Corporate Accounting: Equity, Cash Flow Statements and Comparative Analysis

VerifiedAdded on 2023/06/05

|25

|4769

|87

AI Summary

This document provides an analysis of equity, cash flow statements and comparative analysis of Vodafone PLC and SingTel Optus. It includes a detailed description of the components of owners’ equity and changes to these components over the years, comparative analysis of debt and equity position of two companies, and a comparative analysis of three broad categories of cash flows.

Contribute Materials

Your contribution can guide someone’s learning journey. Share your

documents today.

Running head: CORPORATE ACCOUNTING

Corporate Accounting

Name of the Student:

Name of the University:

Authors Note:

Corporate Accounting

Name of the Student:

Name of the University:

Authors Note:

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

1

CORPORATE ACCOUNTING

Executive summary:

There are five elements that consist of financial statements of an entity, these are; assets,

liabilities, revenue, expenditures and equity. It is important to have specific knowledge about

each of these elements to correctly prepare and present different statements in order to prepare

and present a complete set of financial statements for an entity operating in Australia. A

complete set of financial statements for an entity conducting business operations must have an

income statement, a statement of financial position, a statement to show the changes in equity

from previous year, a statement to record cash flows under three broad categories and notes to

accounts. Throughout this document an in-depth analysis of different items that are reported

under owner’s equity, in cash flow statements, in other comprehensive income statement and in

income statement of an entity shall be carried out for the benefit of the readers.

CORPORATE ACCOUNTING

Executive summary:

There are five elements that consist of financial statements of an entity, these are; assets,

liabilities, revenue, expenditures and equity. It is important to have specific knowledge about

each of these elements to correctly prepare and present different statements in order to prepare

and present a complete set of financial statements for an entity operating in Australia. A

complete set of financial statements for an entity conducting business operations must have an

income statement, a statement of financial position, a statement to show the changes in equity

from previous year, a statement to record cash flows under three broad categories and notes to

accounts. Throughout this document an in-depth analysis of different items that are reported

under owner’s equity, in cash flow statements, in other comprehensive income statement and in

income statement of an entity shall be carried out for the benefit of the readers.

2

CORPORATE ACCOUNTING

Contents

Executive summary:........................................................................................................................1

Introduction:....................................................................................................................................3

Equity:..............................................................................................................................................3

Cash flow statements:......................................................................................................................8

Other Comprehensive income statement:......................................................................................12

Accounting for corporate income tax:...........................................................................................14

Conclusion:....................................................................................................................................20

References:....................................................................................................................................21

CORPORATE ACCOUNTING

Contents

Executive summary:........................................................................................................................1

Introduction:....................................................................................................................................3

Equity:..............................................................................................................................................3

Cash flow statements:......................................................................................................................8

Other Comprehensive income statement:......................................................................................12

Accounting for corporate income tax:...........................................................................................14

Conclusion:....................................................................................................................................20

References:....................................................................................................................................21

3

CORPORATE ACCOUNTING

Introduction:

Vodafone PLC and SingTel Optus are the two companies to be used to complete the exercise in

this document. A brief description about the two companies and their operations would provide

the point of references to the users of this document to understand the various elements discussed

here.

Vodafone PLC operates in Australia with the corporate identity of Vodafone Australia. The

company is worldwide telecom giant with its operations spreading to different countries in all

across the globe. Originated in United Kingdom, Vodafone PLC is now one of the largest

telecommunication companies in the world.

SingTel Optus, a telecommunication company in the country, is also one of the largest

telecommunication companies the country. Along with the market leader in the country, i.e.

Telstra Corporation, SingTel has been quite successful in capturing significant amount of market

share in the domestic market.

Equity:

(i) Components of owners’ equity and changes to these components over the years:

Called up share capital: Vodafone PLC has issued shares in the capital market to raise funds for

running business operations. The face value of shares issued and called up is represented in the

called up share capital account (Burks, 2015).

Share capital: It is the amount of face value of shares received by the company from the

shareholders. Amount of face value received by issuing ordinary shares in the market is

accumulated in share capital account.

CORPORATE ACCOUNTING

Introduction:

Vodafone PLC and SingTel Optus are the two companies to be used to complete the exercise in

this document. A brief description about the two companies and their operations would provide

the point of references to the users of this document to understand the various elements discussed

here.

Vodafone PLC operates in Australia with the corporate identity of Vodafone Australia. The

company is worldwide telecom giant with its operations spreading to different countries in all

across the globe. Originated in United Kingdom, Vodafone PLC is now one of the largest

telecommunication companies in the world.

SingTel Optus, a telecommunication company in the country, is also one of the largest

telecommunication companies the country. Along with the market leader in the country, i.e.

Telstra Corporation, SingTel has been quite successful in capturing significant amount of market

share in the domestic market.

Equity:

(i) Components of owners’ equity and changes to these components over the years:

Called up share capital: Vodafone PLC has issued shares in the capital market to raise funds for

running business operations. The face value of shares issued and called up is represented in the

called up share capital account (Burks, 2015).

Share capital: It is the amount of face value of shares received by the company from the

shareholders. Amount of face value received by issuing ordinary shares in the market is

accumulated in share capital account.

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

4

CORPORATE ACCOUNTING

Additional paid up share capital: Vodafone PLC has issued share over the face value and the

amount received in excess of the face value form issue shares has been accumulated in the

additional paid up share capital account.

Treasury shares: The amount of stock that an entity has brought back from the capital market is

accumulated in treasury shares. Vodafone PLC has balance in treasury shares (Floyd, 2016).

Reserves: SingTel Optus has accumulated balance in reserves. This is the accumulated amount

set aside from profit and loss account of the company to meet specific future obligations.

Accumulated losses: The amount of loss accumulated from the business activities of Vodafone

over the years is stated under accumulated losses in the Balance sheet of the company (Chen,

2015).

Accumulated other comprehensive income: Vodafone PLC has showed accumulated income

from other comprehensive income. This is the amount of income in other comprehensive income

statement.

Other reserves: SingTel has reported other reserves under owners’ equity in the Balance Sheet. It

is the free reserves that has been accumulated from balance of profit and loss account after

making all provisions and declaration of dividend (Heidari and Felden, 2015).

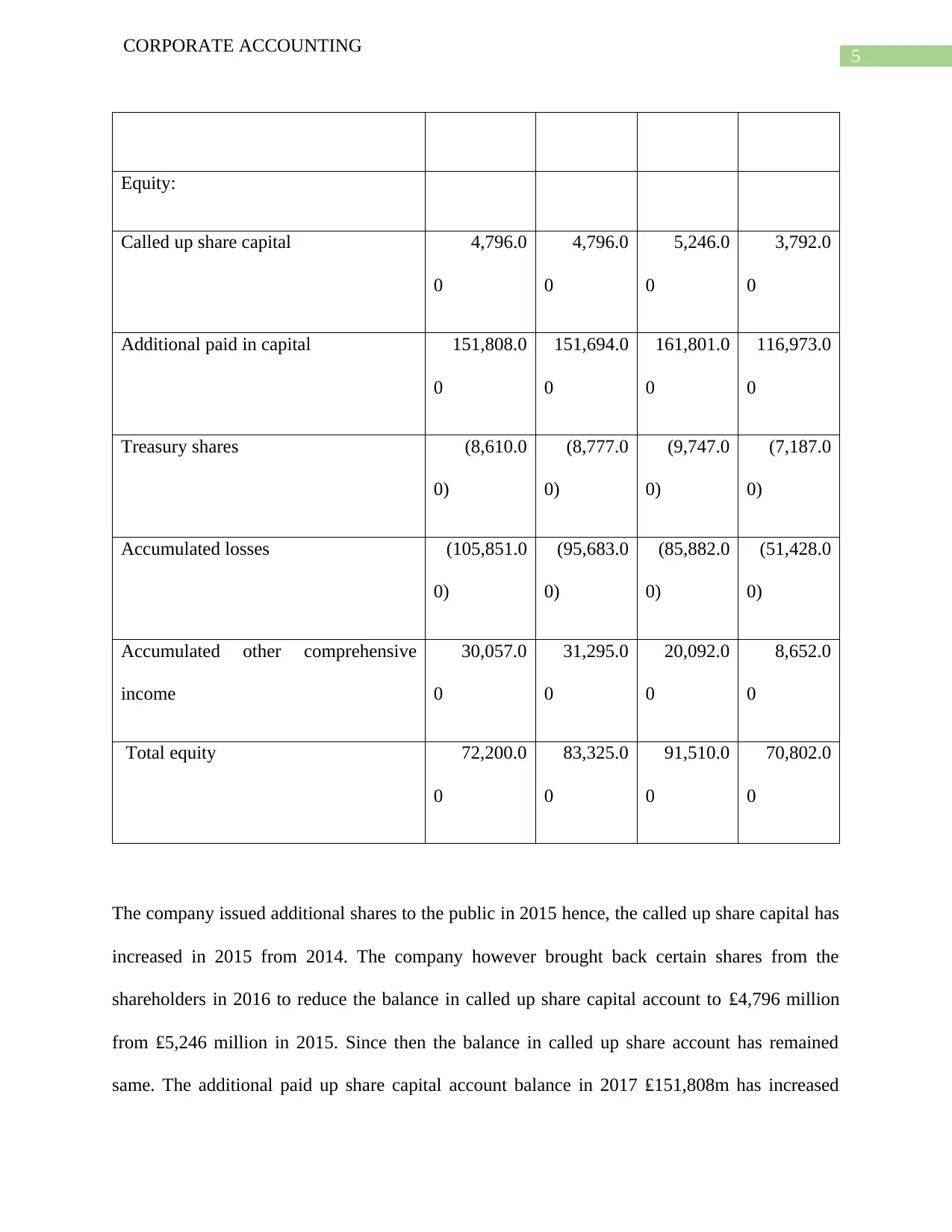

Changes in the items of equity of Vodafone PLC can be seen in the following table:

Vodafone

Amount in ₤' Million

Year 2017 2016 2015 2014

CORPORATE ACCOUNTING

Additional paid up share capital: Vodafone PLC has issued share over the face value and the

amount received in excess of the face value form issue shares has been accumulated in the

additional paid up share capital account.

Treasury shares: The amount of stock that an entity has brought back from the capital market is

accumulated in treasury shares. Vodafone PLC has balance in treasury shares (Floyd, 2016).

Reserves: SingTel Optus has accumulated balance in reserves. This is the accumulated amount

set aside from profit and loss account of the company to meet specific future obligations.

Accumulated losses: The amount of loss accumulated from the business activities of Vodafone

over the years is stated under accumulated losses in the Balance sheet of the company (Chen,

2015).

Accumulated other comprehensive income: Vodafone PLC has showed accumulated income

from other comprehensive income. This is the amount of income in other comprehensive income

statement.

Other reserves: SingTel has reported other reserves under owners’ equity in the Balance Sheet. It

is the free reserves that has been accumulated from balance of profit and loss account after

making all provisions and declaration of dividend (Heidari and Felden, 2015).

Changes in the items of equity of Vodafone PLC can be seen in the following table:

Vodafone

Amount in ₤' Million

Year 2017 2016 2015 2014

5

CORPORATE ACCOUNTING

Equity:

Called up share capital 4,796.0

0

4,796.0

0

5,246.0

0

3,792.0

0

Additional paid in capital 151,808.0

0

151,694.0

0

161,801.0

0

116,973.0

0

Treasury shares (8,610.0

0)

(8,777.0

0)

(9,747.0

0)

(7,187.0

0)

Accumulated losses (105,851.0

0)

(95,683.0

0)

(85,882.0

0)

(51,428.0

0)

Accumulated other comprehensive

income

30,057.0

0

31,295.0

0

20,092.0

0

8,652.0

0

Total equity 72,200.0

0

83,325.0

0

91,510.0

0

70,802.0

0

The company issued additional shares to the public in 2015 hence, the called up share capital has

increased in 2015 from 2014. The company however brought back certain shares from the

shareholders in 2016 to reduce the balance in called up share capital account to ₤4,796 million

from ₤5,246 million in 2015. Since then the balance in called up share account has remained

same. The additional paid up share capital account balance in 2017 ₤151,808m has increased

CORPORATE ACCOUNTING

Equity:

Called up share capital 4,796.0

0

4,796.0

0

5,246.0

0

3,792.0

0

Additional paid in capital 151,808.0

0

151,694.0

0

161,801.0

0

116,973.0

0

Treasury shares (8,610.0

0)

(8,777.0

0)

(9,747.0

0)

(7,187.0

0)

Accumulated losses (105,851.0

0)

(95,683.0

0)

(85,882.0

0)

(51,428.0

0)

Accumulated other comprehensive

income

30,057.0

0

31,295.0

0

20,092.0

0

8,652.0

0

Total equity 72,200.0

0

83,325.0

0

91,510.0

0

70,802.0

0

The company issued additional shares to the public in 2015 hence, the called up share capital has

increased in 2015 from 2014. The company however brought back certain shares from the

shareholders in 2016 to reduce the balance in called up share capital account to ₤4,796 million

from ₤5,246 million in 2015. Since then the balance in called up share account has remained

same. The additional paid up share capital account balance in 2017 ₤151,808m has increased

6

CORPORATE ACCOUNTING

from ₤151,694m of 2016 due to adjustment made to the account (Chen, Miao and Shevlin,

2015).

The balance in treasury stock has reduced to ₤8,610m in 2017 from ₤8,777m in 2016.

Accumulated losses of ₤105,851m of 2017 has increased after every year. This is because the

company has incurred losses from business operations. In 2014 the accumulated losses were only

₤51,428m.

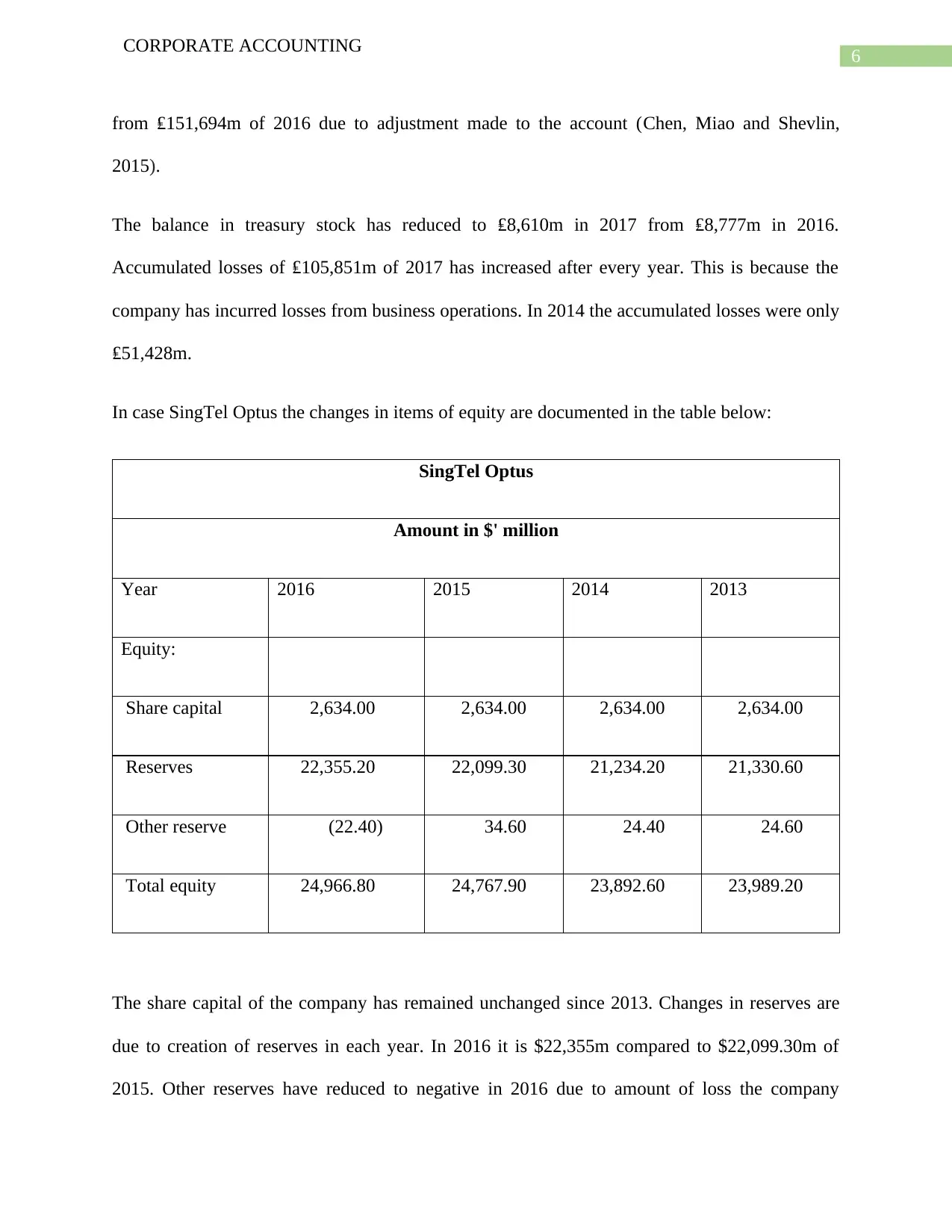

In case SingTel Optus the changes in items of equity are documented in the table below:

SingTel Optus

Amount in $' million

Year 2016 2015 2014 2013

Equity:

Share capital 2,634.00 2,634.00 2,634.00 2,634.00

Reserves 22,355.20 22,099.30 21,234.20 21,330.60

Other reserve (22.40) 34.60 24.40 24.60

Total equity 24,966.80 24,767.90 23,892.60 23,989.20

The share capital of the company has remained unchanged since 2013. Changes in reserves are

due to creation of reserves in each year. In 2016 it is $22,355m compared to $22,099.30m of

2015. Other reserves have reduced to negative in 2016 due to amount of loss the company

CORPORATE ACCOUNTING

from ₤151,694m of 2016 due to adjustment made to the account (Chen, Miao and Shevlin,

2015).

The balance in treasury stock has reduced to ₤8,610m in 2017 from ₤8,777m in 2016.

Accumulated losses of ₤105,851m of 2017 has increased after every year. This is because the

company has incurred losses from business operations. In 2014 the accumulated losses were only

₤51,428m.

In case SingTel Optus the changes in items of equity are documented in the table below:

SingTel Optus

Amount in $' million

Year 2016 2015 2014 2013

Equity:

Share capital 2,634.00 2,634.00 2,634.00 2,634.00

Reserves 22,355.20 22,099.30 21,234.20 21,330.60

Other reserve (22.40) 34.60 24.40 24.60

Total equity 24,966.80 24,767.90 23,892.60 23,989.20

The share capital of the company has remained unchanged since 2013. Changes in reserves are

due to creation of reserves in each year. In 2016 it is $22,355m compared to $22,099.30m of

2015. Other reserves have reduced to negative in 2016 due to amount of loss the company

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

7

CORPORATE ACCOUNTING

incurred I its business operations in 2016 and the same was transferred to the reserves resulted in

negative other reserves balance (Graham et. al. 2017).

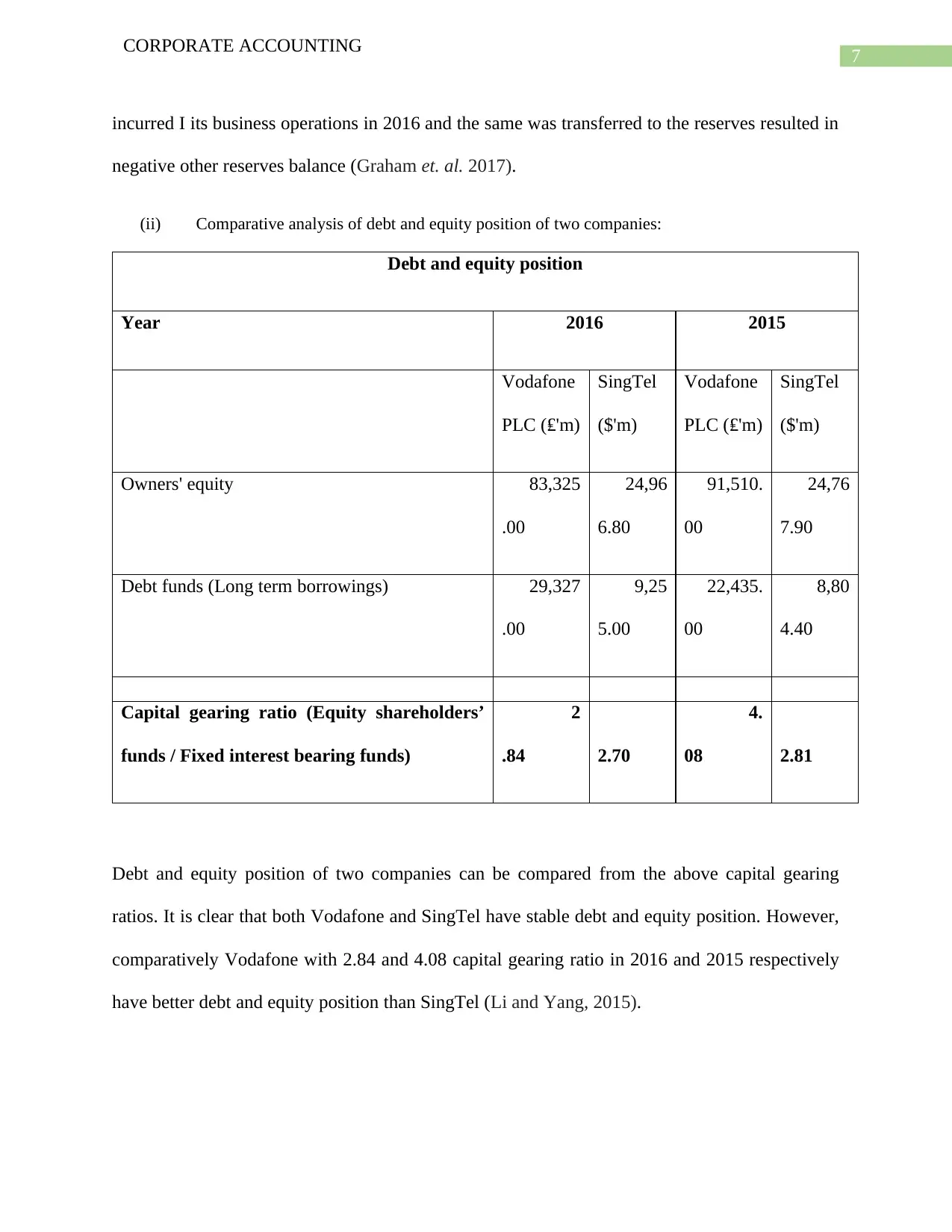

(ii) Comparative analysis of debt and equity position of two companies:

Debt and equity position

Year 2016 2015

Vodafone

PLC (₤'m)

SingTel

($'m)

Vodafone

PLC (₤'m)

SingTel

($'m)

Owners' equity 83,325

.00

24,96

6.80

91,510.

00

24,76

7.90

Debt funds (Long term borrowings) 29,327

.00

9,25

5.00

22,435.

00

8,80

4.40

Capital gearing ratio (Equity shareholders’

funds / Fixed interest bearing funds)

2

.84 2.70

4.

08 2.81

Debt and equity position of two companies can be compared from the above capital gearing

ratios. It is clear that both Vodafone and SingTel have stable debt and equity position. However,

comparatively Vodafone with 2.84 and 4.08 capital gearing ratio in 2016 and 2015 respectively

have better debt and equity position than SingTel (Li and Yang, 2015).

CORPORATE ACCOUNTING

incurred I its business operations in 2016 and the same was transferred to the reserves resulted in

negative other reserves balance (Graham et. al. 2017).

(ii) Comparative analysis of debt and equity position of two companies:

Debt and equity position

Year 2016 2015

Vodafone

PLC (₤'m)

SingTel

($'m)

Vodafone

PLC (₤'m)

SingTel

($'m)

Owners' equity 83,325

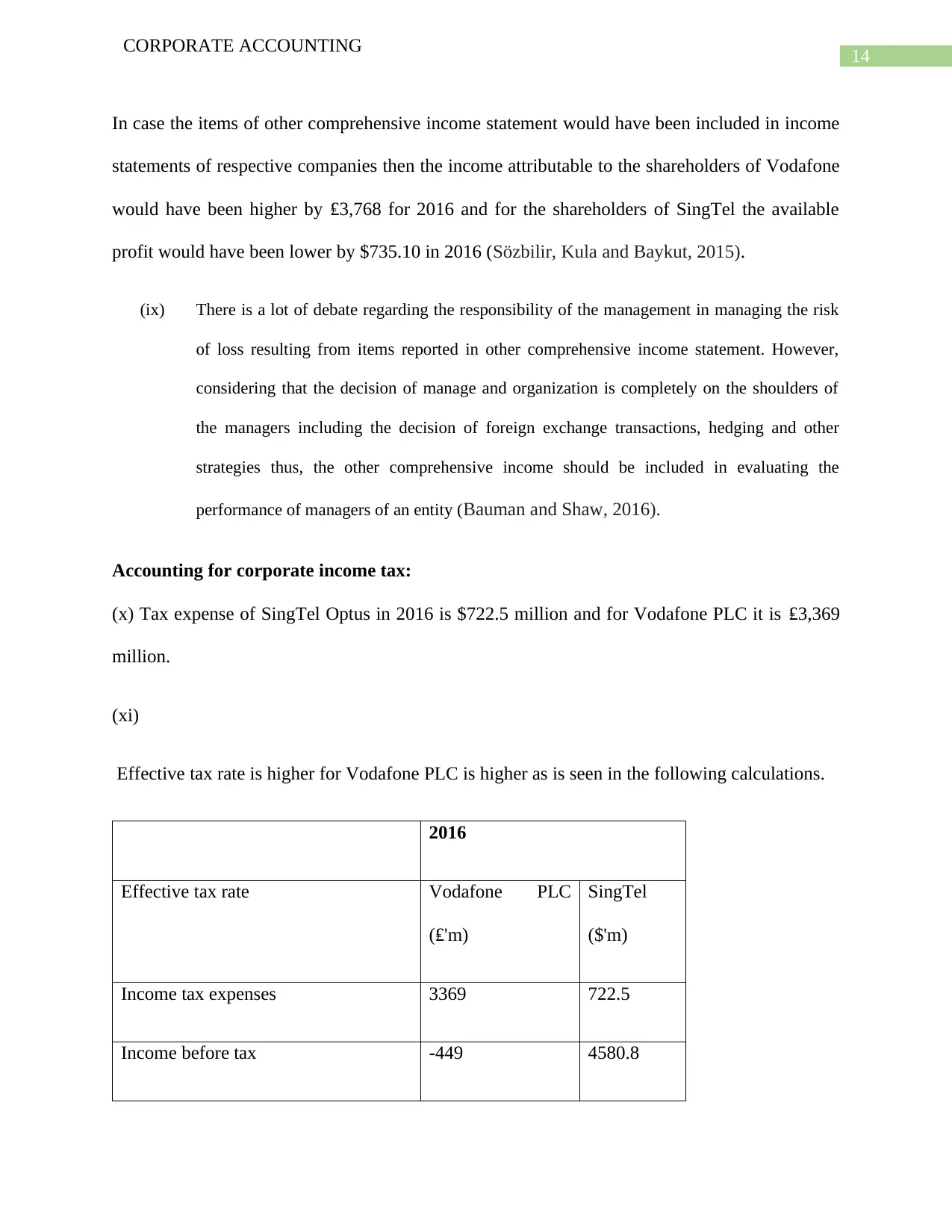

.00

24,96

6.80

91,510.

00

24,76

7.90

Debt funds (Long term borrowings) 29,327

.00

9,25

5.00

22,435.

00

8,80

4.40

Capital gearing ratio (Equity shareholders’

funds / Fixed interest bearing funds)

2

.84 2.70

4.

08 2.81

Debt and equity position of two companies can be compared from the above capital gearing

ratios. It is clear that both Vodafone and SingTel have stable debt and equity position. However,

comparatively Vodafone with 2.84 and 4.08 capital gearing ratio in 2016 and 2015 respectively

have better debt and equity position than SingTel (Li and Yang, 2015).

8

CORPORATE ACCOUNTING

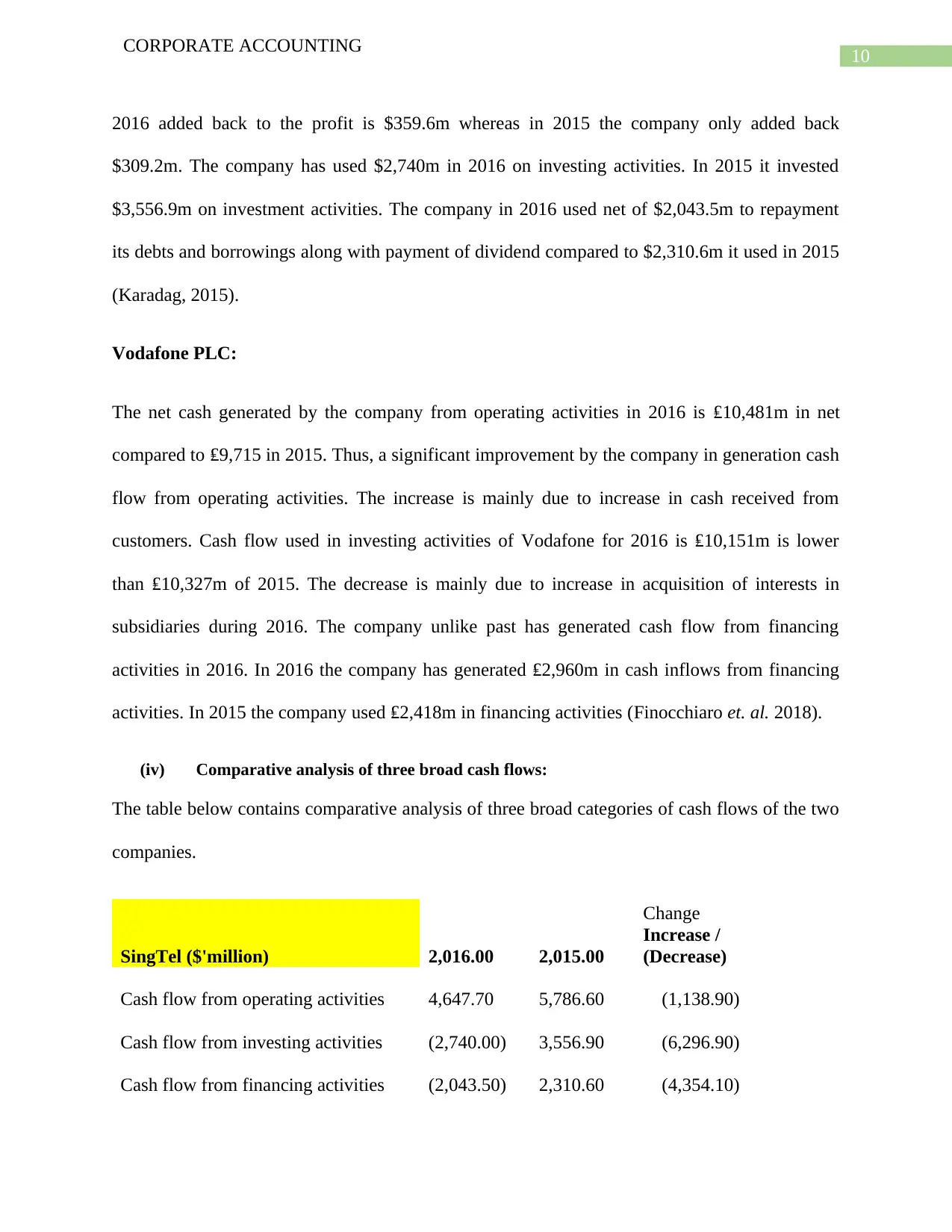

Cash flow statements:

(iii) Both companies have reported cash flows under three broad categories these are cash flow

from operating activities, investing actives and financing activities. Before getting into

changes in these items let’s have a brief understanding of different items reported under three

broad categories of both the companies (Leuz and Wysocki, 2016).

Operating activities: Both Vodafone and SingTel have reported cash received from

customers and cash paid to suppliers and employees. Cash received from customers are the

revenue received from providing telecommunication services to the customers. Payment of

cash to suppliers is the amount paid to suppliers for using the services and operating platform

of suppliers. Payment to employees is the amount paid as salaries and wages to employees

and workers for their services. Without the services of the employees it would not have been

possible to provide services to the customers (Christensen et. al. 2015)). SingTel unlike

Vodafone has used indirect method to present its cash flow from operating activities thus, the

following items have been reported under the cash flow from operating activities of the

company:

Profit before tax: It is the amount of profit earned from business before tax.

Adjustments for depreciation and amortization: Since the depreciation and amortization costs are

not cash expenses hence, these are added back to the profit before tax of the company (Cuccia,

2018).

Adjustment for share of results in associates and joint ventures: The deduction for share of

results in joint ventures and associates is because such profit or loss is generally not received in

cash.

CORPORATE ACCOUNTING

Cash flow statements:

(iii) Both companies have reported cash flows under three broad categories these are cash flow

from operating activities, investing actives and financing activities. Before getting into

changes in these items let’s have a brief understanding of different items reported under three

broad categories of both the companies (Leuz and Wysocki, 2016).

Operating activities: Both Vodafone and SingTel have reported cash received from

customers and cash paid to suppliers and employees. Cash received from customers are the

revenue received from providing telecommunication services to the customers. Payment of

cash to suppliers is the amount paid to suppliers for using the services and operating platform

of suppliers. Payment to employees is the amount paid as salaries and wages to employees

and workers for their services. Without the services of the employees it would not have been

possible to provide services to the customers (Christensen et. al. 2015)). SingTel unlike

Vodafone has used indirect method to present its cash flow from operating activities thus, the

following items have been reported under the cash flow from operating activities of the

company:

Profit before tax: It is the amount of profit earned from business before tax.

Adjustments for depreciation and amortization: Since the depreciation and amortization costs are

not cash expenses hence, these are added back to the profit before tax of the company (Cuccia,

2018).

Adjustment for share of results in associates and joint ventures: The deduction for share of

results in joint ventures and associates is because such profit or loss is generally not received in

cash.

9

CORPORATE ACCOUNTING

Exceptional items of non-cash: Non-cash exceptional items have to be added and deducted as the

case may be depending on whether the item is revenue or expenditures as these have no effect on

cash of the company (Phillips, 2016).

Interest and investment income: Interest from investment income is deducted for the obvious

reason that such income is considered in calculating cash flow from investing activities.

Finance costs: Finance cost will be considered in calculating cash flow from financing activities

hence have to be added back to profit before tax as it not an operating item.

Other non-cash items: All other non-cash items have to be adjusted as these have no effect on

movement of cash (Papanastasopoulos, 2018).

Changes in working capital: The changes in working capital, i.e. total cash assets less total cash

liabilities of the company is added or deducted from adjusted profit before tax after all the above

adjustments. In case increase in working capital it is deduced from the adjusted profit and in case

of reduction the same is added to the adjusted profit.

Income tax payment: The amount paid as income tax is deducted from the resultant amount after

adjustments of changes in working capital (Penman, S.H., 2016).

Changes in items:

SingTel Optus:

Profit before tax in case of SingTel has increased to $4,580.8 million from $4,463 million.

Depreciation and amortization cost has decreased from 2015 to $2,148.8m in 2016. Share of

results (negative) in associates and joint ventures have increased to $2,026.6m in 2016. Non-cash

exception item for 2016 is ($2.4) million is much less than of ($57.7m) of 2015. Fiancé cost of

CORPORATE ACCOUNTING

Exceptional items of non-cash: Non-cash exceptional items have to be added and deducted as the

case may be depending on whether the item is revenue or expenditures as these have no effect on

cash of the company (Phillips, 2016).

Interest and investment income: Interest from investment income is deducted for the obvious

reason that such income is considered in calculating cash flow from investing activities.

Finance costs: Finance cost will be considered in calculating cash flow from financing activities

hence have to be added back to profit before tax as it not an operating item.

Other non-cash items: All other non-cash items have to be adjusted as these have no effect on

movement of cash (Papanastasopoulos, 2018).

Changes in working capital: The changes in working capital, i.e. total cash assets less total cash

liabilities of the company is added or deducted from adjusted profit before tax after all the above

adjustments. In case increase in working capital it is deduced from the adjusted profit and in case

of reduction the same is added to the adjusted profit.

Income tax payment: The amount paid as income tax is deducted from the resultant amount after

adjustments of changes in working capital (Penman, S.H., 2016).

Changes in items:

SingTel Optus:

Profit before tax in case of SingTel has increased to $4,580.8 million from $4,463 million.

Depreciation and amortization cost has decreased from 2015 to $2,148.8m in 2016. Share of

results (negative) in associates and joint ventures have increased to $2,026.6m in 2016. Non-cash

exception item for 2016 is ($2.4) million is much less than of ($57.7m) of 2015. Fiancé cost of

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

10

CORPORATE ACCOUNTING

2016 added back to the profit is $359.6m whereas in 2015 the company only added back

$309.2m. The company has used $2,740m in 2016 on investing activities. In 2015 it invested

$3,556.9m on investment activities. The company in 2016 used net of $2,043.5m to repayment

its debts and borrowings along with payment of dividend compared to $2,310.6m it used in 2015

(Karadag, 2015).

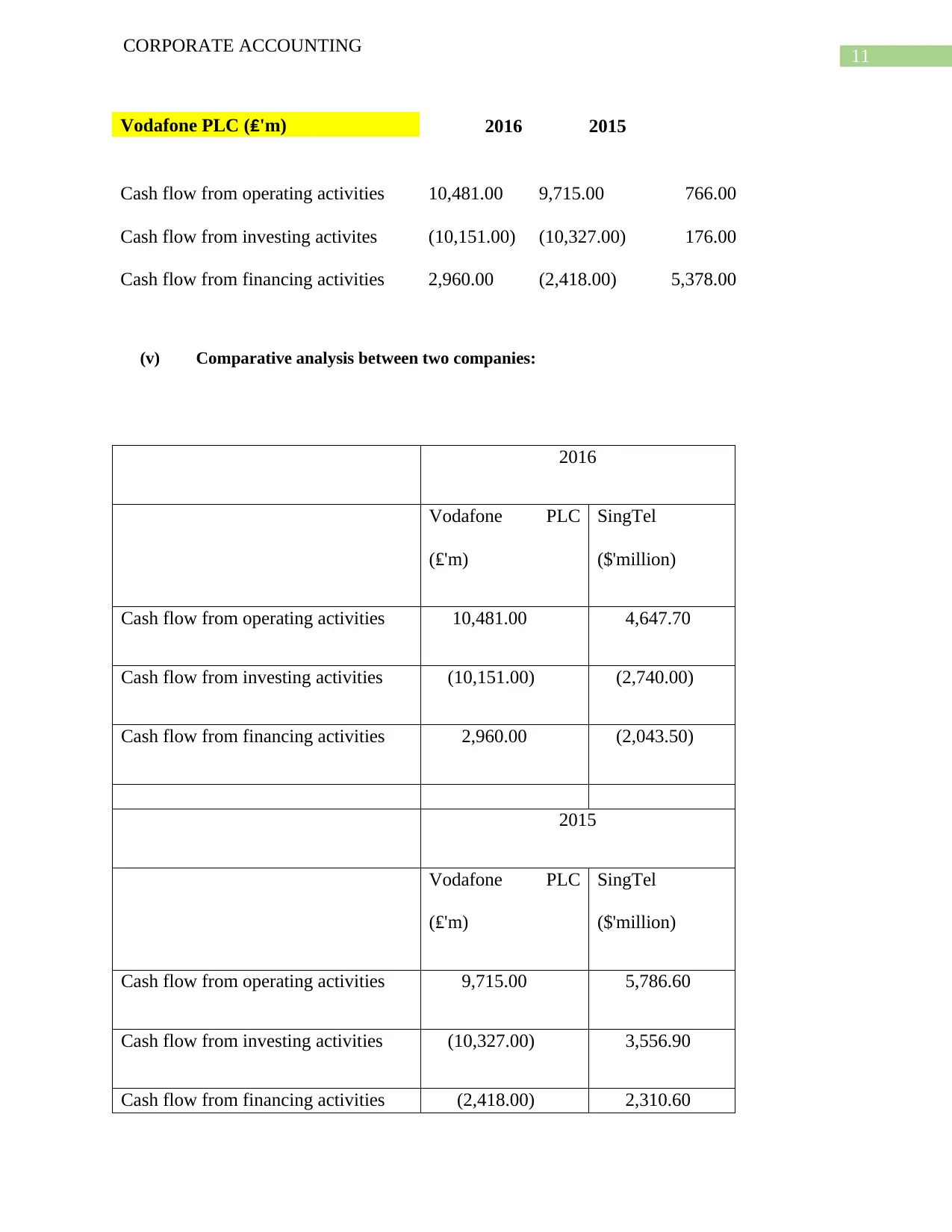

Vodafone PLC:

The net cash generated by the company from operating activities in 2016 is ₤10,481m in net

compared to ₤9,715 in 2015. Thus, a significant improvement by the company in generation cash

flow from operating activities. The increase is mainly due to increase in cash received from

customers. Cash flow used in investing activities of Vodafone for 2016 is ₤10,151m is lower

than ₤10,327m of 2015. The decrease is mainly due to increase in acquisition of interests in

subsidiaries during 2016. The company unlike past has generated cash flow from financing

activities in 2016. In 2016 the company has generated ₤2,960m in cash inflows from financing

activities. In 2015 the company used ₤2,418m in financing activities (Finocchiaro et. al. 2018).

(iv) Comparative analysis of three broad cash flows:

The table below contains comparative analysis of three broad categories of cash flows of the two

companies.

Change

SingTel ($'million) 2,016.00 2,015.00

Increase /

(Decrease)

Cash flow from operating activities 4,647.70 5,786.60 (1,138.90)

Cash flow from investing activities (2,740.00) 3,556.90 (6,296.90)

Cash flow from financing activities (2,043.50) 2,310.60 (4,354.10)

CORPORATE ACCOUNTING

2016 added back to the profit is $359.6m whereas in 2015 the company only added back

$309.2m. The company has used $2,740m in 2016 on investing activities. In 2015 it invested

$3,556.9m on investment activities. The company in 2016 used net of $2,043.5m to repayment

its debts and borrowings along with payment of dividend compared to $2,310.6m it used in 2015

(Karadag, 2015).

Vodafone PLC:

The net cash generated by the company from operating activities in 2016 is ₤10,481m in net

compared to ₤9,715 in 2015. Thus, a significant improvement by the company in generation cash

flow from operating activities. The increase is mainly due to increase in cash received from

customers. Cash flow used in investing activities of Vodafone for 2016 is ₤10,151m is lower

than ₤10,327m of 2015. The decrease is mainly due to increase in acquisition of interests in

subsidiaries during 2016. The company unlike past has generated cash flow from financing

activities in 2016. In 2016 the company has generated ₤2,960m in cash inflows from financing

activities. In 2015 the company used ₤2,418m in financing activities (Finocchiaro et. al. 2018).

(iv) Comparative analysis of three broad cash flows:

The table below contains comparative analysis of three broad categories of cash flows of the two

companies.

Change

SingTel ($'million) 2,016.00 2,015.00

Increase /

(Decrease)

Cash flow from operating activities 4,647.70 5,786.60 (1,138.90)

Cash flow from investing activities (2,740.00) 3,556.90 (6,296.90)

Cash flow from financing activities (2,043.50) 2,310.60 (4,354.10)

11

CORPORATE ACCOUNTING

Vodafone PLC (₤'m) 2016 2015

Cash flow from operating activities 10,481.00 9,715.00 766.00

Cash flow from investing activites (10,151.00) (10,327.00) 176.00

Cash flow from financing activities 2,960.00 (2,418.00) 5,378.00

(v) Comparative analysis between two companies:

2016

Vodafone PLC

(₤'m)

SingTel

($'million)

Cash flow from operating activities 10,481.00 4,647.70

Cash flow from investing activities (10,151.00) (2,740.00)

Cash flow from financing activities 2,960.00 (2,043.50)

2015

Vodafone PLC

(₤'m)

SingTel

($'million)

Cash flow from operating activities 9,715.00 5,786.60

Cash flow from investing activities (10,327.00) 3,556.90

Cash flow from financing activities (2,418.00) 2,310.60

CORPORATE ACCOUNTING

Vodafone PLC (₤'m) 2016 2015

Cash flow from operating activities 10,481.00 9,715.00 766.00

Cash flow from investing activites (10,151.00) (10,327.00) 176.00

Cash flow from financing activities 2,960.00 (2,418.00) 5,378.00

(v) Comparative analysis between two companies:

2016

Vodafone PLC

(₤'m)

SingTel

($'million)

Cash flow from operating activities 10,481.00 4,647.70

Cash flow from investing activities (10,151.00) (2,740.00)

Cash flow from financing activities 2,960.00 (2,043.50)

2015

Vodafone PLC

(₤'m)

SingTel

($'million)

Cash flow from operating activities 9,715.00 5,786.60

Cash flow from investing activities (10,327.00) 3,556.90

Cash flow from financing activities (2,418.00) 2,310.60

12

CORPORATE ACCOUNTING

Other Comprehensive income statement:

(vi) Items of other comprehensive income statement of Vodafone and SingTel:

Vodafone has reported following items:

I. Gain and loss on reclassification of investments available for sale.

II. Gain or loss due to translation of foreign exchange.

III. Gain or loss from foreign exchange translation transferred to income statement.

IV. Gain on fair value.

V. Net actuarial gain or loses (Bratten, Causholli and Khan, 2016).

SingTel Optus has included following items:

I. Exchange differences from translation of foreign exchange operations.

II. Changes in fair value of hedges.

III. Tax effects on the items reported in other comprehensive income statement.

(vii) Reasons to not record above items in income statement:

The above items are not actual realized gain or losses and also not from regular business

operations hence, the above items are not recorded in income statement of an organization. In

this case also these items thus, have been excluded from income statement and included in other

comprehensive income statement (Black, 2016).

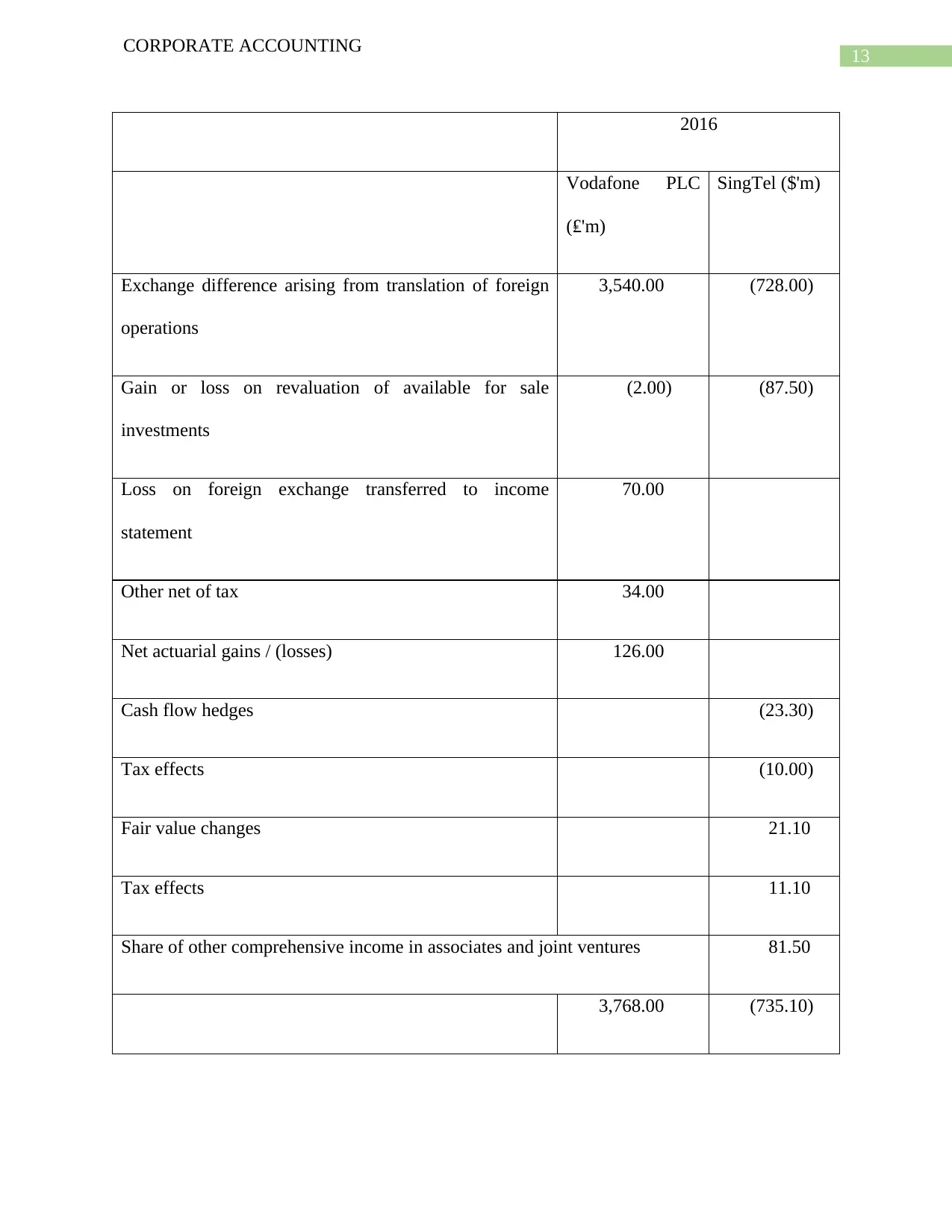

(viii) Comparative analysis of items reported in other comprehensive income statement of

Vodafone PLC and SingTel Optus is provided in a tabular format below:

CORPORATE ACCOUNTING

Other Comprehensive income statement:

(vi) Items of other comprehensive income statement of Vodafone and SingTel:

Vodafone has reported following items:

I. Gain and loss on reclassification of investments available for sale.

II. Gain or loss due to translation of foreign exchange.

III. Gain or loss from foreign exchange translation transferred to income statement.

IV. Gain on fair value.

V. Net actuarial gain or loses (Bratten, Causholli and Khan, 2016).

SingTel Optus has included following items:

I. Exchange differences from translation of foreign exchange operations.

II. Changes in fair value of hedges.

III. Tax effects on the items reported in other comprehensive income statement.

(vii) Reasons to not record above items in income statement:

The above items are not actual realized gain or losses and also not from regular business

operations hence, the above items are not recorded in income statement of an organization. In

this case also these items thus, have been excluded from income statement and included in other

comprehensive income statement (Black, 2016).

(viii) Comparative analysis of items reported in other comprehensive income statement of

Vodafone PLC and SingTel Optus is provided in a tabular format below:

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

13

CORPORATE ACCOUNTING

2016

Vodafone PLC

(₤'m)

SingTel ($'m)

Exchange difference arising from translation of foreign

operations

3,540.00 (728.00)

Gain or loss on revaluation of available for sale

investments

(2.00) (87.50)

Loss on foreign exchange transferred to income

statement

70.00

Other net of tax 34.00

Net actuarial gains / (losses) 126.00

Cash flow hedges (23.30)

Tax effects (10.00)

Fair value changes 21.10

Tax effects 11.10

Share of other comprehensive income in associates and joint ventures 81.50

3,768.00 (735.10)

CORPORATE ACCOUNTING

2016

Vodafone PLC

(₤'m)

SingTel ($'m)

Exchange difference arising from translation of foreign

operations

3,540.00 (728.00)

Gain or loss on revaluation of available for sale

investments

(2.00) (87.50)

Loss on foreign exchange transferred to income

statement

70.00

Other net of tax 34.00

Net actuarial gains / (losses) 126.00

Cash flow hedges (23.30)

Tax effects (10.00)

Fair value changes 21.10

Tax effects 11.10

Share of other comprehensive income in associates and joint ventures 81.50

3,768.00 (735.10)

14

CORPORATE ACCOUNTING

In case the items of other comprehensive income statement would have been included in income

statements of respective companies then the income attributable to the shareholders of Vodafone

would have been higher by ₤3,768 for 2016 and for the shareholders of SingTel the available

profit would have been lower by $735.10 in 2016 (Sözbilir, Kula and Baykut, 2015).

(ix) There is a lot of debate regarding the responsibility of the management in managing the risk

of loss resulting from items reported in other comprehensive income statement. However,

considering that the decision of manage and organization is completely on the shoulders of

the managers including the decision of foreign exchange transactions, hedging and other

strategies thus, the other comprehensive income should be included in evaluating the

performance of managers of an entity (Bauman and Shaw, 2016).

Accounting for corporate income tax:

(x) Tax expense of SingTel Optus in 2016 is $722.5 million and for Vodafone PLC it is ₤3,369

million.

(xi)

Effective tax rate is higher for Vodafone PLC is higher as is seen in the following calculations.

2016

Effective tax rate Vodafone PLC

(₤'m)

SingTel

($'m)

Income tax expenses 3369 722.5

Income before tax -449 4580.8

CORPORATE ACCOUNTING

In case the items of other comprehensive income statement would have been included in income

statements of respective companies then the income attributable to the shareholders of Vodafone

would have been higher by ₤3,768 for 2016 and for the shareholders of SingTel the available

profit would have been lower by $735.10 in 2016 (Sözbilir, Kula and Baykut, 2015).

(ix) There is a lot of debate regarding the responsibility of the management in managing the risk

of loss resulting from items reported in other comprehensive income statement. However,

considering that the decision of manage and organization is completely on the shoulders of

the managers including the decision of foreign exchange transactions, hedging and other

strategies thus, the other comprehensive income should be included in evaluating the

performance of managers of an entity (Bauman and Shaw, 2016).

Accounting for corporate income tax:

(x) Tax expense of SingTel Optus in 2016 is $722.5 million and for Vodafone PLC it is ₤3,369

million.

(xi)

Effective tax rate is higher for Vodafone PLC is higher as is seen in the following calculations.

2016

Effective tax rate Vodafone PLC

(₤'m)

SingTel

($'m)

Income tax expenses 3369 722.5

Income before tax -449 4580.8

15

CORPORATE ACCOUNTING

Effective tax rate (%) (750.33) 15.7

7

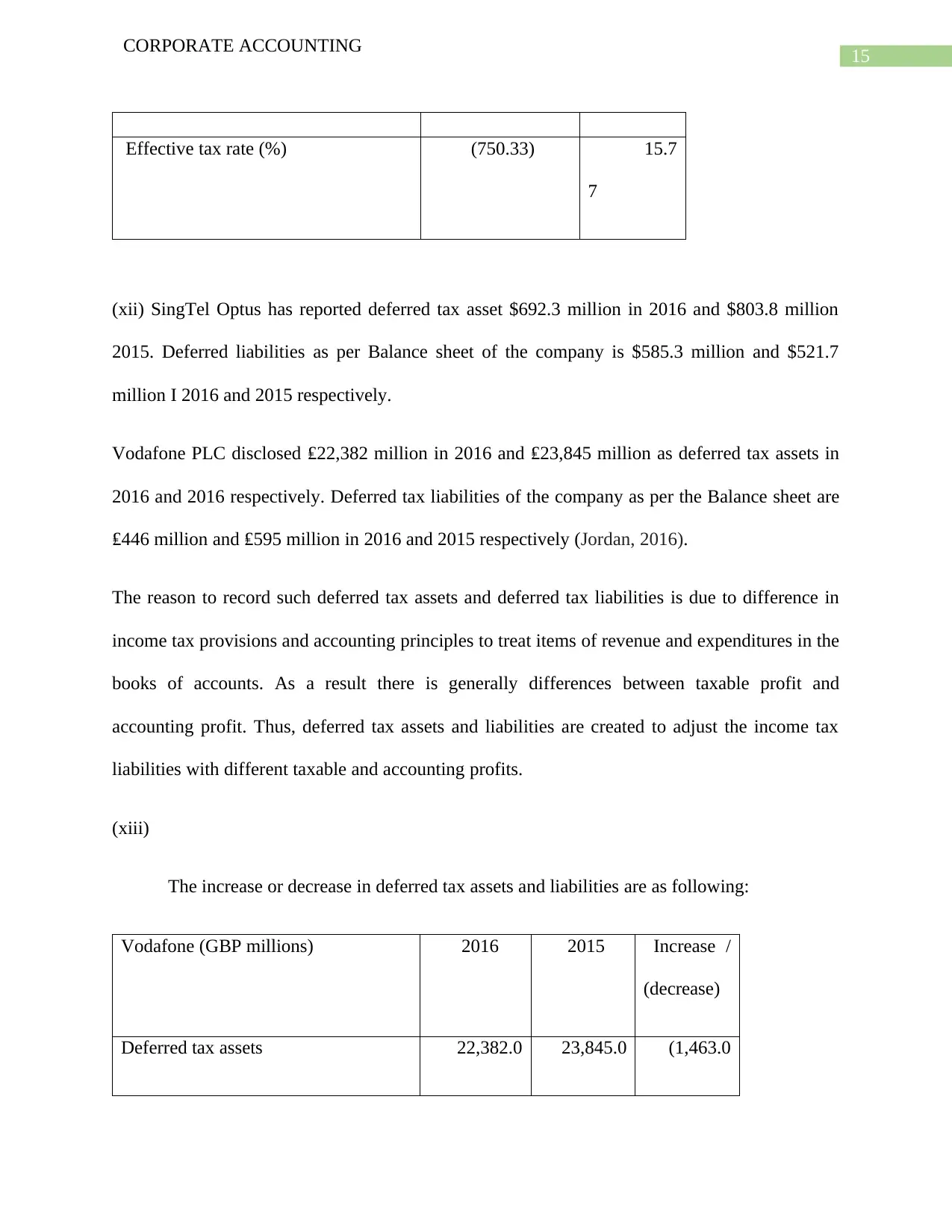

(xii) SingTel Optus has reported deferred tax asset $692.3 million in 2016 and $803.8 million

2015. Deferred liabilities as per Balance sheet of the company is $585.3 million and $521.7

million I 2016 and 2015 respectively.

Vodafone PLC disclosed ₤22,382 million in 2016 and ₤23,845 million as deferred tax assets in

2016 and 2016 respectively. Deferred tax liabilities of the company as per the Balance sheet are

₤446 million and ₤595 million in 2016 and 2015 respectively (Jordan, 2016).

The reason to record such deferred tax assets and deferred tax liabilities is due to difference in

income tax provisions and accounting principles to treat items of revenue and expenditures in the

books of accounts. As a result there is generally differences between taxable profit and

accounting profit. Thus, deferred tax assets and liabilities are created to adjust the income tax

liabilities with different taxable and accounting profits.

(xiii)

The increase or decrease in deferred tax assets and liabilities are as following:

Vodafone (GBP millions) 2016 2015 Increase /

(decrease)

Deferred tax assets 22,382.0 23,845.0 (1,463.0

CORPORATE ACCOUNTING

Effective tax rate (%) (750.33) 15.7

7

(xii) SingTel Optus has reported deferred tax asset $692.3 million in 2016 and $803.8 million

2015. Deferred liabilities as per Balance sheet of the company is $585.3 million and $521.7

million I 2016 and 2015 respectively.

Vodafone PLC disclosed ₤22,382 million in 2016 and ₤23,845 million as deferred tax assets in

2016 and 2016 respectively. Deferred tax liabilities of the company as per the Balance sheet are

₤446 million and ₤595 million in 2016 and 2015 respectively (Jordan, 2016).

The reason to record such deferred tax assets and deferred tax liabilities is due to difference in

income tax provisions and accounting principles to treat items of revenue and expenditures in the

books of accounts. As a result there is generally differences between taxable profit and

accounting profit. Thus, deferred tax assets and liabilities are created to adjust the income tax

liabilities with different taxable and accounting profits.

(xiii)

The increase or decrease in deferred tax assets and liabilities are as following:

Vodafone (GBP millions) 2016 2015 Increase /

(decrease)

Deferred tax assets 22,382.0 23,845.0 (1,463.0

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

16

CORPORATE ACCOUNTING

0 0 0)

Deferred tax liabilities 446.0

0

595.0

0

(149.0

0)

SingTel ($'million) 2,016.0

0

2,015.0

0

Increase /

(decrease)

Deferred tax assets 692.3

0

803.8

0

(111.5

0)

Deferred tax liabilities 583.3

0

521.7

0

61.6

0

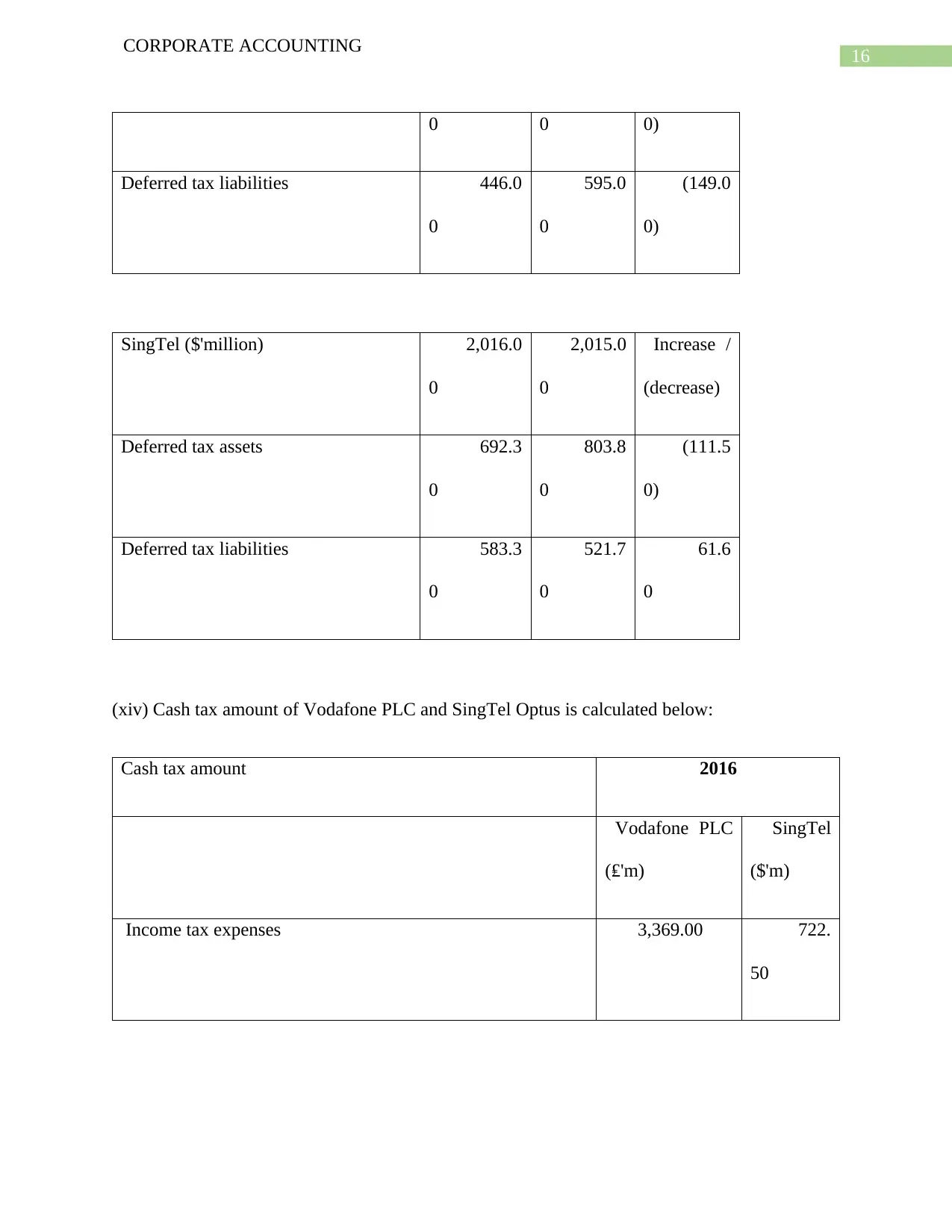

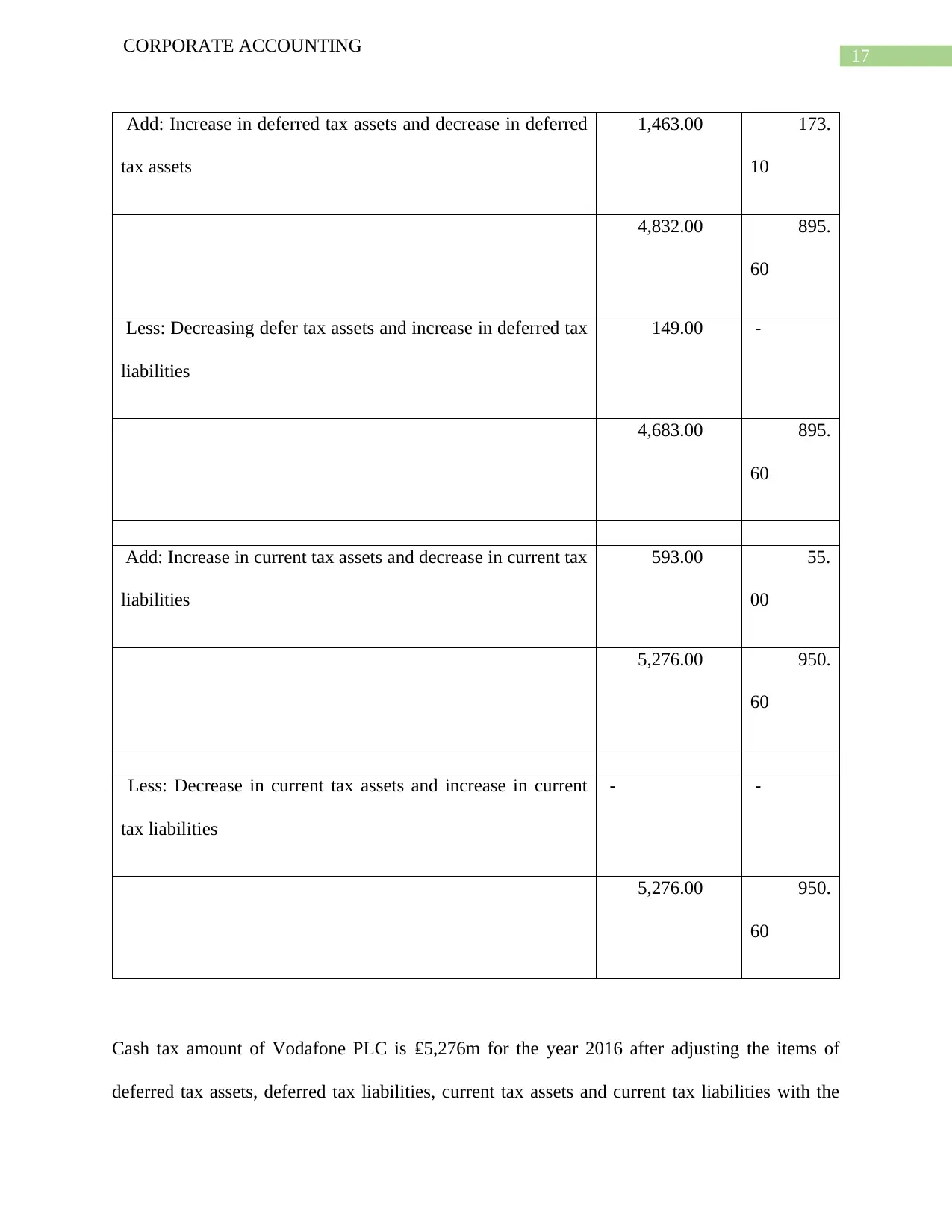

(xiv) Cash tax amount of Vodafone PLC and SingTel Optus is calculated below:

Cash tax amount 2016

Vodafone PLC

(₤'m)

SingTel

($'m)

Income tax expenses 3,369.00 722.

50

CORPORATE ACCOUNTING

0 0 0)

Deferred tax liabilities 446.0

0

595.0

0

(149.0

0)

SingTel ($'million) 2,016.0

0

2,015.0

0

Increase /

(decrease)

Deferred tax assets 692.3

0

803.8

0

(111.5

0)

Deferred tax liabilities 583.3

0

521.7

0

61.6

0

(xiv) Cash tax amount of Vodafone PLC and SingTel Optus is calculated below:

Cash tax amount 2016

Vodafone PLC

(₤'m)

SingTel

($'m)

Income tax expenses 3,369.00 722.

50

17

CORPORATE ACCOUNTING

Add: Increase in deferred tax assets and decrease in deferred

tax assets

1,463.00 173.

10

4,832.00 895.

60

Less: Decreasing defer tax assets and increase in deferred tax

liabilities

149.00 -

4,683.00 895.

60

Add: Increase in current tax assets and decrease in current tax

liabilities

593.00 55.

00

5,276.00 950.

60

Less: Decrease in current tax assets and increase in current

tax liabilities

- -

5,276.00 950.

60

Cash tax amount of Vodafone PLC is ₤5,276m for the year 2016 after adjusting the items of

deferred tax assets, deferred tax liabilities, current tax assets and current tax liabilities with the

CORPORATE ACCOUNTING

Add: Increase in deferred tax assets and decrease in deferred

tax assets

1,463.00 173.

10

4,832.00 895.

60

Less: Decreasing defer tax assets and increase in deferred tax

liabilities

149.00 -

4,683.00 895.

60

Add: Increase in current tax assets and decrease in current tax

liabilities

593.00 55.

00

5,276.00 950.

60

Less: Decrease in current tax assets and increase in current

tax liabilities

- -

5,276.00 950.

60

Cash tax amount of Vodafone PLC is ₤5,276m for the year 2016 after adjusting the items of

deferred tax assets, deferred tax liabilities, current tax assets and current tax liabilities with the

18

CORPORATE ACCOUNTING

amount of income tax expense of the company for the year 2016 (Sözbilir, Kula and Baykut,

2015).

Similarly after making all necessary adjustments to the income tax expense of SingTel Optus the

cash tax amount comes to $950.60m.

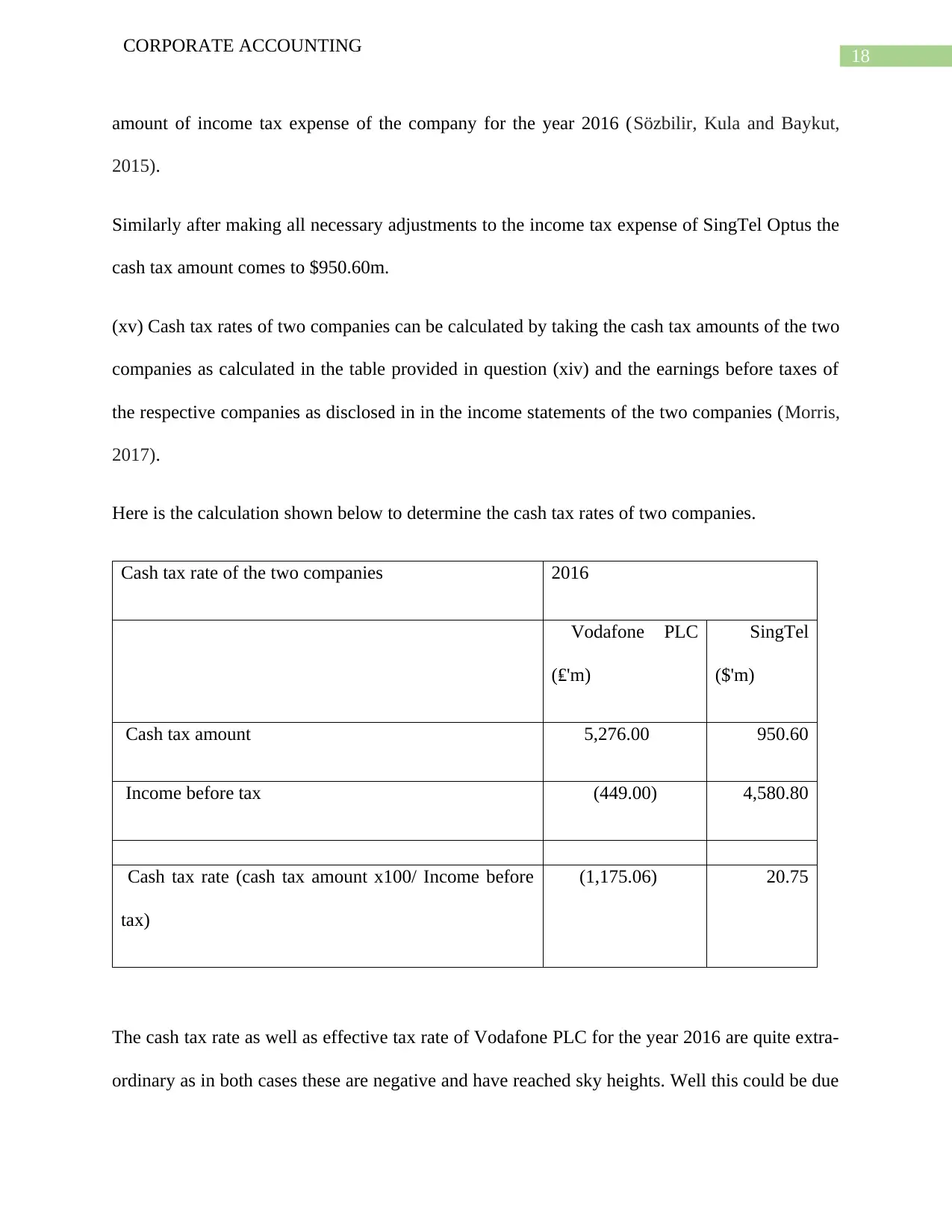

(xv) Cash tax rates of two companies can be calculated by taking the cash tax amounts of the two

companies as calculated in the table provided in question (xiv) and the earnings before taxes of

the respective companies as disclosed in in the income statements of the two companies (Morris,

2017).

Here is the calculation shown below to determine the cash tax rates of two companies.

Cash tax rate of the two companies 2016

Vodafone PLC

(₤'m)

SingTel

($'m)

Cash tax amount 5,276.00 950.60

Income before tax (449.00) 4,580.80

Cash tax rate (cash tax amount x100/ Income before

tax)

(1,175.06) 20.75

The cash tax rate as well as effective tax rate of Vodafone PLC for the year 2016 are quite extra-

ordinary as in both cases these are negative and have reached sky heights. Well this could be due

CORPORATE ACCOUNTING

amount of income tax expense of the company for the year 2016 (Sözbilir, Kula and Baykut,

2015).

Similarly after making all necessary adjustments to the income tax expense of SingTel Optus the

cash tax amount comes to $950.60m.

(xv) Cash tax rates of two companies can be calculated by taking the cash tax amounts of the two

companies as calculated in the table provided in question (xiv) and the earnings before taxes of

the respective companies as disclosed in in the income statements of the two companies (Morris,

2017).

Here is the calculation shown below to determine the cash tax rates of two companies.

Cash tax rate of the two companies 2016

Vodafone PLC

(₤'m)

SingTel

($'m)

Cash tax amount 5,276.00 950.60

Income before tax (449.00) 4,580.80

Cash tax rate (cash tax amount x100/ Income before

tax)

(1,175.06) 20.75

The cash tax rate as well as effective tax rate of Vodafone PLC for the year 2016 are quite extra-

ordinary as in both cases these are negative and have reached sky heights. Well this could be due

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

19

CORPORATE ACCOUNTING

to the certain adjustments of items of revenue and expenditures for taxable purposes. The

accounting profit is negative but the company’s taxable profit is definitely much higher than the

accounting profit hence, the company has paid tax (Richardson, Taylor and Lanis, 2015).

Cash tax rate is way higher for Vodafone PLC with (1,175.06%) however , often such negative

cash rate is considered valid as it does not show the effective as well as actual cash rate. In case

it is assumed that negative tax rates are invalid then in both cases, i.e. effective tax rate and cash

tax rate, SingTel has higher tax rates as the tax rates of Vodafone are negative under both

circumstances (Swank, 2016).

(xvi) The cash tax rates of both the companies are significantly different than the book tax rate,

i.e. the effective tax rates. The table below clearly shows the differences between cash tax and

effective tax rates of both Vodafone and SingTel.

2016

Cash tax rate of the two companies

Vodafone PLC

(₤'m)

SingTel

($'m)

Cash tax amount 5,276.00 950.60

Income before tax (449.00) 4,580.80

Cash tax rate (cash tax amount x100/ Income before

tax) (%) (1,175.06) 20.75

2016

Effective tax rate

Vodafone PLC

(₤'m)

SingTel

($'m)

Income tax expenses 3369 722.5

Income before tax -449 4580.8

Effective tax rate (%) (750.33) 15.77

CORPORATE ACCOUNTING

to the certain adjustments of items of revenue and expenditures for taxable purposes. The

accounting profit is negative but the company’s taxable profit is definitely much higher than the

accounting profit hence, the company has paid tax (Richardson, Taylor and Lanis, 2015).

Cash tax rate is way higher for Vodafone PLC with (1,175.06%) however , often such negative

cash rate is considered valid as it does not show the effective as well as actual cash rate. In case

it is assumed that negative tax rates are invalid then in both cases, i.e. effective tax rate and cash

tax rate, SingTel has higher tax rates as the tax rates of Vodafone are negative under both

circumstances (Swank, 2016).

(xvi) The cash tax rates of both the companies are significantly different than the book tax rate,

i.e. the effective tax rates. The table below clearly shows the differences between cash tax and

effective tax rates of both Vodafone and SingTel.

2016

Cash tax rate of the two companies

Vodafone PLC

(₤'m)

SingTel

($'m)

Cash tax amount 5,276.00 950.60

Income before tax (449.00) 4,580.80

Cash tax rate (cash tax amount x100/ Income before

tax) (%) (1,175.06) 20.75

2016

Effective tax rate

Vodafone PLC

(₤'m)

SingTel

($'m)

Income tax expenses 3369 722.5

Income before tax -449 4580.8

Effective tax rate (%) (750.33) 15.77

20

CORPORATE ACCOUNTING

Simple analysis of the above table would clear the confusion as to the reasons why the cash tax

rates are different from book tax rates of Vodafone PLC and SingTel Optus (Bratten, Causholli

and Khan, U., 2016).

Conclusion:

Different components of financial statements and items reported in these statements have

explained in the document. Analysis of financial statements of two companies have helped in

acquiring substantial knowledge about different financial elements of the companies operating in

practical world. Annual reports of Vodafone PLC and SingTel, the two entities in

telecommunication industry in Australia, have been evaluated in this document to gain practical

knowledge in this regard.

CORPORATE ACCOUNTING

Simple analysis of the above table would clear the confusion as to the reasons why the cash tax

rates are different from book tax rates of Vodafone PLC and SingTel Optus (Bratten, Causholli

and Khan, U., 2016).

Conclusion:

Different components of financial statements and items reported in these statements have

explained in the document. Analysis of financial statements of two companies have helped in

acquiring substantial knowledge about different financial elements of the companies operating in

practical world. Annual reports of Vodafone PLC and SingTel, the two entities in

telecommunication industry in Australia, have been evaluated in this document to gain practical

knowledge in this regard.

21

CORPORATE ACCOUNTING

References:

Bauman, M.P. and Shaw, K.W., 2016. Balance sheet classification and the valuation of deferred

taxes. Research in Accounting Regulation, 28(2), pp.77-85.

Black, D.E., 2016. Other comprehensive income: a review and directions for future

research. Accounting & Finance, 56(1), pp.9-45. [Online] Available at:

https://onlinelibrary.wiley.com/doi/abs/10.1111/acfi.12186 [Accessed 29 September 2018]

Bratten, B., Causholli, M. and Khan, U., 2016. Usefulness of fair values for predicting banks’

future earnings: evidence from other comprehensive income and its components. Review of

Accounting Studies, 21(1), pp.280-315.

Burks, J.J., 2015. Accounting errors in nonprofit organizations. Accounting Horizons, 29(2),

pp.341-361.

Chen, P.C., 2015. Banks' acquisition of private information about financial misreporting. The

Accounting Review, 91(3), pp.835-857.

Chen, S., Miao, B. and Shevlin, T., 2015. A new measure of disclosure quality: The level of

disaggregation of accounting data in annual reports. Journal of Accounting Research, 53(5),

pp.1017-1054.

Christensen, H.B., Lee, E., Walker, M. and Zeng, C., 2015. Incentives or standards: What

determines accounting quality changes around IFRS adoption?. European Accounting

Review, 24(1), pp.31-61.

Cuccia, A., 2018. Potential of IFRS 8: Managerial" customization", relevance of subsidiaries and

separate financial statements. FINANCIAL REPORTING.

CORPORATE ACCOUNTING

References:

Bauman, M.P. and Shaw, K.W., 2016. Balance sheet classification and the valuation of deferred

taxes. Research in Accounting Regulation, 28(2), pp.77-85.

Black, D.E., 2016. Other comprehensive income: a review and directions for future

research. Accounting & Finance, 56(1), pp.9-45. [Online] Available at:

https://onlinelibrary.wiley.com/doi/abs/10.1111/acfi.12186 [Accessed 29 September 2018]

Bratten, B., Causholli, M. and Khan, U., 2016. Usefulness of fair values for predicting banks’

future earnings: evidence from other comprehensive income and its components. Review of

Accounting Studies, 21(1), pp.280-315.

Burks, J.J., 2015. Accounting errors in nonprofit organizations. Accounting Horizons, 29(2),

pp.341-361.

Chen, P.C., 2015. Banks' acquisition of private information about financial misreporting. The

Accounting Review, 91(3), pp.835-857.

Chen, S., Miao, B. and Shevlin, T., 2015. A new measure of disclosure quality: The level of

disaggregation of accounting data in annual reports. Journal of Accounting Research, 53(5),

pp.1017-1054.

Christensen, H.B., Lee, E., Walker, M. and Zeng, C., 2015. Incentives or standards: What

determines accounting quality changes around IFRS adoption?. European Accounting

Review, 24(1), pp.31-61.

Cuccia, A., 2018. Potential of IFRS 8: Managerial" customization", relevance of subsidiaries and

separate financial statements. FINANCIAL REPORTING.

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

22

CORPORATE ACCOUNTING

Finocchiaro, D., Lombardo, G., Mendicino, C. and Weil, P., 2018. Optimal inflation with

corporate taxation and financial constraints. Journal of Monetary Economics, 95, pp.18-31.

Floyd, W.F., 2016. Financial Reporting Quality and Voluntary Disclosure (Doctoral dissertation,

Stanford University).

Graham, A., Nandialath, A.M., Skaradzinski, D. and Rustambekov, E., 2017. Macroeconomic

Determinants of International Financial Reporting Standards (IFRS) Adoption: Evidence from

the Middle East North Africa (MENA) Region. [Online] Available at:

https://papers.ssrn.com/sol3/papers.cfm?abstract_id=3025011 [Accessed 29 September 2018]

Heidari, M. and Felden, C., 2015, May. Impact of text mining application on financial footnotes

analysis. In International Conference on Design Science Research in Information Systems (pp.

463-470). Springer, Cham.

Jordan, C.E., 2016. FASB's New Standard for Classifying Deferred Taxes. The CPA

Journal, 86(7), p.22.

Karadag, H., 2015. Financial management challenges in small and medium-sized enterprises: A

strategic management approach. EMAJ: Emerging Markets Journal, 5(1), pp.26-40. [Online]

Available at: http://emaj.pitt.edu/ojs/index.php/emaj/article/view/67 [Accessed 29 September

2018]

Leuz, C. and Wysocki, P.D., 2016. The economics of disclosure and financial reporting

regulation: Evidence and suggestions for future research. Journal of Accounting Research, 54(2),

pp.525-622.

CORPORATE ACCOUNTING

Finocchiaro, D., Lombardo, G., Mendicino, C. and Weil, P., 2018. Optimal inflation with

corporate taxation and financial constraints. Journal of Monetary Economics, 95, pp.18-31.

Floyd, W.F., 2016. Financial Reporting Quality and Voluntary Disclosure (Doctoral dissertation,

Stanford University).

Graham, A., Nandialath, A.M., Skaradzinski, D. and Rustambekov, E., 2017. Macroeconomic

Determinants of International Financial Reporting Standards (IFRS) Adoption: Evidence from

the Middle East North Africa (MENA) Region. [Online] Available at:

https://papers.ssrn.com/sol3/papers.cfm?abstract_id=3025011 [Accessed 29 September 2018]

Heidari, M. and Felden, C., 2015, May. Impact of text mining application on financial footnotes

analysis. In International Conference on Design Science Research in Information Systems (pp.

463-470). Springer, Cham.

Jordan, C.E., 2016. FASB's New Standard for Classifying Deferred Taxes. The CPA

Journal, 86(7), p.22.

Karadag, H., 2015. Financial management challenges in small and medium-sized enterprises: A

strategic management approach. EMAJ: Emerging Markets Journal, 5(1), pp.26-40. [Online]

Available at: http://emaj.pitt.edu/ojs/index.php/emaj/article/view/67 [Accessed 29 September

2018]

Leuz, C. and Wysocki, P.D., 2016. The economics of disclosure and financial reporting

regulation: Evidence and suggestions for future research. Journal of Accounting Research, 54(2),

pp.525-622.

23

CORPORATE ACCOUNTING

Li, X. and Yang, H.I., 2015. Mandatory financial reporting and voluntary disclosure: The effect

of mandatory IFRS adoption on management forecasts. The Accounting Review, 91(3), pp.933-

953.

Morris, J.L., 2017. Classification of Deferred Tax Assets and Deferred Tax Liabilities: An

Evaluation of FASB's Attempt at Standards Simplification. Journal of Accounting & Finance

(2158-3625), 17(8).

Papanastasopoulos, G.A., 2018. JM WahlenS. P. BaginskiM. BradshawReview of Financial

Reporting, Financial Statement Analysis and Valuation: A Strategic Perspective9th ed.

2018Cengage Learning978-1337614689 (995 pp., $228.25). [Online] Available at:

https://www.sciencedirect.com/science/article/pii/S0020706318301286 [Accessed 29 September

2018]

Penman, S.H., 2016. The design of financial statements. [Online] Available from:

https://academiccommons.columbia.edu/doi/10.7916/D82N5DNK [Accessed 27 September

2018]

Phillips, F., 2016. Withholding Financial Statement Analysis Formulas When Instructing and

Testing: A Desirable Difficulty. [Online] Available at: https://papers.ssrn.com/sol3/papers.cfm?

abstract_id=2835694 [Accessed 29 September 2018]

Richardson, G., Taylor, G. and Lanis, R., 2015. The impact of financial distress on corporate tax

avoidance spanning the global financial crisis: Evidence from Australia. Economic

Modelling, 44, pp.44-53.

CORPORATE ACCOUNTING

Li, X. and Yang, H.I., 2015. Mandatory financial reporting and voluntary disclosure: The effect

of mandatory IFRS adoption on management forecasts. The Accounting Review, 91(3), pp.933-

953.

Morris, J.L., 2017. Classification of Deferred Tax Assets and Deferred Tax Liabilities: An

Evaluation of FASB's Attempt at Standards Simplification. Journal of Accounting & Finance

(2158-3625), 17(8).

Papanastasopoulos, G.A., 2018. JM WahlenS. P. BaginskiM. BradshawReview of Financial

Reporting, Financial Statement Analysis and Valuation: A Strategic Perspective9th ed.

2018Cengage Learning978-1337614689 (995 pp., $228.25). [Online] Available at:

https://www.sciencedirect.com/science/article/pii/S0020706318301286 [Accessed 29 September

2018]

Penman, S.H., 2016. The design of financial statements. [Online] Available from:

https://academiccommons.columbia.edu/doi/10.7916/D82N5DNK [Accessed 27 September

2018]

Phillips, F., 2016. Withholding Financial Statement Analysis Formulas When Instructing and

Testing: A Desirable Difficulty. [Online] Available at: https://papers.ssrn.com/sol3/papers.cfm?

abstract_id=2835694 [Accessed 29 September 2018]

Richardson, G., Taylor, G. and Lanis, R., 2015. The impact of financial distress on corporate tax

avoidance spanning the global financial crisis: Evidence from Australia. Economic

Modelling, 44, pp.44-53.

24

CORPORATE ACCOUNTING

Sözbilir, H., Kula, V. and Baykut, L.E., 2015. A Research on Deferred Taxes: A Case Study of

BIST Listed Banks in Turkey. European Journal of Business and Management, 7(2), pp.1-9.

Swank, D., 2016. Taxing choices: international competition, domestic institutions and the

transformation of corporate tax policy. Journal of European Public Policy, 23(4), pp.571-603.

CORPORATE ACCOUNTING

Sözbilir, H., Kula, V. and Baykut, L.E., 2015. A Research on Deferred Taxes: A Case Study of

BIST Listed Banks in Turkey. European Journal of Business and Management, 7(2), pp.1-9.

Swank, D., 2016. Taxing choices: international competition, domestic institutions and the

transformation of corporate tax policy. Journal of European Public Policy, 23(4), pp.571-603.

1 out of 25

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

© 2024 | Zucol Services PVT LTD | All rights reserved.