Statistics for Business: Statistical Inference and Simple Regression Analysis

VerifiedAdded on 2023/06/12

|9

|1819

|319

AI Summary

This article covers statistical inference and simple regression analysis for business statistics. It includes calculations, hypothesis testing, ANOVA, and testing for normal assumptions.

Contribute Materials

Your contribution can guide someone’s learning journey. Share your

documents today.

Running head: DATA ANALYSIS 1

Statistics for Business

Institution

Name

Id

Statistical Inference and Simple Regression Analysis

Statistics for Business

Institution

Name

Id

Statistical Inference and Simple Regression Analysis

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

Statistics

Contents

1. Calculations Returns and Jarque- Berra Test.................................................................................3

2. Test of Hypothesis for a Single Population Mean..........................................................................4

3. The F-test: comparing equality of Variances in Two Stocks.........................................................4

4. The ANOVA Test..........................................................................................................................5

5. Excess Returns...............................................................................................................................5

6. Test of Hypothesis Using the Confidence Interval Approach........................................................7

7. Testing for normally Assumptions.................................................................................................7

References.............................................................................................................................................9

2

Contents

1. Calculations Returns and Jarque- Berra Test.................................................................................3

2. Test of Hypothesis for a Single Population Mean..........................................................................4

3. The F-test: comparing equality of Variances in Two Stocks.........................................................4

4. The ANOVA Test..........................................................................................................................5

5. Excess Returns...............................................................................................................................5

6. Test of Hypothesis Using the Confidence Interval Approach........................................................7

7. Testing for normally Assumptions.................................................................................................7

References.............................................................................................................................................9

2

Statistics

1. Calculations Returns and Jarque- Berra Test

The returns for each of the stocks have been calculated using the given formula.

These returns signify the performance of the stocks (Jordan, et al., 2010). Similarly the

Jarque- Berra test of normality has been done.

It has been observed that there is a relationship between risk and return for GD stock

and the BA stock. The BA has a comparatively lower return and higher risk. On the other

hand, GD stocks have a higher average return and a comparatively lower risk level. Hence we

could conclude that lower rates of return attract higher levels of risks. The relationship

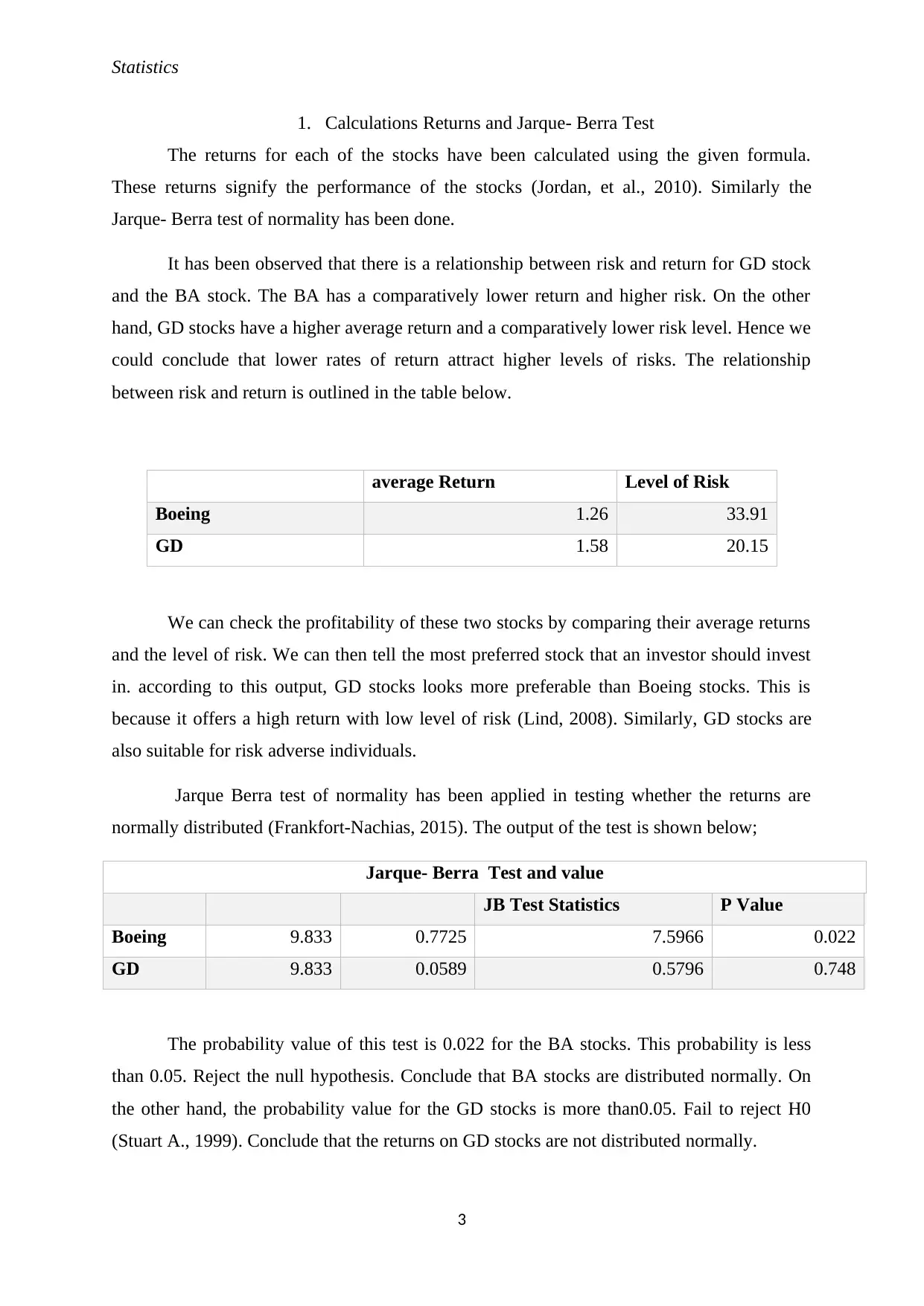

between risk and return is outlined in the table below.

average Return Level of Risk

Boeing 1.26 33.91

GD 1.58 20.15

We can check the profitability of these two stocks by comparing their average returns

and the level of risk. We can then tell the most preferred stock that an investor should invest

in. according to this output, GD stocks looks more preferable than Boeing stocks. This is

because it offers a high return with low level of risk (Lind, 2008). Similarly, GD stocks are

also suitable for risk adverse individuals.

Jarque Berra test of normality has been applied in testing whether the returns are

normally distributed (Frankfort-Nachias, 2015). The output of the test is shown below;

Jarque- Berra Test and value

JB Test Statistics P Value

Boeing 9.833 0.7725 7.5966 0.022

GD 9.833 0.0589 0.5796 0.748

The probability value of this test is 0.022 for the BA stocks. This probability is less

than 0.05. Reject the null hypothesis. Conclude that BA stocks are distributed normally. On

the other hand, the probability value for the GD stocks is more than0.05. Fail to reject H0

(Stuart A., 1999). Conclude that the returns on GD stocks are not distributed normally.

3

1. Calculations Returns and Jarque- Berra Test

The returns for each of the stocks have been calculated using the given formula.

These returns signify the performance of the stocks (Jordan, et al., 2010). Similarly the

Jarque- Berra test of normality has been done.

It has been observed that there is a relationship between risk and return for GD stock

and the BA stock. The BA has a comparatively lower return and higher risk. On the other

hand, GD stocks have a higher average return and a comparatively lower risk level. Hence we

could conclude that lower rates of return attract higher levels of risks. The relationship

between risk and return is outlined in the table below.

average Return Level of Risk

Boeing 1.26 33.91

GD 1.58 20.15

We can check the profitability of these two stocks by comparing their average returns

and the level of risk. We can then tell the most preferred stock that an investor should invest

in. according to this output, GD stocks looks more preferable than Boeing stocks. This is

because it offers a high return with low level of risk (Lind, 2008). Similarly, GD stocks are

also suitable for risk adverse individuals.

Jarque Berra test of normality has been applied in testing whether the returns are

normally distributed (Frankfort-Nachias, 2015). The output of the test is shown below;

Jarque- Berra Test and value

JB Test Statistics P Value

Boeing 9.833 0.7725 7.5966 0.022

GD 9.833 0.0589 0.5796 0.748

The probability value of this test is 0.022 for the BA stocks. This probability is less

than 0.05. Reject the null hypothesis. Conclude that BA stocks are distributed normally. On

the other hand, the probability value for the GD stocks is more than0.05. Fail to reject H0

(Stuart A., 1999). Conclude that the returns on GD stocks are not distributed normally.

3

Statistics

2. Test of Hypothesis for a Single Population Mean

This question aims at testing the hypothesis that the mean return of GD is not equal to

2.8 %. The sample size is sufficiently large meaning the best test is the Z test. (Frankfort-

Nachias, 2015). The hypothesis to be tested is;

H0: The mean of return on GD stocks = 2.8

H1: The mean of return on GD stocks = 2.8

The test results are shown in the table below. From the output, it is clear that the Z

score is -2.092 and the probability value is equal to 0.018, which is less than 0.05. We Reject

the H0 (Frank & Harrell, 2001). Conclude that the mean of return on the GD is not equal to

2.8.

3. The F-test: comparing equality of Variances in Two Stocks

The difference in variances between BA stocks and GD stocks can be investigated

using the F- test for variances. The variance in return for each stock represents the risk

associated with the stock (Frank & Harrell, 2001). The following hypothesis is formulated;

H0: The two stocks have the same variance

H1: The two stocks have difference variances.

The following is the output table:

Boeing GD

Mean 1.256454 1.57727

Variance 33.91273 20.14665

Observations 59 59

Df 58 58

F 1.683294

P(F<=f) one-tail 0.024794

F Critical one-tail 1.545768

4

2. Test of Hypothesis for a Single Population Mean

This question aims at testing the hypothesis that the mean return of GD is not equal to

2.8 %. The sample size is sufficiently large meaning the best test is the Z test. (Frankfort-

Nachias, 2015). The hypothesis to be tested is;

H0: The mean of return on GD stocks = 2.8

H1: The mean of return on GD stocks = 2.8

The test results are shown in the table below. From the output, it is clear that the Z

score is -2.092 and the probability value is equal to 0.018, which is less than 0.05. We Reject

the H0 (Frank & Harrell, 2001). Conclude that the mean of return on the GD is not equal to

2.8.

3. The F-test: comparing equality of Variances in Two Stocks

The difference in variances between BA stocks and GD stocks can be investigated

using the F- test for variances. The variance in return for each stock represents the risk

associated with the stock (Frank & Harrell, 2001). The following hypothesis is formulated;

H0: The two stocks have the same variance

H1: The two stocks have difference variances.

The following is the output table:

Boeing GD

Mean 1.256454 1.57727

Variance 33.91273 20.14665

Observations 59 59

Df 58 58

F 1.683294

P(F<=f) one-tail 0.024794

F Critical one-tail 1.545768

4

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

Statistics

The p value is 0.0024794, less than 0.05. We reject the H0. Consequently we

conclude that statistically, the returns on the two stocks are difference.

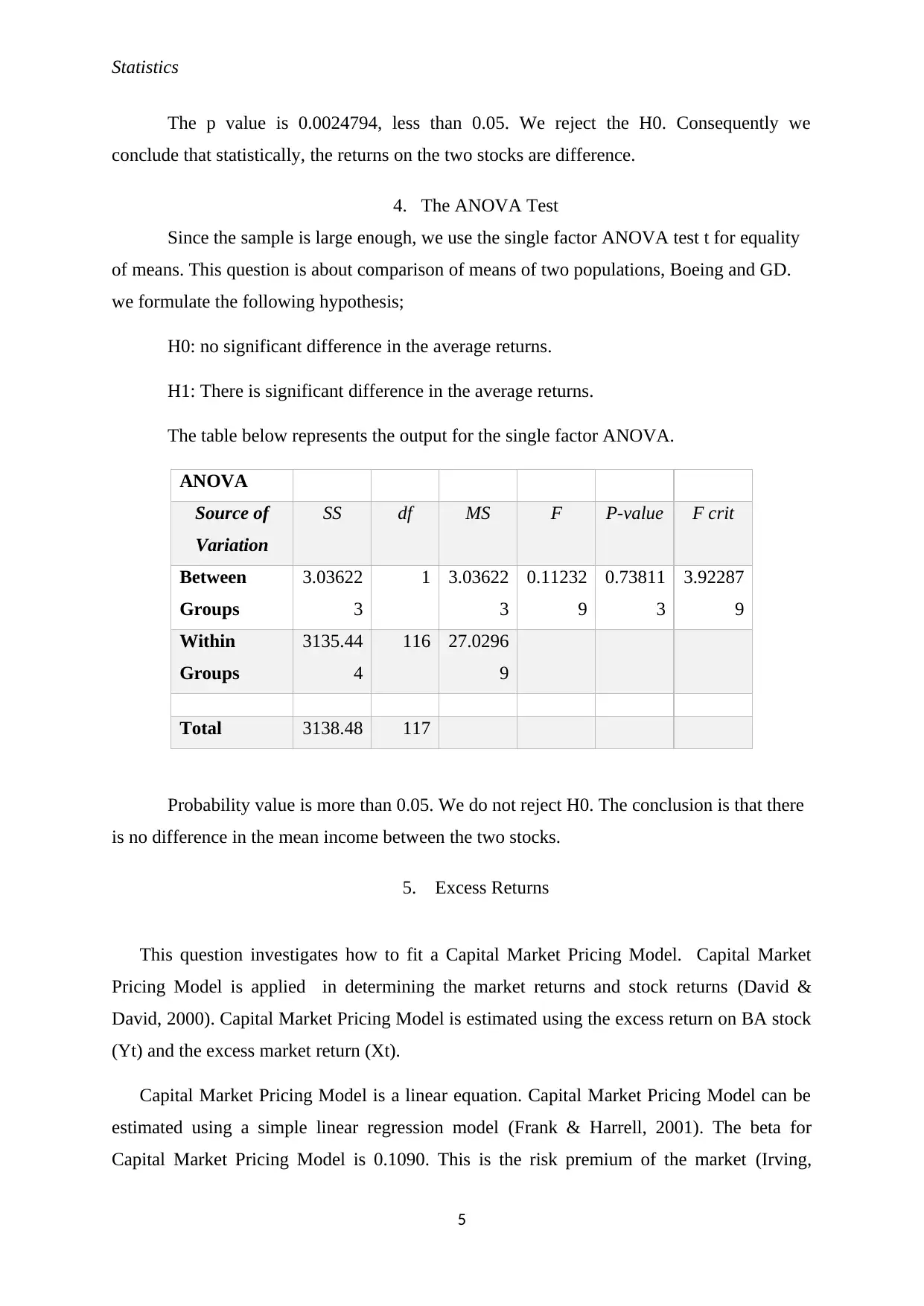

4. The ANOVA Test

Since the sample is large enough, we use the single factor ANOVA test t for equality

of means. This question is about comparison of means of two populations, Boeing and GD.

we formulate the following hypothesis;

H0: no significant difference in the average returns.

H1: There is significant difference in the average returns.

The table below represents the output for the single factor ANOVA.

ANOVA

Source of

Variation

SS df MS F P-value F crit

Between

Groups

3.03622

3

1 3.03622

3

0.11232

9

0.73811

3

3.92287

9

Within

Groups

3135.44

4

116 27.0296

9

Total 3138.48 117

Probability value is more than 0.05. We do not reject H0. The conclusion is that there

is no difference in the mean income between the two stocks.

5. Excess Returns

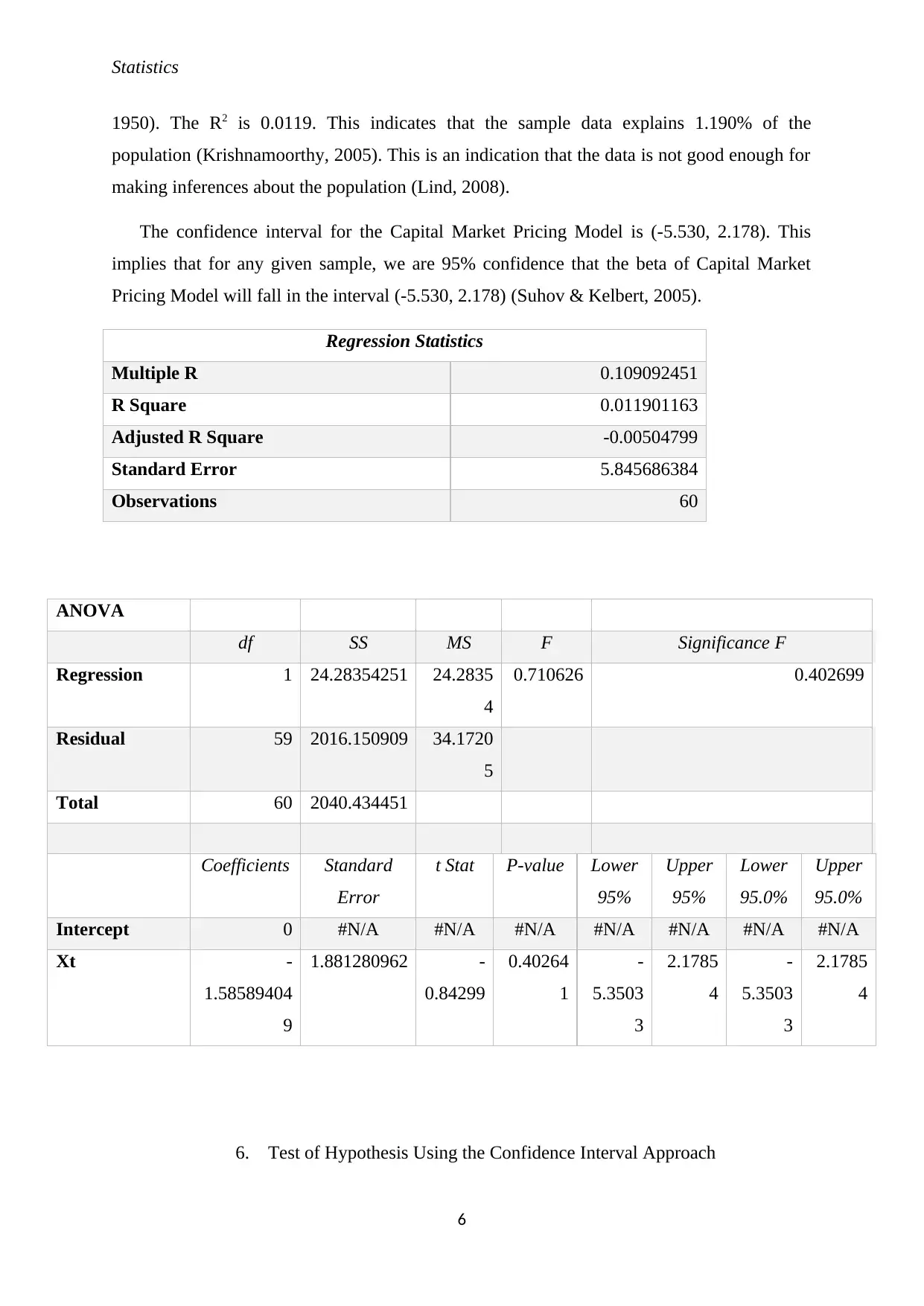

This question investigates how to fit a Capital Market Pricing Model. Capital Market

Pricing Model is applied in determining the market returns and stock returns (David &

David, 2000). Capital Market Pricing Model is estimated using the excess return on BA stock

(Yt) and the excess market return (Xt).

Capital Market Pricing Model is a linear equation. Capital Market Pricing Model can be

estimated using a simple linear regression model (Frank & Harrell, 2001). The beta for

Capital Market Pricing Model is 0.1090. This is the risk premium of the market (Irving,

5

The p value is 0.0024794, less than 0.05. We reject the H0. Consequently we

conclude that statistically, the returns on the two stocks are difference.

4. The ANOVA Test

Since the sample is large enough, we use the single factor ANOVA test t for equality

of means. This question is about comparison of means of two populations, Boeing and GD.

we formulate the following hypothesis;

H0: no significant difference in the average returns.

H1: There is significant difference in the average returns.

The table below represents the output for the single factor ANOVA.

ANOVA

Source of

Variation

SS df MS F P-value F crit

Between

Groups

3.03622

3

1 3.03622

3

0.11232

9

0.73811

3

3.92287

9

Within

Groups

3135.44

4

116 27.0296

9

Total 3138.48 117

Probability value is more than 0.05. We do not reject H0. The conclusion is that there

is no difference in the mean income between the two stocks.

5. Excess Returns

This question investigates how to fit a Capital Market Pricing Model. Capital Market

Pricing Model is applied in determining the market returns and stock returns (David &

David, 2000). Capital Market Pricing Model is estimated using the excess return on BA stock

(Yt) and the excess market return (Xt).

Capital Market Pricing Model is a linear equation. Capital Market Pricing Model can be

estimated using a simple linear regression model (Frank & Harrell, 2001). The beta for

Capital Market Pricing Model is 0.1090. This is the risk premium of the market (Irving,

5

Statistics

1950). The R2 is 0.0119. This indicates that the sample data explains 1.190% of the

population (Krishnamoorthy, 2005). This is an indication that the data is not good enough for

making inferences about the population (Lind, 2008).

The confidence interval for the Capital Market Pricing Model is (-5.530, 2.178). This

implies that for any given sample, we are 95% confidence that the beta of Capital Market

Pricing Model will fall in the interval (-5.530, 2.178) (Suhov & Kelbert, 2005).

ANOVA

df SS MS F Significance F

Regression 1 24.28354251 24.2835

4

0.710626 0.402699

Residual 59 2016.150909 34.1720

5

Total 60 2040.434451

Coefficients Standard

Error

t Stat P-value Lower

95%

Upper

95%

Lower

95.0%

Upper

95.0%

Intercept 0 #N/A #N/A #N/A #N/A #N/A #N/A #N/A

Xt -

1.58589404

9

1.881280962 -

0.84299

0.40264

1

-

5.3503

3

2.1785

4

-

5.3503

3

2.1785

4

6. Test of Hypothesis Using the Confidence Interval Approach

6

Regression Statistics

Multiple R 0.109092451

R Square 0.011901163

Adjusted R Square -0.00504799

Standard Error 5.845686384

Observations 60

1950). The R2 is 0.0119. This indicates that the sample data explains 1.190% of the

population (Krishnamoorthy, 2005). This is an indication that the data is not good enough for

making inferences about the population (Lind, 2008).

The confidence interval for the Capital Market Pricing Model is (-5.530, 2.178). This

implies that for any given sample, we are 95% confidence that the beta of Capital Market

Pricing Model will fall in the interval (-5.530, 2.178) (Suhov & Kelbert, 2005).

ANOVA

df SS MS F Significance F

Regression 1 24.28354251 24.2835

4

0.710626 0.402699

Residual 59 2016.150909 34.1720

5

Total 60 2040.434451

Coefficients Standard

Error

t Stat P-value Lower

95%

Upper

95%

Lower

95.0%

Upper

95.0%

Intercept 0 #N/A #N/A #N/A #N/A #N/A #N/A #N/A

Xt -

1.58589404

9

1.881280962 -

0.84299

0.40264

1

-

5.3503

3

2.1785

4

-

5.3503

3

2.1785

4

6. Test of Hypothesis Using the Confidence Interval Approach

6

Regression Statistics

Multiple R 0.109092451

R Square 0.011901163

Adjusted R Square -0.00504799

Standard Error 5.845686384

Observations 60

Statistics

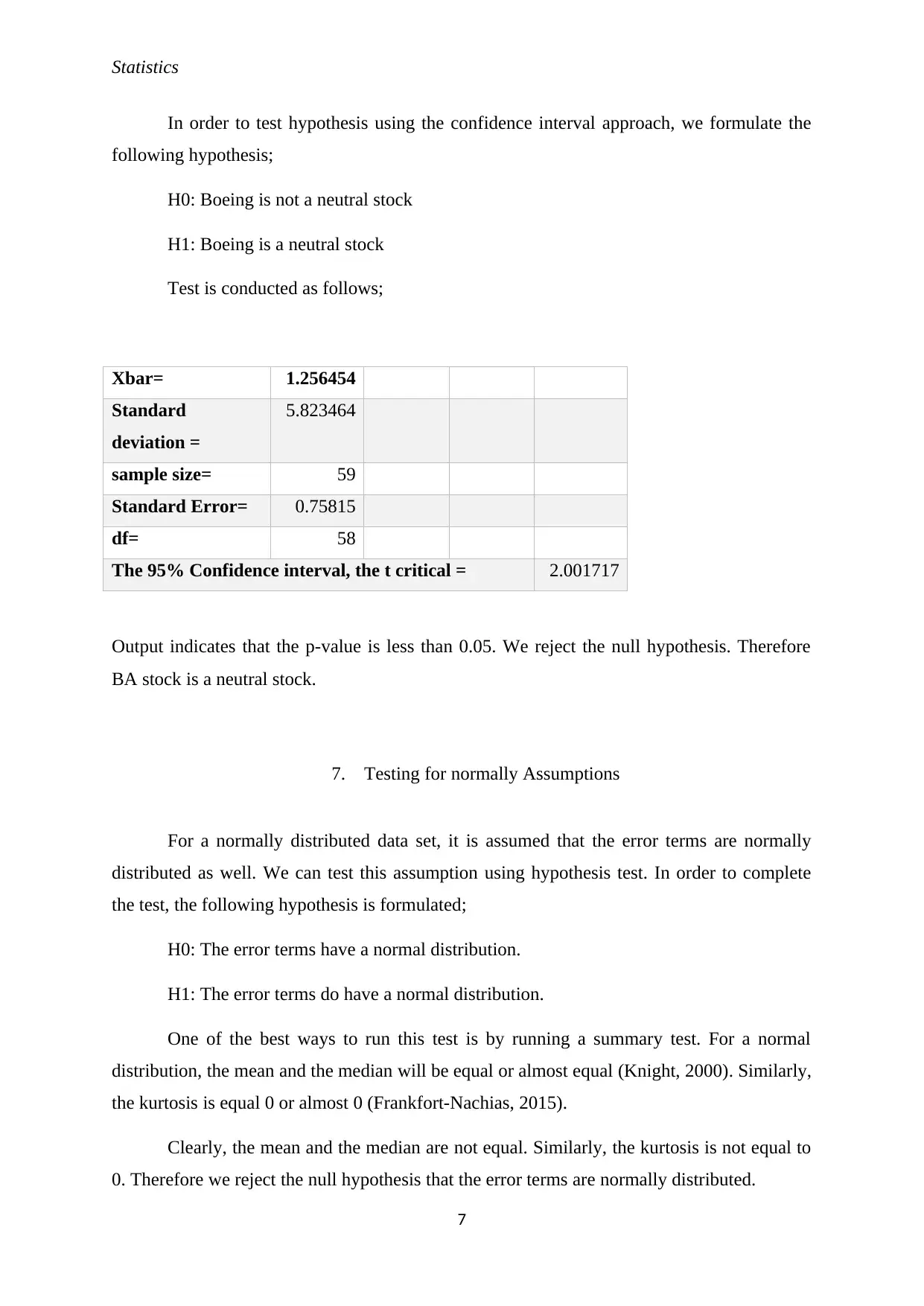

In order to test hypothesis using the confidence interval approach, we formulate the

following hypothesis;

H0: Boeing is not a neutral stock

H1: Boeing is a neutral stock

Test is conducted as follows;

Xbar= 1.256454

Standard

deviation =

5.823464

sample size= 59

Standard Error= 0.75815

df= 58

The 95% Confidence interval, the t critical = 2.001717

Output indicates that the p-value is less than 0.05. We reject the null hypothesis. Therefore

BA stock is a neutral stock.

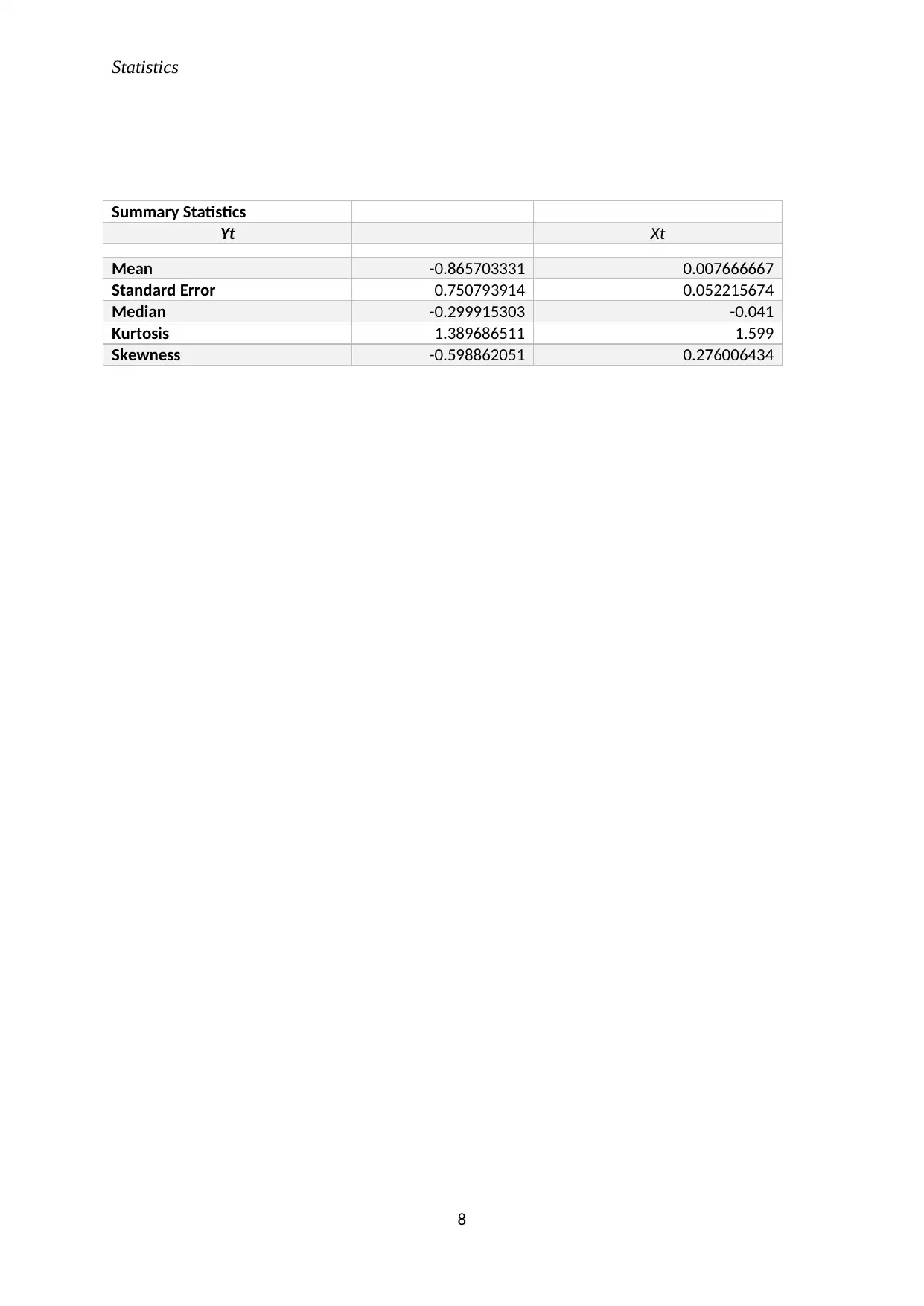

7. Testing for normally Assumptions

For a normally distributed data set, it is assumed that the error terms are normally

distributed as well. We can test this assumption using hypothesis test. In order to complete

the test, the following hypothesis is formulated;

H0: The error terms have a normal distribution.

H1: The error terms do have a normal distribution.

One of the best ways to run this test is by running a summary test. For a normal

distribution, the mean and the median will be equal or almost equal (Knight, 2000). Similarly,

the kurtosis is equal 0 or almost 0 (Frankfort-Nachias, 2015).

Clearly, the mean and the median are not equal. Similarly, the kurtosis is not equal to

0. Therefore we reject the null hypothesis that the error terms are normally distributed.

7

In order to test hypothesis using the confidence interval approach, we formulate the

following hypothesis;

H0: Boeing is not a neutral stock

H1: Boeing is a neutral stock

Test is conducted as follows;

Xbar= 1.256454

Standard

deviation =

5.823464

sample size= 59

Standard Error= 0.75815

df= 58

The 95% Confidence interval, the t critical = 2.001717

Output indicates that the p-value is less than 0.05. We reject the null hypothesis. Therefore

BA stock is a neutral stock.

7. Testing for normally Assumptions

For a normally distributed data set, it is assumed that the error terms are normally

distributed as well. We can test this assumption using hypothesis test. In order to complete

the test, the following hypothesis is formulated;

H0: The error terms have a normal distribution.

H1: The error terms do have a normal distribution.

One of the best ways to run this test is by running a summary test. For a normal

distribution, the mean and the median will be equal or almost equal (Knight, 2000). Similarly,

the kurtosis is equal 0 or almost 0 (Frankfort-Nachias, 2015).

Clearly, the mean and the median are not equal. Similarly, the kurtosis is not equal to

0. Therefore we reject the null hypothesis that the error terms are normally distributed.

7

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Statistics

Summary Statistics

Yt Xt

Mean -0.865703331 0.007666667

Standard Error 0.750793914 0.052215674

Median -0.299915303 -0.041

Kurtosis 1.389686511 1.599

Skewness -0.598862051 0.276006434

8

Summary Statistics

Yt Xt

Mean -0.865703331 0.007666667

Standard Error 0.750793914 0.052215674

Median -0.299915303 -0.041

Kurtosis 1.389686511 1.599

Skewness -0.598862051 0.276006434

8

Statistics

References

Ana, M., Jose, G. B. & Jorge, A. . L., 2003. Stochastic Models: Symposium on Probability and

Stochastic Processes. s.l.:s.n.

David, J. S. & David, S., 2000. Handbook of parametric and nonparametric statistical Procedures.

s.l.:s.n.

Frank, E. & Harrell, J., 2001. Regression Modelling Strategies: Models, Logistic Regression, and

Survival Analysis. s.l.:s.n.

Frankfort-Nachias, C. &. L.-G. A., 2015. Social Statistics for a diverse society. Thousand Oaks, CA: Sage

Publications.

Irving, J. G., 1950. Probability and the Weighing Evidence. s.l.:s.n.

Jordan, Stephen , A. R., Randolph, W. W. & Bradford, D., 2010. Fundamentals of corporate finance.

Boston: McGraw-Hill Irwin.

Knight, K., 2000. Mathematical Statistics- Volume in Texts in Statistical Scence Series. s.l.:Chapman

and Hall.

Krishnamoorthy, K., 2005. Handbook of Statistical Distributions with Applications. s.l.:s.n.

Lind, D. A. M. W. G. &. W. S. A., 2008. Statistical Techniques in Business &. Boston.: McGraw-Hill

Irwin.

Meigs, Walter, B. & Robert , F., 1970. Financial Accounting. s.l.:McGraw-Hill Book Company.

Sid, M., Anandi, P. S. & Robert, A. C., 2007. Practicing Financial Planning for Proffesionals.

s.l.:Rochester Hills Publishing.

Stuart A., O. K. A. S., 1999. Kendall’s Advanced Theory of Statistics: Volume 2A- Classical Inference &

the linear Model.. s.l.:s.n.

Suhov, Y. & Kelbert, M., 2005. Probability and Statisics by exasmple. basic probability and statistics.

s.l.:s.n.

Tim, S., 2005. Mastering Statistical Process Control: A handbook for Performance Improvement Using

Cases. s.l.:s.n.

9

References

Ana, M., Jose, G. B. & Jorge, A. . L., 2003. Stochastic Models: Symposium on Probability and

Stochastic Processes. s.l.:s.n.

David, J. S. & David, S., 2000. Handbook of parametric and nonparametric statistical Procedures.

s.l.:s.n.

Frank, E. & Harrell, J., 2001. Regression Modelling Strategies: Models, Logistic Regression, and

Survival Analysis. s.l.:s.n.

Frankfort-Nachias, C. &. L.-G. A., 2015. Social Statistics for a diverse society. Thousand Oaks, CA: Sage

Publications.

Irving, J. G., 1950. Probability and the Weighing Evidence. s.l.:s.n.

Jordan, Stephen , A. R., Randolph, W. W. & Bradford, D., 2010. Fundamentals of corporate finance.

Boston: McGraw-Hill Irwin.

Knight, K., 2000. Mathematical Statistics- Volume in Texts in Statistical Scence Series. s.l.:Chapman

and Hall.

Krishnamoorthy, K., 2005. Handbook of Statistical Distributions with Applications. s.l.:s.n.

Lind, D. A. M. W. G. &. W. S. A., 2008. Statistical Techniques in Business &. Boston.: McGraw-Hill

Irwin.

Meigs, Walter, B. & Robert , F., 1970. Financial Accounting. s.l.:McGraw-Hill Book Company.

Sid, M., Anandi, P. S. & Robert, A. C., 2007. Practicing Financial Planning for Proffesionals.

s.l.:Rochester Hills Publishing.

Stuart A., O. K. A. S., 1999. Kendall’s Advanced Theory of Statistics: Volume 2A- Classical Inference &

the linear Model.. s.l.:s.n.

Suhov, Y. & Kelbert, M., 2005. Probability and Statisics by exasmple. basic probability and statistics.

s.l.:s.n.

Tim, S., 2005. Mastering Statistical Process Control: A handbook for Performance Improvement Using

Cases. s.l.:s.n.

9

1 out of 9

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

© 2024 | Zucol Services PVT LTD | All rights reserved.