for the peoson. The other way is to prepare the

lodgement file by himself or herself. This study is mainly based on Australia and the preference of the

Australian citizens for tax agents or self-preparers will be assessed in this study.

Two different types of data has been collected for conducting this study. The first data has been

obtained from the Australian Taxation Office (ATO) website. The data on tax lodgement for the year

2013-2014 has been obtained and a sample of 1000 data has been extracted from the original for the

purpose of this study. The data thus collected is a secondary data as it is obtained from a website. The

variables involved such as gender is a categorical variable, age range is a categorical variable and

lodgement method is a categorical variable. Other two variables involved such as total income and total

deduction are both quantitative variables. In table 1 below are the first five cases of the first dataset.

Table 1.1: First five cases of the ATO sample dataset

Gender age_range Lodgment_method Tot_inc_amt Tot_ded_amt

1 0 S 2389 0

1 6 S 4936 0

1 0 S 2462 0

1 9 A 29448 425

1 0 A 49665 684

Unlike the first dataset, the second dataset contains information about the preference of tax

lodgement methods by 150 international students studying in Australian Universities. This data is thus

primary data and the variable involved in this dataset is a categorical variable.

2.0 Analysis of Lodgement Method of ATO Data

Table 2.1 shows a summary of the number of people of Australia who prefer tax agents and who

prefer themselves for the lodgement of tax returns. It can be seen that 73.2 percent of the people prefer

tax agents. The proportion of preference for tax agents is shown diagrammatically in figure 2.1. It has

also been obtained from the analysis that 70 – 76 percent of the people of Australia prefer tax agents.

This can be claimed with 95 percent confidence.

Table 2.1: Summary of Lodgement Methods of ATO Dataset

Row Labels

Count of

Lodgment_method

Count of

Lodgment_method2

A 732 73.20%

S 268 26.80%

1.0 Introduction

Lodging tax returns is the prime responsibility of each and every citizen of any nation. Taxes

should be payed to the government (Gallemore and Labro 2015). Despite of this, all the citizens are not

supposed to pay the income taxes. There is an income limit. Any individual earning more than the

income limit in a year is liable to pay the taxes (Bitler, Hoynes and Kuka 2016). Thus, on the occasion of

lodging the tax returns, an individual can opt for two different ways. The first way is to appoint a

registered tax agent and pay him or her to do the work for the peoson. The other way is to prepare the

lodgement file by himself or herself. This study is mainly based on Australia and the preference of the

Australian citizens for tax agents or self-preparers will be assessed in this study.

Two different types of data has been collected for conducting this study. The first data has been

obtained from the Australian Taxation Office (ATO) website. The data on tax lodgement for the year

2013-2014 has been obtained and a sample of 1000 data has been extracted from the original for the

purpose of this study. The data thus collected is a secondary data as it is obtained from a website. The

variables involved such as gender is a categorical variable, age range is a categorical variable and

lodgement method is a categorical variable. Other two variables involved such as total income and total

deduction are both quantitative variables. In table 1 below are the first five cases of the first dataset.

Table 1.1: First five cases of the ATO sample dataset

Gender age_range Lodgment_method Tot_inc_amt Tot_ded_amt

1 0 S 2389 0

1 6 S 4936 0

1 0 S 2462 0

1 9 A 29448 425

1 0 A 49665 684

Unlike the first dataset, the second dataset contains information about the preference of tax

lodgement methods by 150 international students studying in Australian Universities. This data is thus

primary data and the variable involved in this dataset is a categorical variable.

2.0 Analysis of Lodgement Method of ATO Data

Table 2.1 shows a summary of the number of people of Australia who prefer tax agents and who

prefer themselves for the lodgement of tax returns. It can be seen that 73.2 percent of the people prefer

tax agents. The proportion of preference for tax agents is shown diagrammatically in figure 2.1. It has

also been obtained from the analysis that 70 – 76 percent of the people of Australia prefer tax agents.

This can be claimed with 95 percent confidence.

Table 2.1: Summary of Lodgement Methods of ATO Dataset

Row Labels

Count of

Lodgment_method

Count of

Lodgment_method2

A 732 73.20%

S 268 26.80%

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

3BUS708 STATISTICS AND DATA ANALYSIS

Grand Total 1000 100.00%

73%

27%

Proportion of Lodgement Methods from the ATO Dataset

A

S

Figure 2.1: Pie chart showing proportion of Lodgement Methods for ATO Dataset

Table 2.2: Proportion of Tax Agents of ATO Dataset

Sample Size 1000

Count of Successes 732

Confidence Level 95%

Sample Proportion 0.732

z Value 1.9600

Standard Error of the Proportion 0.014006284

Margin of Error 0.0275

Calculations for Computation of Confidence Interval

Interval Lower Limit 70.45%

Interval Upper Limit 75.95%

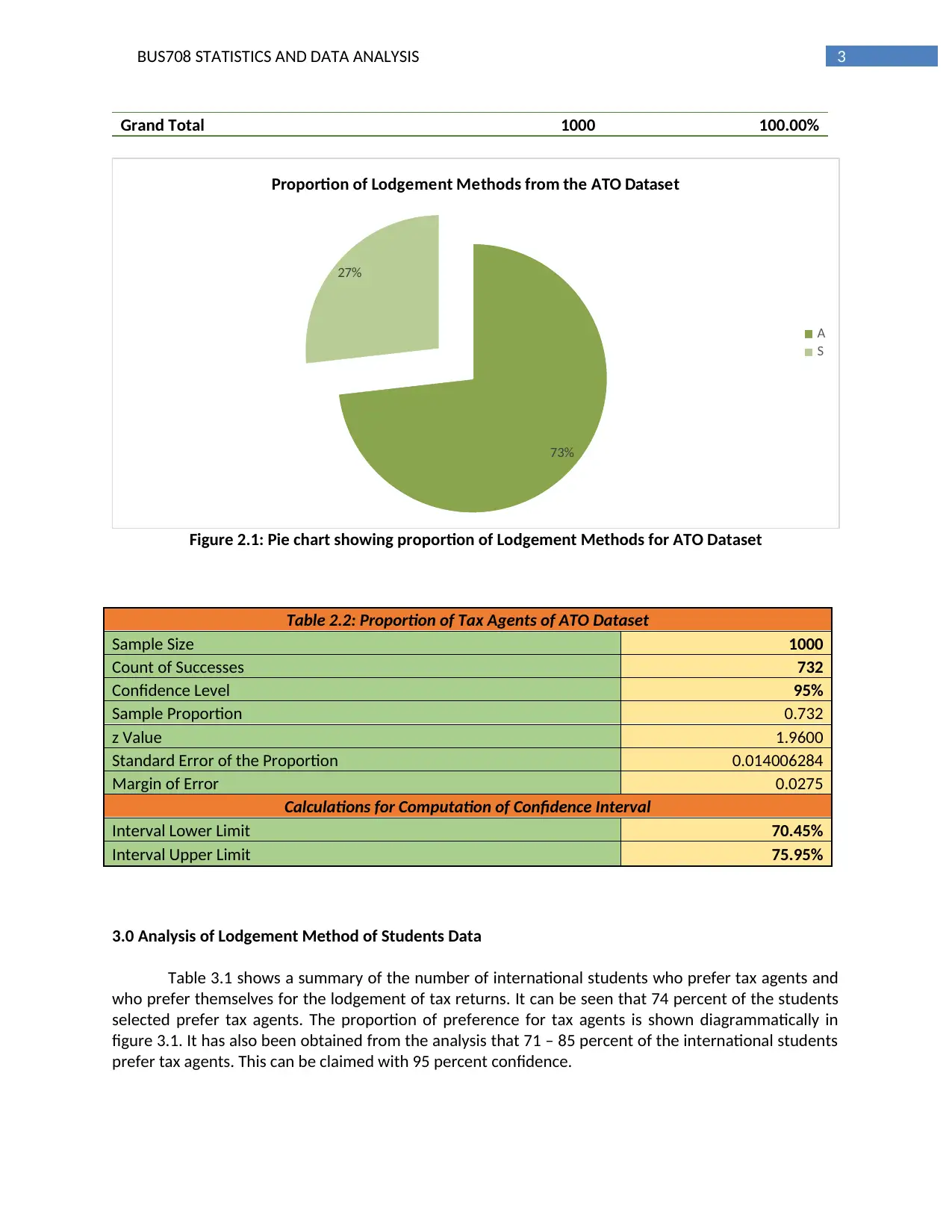

3.0 Analysis of Lodgement Method of Students Data

Table 3.1 shows a summary of the number of international students who prefer tax agents and

who prefer themselves for the lodgement of tax returns. It can be seen that 74 percent of the students

selected prefer tax agents. The proportion of preference for tax agents is shown diagrammatically in

figure 3.1. It has also been obtained from the analysis that 71 – 85 percent of the international students

prefer tax agents. This can be claimed with 95 percent confidence.

Grand Total 1000 100.00%

73%

27%

Proportion of Lodgement Methods from the ATO Dataset

A

S

Figure 2.1: Pie chart showing proportion of Lodgement Methods for ATO Dataset

Table 2.2: Proportion of Tax Agents of ATO Dataset

Sample Size 1000

Count of Successes 732

Confidence Level 95%

Sample Proportion 0.732

z Value 1.9600

Standard Error of the Proportion 0.014006284

Margin of Error 0.0275

Calculations for Computation of Confidence Interval

Interval Lower Limit 70.45%

Interval Upper Limit 75.95%

3.0 Analysis of Lodgement Method of Students Data

Table 3.1 shows a summary of the number of international students who prefer tax agents and

who prefer themselves for the lodgement of tax returns. It can be seen that 74 percent of the students

selected prefer tax agents. The proportion of preference for tax agents is shown diagrammatically in

figure 3.1. It has also been obtained from the analysis that 71 – 85 percent of the international students

prefer tax agents. This can be claimed with 95 percent confidence.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

4BUS708 STATISTICS AND DATA ANALYSIS

Table 3.1: Summary of Lodgement Methods of Students Dataset

Values

Lodgement Method Frequency Proportion

A 134 0.74

S 46 0.26

Grand Total 180 1

78%

22%

Proportion of Lodgement Methods for Students Dataset

A

S

Figure 3.1: Pie chart showing proportion of Lodgement Methods for Students Dataset

Table 3.2: Proportion of Tax Agents of Students Dataset

Sample Size 150

Count of Successes 117

Confidence Level 95%

Sample Proportion 0.78

z Value 1.9600

Standard Error of the Proportion 0.033823069

Margin of Error 0.0663

Calculations for Computation of Confidence Interval

Interval Lower Limit 71.37%

Interval Upper Limit 84.63%

To test whether the proportion of Australian people (p1) and International students (p2)

preferring tax agents are equal, z-test has to be computed (Park 2015). The null and the alternate

hypothesis for this test are defined as follows:

Table 3.1: Summary of Lodgement Methods of Students Dataset

Values

Lodgement Method Frequency Proportion

A 134 0.74

S 46 0.26

Grand Total 180 1

78%

22%

Proportion of Lodgement Methods for Students Dataset

A

S

Figure 3.1: Pie chart showing proportion of Lodgement Methods for Students Dataset

Table 3.2: Proportion of Tax Agents of Students Dataset

Sample Size 150

Count of Successes 117

Confidence Level 95%

Sample Proportion 0.78

z Value 1.9600

Standard Error of the Proportion 0.033823069

Margin of Error 0.0663

Calculations for Computation of Confidence Interval

Interval Lower Limit 71.37%

Interval Upper Limit 84.63%

To test whether the proportion of Australian people (p1) and International students (p2)

preferring tax agents are equal, z-test has to be computed (Park 2015). The null and the alternate

hypothesis for this test are defined as follows:

5BUS708 STATISTICS AND DATA ANALYSIS

Null Hypothesis (H0): p1 – p2 = 0

Alternate Hypothesis (H1): p1 – p2 ≠ 0

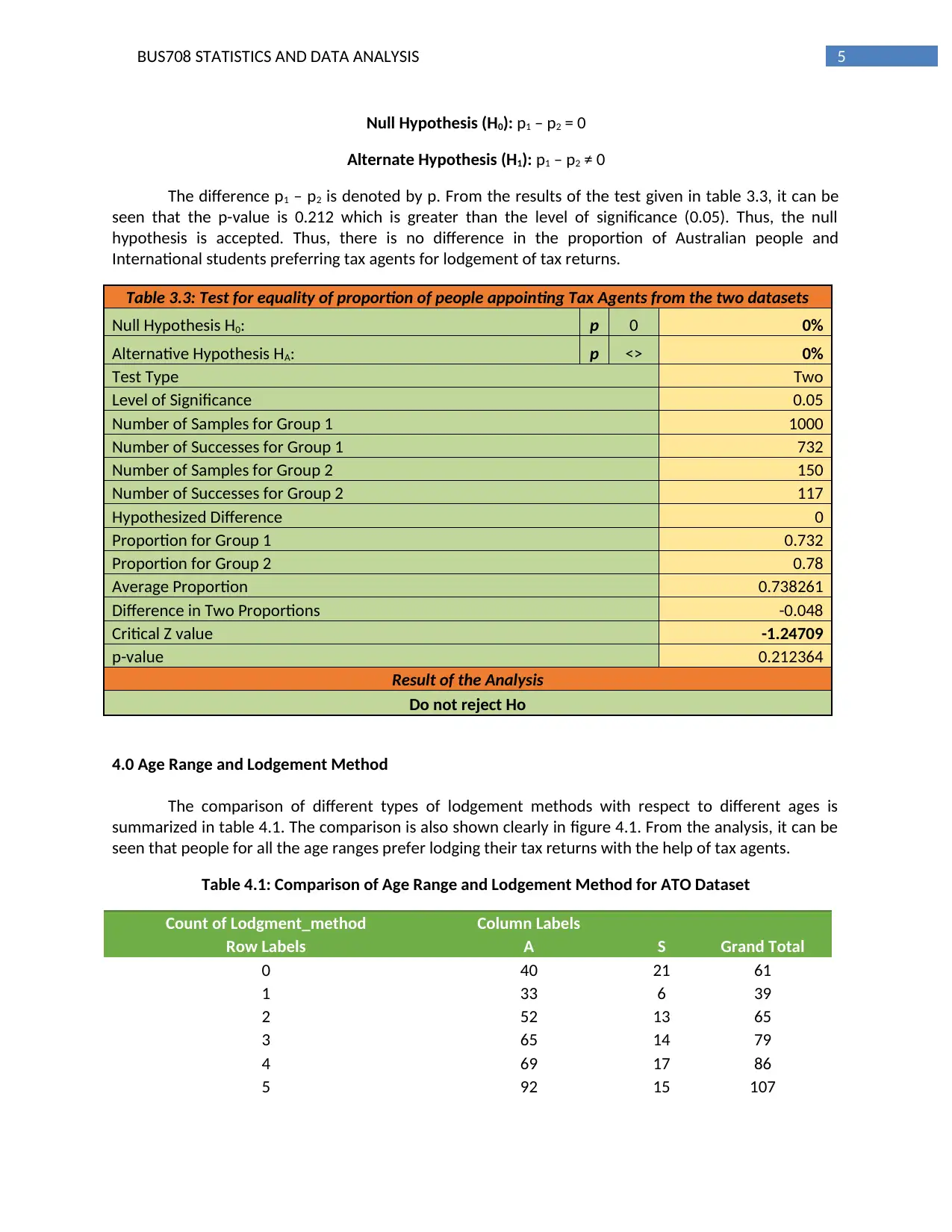

The difference p1 – p2 is denoted by p. From the results of the test given in table 3.3, it can be

seen that the p-value is 0.212 which is greater than the level of significance (0.05). Thus, the null

hypothesis is accepted. Thus, there is no difference in the proportion of Australian people and

International students preferring tax agents for lodgement of tax returns.

Table 3.3: Test for equality of proportion of people appointing Tax Agents from the two datasets

Null Hypothesis H0: p 0 0%

Alternative Hypothesis HA: p <> 0%

Test Type Two

Level of Significance 0.05

Number of Samples for Group 1 1000

Number of Successes for Group 1 732

Number of Samples for Group 2 150

Number of Successes for Group 2 117

Hypothesized Difference 0

Proportion for Group 1 0.732

Proportion for Group 2 0.78

Average Proportion 0.738261

Difference in Two Proportions -0.048

Critical Z value -1.24709

p-value 0.212364

Result of the Analysis

Do not reject Ho

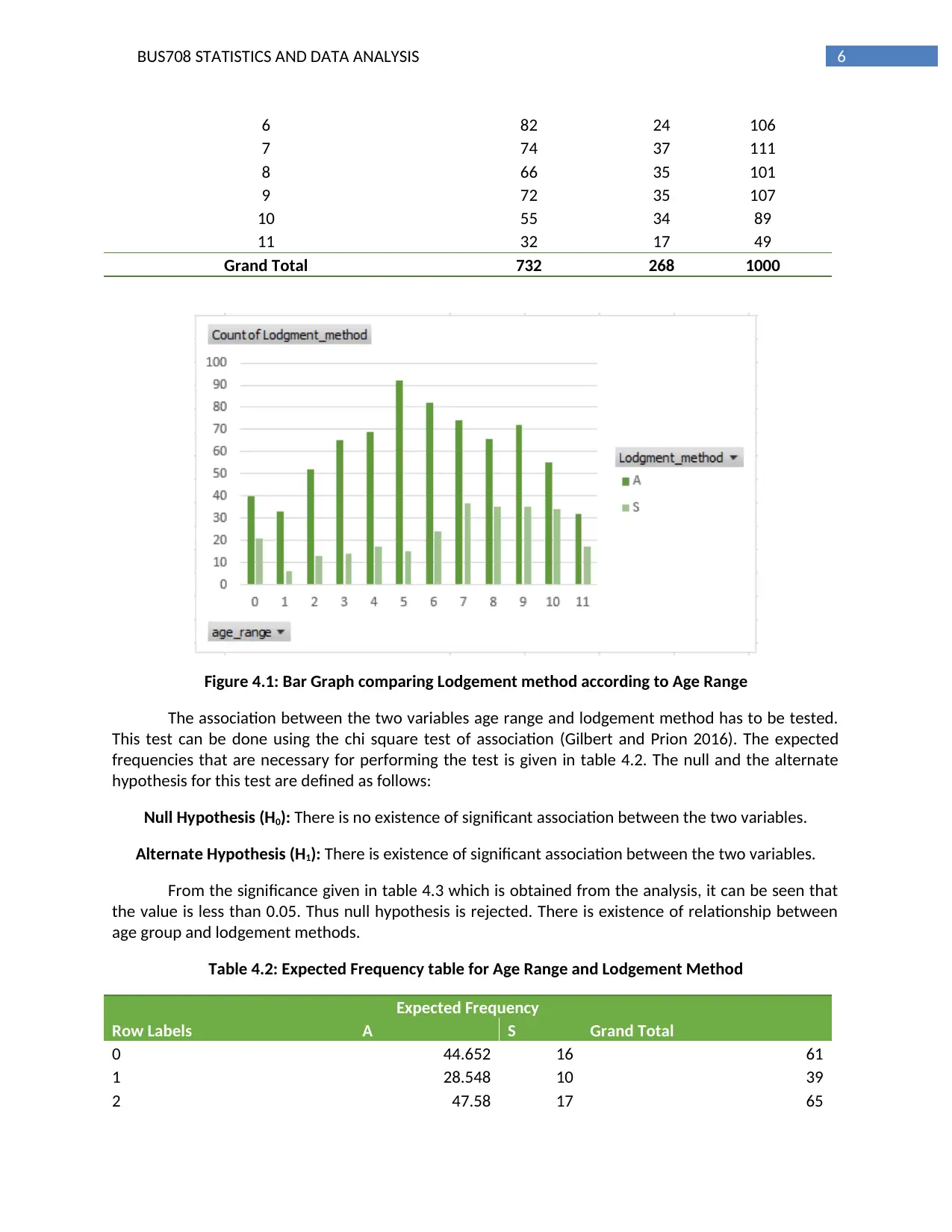

4.0 Age Range and Lodgement Method

The comparison of different types of lodgement methods with respect to different ages is

summarized in table 4.1. The comparison is also shown clearly in figure 4.1. From the analysis, it can be

seen that people for all the age ranges prefer lodging their tax returns with the help of tax agents.

Table 4.1: Comparison of Age Range and Lodgement Method for ATO Dataset

Count of Lodgment_method Column Labels

Row Labels A S Grand Total

0 40 21 61

1 33 6 39

2 52 13 65

3 65 14 79

4 69 17 86

5 92 15 107

Null Hypothesis (H0): p1 – p2 = 0

Alternate Hypothesis (H1): p1 – p2 ≠ 0

The difference p1 – p2 is denoted by p. From the results of the test given in table 3.3, it can be

seen that the p-value is 0.212 which is greater than the level of significance (0.05). Thus, the null

hypothesis is accepted. Thus, there is no difference in the proportion of Australian people and

International students preferring tax agents for lodgement of tax returns.

Table 3.3: Test for equality of proportion of people appointing Tax Agents from the two datasets

Null Hypothesis H0: p 0 0%

Alternative Hypothesis HA: p <> 0%

Test Type Two

Level of Significance 0.05

Number of Samples for Group 1 1000

Number of Successes for Group 1 732

Number of Samples for Group 2 150

Number of Successes for Group 2 117

Hypothesized Difference 0

Proportion for Group 1 0.732

Proportion for Group 2 0.78

Average Proportion 0.738261

Difference in Two Proportions -0.048

Critical Z value -1.24709

p-value 0.212364

Result of the Analysis

Do not reject Ho

4.0 Age Range and Lodgement Method

The comparison of different types of lodgement methods with respect to different ages is

summarized in table 4.1. The comparison is also shown clearly in figure 4.1. From the analysis, it can be

seen that people for all the age ranges prefer lodging their tax returns with the help of tax agents.

Table 4.1: Comparison of Age Range and Lodgement Method for ATO Dataset

Count of Lodgment_method Column Labels

Row Labels A S Grand Total

0 40 21 61

1 33 6 39

2 52 13 65

3 65 14 79

4 69 17 86

5 92 15 107

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

6BUS708 STATISTICS AND DATA ANALYSIS

6 82 24 106

7 74 37 111

8 66 35 101

9 72 35 107

10 55 34 89

11 32 17 49

Grand Total 732 268 1000

Figure 4.1: Bar Graph comparing Lodgement method according to Age Range

The association between the two variables age range and lodgement method has to be tested.

This test can be done using the chi square test of association (Gilbert and Prion 2016). The expected

frequencies that are necessary for performing the test is given in table 4.2. The null and the alternate

hypothesis for this test are defined as follows:

Null Hypothesis (H0): There is no existence of significant association between the two variables.

Alternate Hypothesis (H1): There is existence of significant association between the two variables.

From the significance given in table 4.3 which is obtained from the analysis, it can be seen that

the value is less than 0.05. Thus null hypothesis is rejected. There is existence of relationship between

age group and lodgement methods.

Table 4.2: Expected Frequency table for Age Range and Lodgement Method

Expected Frequency

Row Labels A S Grand Total

0 44.652 16 61

1 28.548 10 39

2 47.58 17 65

6 82 24 106

7 74 37 111

8 66 35 101

9 72 35 107

10 55 34 89

11 32 17 49

Grand Total 732 268 1000

Figure 4.1: Bar Graph comparing Lodgement method according to Age Range

The association between the two variables age range and lodgement method has to be tested.

This test can be done using the chi square test of association (Gilbert and Prion 2016). The expected

frequencies that are necessary for performing the test is given in table 4.2. The null and the alternate

hypothesis for this test are defined as follows:

Null Hypothesis (H0): There is no existence of significant association between the two variables.

Alternate Hypothesis (H1): There is existence of significant association between the two variables.

From the significance given in table 4.3 which is obtained from the analysis, it can be seen that

the value is less than 0.05. Thus null hypothesis is rejected. There is existence of relationship between

age group and lodgement methods.

Table 4.2: Expected Frequency table for Age Range and Lodgement Method

Expected Frequency

Row Labels A S Grand Total

0 44.652 16 61

1 28.548 10 39

2 47.58 17 65

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

7BUS708 STATISTICS AND DATA ANALYSIS

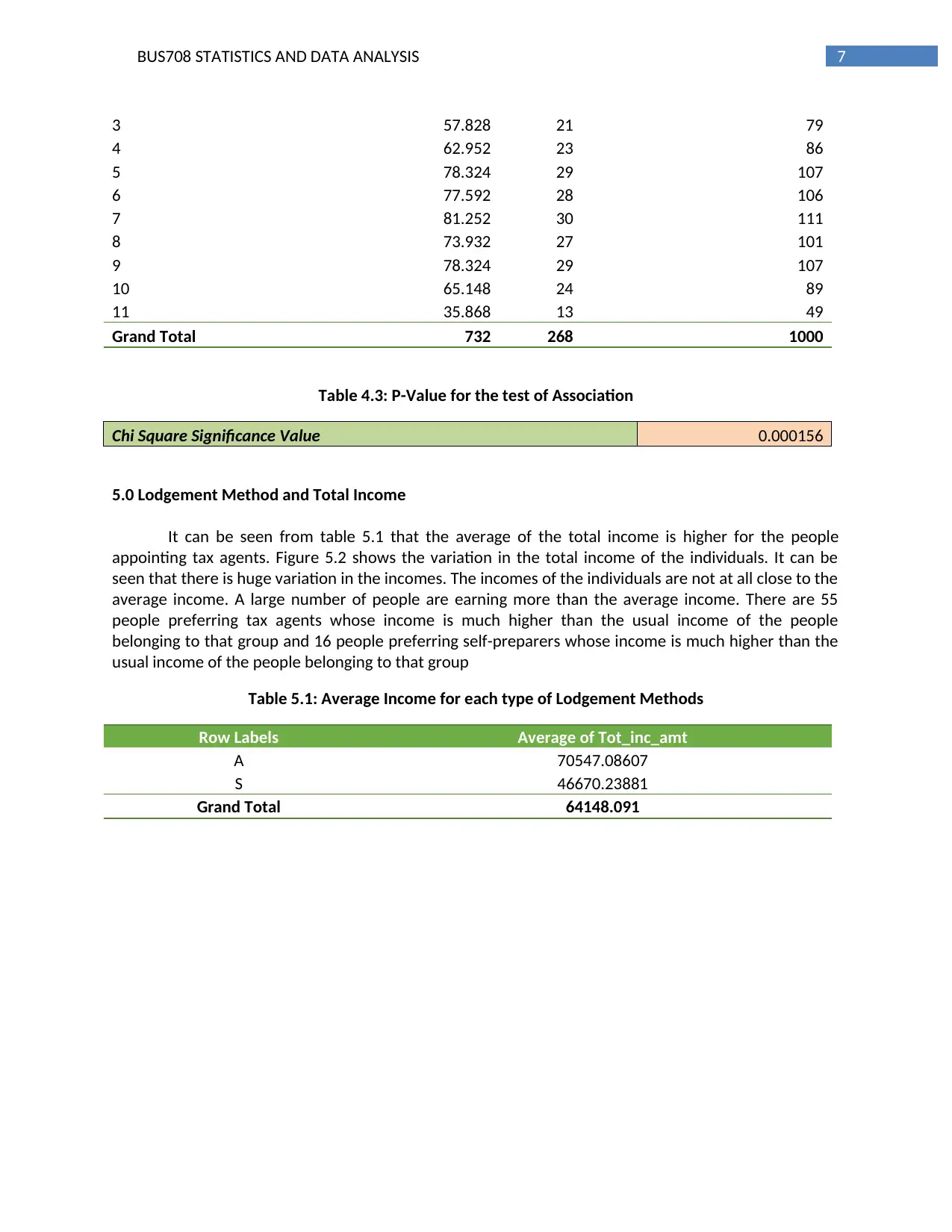

3 57.828 21 79

4 62.952 23 86

5 78.324 29 107

6 77.592 28 106

7 81.252 30 111

8 73.932 27 101

9 78.324 29 107

10 65.148 24 89

11 35.868 13 49

Grand Total 732 268 1000

Table 4.3: P-Value for the test of Association

Chi Square Significance Value 0.000156

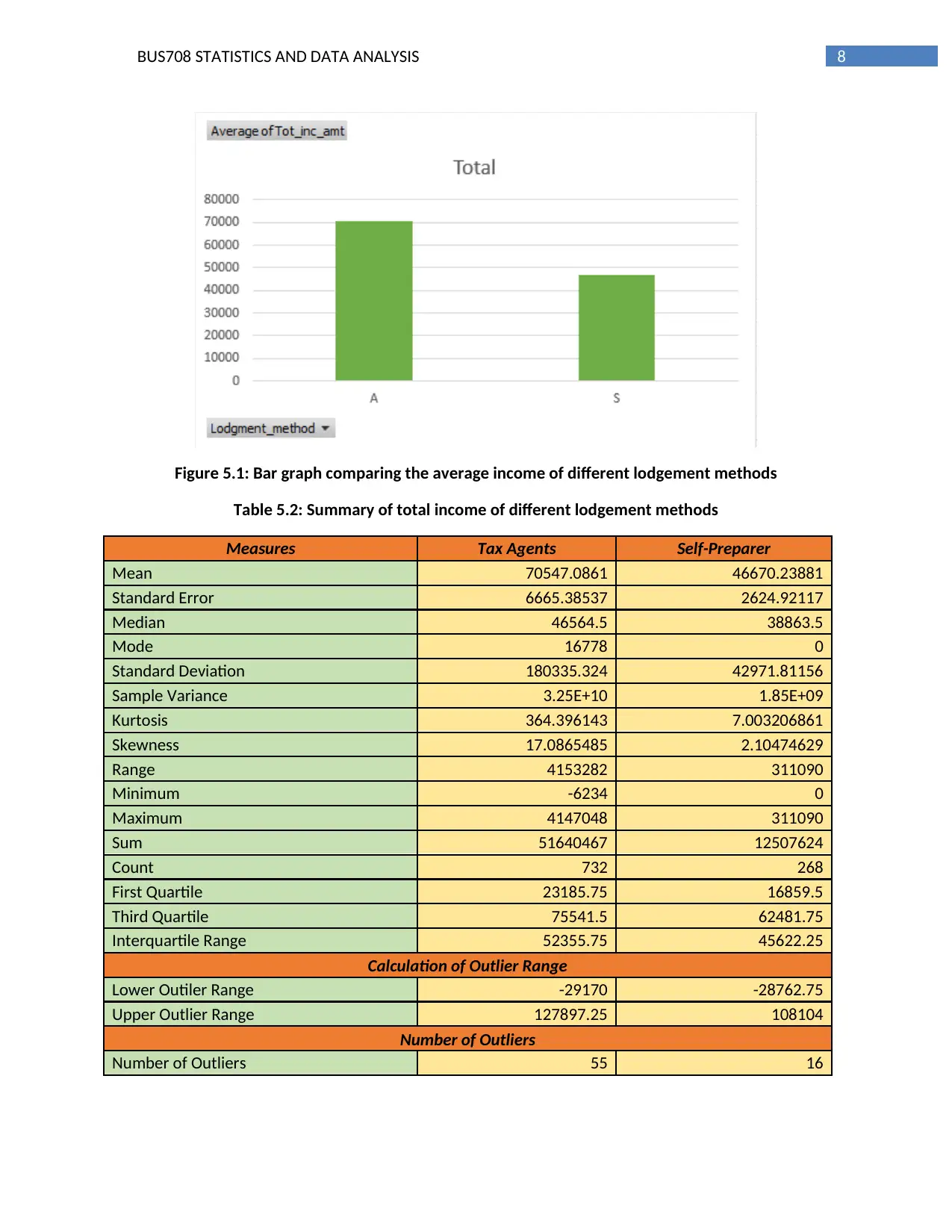

5.0 Lodgement Method and Total Income

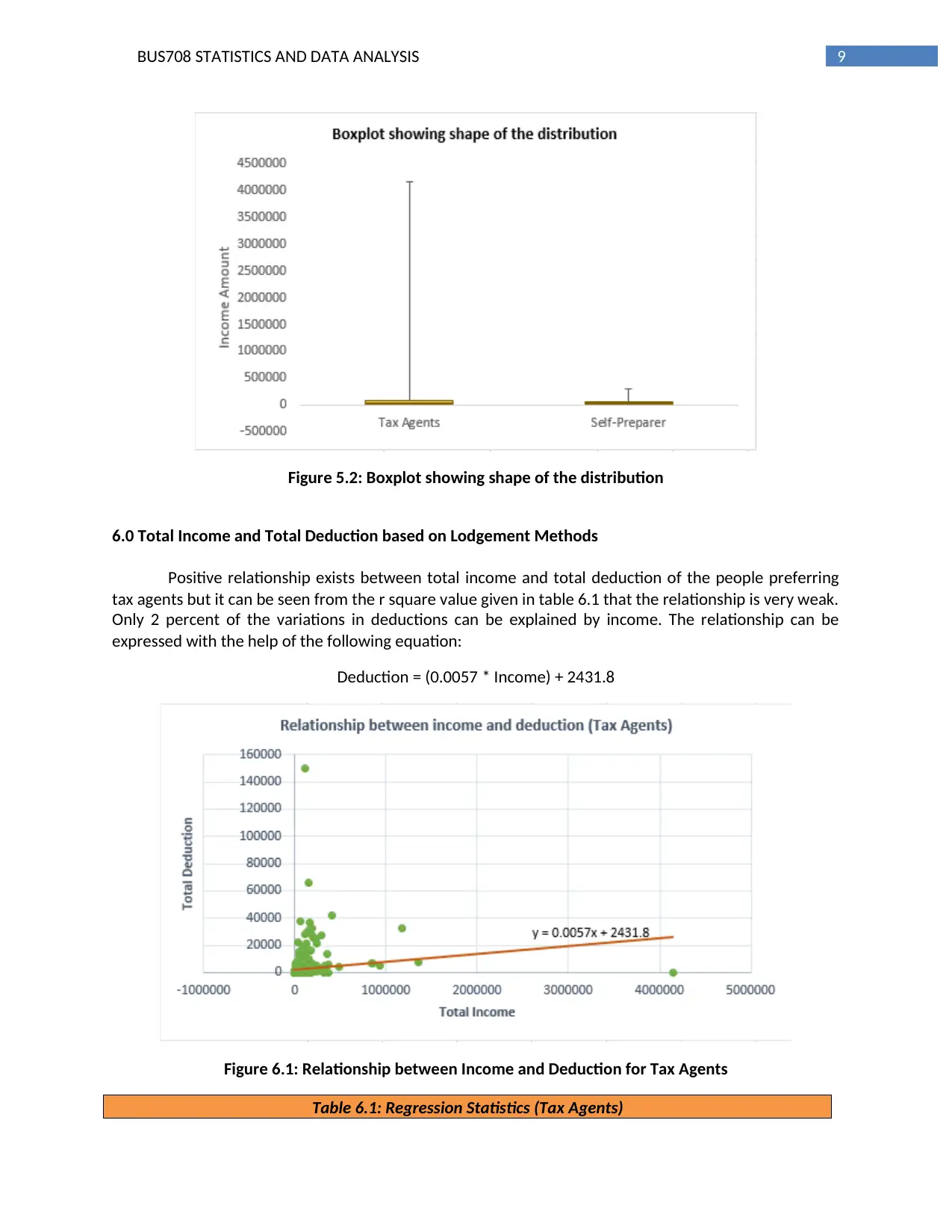

It can be seen from table 5.1 that the average of the total income is higher for the people

appointing tax agents. Figure 5.2 shows the variation in the total income of the individuals. It can be

seen that there is huge variation in the incomes. The incomes of the individuals are not at all close to the

average income. A large number of people are earning more than the average income. There are 55

people preferring tax agents whose income is much higher than the usual income of the people

belonging to that group and 16 people preferring self-preparers whose income is much higher than the

usual income of the people belonging to that group

Table 5.1: Average Income for each type of Lodgement Methods

Row Labels Average of Tot_inc_amt

A 70547.08607

S 46670.23881

Grand Total 64148.091

3 57.828 21 79

4 62.952 23 86

5 78.324 29 107

6 77.592 28 106

7 81.252 30 111

8 73.932 27 101

9 78.324 29 107

10 65.148 24 89

11 35.868 13 49

Grand Total 732 268 1000

Table 4.3: P-Value for the test of Association

Chi Square Significance Value 0.000156

5.0 Lodgement Method and Total Income

It can be seen from table 5.1 that the average of the total income is higher for the people

appointing tax agents. Figure 5.2 shows the variation in the total income of the individuals. It can be

seen that there is huge variation in the incomes. The incomes of the individuals are not at all close to the

average income. A large number of people are earning more than the average income. There are 55

people preferring tax agents whose income is much higher than the usual income of the people

belonging to that group and 16 people preferring self-preparers whose income is much higher than the

usual income of the people belonging to that group

Table 5.1: Average Income for each type of Lodgement Methods

Row Labels Average of Tot_inc_amt

A 70547.08607

S 46670.23881

Grand Total 64148.091

8BUS708 STATISTICS AND DATA ANALYSIS

Figure 5.1: Bar graph comparing the average income of different lodgement methods

Table 5.2: Summary of total income of different lodgement methods

Measures Tax Agents Self-Preparer

Mean 70547.0861 46670.23881

Standard Error 6665.38537 2624.92117

Median 46564.5 38863.5

Mode 16778 0

Standard Deviation 180335.324 42971.81156

Sample Variance 3.25E+10 1.85E+09

Kurtosis 364.396143 7.003206861

Skewness 17.0865485 2.10474629

Range 4153282 311090

Minimum -6234 0

Maximum 4147048 311090

Sum 51640467 12507624

Count 732 268

First Quartile 23185.75 16859.5

Third Quartile 75541.5 62481.75

Interquartile Range 52355.75 45622.25

Calculation of Outlier Range

Lower Outiler Range -29170 -28762.75

Upper Outlier Range 127897.25 108104

Number of Outliers

Number of Outliers 55 16

Figure 5.1: Bar graph comparing the average income of different lodgement methods

Table 5.2: Summary of total income of different lodgement methods

Measures Tax Agents Self-Preparer

Mean 70547.0861 46670.23881

Standard Error 6665.38537 2624.92117

Median 46564.5 38863.5

Mode 16778 0

Standard Deviation 180335.324 42971.81156

Sample Variance 3.25E+10 1.85E+09

Kurtosis 364.396143 7.003206861

Skewness 17.0865485 2.10474629

Range 4153282 311090

Minimum -6234 0

Maximum 4147048 311090

Sum 51640467 12507624

Count 732 268

First Quartile 23185.75 16859.5

Third Quartile 75541.5 62481.75

Interquartile Range 52355.75 45622.25

Calculation of Outlier Range

Lower Outiler Range -29170 -28762.75

Upper Outlier Range 127897.25 108104

Number of Outliers

Number of Outliers 55 16

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

9BUS708 STATISTICS AND DATA ANALYSIS

Figure 5.2: Boxplot showing shape of the distribution

6.0 Total Income and Total Deduction based on Lodgement Methods

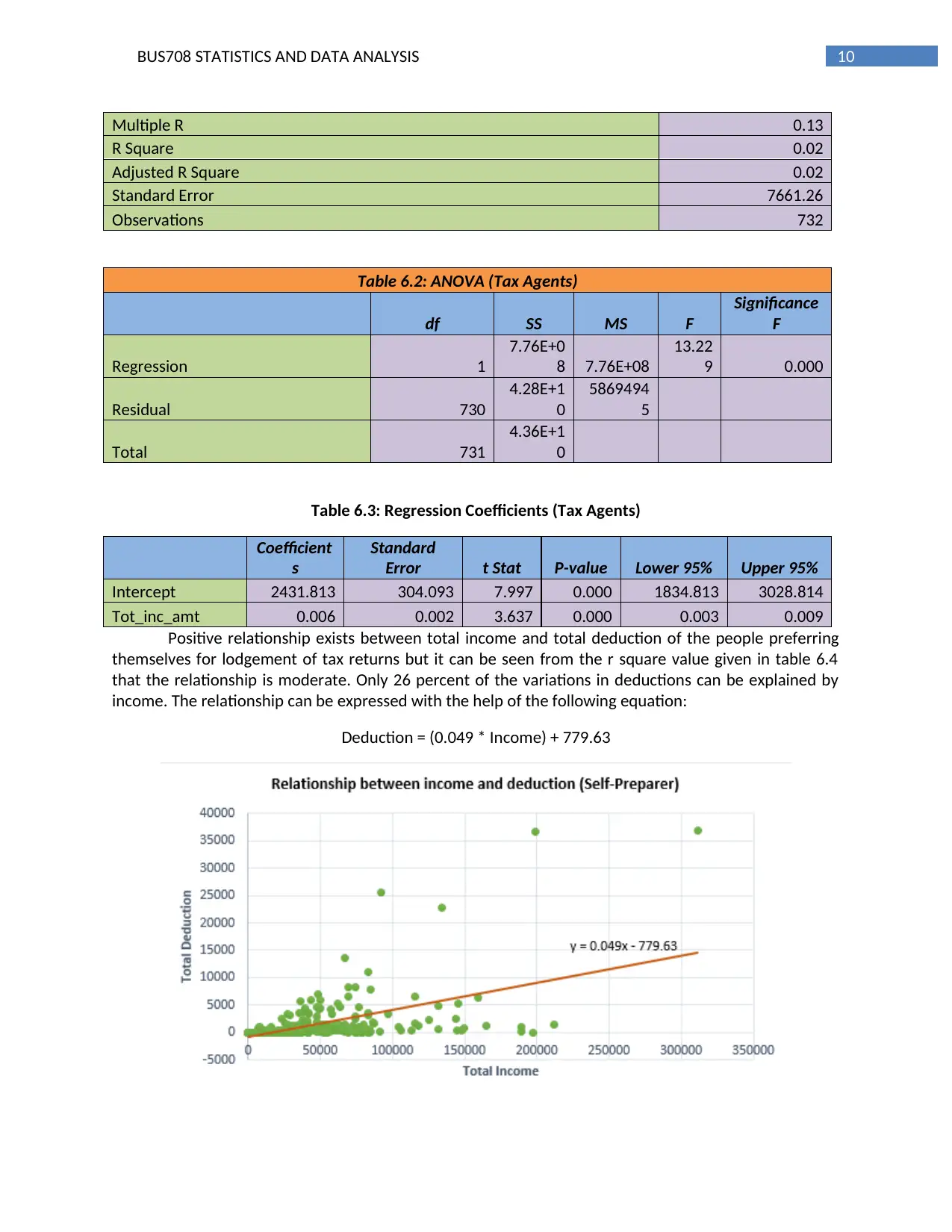

Positive relationship exists between total income and total deduction of the people preferring

tax agents but it can be seen from the r square value given in table 6.1 that the relationship is very weak.

Only 2 percent of the variations in deductions can be explained by income. The relationship can be

expressed with the help of the following equation:

Deduction = (0.0057 * Income) + 2431.8

Figure 6.1: Relationship between Income and Deduction for Tax Agents

Table 6.1: Regression Statistics (Tax Agents)

Figure 5.2: Boxplot showing shape of the distribution

6.0 Total Income and Total Deduction based on Lodgement Methods

Positive relationship exists between total income and total deduction of the people preferring

tax agents but it can be seen from the r square value given in table 6.1 that the relationship is very weak.

Only 2 percent of the variations in deductions can be explained by income. The relationship can be

expressed with the help of the following equation:

Deduction = (0.0057 * Income) + 2431.8

Figure 6.1: Relationship between Income and Deduction for Tax Agents

Table 6.1: Regression Statistics (Tax Agents)

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

10BUS708 STATISTICS AND DATA ANALYSIS

Multiple R 0.13

R Square 0.02

Adjusted R Square 0.02

Standard Error 7661.26

Observations 732

Table 6.2: ANOVA (Tax Agents)

df SS MS F

Significance

F

Regression 1

7.76E+0

8 7.76E+08

13.22

9 0.000

Residual 730

4.28E+1

0

5869494

5

Total 731

4.36E+1

0

Table 6.3: Regression Coefficients (Tax Agents)

Coefficient

s

Standard

Error t Stat P-value Lower 95% Upper 95%

Intercept 2431.813 304.093 7.997 0.000 1834.813 3028.814

Tot_inc_amt 0.006 0.002 3.637 0.000 0.003 0.009

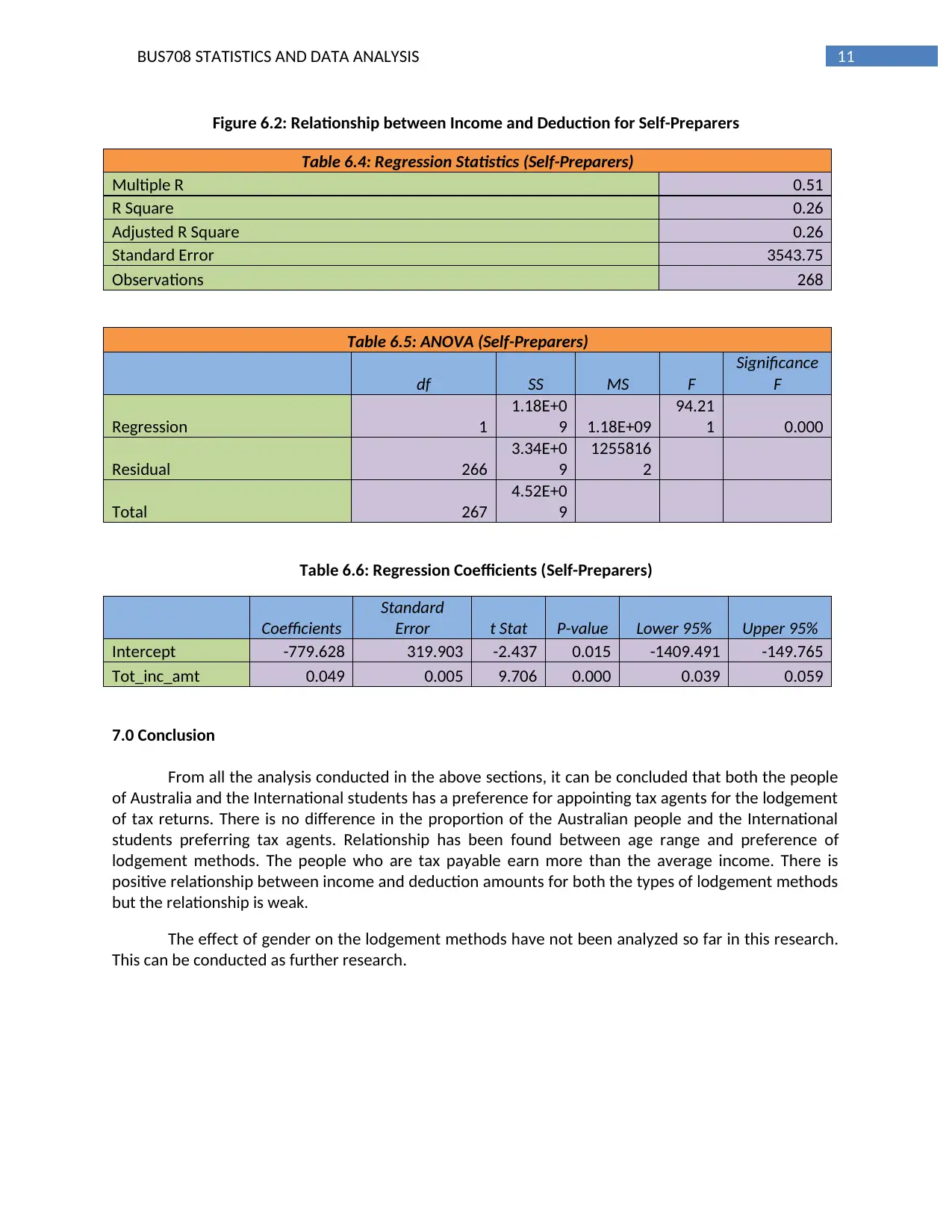

Positive relationship exists between total income and total deduction of the people preferring

themselves for lodgement of tax returns but it can be seen from the r square value given in table 6.4

that the relationship is moderate. Only 26 percent of the variations in deductions can be explained by

income. The relationship can be expressed with the help of the following equation:

Deduction = (0.049 * Income) + 779.63

Multiple R 0.13

R Square 0.02

Adjusted R Square 0.02

Standard Error 7661.26

Observations 732

Table 6.2: ANOVA (Tax Agents)

df SS MS F

Significance

F

Regression 1

7.76E+0

8 7.76E+08

13.22

9 0.000

Residual 730

4.28E+1

0

5869494

5

Total 731

4.36E+1

0

Table 6.3: Regression Coefficients (Tax Agents)

Coefficient

s

Standard

Error t Stat P-value Lower 95% Upper 95%

Intercept 2431.813 304.093 7.997 0.000 1834.813 3028.814

Tot_inc_amt 0.006 0.002 3.637 0.000 0.003 0.009

Positive relationship exists between total income and total deduction of the people preferring

themselves for lodgement of tax returns but it can be seen from the r square value given in table 6.4

that the relationship is moderate. Only 26 percent of the variations in deductions can be explained by

income. The relationship can be expressed with the help of the following equation:

Deduction = (0.049 * Income) + 779.63

11BUS708 STATISTICS AND DATA ANALYSIS

Figure 6.2: Relationship between Income and Deduction for Self-Preparers

Table 6.4: Regression Statistics (Self-Preparers)

Multiple R 0.51

R Square 0.26

Adjusted R Square 0.26

Standard Error 3543.75

Observations 268

Table 6.5: ANOVA (Self-Preparers)

df SS MS F

Significance

F

Regression 1

1.18E+0

9 1.18E+09

94.21

1 0.000

Residual 266

3.34E+0

9

1255816

2

Total 267

4.52E+0

9

Table 6.6: Regression Coefficients (Self-Preparers)

Coefficients

Standard

Error t Stat P-value Lower 95% Upper 95%

Intercept -779.628 319.903 -2.437 0.015 -1409.491 -149.765

Tot_inc_amt 0.049 0.005 9.706 0.000 0.039 0.059

7.0 Conclusion

From all the analysis conducted in the above sections, it can be concluded that both the people

of Australia and the International students has a preference for appointing tax agents for the lodgement

of tax returns. There is no difference in the proportion of the Australian people and the International

students preferring tax agents. Relationship has been found between age range and preference of

lodgement methods. The people who are tax payable earn more than the average income. There is

positive relationship between income and deduction amounts for both the types of lodgement methods

but the relationship is weak.

The effect of gender on the lodgement methods have not been analyzed so far in this research.

This can be conducted as further research.

Figure 6.2: Relationship between Income and Deduction for Self-Preparers

Table 6.4: Regression Statistics (Self-Preparers)

Multiple R 0.51

R Square 0.26

Adjusted R Square 0.26

Standard Error 3543.75

Observations 268

Table 6.5: ANOVA (Self-Preparers)

df SS MS F

Significance

F

Regression 1

1.18E+0

9 1.18E+09

94.21

1 0.000

Residual 266

3.34E+0

9

1255816

2

Total 267

4.52E+0

9

Table 6.6: Regression Coefficients (Self-Preparers)

Coefficients

Standard

Error t Stat P-value Lower 95% Upper 95%

Intercept -779.628 319.903 -2.437 0.015 -1409.491 -149.765

Tot_inc_amt 0.049 0.005 9.706 0.000 0.039 0.059

7.0 Conclusion

From all the analysis conducted in the above sections, it can be concluded that both the people

of Australia and the International students has a preference for appointing tax agents for the lodgement

of tax returns. There is no difference in the proportion of the Australian people and the International

students preferring tax agents. Relationship has been found between age range and preference of

lodgement methods. The people who are tax payable earn more than the average income. There is

positive relationship between income and deduction amounts for both the types of lodgement methods

but the relationship is weak.

The effect of gender on the lodgement methods have not been analyzed so far in this research.

This can be conducted as further research.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 13

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.