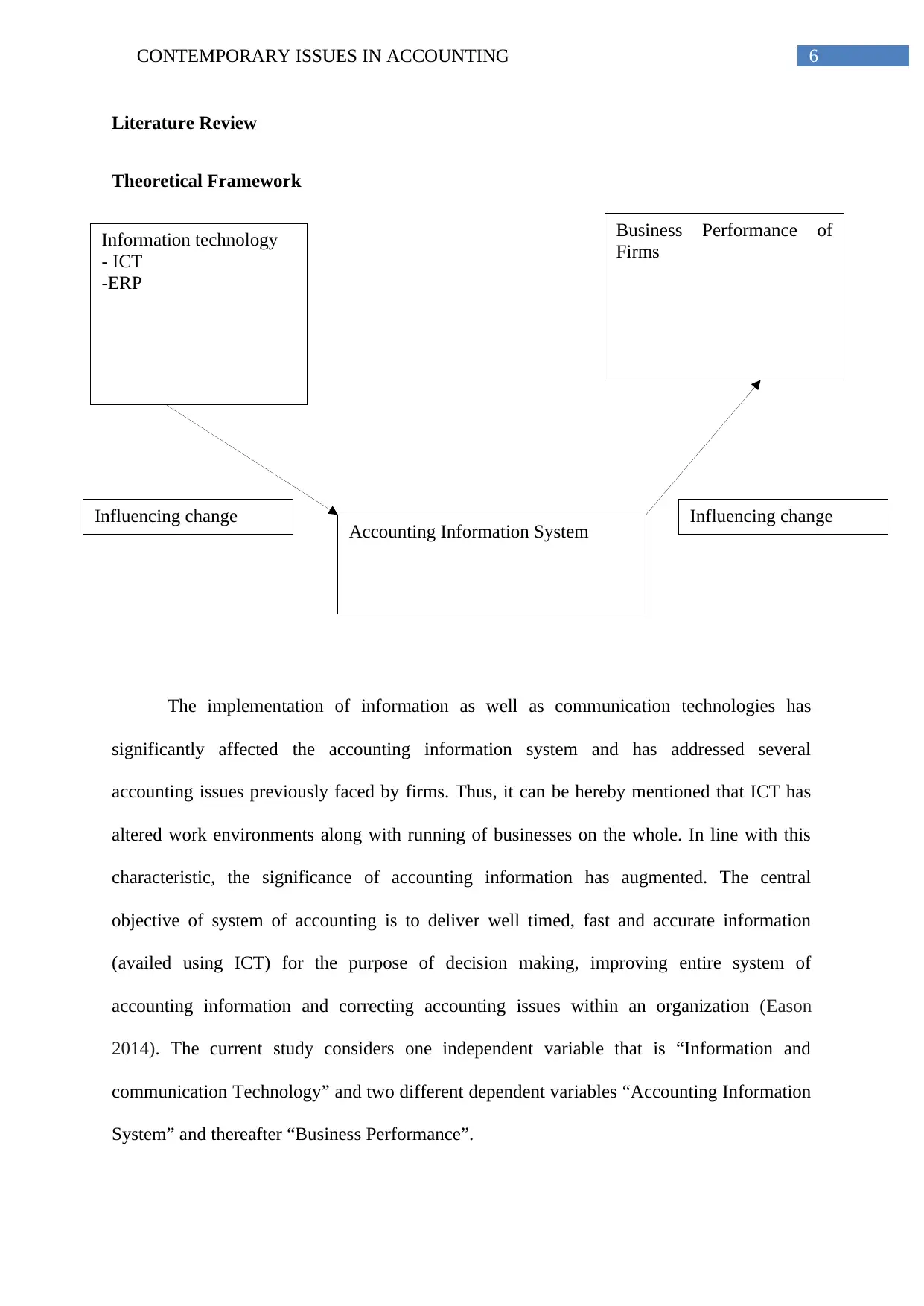

Effect of Information and Communication technology (ICT) on Accounting Information System and Business Performance

VerifiedAI Summary

This study examines the impact of Information and Communication Technology (ICT) on accounting information system and business performance. It highlights the ways ICT can address the issues faced by the manual system of accounting by replacing the same with automated/computerised software based system of accounting. The study aims to examine the influence of the implementation of ICT on overall efficiency of accounting systems and evaluate the influence of the implementation of ICT on overall efficiency of business performance through development of accounting information system.

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)