TABLE OF CONTENTS INTRODUCTION 4 (1) Regulations relating to financial accounting

38 Pages3927 Words437 Views

Added on 2020-10-22

About This Document

7 Client 1 8 A Journal entries8 11 12 13 13 14 14 15 16 17 18 19 20 21 22 23 C trial balance 23 CLIENT 2 24 A. Presenting a statement of financial position 27 27 (c)Explain the following accounting concepts: ‘consistency’ and ‘Prudence’ 27 (d)Purpose of depreciation in formulating accounting statements with the widely used accounting method. Drafting the trial balance with consideration of suspense accounts 36 (d)Regulation between suspense account and clearing

TABLE OF CONTENTS INTRODUCTION 4 (1) Regulations relating to financial accounting

Added on 2020-10-22

ShareRelated Documents

Title

TABLE OF CONTENTSINTRODUCTION...........................................................................................................................4(1) Financial accounting and its purpose....................................................................................4(2) Regulations relating to financial accounting........................................................................5(3)Accounting rules and principles.............................................................................................6Following are the accounting rules and principles-....................................................................6(4)The conventions and concepts relating to consistency and material disclosure....................7Client 1.............................................................................................................................................8A Journal entries.........................................................................................................................8...................................................................................................................................................11...................................................................................................................................................12...................................................................................................................................................12...................................................................................................................................................13...................................................................................................................................................13...................................................................................................................................................14...................................................................................................................................................14...................................................................................................................................................15...................................................................................................................................................16...................................................................................................................................................17...................................................................................................................................................18...................................................................................................................................................18...................................................................................................................................................19...................................................................................................................................................20...................................................................................................................................................21...................................................................................................................................................22...................................................................................................................................................23C trial balance ..........................................................................................................................23CLIENT 2......................................................................................................................................24A. Drafting an income statement..............................................................................................24B. Preparing a statement of financial position..........................................................................25

...................................................................................................................................................26CLIENT 3......................................................................................................................................26A. Preparing and Income statement..........................................................................................26B. Presenting a statement of financial position.........................................................................27...................................................................................................................................................27(c)Explain the following accounting concepts: ‘consistency’ and ‘Prudence’.........................27(d)Purpose of depreciation in formulating accounting statements with the widely usedmethod. .....................................................................................................................................28(a)purpose of preparing the Bank Reconciliation Statement ...................................................29(b)Following are the areas where the difference between company accounts to bank accountsoccurs. ......................................................................................................................................30C. Preparing the cash book (bank only) for Kedal Ltd.............................................................30CLIENT 5......................................................................................................................................32A. Drafting and balancing the accounts....................................................................................32(b) Explain the term control account.........................................................................................34CLIENT 6......................................................................................................................................35(a)Explain the suspense account and its features with examples. ............................................35B. & C. Drafting the trial balance with consideration of suspense accounts............................36(d)Difference between suspense account and clearing account................................................36CONCLUSION .............................................................................................................................37REFERENCES..............................................................................................................................38

INTRODUCTIONFinancial accounting is the field of accounting which deals with the financial informationof the company. This reports provide the information about the financial accounting , accountingregulations, accounting principles and the convention concepts. This report consist of journal,ledgers and trial balance of the given records. The report also provides the profit and lossaccount and balance of ask data . The assignment has given the deeper insight of the consistency, prudence concept and the purpose of depreciation, bank reconciliation statements suspenseaccount and its features, this assignment presents the bank reconciliation statements and the cashbooks of Kendall ltd. The report provides the information about the sales ledger control accountand purchase ledger control account of the company. Report has discussed about the differencebetween clearing and suspense account. (1) Financial accounting and its purpose.Financial accounting is the field of accounting which deals with the financial tracks ofmonetary transaction. It is that field of accounting which examines all the working of financialtransactions in an accounting (Hatfield, 2014). The branch of accounting which concern with the

analysis , summary and reporting of financial statements . A financial statement on a routineschedule are issued by the company. Every organization has a department named finance ,which is critical part of the organization and every employee cannot handle it, only the financeexecutives , or finance manager has right to take care of it , the working of these departments iscontrolled and performed by the financial accounting.The purpose of financial accounting is to give the data that is required for efficientdecision making. Another essential purpose of financial accounting is to prepare the report andanalyse it so that the position of the company can be determined. It also helps to identify thefirms' performance to outsiders such as creditors , tax authority and the investors(Macve, 2015. ).The financial accounting emphasize all the cash flows in order check the stability of thecompany . It accumulates and informs the financial information for the purpose to determine theperformance financial position of the business. This all information later, used to take thedecision about how to manage the working of the business or invest in it . (2) Regulations relating to financialaccounting.The organizations' success is dependent upon the financial accounting. There arenumerous regulatory bodies that direct the accounting. They consist of certain norms which anorganization has to be follow. There are the set standards which need to be follow by theorganization at the time of decision making of financial activity. The regulatory bodies consist ofvarious association, commission, boards etc. they include the predefined working which need tobe follow. Some governing bodies of accounting are discussed under- Security and exchange commission The objective of the US. Securities and exchange commission is to save investors , andmaintain the fair market and ease the formation of capital. The main mission of SEC's is toexpound the law that are passes by the congress and guide the organization to implement theselaws.The Financial Accounting Standards Boards (FASB)The financial accounting standard boards were propounded on 1973 by the securityexchange commission. The main aim of the FASB is to create the financial accounting andreporting standards for the public(Ruppel, , 2017.). FASB works on to modify the standards ofFA for the public. Another important mission of financial accounting standard accounting boardis that to protect the public from fraudulent and deceptive information from the organization.

International financial reporting system International financial reporting system is taken out by IFRS foundation. Its mainobjective is to provide the common language of accounting so it can be understand by the everyorganisation across the country. (3)Accounting rules andprinciplesFollowing are the accounting rules and principles-(i) separate legal entity An organization is separate from its owner in the eye of law. This accounting rulesignifies that the identity of the business is separate from its owner. All the workings areundertaken separately from that of its owner.(ii) Ongoing processOngoing process identifies that business keeps ongoing until it cannot be wind-up as peraccounting standards. In other words you cannot wind up or close the working with mutualdiscussion. Any death of insolvency cannot stop the working of business or close the business. (iii)The specific time period participlesFinancial statements are always concern to a specific time. Accounting statement havebeginning date and closing date for the reporting of balance sheet. That helps the reader toidentify that when the transactions were conducted. (iv)The Historical Cost PrincipleFor the valuation of the items historical cost is used. The amount at which item arepurchased and sale is use d for the valuation. The value of price due change due to recession ,inflation, but these are not taken for the reporting purposes. (v) The Full Disclosure PrincipleThese principles always signifies or keep strict focus on the scandals related to theaccounting in the news now a days (Maynard, 2017.). It needs all the information from thecompany about their functioning in their financial statements. (vi) The Recognition PrincipleThis principle of accounting states that company should recognize its income and expenses at thetime whey are accrued. (vii) The Matching Principle

These principles work on the rule that for every transaction the accrual system ofaccounting is used that means for every debit there should be the credit also and vice versa. (viii )Money measurement principleThis accounting rules identifies that all the transactions , events and happenings arerecorded in terms of money. (ix) The principles of materialityThe principle of materiality arises when the bookkeepers have to use their judgement.This principle helps to correct the inaccuracies in all accounting records. (x) The Principle of Conservative AccountingThe conservative accounting principles is adopted for the betterment for the company.When the expenses takes place they are to be record immediately, but the income are to berecord when the cash is actually received. (4)The conventions and concepts relating to consistency and materialdisclosure.Convention of consistencyThis convention of consistency focus that the accounting practices which are runningshould remain same during over the year to year. The valuation methods were treated same asperiod to period. For example , while the valuation of stock, it is taken that stock is valued at costor market price which ever is less , then this should be followed year after year. Consistencydoest not mean the inflexibility , if the necessity of change arises, it should be done and its effectshould be stated clearly. Convention of material disclosureThe convention of material disclosure states that, at the time of disclosing the account allthe transaction recorded must have valid proof that from where they have arrived and recorded.

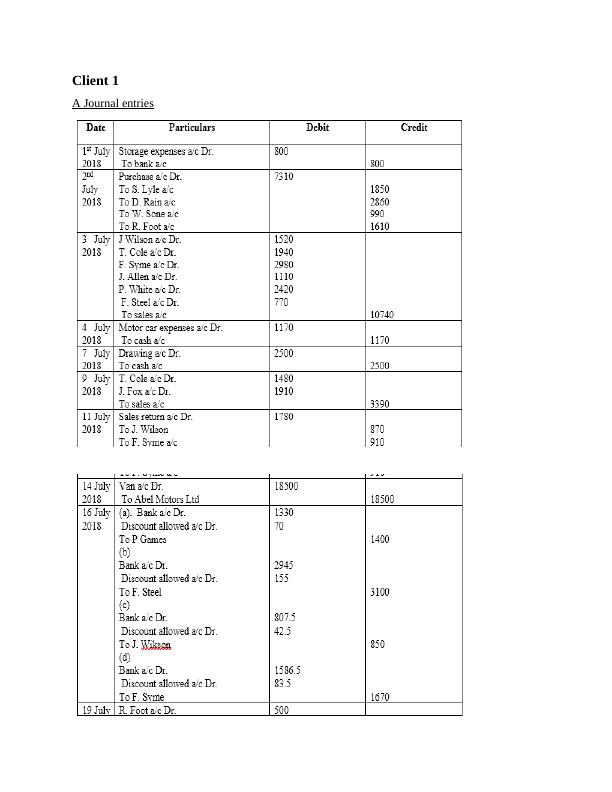

Client 1A Journal entries

End of preview

Want to access all the pages? Upload your documents or become a member.

Related Documents

Report on Accounting Conventions and Principleslg...

|34

|3968

|114

FINANCIAL ACCOUNTING PRINCIPLES TABLE OF CONTENTS INTRODUCTION 1lg...

|40

|5315

|463

Financial accounting Field PDFlg...

|32

|3855

|370

Financial Accounting: Assignment Samplelg...

|37

|5577

|390

[DOC] Financial Accounting Principles Assignmentlg...

|41

|5398

|84

Financial Accounting Principles Doclg...

|39

|5227

|225