Digital Disruption in Banking: Work Centered Analysis Case Study

VerifiedAdded on 2023/06/14

|14

|2951

|185

Case Study

AI Summary

This case study report examines the impact of digital disruption on the banking sector through a work-centered analysis (WCA). It begins by evaluating the banking system before digital disruption, focusing on customer interactions, products, business processes, participants, information flow, and technology used. A retrospective analysis highlights the manpower-intensive nature of traditional banking and its limitations. Subsequently, the report analyzes the banking system after digital disruption, noting changes in customer access, product delivery (online and offline), business processes (online and offline), information management, and technology adoption, including cloud storage and ATM systems. The analysis identifies advantages such as customer satisfaction, cost-effectiveness, improved resource utilization, enhanced security, and increased transparency. The report concludes by emphasizing the positive impact of digital disruption on the banking sector and its overall efficiency.

Running head: DIGITAL DISRUPTION IN THE BANKING SECTOR

DIGITAL DISRUPTION IN THE BANKING SECTOR

Name of the Student:

Name of the University:

Author Note:

DIGITAL DISRUPTION IN THE BANKING SECTOR

Name of the Student:

Name of the University:

Author Note:

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

1

DIGITAL DISRUPTION IN THE BANKING SECTOR

Executive Summery

The main aim of this paper is to discuss the impacts of the use of advanced technology in the

banking sector. The changes those are happened for the implementation of the digital technology

are called digital disruption. The effect of digital disruption is evaluated in a certain way in this

paper. At first the work centered analysis is evaluated before the digital disruption followed by a

retrospective analysis if the banking system. The work centered analysis is done after the digital

disruption and certain changes are noted. The comparison between the past and present scenario

is done in order to evaluate the advantages of the digital disruption in the banking sector. It can

be concluded from the study that the digital disruption is preferable for the banking sector.

DIGITAL DISRUPTION IN THE BANKING SECTOR

Executive Summery

The main aim of this paper is to discuss the impacts of the use of advanced technology in the

banking sector. The changes those are happened for the implementation of the digital technology

are called digital disruption. The effect of digital disruption is evaluated in a certain way in this

paper. At first the work centered analysis is evaluated before the digital disruption followed by a

retrospective analysis if the banking system. The work centered analysis is done after the digital

disruption and certain changes are noted. The comparison between the past and present scenario

is done in order to evaluate the advantages of the digital disruption in the banking sector. It can

be concluded from the study that the digital disruption is preferable for the banking sector.

2

DIGITAL DISRUPTION IN THE BANKING SECTOR

Table of Contents

List of Abbreviations and assumptions made:.................................................................................3

List of Assumptions made:..............................................................................................................3

Introduction......................................................................................................................................4

Discussion........................................................................................................................................4

Background and problem definition:...........................................................................................4

Work centered analysis:...............................................................................................................5

Work centered analysis of the bank before the digital disruption:..............................................5

Retrospective analysis of the banking system before the digital disruption:...............................7

Work centered analysis of the bank after the digital disruption:.................................................7

Analysis of the new process after the digital disruption:.............................................................9

Recommendations:......................................................................................................................9

Implementation of the recommended plans:..............................................................................10

Conclusion.....................................................................................................................................10

References......................................................................................................................................11

DIGITAL DISRUPTION IN THE BANKING SECTOR

Table of Contents

List of Abbreviations and assumptions made:.................................................................................3

List of Assumptions made:..............................................................................................................3

Introduction......................................................................................................................................4

Discussion........................................................................................................................................4

Background and problem definition:...........................................................................................4

Work centered analysis:...............................................................................................................5

Work centered analysis of the bank before the digital disruption:..............................................5

Retrospective analysis of the banking system before the digital disruption:...............................7

Work centered analysis of the bank after the digital disruption:.................................................7

Analysis of the new process after the digital disruption:.............................................................9

Recommendations:......................................................................................................................9

Implementation of the recommended plans:..............................................................................10

Conclusion.....................................................................................................................................10

References......................................................................................................................................11

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

3

DIGITAL DISRUPTION IN THE BANKING SECTOR

List of Abbreviations and assumptions made:

WCS- Work Centered Analysis

List of Assumptions made:

The impacts of the digital disruption in a company can be well explained with the help of

WCA. The component of WCA depends on certain factors. The WCA analysis indicates that the

implementation of the digitization can be beneficial for the company.

DIGITAL DISRUPTION IN THE BANKING SECTOR

List of Abbreviations and assumptions made:

WCS- Work Centered Analysis

List of Assumptions made:

The impacts of the digital disruption in a company can be well explained with the help of

WCA. The component of WCA depends on certain factors. The WCA analysis indicates that the

implementation of the digitization can be beneficial for the company.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

4

DIGITAL DISRUPTION IN THE BANKING SECTOR

Introduction

The advancement of technology has its impact on various sectors. The application of

technology is also considerable in case of banking sectors. The banks are aware of the changing

of the technology and are eager to adopt the new technology in order to make the services more

easily accessible to the users. It has been found out in a survey conducted by Nordea that the

increase of the uses availing the online and net banking facilities has grown up to 90% in 2014

(Oshodin et al. 2017). Figure shows that the demands of the users are changing. Using

technology in the banking sector has made the services like switching between banks, making

payment through bank easily available to the users in a cost and time effective way. The

application of the digital innovations in the banking sector has made the business more

competitive both for the technological companies and the banking organization (Curley and

Salmelin 2018). This study will discuss the certain impacts of digitization in the banking sectors

in order to do this, the impacts of the digital disruption in a particular bank is evaluated (Arnold

and Jeffery 2016). The comparison of the situation before the digital disruption in the bank and

the situation after the digital disruption in the bank is done in order to make the recommendation

and conclusion. In order to carry out the analysis more effectively, the work centered analysis is

done on the particular bank. The challenges and the advantages that the bank can phase due to

the digital innovation is also discussed in this study.

DIGITAL DISRUPTION IN THE BANKING SECTOR

Introduction

The advancement of technology has its impact on various sectors. The application of

technology is also considerable in case of banking sectors. The banks are aware of the changing

of the technology and are eager to adopt the new technology in order to make the services more

easily accessible to the users. It has been found out in a survey conducted by Nordea that the

increase of the uses availing the online and net banking facilities has grown up to 90% in 2014

(Oshodin et al. 2017). Figure shows that the demands of the users are changing. Using

technology in the banking sector has made the services like switching between banks, making

payment through bank easily available to the users in a cost and time effective way. The

application of the digital innovations in the banking sector has made the business more

competitive both for the technological companies and the banking organization (Curley and

Salmelin 2018). This study will discuss the certain impacts of digitization in the banking sectors

in order to do this, the impacts of the digital disruption in a particular bank is evaluated (Arnold

and Jeffery 2016). The comparison of the situation before the digital disruption in the bank and

the situation after the digital disruption in the bank is done in order to make the recommendation

and conclusion. In order to carry out the analysis more effectively, the work centered analysis is

done on the particular bank. The challenges and the advantages that the bank can phase due to

the digital innovation is also discussed in this study.

5

DIGITAL DISRUPTION IN THE BANKING SECTOR

Discussion

Background and problem definition:

The innovations of technologies and their implementation on the banking sectors are

bringing the significant change in the service systems of the banks. The use of technology in

different sections of service such as making payment and other bank account related services has

made the baking easier for the consumers (Lee 2015). These type services are known as net

banking or e-services provided by the bank. These services are cost effective in nature, for both

the consumer and the banking organization. Using technology is also making the service to be

served accurately and taking the small time span.

Work centered analysis:

There are six fundamental elements in the work process analysis.

Customer

Product

Business Process

Participants

Information

Technology

Work centered analysis of the bank before the digital disruption:

Customer: Customers used to withdraw or deposit the money to the bank account. The

process is done manually. The customer had to go to the bank and had to fulfill certain

formalities for these services.

DIGITAL DISRUPTION IN THE BANKING SECTOR

Discussion

Background and problem definition:

The innovations of technologies and their implementation on the banking sectors are

bringing the significant change in the service systems of the banks. The use of technology in

different sections of service such as making payment and other bank account related services has

made the baking easier for the consumers (Lee 2015). These type services are known as net

banking or e-services provided by the bank. These services are cost effective in nature, for both

the consumer and the banking organization. Using technology is also making the service to be

served accurately and taking the small time span.

Work centered analysis:

There are six fundamental elements in the work process analysis.

Customer

Product

Business Process

Participants

Information

Technology

Work centered analysis of the bank before the digital disruption:

Customer: Customers used to withdraw or deposit the money to the bank account. The

process is done manually. The customer had to go to the bank and had to fulfill certain

formalities for these services.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

6

DIGITAL DISRUPTION IN THE BANKING SECTOR

Product: The bank checks all the fields in the forms submitted by the customers and

proceed according to the requirements of the consumers. The consumer can get the services after

the verification and transaction process.

Business Process: Major activities of the bank:

Handling and managing the consumer’s account.

Doing the transaction.

Deposition of cash.

Update the balance of the account.

Closing of the customer’s account.

Printing of confirmation.

Opening the new bank account for the new customer.

Participants: The participants in the whole business process are the customers of the bank

and the employees of the bank. The services were demanded by the consumers and the

employees did the proceeding according to the demand of the customer (Ibegbulem and

Andersson 2017). The whole process did not stand in the absence of any one participant.

Information: During the course of the business process, exchanging of information did

happen in a large scale. The information is sensitive in nature ads it holds the personal details

along with the account information of the consumers.

Technology used by the bank: There was little use of technology in the process. The

requests for services, made by the customers were initially processed by the bank employees in a

manual way. The use of technology did used for doing certain things like maintaining the record

of the accounts of the consumer along with the customer database, checking the amount of

DIGITAL DISRUPTION IN THE BANKING SECTOR

Product: The bank checks all the fields in the forms submitted by the customers and

proceed according to the requirements of the consumers. The consumer can get the services after

the verification and transaction process.

Business Process: Major activities of the bank:

Handling and managing the consumer’s account.

Doing the transaction.

Deposition of cash.

Update the balance of the account.

Closing of the customer’s account.

Printing of confirmation.

Opening the new bank account for the new customer.

Participants: The participants in the whole business process are the customers of the bank

and the employees of the bank. The services were demanded by the consumers and the

employees did the proceeding according to the demand of the customer (Ibegbulem and

Andersson 2017). The whole process did not stand in the absence of any one participant.

Information: During the course of the business process, exchanging of information did

happen in a large scale. The information is sensitive in nature ads it holds the personal details

along with the account information of the consumers.

Technology used by the bank: There was little use of technology in the process. The

requests for services, made by the customers were initially processed by the bank employees in a

manual way. The use of technology did used for doing certain things like maintaining the record

of the accounts of the consumer along with the customer database, checking the amount of

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

7

DIGITAL DISRUPTION IN THE BANKING SECTOR

balance in particular account and counting the currency (Walker 2014). The storage was mainly

server based storage.

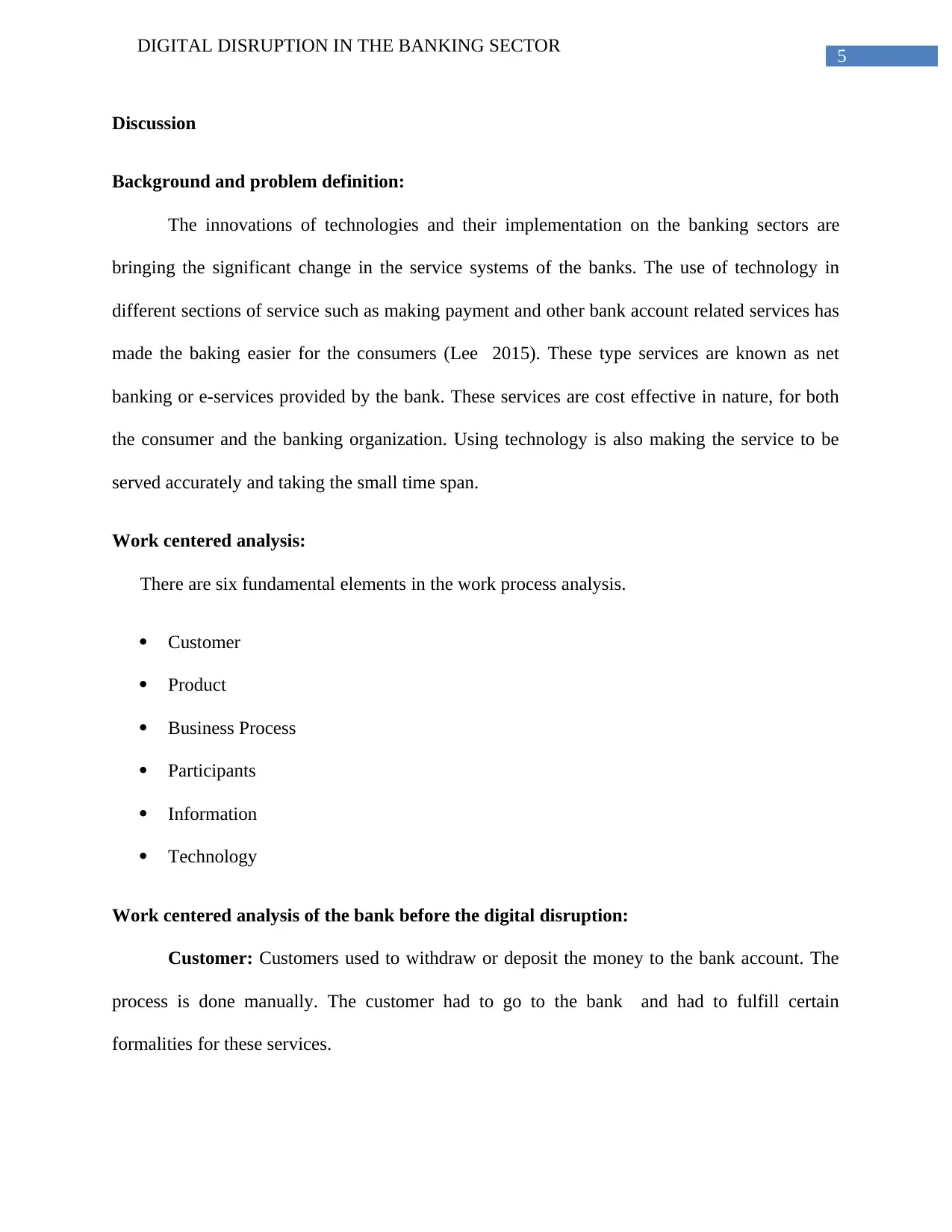

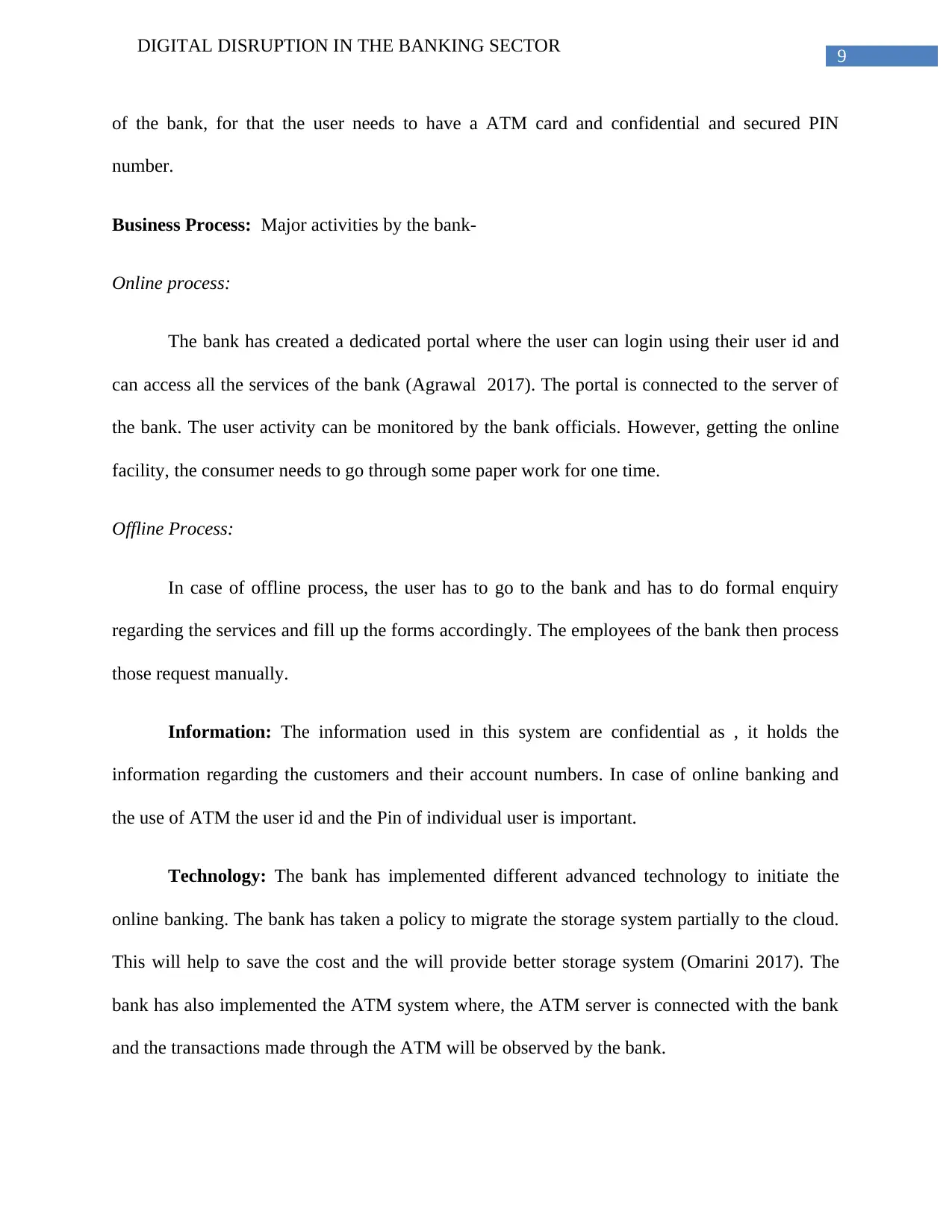

Figure 1: WCS before digital disruption.

(Source: Created by author)

Cu stome r(Cl

ien ts of the

bank)

Pr odu ct (M anu al

pr oces s ing of t he

s erv ices )

B u sin e ss P ro ce ss(All

th e s erv ic e sp r ovi d e d

b y re tail b a nk in g

in clu ding -ca sh

wi th d raw, cas h

d ep o siti on )

Participants:

Clients of

Information:

Users account

information

Technology:

Manual

DIGITAL DISRUPTION IN THE BANKING SECTOR

balance in particular account and counting the currency (Walker 2014). The storage was mainly

server based storage.

Figure 1: WCS before digital disruption.

(Source: Created by author)

Cu stome r(Cl

ien ts of the

bank)

Pr odu ct (M anu al

pr oces s ing of t he

s erv ices )

B u sin e ss P ro ce ss(All

th e s erv ic e sp r ovi d e d

b y re tail b a nk in g

in clu ding -ca sh

wi th d raw, cas h

d ep o siti on )

Participants:

Clients of

Information:

Users account

information

Technology:

Manual

8

DIGITAL DISRUPTION IN THE BANKING SECTOR

Retrospective analysis of the banking system before the digital disruption:

The banking system before the digital disruption was heavily based on the manpower.

The processing of the forms submitted by the consumers for availing the service was processed

manually by the employees of the bank. There was a chance that a mistake may occur during the

course of verification. It has been found that such mistakes did happen and it had a large impact

on both the account holder and the bank. The processing was based on the manpower, so, it used

to take much time to process. Thee consumers had to go to the bank for availing the service,

which could sometimes become impossible for them (Dermine 2017). The whole system was

doing well but there were lots of scope for the improvement of the banking system (Tornjanski et

al. 2015). At that time the main challenge for the bank was to introduce a error free service to the

consumers and easy detection of the frauds.

Work centered analysis of the bank after the digital disruption:

Customers: The customers deposit, withdrawals the money from the bank. The

consumers can avail these services after going to the bank or they can avail the service through

the internet. All services are available through internet, so that the consumers of the bank can

avail services without going to the bank.

Products: The products or the services are made available in both online and offline

mode. In case of the offline service the consumer has to go to the bank and avail the services in

conventional way. In order to avail the services online, the consumer has to access the portal of

the bank through internet. The user has to give the right information including the bank account

number and the user id number in the portal to avail the services (Bughin 2017). The bank has

implemented another way for withdrawal of the cash. The money can be drawn using the ATM

DIGITAL DISRUPTION IN THE BANKING SECTOR

Retrospective analysis of the banking system before the digital disruption:

The banking system before the digital disruption was heavily based on the manpower.

The processing of the forms submitted by the consumers for availing the service was processed

manually by the employees of the bank. There was a chance that a mistake may occur during the

course of verification. It has been found that such mistakes did happen and it had a large impact

on both the account holder and the bank. The processing was based on the manpower, so, it used

to take much time to process. Thee consumers had to go to the bank for availing the service,

which could sometimes become impossible for them (Dermine 2017). The whole system was

doing well but there were lots of scope for the improvement of the banking system (Tornjanski et

al. 2015). At that time the main challenge for the bank was to introduce a error free service to the

consumers and easy detection of the frauds.

Work centered analysis of the bank after the digital disruption:

Customers: The customers deposit, withdrawals the money from the bank. The

consumers can avail these services after going to the bank or they can avail the service through

the internet. All services are available through internet, so that the consumers of the bank can

avail services without going to the bank.

Products: The products or the services are made available in both online and offline

mode. In case of the offline service the consumer has to go to the bank and avail the services in

conventional way. In order to avail the services online, the consumer has to access the portal of

the bank through internet. The user has to give the right information including the bank account

number and the user id number in the portal to avail the services (Bughin 2017). The bank has

implemented another way for withdrawal of the cash. The money can be drawn using the ATM

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

9

DIGITAL DISRUPTION IN THE BANKING SECTOR

of the bank, for that the user needs to have a ATM card and confidential and secured PIN

number.

Business Process: Major activities by the bank-

Online process:

The bank has created a dedicated portal where the user can login using their user id and

can access all the services of the bank (Agrawal 2017). The portal is connected to the server of

the bank. The user activity can be monitored by the bank officials. However, getting the online

facility, the consumer needs to go through some paper work for one time.

Offline Process:

In case of offline process, the user has to go to the bank and has to do formal enquiry

regarding the services and fill up the forms accordingly. The employees of the bank then process

those request manually.

Information: The information used in this system are confidential as , it holds the

information regarding the customers and their account numbers. In case of online banking and

the use of ATM the user id and the Pin of individual user is important.

Technology: The bank has implemented different advanced technology to initiate the

online banking. The bank has taken a policy to migrate the storage system partially to the cloud.

This will help to save the cost and the will provide better storage system (Omarini 2017). The

bank has also implemented the ATM system where, the ATM server is connected with the bank

and the transactions made through the ATM will be observed by the bank.

DIGITAL DISRUPTION IN THE BANKING SECTOR

of the bank, for that the user needs to have a ATM card and confidential and secured PIN

number.

Business Process: Major activities by the bank-

Online process:

The bank has created a dedicated portal where the user can login using their user id and

can access all the services of the bank (Agrawal 2017). The portal is connected to the server of

the bank. The user activity can be monitored by the bank officials. However, getting the online

facility, the consumer needs to go through some paper work for one time.

Offline Process:

In case of offline process, the user has to go to the bank and has to do formal enquiry

regarding the services and fill up the forms accordingly. The employees of the bank then process

those request manually.

Information: The information used in this system are confidential as , it holds the

information regarding the customers and their account numbers. In case of online banking and

the use of ATM the user id and the Pin of individual user is important.

Technology: The bank has implemented different advanced technology to initiate the

online banking. The bank has taken a policy to migrate the storage system partially to the cloud.

This will help to save the cost and the will provide better storage system (Omarini 2017). The

bank has also implemented the ATM system where, the ATM server is connected with the bank

and the transactions made through the ATM will be observed by the bank.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

10

DIGITAL DISRUPTION IN THE BANKING SECTOR

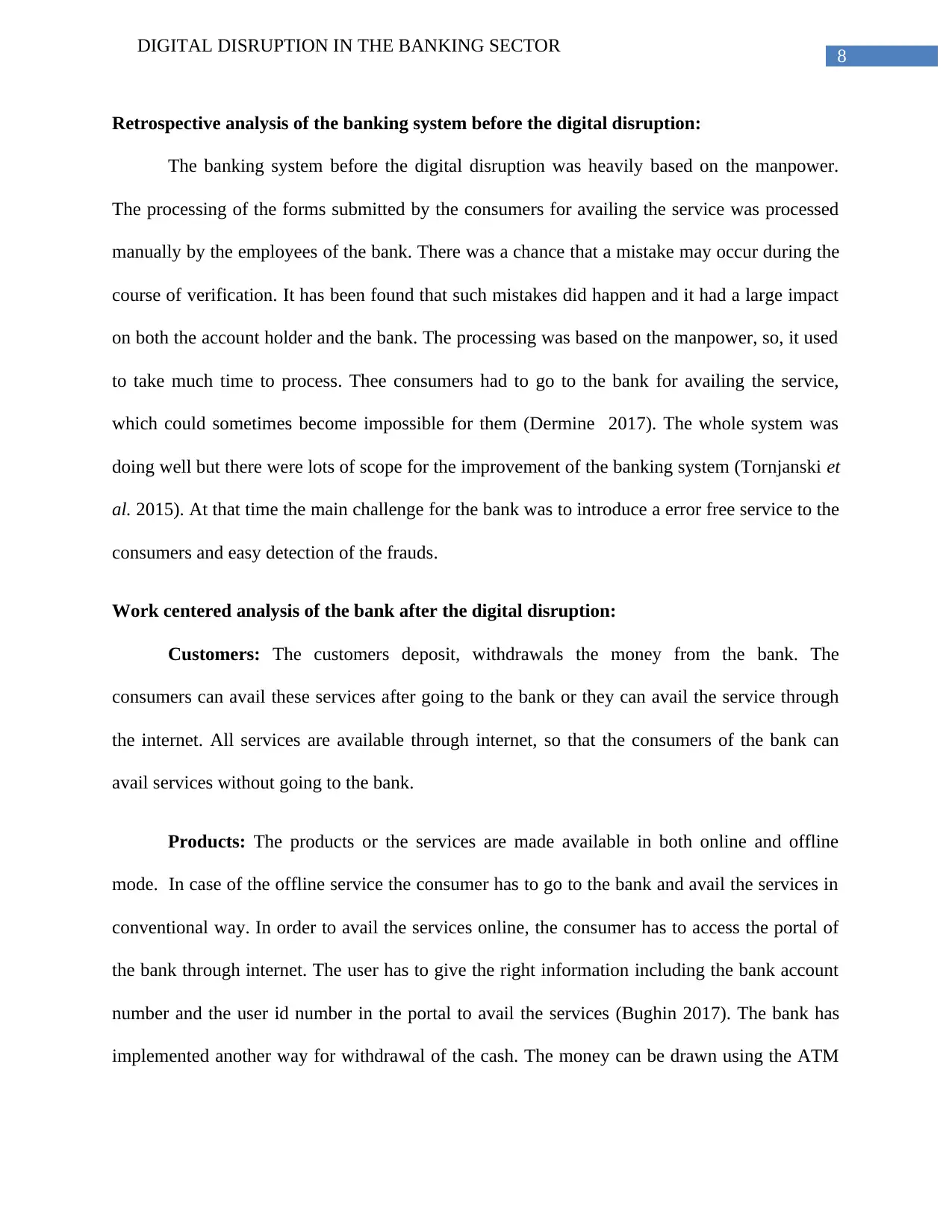

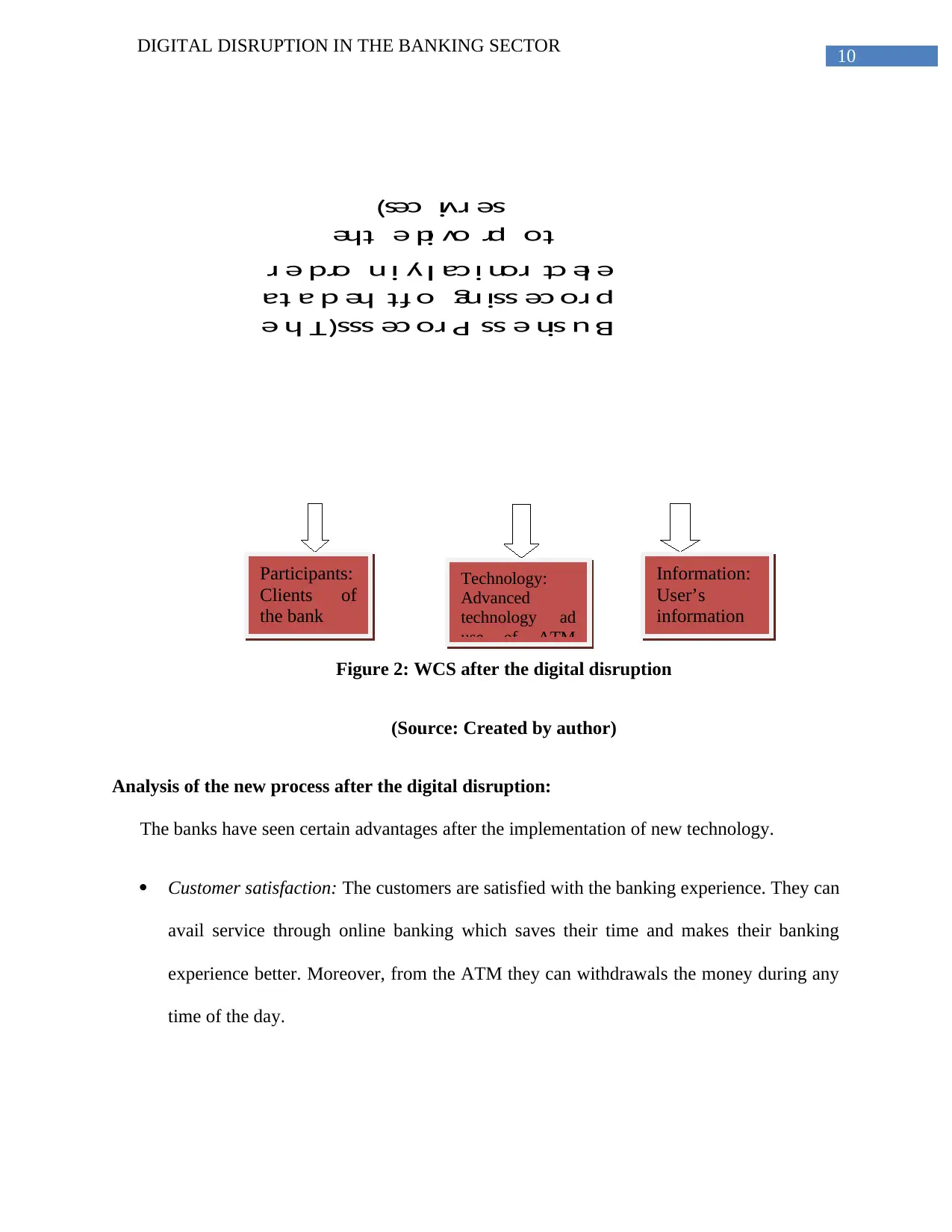

Figure 2: WCS after the digital disruption

(Source: Created by author)

Analysis of the new process after the digital disruption:

The banks have seen certain advantages after the implementation of new technology.

Customer satisfaction: The customers are satisfied with the banking experience. They can

avail service through online banking which saves their time and makes their banking

experience better. Moreover, from the ATM they can withdrawals the money during any

time of the day.

Customer

s(Clients

of bank )

Pr odu ct s (e-

Ser vices

pr ovide d on

diff er ent s ecto rs

by t he b an k)

B u sin e ss P ro ce sss(T h e

p ro ce ssi ng o ft he d a ta

e le ct ron i ca ll y i n ord e r

to pr ov id e the

se rvi ces)

Technology:

Advanced

technology ad

use of ATM

Participants:

Clients of

the bank

Information:

User’s

information

DIGITAL DISRUPTION IN THE BANKING SECTOR

Figure 2: WCS after the digital disruption

(Source: Created by author)

Analysis of the new process after the digital disruption:

The banks have seen certain advantages after the implementation of new technology.

Customer satisfaction: The customers are satisfied with the banking experience. They can

avail service through online banking which saves their time and makes their banking

experience better. Moreover, from the ATM they can withdrawals the money during any

time of the day.

Customer

s(Clients

of bank )

Pr odu ct s (e-

Ser vices

pr ovide d on

diff er ent s ecto rs

by t he b an k)

B u sin e ss P ro ce sss(T h e

p ro ce ssi ng o ft he d a ta

e le ct ron i ca ll y i n ord e r

to pr ov id e the

se rvi ces)

Technology:

Advanced

technology ad

use of ATM

Participants:

Clients of

the bank

Information:

User’s

information

11

DIGITAL DISRUPTION IN THE BANKING SECTOR

Cost effectiveness and better use of resources: The use of the technology in the banking

sector enables the fair use of resources and the online banking helps to reduce the cost

overhead. It indirectly helps in the growth of the business of the bank.

Better security: The adaptation of the technology in the banking system reduces the risk

of mistakes those could be happen in case of manual processing (Hunter, dela and Dole

2016). The works can be done in a small time span using the technologies.

Transparency in the process: The use of the technology has made the whole banking

system clear and transparent.

Availability of service: The technology has made the banking system available for 24*7

hours. The consumers can avail services through internet at any time of the day.

Recommendations:

There are certain advantages of the digital disruption have been concluded from the

discussion. However, it can be assumed that the banking system has partially adopted the use of

technology. In order for the full digitization of the banking system certain steps are needed to be

taken care of. This are-

The awareness regarding the online banking among the consumers.

The security system of the transactions through online is needed to be improved.

The bank should think to migrate the data fully to the cloud.

The bank can recruit a team of dedicated IT experts to maintain the whole system.

Implementation of the recommended plans:

The migration of data to cloud can be done after taking advice to the cloud security

experts. They can ensure the implementation of the whole system along with maintaining the

DIGITAL DISRUPTION IN THE BANKING SECTOR

Cost effectiveness and better use of resources: The use of the technology in the banking

sector enables the fair use of resources and the online banking helps to reduce the cost

overhead. It indirectly helps in the growth of the business of the bank.

Better security: The adaptation of the technology in the banking system reduces the risk

of mistakes those could be happen in case of manual processing (Hunter, dela and Dole

2016). The works can be done in a small time span using the technologies.

Transparency in the process: The use of the technology has made the whole banking

system clear and transparent.

Availability of service: The technology has made the banking system available for 24*7

hours. The consumers can avail services through internet at any time of the day.

Recommendations:

There are certain advantages of the digital disruption have been concluded from the

discussion. However, it can be assumed that the banking system has partially adopted the use of

technology. In order for the full digitization of the banking system certain steps are needed to be

taken care of. This are-

The awareness regarding the online banking among the consumers.

The security system of the transactions through online is needed to be improved.

The bank should think to migrate the data fully to the cloud.

The bank can recruit a team of dedicated IT experts to maintain the whole system.

Implementation of the recommended plans:

The migration of data to cloud can be done after taking advice to the cloud security

experts. They can ensure the implementation of the whole system along with maintaining the

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 14

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.