Business Decision Making: Investment Appraisal and Performance Ratios

VerifiedAdded on 2023/06/17

|11

|1980

|215

Report

AI Summary

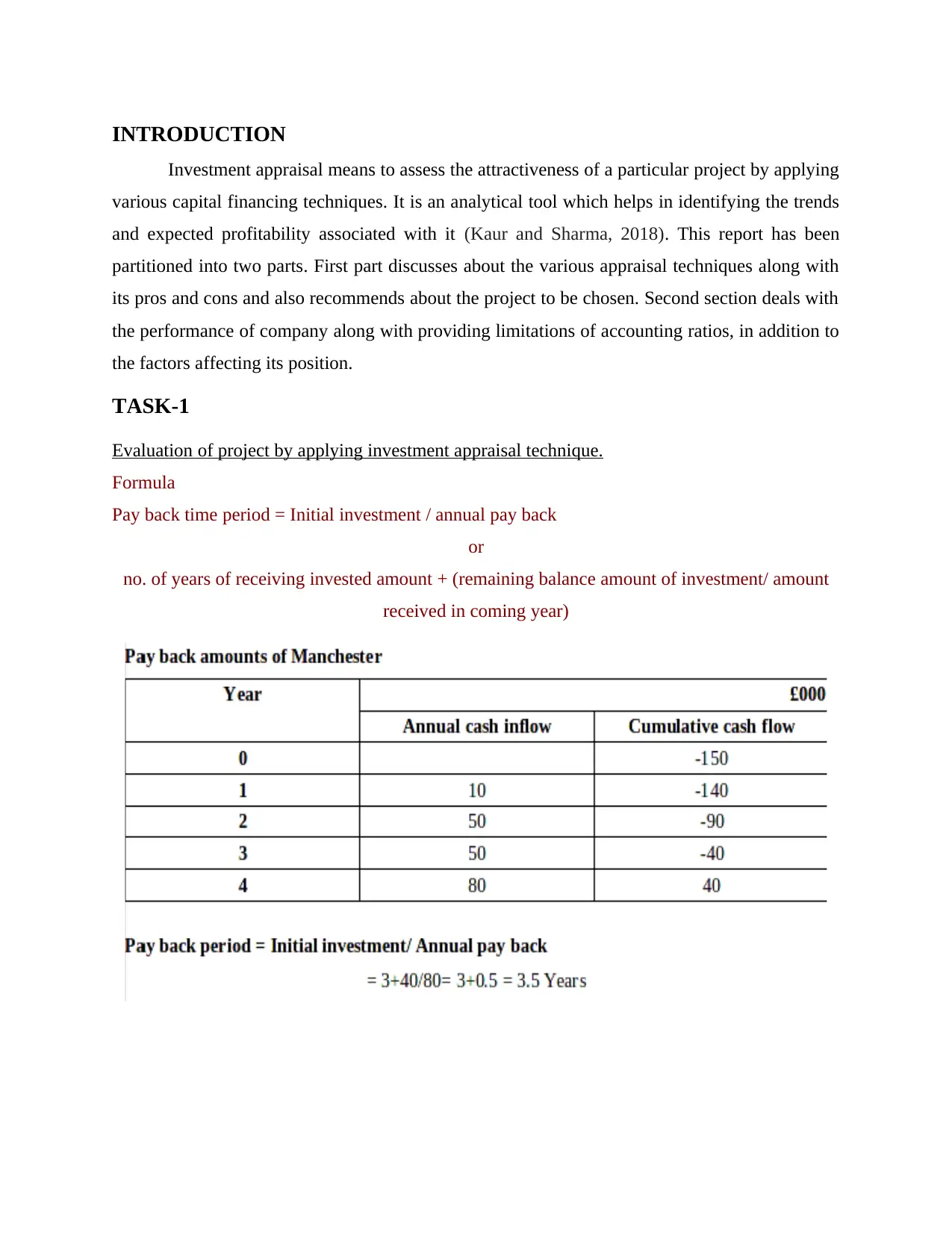

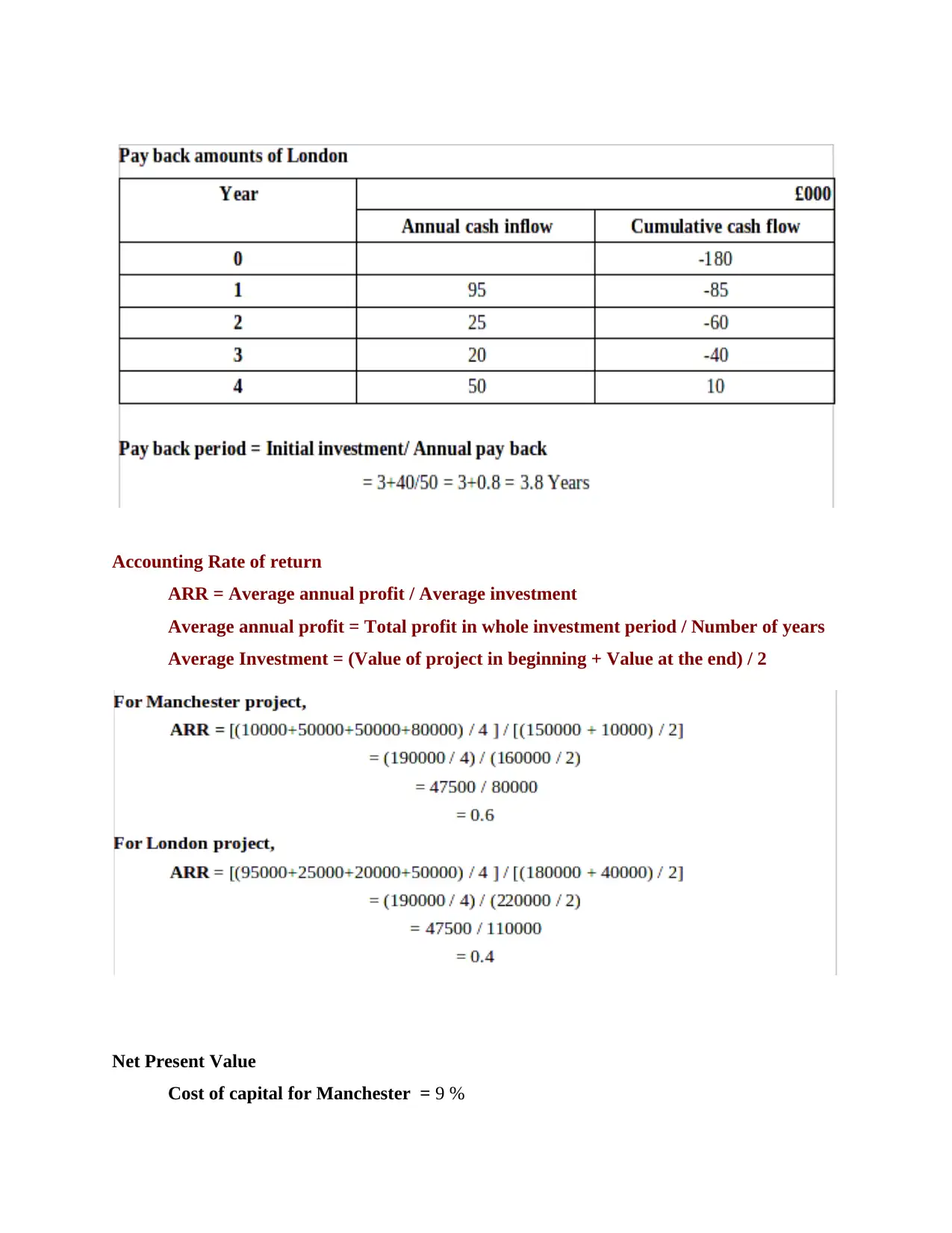

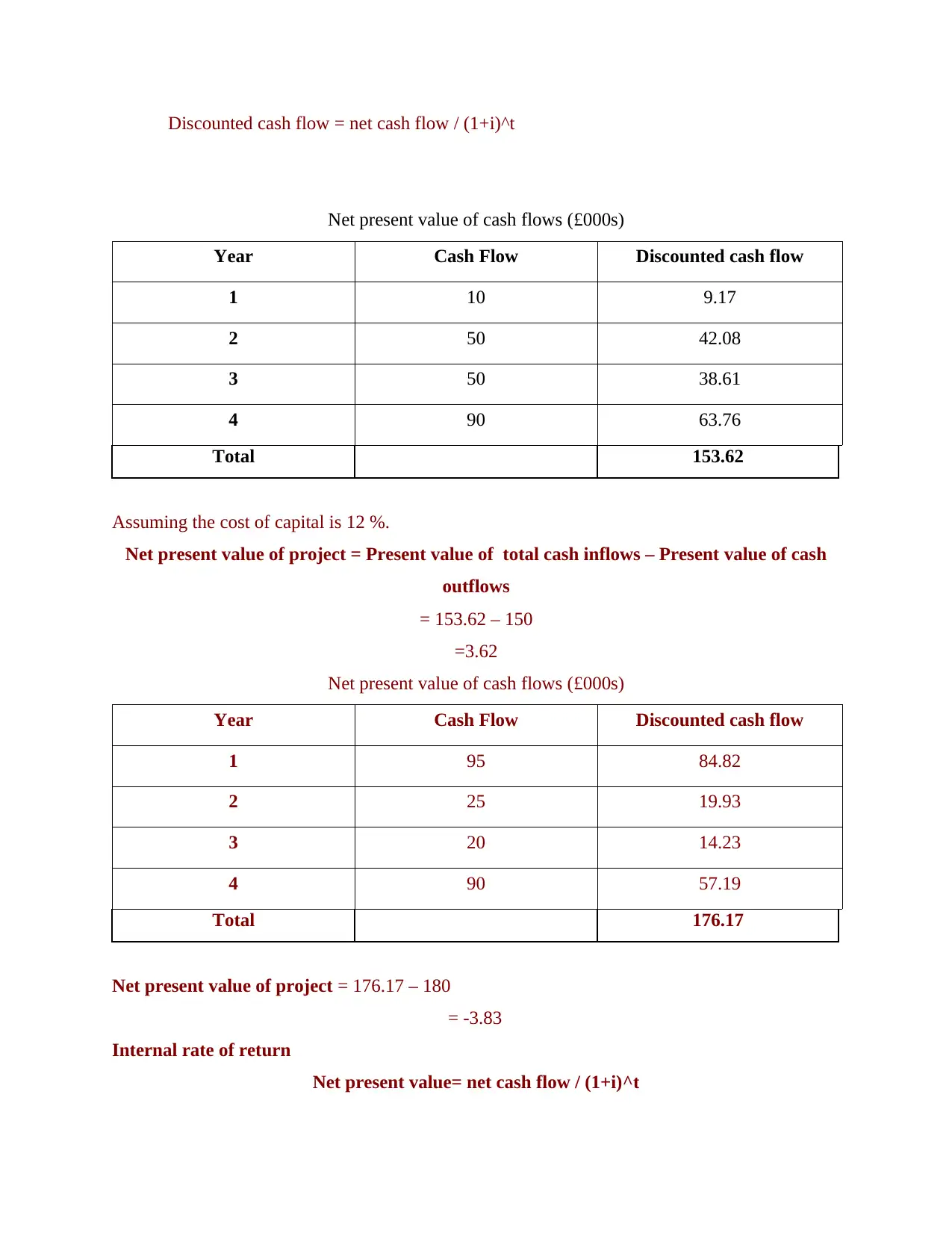

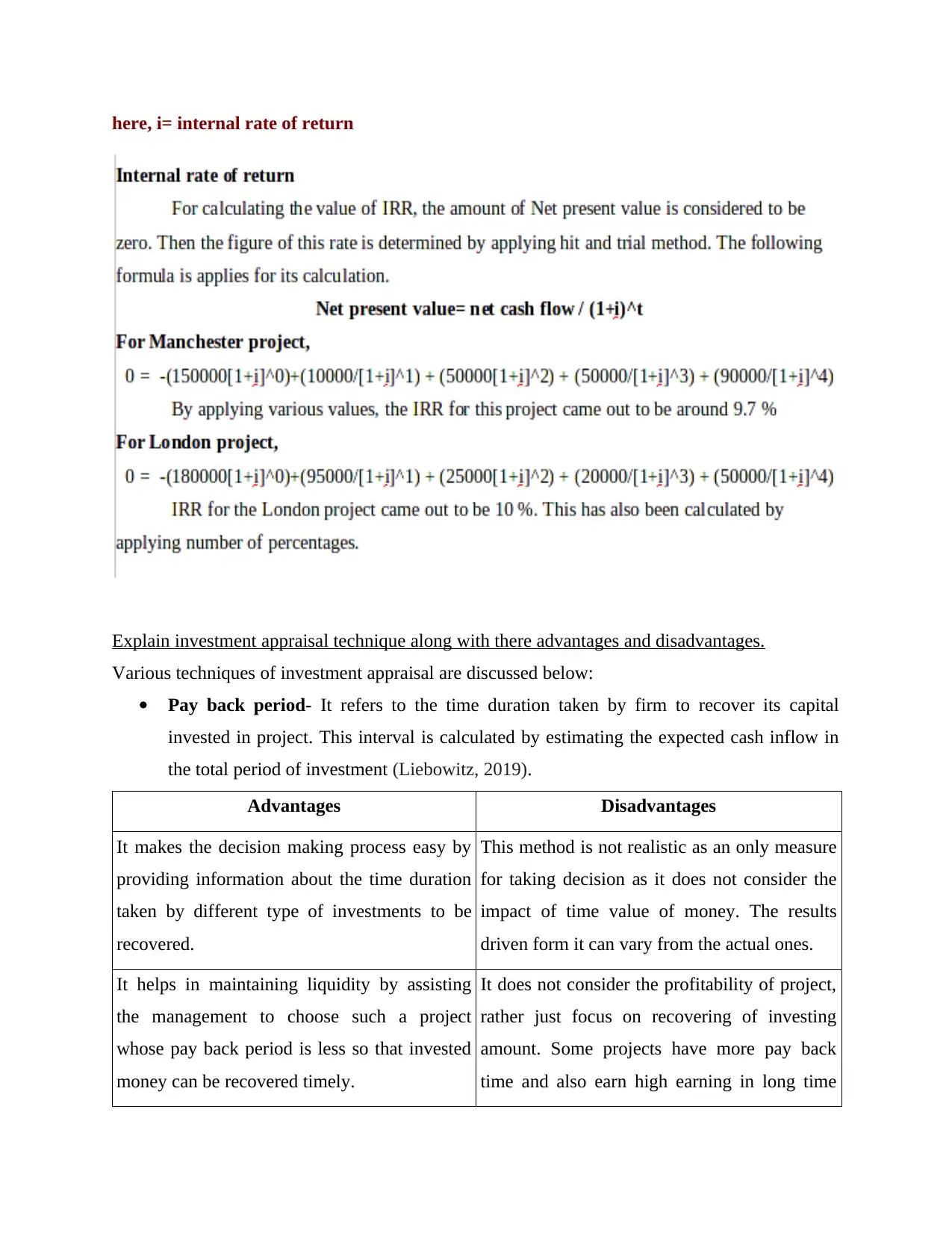

This report provides a comprehensive analysis of business decision-making through investment appraisal techniques and accounting ratios. The first section evaluates project investments using methods like payback period, accounting rate of return, net present value, and internal rate of return, highlighting their advantages and disadvantages, ultimately recommending the Manchester project based on its favorable results. The second section assesses Tesco's performance using accounting ratios, noting its fluctuating return on capital employed and liquidity, while also discussing the limitations of accounting ratios and external factors impacting Tesco's position, such as demand, innovation, and labor costs. The report concludes that while appraisal techniques and accounting ratios have limitations, they are crucial tools for making informed business decisions. Desklib offers a range of similar solved assignments and study resources for students.

1 out of 11

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2025 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.