Investment Portfolio Risk-Return Analysis

VerifiedAdded on 2020/07/22

|21

|2708

|219

AI Summary

This assignment involves evaluating three given investment portfolios using various financial analysis tools such as Sharpe Ratio, Security Market Line (SML), Capital Market Line (CML), and regression analysis. The primary goal is to identify the best portfolio option available to an investor in terms of risk-adjusted return, while also understanding the relationship between these portfolios and their corresponding Sharpe ratios.

Contribute Materials

Your contribution can guide someone’s learning journey. Share your

documents today.

BUSINESS FINANCE

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

EXECUTIVE SUMMARY

Investment is made by all sort of people in terms of income level but making prudent decisions

is very difficult task. In order to take perfect decision some tools and techniques need to be used.

In the present research study index return and firms returns are analyzed by using tools like

mean , standard deviation and beta. It is observed that security markert line is the one of the

important approach that help one in making correct decisions. By comparing requred rate of

return with market return it is identified whether investment must be made in specific security or

not. Beta is another tool that must be widely used in order to meausre risk and to make

decisions. Thus, investors must not rely on single approach as they must use multiple methods to

take investment decisions.

Investment is made by all sort of people in terms of income level but making prudent decisions

is very difficult task. In order to take perfect decision some tools and techniques need to be used.

In the present research study index return and firms returns are analyzed by using tools like

mean , standard deviation and beta. It is observed that security markert line is the one of the

important approach that help one in making correct decisions. By comparing requred rate of

return with market return it is identified whether investment must be made in specific security or

not. Beta is another tool that must be widely used in order to meausre risk and to make

decisions. Thus, investors must not rely on single approach as they must use multiple methods to

take investment decisions.

TABLE OF CONTENTS

INTRODUCTION...........................................................................................................................1

REQUIRED.....................................................................................................................................1

(1)Monthly return series of stocks and index..............................................................................1

(2)Portolio construction...............................................................................................................1

(3) Mean return and standard deviation of stock, index and portfolio........................................2

(4) Regression analysis................................................................................................................3

(3) Beta estimates of portfolio...................................................................................................12

5 Combination line chart...........................................................................................................24

ANALYSIS....................................................................................................................................24

(1)Performance of market and six stocks..................................................................................24

(2) Comparison of portfolios.....................................................................................................25

(3) Relationship between sharpe ratio portfolio 3,2 and chart ploted in 5th point.....................25

(4) SML and CML.....................................................................................................................25

5 Discussion on calculations......................................................................................................26

CONCLUSION..............................................................................................................................26

REFERENCES..............................................................................................................................27

Figure 1Mean and standard deviation chart...................................................................................13

Figure 2Mean and beta chart.........................................................................................................13

Figure 3Mean and standard deviation chart...................................................................................14

Figure 4Mean and beta chart.........................................................................................................14

Figure 5Mean and standard deviation chart...................................................................................15

Figure 6Mean and beta chart.........................................................................................................15

Figure 7Mean and standard deviation chart...................................................................................16

Figure 8Mean and beta chart.........................................................................................................16

Figure 9Mean and standard deviation chart...................................................................................17

INTRODUCTION...........................................................................................................................1

REQUIRED.....................................................................................................................................1

(1)Monthly return series of stocks and index..............................................................................1

(2)Portolio construction...............................................................................................................1

(3) Mean return and standard deviation of stock, index and portfolio........................................2

(4) Regression analysis................................................................................................................3

(3) Beta estimates of portfolio...................................................................................................12

5 Combination line chart...........................................................................................................24

ANALYSIS....................................................................................................................................24

(1)Performance of market and six stocks..................................................................................24

(2) Comparison of portfolios.....................................................................................................25

(3) Relationship between sharpe ratio portfolio 3,2 and chart ploted in 5th point.....................25

(4) SML and CML.....................................................................................................................25

5 Discussion on calculations......................................................................................................26

CONCLUSION..............................................................................................................................26

REFERENCES..............................................................................................................................27

Figure 1Mean and standard deviation chart...................................................................................13

Figure 2Mean and beta chart.........................................................................................................13

Figure 3Mean and standard deviation chart...................................................................................14

Figure 4Mean and beta chart.........................................................................................................14

Figure 5Mean and standard deviation chart...................................................................................15

Figure 6Mean and beta chart.........................................................................................................15

Figure 7Mean and standard deviation chart...................................................................................16

Figure 8Mean and beta chart.........................................................................................................16

Figure 9Mean and standard deviation chart...................................................................................17

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

Figure 10Mean and beta chart.......................................................................................................17

Figure 11Mean and standard deviation chart.................................................................................18

Figure 12Mean and beta chart.......................................................................................................18

Figure 13Mean and standard deviation chart.................................................................................19

Figure 14Mean and beta chart.......................................................................................................19

Figure 15Mean and standard deviation chart.................................................................................20

Figure 16Mean and beta chart.......................................................................................................20

Figure 17Mean and standard deviation chart.................................................................................21

Figure 18Mean and beta chart.......................................................................................................21

Figure 19Mean and standard deviation chart.................................................................................22

Figure 20Mean and beta chart.......................................................................................................22

Figure 21Mean and standard deviation chart.................................................................................23

Figure 22Mean and beta chart.......................................................................................................23

Figure 23Combination chart..........................................................................................................24

Figure 24SML chart.......................................................................................................................25

Figure 25CML chart......................................................................................................................26

Table 1Return profile of index and shares.......................................................................................1

Table 2Portfolio 1............................................................................................................................1

Table 3Portfolio 2............................................................................................................................2

Table 4Portfolio 3............................................................................................................................2

Table 5Portfolio 1mean and standard deviation..............................................................................3

Table 6Portfolio 2 mean and standard deviation.............................................................................3

Table 7Portfolio 3 mean and standard deviation.............................................................................3

Table 8Calculation of beta.............................................................................................................12

Figure 11Mean and standard deviation chart.................................................................................18

Figure 12Mean and beta chart.......................................................................................................18

Figure 13Mean and standard deviation chart.................................................................................19

Figure 14Mean and beta chart.......................................................................................................19

Figure 15Mean and standard deviation chart.................................................................................20

Figure 16Mean and beta chart.......................................................................................................20

Figure 17Mean and standard deviation chart.................................................................................21

Figure 18Mean and beta chart.......................................................................................................21

Figure 19Mean and standard deviation chart.................................................................................22

Figure 20Mean and beta chart.......................................................................................................22

Figure 21Mean and standard deviation chart.................................................................................23

Figure 22Mean and beta chart.......................................................................................................23

Figure 23Combination chart..........................................................................................................24

Figure 24SML chart.......................................................................................................................25

Figure 25CML chart......................................................................................................................26

Table 1Return profile of index and shares.......................................................................................1

Table 2Portfolio 1............................................................................................................................1

Table 3Portfolio 2............................................................................................................................2

Table 4Portfolio 3............................................................................................................................2

Table 5Portfolio 1mean and standard deviation..............................................................................3

Table 6Portfolio 2 mean and standard deviation.............................................................................3

Table 7Portfolio 3 mean and standard deviation.............................................................................3

Table 8Calculation of beta.............................................................................................................12

INTRODUCTION

Investment is one of the important area that is related to every human being whether it

comes in upper or middle classs. There are number of tools and techniques that need to be used

in order to make prudent decisions. In current report, portfolios are created and varied tools are

used like beta and standard deviation, CML and SML for evaluating stocks and identifying

varied facts. In second part of report all results are discussed and in this way entire research work

is done.

REQUIRED

Introduction to firms ANZ: ANZ is also known by name Australia and New Zealand Banking group as it is one

of the largest bank of Australia in terms of market capitalization. Currently, firm is

offering number of products to its customers whether they are retail or HNI. Firm have its

own future plans and have good growth prospects. BHP: BHP is one of well known firm that is operating in mines, metals and petroleum

products. It is Australia largest mining company in terms of turnover. Presently, firm is

operating its business in number of nations of world and have good growth rate in

business. CSL: It is a company operating in biotechnology field. There are number of areas in this

field and CSL is operating streams from where good amount of cash flow can be

received. Firm product portfolio is wide and also provide good quality of services to

customers. FMG: It is largest iron ore company and is considered as one of the largest iron mineral

marker in the world. FMG is considered as greater in size in comparison to rivals Rio

Tinto and BHP. FMG have USP which make it different from rivals. WOW: It is a retail firm that is operating in both Australia and New Zelanad. Firm is

consistently opening new branches in foreign nations and is earning good amount of

revenue in the business. Thus, it can be said that with improvement in global economy

good profit will be earned by the firm.

(1)Monthly return series of stocks and index

Table 1Return profile of index and shares

Compan Return

1 | P a g e

Investment is one of the important area that is related to every human being whether it

comes in upper or middle classs. There are number of tools and techniques that need to be used

in order to make prudent decisions. In current report, portfolios are created and varied tools are

used like beta and standard deviation, CML and SML for evaluating stocks and identifying

varied facts. In second part of report all results are discussed and in this way entire research work

is done.

REQUIRED

Introduction to firms ANZ: ANZ is also known by name Australia and New Zealand Banking group as it is one

of the largest bank of Australia in terms of market capitalization. Currently, firm is

offering number of products to its customers whether they are retail or HNI. Firm have its

own future plans and have good growth prospects. BHP: BHP is one of well known firm that is operating in mines, metals and petroleum

products. It is Australia largest mining company in terms of turnover. Presently, firm is

operating its business in number of nations of world and have good growth rate in

business. CSL: It is a company operating in biotechnology field. There are number of areas in this

field and CSL is operating streams from where good amount of cash flow can be

received. Firm product portfolio is wide and also provide good quality of services to

customers. FMG: It is largest iron ore company and is considered as one of the largest iron mineral

marker in the world. FMG is considered as greater in size in comparison to rivals Rio

Tinto and BHP. FMG have USP which make it different from rivals. WOW: It is a retail firm that is operating in both Australia and New Zelanad. Firm is

consistently opening new branches in foreign nations and is earning good amount of

revenue in the business. Thus, it can be said that with improvement in global economy

good profit will be earned by the firm.

(1)Monthly return series of stocks and index

Table 1Return profile of index and shares

Compan Return

1 | P a g e

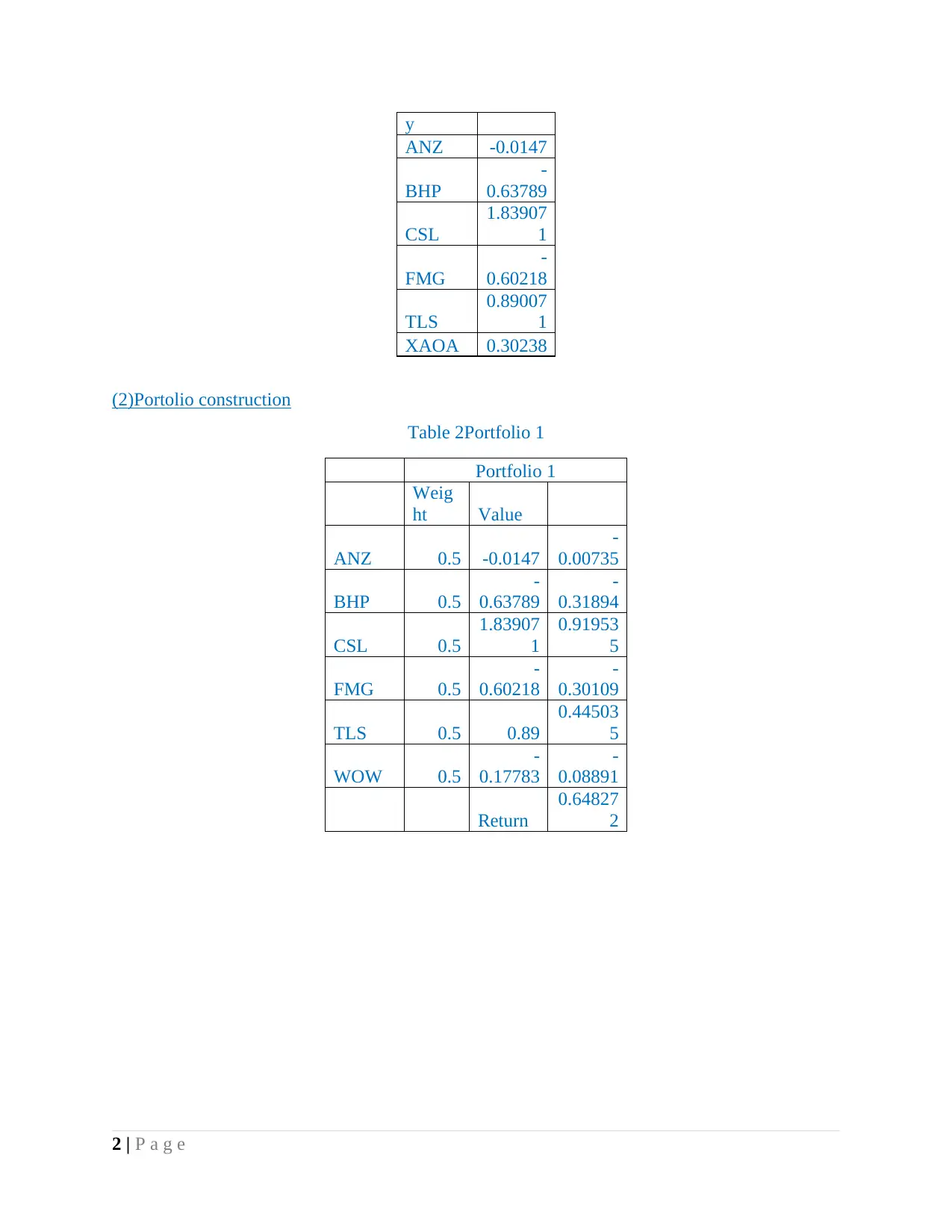

y

ANZ -0.0147

BHP

-

0.63789

CSL

1.83907

1

FMG

-

0.60218

TLS

0.89007

1

XAOA 0.30238

(2)Portolio construction

Table 2Portfolio 1

Portfolio 1

Weig

ht Value

ANZ 0.5 -0.0147

-

0.00735

BHP 0.5

-

0.63789

-

0.31894

CSL 0.5

1.83907

1

0.91953

5

FMG 0.5

-

0.60218

-

0.30109

TLS 0.5 0.89

0.44503

5

WOW 0.5

-

0.17783

-

0.08891

Return

0.64827

2

2 | P a g e

ANZ -0.0147

BHP

-

0.63789

CSL

1.83907

1

FMG

-

0.60218

TLS

0.89007

1

XAOA 0.30238

(2)Portolio construction

Table 2Portfolio 1

Portfolio 1

Weig

ht Value

ANZ 0.5 -0.0147

-

0.00735

BHP 0.5

-

0.63789

-

0.31894

CSL 0.5

1.83907

1

0.91953

5

FMG 0.5

-

0.60218

-

0.30109

TLS 0.5 0.89

0.44503

5

WOW 0.5

-

0.17783

-

0.08891

Return

0.64827

2

2 | P a g e

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Mean STDEV

0

0.1

0.2

0.3

0.4

0.5

0.6

0.10804532988083

5

0.48454103502003

6

Chart Title

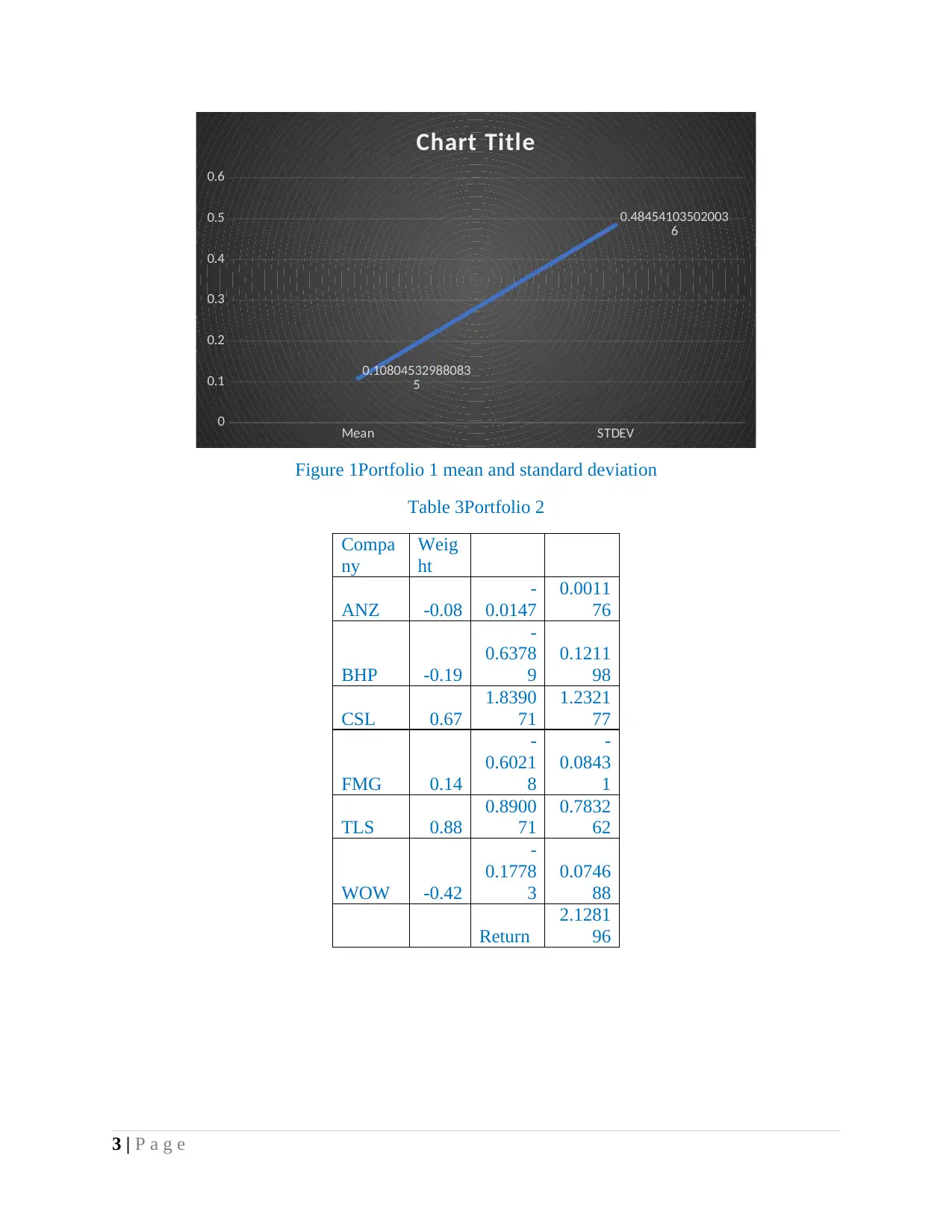

Figure 1Portfolio 1 mean and standard deviation

Table 3Portfolio 2

Compa

ny

Weig

ht

ANZ -0.08

-

0.0147

0.0011

76

BHP -0.19

-

0.6378

9

0.1211

98

CSL 0.67

1.8390

71

1.2321

77

FMG 0.14

-

0.6021

8

-

0.0843

1

TLS 0.88

0.8900

71

0.7832

62

WOW -0.42

-

0.1778

3

0.0746

88

Return

2.1281

96

3 | P a g e

0

0.1

0.2

0.3

0.4

0.5

0.6

0.10804532988083

5

0.48454103502003

6

Chart Title

Figure 1Portfolio 1 mean and standard deviation

Table 3Portfolio 2

Compa

ny

Weig

ht

ANZ -0.08

-

0.0147

0.0011

76

BHP -0.19

-

0.6378

9

0.1211

98

CSL 0.67

1.8390

71

1.2321

77

FMG 0.14

-

0.6021

8

-

0.0843

1

TLS 0.88

0.8900

71

0.7832

62

WOW -0.42

-

0.1778

3

0.0746

88

Return

2.1281

96

3 | P a g e

1 2

0

0.005

0.01

0.015

0.02

0.025

0.03

0.035

0.04

0.045

0.05

0.02504536555704

98

0.04502188619066

27

Chart Title

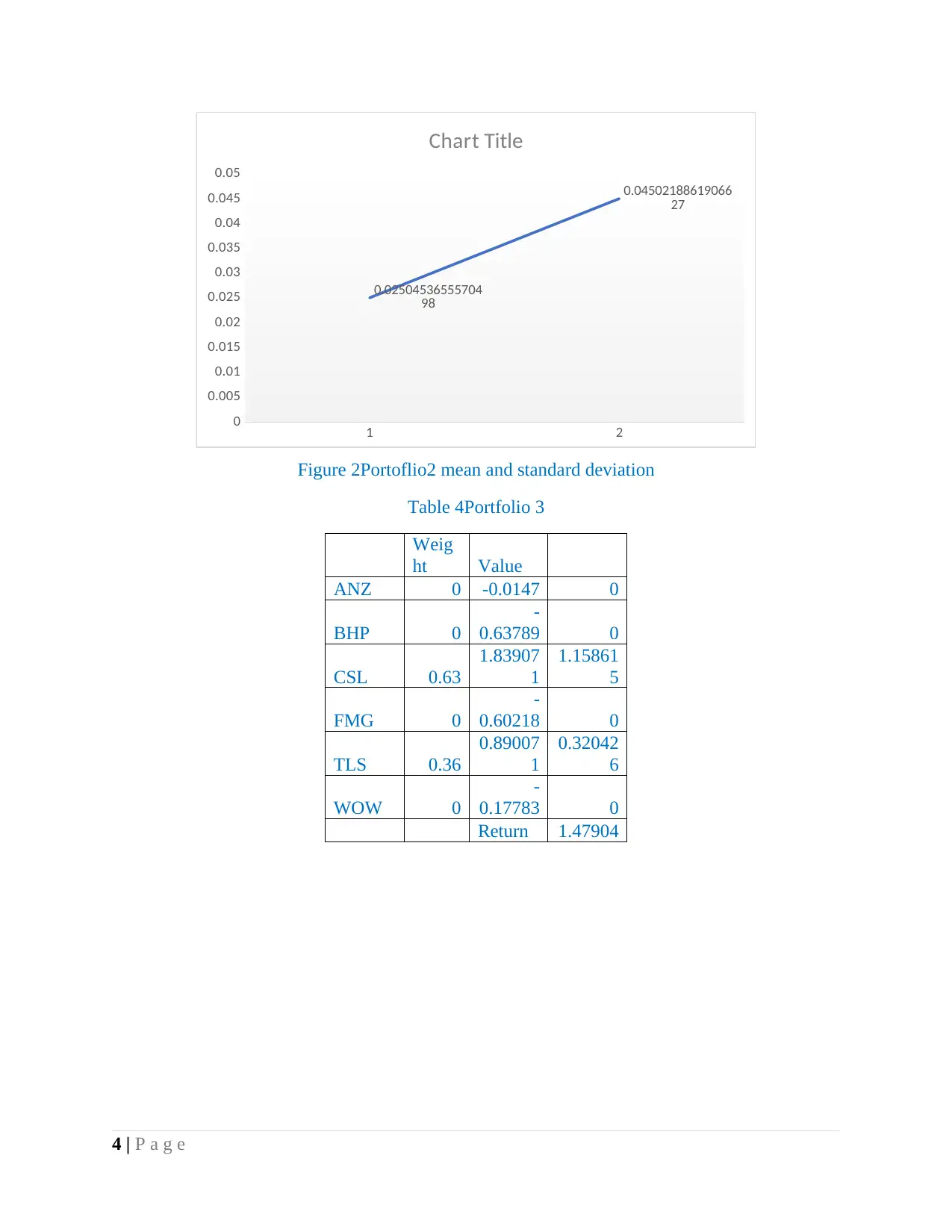

Figure 2Portoflio2 mean and standard deviation

Table 4Portfolio 3

Weig

ht Value

ANZ 0 -0.0147 0

BHP 0

-

0.63789 0

CSL 0.63

1.83907

1

1.15861

5

FMG 0

-

0.60218 0

TLS 0.36

0.89007

1

0.32042

6

WOW 0

-

0.17783 0

Return 1.47904

4 | P a g e

0

0.005

0.01

0.015

0.02

0.025

0.03

0.035

0.04

0.045

0.05

0.02504536555704

98

0.04502188619066

27

Chart Title

Figure 2Portoflio2 mean and standard deviation

Table 4Portfolio 3

Weig

ht Value

ANZ 0 -0.0147 0

BHP 0

-

0.63789 0

CSL 0.63

1.83907

1

1.15861

5

FMG 0

-

0.60218 0

TLS 0.36

0.89007

1

0.32042

6

WOW 0

-

0.17783 0

Return 1.47904

4 | P a g e

1 2

0.01608831666834

97

0.03953822865183

99

Chart Title

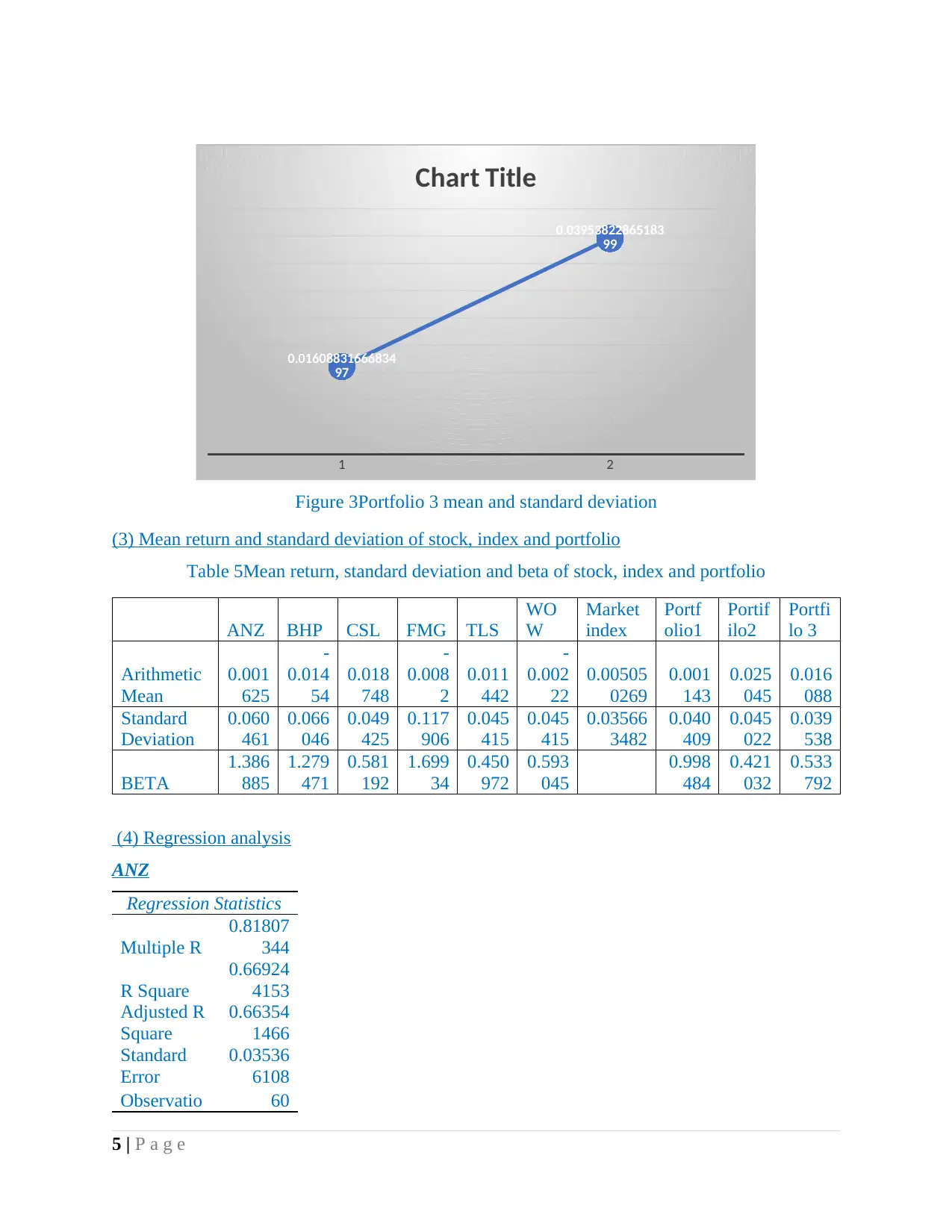

Figure 3Portfolio 3 mean and standard deviation

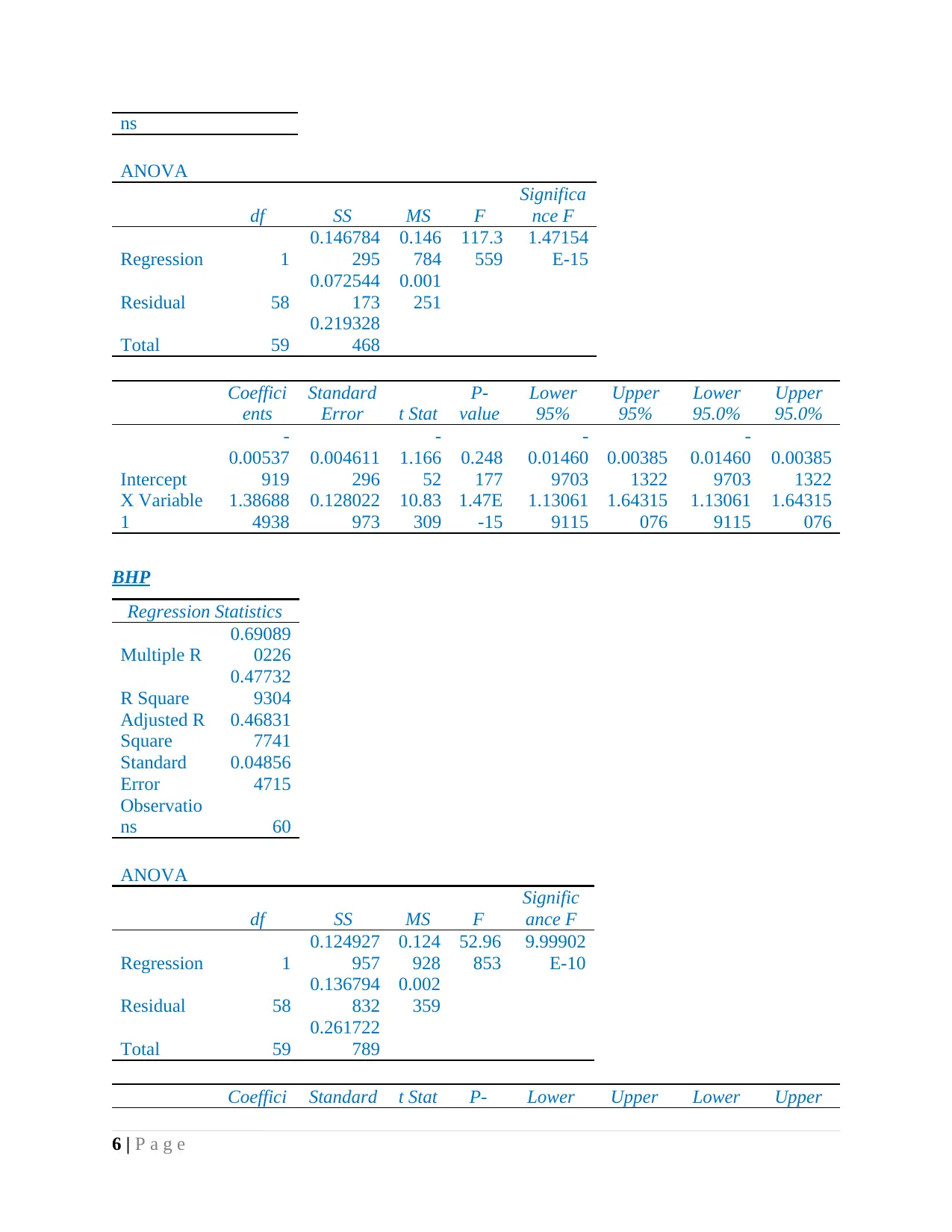

(3) Mean return and standard deviation of stock, index and portfolio

Table 5Mean return, standard deviation and beta of stock, index and portfolio

ANZ BHP CSL FMG TLS

WO

W

Market

index

Portf

olio1

Portif

ilo2

Portfi

lo 3

Arithmetic

Mean

0.001

625

-

0.014

54

0.018

748

-

0.008

2

0.011

442

-

0.002

22

0.00505

0269

0.001

143

0.025

045

0.016

088

Standard

Deviation

0.060

461

0.066

046

0.049

425

0.117

906

0.045

415

0.045

415

0.03566

3482

0.040

409

0.045

022

0.039

538

BETA

1.386

885

1.279

471

0.581

192

1.699

34

0.450

972

0.593

045

0.998

484

0.421

032

0.533

792

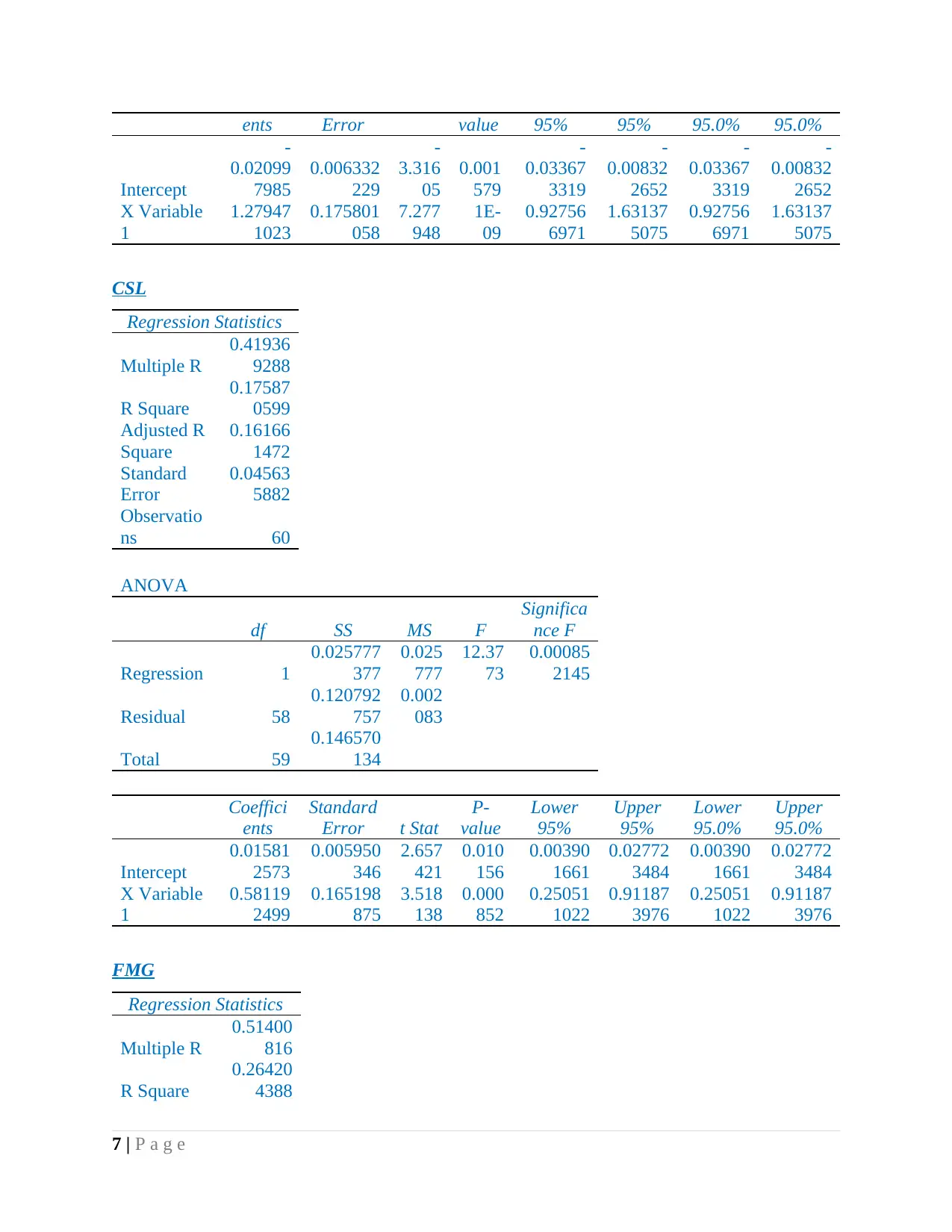

(4) Regression analysis

ANZ

Regression Statistics

Multiple R

0.81807

344

R Square

0.66924

4153

Adjusted R

Square

0.66354

1466

Standard

Error

0.03536

6108

Observatio 60

5 | P a g e

0.01608831666834

97

0.03953822865183

99

Chart Title

Figure 3Portfolio 3 mean and standard deviation

(3) Mean return and standard deviation of stock, index and portfolio

Table 5Mean return, standard deviation and beta of stock, index and portfolio

ANZ BHP CSL FMG TLS

WO

W

Market

index

Portf

olio1

Portif

ilo2

Portfi

lo 3

Arithmetic

Mean

0.001

625

-

0.014

54

0.018

748

-

0.008

2

0.011

442

-

0.002

22

0.00505

0269

0.001

143

0.025

045

0.016

088

Standard

Deviation

0.060

461

0.066

046

0.049

425

0.117

906

0.045

415

0.045

415

0.03566

3482

0.040

409

0.045

022

0.039

538

BETA

1.386

885

1.279

471

0.581

192

1.699

34

0.450

972

0.593

045

0.998

484

0.421

032

0.533

792

(4) Regression analysis

ANZ

Regression Statistics

Multiple R

0.81807

344

R Square

0.66924

4153

Adjusted R

Square

0.66354

1466

Standard

Error

0.03536

6108

Observatio 60

5 | P a g e

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

ns

ANOVA

df SS MS F

Significa

nce F

Regression 1

0.146784

295

0.146

784

117.3

559

1.47154

E-15

Residual 58

0.072544

173

0.001

251

Total 59

0.219328

468

Coeffici

ents

Standard

Error t Stat

P-

value

Lower

95%

Upper

95%

Lower

95.0%

Upper

95.0%

Intercept

-

0.00537

919

0.004611

296

-

1.166

52

0.248

177

-

0.01460

9703

0.00385

1322

-

0.01460

9703

0.00385

1322

X Variable

1

1.38688

4938

0.128022

973

10.83

309

1.47E

-15

1.13061

9115

1.64315

076

1.13061

9115

1.64315

076

BHP

Regression Statistics

Multiple R

0.69089

0226

R Square

0.47732

9304

Adjusted R

Square

0.46831

7741

Standard

Error

0.04856

4715

Observatio

ns 60

ANOVA

df SS MS F

Signific

ance F

Regression 1

0.124927

957

0.124

928

52.96

853

9.99902

E-10

Residual 58

0.136794

832

0.002

359

Total 59

0.261722

789

Coeffici Standard t Stat P- Lower Upper Lower Upper

6 | P a g e

ANOVA

df SS MS F

Significa

nce F

Regression 1

0.146784

295

0.146

784

117.3

559

1.47154

E-15

Residual 58

0.072544

173

0.001

251

Total 59

0.219328

468

Coeffici

ents

Standard

Error t Stat

P-

value

Lower

95%

Upper

95%

Lower

95.0%

Upper

95.0%

Intercept

-

0.00537

919

0.004611

296

-

1.166

52

0.248

177

-

0.01460

9703

0.00385

1322

-

0.01460

9703

0.00385

1322

X Variable

1

1.38688

4938

0.128022

973

10.83

309

1.47E

-15

1.13061

9115

1.64315

076

1.13061

9115

1.64315

076

BHP

Regression Statistics

Multiple R

0.69089

0226

R Square

0.47732

9304

Adjusted R

Square

0.46831

7741

Standard

Error

0.04856

4715

Observatio

ns 60

ANOVA

df SS MS F

Signific

ance F

Regression 1

0.124927

957

0.124

928

52.96

853

9.99902

E-10

Residual 58

0.136794

832

0.002

359

Total 59

0.261722

789

Coeffici Standard t Stat P- Lower Upper Lower Upper

6 | P a g e

ents Error value 95% 95% 95.0% 95.0%

Intercept

-

0.02099

7985

0.006332

229

-

3.316

05

0.001

579

-

0.03367

3319

-

0.00832

2652

-

0.03367

3319

-

0.00832

2652

X Variable

1

1.27947

1023

0.175801

058

7.277

948

1E-

09

0.92756

6971

1.63137

5075

0.92756

6971

1.63137

5075

CSL

Regression Statistics

Multiple R

0.41936

9288

R Square

0.17587

0599

Adjusted R

Square

0.16166

1472

Standard

Error

0.04563

5882

Observatio

ns 60

ANOVA

df SS MS F

Significa

nce F

Regression 1

0.025777

377

0.025

777

12.37

73

0.00085

2145

Residual 58

0.120792

757

0.002

083

Total 59

0.146570

134

Coeffici

ents

Standard

Error t Stat

P-

value

Lower

95%

Upper

95%

Lower

95.0%

Upper

95.0%

Intercept

0.01581

2573

0.005950

346

2.657

421

0.010

156

0.00390

1661

0.02772

3484

0.00390

1661

0.02772

3484

X Variable

1

0.58119

2499

0.165198

875

3.518

138

0.000

852

0.25051

1022

0.91187

3976

0.25051

1022

0.91187

3976

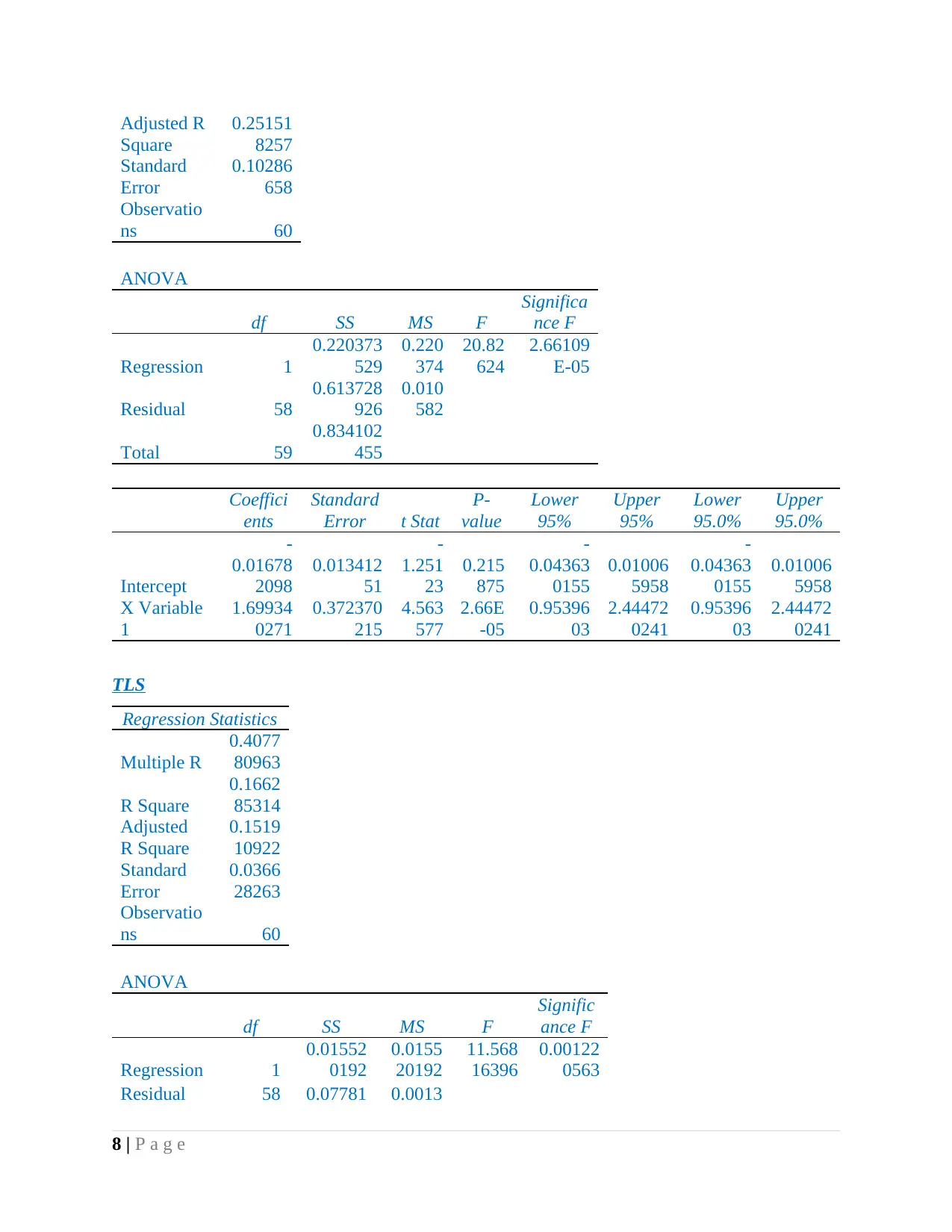

FMG

Regression Statistics

Multiple R

0.51400

816

R Square

0.26420

4388

7 | P a g e

Intercept

-

0.02099

7985

0.006332

229

-

3.316

05

0.001

579

-

0.03367

3319

-

0.00832

2652

-

0.03367

3319

-

0.00832

2652

X Variable

1

1.27947

1023

0.175801

058

7.277

948

1E-

09

0.92756

6971

1.63137

5075

0.92756

6971

1.63137

5075

CSL

Regression Statistics

Multiple R

0.41936

9288

R Square

0.17587

0599

Adjusted R

Square

0.16166

1472

Standard

Error

0.04563

5882

Observatio

ns 60

ANOVA

df SS MS F

Significa

nce F

Regression 1

0.025777

377

0.025

777

12.37

73

0.00085

2145

Residual 58

0.120792

757

0.002

083

Total 59

0.146570

134

Coeffici

ents

Standard

Error t Stat

P-

value

Lower

95%

Upper

95%

Lower

95.0%

Upper

95.0%

Intercept

0.01581

2573

0.005950

346

2.657

421

0.010

156

0.00390

1661

0.02772

3484

0.00390

1661

0.02772

3484

X Variable

1

0.58119

2499

0.165198

875

3.518

138

0.000

852

0.25051

1022

0.91187

3976

0.25051

1022

0.91187

3976

FMG

Regression Statistics

Multiple R

0.51400

816

R Square

0.26420

4388

7 | P a g e

Adjusted R

Square

0.25151

8257

Standard

Error

0.10286

658

Observatio

ns 60

ANOVA

df SS MS F

Significa

nce F

Regression 1

0.220373

529

0.220

374

20.82

624

2.66109

E-05

Residual 58

0.613728

926

0.010

582

Total 59

0.834102

455

Coeffici

ents

Standard

Error t Stat

P-

value

Lower

95%

Upper

95%

Lower

95.0%

Upper

95.0%

Intercept

-

0.01678

2098

0.013412

51

-

1.251

23

0.215

875

-

0.04363

0155

0.01006

5958

-

0.04363

0155

0.01006

5958

X Variable

1

1.69934

0271

0.372370

215

4.563

577

2.66E

-05

0.95396

03

2.44472

0241

0.95396

03

2.44472

0241

TLS

Regression Statistics

Multiple R

0.4077

80963

R Square

0.1662

85314

Adjusted

R Square

0.1519

10922

Standard

Error

0.0366

28263

Observatio

ns 60

ANOVA

df SS MS F

Signific

ance F

Regression 1

0.01552

0192

0.0155

20192

11.568

16396

0.00122

0563

Residual 58 0.07781 0.0013

8 | P a g e

Square

0.25151

8257

Standard

Error

0.10286

658

Observatio

ns 60

ANOVA

df SS MS F

Significa

nce F

Regression 1

0.220373

529

0.220

374

20.82

624

2.66109

E-05

Residual 58

0.613728

926

0.010

582

Total 59

0.834102

455

Coeffici

ents

Standard

Error t Stat

P-

value

Lower

95%

Upper

95%

Lower

95.0%

Upper

95.0%

Intercept

-

0.01678

2098

0.013412

51

-

1.251

23

0.215

875

-

0.04363

0155

0.01006

5958

-

0.04363

0155

0.01006

5958

X Variable

1

1.69934

0271

0.372370

215

4.563

577

2.66E

-05

0.95396

03

2.44472

0241

0.95396

03

2.44472

0241

TLS

Regression Statistics

Multiple R

0.4077

80963

R Square

0.1662

85314

Adjusted

R Square

0.1519

10922

Standard

Error

0.0366

28263

Observatio

ns 60

ANOVA

df SS MS F

Signific

ance F

Regression 1

0.01552

0192

0.0155

20192

11.568

16396

0.00122

0563

Residual 58 0.07781 0.0013

8 | P a g e

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

4519 4163

Total 59

0.09333

471

Coeffic

ients

Standar

d Error t Stat

P-

value

Lower

95%

Upper

95%

Lower

95.0%

Upper

95.0%

Intercept

0.0091

64085

0.00477

5865

1.9188

32325

0.0599

31095

-

0.00039

5848

0.0187

24019

-

0.00039

5848

0.0187

24019

X Variable

1

0.4509

71582

0.13259

1889

3.4012

00371

0.0012

20563

0.18556

0079

0.7163

83084

0.18556

0079

0.7163

83084

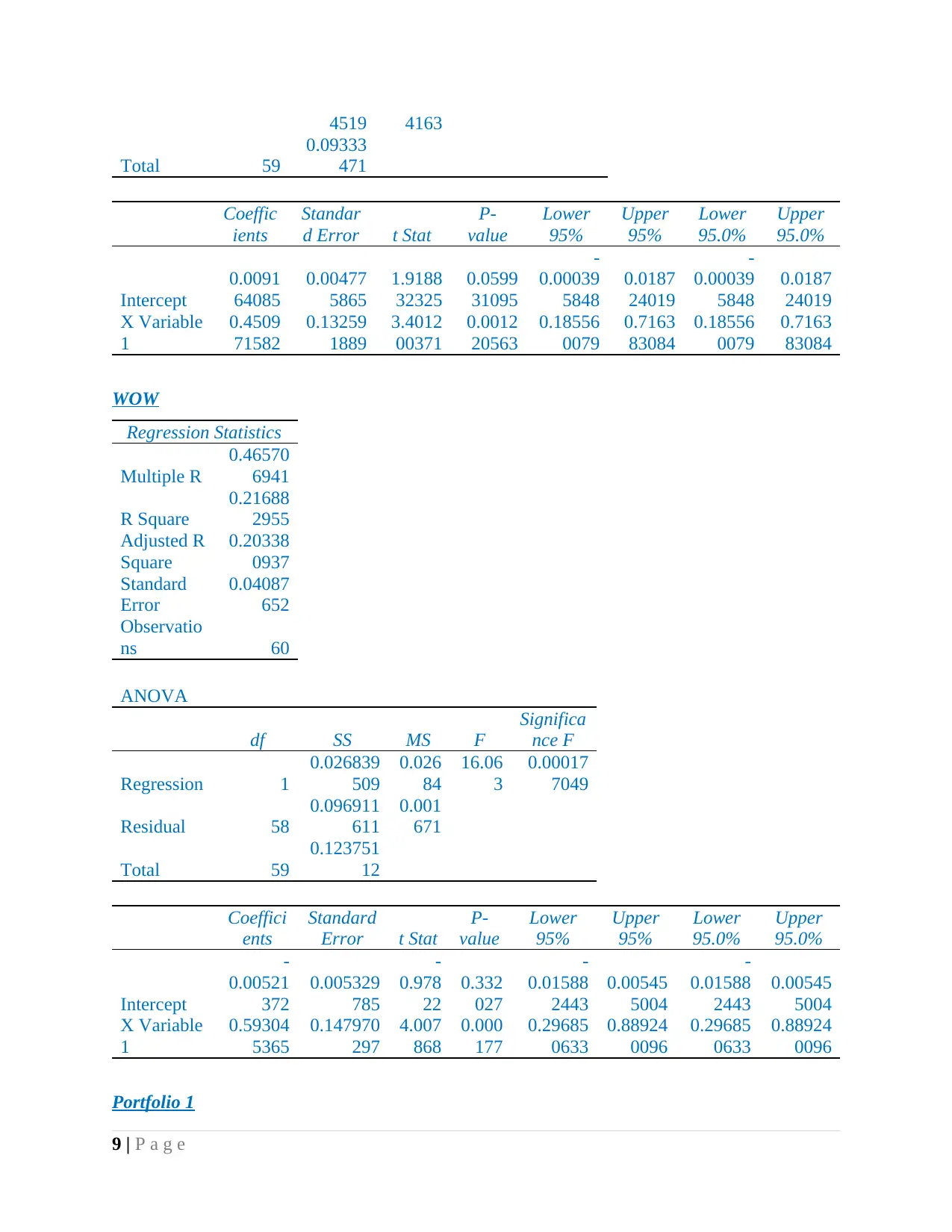

WOW

Regression Statistics

Multiple R

0.46570

6941

R Square

0.21688

2955

Adjusted R

Square

0.20338

0937

Standard

Error

0.04087

652

Observatio

ns 60

ANOVA

df SS MS F

Significa

nce F

Regression 1

0.026839

509

0.026

84

16.06

3

0.00017

7049

Residual 58

0.096911

611

0.001

671

Total 59

0.123751

12

Coeffici

ents

Standard

Error t Stat

P-

value

Lower

95%

Upper

95%

Lower

95.0%

Upper

95.0%

Intercept

-

0.00521

372

0.005329

785

-

0.978

22

0.332

027

-

0.01588

2443

0.00545

5004

-

0.01588

2443

0.00545

5004

X Variable

1

0.59304

5365

0.147970

297

4.007

868

0.000

177

0.29685

0633

0.88924

0096

0.29685

0633

0.88924

0096

Portfolio 1

9 | P a g e

Total 59

0.09333

471

Coeffic

ients

Standar

d Error t Stat

P-

value

Lower

95%

Upper

95%

Lower

95.0%

Upper

95.0%

Intercept

0.0091

64085

0.00477

5865

1.9188

32325

0.0599

31095

-

0.00039

5848

0.0187

24019

-

0.00039

5848

0.0187

24019

X Variable

1

0.4509

71582

0.13259

1889

3.4012

00371

0.0012

20563

0.18556

0079

0.7163

83084

0.18556

0079

0.7163

83084

WOW

Regression Statistics

Multiple R

0.46570

6941

R Square

0.21688

2955

Adjusted R

Square

0.20338

0937

Standard

Error

0.04087

652

Observatio

ns 60

ANOVA

df SS MS F

Significa

nce F

Regression 1

0.026839

509

0.026

84

16.06

3

0.00017

7049

Residual 58

0.096911

611

0.001

671

Total 59

0.123751

12

Coeffici

ents

Standard

Error t Stat

P-

value

Lower

95%

Upper

95%

Lower

95.0%

Upper

95.0%

Intercept

-

0.00521

372

0.005329

785

-

0.978

22

0.332

027

-

0.01588

2443

0.00545

5004

-

0.01588

2443

0.00545

5004

X Variable

1

0.59304

5365

0.147970

297

4.007

868

0.000

177

0.29685

0633

0.88924

0096

0.29685

0633

0.88924

0096

Portfolio 1

9 | P a g e

Regression Statistics

Multiple R

0.88122

0373

R Square

0.77654

9346

Adjusted

R Square

0.77269

6748

Standard

Error

0.01942

8214

Observatio

ns 60

ANOVA

df SS MS F

Signific

ance F

Regression 1

0.07608

1872

0.07608

1872

201.56

51382

1.57571

E-20

Residual 58

0.02189

242

0.00037

7456

Total 59

0.09797

4292

Coeffici

ents

Standar

d Error t Stat

P-

value

Lower

95%

Upper

95%

Lower

95.0%

Upper

95.0%

Intercept

-

0.00389

9389

0.00253

3195

-

1.53931

6572

0.1291

65368

-

0.00897

013

0.0011

71352

-

0.0089

7013

0.0011

71352

X Variable

1

0.99848

428

0.07032

8851

14.1973

6378

1.5757

1E-20

0.85770

5789

1.1392

6277

0.8577

05789

1.1392

6277

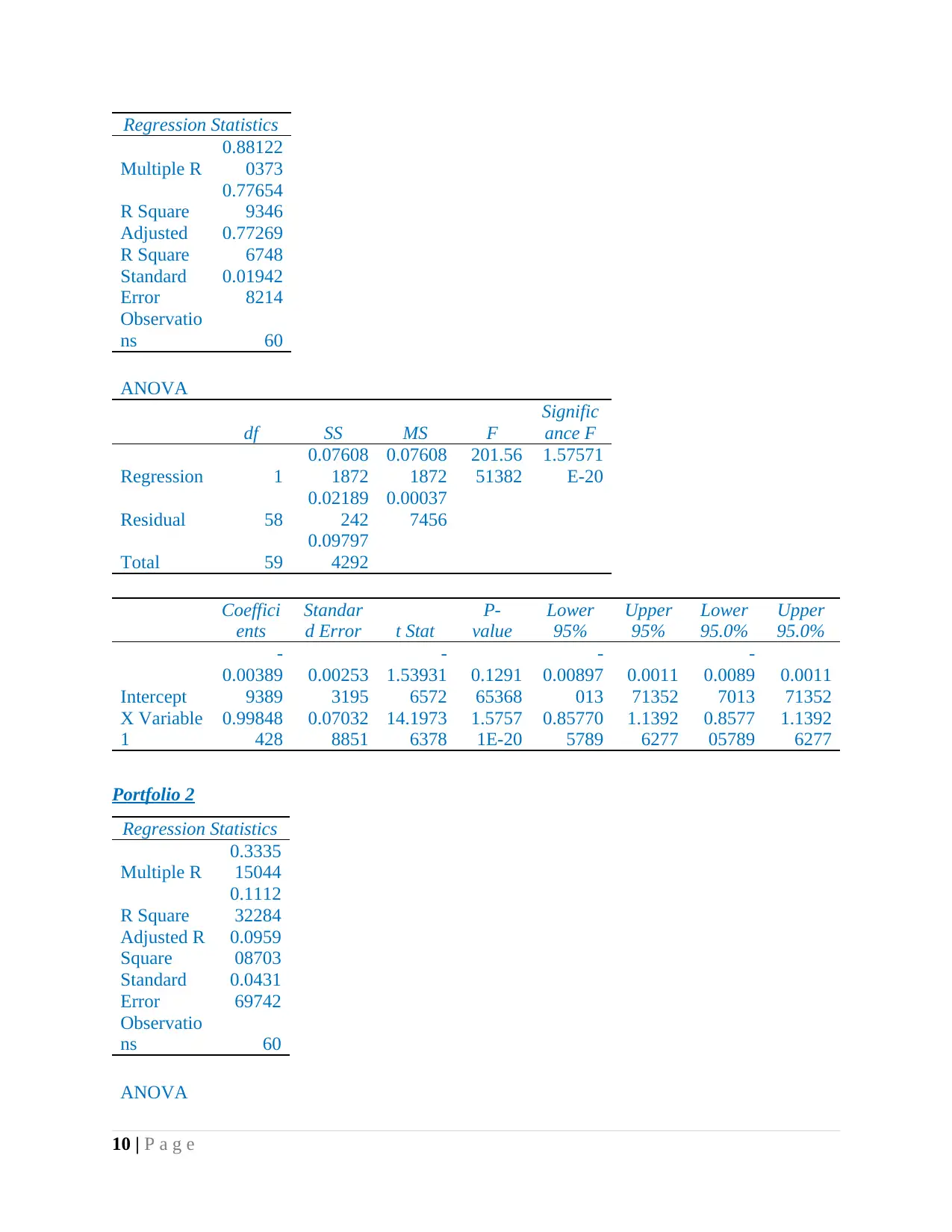

Portfolio 2

Regression Statistics

Multiple R

0.3335

15044

R Square

0.1112

32284

Adjusted R

Square

0.0959

08703

Standard

Error

0.0431

69742

Observatio

ns 60

ANOVA

10 | P a g e

Multiple R

0.88122

0373

R Square

0.77654

9346

Adjusted

R Square

0.77269

6748

Standard

Error

0.01942

8214

Observatio

ns 60

ANOVA

df SS MS F

Signific

ance F

Regression 1

0.07608

1872

0.07608

1872

201.56

51382

1.57571

E-20

Residual 58

0.02189

242

0.00037

7456

Total 59

0.09797

4292

Coeffici

ents

Standar

d Error t Stat

P-

value

Lower

95%

Upper

95%

Lower

95.0%

Upper

95.0%

Intercept

-

0.00389

9389

0.00253

3195

-

1.53931

6572

0.1291

65368

-

0.00897

013

0.0011

71352

-

0.0089

7013

0.0011

71352

X Variable

1

0.99848

428

0.07032

8851

14.1973

6378

1.5757

1E-20

0.85770

5789

1.1392

6277

0.8577

05789

1.1392

6277

Portfolio 2

Regression Statistics

Multiple R

0.3335

15044

R Square

0.1112

32284

Adjusted R

Square

0.0959

08703

Standard

Error

0.0431

69742

Observatio

ns 60

ANOVA

10 | P a g e

df SS MS F

Signific

ance F

Regression 1

0.01352

7872

0.0135

27872

7.2588

96078

0.00921

2299

Residual 58

0.10809

0342

0.0018

63627

Total 59

0.12161

8214

Coeffic

ients

Standar

d Error t Stat

P-

value

Lower

95%

Upper

95%

Lower

95.0%

Upper

95.0%

Intercept

0.0229

19039

0.00562

8792

4.0717

5088

0.0001

43189

0.01165

1788

0.0341

86291

0.0116

51788

0.03418

6291

X Variable

1

0.4210

32262

0.15627

161

2.6942

33857

0.0092

12299

0.10822

0648

0.7338

43875

0.1082

20648

0.73384

3875

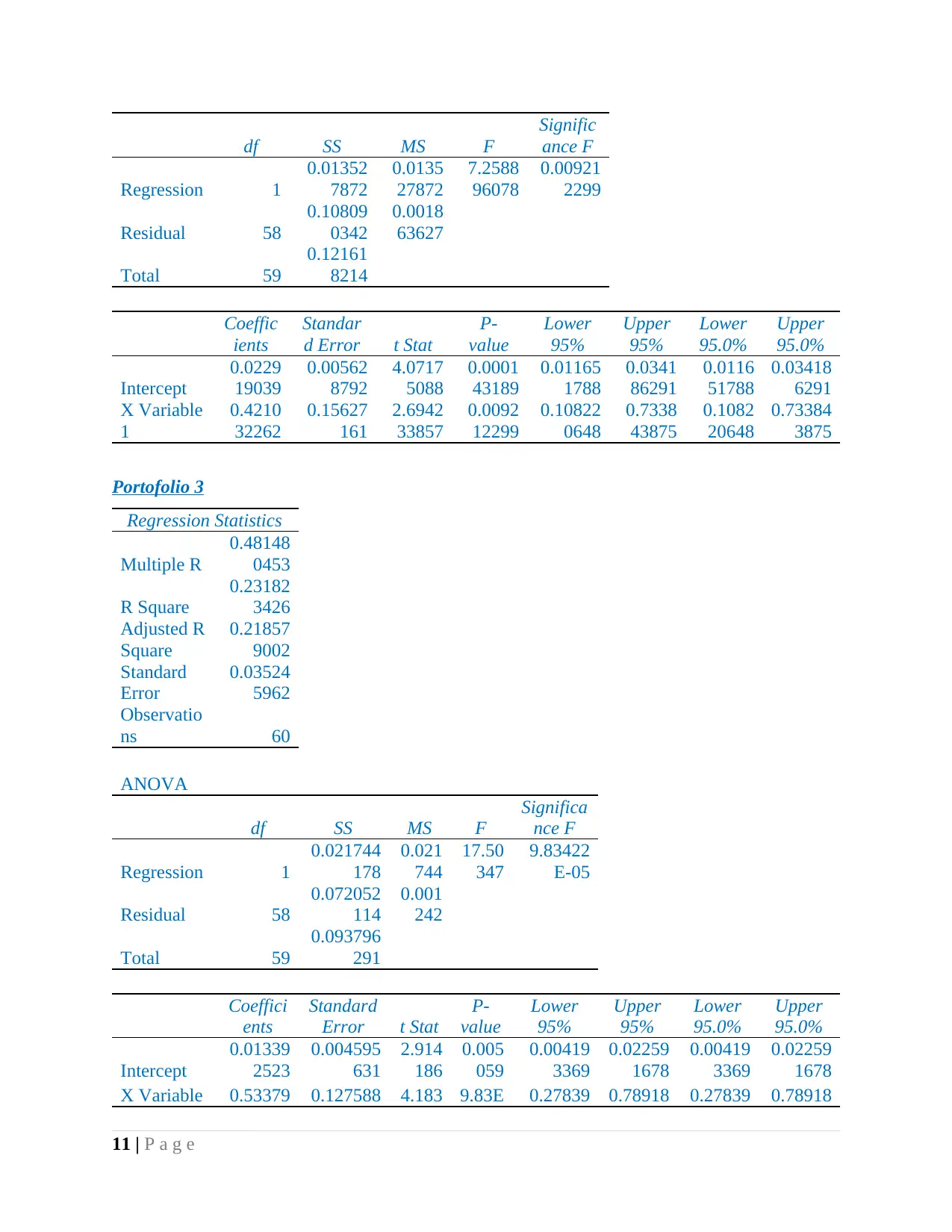

Portofolio 3

Regression Statistics

Multiple R

0.48148

0453

R Square

0.23182

3426

Adjusted R

Square

0.21857

9002

Standard

Error

0.03524

5962

Observatio

ns 60

ANOVA

df SS MS F

Significa

nce F

Regression 1

0.021744

178

0.021

744

17.50

347

9.83422

E-05

Residual 58

0.072052

114

0.001

242

Total 59

0.093796

291

Coeffici

ents

Standard

Error t Stat

P-

value

Lower

95%

Upper

95%

Lower

95.0%

Upper

95.0%

Intercept

0.01339

2523

0.004595

631

2.914

186

0.005

059

0.00419

3369

0.02259

1678

0.00419

3369

0.02259

1678

X Variable 0.53379 0.127588 4.183 9.83E 0.27839 0.78918 0.27839 0.78918

11 | P a g e

Signific

ance F

Regression 1

0.01352

7872

0.0135

27872

7.2588

96078

0.00921

2299

Residual 58

0.10809

0342

0.0018

63627

Total 59

0.12161

8214

Coeffic

ients

Standar

d Error t Stat

P-

value

Lower

95%

Upper

95%

Lower

95.0%

Upper

95.0%

Intercept

0.0229

19039

0.00562

8792

4.0717

5088

0.0001

43189

0.01165

1788

0.0341

86291

0.0116

51788

0.03418

6291

X Variable

1

0.4210

32262

0.15627

161

2.6942

33857

0.0092

12299

0.10822

0648

0.7338

43875

0.1082

20648

0.73384

3875

Portofolio 3

Regression Statistics

Multiple R

0.48148

0453

R Square

0.23182

3426

Adjusted R

Square

0.21857

9002

Standard

Error

0.03524

5962

Observatio

ns 60

ANOVA

df SS MS F

Significa

nce F

Regression 1

0.021744

178

0.021

744

17.50

347

9.83422

E-05

Residual 58

0.072052

114

0.001

242

Total 59

0.093796

291

Coeffici

ents

Standard

Error t Stat

P-

value

Lower

95%

Upper

95%

Lower

95.0%

Upper

95.0%

Intercept

0.01339

2523

0.004595

631

2.914

186

0.005

059

0.00419

3369

0.02259

1678

0.00419

3369

0.02259

1678

X Variable 0.53379 0.127588 4.183 9.83E 0.27839 0.78918 0.27839 0.78918

11 | P a g e

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

1 2085 051 715 -05 6853 7318 6853 7318

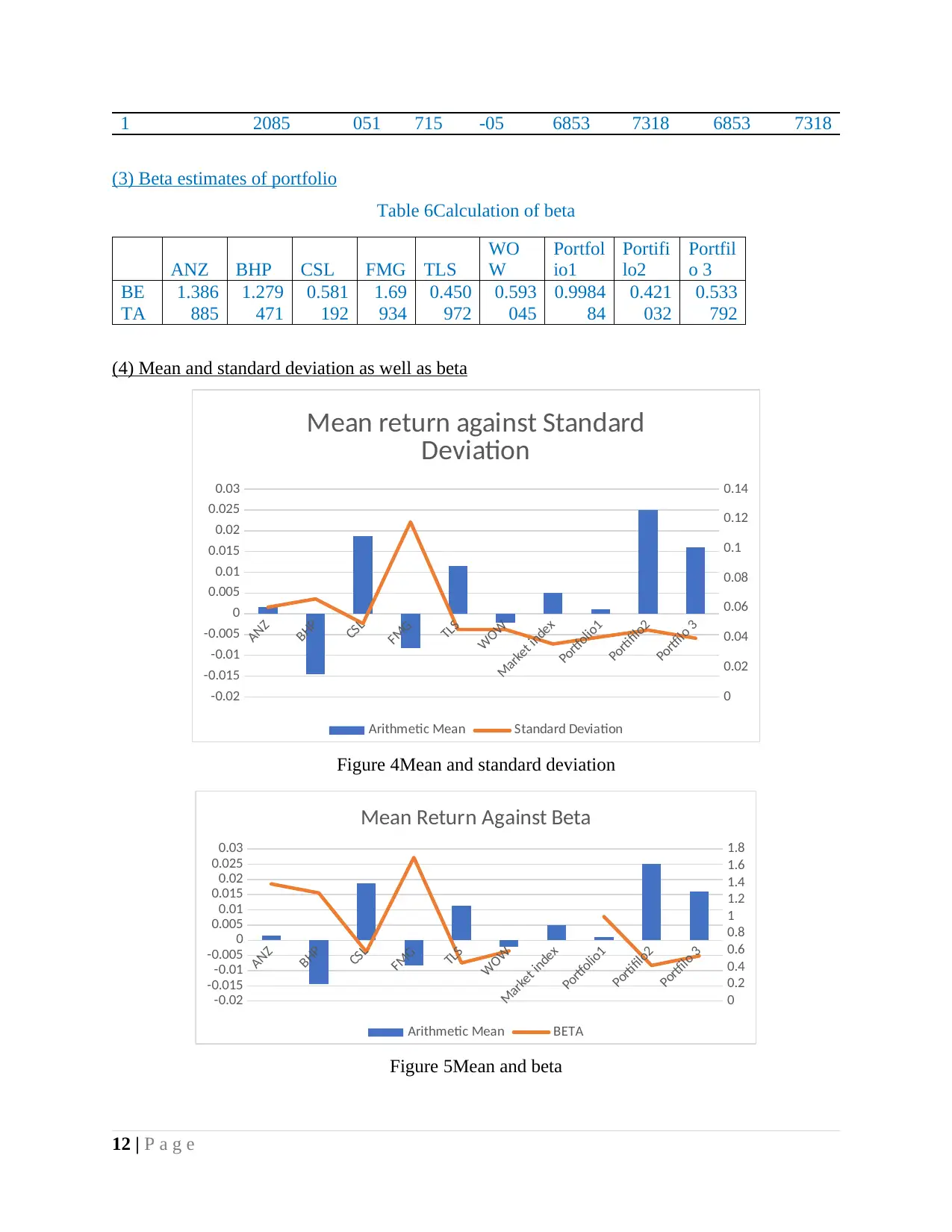

(3) Beta estimates of portfolio

Table 6Calculation of beta

ANZ BHP CSL FMG TLS

WO

W

Portfol

io1

Portifi

lo2

Portfil

o 3

BE

TA

1.386

885

1.279

471

0.581

192

1.69

934

0.450

972

0.593

045

0.9984

84

0.421

032

0.533

792

(4) Mean and standard deviation as well as beta

ANZ

BHP

CSL

FMG

TLS

WOW

Market index

Portfolio1

Portifilo2

Portfilo 3

-0.02

-0.015

-0.01

-0.005

0

0.005

0.01

0.015

0.02

0.025

0.03

0

0.02

0.04

0.06

0.08

0.1

0.12

0.14

Mean return against Standard

Deviation

Arithmetic Mean Standard Deviation

Figure 4Mean and standard deviation

ANZ

BHP

CSL

FMG

TLS

WOW

Market index

Portfolio1

Portifilo2

Portfilo 3

-0.02

-0.015

-0.01

-0.005

0

0.005

0.01

0.015

0.02

0.025

0.03

0

0.2

0.4

0.6

0.8

1

1.2

1.4

1.6

1.8

Mean Return Against Beta

Arithmetic Mean BETA

Figure 5Mean and beta

12 | P a g e

(3) Beta estimates of portfolio

Table 6Calculation of beta

ANZ BHP CSL FMG TLS

WO

W

Portfol

io1

Portifi

lo2

Portfil

o 3

BE

TA

1.386

885

1.279

471

0.581

192

1.69

934

0.450

972

0.593

045

0.9984

84

0.421

032

0.533

792

(4) Mean and standard deviation as well as beta

ANZ

BHP

CSL

FMG

TLS

WOW

Market index

Portfolio1

Portifilo2

Portfilo 3

-0.02

-0.015

-0.01

-0.005

0

0.005

0.01

0.015

0.02

0.025

0.03

0

0.02

0.04

0.06

0.08

0.1

0.12

0.14

Mean return against Standard

Deviation

Arithmetic Mean Standard Deviation

Figure 4Mean and standard deviation

ANZ

BHP

CSL

FMG

TLS

WOW

Market index

Portfolio1

Portifilo2

Portfilo 3

-0.02

-0.015

-0.01

-0.005

0

0.005

0.01

0.015

0.02

0.025

0.03

0

0.2

0.4

0.6

0.8

1

1.2

1.4

1.6

1.8

Mean Return Against Beta

Arithmetic Mean BETA

Figure 5Mean and beta

12 | P a g e

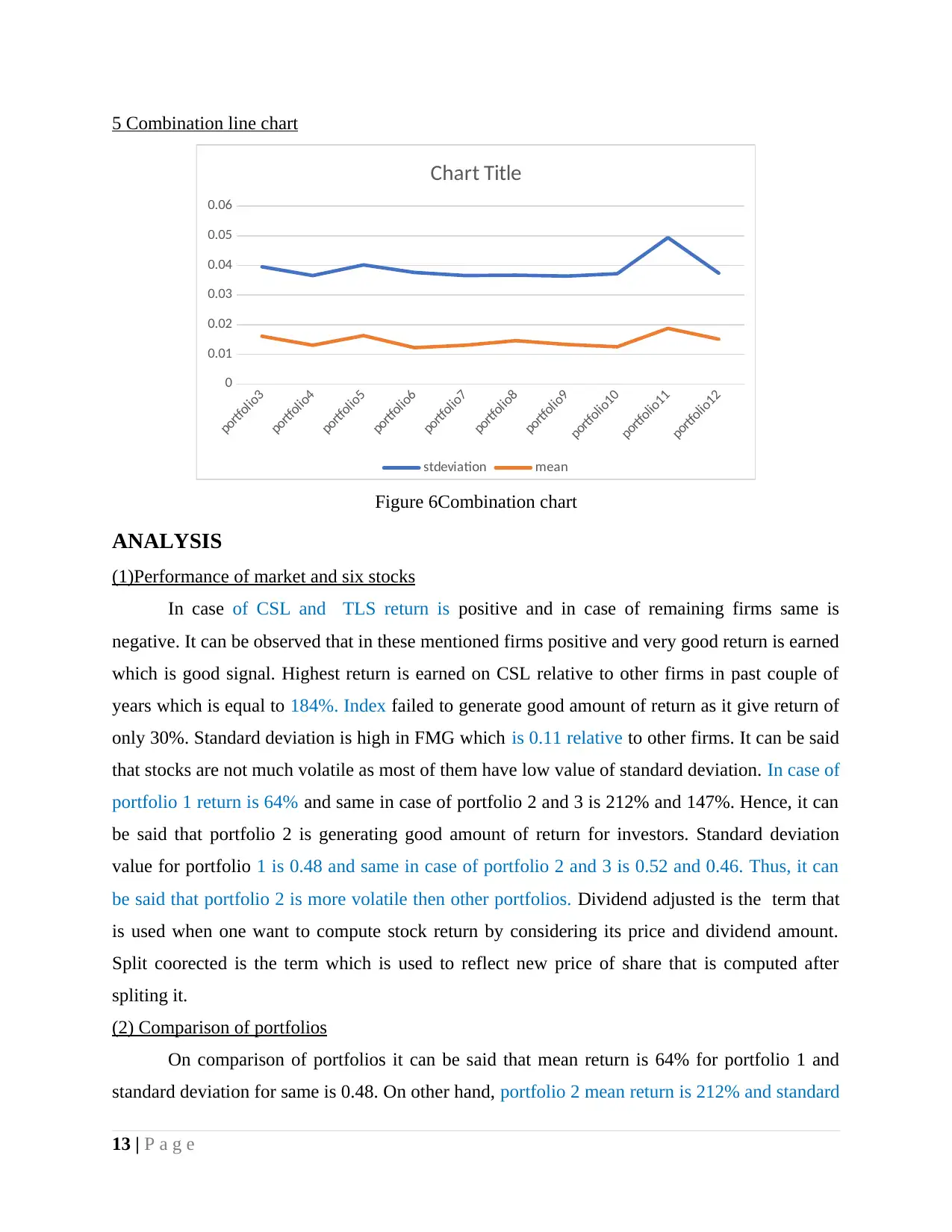

5 Combination line chart

portfolio3

portfolio4

portfolio5

portfolio6

portfolio7

portfolio8

portfolio9

portfolio10

portfolio11

portfolio12

0

0.01

0.02

0.03

0.04

0.05

0.06

Chart Title

stdeviation mean

Figure 6Combination chart

ANALYSIS

(1)Performance of market and six stocks

In case of CSL and TLS return is positive and in case of remaining firms same is

negative. It can be observed that in these mentioned firms positive and very good return is earned

which is good signal. Highest return is earned on CSL relative to other firms in past couple of

years which is equal to 184%. Index failed to generate good amount of return as it give return of

only 30%. Standard deviation is high in FMG which is 0.11 relative to other firms. It can be said

that stocks are not much volatile as most of them have low value of standard deviation. In case of

portfolio 1 return is 64% and same in case of portfolio 2 and 3 is 212% and 147%. Hence, it can

be said that portfolio 2 is generating good amount of return for investors. Standard deviation

value for portfolio 1 is 0.48 and same in case of portfolio 2 and 3 is 0.52 and 0.46. Thus, it can

be said that portfolio 2 is more volatile then other portfolios. Dividend adjusted is the term that

is used when one want to compute stock return by considering its price and dividend amount.

Split coorected is the term which is used to reflect new price of share that is computed after

spliting it.

(2) Comparison of portfolios

On comparison of portfolios it can be said that mean return is 64% for portfolio 1 and

standard deviation for same is 0.48. On other hand, portfolio 2 mean return is 212% and standard

13 | P a g e

portfolio3

portfolio4

portfolio5

portfolio6

portfolio7

portfolio8

portfolio9

portfolio10

portfolio11

portfolio12

0

0.01

0.02

0.03

0.04

0.05

0.06

Chart Title

stdeviation mean

Figure 6Combination chart

ANALYSIS

(1)Performance of market and six stocks

In case of CSL and TLS return is positive and in case of remaining firms same is

negative. It can be observed that in these mentioned firms positive and very good return is earned

which is good signal. Highest return is earned on CSL relative to other firms in past couple of

years which is equal to 184%. Index failed to generate good amount of return as it give return of

only 30%. Standard deviation is high in FMG which is 0.11 relative to other firms. It can be said

that stocks are not much volatile as most of them have low value of standard deviation. In case of

portfolio 1 return is 64% and same in case of portfolio 2 and 3 is 212% and 147%. Hence, it can

be said that portfolio 2 is generating good amount of return for investors. Standard deviation

value for portfolio 1 is 0.48 and same in case of portfolio 2 and 3 is 0.52 and 0.46. Thus, it can

be said that portfolio 2 is more volatile then other portfolios. Dividend adjusted is the term that

is used when one want to compute stock return by considering its price and dividend amount.

Split coorected is the term which is used to reflect new price of share that is computed after

spliting it.

(2) Comparison of portfolios

On comparison of portfolios it can be said that mean return is 64% for portfolio 1 and

standard deviation for same is 0.48. On other hand, portfolio 2 mean return is 212% and standard

13 | P a g e

deviation is 0.2 followed by return is 147% and standard deviation is 0.46 in case of portoflio 3.

Thus, on the basis of return it can be said that portfolio 2 is one of best option that is available to

investor in terms of return. It can be said that it is one of best option in terms of risk also because

same is not very high in case of same then other portfolios (Bodie, 2013).

(3) Relationship between sharpe ratio portfolio 3,2 and chart ploted in 5th point

Sharpe is related to mentioned portfolios because by using same it can be identified that

apart from risk free rate of return what amount of profit is made for taking each unit of risk on

invested amount. In fifth point combination line is prepared which is reflecting change that

comes in return with change in standard deviation (Meskendahl, 2010). Sharpe ratio reflect same

thing and in this way portfolio and Sharpe ratio are related to each other.

(4) SML and CML

RFR Market ANZ BHP CSL FMG TLS WOW

0

0.02

0.04

0.06

0.08

0.1

0.12

0.14

0.16

0.015

0.09

0.01504942152719

99

0.11096032672661

9

0.05858943745386

44

0.14245052028915

2

0.04882286863478

12

0.05947840234355

24

CAPM

Figure 7SML chart

SML chart basically is plotting of CAPM values and it reflect required rate of return. SML chart

is clearly reflecting that market return is much higher then required rate of return on stocks

(Understanding the security market line, 2017). It can be said on the basis of chart that required

rate of return is almost different in case of most of securities as there is huge difference in

required rate of returns that need to be earn on them for taking risk.

14 | P a g e

Thus, on the basis of return it can be said that portfolio 2 is one of best option that is available to

investor in terms of return. It can be said that it is one of best option in terms of risk also because

same is not very high in case of same then other portfolios (Bodie, 2013).

(3) Relationship between sharpe ratio portfolio 3,2 and chart ploted in 5th point

Sharpe is related to mentioned portfolios because by using same it can be identified that

apart from risk free rate of return what amount of profit is made for taking each unit of risk on

invested amount. In fifth point combination line is prepared which is reflecting change that

comes in return with change in standard deviation (Meskendahl, 2010). Sharpe ratio reflect same

thing and in this way portfolio and Sharpe ratio are related to each other.

(4) SML and CML

RFR Market ANZ BHP CSL FMG TLS WOW

0

0.02

0.04

0.06

0.08

0.1

0.12

0.14

0.16

0.015

0.09

0.01504942152719

99

0.11096032672661

9

0.05858943745386

44

0.14245052028915

2

0.04882286863478

12

0.05947840234355

24

CAPM

Figure 7SML chart

SML chart basically is plotting of CAPM values and it reflect required rate of return. SML chart

is clearly reflecting that market return is much higher then required rate of return on stocks

(Understanding the security market line, 2017). It can be said on the basis of chart that required

rate of return is almost different in case of most of securities as there is huge difference in

required rate of returns that need to be earn on them for taking risk.

14 | P a g e

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

0.034 0.036 0.038 0.04 0.042 0.044 0.046 0.048 0.05 0.052

0

0.002

0.004

0.006

0.008

0.01

0.012

0.014

0.016

0.018

0.02

Risk and Return Combination Line

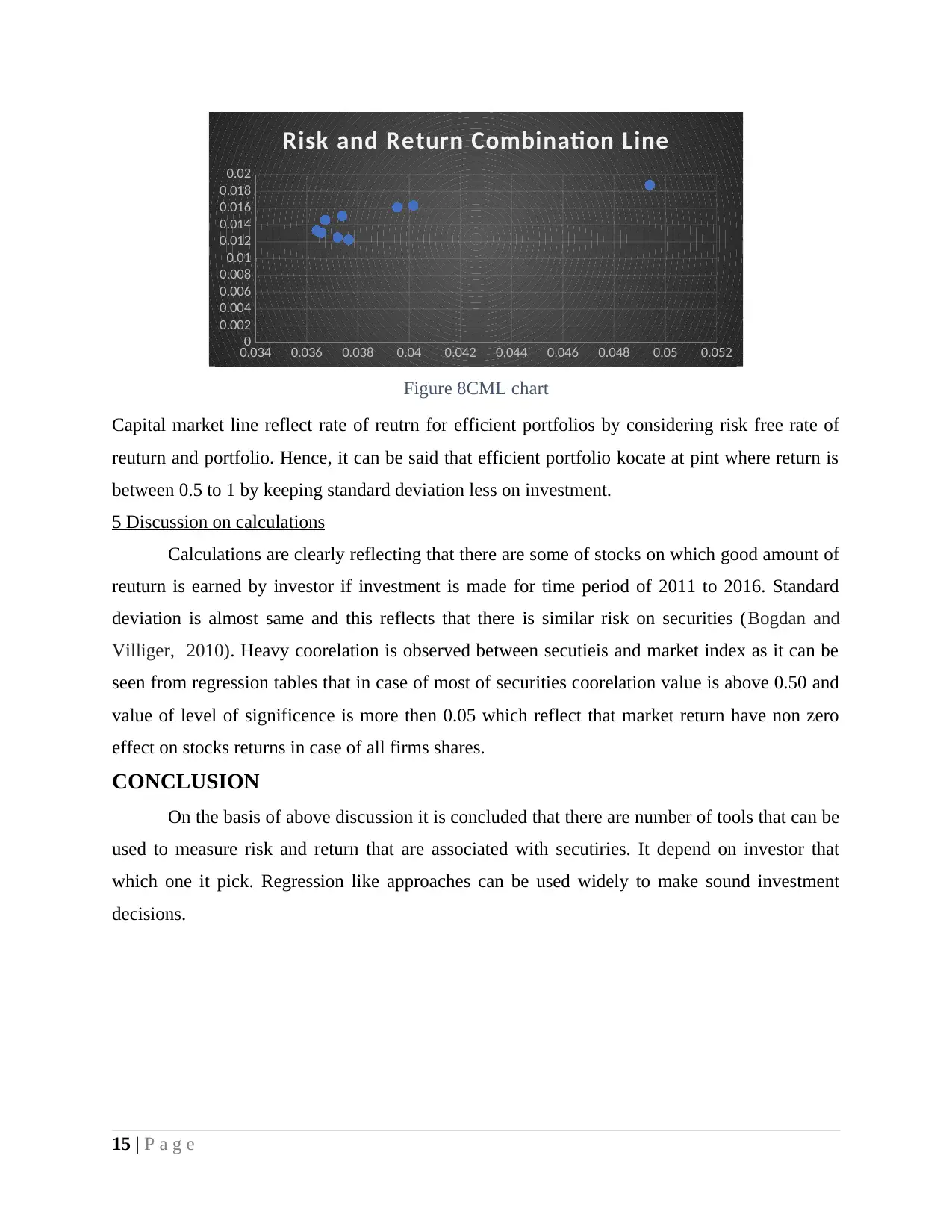

Figure 8CML chart

Capital market line reflect rate of reutrn for efficient portfolios by considering risk free rate of

reuturn and portfolio. Hence, it can be said that efficient portfolio kocate at pint where return is

between 0.5 to 1 by keeping standard deviation less on investment.

5 Discussion on calculations

Calculations are clearly reflecting that there are some of stocks on which good amount of

reuturn is earned by investor if investment is made for time period of 2011 to 2016. Standard

deviation is almost same and this reflects that there is similar risk on securities (Bogdan and

Villiger, 2010). Heavy coorelation is observed between secutieis and market index as it can be

seen from regression tables that in case of most of securities coorelation value is above 0.50 and

value of level of significence is more then 0.05 which reflect that market return have non zero

effect on stocks returns in case of all firms shares.

CONCLUSION

On the basis of above discussion it is concluded that there are number of tools that can be

used to measure risk and return that are associated with secutiries. It depend on investor that

which one it pick. Regression like approaches can be used widely to make sound investment

decisions.

15 | P a g e

0

0.002

0.004

0.006

0.008

0.01

0.012

0.014

0.016

0.018

0.02

Risk and Return Combination Line

Figure 8CML chart

Capital market line reflect rate of reutrn for efficient portfolios by considering risk free rate of

reuturn and portfolio. Hence, it can be said that efficient portfolio kocate at pint where return is

between 0.5 to 1 by keeping standard deviation less on investment.

5 Discussion on calculations

Calculations are clearly reflecting that there are some of stocks on which good amount of

reuturn is earned by investor if investment is made for time period of 2011 to 2016. Standard

deviation is almost same and this reflects that there is similar risk on securities (Bogdan and

Villiger, 2010). Heavy coorelation is observed between secutieis and market index as it can be

seen from regression tables that in case of most of securities coorelation value is above 0.50 and

value of level of significence is more then 0.05 which reflect that market return have non zero

effect on stocks returns in case of all firms shares.

CONCLUSION

On the basis of above discussion it is concluded that there are number of tools that can be

used to measure risk and return that are associated with secutiries. It depend on investor that

which one it pick. Regression like approaches can be used widely to make sound investment

decisions.

15 | P a g e

REFERENCES

Books and Journals

Bodie, Z., (2013). Investments. McGraw-Hill.

Bogdan, B. and Villiger, R., (2010). Introduction. In Valuation in Life Sciences (pp. 1-9).

Springer Berlin Heidelberg.

Meskendahl, S., (2010). The influence of business strategy on project portfolio management and

its success—a conceptual framework. International Journal of Project Management. 28(8).

pp.807-817.

Online

Understanding the security market line, (2017). [Online]. Available through:<

https://courses.lumenlearning.com/boundless-finance/chapter/understanding-the-security-

market-line/>. [Acessed on 12th Octomber 2017].

16 | P a g e

Books and Journals

Bodie, Z., (2013). Investments. McGraw-Hill.

Bogdan, B. and Villiger, R., (2010). Introduction. In Valuation in Life Sciences (pp. 1-9).

Springer Berlin Heidelberg.

Meskendahl, S., (2010). The influence of business strategy on project portfolio management and

its success—a conceptual framework. International Journal of Project Management. 28(8).

pp.807-817.

Online

Understanding the security market line, (2017). [Online]. Available through:<

https://courses.lumenlearning.com/boundless-finance/chapter/understanding-the-security-

market-line/>. [Acessed on 12th Octomber 2017].

16 | P a g e

1 out of 21

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

© 2024 | Zucol Services PVT LTD | All rights reserved.