FNS40815 Assessment Task

VerifiedAdded on 2019/10/31

|41

|11459

|2762

Practical Assignment

AI Summary

This document presents a comprehensive assessment task for the FNS40815 Certificate IV in Finance and Mortgage Broking course offered by Mentor Education Group Pty Ltd. The assessment is divided into eight tasks, covering various aspects of mortgage broking, including compliance requirements, customer service, occupational health and safety (OHS), professional development, client relationship management, credit promotion, loan application preparation, and credit provider procedures. Each task includes multiple questions and scenarios requiring detailed written answers, demonstrating the student's understanding of relevant legislation, regulations, and industry best practices. The assessment emphasizes the importance of ethical conduct, client communication, risk management, and professional development within the mortgage broking industry. The provided solution includes detailed answers to all questions, offering a valuable resource for students preparing for this assessment. The website offers past papers and solved assignments to assist students in their studies.

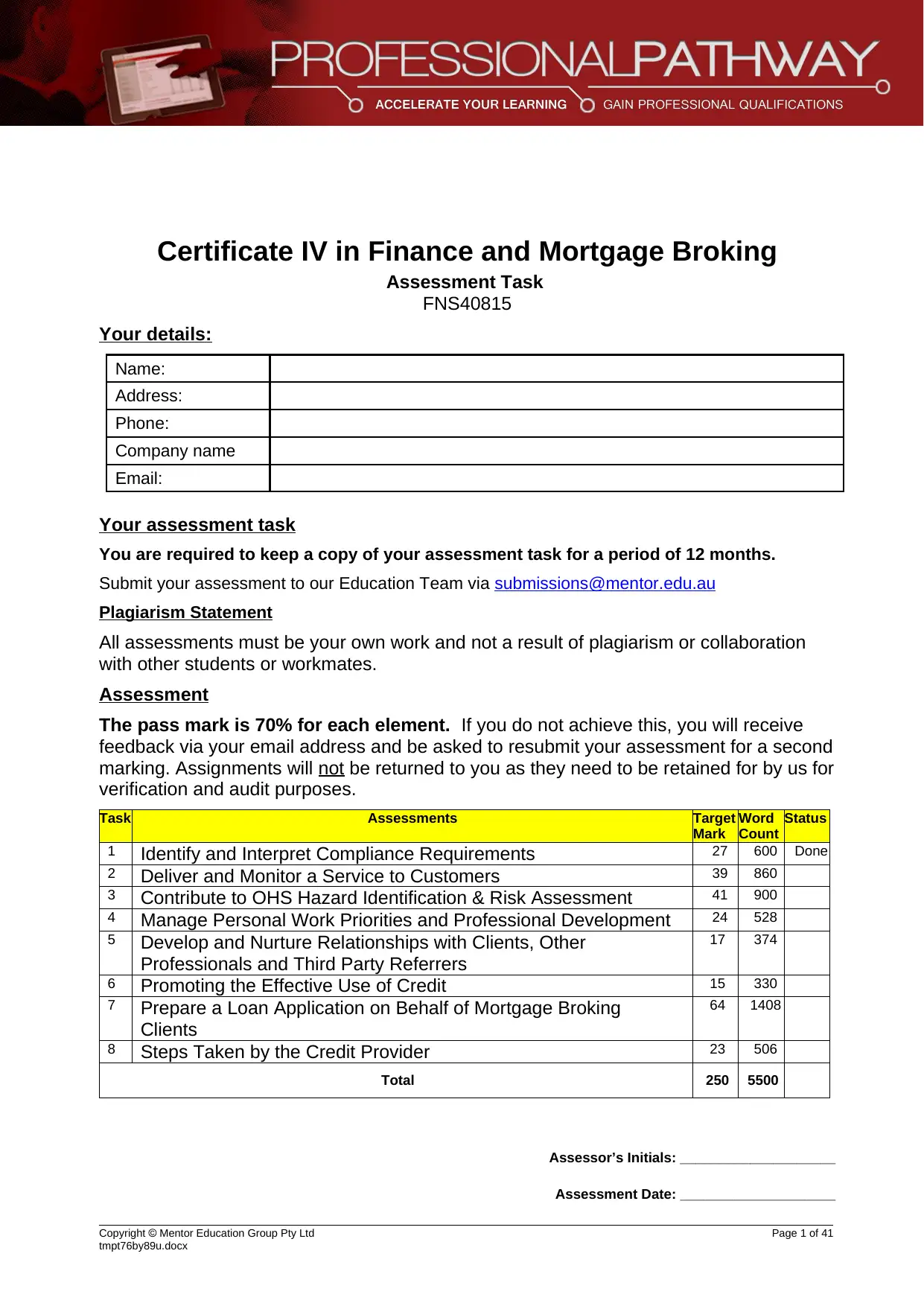

Certificate IV in Finance and Mortgage Broking

Assessment Task

FNS40815

Your details:

Name:

Address:

Phone:

Company name

Email:

Your assessment task

You are required to keep a copy of your assessment task for a period of 12 months.

Submit your assessment to our Education Team via submissions@mentor.edu.au

Plagiarism Statement

All assessments must be your own work and not a result of plagiarism or collaboration

with other students or workmates.

Assessment

The pass mark is 70% for each element. If you do not achieve this, you will receive

feedback via your email address and be asked to resubmit your assessment for a second

marking. Assignments will not be returned to you as they need to be retained for by us for

verification and audit purposes.

Task Assessments Target

Mark

Word

Count

Status

1 Identify and Interpret Compliance Requirements 27 600 Done

2 Deliver and Monitor a Service to Customers 39 860

3 Contribute to OHS Hazard Identification & Risk Assessment 41 900

4 Manage Personal Work Priorities and Professional Development 24 528

5 Develop and Nurture Relationships with Clients, Other

Professionals and Third Party Referrers

17 374

6 Promoting the Effective Use of Credit 15 330

7 Prepare a Loan Application on Behalf of Mortgage Broking

Clients

64 1408

8 Steps Taken by the Credit Provider 23 506

Total 250 5500

Assessor’s Initials: ____________________

Assessment Date: ____________________

Copyright Mentor Education Group Pty Ltd Page 1 of 41

tmpt76by89u.docx

Assessment Task

FNS40815

Your details:

Name:

Address:

Phone:

Company name

Email:

Your assessment task

You are required to keep a copy of your assessment task for a period of 12 months.

Submit your assessment to our Education Team via submissions@mentor.edu.au

Plagiarism Statement

All assessments must be your own work and not a result of plagiarism or collaboration

with other students or workmates.

Assessment

The pass mark is 70% for each element. If you do not achieve this, you will receive

feedback via your email address and be asked to resubmit your assessment for a second

marking. Assignments will not be returned to you as they need to be retained for by us for

verification and audit purposes.

Task Assessments Target

Mark

Word

Count

Status

1 Identify and Interpret Compliance Requirements 27 600 Done

2 Deliver and Monitor a Service to Customers 39 860

3 Contribute to OHS Hazard Identification & Risk Assessment 41 900

4 Manage Personal Work Priorities and Professional Development 24 528

5 Develop and Nurture Relationships with Clients, Other

Professionals and Third Party Referrers

17 374

6 Promoting the Effective Use of Credit 15 330

7 Prepare a Loan Application on Behalf of Mortgage Broking

Clients

64 1408

8 Steps Taken by the Credit Provider 23 506

Total 250 5500

Assessor’s Initials: ____________________

Assessment Date: ____________________

Copyright Mentor Education Group Pty Ltd Page 1 of 41

tmpt76by89u.docx

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Introduction

Objective The objective of this Assessment Task is to demonstrate that you have the

skills and knowledge required to conduct a client relationship and comply with

statutory, industry and organization compliance requirements.

Elements to

be assessed

To achieve this objective, you will need to demonstrate your ability to:

The assessment tasks in this assessment will allow you to demonstrate your

knowledge and skills in relation to these elements.

Assessment

process

Start by:

1. Reading the Assessment Task.

2. Type your answers to the assessment tasks into this template document

(hand-written answers are not accepted)

3. Submit your completed document by uploading it on the ‘Ready for

Assessment’ area of www.CPDplus.com

Don’t forget to keep a copy and retain it for 12 months.

Need help? If you have any questions or would like to request a digital copy of this

assessment task, please email the Mentor Support Team at

service@mentor.edu.au

Statement of

Completion

Upon successful completion of this assessment you will be awarded the

Statement of Completion for FNS40811 Certificate 4 in Finance and Mortgage

Broking.

Copyright Mentor Education Group Pty Ltd Page 2 of 41

tmpt76by89u.docx

Objective The objective of this Assessment Task is to demonstrate that you have the

skills and knowledge required to conduct a client relationship and comply with

statutory, industry and organization compliance requirements.

Elements to

be assessed

To achieve this objective, you will need to demonstrate your ability to:

The assessment tasks in this assessment will allow you to demonstrate your

knowledge and skills in relation to these elements.

Assessment

process

Start by:

1. Reading the Assessment Task.

2. Type your answers to the assessment tasks into this template document

(hand-written answers are not accepted)

3. Submit your completed document by uploading it on the ‘Ready for

Assessment’ area of www.CPDplus.com

Don’t forget to keep a copy and retain it for 12 months.

Need help? If you have any questions or would like to request a digital copy of this

assessment task, please email the Mentor Support Team at

service@mentor.edu.au

Statement of

Completion

Upon successful completion of this assessment you will be awarded the

Statement of Completion for FNS40811 Certificate 4 in Finance and Mortgage

Broking.

Copyright Mentor Education Group Pty Ltd Page 2 of 41

tmpt76by89u.docx

Task 1: Identify and Interpret Compliance Requirements

1. Identify

compliance

requirements

Mortgage brokers face important compliance requirements, the foremost among

them being the reasonable lending provisions of the NCCP Act. The penalties for

non-compliance include loss of license (for businesses) and removal from the

industry (for individuals). If fraud is involved there may also be the criminal

penalties of fines and / or imprisonment.

Compliance requirements are not static. It is therefore important to stay up to

date with them.

Mortgage brokers also need to keep up-to-date with the actions of the regulatory

authorities such as APRA and the Reserve Bank. Their actions may not amount

to direct regulation, but through their effects on interest rates and bank lending

these authorities can have a very direct impact on the business mortgage

brokers are able to do.

(a) A key requirement of the responsible lending obligations is the ‘unsuitability test.’ What must a

mortgage do to comply with the unsuitability test?

No Mark

1. /1

2. /1

3. /1

(b) List the sorts of items a client’s requirements and objectives could include (as indicated by

ASIC).

Mark

/2

(c) Leading credit providers and other financial organisations have code of ethics, sometime

called codes of conduct. Select one of them and summarise it by itemising its main principles.

Mark

/4

Sub-total /9

Continued

Copyright Mentor Education Group Pty Ltd Page 3 of 41

tmpt76by89u.docx

1. Identify

compliance

requirements

Mortgage brokers face important compliance requirements, the foremost among

them being the reasonable lending provisions of the NCCP Act. The penalties for

non-compliance include loss of license (for businesses) and removal from the

industry (for individuals). If fraud is involved there may also be the criminal

penalties of fines and / or imprisonment.

Compliance requirements are not static. It is therefore important to stay up to

date with them.

Mortgage brokers also need to keep up-to-date with the actions of the regulatory

authorities such as APRA and the Reserve Bank. Their actions may not amount

to direct regulation, but through their effects on interest rates and bank lending

these authorities can have a very direct impact on the business mortgage

brokers are able to do.

(a) A key requirement of the responsible lending obligations is the ‘unsuitability test.’ What must a

mortgage do to comply with the unsuitability test?

No Mark

1. /1

2. /1

3. /1

(b) List the sorts of items a client’s requirements and objectives could include (as indicated by

ASIC).

Mark

/2

(c) Leading credit providers and other financial organisations have code of ethics, sometime

called codes of conduct. Select one of them and summarise it by itemising its main principles.

Mark

/4

Sub-total /9

Continued

Copyright Mentor Education Group Pty Ltd Page 3 of 41

tmpt76by89u.docx

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

(d) In point form, list the key information that the NCCP Act requires to be contained in a Credit

Guide.

Mark

/3

(e) It is important to keep up to date with compliance requirements so that the required changes

can be made to organization procedures and product offerings. Suggest three sources that

you can use.

Mark

/3

(f) Explain the requirement for Australian Credit Licensees to keep a training register.

Mark

/2

(g) Explain APRA’s current attitude towards bank lending for investment properties.

Mark

/2

Sub-total / 10

Continued

Copyright Mentor Education Group Pty Ltd Page 4 of 41

tmpt76by89u.docx

Guide.

Mark

/3

(e) It is important to keep up to date with compliance requirements so that the required changes

can be made to organization procedures and product offerings. Suggest three sources that

you can use.

Mark

/3

(f) Explain the requirement for Australian Credit Licensees to keep a training register.

Mark

/2

(g) Explain APRA’s current attitude towards bank lending for investment properties.

Mark

/2

Sub-total / 10

Continued

Copyright Mentor Education Group Pty Ltd Page 4 of 41

tmpt76by89u.docx

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Task 1: Identify and Interpret Compliance Requirements Continued

1.2

Interpret,

analyse

and

prioritise

identified

complian

ce

requirem

ents

Some of the compliance requirements are difficult to meet. Unfortunately, also

there have been some ‘rogue’ mortgage brokers who have failed to comply – to the

disadvantage of their clients.

The finance planning industry has been plagued by non-compliance in the largest

planning groups, with the image of the industry being substantially tarnished as a

result. It may not suffer greatly because of the absence of an alternative source of

financial advice.

This is not so with mortgage brokers. They are just establishing their reputation and

consumers always have alternative of going to the lenders directly.

(a) Select three tasks you perform on a regular basis that are subject to compliance

requirements.

No Mark

1. /1

2. /1

3. /1

(b) Identify the compliance requirements that are relevant to the three tasks selected, indicating

the name of the relevant legislation, regulation or code of conduct.

No

1. /1

2. /1

3. /1

(c) How does your organisation monitor your compliance?

Mark

/2

Sub-total /8

Continued

Total /27

Copyright Mentor Education Group Pty Ltd Page 5 of 41

tmpt76by89u.docx

1.2

Interpret,

analyse

and

prioritise

identified

complian

ce

requirem

ents

Some of the compliance requirements are difficult to meet. Unfortunately, also

there have been some ‘rogue’ mortgage brokers who have failed to comply – to the

disadvantage of their clients.

The finance planning industry has been plagued by non-compliance in the largest

planning groups, with the image of the industry being substantially tarnished as a

result. It may not suffer greatly because of the absence of an alternative source of

financial advice.

This is not so with mortgage brokers. They are just establishing their reputation and

consumers always have alternative of going to the lenders directly.

(a) Select three tasks you perform on a regular basis that are subject to compliance

requirements.

No Mark

1. /1

2. /1

3. /1

(b) Identify the compliance requirements that are relevant to the three tasks selected, indicating

the name of the relevant legislation, regulation or code of conduct.

No

1. /1

2. /1

3. /1

(c) How does your organisation monitor your compliance?

Mark

/2

Sub-total /8

Continued

Total /27

Copyright Mentor Education Group Pty Ltd Page 5 of 41

tmpt76by89u.docx

Task 2: Deliver and Monitor a Service to Customers

2.

Identify

customer

needs

The relationship with a client is generally described as beginning with the

establishment of empathy. In other words, it is first necessary for a mortgage

broker to establish that he / she is truly interested in the client and the client’s

needs. It is only after that that the mortgage broker has established the right to

interview a client.

(a) Use the internet or any other source to find a definition of empathy.

Mark

Empathy is an emotion between sympathy and affection. It is a feeling which someone

expresses to someone else.

/1

(b) List three open-ended questions that assist in developing empathy with a client? How do such

questions indicate empathy?

No. Mark

Are you comfortable with our services?

What are the problems that you are experiencing?

Can anything else be done to help you further with your current problem?

/2

The fact that in each question an effort has been made to comfort the client indicate

empathy.

/1

(c) List and explain the steps involved in an ‘active listening approach’.

Mark

Concentrate completely on what speaker is saying. /1

Do not ask any question while the speaker is speaking. /1

Have a clear mind while listening to the speaker. /1

(d) How is client service commonly monitored in your organisation? What are the two possible

outcomes?

No. Mark

1. In order to monitor the client services in an organization the following standards

procedure shall be followed:

I. A clear strategy shall be there to improve the quality of services that are

being provided to clients.

II. Survey should conducted on the clients to find out the quality of services

they expect from the organization.

III. A system of feedback shall be instituted within the organization to

accumulate the feedback of clients on quality of services that are being

provided by the organization.

IV. Continuous endeavor to improve the quality of services.

/1

Copyright Mentor Education Group Pty Ltd Page 6 of 41

tmpt76by89u.docx

2.

Identify

customer

needs

The relationship with a client is generally described as beginning with the

establishment of empathy. In other words, it is first necessary for a mortgage

broker to establish that he / she is truly interested in the client and the client’s

needs. It is only after that that the mortgage broker has established the right to

interview a client.

(a) Use the internet or any other source to find a definition of empathy.

Mark

Empathy is an emotion between sympathy and affection. It is a feeling which someone

expresses to someone else.

/1

(b) List three open-ended questions that assist in developing empathy with a client? How do such

questions indicate empathy?

No. Mark

Are you comfortable with our services?

What are the problems that you are experiencing?

Can anything else be done to help you further with your current problem?

/2

The fact that in each question an effort has been made to comfort the client indicate

empathy.

/1

(c) List and explain the steps involved in an ‘active listening approach’.

Mark

Concentrate completely on what speaker is saying. /1

Do not ask any question while the speaker is speaking. /1

Have a clear mind while listening to the speaker. /1

(d) How is client service commonly monitored in your organisation? What are the two possible

outcomes?

No. Mark

1. In order to monitor the client services in an organization the following standards

procedure shall be followed:

I. A clear strategy shall be there to improve the quality of services that are

being provided to clients.

II. Survey should conducted on the clients to find out the quality of services

they expect from the organization.

III. A system of feedback shall be instituted within the organization to

accumulate the feedback of clients on quality of services that are being

provided by the organization.

IV. Continuous endeavor to improve the quality of services.

/1

Copyright Mentor Education Group Pty Ltd Page 6 of 41

tmpt76by89u.docx

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

2. I. Improvement in quality of services that are offered by an organization.

II. Increase amount of customer / client satisfaction.

/2

Sub-total /10

Continued

Task 2: Deliver and Monitor a Service to Customers Continued

2.1 Deliver

a service to

customers

In a survey on the reasons for referrals conducted by David Maister, only 10%

were due to the quality of technical work. The remaining 90% of referrals were due

to the quality of service.

This indicates that the key to maintaining client relationships and gaining referrals

is the provision of outstanding service. This has been described by Maister as

‘over-servicing’.

(a) Describe three ways in which a mortgage broking organisation can attempt to ‘overservice’

clients?

No. Mark

1. Huge increase in marketing and advertisement to attract client. /1

2. Making a pitch for sale always. /1

3. Making a pitch for purchase always. /1

(b) How would you keep a client informed about the progress of an application as it passed through a

creditor provider’s hands? What approximate timing might be involved?

No. Mark

1. Effective communication with the client by using calling services about the progress of an

application as it passed through a creditor provider’s hands. Providing timely response to the

clients and customers is essential to the success of a broking business thus, it is important to have a

great customer service to clients and customers up-to-date with progress in different matters.

/2

2. A period of 12 months is approximate time for ensuring that proper communication is made with

the client to let him know about the status of such application.

/2

(c) Describe how you might attempt to resolve conflicts with clients.

Mark

Discussion with the client is one of the most effective ways to resolve conflicts and disagreement

with client. Understanding the issue on which the conflict has arisen between the organization

and the client, then a discussion on the issue with the client could be very helpful in resolving such

/2

Copyright Mentor Education Group Pty Ltd Page 7 of 41

tmpt76by89u.docx

II. Increase amount of customer / client satisfaction.

/2

Sub-total /10

Continued

Task 2: Deliver and Monitor a Service to Customers Continued

2.1 Deliver

a service to

customers

In a survey on the reasons for referrals conducted by David Maister, only 10%

were due to the quality of technical work. The remaining 90% of referrals were due

to the quality of service.

This indicates that the key to maintaining client relationships and gaining referrals

is the provision of outstanding service. This has been described by Maister as

‘over-servicing’.

(a) Describe three ways in which a mortgage broking organisation can attempt to ‘overservice’

clients?

No. Mark

1. Huge increase in marketing and advertisement to attract client. /1

2. Making a pitch for sale always. /1

3. Making a pitch for purchase always. /1

(b) How would you keep a client informed about the progress of an application as it passed through a

creditor provider’s hands? What approximate timing might be involved?

No. Mark

1. Effective communication with the client by using calling services about the progress of an

application as it passed through a creditor provider’s hands. Providing timely response to the

clients and customers is essential to the success of a broking business thus, it is important to have a

great customer service to clients and customers up-to-date with progress in different matters.

/2

2. A period of 12 months is approximate time for ensuring that proper communication is made with

the client to let him know about the status of such application.

/2

(c) Describe how you might attempt to resolve conflicts with clients.

Mark

Discussion with the client is one of the most effective ways to resolve conflicts and disagreement

with client. Understanding the issue on which the conflict has arisen between the organization

and the client, then a discussion on the issue with the client could be very helpful in resolving such

/2

Copyright Mentor Education Group Pty Ltd Page 7 of 41

tmpt76by89u.docx

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

issue. Information is another important component that helps in resolving conflicts as often wrong

information leads to conflicts between the client and an organization.

(d) How do you can prepare clients for the hiccups that can happen while their credit application is being

processed

Mark

A complete way through shall be provided to the client and he shall be made aware of the various situations

that he might have to face over the period of time during which the status of the application shows pending.

An in-depth discussion shall be held with the client to make him aware of various issues that might arise in

the future in the application stage. This will help the client to deal with various issues that generally arise in

application stage.

/2

Sub-total /11

Continued

(e) The chapter on Operating a Mortgage Broking Business contains an example suggesting that a

mortgage broker acting in the best interests of clients should act as a Protector rather than an Expert.

What are the implications for this in regard to (i) advice given to clients and (ii) recommending the

most suitable loan products?.

No. Mark

1. The client should be advised with more caution than flamboyance. Only the deals that will surely

benefit a client should be suggested to the client. Thus, even if there is a minute chance of any

issue that a client might be facing the expert shall withdraw the client engagement from such

deals.

/2

2. The most suitable loan products are the ones that bear minimum rate of interests and have other

beneficiary attributes for a client. The repayment scheme of suitable loan products shall be

beneficiary to a client from every aspects.

/2

(f) How could you prepare yourself to deal with client concerns?

Mark

A thorough knowledge of the market is vital to deal with the concerns of clients. Along with the knowledge

of the market the client should have good communication skill to be able to communicate different matters

clearly with the clients. Thus, one should work on their communication skills to prepare his / herself to deal

with clients’ concerns.

/2

(g) Give examples of the following legal breaches: breach of the duty of care, false and

misleading conduct, unconscionable conduct & conflict of interest without disclosure.

No. Mark

Copyright Mentor Education Group Pty Ltd Page 8 of 41

tmpt76by89u.docx

information leads to conflicts between the client and an organization.

(d) How do you can prepare clients for the hiccups that can happen while their credit application is being

processed

Mark

A complete way through shall be provided to the client and he shall be made aware of the various situations

that he might have to face over the period of time during which the status of the application shows pending.

An in-depth discussion shall be held with the client to make him aware of various issues that might arise in

the future in the application stage. This will help the client to deal with various issues that generally arise in

application stage.

/2

Sub-total /11

Continued

(e) The chapter on Operating a Mortgage Broking Business contains an example suggesting that a

mortgage broker acting in the best interests of clients should act as a Protector rather than an Expert.

What are the implications for this in regard to (i) advice given to clients and (ii) recommending the

most suitable loan products?.

No. Mark

1. The client should be advised with more caution than flamboyance. Only the deals that will surely

benefit a client should be suggested to the client. Thus, even if there is a minute chance of any

issue that a client might be facing the expert shall withdraw the client engagement from such

deals.

/2

2. The most suitable loan products are the ones that bear minimum rate of interests and have other

beneficiary attributes for a client. The repayment scheme of suitable loan products shall be

beneficiary to a client from every aspects.

/2

(f) How could you prepare yourself to deal with client concerns?

Mark

A thorough knowledge of the market is vital to deal with the concerns of clients. Along with the knowledge

of the market the client should have good communication skill to be able to communicate different matters

clearly with the clients. Thus, one should work on their communication skills to prepare his / herself to deal

with clients’ concerns.

/2

(g) Give examples of the following legal breaches: breach of the duty of care, false and

misleading conduct, unconscionable conduct & conflict of interest without disclosure.

No. Mark

Copyright Mentor Education Group Pty Ltd Page 8 of 41

tmpt76by89u.docx

1. Engaging clients in deals which will not be very beneficiary to them despite existence of better

deals.

/1

2. Convincing clients to enter into loss making deal knowing such deals will end up making losses for

the clients for personal benefit.

/1

3. Allowing the clients to enter into wrong and bad deals despite having prior knowledge of the same. /1

4. Making money by convincing client to enter into a particular deal at the exception of the other

deals and not disclosing the benefit to the client.

/1

(h) Once a desirable market segment has been identified, a mortgage broking business can put

its mind o developing suitable marketing strategies. List examples of different strategies that

might be used.

Mark

Aggressive marketing and promotional campaign shall be help to promote the desirable market

segment to attract customers.

Convincing the clients to engage themselves to understand the components of the market.

Engaging the clients to make them feel part of the whole proceeding.

Listing the probable benefits of different products in the market and how the clients can be financially

benefitted from these products.

/2

Sub-total /12

Continued

(i) What steps can be taken to keep up to date with product changes and ensure that this

knowledge is properly disseminated?

Mark

Shall be kept up-to-dated by keeping necessary information about different products and changes that have

been made in the characteristics of these products. In case of disposal of any old product and

introduction of a new product the reasons shall be searched and verified for gather further knowledge

that will be helpful for the future.

/2

(j) What are the procedures for dealing with client complaints in your organisation?

Copyright Mentor Education Group Pty Ltd Page 9 of 41

tmpt76by89u.docx

deals.

/1

2. Convincing clients to enter into loss making deal knowing such deals will end up making losses for

the clients for personal benefit.

/1

3. Allowing the clients to enter into wrong and bad deals despite having prior knowledge of the same. /1

4. Making money by convincing client to enter into a particular deal at the exception of the other

deals and not disclosing the benefit to the client.

/1

(h) Once a desirable market segment has been identified, a mortgage broking business can put

its mind o developing suitable marketing strategies. List examples of different strategies that

might be used.

Mark

Aggressive marketing and promotional campaign shall be help to promote the desirable market

segment to attract customers.

Convincing the clients to engage themselves to understand the components of the market.

Engaging the clients to make them feel part of the whole proceeding.

Listing the probable benefits of different products in the market and how the clients can be financially

benefitted from these products.

/2

Sub-total /12

Continued

(i) What steps can be taken to keep up to date with product changes and ensure that this

knowledge is properly disseminated?

Mark

Shall be kept up-to-dated by keeping necessary information about different products and changes that have

been made in the characteristics of these products. In case of disposal of any old product and

introduction of a new product the reasons shall be searched and verified for gather further knowledge

that will be helpful for the future.

/2

(j) What are the procedures for dealing with client complaints in your organisation?

Copyright Mentor Education Group Pty Ltd Page 9 of 41

tmpt76by89u.docx

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Mark

Checking the issues that the clients have listed in his / her complaint.

Proper investigation shall be made to see whether the accusations are true or not.

Based on the findings of the investigation necessary decisions shall be made on the complaints of the

clients.

/2

(k) What normal protocols should for protecting the confidentiality of client files?

Mark

Keeping the files in a safe and secure place with proper lock and key system in place.

Ensuring that only those who are authorised to see the files of the clients are using such files.

No unauthorised person shall be allowed to open the safe and lockers where the clients files have

been stored for confidentiality and security purposes.

/2

Sub-total /6

Total /39

Copyright Mentor Education Group Pty Ltd Page 10 of 41

tmpt76by89u.docx

Checking the issues that the clients have listed in his / her complaint.

Proper investigation shall be made to see whether the accusations are true or not.

Based on the findings of the investigation necessary decisions shall be made on the complaints of the

clients.

/2

(k) What normal protocols should for protecting the confidentiality of client files?

Mark

Keeping the files in a safe and secure place with proper lock and key system in place.

Ensuring that only those who are authorised to see the files of the clients are using such files.

No unauthorised person shall be allowed to open the safe and lockers where the clients files have

been stored for confidentiality and security purposes.

/2

Sub-total /6

Total /39

Copyright Mentor Education Group Pty Ltd Page 10 of 41

tmpt76by89u.docx

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Task 3: Contribute to OHS Hazard Identification & Risk Assessment

3. Contribute

to workplace

hazard

identificatio

n

Occupational health and safety hazards are often considered only in terms of

physical injury, perhaps the result of working with heavy machinery, working in an

excessively noisy environment, or slipping or falling. Just as relevant, however, is

work-related stress. This describes the physical, mental and emotional

reactions of workers who perceive that their work demands exceed their

abilities and/or their resources (such as time, help/support) to do the work.

For the questions that follow, please read ‘Overview of Work-related Stress’

from the NSW Government. It may be found at:

http://www.safework.nsw.gov.au/__data/assets/pdf_file/0008/99233/overview-

work-related-stress-6071.pdf

Other ‘Tip Sheets’ from the same website may also be useful.

(a) How would you define workplace stress?

Mark

Work place stress is the emotional fatigue and feeling of a void which comes with the

excessive pressure of performance at the work place. The feeling of lack of motivation due

to working in a particular environment day in day out is also attributable to emotional

stress.

/4

(b) Suggest at least two ways in which work-related stress may affect client relationships.

Mark

I. Inability to serve the clients due to work related stress in employees and

workers.

II. Lack of effective communication due to stress factors in the work place.

/2

(c) Suggest at least four approaches you can take to reduce workplace stress? (Hint: you may

find suggested ways if you key ‘handling workplace stress’ into a search engine).

Mark

I. Efforts to create a friendly environment at the place of work.

II. Allowing the employees and workers to communicate freely with each other to

ensure there is enough discussions between them to make them feel happy

and contained at the work place.

III. Creating group culture within the organization so that there is bonding between

the employees and workers.

IV. Taking the employees and workers into confidence and engaging them in every

important decisions making process to make them feel an important part of an

organization.

V. Planning official picnics and get a ways to create a friendly environment within

the employees and workers.

/4

Copyright Mentor Education Group Pty Ltd Page 11 of 41

tmpt76by89u.docx

3. Contribute

to workplace

hazard

identificatio

n

Occupational health and safety hazards are often considered only in terms of

physical injury, perhaps the result of working with heavy machinery, working in an

excessively noisy environment, or slipping or falling. Just as relevant, however, is

work-related stress. This describes the physical, mental and emotional

reactions of workers who perceive that their work demands exceed their

abilities and/or their resources (such as time, help/support) to do the work.

For the questions that follow, please read ‘Overview of Work-related Stress’

from the NSW Government. It may be found at:

http://www.safework.nsw.gov.au/__data/assets/pdf_file/0008/99233/overview-

work-related-stress-6071.pdf

Other ‘Tip Sheets’ from the same website may also be useful.

(a) How would you define workplace stress?

Mark

Work place stress is the emotional fatigue and feeling of a void which comes with the

excessive pressure of performance at the work place. The feeling of lack of motivation due

to working in a particular environment day in day out is also attributable to emotional

stress.

/4

(b) Suggest at least two ways in which work-related stress may affect client relationships.

Mark

I. Inability to serve the clients due to work related stress in employees and

workers.

II. Lack of effective communication due to stress factors in the work place.

/2

(c) Suggest at least four approaches you can take to reduce workplace stress? (Hint: you may

find suggested ways if you key ‘handling workplace stress’ into a search engine).

Mark

I. Efforts to create a friendly environment at the place of work.

II. Allowing the employees and workers to communicate freely with each other to

ensure there is enough discussions between them to make them feel happy

and contained at the work place.

III. Creating group culture within the organization so that there is bonding between

the employees and workers.

IV. Taking the employees and workers into confidence and engaging them in every

important decisions making process to make them feel an important part of an

organization.

V. Planning official picnics and get a ways to create a friendly environment within

the employees and workers.

/4

Copyright Mentor Education Group Pty Ltd Page 11 of 41

tmpt76by89u.docx

Sub-total /10

Continued

Task 3: Contribute to OHS Hazard Identification & Risk

Assessment Continued

3.1 Gather

information

about

workplace

hazards

In assisting in the control of work-related hazards, you will need to be access

suitable information.

Please read ‘Glossary of Job Demands and Job Resources’ from the QUT/ANU

People at Work project. It may be found here:

http://web.archive.org/web/20150227212940/http://

www.peopleatworkproject.com.au/LiteratureRetrieve.aspx?ID=174670

(a) Explain the distinction between ‘job demands’ and ‘job resources’ risk factors.

Mark

Job demands are the expectations of the management from the workers and employees of

an organization whereas job resources are the components and resources needed by the

workers and employees to live up to the expectations of the management of such an

organization. Job demands are only possible to be fulfilled if there are enough job

resources available within the organization. Even with best of workers and employees an

organization will not be able to achieve much if there is not enough job resources available

at the workplace.

4/4

(b) Identify two ‘job demands’ risk factors that are relevant to your workplace and describe what

detrimental effect they might have.

No. Mark

1. Over the top expectations of the management from the employees and workers. This

might increase the stress level in the workers at the work place which could be very

detrimental to the overall performance of such organization.

/ 2

2. Putting too much pressure on the workers and employees and not allowing them any

breathing space in order attain certain objectives. This could harm the environment

at the workplace and subsequently the financial performance of such organization.

/ 2

Copyright Mentor Education Group Pty Ltd Page 12 of 41

tmpt76by89u.docx

Continued

Task 3: Contribute to OHS Hazard Identification & Risk

Assessment Continued

3.1 Gather

information

about

workplace

hazards

In assisting in the control of work-related hazards, you will need to be access

suitable information.

Please read ‘Glossary of Job Demands and Job Resources’ from the QUT/ANU

People at Work project. It may be found here:

http://web.archive.org/web/20150227212940/http://

www.peopleatworkproject.com.au/LiteratureRetrieve.aspx?ID=174670

(a) Explain the distinction between ‘job demands’ and ‘job resources’ risk factors.

Mark

Job demands are the expectations of the management from the workers and employees of

an organization whereas job resources are the components and resources needed by the

workers and employees to live up to the expectations of the management of such an

organization. Job demands are only possible to be fulfilled if there are enough job

resources available within the organization. Even with best of workers and employees an

organization will not be able to achieve much if there is not enough job resources available

at the workplace.

4/4

(b) Identify two ‘job demands’ risk factors that are relevant to your workplace and describe what

detrimental effect they might have.

No. Mark

1. Over the top expectations of the management from the employees and workers. This

might increase the stress level in the workers at the work place which could be very

detrimental to the overall performance of such organization.

/ 2

2. Putting too much pressure on the workers and employees and not allowing them any

breathing space in order attain certain objectives. This could harm the environment

at the workplace and subsequently the financial performance of such organization.

/ 2

Copyright Mentor Education Group Pty Ltd Page 12 of 41

tmpt76by89u.docx

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 41

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.