Accounting Assignment: Taxation, Business Combinations, Consolidation

VerifiedAdded on 2021/06/17

|13

|3457

|68

Practical Assignment

AI Summary

This assignment provides detailed solutions to complex financial accounting problems. The first part focuses on the computation of tax payable, including adjustments for various expenses, revenues, and tax payments, culminating in the calculation of net tax payable. It also includes a deferred tax worksheet, outlining temporary differences, and the journal entries to record deferred tax assets and liabilities. The second part delves into acquisition analysis, including acquisition analysis, journal entries to record the acquisition, and the accounting treatment of acquisition-related costs, such as advisor fees and legal fees. The third part covers consolidation, including consolidation journal entries and a consolidated worksheet, addressing topics such as the elimination of unrealized profits and the impact of intra-group transactions, including the sale of inventory and non-current assets. The assignment analyzes various scenarios and provides comprehensive solutions to enhance the understanding of complex accounting concepts.

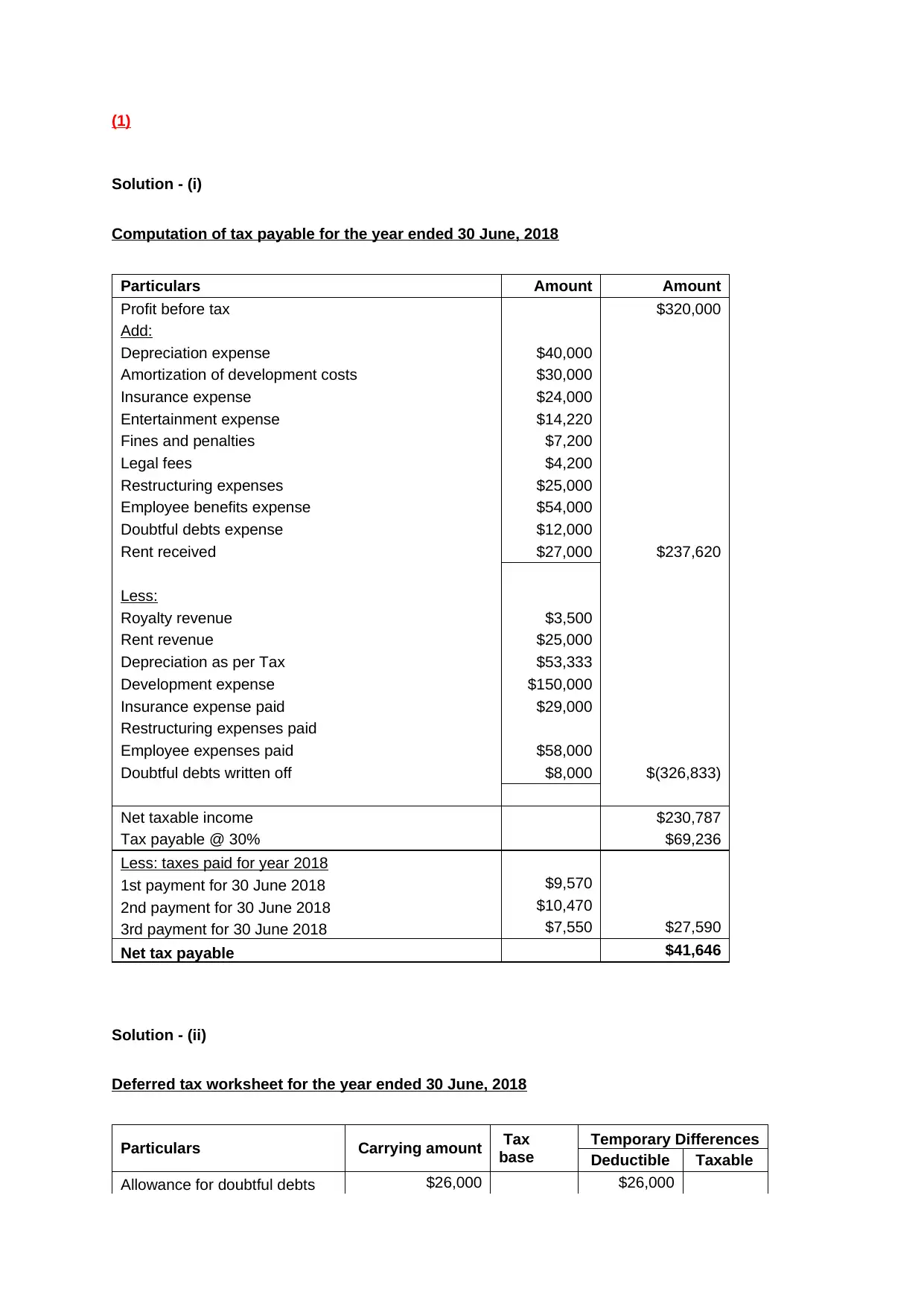

(1)

Solution - (i)

Computation of tax payable for the year ended 30 June, 2018

Particulars Amount Amount

Profit before tax $320,000

Add:

Depreciation expense $40,000

Amortization of development costs $30,000

Insurance expense $24,000

Entertainment expense $14,220

Fines and penalties $7,200

Legal fees $4,200

Restructuring expenses $25,000

Employee benefits expense $54,000

Doubtful debts expense $12,000

Rent received $27,000 $237,620

Less:

Royalty revenue $3,500

Rent revenue $25,000

Depreciation as per Tax $53,333

Development expense $150,000

Insurance expense paid $29,000

Restructuring expenses paid

Employee expenses paid $58,000

Doubtful debts written off $8,000 $(326,833)

Net taxable income $230,787

Tax payable @ 30% $69,236

Less: taxes paid for year 2018

1st payment for 30 June 2018 $9,570

2nd payment for 30 June 2018 $10,470

3rd payment for 30 June 2018 $7,550 $27,590

Net tax payable $41,646

Solution - (ii)

Deferred tax worksheet for the year ended 30 June, 2018

Particulars Carrying amount Tax

base

Temporary Differences

Deductible Taxable

Allowance for doubtful debts $26,000 $26,000

Solution - (i)

Computation of tax payable for the year ended 30 June, 2018

Particulars Amount Amount

Profit before tax $320,000

Add:

Depreciation expense $40,000

Amortization of development costs $30,000

Insurance expense $24,000

Entertainment expense $14,220

Fines and penalties $7,200

Legal fees $4,200

Restructuring expenses $25,000

Employee benefits expense $54,000

Doubtful debts expense $12,000

Rent received $27,000 $237,620

Less:

Royalty revenue $3,500

Rent revenue $25,000

Depreciation as per Tax $53,333

Development expense $150,000

Insurance expense paid $29,000

Restructuring expenses paid

Employee expenses paid $58,000

Doubtful debts written off $8,000 $(326,833)

Net taxable income $230,787

Tax payable @ 30% $69,236

Less: taxes paid for year 2018

1st payment for 30 June 2018 $9,570

2nd payment for 30 June 2018 $10,470

3rd payment for 30 June 2018 $7,550 $27,590

Net tax payable $41,646

Solution - (ii)

Deferred tax worksheet for the year ended 30 June, 2018

Particulars Carrying amount Tax

base

Temporary Differences

Deductible Taxable

Allowance for doubtful debts $26,000 $26,000

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

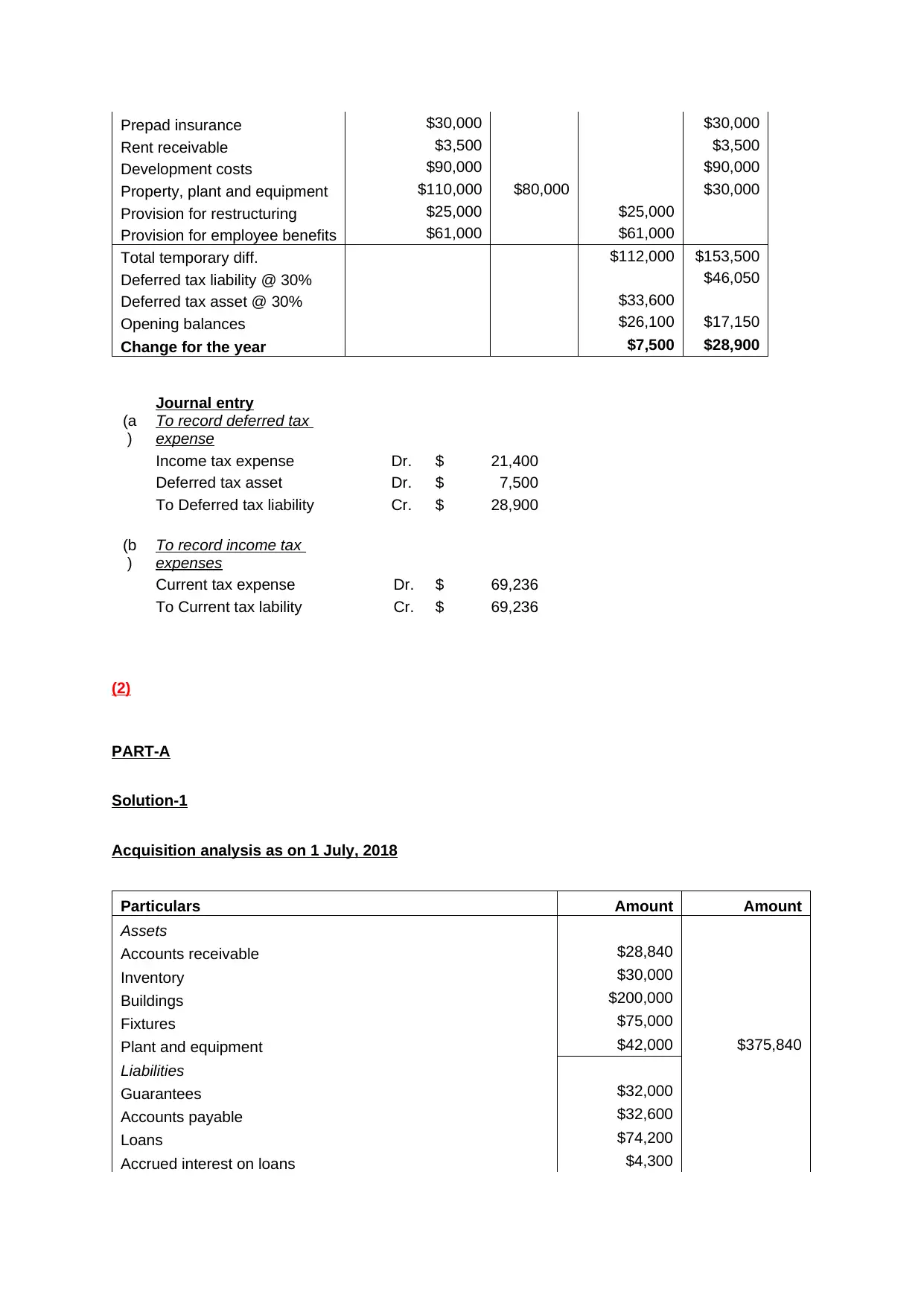

Prepad insurance $30,000 $30,000

Rent receivable $3,500 $3,500

Development costs $90,000 $90,000

Property, plant and equipment $110,000 $80,000 $30,000

Provision for restructuring $25,000 $25,000

Provision for employee benefits $61,000 $61,000

Total temporary diff. $112,000 $153,500

Deferred tax liability @ 30% $46,050

Deferred tax asset @ 30% $33,600

Opening balances $26,100 $17,150

Change for the year $7,500 $28,900

Journal entry

(a

)

To record deferred tax

expense

Income tax expense Dr. $ 21,400

Deferred tax asset Dr. $ 7,500

To Deferred tax liability Cr. $ 28,900

(b

)

To record income tax

expenses

Current tax expense Dr. $ 69,236

To Current tax lability Cr. $ 69,236

(2)

PART-A

Solution-1

Acquisition analysis as on 1 July, 2018

Particulars Amount Amount

Assets

Accounts receivable $28,840

Inventory $30,000

Buildings $200,000

Fixtures $75,000

Plant and equipment $42,000 $375,840

Liabilities

Guarantees $32,000

Accounts payable $32,600

Loans $74,200

Accrued interest on loans $4,300

Rent receivable $3,500 $3,500

Development costs $90,000 $90,000

Property, plant and equipment $110,000 $80,000 $30,000

Provision for restructuring $25,000 $25,000

Provision for employee benefits $61,000 $61,000

Total temporary diff. $112,000 $153,500

Deferred tax liability @ 30% $46,050

Deferred tax asset @ 30% $33,600

Opening balances $26,100 $17,150

Change for the year $7,500 $28,900

Journal entry

(a

)

To record deferred tax

expense

Income tax expense Dr. $ 21,400

Deferred tax asset Dr. $ 7,500

To Deferred tax liability Cr. $ 28,900

(b

)

To record income tax

expenses

Current tax expense Dr. $ 69,236

To Current tax lability Cr. $ 69,236

(2)

PART-A

Solution-1

Acquisition analysis as on 1 July, 2018

Particulars Amount Amount

Assets

Accounts receivable $28,840

Inventory $30,000

Buildings $200,000

Fixtures $75,000

Plant and equipment $42,000 $375,840

Liabilities

Guarantees $32,000

Accounts payable $32,600

Loans $74,200

Accrued interest on loans $4,300

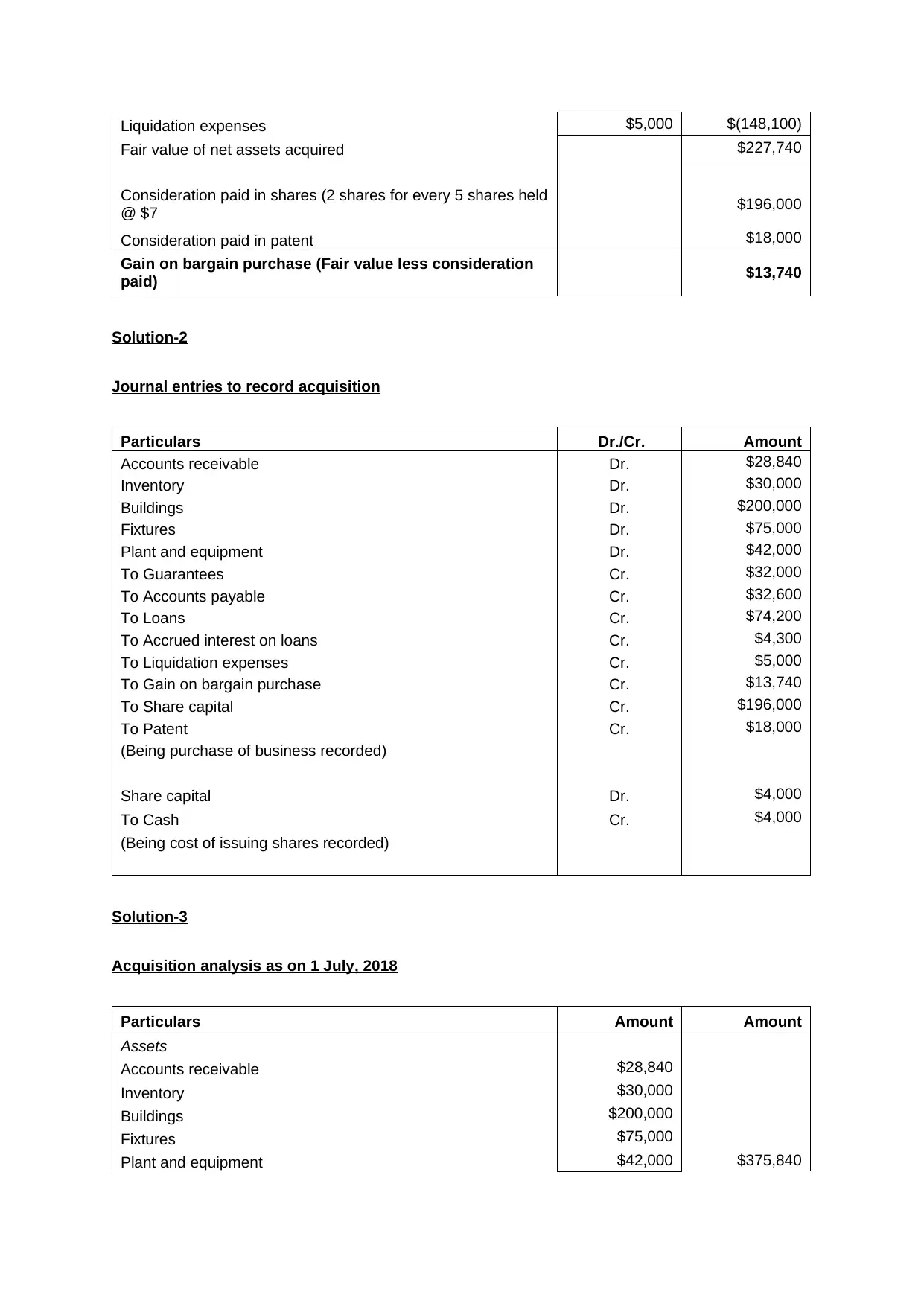

Liquidation expenses $5,000 $(148,100)

Fair value of net assets acquired $227,740

Consideration paid in shares (2 shares for every 5 shares held

@ $7 $196,000

Consideration paid in patent $18,000

Gain on bargain purchase (Fair value less consideration

paid) $13,740

Solution-2

Journal entries to record acquisition

Particulars Dr./Cr. Amount

Accounts receivable Dr. $28,840

Inventory Dr. $30,000

Buildings Dr. $200,000

Fixtures Dr. $75,000

Plant and equipment Dr. $42,000

To Guarantees Cr. $32,000

To Accounts payable Cr. $32,600

To Loans Cr. $74,200

To Accrued interest on loans Cr. $4,300

To Liquidation expenses Cr. $5,000

To Gain on bargain purchase Cr. $13,740

To Share capital Cr. $196,000

To Patent Cr. $18,000

(Being purchase of business recorded)

Share capital Dr. $4,000

To Cash Cr. $4,000

(Being cost of issuing shares recorded)

Solution-3

Acquisition analysis as on 1 July, 2018

Particulars Amount Amount

Assets

Accounts receivable $28,840

Inventory $30,000

Buildings $200,000

Fixtures $75,000

Plant and equipment $42,000 $375,840

Fair value of net assets acquired $227,740

Consideration paid in shares (2 shares for every 5 shares held

@ $7 $196,000

Consideration paid in patent $18,000

Gain on bargain purchase (Fair value less consideration

paid) $13,740

Solution-2

Journal entries to record acquisition

Particulars Dr./Cr. Amount

Accounts receivable Dr. $28,840

Inventory Dr. $30,000

Buildings Dr. $200,000

Fixtures Dr. $75,000

Plant and equipment Dr. $42,000

To Guarantees Cr. $32,000

To Accounts payable Cr. $32,600

To Loans Cr. $74,200

To Accrued interest on loans Cr. $4,300

To Liquidation expenses Cr. $5,000

To Gain on bargain purchase Cr. $13,740

To Share capital Cr. $196,000

To Patent Cr. $18,000

(Being purchase of business recorded)

Share capital Dr. $4,000

To Cash Cr. $4,000

(Being cost of issuing shares recorded)

Solution-3

Acquisition analysis as on 1 July, 2018

Particulars Amount Amount

Assets

Accounts receivable $28,840

Inventory $30,000

Buildings $200,000

Fixtures $75,000

Plant and equipment $42,000 $375,840

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

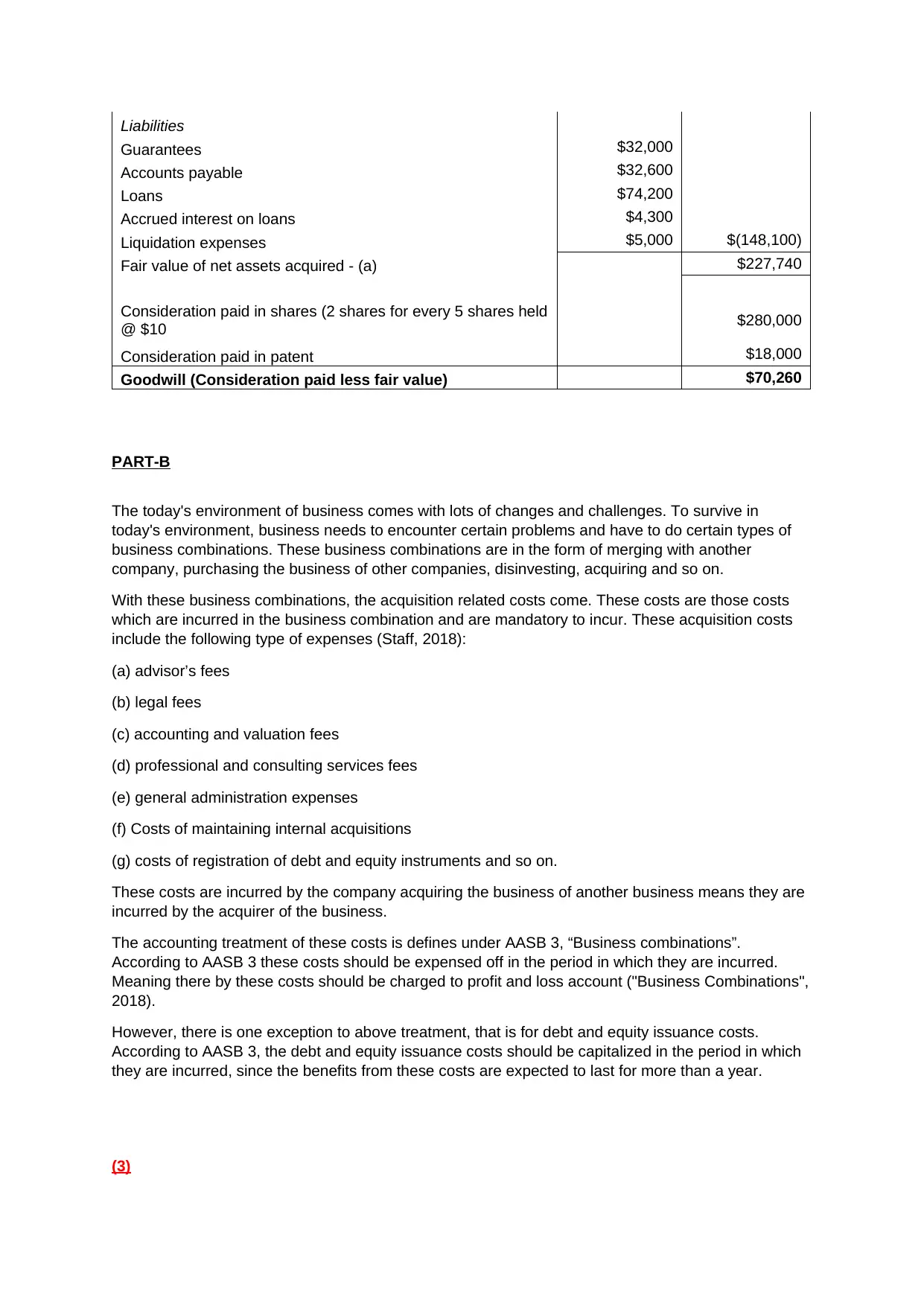

Liabilities

Guarantees $32,000

Accounts payable $32,600

Loans $74,200

Accrued interest on loans $4,300

Liquidation expenses $5,000 $(148,100)

Fair value of net assets acquired - (a) $227,740

Consideration paid in shares (2 shares for every 5 shares held

@ $10 $280,000

Consideration paid in patent $18,000

Goodwill (Consideration paid less fair value) $70,260

PART-B

The today's environment of business comes with lots of changes and challenges. To survive in

today's environment, business needs to encounter certain problems and have to do certain types of

business combinations. These business combinations are in the form of merging with another

company, purchasing the business of other companies, disinvesting, acquiring and so on.

With these business combinations, the acquisition related costs come. These costs are those costs

which are incurred in the business combination and are mandatory to incur. These acquisition costs

include the following type of expenses (Staff, 2018):

(a) advisor’s fees

(b) legal fees

(c) accounting and valuation fees

(d) professional and consulting services fees

(e) general administration expenses

(f) Costs of maintaining internal acquisitions

(g) costs of registration of debt and equity instruments and so on.

These costs are incurred by the company acquiring the business of another business means they are

incurred by the acquirer of the business.

The accounting treatment of these costs is defines under AASB 3, “Business combinations”.

According to AASB 3 these costs should be expensed off in the period in which they are incurred.

Meaning there by these costs should be charged to profit and loss account ("Business Combinations",

2018).

However, there is one exception to above treatment, that is for debt and equity issuance costs.

According to AASB 3, the debt and equity issuance costs should be capitalized in the period in which

they are incurred, since the benefits from these costs are expected to last for more than a year.

(3)

Guarantees $32,000

Accounts payable $32,600

Loans $74,200

Accrued interest on loans $4,300

Liquidation expenses $5,000 $(148,100)

Fair value of net assets acquired - (a) $227,740

Consideration paid in shares (2 shares for every 5 shares held

@ $10 $280,000

Consideration paid in patent $18,000

Goodwill (Consideration paid less fair value) $70,260

PART-B

The today's environment of business comes with lots of changes and challenges. To survive in

today's environment, business needs to encounter certain problems and have to do certain types of

business combinations. These business combinations are in the form of merging with another

company, purchasing the business of other companies, disinvesting, acquiring and so on.

With these business combinations, the acquisition related costs come. These costs are those costs

which are incurred in the business combination and are mandatory to incur. These acquisition costs

include the following type of expenses (Staff, 2018):

(a) advisor’s fees

(b) legal fees

(c) accounting and valuation fees

(d) professional and consulting services fees

(e) general administration expenses

(f) Costs of maintaining internal acquisitions

(g) costs of registration of debt and equity instruments and so on.

These costs are incurred by the company acquiring the business of another business means they are

incurred by the acquirer of the business.

The accounting treatment of these costs is defines under AASB 3, “Business combinations”.

According to AASB 3 these costs should be expensed off in the period in which they are incurred.

Meaning there by these costs should be charged to profit and loss account ("Business Combinations",

2018).

However, there is one exception to above treatment, that is for debt and equity issuance costs.

According to AASB 3, the debt and equity issuance costs should be capitalized in the period in which

they are incurred, since the benefits from these costs are expected to last for more than a year.

(3)

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

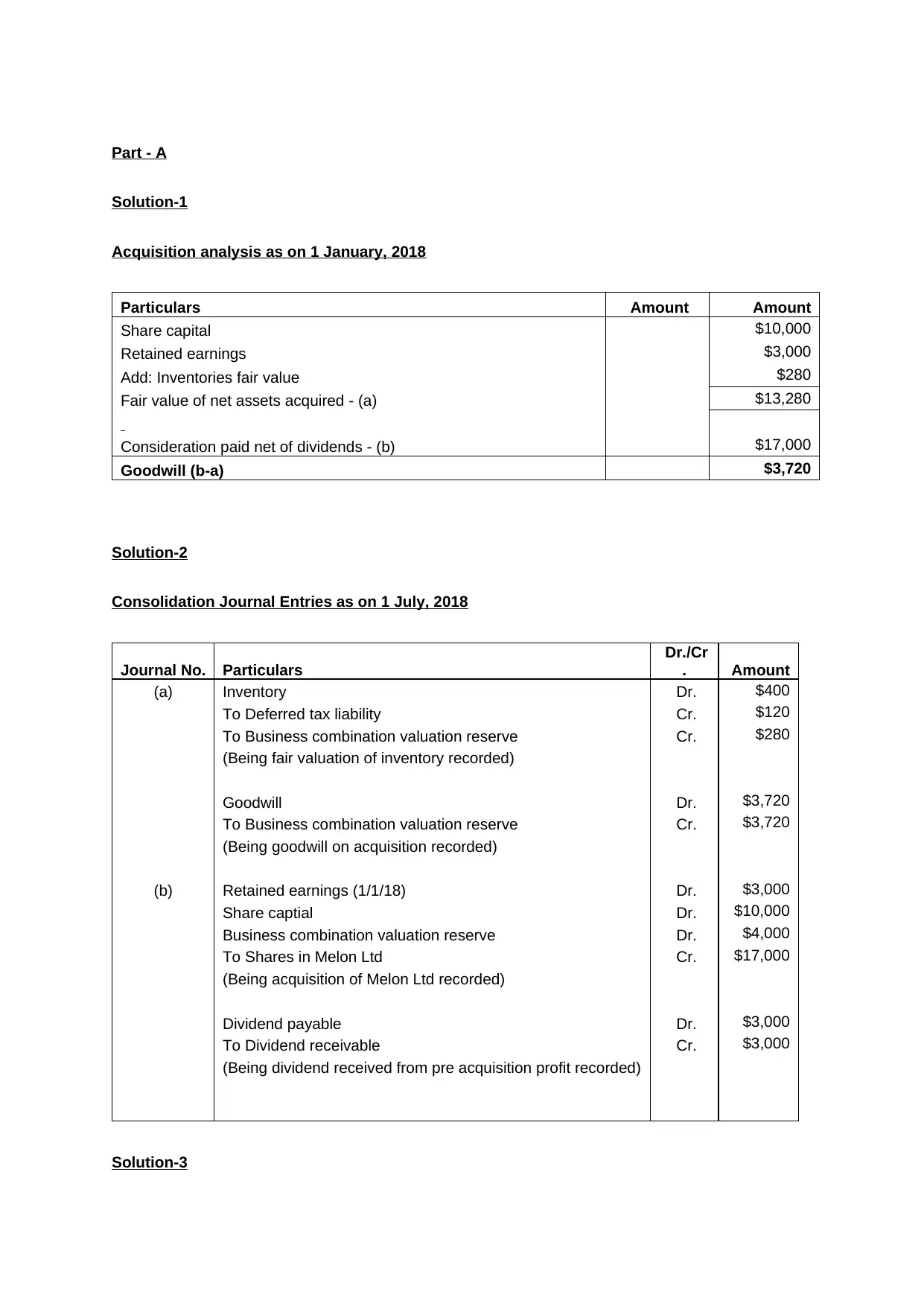

Part - A

Solution-1

Acquisition analysis as on 1 January, 2018

Particulars Amount Amount

Share capital $10,000

Retained earnings $3,000

Add: Inventories fair value $280

Fair value of net assets acquired - (a) $13,280

Consideration paid net of dividends - (b) $17,000

Goodwill (b-a) $3,720

Solution-2

Consolidation Journal Entries as on 1 July, 2018

Journal No. Particulars

Dr./Cr

. Amount

(a) Inventory Dr. $400

To Deferred tax liability Cr. $120

To Business combination valuation reserve Cr. $280

(Being fair valuation of inventory recorded)

Goodwill Dr. $3,720

To Business combination valuation reserve Cr. $3,720

(Being goodwill on acquisition recorded)

(b) Retained earnings (1/1/18) Dr. $3,000

Share captial Dr. $10,000

Business combination valuation reserve Dr. $4,000

To Shares in Melon Ltd Cr. $17,000

(Being acquisition of Melon Ltd recorded)

Dividend payable Dr. $3,000

To Dividend receivable Cr. $3,000

(Being dividend received from pre acquisition profit recorded)

Solution-3

Solution-1

Acquisition analysis as on 1 January, 2018

Particulars Amount Amount

Share capital $10,000

Retained earnings $3,000

Add: Inventories fair value $280

Fair value of net assets acquired - (a) $13,280

Consideration paid net of dividends - (b) $17,000

Goodwill (b-a) $3,720

Solution-2

Consolidation Journal Entries as on 1 July, 2018

Journal No. Particulars

Dr./Cr

. Amount

(a) Inventory Dr. $400

To Deferred tax liability Cr. $120

To Business combination valuation reserve Cr. $280

(Being fair valuation of inventory recorded)

Goodwill Dr. $3,720

To Business combination valuation reserve Cr. $3,720

(Being goodwill on acquisition recorded)

(b) Retained earnings (1/1/18) Dr. $3,000

Share captial Dr. $10,000

Business combination valuation reserve Dr. $4,000

To Shares in Melon Ltd Cr. $17,000

(Being acquisition of Melon Ltd recorded)

Dividend payable Dr. $3,000

To Dividend receivable Cr. $3,000

(Being dividend received from pre acquisition profit recorded)

Solution-3

Consolidation Journal Entries as on 31 December, 2018

Journal No. Particulars Dr./Cr. Amount

(c) Cost of sales Dr. $360

To Income tax expense Cr. $108

To Transfer from business combination valuation reserve Cr. $252

(Being sale of inventory recorded)

Inventories Dr. $40

To Deferred tax liability Cr. $12

To Business combination valuation reserve Cr. $28

(Being fair valuation of closing inventory recorded)

(d) Sales Dr. $5,000

To Cost of sales Cr. $4,000

To Inventory Cr. $1,000

(Being profit eliminated in ending inventory)

(e) Deferred tax asset Dr. $300

To Income tax expense Cr. $300

(Being tax expense recorded on above)

(f) Impairment loss of goodwill Dr. $1,860

To Goodwill Cr. $1,860

(Being goodwill written off)

(g) Other income Dr. $700

To Other expense Cr. $700

(Being elimination of management fee transaction recorded)

(h) Gain on sale of property, plant and equipment Dr. $3,500

To Machinery Cr. $3,500

(Being elimination of profit in sale of machinery recorded)

(i) Deferred tax asset Dr. $1,050

To Income tax expense Cr. $1,050

(Being tax expense on above recorded)

(j) Accumulated Depreciation Dr. $350

To Depreciation expense Cr. $350

(Being reversal of excess depreciation charged recorded)

(k) Income tax expense Dr. $105

To Deferred tax asset Cr. $105

(Being tax expense on above recorded)

(l) Dividend revenue Dr. $1,000

To Interim dividend paid Cr. $1,000

Journal No. Particulars Dr./Cr. Amount

(c) Cost of sales Dr. $360

To Income tax expense Cr. $108

To Transfer from business combination valuation reserve Cr. $252

(Being sale of inventory recorded)

Inventories Dr. $40

To Deferred tax liability Cr. $12

To Business combination valuation reserve Cr. $28

(Being fair valuation of closing inventory recorded)

(d) Sales Dr. $5,000

To Cost of sales Cr. $4,000

To Inventory Cr. $1,000

(Being profit eliminated in ending inventory)

(e) Deferred tax asset Dr. $300

To Income tax expense Cr. $300

(Being tax expense recorded on above)

(f) Impairment loss of goodwill Dr. $1,860

To Goodwill Cr. $1,860

(Being goodwill written off)

(g) Other income Dr. $700

To Other expense Cr. $700

(Being elimination of management fee transaction recorded)

(h) Gain on sale of property, plant and equipment Dr. $3,500

To Machinery Cr. $3,500

(Being elimination of profit in sale of machinery recorded)

(i) Deferred tax asset Dr. $1,050

To Income tax expense Cr. $1,050

(Being tax expense on above recorded)

(j) Accumulated Depreciation Dr. $350

To Depreciation expense Cr. $350

(Being reversal of excess depreciation charged recorded)

(k) Income tax expense Dr. $105

To Deferred tax asset Cr. $105

(Being tax expense on above recorded)

(l) Dividend revenue Dr. $1,000

To Interim dividend paid Cr. $1,000

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

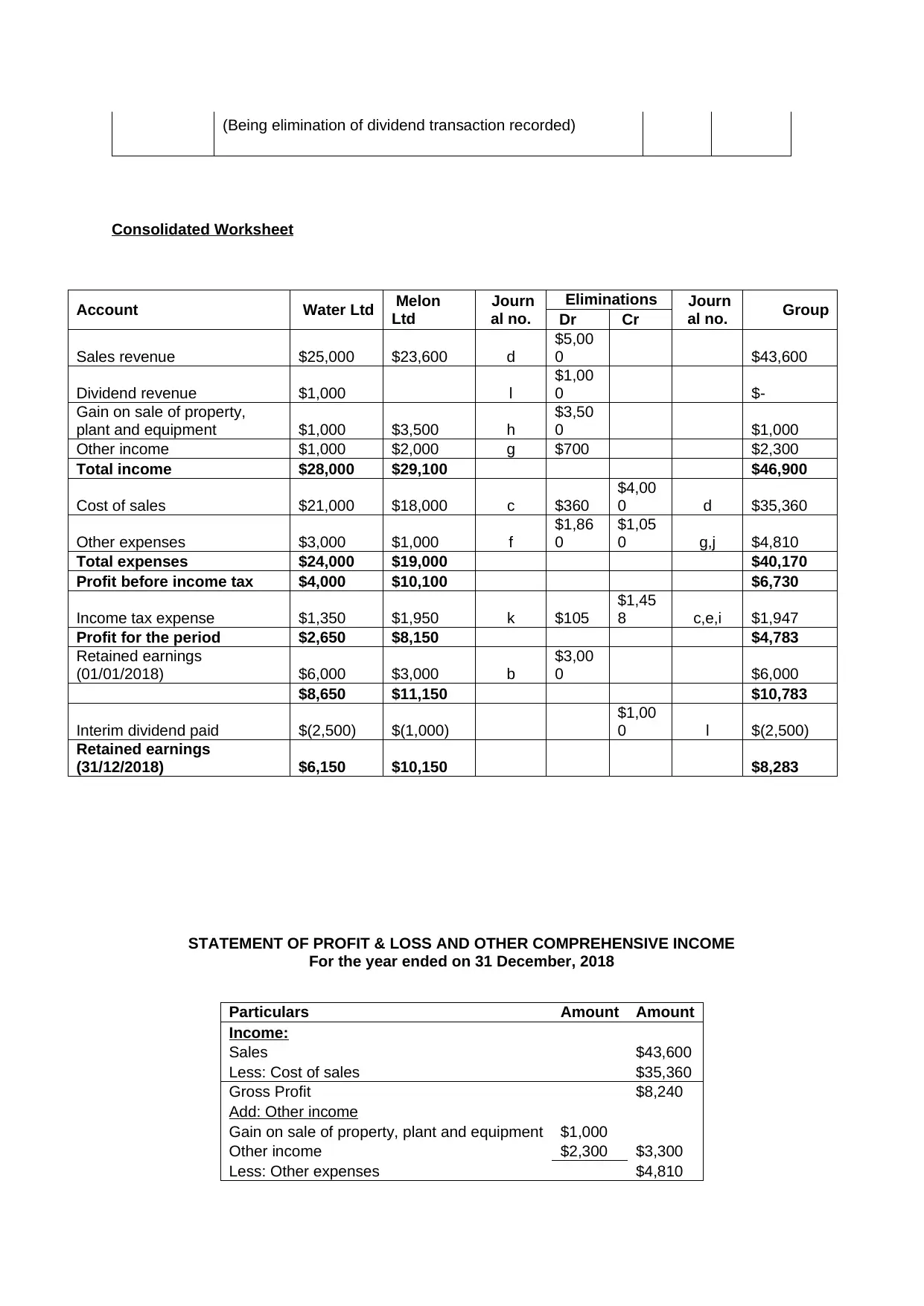

(Being elimination of dividend transaction recorded)

Consolidated Worksheet

Account Water Ltd Melon

Ltd

Journ

al no.

Eliminations Journ

al no. Group

Dr Cr

Sales revenue $25,000 $23,600 d

$5,00

0 $43,600

Dividend revenue $1,000 l

$1,00

0 $-

Gain on sale of property,

plant and equipment $1,000 $3,500 h

$3,50

0 $1,000

Other income $1,000 $2,000 g $700 $2,300

Total income $28,000 $29,100 $46,900

Cost of sales $21,000 $18,000 c $360

$4,00

0 d $35,360

Other expenses $3,000 $1,000 f

$1,86

0

$1,05

0 g,j $4,810

Total expenses $24,000 $19,000 $40,170

Profit before income tax $4,000 $10,100 $6,730

Income tax expense $1,350 $1,950 k $105

$1,45

8 c,e,i $1,947

Profit for the period $2,650 $8,150 $4,783

Retained earnings

(01/01/2018) $6,000 $3,000 b

$3,00

0 $6,000

$8,650 $11,150 $10,783

Interim dividend paid $(2,500) $(1,000)

$1,00

0 l $(2,500)

Retained earnings

(31/12/2018) $6,150 $10,150 $8,283

STATEMENT OF PROFIT & LOSS AND OTHER COMPREHENSIVE INCOME

For the year ended on 31 December, 2018

Particulars Amount Amount

Income:

Sales $43,600

Less: Cost of sales $35,360

Gross Profit $8,240

Add: Other income

Gain on sale of property, plant and equipment $1,000

Other income $2,300 $3,300

Less: Other expenses $4,810

Consolidated Worksheet

Account Water Ltd Melon

Ltd

Journ

al no.

Eliminations Journ

al no. Group

Dr Cr

Sales revenue $25,000 $23,600 d

$5,00

0 $43,600

Dividend revenue $1,000 l

$1,00

0 $-

Gain on sale of property,

plant and equipment $1,000 $3,500 h

$3,50

0 $1,000

Other income $1,000 $2,000 g $700 $2,300

Total income $28,000 $29,100 $46,900

Cost of sales $21,000 $18,000 c $360

$4,00

0 d $35,360

Other expenses $3,000 $1,000 f

$1,86

0

$1,05

0 g,j $4,810

Total expenses $24,000 $19,000 $40,170

Profit before income tax $4,000 $10,100 $6,730

Income tax expense $1,350 $1,950 k $105

$1,45

8 c,e,i $1,947

Profit for the period $2,650 $8,150 $4,783

Retained earnings

(01/01/2018) $6,000 $3,000 b

$3,00

0 $6,000

$8,650 $11,150 $10,783

Interim dividend paid $(2,500) $(1,000)

$1,00

0 l $(2,500)

Retained earnings

(31/12/2018) $6,150 $10,150 $8,283

STATEMENT OF PROFIT & LOSS AND OTHER COMPREHENSIVE INCOME

For the year ended on 31 December, 2018

Particulars Amount Amount

Income:

Sales $43,600

Less: Cost of sales $35,360

Gross Profit $8,240

Add: Other income

Gain on sale of property, plant and equipment $1,000

Other income $2,300 $3,300

Less: Other expenses $4,810

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

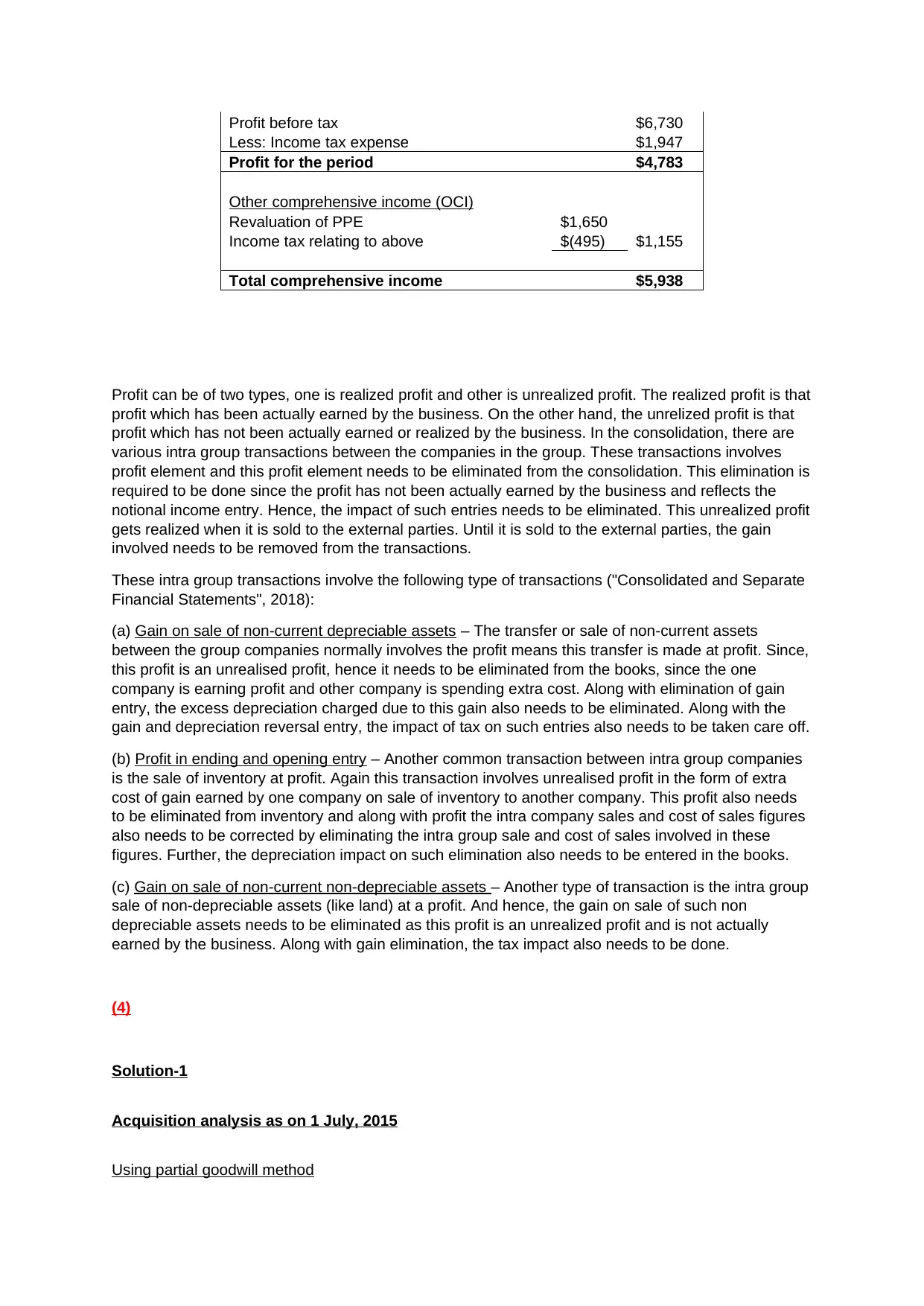

Profit before tax $6,730

Less: Income tax expense $1,947

Profit for the period $4,783

Other comprehensive income (OCI)

Revaluation of PPE $1,650

Income tax relating to above $(495) $1,155

Total comprehensive income $5,938

Profit can be of two types, one is realized profit and other is unrealized profit. The realized profit is that

profit which has been actually earned by the business. On the other hand, the unrelized profit is that

profit which has not been actually earned or realized by the business. In the consolidation, there are

various intra group transactions between the companies in the group. These transactions involves

profit element and this profit element needs to be eliminated from the consolidation. This elimination is

required to be done since the profit has not been actually earned by the business and reflects the

notional income entry. Hence, the impact of such entries needs to be eliminated. This unrealized profit

gets realized when it is sold to the external parties. Until it is sold to the external parties, the gain

involved needs to be removed from the transactions.

These intra group transactions involve the following type of transactions ("Consolidated and Separate

Financial Statements", 2018):

(a) Gain on sale of non-current depreciable assets – The transfer or sale of non-current assets

between the group companies normally involves the profit means this transfer is made at profit. Since,

this profit is an unrealised profit, hence it needs to be eliminated from the books, since the one

company is earning profit and other company is spending extra cost. Along with elimination of gain

entry, the excess depreciation charged due to this gain also needs to be eliminated. Along with the

gain and depreciation reversal entry, the impact of tax on such entries also needs to be taken care off.

(b) Profit in ending and opening entry – Another common transaction between intra group companies

is the sale of inventory at profit. Again this transaction involves unrealised profit in the form of extra

cost of gain earned by one company on sale of inventory to another company. This profit also needs

to be eliminated from inventory and along with profit the intra company sales and cost of sales figures

also needs to be corrected by eliminating the intra group sale and cost of sales involved in these

figures. Further, the depreciation impact on such elimination also needs to be entered in the books.

(c) Gain on sale of non-current non-depreciable assets – Another type of transaction is the intra group

sale of non-depreciable assets (like land) at a profit. And hence, the gain on sale of such non

depreciable assets needs to be eliminated as this profit is an unrealized profit and is not actually

earned by the business. Along with gain elimination, the tax impact also needs to be done.

(4)

Solution-1

Acquisition analysis as on 1 July, 2015

Using partial goodwill method

Less: Income tax expense $1,947

Profit for the period $4,783

Other comprehensive income (OCI)

Revaluation of PPE $1,650

Income tax relating to above $(495) $1,155

Total comprehensive income $5,938

Profit can be of two types, one is realized profit and other is unrealized profit. The realized profit is that

profit which has been actually earned by the business. On the other hand, the unrelized profit is that

profit which has not been actually earned or realized by the business. In the consolidation, there are

various intra group transactions between the companies in the group. These transactions involves

profit element and this profit element needs to be eliminated from the consolidation. This elimination is

required to be done since the profit has not been actually earned by the business and reflects the

notional income entry. Hence, the impact of such entries needs to be eliminated. This unrealized profit

gets realized when it is sold to the external parties. Until it is sold to the external parties, the gain

involved needs to be removed from the transactions.

These intra group transactions involve the following type of transactions ("Consolidated and Separate

Financial Statements", 2018):

(a) Gain on sale of non-current depreciable assets – The transfer or sale of non-current assets

between the group companies normally involves the profit means this transfer is made at profit. Since,

this profit is an unrealised profit, hence it needs to be eliminated from the books, since the one

company is earning profit and other company is spending extra cost. Along with elimination of gain

entry, the excess depreciation charged due to this gain also needs to be eliminated. Along with the

gain and depreciation reversal entry, the impact of tax on such entries also needs to be taken care off.

(b) Profit in ending and opening entry – Another common transaction between intra group companies

is the sale of inventory at profit. Again this transaction involves unrealised profit in the form of extra

cost of gain earned by one company on sale of inventory to another company. This profit also needs

to be eliminated from inventory and along with profit the intra company sales and cost of sales figures

also needs to be corrected by eliminating the intra group sale and cost of sales involved in these

figures. Further, the depreciation impact on such elimination also needs to be entered in the books.

(c) Gain on sale of non-current non-depreciable assets – Another type of transaction is the intra group

sale of non-depreciable assets (like land) at a profit. And hence, the gain on sale of such non

depreciable assets needs to be eliminated as this profit is an unrealized profit and is not actually

earned by the business. Along with gain elimination, the tax impact also needs to be done.

(4)

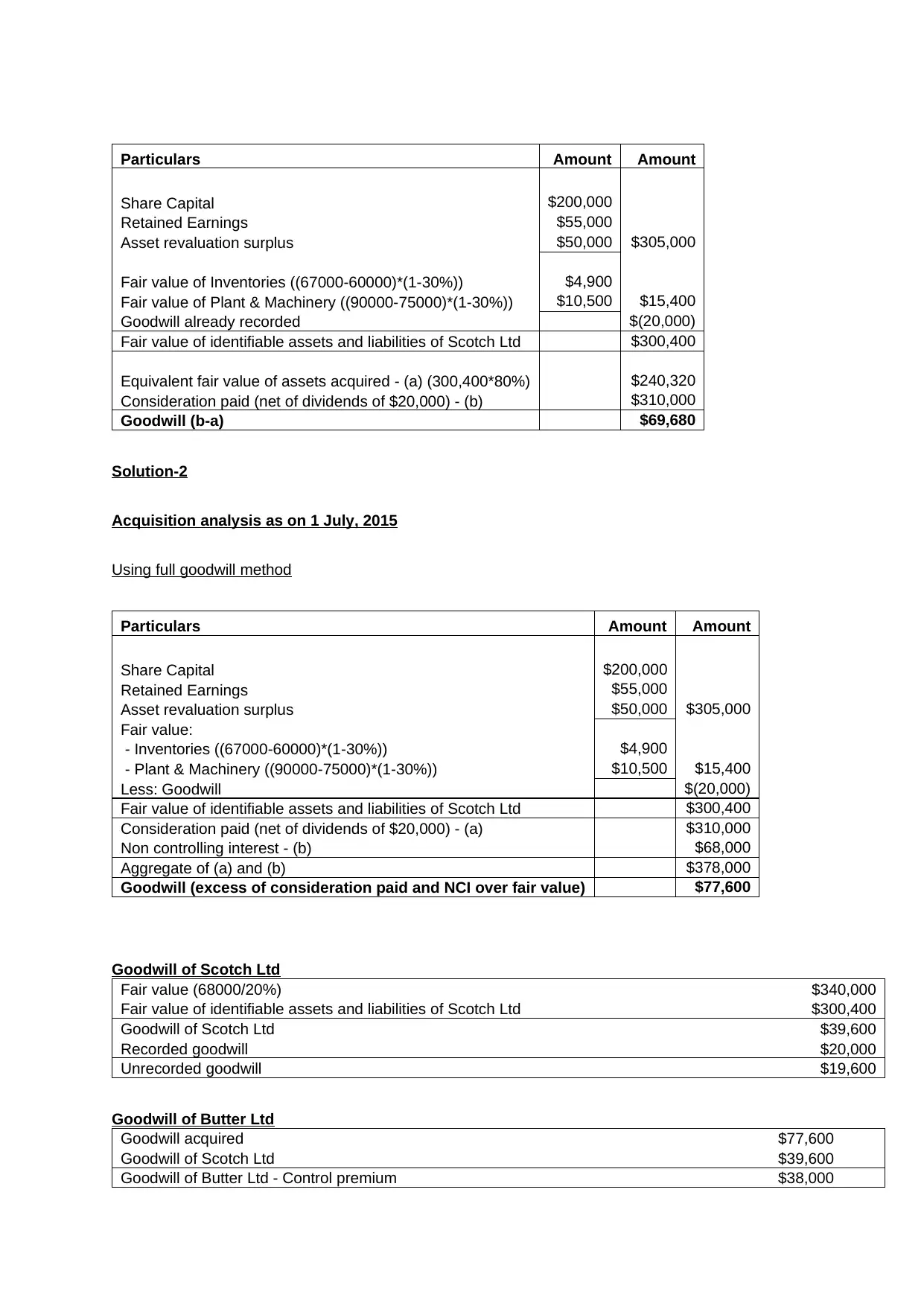

Solution-1

Acquisition analysis as on 1 July, 2015

Using partial goodwill method

Particulars Amount Amount

Share Capital $200,000

Retained Earnings $55,000

Asset revaluation surplus $50,000 $305,000

Fair value of Inventories ((67000-60000)*(1-30%)) $4,900

Fair value of Plant & Machinery ((90000-75000)*(1-30%)) $10,500 $15,400

Goodwill already recorded $(20,000)

Fair value of identifiable assets and liabilities of Scotch Ltd $300,400

Equivalent fair value of assets acquired - (a) (300,400*80%) $240,320

Consideration paid (net of dividends of $20,000) - (b) $310,000

Goodwill (b-a) $69,680

Solution-2

Acquisition analysis as on 1 July, 2015

Using full goodwill method

Particulars Amount Amount

Share Capital $200,000

Retained Earnings $55,000

Asset revaluation surplus $50,000 $305,000

Fair value:

- Inventories ((67000-60000)*(1-30%)) $4,900

- Plant & Machinery ((90000-75000)*(1-30%)) $10,500 $15,400

Less: Goodwill $(20,000)

Fair value of identifiable assets and liabilities of Scotch Ltd $300,400

Consideration paid (net of dividends of $20,000) - (a) $310,000

Non controlling interest - (b) $68,000

Aggregate of (a) and (b) $378,000

Goodwill (excess of consideration paid and NCI over fair value) $77,600

Goodwill of Scotch Ltd

Fair value (68000/20%) $340,000

Fair value of identifiable assets and liabilities of Scotch Ltd $300,400

Goodwill of Scotch Ltd $39,600

Recorded goodwill $20,000

Unrecorded goodwill $19,600

Goodwill of Butter Ltd

Goodwill acquired $77,600

Goodwill of Scotch Ltd $39,600

Goodwill of Butter Ltd - Control premium $38,000

Share Capital $200,000

Retained Earnings $55,000

Asset revaluation surplus $50,000 $305,000

Fair value of Inventories ((67000-60000)*(1-30%)) $4,900

Fair value of Plant & Machinery ((90000-75000)*(1-30%)) $10,500 $15,400

Goodwill already recorded $(20,000)

Fair value of identifiable assets and liabilities of Scotch Ltd $300,400

Equivalent fair value of assets acquired - (a) (300,400*80%) $240,320

Consideration paid (net of dividends of $20,000) - (b) $310,000

Goodwill (b-a) $69,680

Solution-2

Acquisition analysis as on 1 July, 2015

Using full goodwill method

Particulars Amount Amount

Share Capital $200,000

Retained Earnings $55,000

Asset revaluation surplus $50,000 $305,000

Fair value:

- Inventories ((67000-60000)*(1-30%)) $4,900

- Plant & Machinery ((90000-75000)*(1-30%)) $10,500 $15,400

Less: Goodwill $(20,000)

Fair value of identifiable assets and liabilities of Scotch Ltd $300,400

Consideration paid (net of dividends of $20,000) - (a) $310,000

Non controlling interest - (b) $68,000

Aggregate of (a) and (b) $378,000

Goodwill (excess of consideration paid and NCI over fair value) $77,600

Goodwill of Scotch Ltd

Fair value (68000/20%) $340,000

Fair value of identifiable assets and liabilities of Scotch Ltd $300,400

Goodwill of Scotch Ltd $39,600

Recorded goodwill $20,000

Unrecorded goodwill $19,600

Goodwill of Butter Ltd

Goodwill acquired $77,600

Goodwill of Scotch Ltd $39,600

Goodwill of Butter Ltd - Control premium $38,000

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

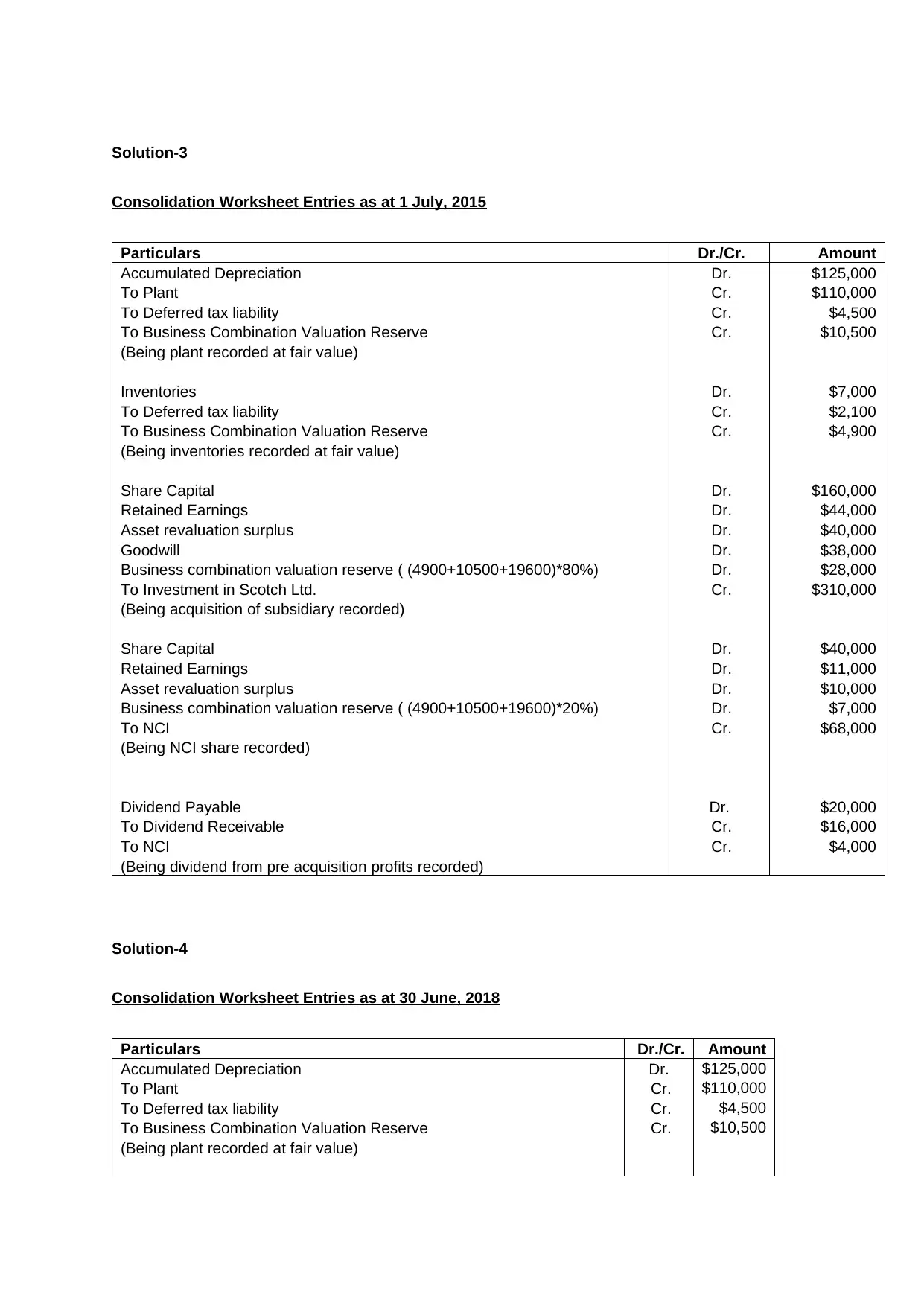

Solution-3

Consolidation Worksheet Entries as at 1 July, 2015

Particulars Dr./Cr. Amount

Accumulated Depreciation Dr. $125,000

To Plant Cr. $110,000

To Deferred tax liability Cr. $4,500

To Business Combination Valuation Reserve Cr. $10,500

(Being plant recorded at fair value)

Inventories Dr. $7,000

To Deferred tax liability Cr. $2,100

To Business Combination Valuation Reserve Cr. $4,900

(Being inventories recorded at fair value)

Share Capital Dr. $160,000

Retained Earnings Dr. $44,000

Asset revaluation surplus Dr. $40,000

Goodwill Dr. $38,000

Business combination valuation reserve ( (4900+10500+19600)*80%) Dr. $28,000

To Investment in Scotch Ltd. Cr. $310,000

(Being acquisition of subsidiary recorded)

Share Capital Dr. $40,000

Retained Earnings Dr. $11,000

Asset revaluation surplus Dr. $10,000

Business combination valuation reserve ( (4900+10500+19600)*20%) Dr. $7,000

To NCI Cr. $68,000

(Being NCI share recorded)

Dividend Payable Dr. $20,000

To Dividend Receivable Cr. $16,000

To NCI Cr. $4,000

(Being dividend from pre acquisition profits recorded)

Solution-4

Consolidation Worksheet Entries as at 30 June, 2018

Particulars Dr./Cr. Amount

Accumulated Depreciation Dr. $125,000

To Plant Cr. $110,000

To Deferred tax liability Cr. $4,500

To Business Combination Valuation Reserve Cr. $10,500

(Being plant recorded at fair value)

Consolidation Worksheet Entries as at 1 July, 2015

Particulars Dr./Cr. Amount

Accumulated Depreciation Dr. $125,000

To Plant Cr. $110,000

To Deferred tax liability Cr. $4,500

To Business Combination Valuation Reserve Cr. $10,500

(Being plant recorded at fair value)

Inventories Dr. $7,000

To Deferred tax liability Cr. $2,100

To Business Combination Valuation Reserve Cr. $4,900

(Being inventories recorded at fair value)

Share Capital Dr. $160,000

Retained Earnings Dr. $44,000

Asset revaluation surplus Dr. $40,000

Goodwill Dr. $38,000

Business combination valuation reserve ( (4900+10500+19600)*80%) Dr. $28,000

To Investment in Scotch Ltd. Cr. $310,000

(Being acquisition of subsidiary recorded)

Share Capital Dr. $40,000

Retained Earnings Dr. $11,000

Asset revaluation surplus Dr. $10,000

Business combination valuation reserve ( (4900+10500+19600)*20%) Dr. $7,000

To NCI Cr. $68,000

(Being NCI share recorded)

Dividend Payable Dr. $20,000

To Dividend Receivable Cr. $16,000

To NCI Cr. $4,000

(Being dividend from pre acquisition profits recorded)

Solution-4

Consolidation Worksheet Entries as at 30 June, 2018

Particulars Dr./Cr. Amount

Accumulated Depreciation Dr. $125,000

To Plant Cr. $110,000

To Deferred tax liability Cr. $4,500

To Business Combination Valuation Reserve Cr. $10,500

(Being plant recorded at fair value)

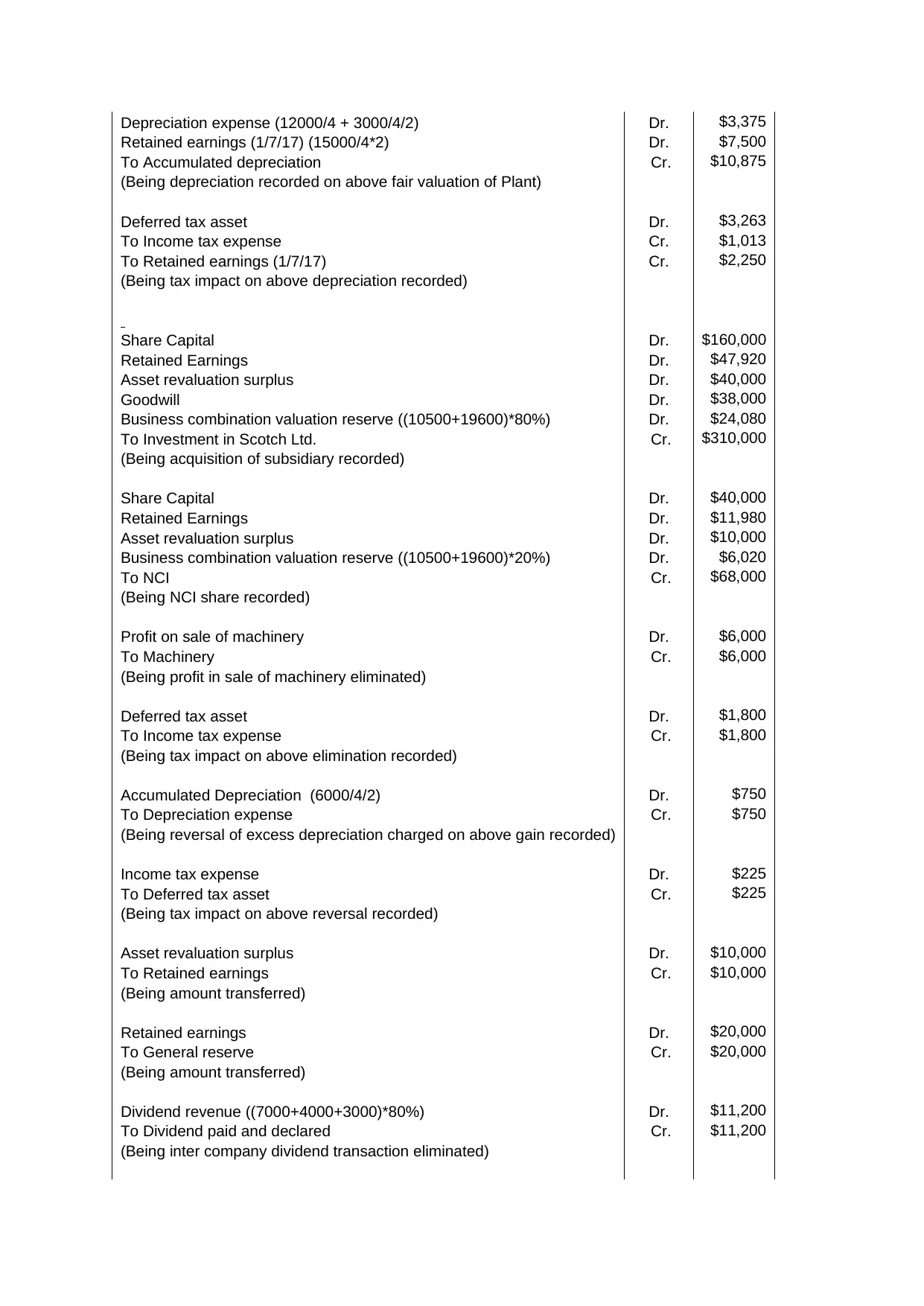

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Depreciation expense (12000/4 + 3000/4/2) Dr. $3,375

Retained earnings (1/7/17) (15000/4*2) Dr. $7,500

To Accumulated depreciation Cr. $10,875

(Being depreciation recorded on above fair valuation of Plant)

Deferred tax asset Dr. $3,263

To Income tax expense Cr. $1,013

To Retained earnings (1/7/17) Cr. $2,250

(Being tax impact on above depreciation recorded)

Share Capital Dr. $160,000

Retained Earnings Dr. $47,920

Asset revaluation surplus Dr. $40,000

Goodwill Dr. $38,000

Business combination valuation reserve ((10500+19600)*80%) Dr. $24,080

To Investment in Scotch Ltd. Cr. $310,000

(Being acquisition of subsidiary recorded)

Share Capital Dr. $40,000

Retained Earnings Dr. $11,980

Asset revaluation surplus Dr. $10,000

Business combination valuation reserve ((10500+19600)*20%) Dr. $6,020

To NCI Cr. $68,000

(Being NCI share recorded)

Profit on sale of machinery Dr. $6,000

To Machinery Cr. $6,000

(Being profit in sale of machinery eliminated)

Deferred tax asset Dr. $1,800

To Income tax expense Cr. $1,800

(Being tax impact on above elimination recorded)

Accumulated Depreciation (6000/4/2) Dr. $750

To Depreciation expense Cr. $750

(Being reversal of excess depreciation charged on above gain recorded)

Income tax expense Dr. $225

To Deferred tax asset Cr. $225

(Being tax impact on above reversal recorded)

Asset revaluation surplus Dr. $10,000

To Retained earnings Cr. $10,000

(Being amount transferred)

Retained earnings Dr. $20,000

To General reserve Cr. $20,000

(Being amount transferred)

Dividend revenue ((7000+4000+3000)*80%) Dr. $11,200

To Dividend paid and declared Cr. $11,200

(Being inter company dividend transaction eliminated)

Retained earnings (1/7/17) (15000/4*2) Dr. $7,500

To Accumulated depreciation Cr. $10,875

(Being depreciation recorded on above fair valuation of Plant)

Deferred tax asset Dr. $3,263

To Income tax expense Cr. $1,013

To Retained earnings (1/7/17) Cr. $2,250

(Being tax impact on above depreciation recorded)

Share Capital Dr. $160,000

Retained Earnings Dr. $47,920

Asset revaluation surplus Dr. $40,000

Goodwill Dr. $38,000

Business combination valuation reserve ((10500+19600)*80%) Dr. $24,080

To Investment in Scotch Ltd. Cr. $310,000

(Being acquisition of subsidiary recorded)

Share Capital Dr. $40,000

Retained Earnings Dr. $11,980

Asset revaluation surplus Dr. $10,000

Business combination valuation reserve ((10500+19600)*20%) Dr. $6,020

To NCI Cr. $68,000

(Being NCI share recorded)

Profit on sale of machinery Dr. $6,000

To Machinery Cr. $6,000

(Being profit in sale of machinery eliminated)

Deferred tax asset Dr. $1,800

To Income tax expense Cr. $1,800

(Being tax impact on above elimination recorded)

Accumulated Depreciation (6000/4/2) Dr. $750

To Depreciation expense Cr. $750

(Being reversal of excess depreciation charged on above gain recorded)

Income tax expense Dr. $225

To Deferred tax asset Cr. $225

(Being tax impact on above reversal recorded)

Asset revaluation surplus Dr. $10,000

To Retained earnings Cr. $10,000

(Being amount transferred)

Retained earnings Dr. $20,000

To General reserve Cr. $20,000

(Being amount transferred)

Dividend revenue ((7000+4000+3000)*80%) Dr. $11,200

To Dividend paid and declared Cr. $11,200

(Being inter company dividend transaction eliminated)

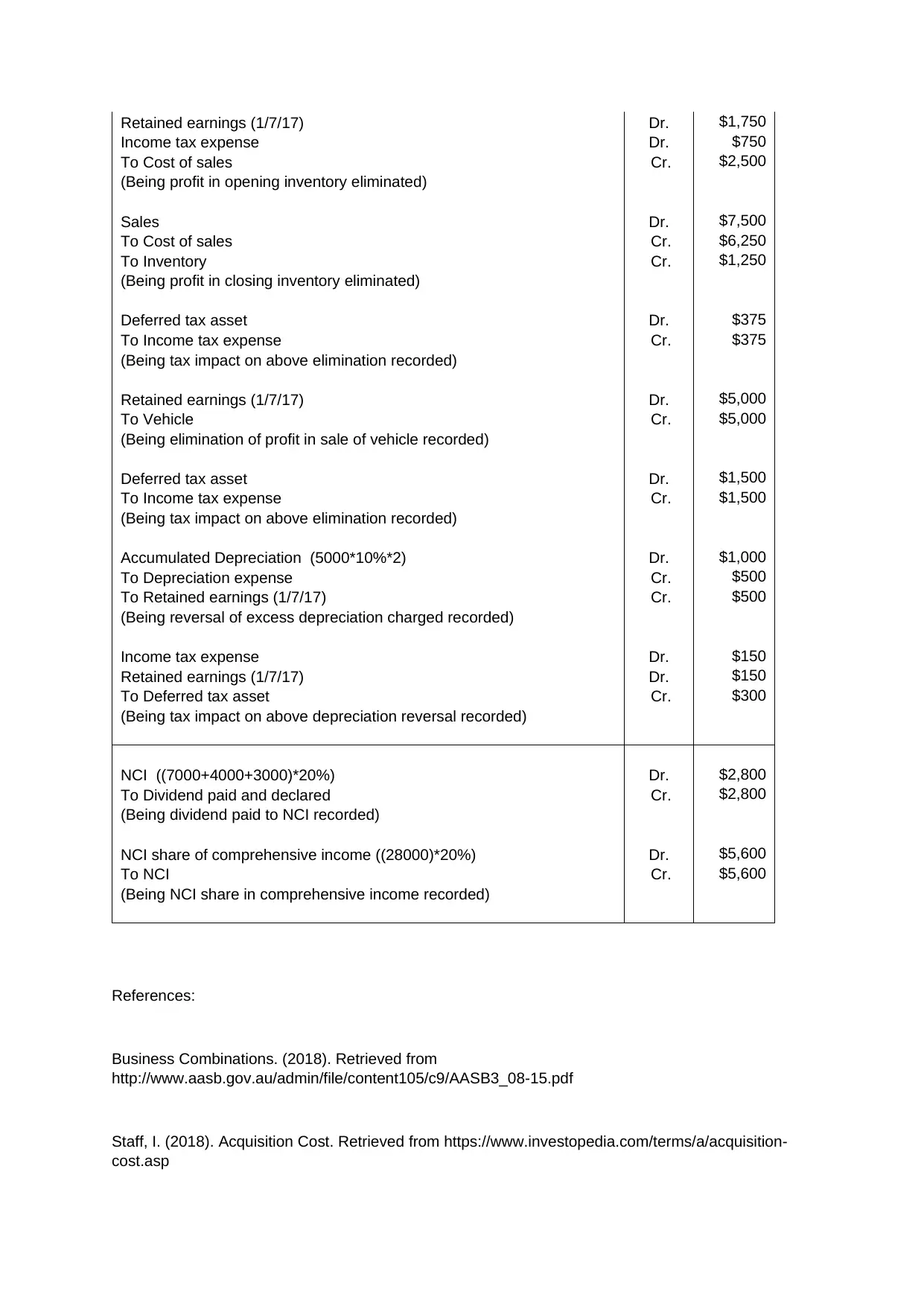

Retained earnings (1/7/17) Dr. $1,750

Income tax expense Dr. $750

To Cost of sales Cr. $2,500

(Being profit in opening inventory eliminated)

Sales Dr. $7,500

To Cost of sales Cr. $6,250

To Inventory Cr. $1,250

(Being profit in closing inventory eliminated)

Deferred tax asset Dr. $375

To Income tax expense Cr. $375

(Being tax impact on above elimination recorded)

Retained earnings (1/7/17) Dr. $5,000

To Vehicle Cr. $5,000

(Being elimination of profit in sale of vehicle recorded)

Deferred tax asset Dr. $1,500

To Income tax expense Cr. $1,500

(Being tax impact on above elimination recorded)

Accumulated Depreciation (5000*10%*2) Dr. $1,000

To Depreciation expense Cr. $500

To Retained earnings (1/7/17) Cr. $500

(Being reversal of excess depreciation charged recorded)

Income tax expense Dr. $150

Retained earnings (1/7/17) Dr. $150

To Deferred tax asset Cr. $300

(Being tax impact on above depreciation reversal recorded)

NCI ((7000+4000+3000)*20%) Dr. $2,800

To Dividend paid and declared Cr. $2,800

(Being dividend paid to NCI recorded)

NCI share of comprehensive income ((28000)*20%) Dr. $5,600

To NCI Cr. $5,600

(Being NCI share in comprehensive income recorded)

References:

Business Combinations. (2018). Retrieved from

http://www.aasb.gov.au/admin/file/content105/c9/AASB3_08-15.pdf

Staff, I. (2018). Acquisition Cost. Retrieved from https://www.investopedia.com/terms/a/acquisition-

cost.asp

Income tax expense Dr. $750

To Cost of sales Cr. $2,500

(Being profit in opening inventory eliminated)

Sales Dr. $7,500

To Cost of sales Cr. $6,250

To Inventory Cr. $1,250

(Being profit in closing inventory eliminated)

Deferred tax asset Dr. $375

To Income tax expense Cr. $375

(Being tax impact on above elimination recorded)

Retained earnings (1/7/17) Dr. $5,000

To Vehicle Cr. $5,000

(Being elimination of profit in sale of vehicle recorded)

Deferred tax asset Dr. $1,500

To Income tax expense Cr. $1,500

(Being tax impact on above elimination recorded)

Accumulated Depreciation (5000*10%*2) Dr. $1,000

To Depreciation expense Cr. $500

To Retained earnings (1/7/17) Cr. $500

(Being reversal of excess depreciation charged recorded)

Income tax expense Dr. $150

Retained earnings (1/7/17) Dr. $150

To Deferred tax asset Cr. $300

(Being tax impact on above depreciation reversal recorded)

NCI ((7000+4000+3000)*20%) Dr. $2,800

To Dividend paid and declared Cr. $2,800

(Being dividend paid to NCI recorded)

NCI share of comprehensive income ((28000)*20%) Dr. $5,600

To NCI Cr. $5,600

(Being NCI share in comprehensive income recorded)

References:

Business Combinations. (2018). Retrieved from

http://www.aasb.gov.au/admin/file/content105/c9/AASB3_08-15.pdf

Staff, I. (2018). Acquisition Cost. Retrieved from https://www.investopedia.com/terms/a/acquisition-

cost.asp

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 13

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2025 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.