Impact of Corporate Governance in Retail Segment in Singapore

VerifiedAdded on 2023/06/11

|47

|11069

|165

AI Summary

This dissertation analyzes the effect of corporate governance on the retail sector companies in Singapore. It includes a literature review, research methodology, data analysis, and results. The research questions address the level of corporate governance in the retail industry and the difference between firms listed in the Main Board and Catalyst. The study's contributions include identifying the necessity of corporate governance disclosures, laws, and exercises regarding corporate social accountability.

Contribute Materials

Your contribution can guide someone’s learning journey. Share your

documents today.

Running head: CORPORATE GOVERNANCE IN RETAIL SEGMENT IN

SINGAPORE

Analysis of the effect of corporate governance in particularly retail segment in

Singapore

University Name

Student Name

Authors’ Note

SINGAPORE

Analysis of the effect of corporate governance in particularly retail segment in

Singapore

University Name

Student Name

Authors’ Note

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

2CORPORATE GOVERNANCE IN RETAIL SEGMENT IN SINGAPORE Appendix

Abstract

The dissertation constitutes of having an understanding of the impact of corporate

governance on the retail sector companies. In order to have proper understanding

thirty companies have been selected and thereafter analysis has been done. The

research questions that have been constructed addresses these areas and

accordingly an idea can be attained with the help of which completion of the paper

has been done. The literature review has provided extensive idea about the previous

researches and what theories have been applicable for corporate governance index.

The research methodology highlights the methods and the processes that have been

used with the help of which data analysis has been possible. In this manner the

analysis has been complete and the results have been able to address the objective

of the dissertation.

Abstract

The dissertation constitutes of having an understanding of the impact of corporate

governance on the retail sector companies. In order to have proper understanding

thirty companies have been selected and thereafter analysis has been done. The

research questions that have been constructed addresses these areas and

accordingly an idea can be attained with the help of which completion of the paper

has been done. The literature review has provided extensive idea about the previous

researches and what theories have been applicable for corporate governance index.

The research methodology highlights the methods and the processes that have been

used with the help of which data analysis has been possible. In this manner the

analysis has been complete and the results have been able to address the objective

of the dissertation.

3CORPORATE GOVERNANCE IN RETAIL SEGMENT IN SINGAPORE Appendix

Table of Contents

Chapter 1: Introduction.................................................................................................4

1.1 Background of the research study......................................................................4

1.2 Objectives of the research..................................................................................6

1.3 Research Questions...........................................................................................6

1.4Research Contributions.......................................................................................6

1.5 Organization of the Dissertation.........................................................................7

Chapter 2......................................................................................................................9

2.1 Introduction.........................................................................................................9

2.2 Definitions of Corporate Governance.................................................................9

2.2.1 Benefits of Corporate Governance................................................................10

2.3 Code of Corporate governance use for the research.......................................10

2.4 Prior Studies on corporate governance............................................................12

2.4.1 Agency Theory...............................................................................................16

2.4.2 Stewardship Theory.......................................................................................17

2.5 Summary of the Literature................................................................................18

Chapter 3....................................................................................................................19

3.1 Introduction.......................................................................................................19

3.2 Research Context.............................................................................................19

3.3 Research Method..............................................................................................20

3.4 Data Analysis....................................................................................................21

Table of Contents

Chapter 1: Introduction.................................................................................................4

1.1 Background of the research study......................................................................4

1.2 Objectives of the research..................................................................................6

1.3 Research Questions...........................................................................................6

1.4Research Contributions.......................................................................................6

1.5 Organization of the Dissertation.........................................................................7

Chapter 2......................................................................................................................9

2.1 Introduction.........................................................................................................9

2.2 Definitions of Corporate Governance.................................................................9

2.2.1 Benefits of Corporate Governance................................................................10

2.3 Code of Corporate governance use for the research.......................................10

2.4 Prior Studies on corporate governance............................................................12

2.4.1 Agency Theory...............................................................................................16

2.4.2 Stewardship Theory.......................................................................................17

2.5 Summary of the Literature................................................................................18

Chapter 3....................................................................................................................19

3.1 Introduction.......................................................................................................19

3.2 Research Context.............................................................................................19

3.3 Research Method..............................................................................................20

3.4 Data Analysis....................................................................................................21

4CORPORATE GOVERNANCE IN RETAIL SEGMENT IN SINGAPORE Appendix

3.5 Summary...........................................................................................................22

Chapter 4....................................................................................................................24

4.1 Descriptive Statistics.........................................................................................24

Chapter 5:...................................................................................................................30

5.1 Conclusion and Recommendation....................................................................30

References.................................................................................................................34

Appendix.....................................................................................................................42

3.5 Summary...........................................................................................................22

Chapter 4....................................................................................................................24

4.1 Descriptive Statistics.........................................................................................24

Chapter 5:...................................................................................................................30

5.1 Conclusion and Recommendation....................................................................30

References.................................................................................................................34

Appendix.....................................................................................................................42

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

5CORPORATE GOVERNANCE IN RETAIL SEGMENT IN SINGAPORE Appendix

Chapter 1: Introduction

1.1 Background/Context of the research study

Corporate governance (CG) can be illustrated as the specific system by which

business concerns can be directed and at the same time controlled. The primary

objective is often mentioned as being the augmentation of corporate profit and gains

from shareholders whilst having regard to the influence that this might have on other

stakeholders of the firm. Sir Adrian Cadbury affirmed that corporate governance

(CG) is apprehensive about presenting a sense of balance between different

financial as well as social purposes as well as between individuals with communal

intentions (Trickerand Tricker2015). In essence, the framework for corporate

governance (CG) is expected to inspire effective employment of resources and to

call for liability for principally stewardship of firms’ resources. In particular, the

primary intention is to bring into line specific interests of different individuals,

businesses and society as per reports of “Global Corporate Governance Forum,

World Bank of the year 2000 (Du Plessiset al. 2018). Thus, in line with the above

mentioned discussions mentioned above, framework and structure of corporate

governance along with mechanisms are commonly targeted at enhancing overall

efficacy of the company otherwise performance and delivering higher transparency

along with accountability to firm’s shareholders along with other stakeholders.

Retail firms in Singapore

Retail as well as consumer product firms encounter different challenges in

competitive climate. Particularly, in different mature markets, companies operating in

R&C industry in Singapore are constrained in their capability to develop and maintain

Chapter 1: Introduction

1.1 Background/Context of the research study

Corporate governance (CG) can be illustrated as the specific system by which

business concerns can be directed and at the same time controlled. The primary

objective is often mentioned as being the augmentation of corporate profit and gains

from shareholders whilst having regard to the influence that this might have on other

stakeholders of the firm. Sir Adrian Cadbury affirmed that corporate governance

(CG) is apprehensive about presenting a sense of balance between different

financial as well as social purposes as well as between individuals with communal

intentions (Trickerand Tricker2015). In essence, the framework for corporate

governance (CG) is expected to inspire effective employment of resources and to

call for liability for principally stewardship of firms’ resources. In particular, the

primary intention is to bring into line specific interests of different individuals,

businesses and society as per reports of “Global Corporate Governance Forum,

World Bank of the year 2000 (Du Plessiset al. 2018). Thus, in line with the above

mentioned discussions mentioned above, framework and structure of corporate

governance along with mechanisms are commonly targeted at enhancing overall

efficacy of the company otherwise performance and delivering higher transparency

along with accountability to firm’s shareholders along with other stakeholders.

Retail firms in Singapore

Retail as well as consumer product firms encounter different challenges in

competitive climate. Particularly, in different mature markets, companies operating in

R&C industry in Singapore are constrained in their capability to develop and maintain

6CORPORATE GOVERNANCE IN RETAIL SEGMENT IN SINGAPORE Appendix

specific profit margins as an outcome of a deflationary operating environment,

saturation in the market, declining growth of population, and more discriminating but

less trustworthy customers. In addition to this, pressure is the emergence of

alternative channels of sales, a blurring of roles between suppliers as well as

retailers and a transformation in the balance of power to different retailers. As

suggested by Larcker and Tayan(2015), this has shifted the strategic concentration

of the segment towards the expanding consumer market of both India as well as

China that presents novel opportunities for growth by means of global sourcing, off-

sourcing along with development of current retailers. Furthermore, owing to

stakeholder demands and ensuing Sarbanes-Oxley Legislation, the retail as well as

consumer product segment is also experiencing heightened pressure and stress of

regulation (Cuomo et al. 2016). In essence, these involve greater liability and

accuracy in the process of reporting of financial outcomes under the standards of

IFRS together with US GAAP, enhanced level of corporate governance and

engagement of the Board, stronger internal control documentation and a greater

need for stringer risk management exercises across the business enterprises (Ilievet

al.2015). One of the major challenges encountered by the retail and consumer

product firms in Singapore is that of corporate governance.

1.2 Research Objectives

The primary objective of the research study at hand is

- To comprehend and analyse overall level of corporate governance in particularly

retail segment in Singapore

- To analytically assess difference between overall corporate governance between

firms that is listed in mainly the Main Board and Catalyst

specific profit margins as an outcome of a deflationary operating environment,

saturation in the market, declining growth of population, and more discriminating but

less trustworthy customers. In addition to this, pressure is the emergence of

alternative channels of sales, a blurring of roles between suppliers as well as

retailers and a transformation in the balance of power to different retailers. As

suggested by Larcker and Tayan(2015), this has shifted the strategic concentration

of the segment towards the expanding consumer market of both India as well as

China that presents novel opportunities for growth by means of global sourcing, off-

sourcing along with development of current retailers. Furthermore, owing to

stakeholder demands and ensuing Sarbanes-Oxley Legislation, the retail as well as

consumer product segment is also experiencing heightened pressure and stress of

regulation (Cuomo et al. 2016). In essence, these involve greater liability and

accuracy in the process of reporting of financial outcomes under the standards of

IFRS together with US GAAP, enhanced level of corporate governance and

engagement of the Board, stronger internal control documentation and a greater

need for stringer risk management exercises across the business enterprises (Ilievet

al.2015). One of the major challenges encountered by the retail and consumer

product firms in Singapore is that of corporate governance.

1.2 Research Objectives

The primary objective of the research study at hand is

- To comprehend and analyse overall level of corporate governance in particularly

retail segment in Singapore

- To analytically assess difference between overall corporate governance between

firms that is listed in mainly the Main Board and Catalyst

7CORPORATE GOVERNANCE IN RETAIL SEGMENT IN SINGAPORE Appendix

1.3 Questions of the research study

Q1: What is the degree and level of corporate governance disclosure in retail

industry in Singapore?

Q2: What is the difference in degree and level of corporate governance (CG)

between xx firm listed in the Main Board vs Catalist?

1.4 Research Contributions

The study of the level of corporate governance in firms can aid in

understanding the requirement for enhancement of accountability of the firm for

averting massive disaster before they take place (Iliev et al.2015). Based on the

findings of the study, it will be possible to understand necessity of corporate

governance associated disclosures, laws and exercises regarding corporate social

accountability. It helps in understanding the practices that mainly take account of

having an effectual board that is aware of roles as well as accountabilities and that is

delivered with access to requisite information to perform these accountabilities. This

study helps in gaining insight regarding the governance exercises that include strong

self-governing component on the specific board with no power concentration in any

specific individual. They also have formal as well as transparent procedures for

appointment of boards, performance of boards and executive remuneration (Cuomo

et al.2016).

Also, this study can help in identifying persons accountable for both disclosure

as well as transparency, corporate governance associated disclosures and role of

auditors in such kind of auditors (Armstrong et al.2015). Also, the study on corporate

governance of firms operating in the retail sector can aid in understanding

performance of companies as well as boards, association between both board and

1.3 Questions of the research study

Q1: What is the degree and level of corporate governance disclosure in retail

industry in Singapore?

Q2: What is the difference in degree and level of corporate governance (CG)

between xx firm listed in the Main Board vs Catalist?

1.4 Research Contributions

The study of the level of corporate governance in firms can aid in

understanding the requirement for enhancement of accountability of the firm for

averting massive disaster before they take place (Iliev et al.2015). Based on the

findings of the study, it will be possible to understand necessity of corporate

governance associated disclosures, laws and exercises regarding corporate social

accountability. It helps in understanding the practices that mainly take account of

having an effectual board that is aware of roles as well as accountabilities and that is

delivered with access to requisite information to perform these accountabilities. This

study helps in gaining insight regarding the governance exercises that include strong

self-governing component on the specific board with no power concentration in any

specific individual. They also have formal as well as transparent procedures for

appointment of boards, performance of boards and executive remuneration (Cuomo

et al.2016).

Also, this study can help in identifying persons accountable for both disclosure

as well as transparency, corporate governance associated disclosures and role of

auditors in such kind of auditors (Armstrong et al.2015). Also, the study on corporate

governance of firms operating in the retail sector can aid in understanding

performance of companies as well as boards, association between both board and

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

8CORPORATE GOVERNANCE IN RETAIL SEGMENT IN SINGAPORE Appendix

management of executive. Furthermore, this study also helps in understanding

membership of boards and accountabilities, management of risk, compliance and

internal controls. Moreover, this study helps in understanding communication

between the board, with the shareholders and financial reporting.

1.5 Dissertation Organization

The dissertation will be completed in a structured manner. The initial chapter

of the dissertation constitutes of the introduction where a background has been

provided and thereafter research question for this paper is constructed. In this

manner, the next section of the dissertation is prepared which is known as the

literature review. This section provides an idea about the topic and accordingly

points out the previous studies that have been undertaken. This assists in

understanding the process that will be undertaken with the help of which proper

analysis of the paper can be constructed. The third section of the paper is the

methodology where the process of collecting data and what kind of data will be

considered so as to complete the entire paper. Investigation section will provide

extensive answer as to how the research was done and the last section of the paper

will provide an idea about the final result that has been attained and any kind of

recommendation that can b given with the help of which the completion of the

dissertation will be possible.

management of executive. Furthermore, this study also helps in understanding

membership of boards and accountabilities, management of risk, compliance and

internal controls. Moreover, this study helps in understanding communication

between the board, with the shareholders and financial reporting.

1.5 Dissertation Organization

The dissertation will be completed in a structured manner. The initial chapter

of the dissertation constitutes of the introduction where a background has been

provided and thereafter research question for this paper is constructed. In this

manner, the next section of the dissertation is prepared which is known as the

literature review. This section provides an idea about the topic and accordingly

points out the previous studies that have been undertaken. This assists in

understanding the process that will be undertaken with the help of which proper

analysis of the paper can be constructed. The third section of the paper is the

methodology where the process of collecting data and what kind of data will be

considered so as to complete the entire paper. Investigation section will provide

extensive answer as to how the research was done and the last section of the paper

will provide an idea about the final result that has been attained and any kind of

recommendation that can b given with the help of which the completion of the

dissertation will be possible.

9CORPORATE GOVERNANCE IN RETAIL SEGMENT IN SINGAPORE Appendix

Chapter 2

Review of Literature

2.1 Introduction

The current section reviews prior academic works undertaken on corporate

governance by scholars and extracts relevant concepts useful concepts for the

current study. This segment gives details about the benefits and advantages of

corporate governance, varied latest codes of uses of corporate governance along

with theoretical reflection. The literature review of the paper would initially look to

discuss the definitions of corporate governance with the help of which an idea can be

attained so that the work can proceed further. The benefits of corporate governance

within a company will even be discussed with the help of which better idea about

corporate governance will be known. The latest code of corporate governance will

even be discussed with the help of which proper idea on the topic can be known with

respect to Singapore. There are various theories that have been explained that are

related to corporate governance.

2.2 Definitions of Corporate Governance

As rightly indicated by Ocak and Arıkboğa (2017), corporate governance

indicates towards the way a specific business corporation is governed. In essence,

this is the manner by which firms are essentially directed and handled and implies

undertaking the business according to the desires of stakeholders. Fundamentally,

this is actually undertaken by Directors and the concerned committees for the firm’s

stakeholder’s advantage. In actual fact, this corporate governance can be said to be

all about balancing individual and at the same time individual objectives, in addition

to socio-economic objectives. Essentially, corporate governance can be said to be

Chapter 2

Review of Literature

2.1 Introduction

The current section reviews prior academic works undertaken on corporate

governance by scholars and extracts relevant concepts useful concepts for the

current study. This segment gives details about the benefits and advantages of

corporate governance, varied latest codes of uses of corporate governance along

with theoretical reflection. The literature review of the paper would initially look to

discuss the definitions of corporate governance with the help of which an idea can be

attained so that the work can proceed further. The benefits of corporate governance

within a company will even be discussed with the help of which better idea about

corporate governance will be known. The latest code of corporate governance will

even be discussed with the help of which proper idea on the topic can be known with

respect to Singapore. There are various theories that have been explained that are

related to corporate governance.

2.2 Definitions of Corporate Governance

As rightly indicated by Ocak and Arıkboğa (2017), corporate governance

indicates towards the way a specific business corporation is governed. In essence,

this is the manner by which firms are essentially directed and handled and implies

undertaking the business according to the desires of stakeholders. Fundamentally,

this is actually undertaken by Directors and the concerned committees for the firm’s

stakeholder’s advantage. In actual fact, this corporate governance can be said to be

all about balancing individual and at the same time individual objectives, in addition

to socio-economic objectives. Essentially, corporate governance can be said to be

10CORPORATE GOVERNANCE IN RETAIL SEGMENT IN SINGAPORE Appendix

an interaction between different participants that can help in shaping performance of

associations and the way it is proceeding towards.

2.2.1 Benefits of Corporate Governance

As suggested by Bain and Band (2016), good corporate governance makes

certain success of corporate governance and ensure higher rate of economic growth.

good corporate governance asserts the fact that nature of association between

owners and managers operating in a business concern need to be healthy and there

must not be any kind of disagreement (De Haanand Vlahu2016). Also, the owners

need to see that actual performance of individuals is as per standard performance.

As suggested by Ilievet al.(2015), corporate governance helps in the process of

ascertainment of specific ways to undertake effectual strategic decisions. This

provides authority and at the same time accountability to directors of the board of

firms. Nowadays, in case of market oriented system, requirement for corporate

governance stems. Additionally, level of efficacy of operation and globalization can

be considered to be significant facets that advocate corporate governance. As such,

corporate governance is necessary to build up value to firm’s stakeholders.

Essentially, corporate governance makes certain maintenance of transparency that

ensures strong and balanced economic development (Cuomo et al.2016). This also

makes certain that interests of shareholders are shielded appropriately and helps in

exercising rights and proper recognition of rights of corporation.

2.3 Code of Corporate governance (CG) use for research

The backdrop of corporate governance- CG code goes back long back when

it known as Combined Code, which provided the standards of the effective practices

for the companies that are listed relating to composition of firms’ board and other

factors as well (Tricker and Tricker 2015). The code used to get published by the

an interaction between different participants that can help in shaping performance of

associations and the way it is proceeding towards.

2.2.1 Benefits of Corporate Governance

As suggested by Bain and Band (2016), good corporate governance makes

certain success of corporate governance and ensure higher rate of economic growth.

good corporate governance asserts the fact that nature of association between

owners and managers operating in a business concern need to be healthy and there

must not be any kind of disagreement (De Haanand Vlahu2016). Also, the owners

need to see that actual performance of individuals is as per standard performance.

As suggested by Ilievet al.(2015), corporate governance helps in the process of

ascertainment of specific ways to undertake effectual strategic decisions. This

provides authority and at the same time accountability to directors of the board of

firms. Nowadays, in case of market oriented system, requirement for corporate

governance stems. Additionally, level of efficacy of operation and globalization can

be considered to be significant facets that advocate corporate governance. As such,

corporate governance is necessary to build up value to firm’s stakeholders.

Essentially, corporate governance makes certain maintenance of transparency that

ensures strong and balanced economic development (Cuomo et al.2016). This also

makes certain that interests of shareholders are shielded appropriately and helps in

exercising rights and proper recognition of rights of corporation.

2.3 Code of Corporate governance (CG) use for research

The backdrop of corporate governance- CG code goes back long back when

it known as Combined Code, which provided the standards of the effective practices

for the companies that are listed relating to composition of firms’ board and other

factors as well (Tricker and Tricker 2015). The code used to get published by the

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

11CORPORATE GOVERNANCE IN RETAIL SEGMENT IN SINGAPORE Appendix

Financial Reporting Council. The study on analysis of level and degree of corporate

governance in firms operating in retail segment in Singapore can help in

understanding method of governing firms, instating, laws, and customs along with

strategies. The study at hand aids in understanding the study of corporate

governance in the area of Singapore based on latest code of corporate governance.

This study helps in understanding the practices stipulated under the latest codes

under corporate governance laws. Essentially, this study helps in understanding the

code implementing 15 principles, complemented by guidelines related to board

matters, remuneration matters, accountability and executive remuneration (Tricker

and Tricker 2015). This needs to be facilitated by nomination as well as

remuneration committee for overseeing different matters. Particularly, this study also

explains importance of accountability and audit, and requires institution of audit

committees and internal audit function as a significant aspect of corporate

governance as per latest codes. In addition to this, this study also helps in

understanding significance of strong internal control procedures in place and this

promotes greater disclosure for and communicates with different shareholders

(McCaheryet al. 2016). Therefore, the current research paper discusses current

developments along with future trends in the region of corporate governance-CG in

the region of Singapore.

This account of the Code has at its heart Principles of CG-corporate

governance. Conformity with specific principles can be said to be obligatory. In

essence, these principles established widely accepted features of proper corporate

governance. Firms call for 1 to explain their corporate governance exercises with

orientation to both the Principles as well as Provisions. The principles include

conduct of affairs by the board, composition as well as guidance by the committee,

Financial Reporting Council. The study on analysis of level and degree of corporate

governance in firms operating in retail segment in Singapore can help in

understanding method of governing firms, instating, laws, and customs along with

strategies. The study at hand aids in understanding the study of corporate

governance in the area of Singapore based on latest code of corporate governance.

This study helps in understanding the practices stipulated under the latest codes

under corporate governance laws. Essentially, this study helps in understanding the

code implementing 15 principles, complemented by guidelines related to board

matters, remuneration matters, accountability and executive remuneration (Tricker

and Tricker 2015). This needs to be facilitated by nomination as well as

remuneration committee for overseeing different matters. Particularly, this study also

explains importance of accountability and audit, and requires institution of audit

committees and internal audit function as a significant aspect of corporate

governance as per latest codes. In addition to this, this study also helps in

understanding significance of strong internal control procedures in place and this

promotes greater disclosure for and communicates with different shareholders

(McCaheryet al. 2016). Therefore, the current research paper discusses current

developments along with future trends in the region of corporate governance-CG in

the region of Singapore.

This account of the Code has at its heart Principles of CG-corporate

governance. Conformity with specific principles can be said to be obligatory. In

essence, these principles established widely accepted features of proper corporate

governance. Firms call for 1 to explain their corporate governance exercises with

orientation to both the Principles as well as Provisions. The principles include

conduct of affairs by the board, composition as well as guidance by the committee,

12CORPORATE GOVERNANCE IN RETAIL SEGMENT IN SINGAPORE Appendix

clear separation of responsibilities between Board and firm’s, Management,

membership of the firm’s board, performance of the board, matters of remuneration,

level of remuneration, remuneration revelations and many others.

2.4 Prior Studies on corporate governance

There have been numerous studies that have been prepared on the subject

matter of corporate governance. In itself, corporate governance-CG can be

considered to be one of the most important topics taken into consideration by firms.

The companies in Singapore have been taking actions and steps with the help of

which they have been able to manage their companies in an effective manner

(McCahery et al. 2016).

There have been several meta-analyses that have been done on this topic

and in this manner proper and effective governance has been maintained. It is seen

that corporate governance has been very much influential in USA, where all the

companies have their corporate governance plans with the help of which strengths

and weaknesses of the companies are understood. The corporate governance plans

are constructed on an annual basis and accordingly plans and processes are

prepared and are reviewed accordingly (Davies 2016). There are countries like India

and China that have even incorporated this plan with the help of which better

understanding of the operations of the company can be understood. This process is

even helpful in having an understanding of the relationship among the stakeholders

and in this manner enhance functional activities are executed. The developing

countries like India and Korea have been influencing this process and thereby all the

companies have been making use of the same (Azeez 2015). Therefore, it can

hereby be ascertained that corporate governance-CG has an important role in the

process of development of the companies and hence the organizations in Singapore

clear separation of responsibilities between Board and firm’s, Management,

membership of the firm’s board, performance of the board, matters of remuneration,

level of remuneration, remuneration revelations and many others.

2.4 Prior Studies on corporate governance

There have been numerous studies that have been prepared on the subject

matter of corporate governance. In itself, corporate governance-CG can be

considered to be one of the most important topics taken into consideration by firms.

The companies in Singapore have been taking actions and steps with the help of

which they have been able to manage their companies in an effective manner

(McCahery et al. 2016).

There have been several meta-analyses that have been done on this topic

and in this manner proper and effective governance has been maintained. It is seen

that corporate governance has been very much influential in USA, where all the

companies have their corporate governance plans with the help of which strengths

and weaknesses of the companies are understood. The corporate governance plans

are constructed on an annual basis and accordingly plans and processes are

prepared and are reviewed accordingly (Davies 2016). There are countries like India

and China that have even incorporated this plan with the help of which better

understanding of the operations of the company can be understood. This process is

even helpful in having an understanding of the relationship among the stakeholders

and in this manner enhance functional activities are executed. The developing

countries like India and Korea have been influencing this process and thereby all the

companies have been making use of the same (Azeez 2015). Therefore, it can

hereby be ascertained that corporate governance-CG has an important role in the

process of development of the companies and hence the organizations in Singapore

13CORPORATE GOVERNANCE IN RETAIL SEGMENT IN SINGAPORE Appendix

have been looking forward to incorporate the same. There have been limited studies

on this topic in Singapore and therefore it has become pertinent to undertake a

research on this topic for this country (Larcker and Tayan 2015).

Boards mainly comprise of executives as well as non-executive directors. In

particular, executive directors indicate towards dependent directors together with

non-executive ones together with independent directors. In any case one-third (1/3)

of different independent directors are necessarily favoured in firms’ board, for

effectual operation of board and for the purpose of unbiased tracking (Dalwai et al.

2015). Again, dependent directors are necessarily vital as they possess insider

familiarity regarding the firm that is not available to diverse external directors.

Nevertheless, they can exploit vital knowledge by shuffling wealth of corporations’

stockholders. In essence, a board comprised of different members who are

necessarily not executives of a firm or investors (Schmidt and Fahlenbrach 2017).

As suggested by Admati (2017), self-governing board normally comprises of

different members that possess no ties to the corporation in any manner. As a result

there remains no or least possibility of engaging in a disagreement/clash of interest

as autonomous directors possess no material welfare in an enterprise. Dignam and

Galanis (2016) state that self-governing directors are indispensable as

internal/dependent directors might perhaps get no admittance to external

information.

Whincop (2017) mentioned the fact that the possibility that large sized boards

can prove to be less effectual than small sized boards. At the time when boards are

made up of numerous members, then agency issues might possibly enhance, since

some directors might probably label along as free-rider. Also, they also disputed that

have been looking forward to incorporate the same. There have been limited studies

on this topic in Singapore and therefore it has become pertinent to undertake a

research on this topic for this country (Larcker and Tayan 2015).

Boards mainly comprise of executives as well as non-executive directors. In

particular, executive directors indicate towards dependent directors together with

non-executive ones together with independent directors. In any case one-third (1/3)

of different independent directors are necessarily favoured in firms’ board, for

effectual operation of board and for the purpose of unbiased tracking (Dalwai et al.

2015). Again, dependent directors are necessarily vital as they possess insider

familiarity regarding the firm that is not available to diverse external directors.

Nevertheless, they can exploit vital knowledge by shuffling wealth of corporations’

stockholders. In essence, a board comprised of different members who are

necessarily not executives of a firm or investors (Schmidt and Fahlenbrach 2017).

As suggested by Admati (2017), self-governing board normally comprises of

different members that possess no ties to the corporation in any manner. As a result

there remains no or least possibility of engaging in a disagreement/clash of interest

as autonomous directors possess no material welfare in an enterprise. Dignam and

Galanis (2016) state that self-governing directors are indispensable as

internal/dependent directors might perhaps get no admittance to external

information.

Whincop (2017) mentioned the fact that the possibility that large sized boards

can prove to be less effectual than small sized boards. At the time when boards are

made up of numerous members, then agency issues might possibly enhance, since

some directors might probably label along as free-rider. Also, they also disputed that

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

14CORPORATE GOVERNANCE IN RETAIL SEGMENT IN SINGAPORE Appendix

at the time when size of the board becomes extremely big, and then it undertakes a

more symbolic role and fulfils intended operations as part of the administration.

Conversely, extremely small sized boards require benefit of possessing the spread

of specialist advice and outlook around the specific table that is observed in large

sized boards (Darrat et al. 2016). Additionally, large boards have greater propensity

to be linked to an augmentation in diversity of board as to knowledge, expertise,

gender as well as nationality. Taking away off wealth by chief executive officers or

else inside directors is reasonably easier with small sized boards as small sized

boards are also connected to a smaller figure of external directors. Essentially, the

fewer number of directors in particularly small sized boards are engaged with

decision making procedure, leaving fewer time for tracking actions (Christensen et

al. 2015).

Lins et al. (2017) mentioned the fact that corporations having small sized

boards (minimum 5 members of the board) are more informed regarding earnings of

the corporation and therefore can be concerned to be having superior tracking

capabilities. Founded on findings of the study, Abdullah et al. (2016) mentioned that

valuations of listed corporations of Singapore and Malaysia are observed to be

highest at the time when members of the board comprise of 5 members. Arora and

Sharma (2016) mentioned that in evaluation of both small as well as medium sized

Danish corporations, it can be hereby observed that size of the board has no

influence on overall performance for particularly a board size that is below 6. Again,

there is seen to be a negative relationship between the two when board size rises to

7 or above. Dalwai et al. (2015) observed no solid evidence on linkage between

board size and level and degree of firm performance.

at the time when size of the board becomes extremely big, and then it undertakes a

more symbolic role and fulfils intended operations as part of the administration.

Conversely, extremely small sized boards require benefit of possessing the spread

of specialist advice and outlook around the specific table that is observed in large

sized boards (Darrat et al. 2016). Additionally, large boards have greater propensity

to be linked to an augmentation in diversity of board as to knowledge, expertise,

gender as well as nationality. Taking away off wealth by chief executive officers or

else inside directors is reasonably easier with small sized boards as small sized

boards are also connected to a smaller figure of external directors. Essentially, the

fewer number of directors in particularly small sized boards are engaged with

decision making procedure, leaving fewer time for tracking actions (Christensen et

al. 2015).

Lins et al. (2017) mentioned the fact that corporations having small sized

boards (minimum 5 members of the board) are more informed regarding earnings of

the corporation and therefore can be concerned to be having superior tracking

capabilities. Founded on findings of the study, Abdullah et al. (2016) mentioned that

valuations of listed corporations of Singapore and Malaysia are observed to be

highest at the time when members of the board comprise of 5 members. Arora and

Sharma (2016) mentioned that in evaluation of both small as well as medium sized

Danish corporations, it can be hereby observed that size of the board has no

influence on overall performance for particularly a board size that is below 6. Again,

there is seen to be a negative relationship between the two when board size rises to

7 or above. Dalwai et al. (2015) observed no solid evidence on linkage between

board size and level and degree of firm performance.

15CORPORATE GOVERNANCE IN RETAIL SEGMENT IN SINGAPORE Appendix

Comparison of impact of structure of board on performance of corporations

shows negative association for different Japanese corporation. This was enumerated

by market/book ratio as well as return earned on assets. However, no association

was observed between two different variables for particularly Australian counterpart.

Nevertheless, contrary to Japanese corporations, the ratios of different directors as

well as female directors to overall members of the board have a positive influence on

essentially the Australian section (Schmidt and Fahlenbrach 2017). At variance with

above mentioned findings, it can be found that there was a positive influence on

corporate performance with large sized boards. Assessment of 147 Singaporean

corporations from 1995 data reflects the fact structure of board is endogenously

ascertained when the outcomes of OLS reflect the board size, structure of headship

and size of enterprise have a positive control on performance of enterprises (Zabri et

al. 2016).

Mishra and Mohanty (2014) observed a direct positive linkage between board

size and firm performance (enumerated by the dimension of Tobin’s Q) in essentially

the U.S banking segment. Larcker and Tayan (2015) outcomes propose the fact that

this kind of performance association might possibly be industry specific, reflecting

the fact those large sized boards’ functions well for definite type of corporations

based on structures of business concerns. Essentially, a meta-analysis founded on

131 studies undertaken by Ferrero‐Ferrero et al. (2015) revealed that large sized

boards are related to higher performance of business enterprises.

Qiu et al. (2016) examined the Corporate Governance as well as firm

valuation by means of an index of Corporate Governance and supplementary

variables associated to ownership arrangement, board features, along with leverage

to deliver a inclusive explanation of Corporate Governance at particularly level of

Comparison of impact of structure of board on performance of corporations

shows negative association for different Japanese corporation. This was enumerated

by market/book ratio as well as return earned on assets. However, no association

was observed between two different variables for particularly Australian counterpart.

Nevertheless, contrary to Japanese corporations, the ratios of different directors as

well as female directors to overall members of the board have a positive influence on

essentially the Australian section (Schmidt and Fahlenbrach 2017). At variance with

above mentioned findings, it can be found that there was a positive influence on

corporate performance with large sized boards. Assessment of 147 Singaporean

corporations from 1995 data reflects the fact structure of board is endogenously

ascertained when the outcomes of OLS reflect the board size, structure of headship

and size of enterprise have a positive control on performance of enterprises (Zabri et

al. 2016).

Mishra and Mohanty (2014) observed a direct positive linkage between board

size and firm performance (enumerated by the dimension of Tobin’s Q) in essentially

the U.S banking segment. Larcker and Tayan (2015) outcomes propose the fact that

this kind of performance association might possibly be industry specific, reflecting

the fact those large sized boards’ functions well for definite type of corporations

based on structures of business concerns. Essentially, a meta-analysis founded on

131 studies undertaken by Ferrero‐Ferrero et al. (2015) revealed that large sized

boards are related to higher performance of business enterprises.

Qiu et al. (2016) examined the Corporate Governance as well as firm

valuation by means of an index of Corporate Governance and supplementary

variables associated to ownership arrangement, board features, along with leverage

to deliver a inclusive explanation of Corporate Governance at particularly level of

16CORPORATE GOVERNANCE IN RETAIL SEGMENT IN SINGAPORE Appendix

firm. In essence, an enhancement in index of Corporate Governance by 1 point

generated an enhancement of market capitalization by approximately 8.6%. Larcker

and Tayan (2015) investigated the influence of Corporate Governance-CG on

performance on the whole by presenting a Corporate Governance-CG index. This

index replicates predicted productivity at firm level in the region of Ukraine. In

essence, the outcomes mean that a 1-point-enhancement in the index leads to

approximately 0.4%-1.9% enhancement in overall performance (Zabri et al. 2016).

Again, a most unpleasant to most excellent change forecasts a 40% enhancement in

performance of corporation. Data on firms in several African nations shows that

superior governance exercises are related to greater valuations and improved

operational performance.

2.4.1 Agency Theory

This specific theory is regarded as a principal role that assists in explaining

specific role of board directors on performance of corporations. This theory was

proposed by Steven Ross and Barry Mitnick and they created the theory in order to

provide better understanding of corporate governance.Armstrong et al.(2015)

assessed research study synthesizes the same into main regulation so as to explore

this association. With regard to agency theory, it can be hereby said that the

principal as well as agent can be considered as shareholders and firm’s directors.

Essentially, their theory reflected the fact that there exists an irregularity between the

advantages of owners and managers founded on attributes of four features as

illustrated legalistic standpoint. With the help of agency theory the actions and the

interests of all the groups can be known and thereby better understanding of their

actions can be known. With the help of this theory the functioning and the activities

firm. In essence, an enhancement in index of Corporate Governance by 1 point

generated an enhancement of market capitalization by approximately 8.6%. Larcker

and Tayan (2015) investigated the influence of Corporate Governance-CG on

performance on the whole by presenting a Corporate Governance-CG index. This

index replicates predicted productivity at firm level in the region of Ukraine. In

essence, the outcomes mean that a 1-point-enhancement in the index leads to

approximately 0.4%-1.9% enhancement in overall performance (Zabri et al. 2016).

Again, a most unpleasant to most excellent change forecasts a 40% enhancement in

performance of corporation. Data on firms in several African nations shows that

superior governance exercises are related to greater valuations and improved

operational performance.

2.4.1 Agency Theory

This specific theory is regarded as a principal role that assists in explaining

specific role of board directors on performance of corporations. This theory was

proposed by Steven Ross and Barry Mitnick and they created the theory in order to

provide better understanding of corporate governance.Armstrong et al.(2015)

assessed research study synthesizes the same into main regulation so as to explore

this association. With regard to agency theory, it can be hereby said that the

principal as well as agent can be considered as shareholders and firm’s directors.

Essentially, their theory reflected the fact that there exists an irregularity between the

advantages of owners and managers founded on attributes of four features as

illustrated legalistic standpoint. With the help of agency theory the actions and the

interests of all the groups can be known and thereby better understanding of their

actions can be known. With the help of this theory the functioning and the activities

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

17CORPORATE GOVERNANCE IN RETAIL SEGMENT IN SINGAPORE Appendix

of the stakeholders can be known and thereby better steps and actions can be

undertaken.

2.4.2 Stewardship Theory

Contrary to agency theory and its premises, Mishra and Mohanty (2014)

assessed the novel approach to the association between the advantage of

shareholders as well as managers that is developed founded on psychological along

with sociological notions. This theory was proposed by Donaldson and Davis and

this was created to have an understanding about the relationship among the

management and the owners of the company. This understanding is significant in

order to operate an organization in an effective manner. Essentially, the interests of

different individuals and business concerns are mixed and managers operate firms

to make best use of utility (Larcker and Tayan2015).

This theory is very popular as it helps in determining the factors that have an

effect on the relationship among the owners and the management. With the help of

this theory, various plans and processes can be constructed with the help of which

better performance of the companies can be attained and efficient operational

activities can be ascertained.

S/NO. Authors Year Country Sample Size

1 McNulty, T., Zattoni, A.

and Douglas, T.,

2013 USA 20

2 Siebels, J.F. and

zuKnyphausen‐Aufseß

2012 Russia 26

3 Wintoki, M.B., Linck, J.S.

and Netter

2012 NA NA

of the stakeholders can be known and thereby better steps and actions can be

undertaken.

2.4.2 Stewardship Theory

Contrary to agency theory and its premises, Mishra and Mohanty (2014)

assessed the novel approach to the association between the advantage of

shareholders as well as managers that is developed founded on psychological along

with sociological notions. This theory was proposed by Donaldson and Davis and

this was created to have an understanding about the relationship among the

management and the owners of the company. This understanding is significant in

order to operate an organization in an effective manner. Essentially, the interests of

different individuals and business concerns are mixed and managers operate firms

to make best use of utility (Larcker and Tayan2015).

This theory is very popular as it helps in determining the factors that have an

effect on the relationship among the owners and the management. With the help of

this theory, various plans and processes can be constructed with the help of which

better performance of the companies can be attained and efficient operational

activities can be ascertained.

S/NO. Authors Year Country Sample Size

1 McNulty, T., Zattoni, A.

and Douglas, T.,

2013 USA 20

2 Siebels, J.F. and

zuKnyphausen‐Aufseß

2012 Russia 26

3 Wintoki, M.B., Linck, J.S.

and Netter

2012 NA NA

18CORPORATE GOVERNANCE IN RETAIL SEGMENT IN SINGAPORE Appendix

4 Filatotchev, I., Jackson,

G. and Nakajima

2013 NA 12

5 Aguinis, H. and Glavas 2012 NA NA

2.5 Synopsis of the Literature

The review of literature has delivered ideas and concepts about corporate

governance. This section has addressed all the key areas that are related to

corporate governance-CG codes. Various themes that are related to corporate

governance-CG have even been addressed with the help of which an idea is

obtained that will be helpful in undertaking the data analysis process.

4 Filatotchev, I., Jackson,

G. and Nakajima

2013 NA 12

5 Aguinis, H. and Glavas 2012 NA NA

2.5 Synopsis of the Literature

The review of literature has delivered ideas and concepts about corporate

governance. This section has addressed all the key areas that are related to

corporate governance-CG codes. Various themes that are related to corporate

governance-CG have even been addressed with the help of which an idea is

obtained that will be helpful in undertaking the data analysis process.

19CORPORATE GOVERNANCE IN RETAIL SEGMENT IN SINGAPORE Appendix

Chapter 3

Methodology of Research Study

3.1 Introduction

The current segment explains in detail the context of the research that

illustrates in detail the background setting of the study. This section on research

context gives details regarding retail industry in the Singapore market and the two

forms of the Singapore stock exchange. Thereafter, this segment explains about

implementation of quantitative analysis of secondary data with justification. Moving

further, this section throws light on data collection, data sources, sample details,

sampling techniques and explicates data analysis and techniques of interpretation.

This paper has selected retail companies mainly due to the fact that the retail

companies in Singapore are more and they have been the ones that have been

operating in an effective manner. It is due to this fact that retail companies have

been selected.

3.2 Research Context

The retail market of Singapore is anticipated to stay demanding and difficult

for both landlords as well as retailers in the midst of indecisive market outlook, feeble

retail spending, increasing business cost along with shortage of manpower.

Essentially, retail rents are liable to encounter downward load for the year 2017

since demand remained flexible with forthcoming insertion of novel retail space

(Dumay and Cai 2015). Also, landlords as well as merchants have the need to drive

superior innovation in particular business stratagems to find the way out of the hard-

hitting retail climate. Founded on bi-yearly Consumer Confidence Index, index of

Singapore witnessed further decrease by around 3.6 points to approximately 30.0 in

Chapter 3

Methodology of Research Study

3.1 Introduction

The current segment explains in detail the context of the research that

illustrates in detail the background setting of the study. This section on research

context gives details regarding retail industry in the Singapore market and the two

forms of the Singapore stock exchange. Thereafter, this segment explains about

implementation of quantitative analysis of secondary data with justification. Moving

further, this section throws light on data collection, data sources, sample details,

sampling techniques and explicates data analysis and techniques of interpretation.

This paper has selected retail companies mainly due to the fact that the retail

companies in Singapore are more and they have been the ones that have been

operating in an effective manner. It is due to this fact that retail companies have

been selected.

3.2 Research Context

The retail market of Singapore is anticipated to stay demanding and difficult

for both landlords as well as retailers in the midst of indecisive market outlook, feeble

retail spending, increasing business cost along with shortage of manpower.

Essentially, retail rents are liable to encounter downward load for the year 2017

since demand remained flexible with forthcoming insertion of novel retail space

(Dumay and Cai 2015). Also, landlords as well as merchants have the need to drive

superior innovation in particular business stratagems to find the way out of the hard-

hitting retail climate. Founded on bi-yearly Consumer Confidence Index, index of

Singapore witnessed further decrease by around 3.6 points to approximately 30.0 in

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

20CORPORATE GOVERNANCE IN RETAIL SEGMENT IN SINGAPORE Appendix

H2 in the period 2016 as compared to H1 in the period 2016. Essentially, Retail

Sales Index (not including motor vehicles as well as non- adjusted ones, essentially

at stable prices) decreased by around 4.6% year-after-year during the period 2017

(Schmidt and Fahlenbrach 2017).

The enterprises listed on Singapore stock exchange (SGX) are categorised

into two different clusters: the firms listed on Singapore stock exchange (SGX) Main

board and the firms listed on essentially SGX Catalyst.

3.3 Research Method

The researcher has utilized quantitative analysis of secondary data on

corporate governance for 30 different firms. Selection of this specific technique can

be said to be justified in this case as this is a viable option for the learner facing

constraints of limited time as well as resources. The process will look to assess the

various corporate governance indexes that are within corporate governance. In this

manner, the various aspects of corporate governance like auditing, structure and

process of management and the board can be understood (Taylor et al. 2015).

Compliance of the companies and corporate responsibility along with the financial

transparency of the companies and information disclosure is very important (Schmidt

and Fahlenbrach 2017). The ownership structure as the exercise of the control rights

will be taken into consideration with the help of which proper actions and analysis

can be undertaken. Therefore quantitative analysis would be done with the help of

the corporate governance index.

H2 in the period 2016 as compared to H1 in the period 2016. Essentially, Retail

Sales Index (not including motor vehicles as well as non- adjusted ones, essentially

at stable prices) decreased by around 4.6% year-after-year during the period 2017

(Schmidt and Fahlenbrach 2017).

The enterprises listed on Singapore stock exchange (SGX) are categorised

into two different clusters: the firms listed on Singapore stock exchange (SGX) Main

board and the firms listed on essentially SGX Catalyst.

3.3 Research Method

The researcher has utilized quantitative analysis of secondary data on

corporate governance for 30 different firms. Selection of this specific technique can

be said to be justified in this case as this is a viable option for the learner facing

constraints of limited time as well as resources. The process will look to assess the

various corporate governance indexes that are within corporate governance. In this

manner, the various aspects of corporate governance like auditing, structure and

process of management and the board can be understood (Taylor et al. 2015).

Compliance of the companies and corporate responsibility along with the financial

transparency of the companies and information disclosure is very important (Schmidt

and Fahlenbrach 2017). The ownership structure as the exercise of the control rights

will be taken into consideration with the help of which proper actions and analysis

can be undertaken. Therefore quantitative analysis would be done with the help of

the corporate governance index.

21CORPORATE GOVERNANCE IN RETAIL SEGMENT IN SINGAPORE Appendix

3.4 Data Analysis

Data

The current study utilizes secondary data for undertaking the current study.

The MAS and the data in relation to 30 companies have been collected from the

SGX websites and online resources and many other sources are taken into account

for acquirement of secondary data. Also, corporate governance code is taken into

consideration. Essentially, the code of corporate governance from yearly report of

the firm is taken into consideration (Lewis 2015). The corporate governance codes

examination refers to examination of annual reports of the firm where there is need

to check compliance of companies to different codes of CG. Essentially, higher

match implies degree of compliance of the firm (Dalwai et al. 2015). Therefore, there

is need to find data from annual reports of chosen companies. The CG Code along

with amended the CG Index need to be reviewed in this regard.

Sample

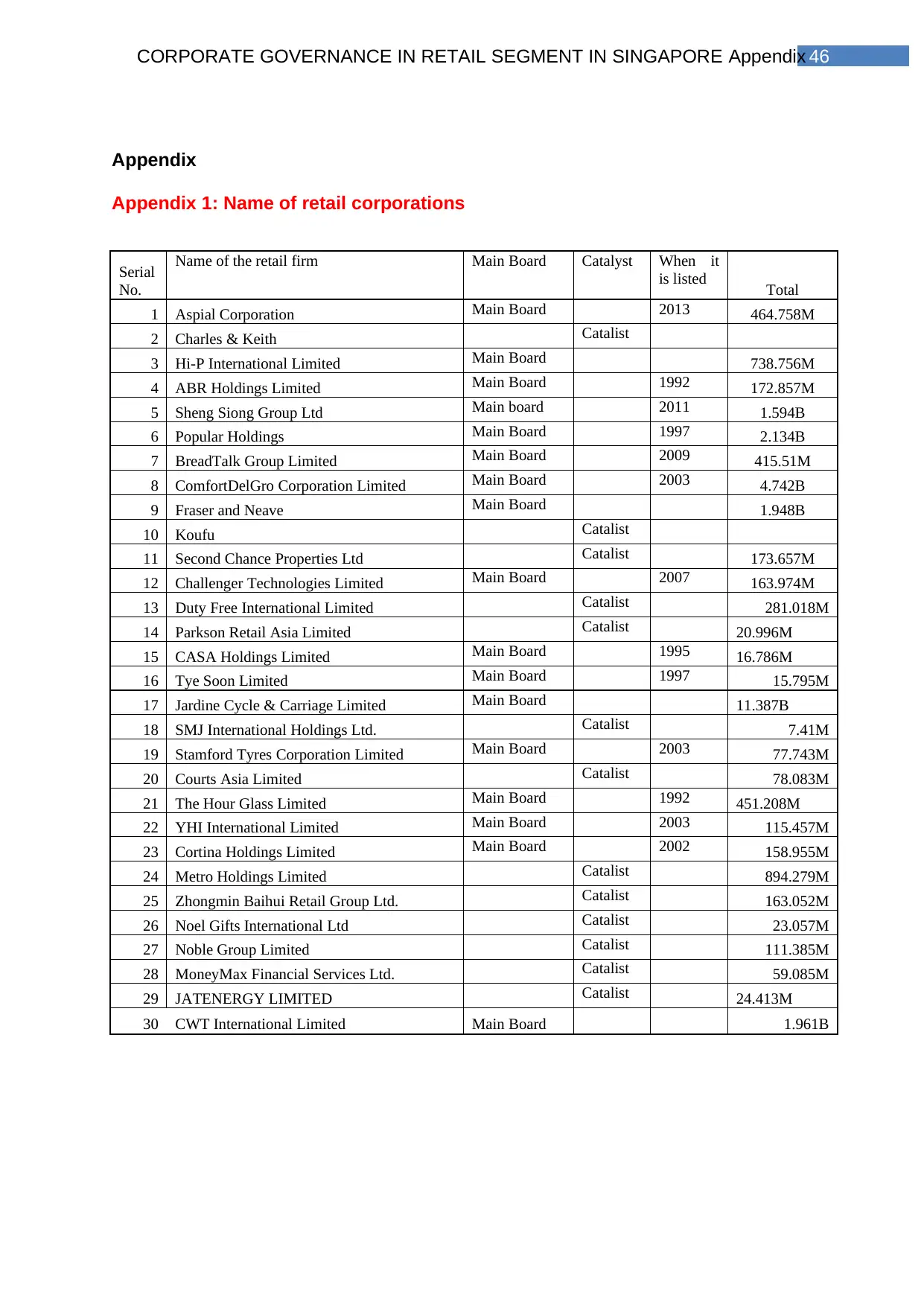

The current study uses data of 30 companies operating in the retail segment

in Singapore that necessarily use quantitative data and need to be a listed firm. In

addition to this, the study also refers to specific case studies that deal with the

current subject matter under deliberation. The 30 companies have been selected

from a total of 45 companies that were shortlisted earlier.

Sampling

The 30 different firms operating in the retail segment of the nation

Singapore are selected for the current study under consideration. The learner

has selected the sample using non-probabilistic sampling where the samples do not

3.4 Data Analysis

Data

The current study utilizes secondary data for undertaking the current study.

The MAS and the data in relation to 30 companies have been collected from the

SGX websites and online resources and many other sources are taken into account

for acquirement of secondary data. Also, corporate governance code is taken into

consideration. Essentially, the code of corporate governance from yearly report of

the firm is taken into consideration (Lewis 2015). The corporate governance codes

examination refers to examination of annual reports of the firm where there is need

to check compliance of companies to different codes of CG. Essentially, higher

match implies degree of compliance of the firm (Dalwai et al. 2015). Therefore, there

is need to find data from annual reports of chosen companies. The CG Code along

with amended the CG Index need to be reviewed in this regard.

Sample

The current study uses data of 30 companies operating in the retail segment

in Singapore that necessarily use quantitative data and need to be a listed firm. In

addition to this, the study also refers to specific case studies that deal with the

current subject matter under deliberation. The 30 companies have been selected

from a total of 45 companies that were shortlisted earlier.

Sampling

The 30 different firms operating in the retail segment of the nation

Singapore are selected for the current study under consideration. The learner

has selected the sample using non-probabilistic sampling where the samples do not

22CORPORATE GOVERNANCE IN RETAIL SEGMENT IN SINGAPORE Appendix

have equal probability of being selected. The 30 listed retail firms are chosen by the

learner based in their own judgement and are tested for maintenance of corporate

governance. For that reason, the reports and declarations particularly on corporate

governance of the firm are analysed to examine their match. Also, review of prior

literature presented by scholars is carried out. The primary themes are analytically

examined.

Data Analysis and Interpretation

Quantitative analysis of acquired secondary data for the study uses thematic

analysis as well as content analysis. Again, conversely, corporate governance-CG

codes of the enterprises scrutinized and matched is necessarily applied rates and

points that can quantify the points acquired by firm (Dalwai et al. 2015). Thereafter,

the total found out for each of the firms can be ranked from particularly highest to

essentially the lowest score (refer to appendix). The total scores for each of the

company are presented and the same are ranked starting from the highest to the

lowest rank as per scores (Flick 2015). The minimum as well as maximum score

based on ranks are presented. Moving further, the learner implement the statistical

technique of standard deviation utilizing Microsoft excel software.

3.5 Summary

The current study uses both the methods of quantitative analysis of secondary

data. The cases of 30 different enterprises listed in the Singapore Stock Exchange

are selected for present evaluation. Corporate governance-CG codes of the

enterprises are necessarily assessed and total scores are presented for the nine

different areas of governance. Statistical techniques are applied for analysing overall

have equal probability of being selected. The 30 listed retail firms are chosen by the

learner based in their own judgement and are tested for maintenance of corporate

governance. For that reason, the reports and declarations particularly on corporate

governance of the firm are analysed to examine their match. Also, review of prior

literature presented by scholars is carried out. The primary themes are analytically

examined.

Data Analysis and Interpretation

Quantitative analysis of acquired secondary data for the study uses thematic

analysis as well as content analysis. Again, conversely, corporate governance-CG

codes of the enterprises scrutinized and matched is necessarily applied rates and

points that can quantify the points acquired by firm (Dalwai et al. 2015). Thereafter,

the total found out for each of the firms can be ranked from particularly highest to

essentially the lowest score (refer to appendix). The total scores for each of the

company are presented and the same are ranked starting from the highest to the

lowest rank as per scores (Flick 2015). The minimum as well as maximum score

based on ranks are presented. Moving further, the learner implement the statistical

technique of standard deviation utilizing Microsoft excel software.

3.5 Summary

The current study uses both the methods of quantitative analysis of secondary

data. The cases of 30 different enterprises listed in the Singapore Stock Exchange

are selected for present evaluation. Corporate governance-CG codes of the

enterprises are necessarily assessed and total scores are presented for the nine

different areas of governance. Statistical techniques are applied for analysing overall

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

23CORPORATE GOVERNANCE IN RETAIL SEGMENT IN SINGAPORE Appendix

level of corporate governance and differences reflected from the financial

performance (financial performance analysed using ROA and ROE) of the firm.

level of corporate governance and differences reflected from the financial

performance (financial performance analysed using ROA and ROE) of the firm.

24CORPORATE GOVERNANCE IN RETAIL SEGMENT IN SINGAPORE Appendix

Chapter 4

Findings of the study and Evaluation

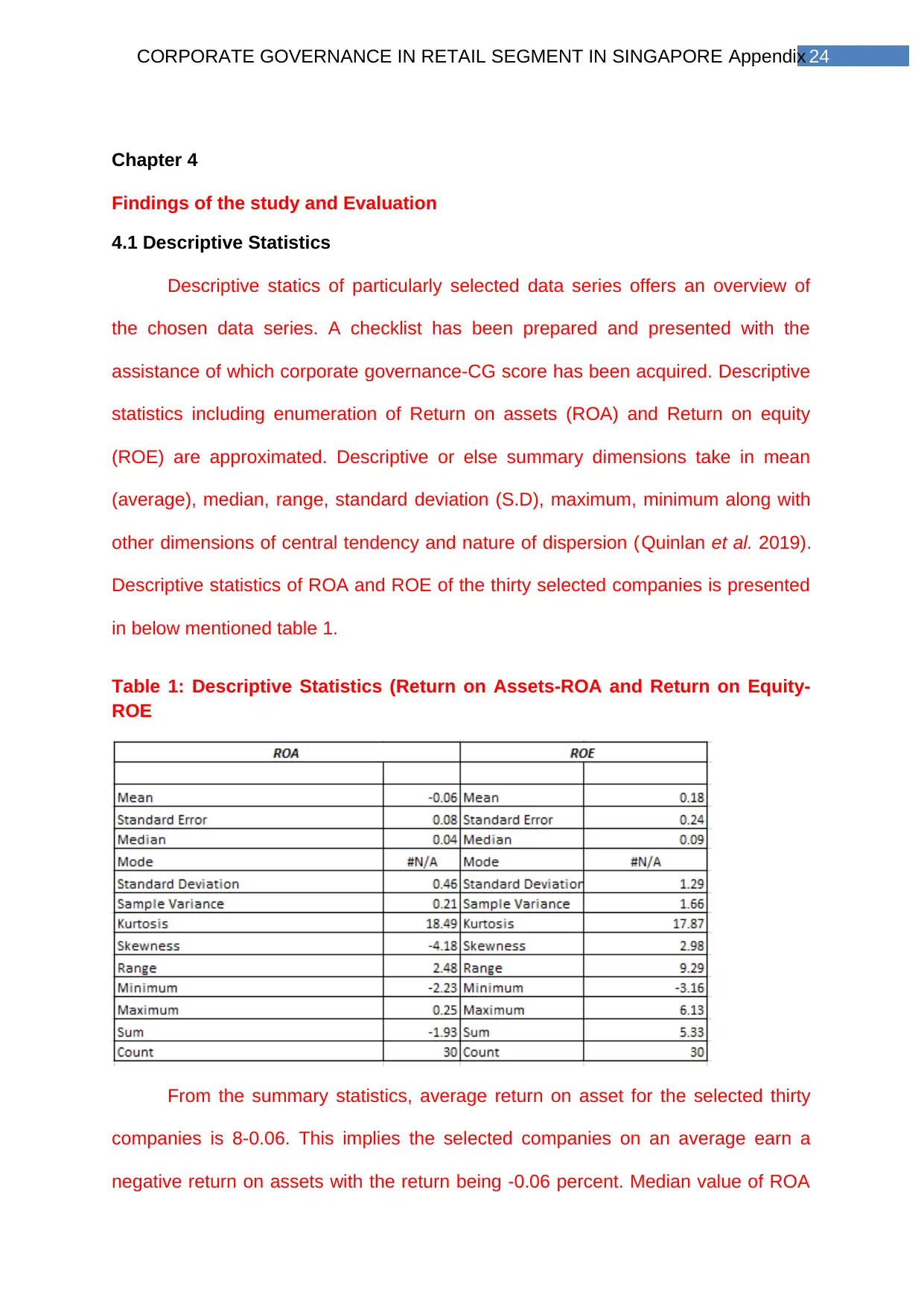

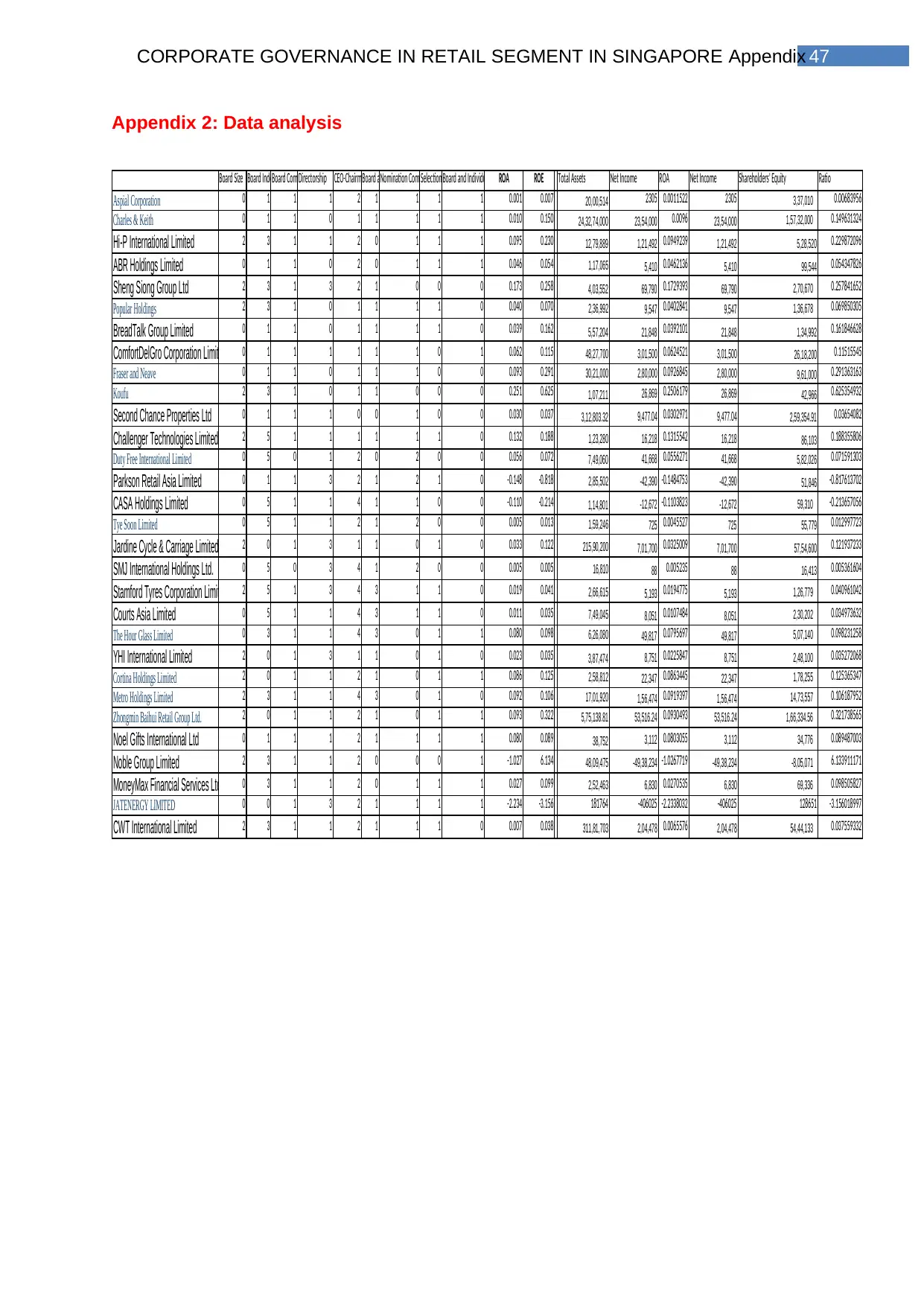

4.1 Descriptive Statistics

Descriptive statics of particularly selected data series offers an overview of

the chosen data series. A checklist has been prepared and presented with the

assistance of which corporate governance-CG score has been acquired. Descriptive

statistics including enumeration of Return on assets (ROA) and Return on equity

(ROE) are approximated. Descriptive or else summary dimensions take in mean

(average), median, range, standard deviation (S.D), maximum, minimum along with

other dimensions of central tendency and nature of dispersion (Quinlan et al. 2019).

Descriptive statistics of ROA and ROE of the thirty selected companies is presented

in below mentioned table 1.

Table 1: Descriptive Statistics (Return on Assets-ROA and Return on Equity-

ROE

From the summary statistics, average return on asset for the selected thirty

companies is 8-0.06. This implies the selected companies on an average earn a

negative return on assets with the return being -0.06 percent. Median value of ROA

Chapter 4

Findings of the study and Evaluation

4.1 Descriptive Statistics

Descriptive statics of particularly selected data series offers an overview of

the chosen data series. A checklist has been prepared and presented with the

assistance of which corporate governance-CG score has been acquired. Descriptive

statistics including enumeration of Return on assets (ROA) and Return on equity

(ROE) are approximated. Descriptive or else summary dimensions take in mean

(average), median, range, standard deviation (S.D), maximum, minimum along with

other dimensions of central tendency and nature of dispersion (Quinlan et al. 2019).

Descriptive statistics of ROA and ROE of the thirty selected companies is presented

in below mentioned table 1.

Table 1: Descriptive Statistics (Return on Assets-ROA and Return on Equity-

ROE

From the summary statistics, average return on asset for the selected thirty

companies is 8-0.06. This implies the selected companies on an average earn a

negative return on assets with the return being -0.06 percent. Median value of ROA

25CORPORATE GOVERNANCE IN RETAIL SEGMENT IN SINGAPORE Appendix

series is 0.04. That means half of the selected companies have a return on asset of

0.04 percent. Standard deviation of the return on asset series is 0.21. Standard

deviation of the series exceeds the mean return on. The high standard deviation

indicates return on asset is highly fluctuating for the companies. This is not a good

sign of financial position of the company and adversely affects confidence of the

investors (Choy 2014). The highest return on asset is 0.25. The return on assets is

observed for Koufu.

The average return on equity for the selected thirty companies is 0.18

percent. This implies the selected companies’ record an average earn an average

return of 0.18 percent on shareholder’s equity. Median value of ROE series is 0.09