Financial Accounting Principles Report: Application and Analysis

VerifiedAdded on 2021/01/03

|29

|4156

|52

Report

AI Summary

This report provides a comprehensive overview of financial accounting principles, regulations, and their practical application. It begins by defining financial accounting and its purpose, followed by an examination of relevant regulations, accounting rules, and conventions. The report then delves into practical examples, including journal entries, ledger accounts, cash books, and trial balances, using various client scenarios to illustrate key concepts. It covers the preparation of income statements, financial statements, profit and loss accounts, and statements of financial position. Additionally, the report addresses accounting concepts such as prudency and consistency, the purpose of depreciation, and bank reconciliation. It also explores control accounts, suspense accounts, and the importance of these elements in ensuring accurate financial reporting. The report concludes with a summary of the main points and provides a list of references.

FINANCIAL ACCOUNTING

PRINCIPLES

PRINCIPLES

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

TABLE OF CONTENTS

INTRODUCTION...........................................................................................................................1

REPORT..........................................................................................................................................1

1. Defining financial accounting and its purpose...................................................................2

2. Regulations relating to financial accounting......................................................................2

3. Accounting rules and principles.........................................................................................3

4 Convention and concepts of financial accounting...............................................................5

CLIENT 1........................................................................................................................................6

A. Journals entries..................................................................................................................6

B. Ledger Account..................................................................................................................8

Cash Book............................................................................................................................14

C. Trial balance ...................................................................................................................16

CLIENT 2......................................................................................................................................17

A. Laurent's income statement.............................................................................................17

B. Financial statements of Laurent.......................................................................................17

CLIENT 3......................................................................................................................................18

A. Preparation of profit and loss account.............................................................................18

B. Preparation of statement of financial position ................................................................18

C. Accounting concept of prudency and consistency...........................................................19

D. Purpose of depreciation in formulation of accounting statements..................................20

CLIENT 4......................................................................................................................................21

A. Purpose of preparation of Bank reconciliation statement...............................................21

B. Reasons for occurrence of variation between cash book and bank records.....................21

C. I) Cash book.....................................................................................................................22

C. II) Bank reconciliation statement ....................................................................................23

CLIENT 5......................................................................................................................................23

A. Preparation of Ledger accounts ......................................................................................23

B. Control accounts and its importance................................................................................24

CLIENT 6......................................................................................................................................24

A. Suspense accounts and its main features.........................................................................24

INTRODUCTION...........................................................................................................................1

REPORT..........................................................................................................................................1

1. Defining financial accounting and its purpose...................................................................2

2. Regulations relating to financial accounting......................................................................2

3. Accounting rules and principles.........................................................................................3

4 Convention and concepts of financial accounting...............................................................5

CLIENT 1........................................................................................................................................6

A. Journals entries..................................................................................................................6

B. Ledger Account..................................................................................................................8

Cash Book............................................................................................................................14

C. Trial balance ...................................................................................................................16

CLIENT 2......................................................................................................................................17

A. Laurent's income statement.............................................................................................17

B. Financial statements of Laurent.......................................................................................17

CLIENT 3......................................................................................................................................18

A. Preparation of profit and loss account.............................................................................18

B. Preparation of statement of financial position ................................................................18

C. Accounting concept of prudency and consistency...........................................................19

D. Purpose of depreciation in formulation of accounting statements..................................20

CLIENT 4......................................................................................................................................21

A. Purpose of preparation of Bank reconciliation statement...............................................21

B. Reasons for occurrence of variation between cash book and bank records.....................21

C. I) Cash book.....................................................................................................................22

C. II) Bank reconciliation statement ....................................................................................23

CLIENT 5......................................................................................................................................23

A. Preparation of Ledger accounts ......................................................................................23

B. Control accounts and its importance................................................................................24

CLIENT 6......................................................................................................................................24

A. Suspense accounts and its main features.........................................................................24

B and C. Preparation of Trial Balance making correction ..................................................25

D. Differentiation between clearing and suspense account .................................................26

CONCLUSION..............................................................................................................................26

REFERENCES..............................................................................................................................27

D. Differentiation between clearing and suspense account .................................................26

CONCLUSION..............................................................................................................................26

REFERENCES..............................................................................................................................27

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

INTRODUCTION

In an organisation accounting is integral part as it is the process through which all

monetary transactions related with business operations are summarized and reported to draw an

interpretation about flow of organization finance and its performance in an accounting year. All

material financial transactions are identified and with following relevant accounting principles

and standards they are recorded in books of accounts. In the present report accounting standards

and regulations which a business must comply are mentioned along with their relevance and

importance. Apart from this various accounting terms and statements are prepared in an entity

for reconciliation and closing of books of accounts are also explained with purpose they serve.

REPORT

1

In an organisation accounting is integral part as it is the process through which all

monetary transactions related with business operations are summarized and reported to draw an

interpretation about flow of organization finance and its performance in an accounting year. All

material financial transactions are identified and with following relevant accounting principles

and standards they are recorded in books of accounts. In the present report accounting standards

and regulations which a business must comply are mentioned along with their relevance and

importance. Apart from this various accounting terms and statements are prepared in an entity

for reconciliation and closing of books of accounts are also explained with purpose they serve.

REPORT

1

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

To

Line Manager

From: Junior Accountant

Subject: Presentation and application of accounting principles, standards and regulation in

business accounting and reporting which is helpful in evaluation of operational efficiency.

Sir,

The present report is prepared to explain and define knowledge acquaintance of

financial accounting for all personnel in organisation. This report will define that how

accounting principles and regulation are applied to different financial transactions. The

treatment of revenue and capital expenses/incomes is determined by various accounting

standards laid down for this purpose. These reports present all regulations and bodies

responsible for formation of those rules, applicable in accounting of business.

1. Defining financial accounting and its purpose

Financial accounting means to present all monetary transactions of a business for a

particular fiscal period in a definite format. The information is laid down by following all

accounting regulations and standards by regulating bodies and authorities formed by

government. This is mainly concerned with collection al financial information of a business,

analysing and reporting them. This process determines income generated, expenses incurred

and profits earned by business. This information presented through preparation of financial

reports provide significant info to related people outside the business. These people can be

stakeholders, creditors, banks, government, business owners, investors etc. The financial reports

prepared under this are profit and loss account, balance sheet, statement of cash flow and

shareholders equity's statement (Miller-Nobles, Mattison and Matsumura, 2016). These

statements all together reveals relevant information related with a business such as net worth,

profits earned, financial growth of firm, market valuation, cash inflows and outflows along with

assets with and liability that company needs to meet.

2. Regulations relating to financial accounting

Financial accounting regulations are important laws and generalisation for preparation

of fiscal statements of a business. These are formed and regulated by authoritative bodies made

by monitoring board. Regulations are formed for both domestic and international business.

Domestic regulation is formed by institute of charted accountants in England and Wales.

2

Line Manager

From: Junior Accountant

Subject: Presentation and application of accounting principles, standards and regulation in

business accounting and reporting which is helpful in evaluation of operational efficiency.

Sir,

The present report is prepared to explain and define knowledge acquaintance of

financial accounting for all personnel in organisation. This report will define that how

accounting principles and regulation are applied to different financial transactions. The

treatment of revenue and capital expenses/incomes is determined by various accounting

standards laid down for this purpose. These reports present all regulations and bodies

responsible for formation of those rules, applicable in accounting of business.

1. Defining financial accounting and its purpose

Financial accounting means to present all monetary transactions of a business for a

particular fiscal period in a definite format. The information is laid down by following all

accounting regulations and standards by regulating bodies and authorities formed by

government. This is mainly concerned with collection al financial information of a business,

analysing and reporting them. This process determines income generated, expenses incurred

and profits earned by business. This information presented through preparation of financial

reports provide significant info to related people outside the business. These people can be

stakeholders, creditors, banks, government, business owners, investors etc. The financial reports

prepared under this are profit and loss account, balance sheet, statement of cash flow and

shareholders equity's statement (Miller-Nobles, Mattison and Matsumura, 2016). These

statements all together reveals relevant information related with a business such as net worth,

profits earned, financial growth of firm, market valuation, cash inflows and outflows along with

assets with and liability that company needs to meet.

2. Regulations relating to financial accounting

Financial accounting regulations are important laws and generalisation for preparation

of fiscal statements of a business. These are formed and regulated by authoritative bodies made

by monitoring board. Regulations are formed for both domestic and international business.

Domestic regulation is formed by institute of charted accountants in England and Wales.

2

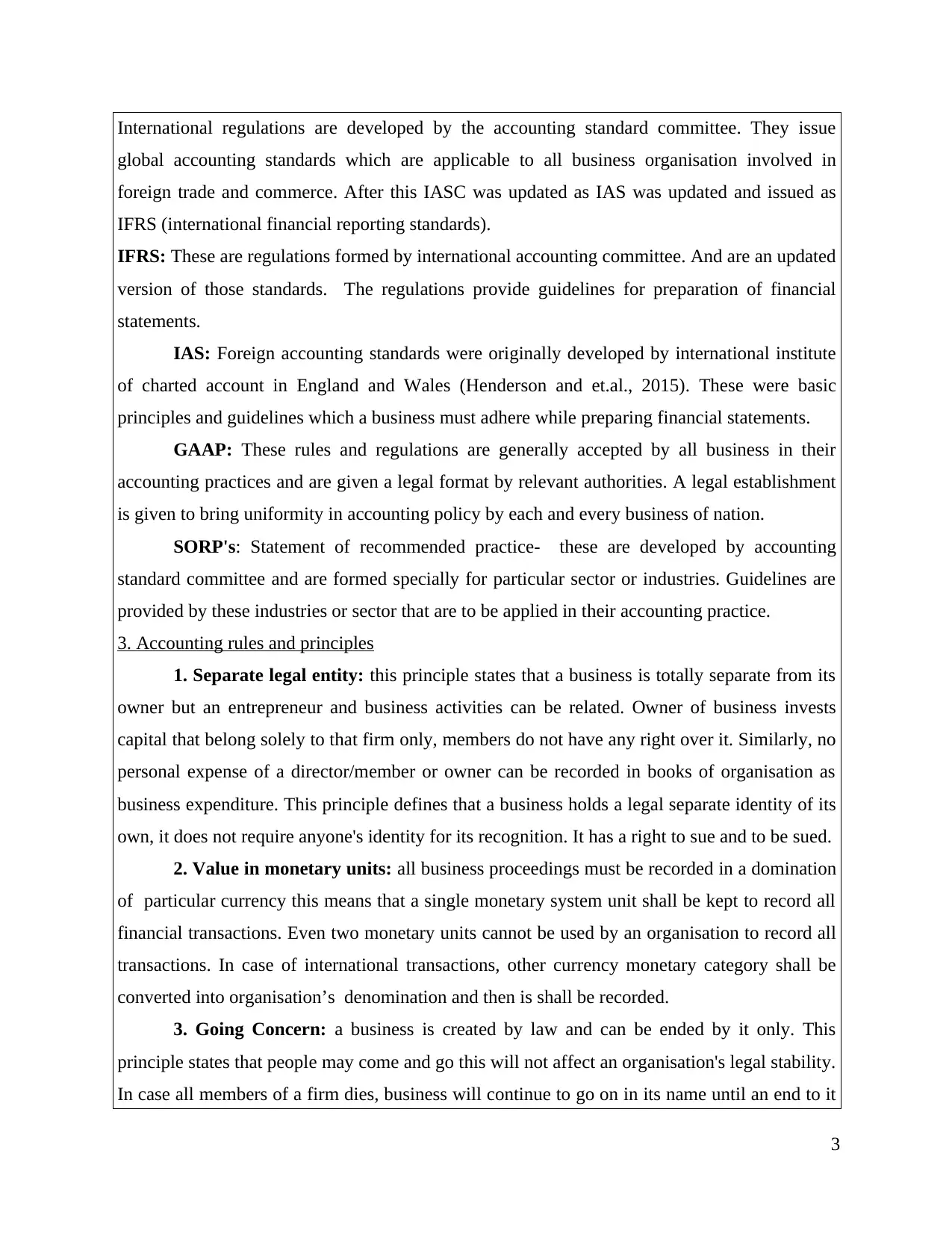

International regulations are developed by the accounting standard committee. They issue

global accounting standards which are applicable to all business organisation involved in

foreign trade and commerce. After this IASC was updated as IAS was updated and issued as

IFRS (international financial reporting standards).

IFRS: These are regulations formed by international accounting committee. And are an updated

version of those standards. The regulations provide guidelines for preparation of financial

statements.

IAS: Foreign accounting standards were originally developed by international institute

of charted account in England and Wales (Henderson and et.al., 2015). These were basic

principles and guidelines which a business must adhere while preparing financial statements.

GAAP: These rules and regulations are generally accepted by all business in their

accounting practices and are given a legal format by relevant authorities. A legal establishment

is given to bring uniformity in accounting policy by each and every business of nation.

SORP's: Statement of recommended practice- these are developed by accounting

standard committee and are formed specially for particular sector or industries. Guidelines are

provided by these industries or sector that are to be applied in their accounting practice.

3. Accounting rules and principles

1. Separate legal entity: this principle states that a business is totally separate from its

owner but an entrepreneur and business activities can be related. Owner of business invests

capital that belong solely to that firm only, members do not have any right over it. Similarly, no

personal expense of a director/member or owner can be recorded in books of organisation as

business expenditure. This principle defines that a business holds a legal separate identity of its

own, it does not require anyone's identity for its recognition. It has a right to sue and to be sued.

2. Value in monetary units: all business proceedings must be recorded in a domination

of particular currency this means that a single monetary system unit shall be kept to record all

financial transactions. Even two monetary units cannot be used by an organisation to record all

transactions. In case of international transactions, other currency monetary category shall be

converted into organisation’s denomination and then is shall be recorded.

3. Going Concern: a business is created by law and can be ended by it only. This

principle states that people may come and go this will not affect an organisation's legal stability.

In case all members of a firm dies, business will continue to go on in its name until an end to it

3

global accounting standards which are applicable to all business organisation involved in

foreign trade and commerce. After this IASC was updated as IAS was updated and issued as

IFRS (international financial reporting standards).

IFRS: These are regulations formed by international accounting committee. And are an updated

version of those standards. The regulations provide guidelines for preparation of financial

statements.

IAS: Foreign accounting standards were originally developed by international institute

of charted account in England and Wales (Henderson and et.al., 2015). These were basic

principles and guidelines which a business must adhere while preparing financial statements.

GAAP: These rules and regulations are generally accepted by all business in their

accounting practices and are given a legal format by relevant authorities. A legal establishment

is given to bring uniformity in accounting policy by each and every business of nation.

SORP's: Statement of recommended practice- these are developed by accounting

standard committee and are formed specially for particular sector or industries. Guidelines are

provided by these industries or sector that are to be applied in their accounting practice.

3. Accounting rules and principles

1. Separate legal entity: this principle states that a business is totally separate from its

owner but an entrepreneur and business activities can be related. Owner of business invests

capital that belong solely to that firm only, members do not have any right over it. Similarly, no

personal expense of a director/member or owner can be recorded in books of organisation as

business expenditure. This principle defines that a business holds a legal separate identity of its

own, it does not require anyone's identity for its recognition. It has a right to sue and to be sued.

2. Value in monetary units: all business proceedings must be recorded in a domination

of particular currency this means that a single monetary system unit shall be kept to record all

financial transactions. Even two monetary units cannot be used by an organisation to record all

transactions. In case of international transactions, other currency monetary category shall be

converted into organisation’s denomination and then is shall be recorded.

3. Going Concern: a business is created by law and can be ended by it only. This

principle states that people may come and go this will not affect an organisation's legal stability.

In case all members of a firm dies, business will continue to go on in its name until an end to it

3

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

is put by following procedure of law that is dissolution or liquidation.

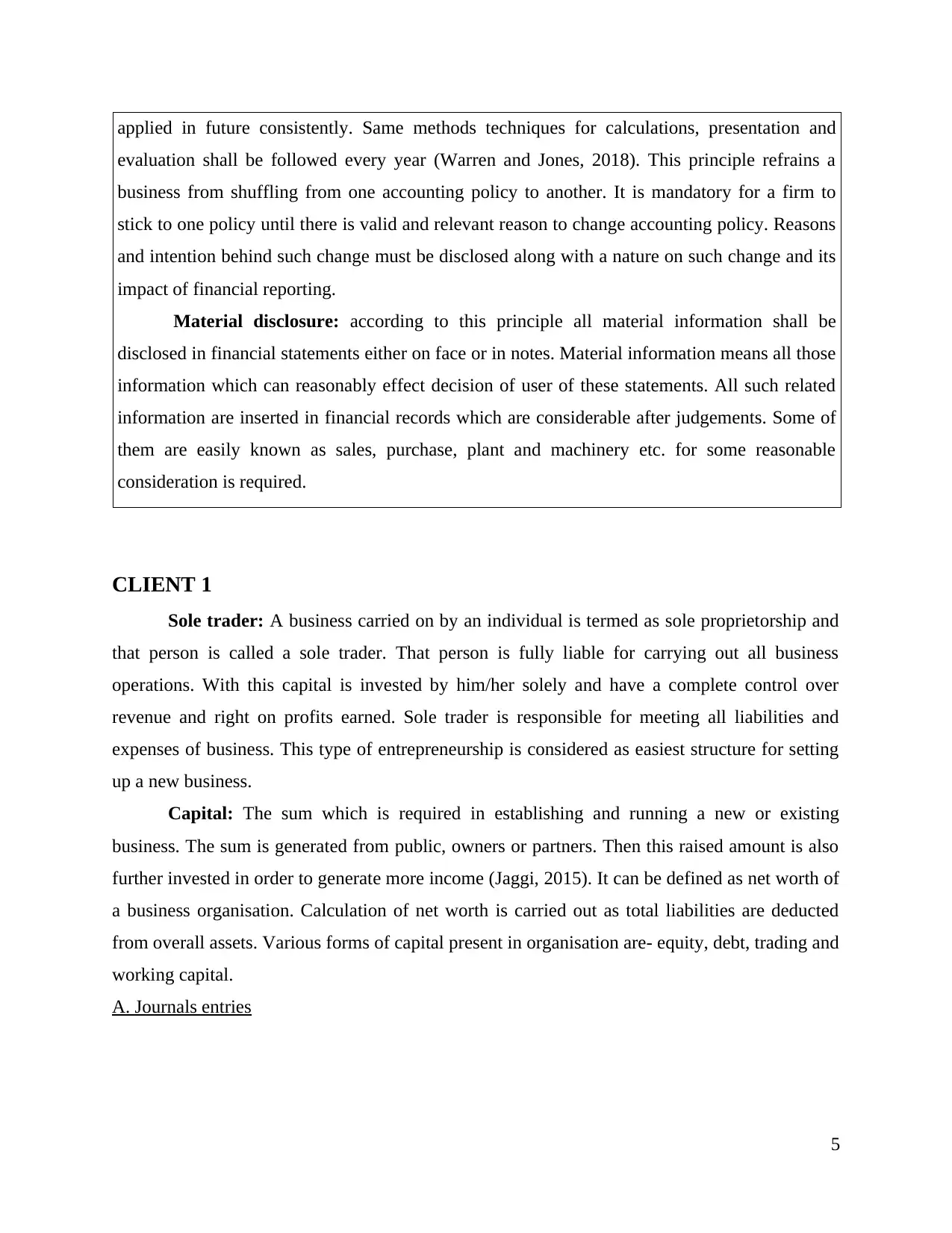

4. Historical cost: this means assets of a business must be valued on its acquisition cost

not at prevailing market rate, as it does not provide actual value of assets as it fluctuates with

inflation and deflation of economy (Beatty and Liao, 2014). So this principle makes action that

all assets are recorded in balance sheet as its original cost, which will present true and actual net

worth and financial position of business.

5. Accrual basis: record transaction pertaining to a business as and when they occur

irrespective of the fact of actual cash flow. This means a revenue when earned shall be booked

in books of business though amount related with it will be received on a later date or is received

in advance, same is case with expenses. Book a transaction as when it happens though cash is

received or paid in the future.

6. Matching principle: this principle states that a dual accounting system has to be

followed by a business. This means for every income there shall be an expense and vice a versa.

This means for expenses incurred income generation shall be showed.

7. Accounting period: Accounting period means a particular time period for which

financial accounts of an organisation are prepared. This preparation can be monthly, quarterly

or annually. Generally, time frame which is followed is annual. All statements reflecting

financial position of business are for a year which can start from either January, March or

September.

8. Relevance and reliability: all data and information recorded in books of accounts

must be relevant and reliable. Relevancy can be determined as all financial transaction books

must belong to that particular year and involves cash flow. Reliability of a transaction can be

checked to prove its authenticity all documentary evidences are available.

9. Conservatism: sometimes accounting transactions and other events are uncertain

and for maintaining relevancy they have to be reported in time. Estimation are made for

making judgement to deal with such uncertainty.

10. Comparability: this is a key quality which must be possessed by accounting

information. A comparison of such data can be carried out when accounting-standards and

polices are applied consistently from one period to other.

4 Convention and concepts of financial accounting

Consistency: once a method is adopted for recording financial transaction it must be

4

4. Historical cost: this means assets of a business must be valued on its acquisition cost

not at prevailing market rate, as it does not provide actual value of assets as it fluctuates with

inflation and deflation of economy (Beatty and Liao, 2014). So this principle makes action that

all assets are recorded in balance sheet as its original cost, which will present true and actual net

worth and financial position of business.

5. Accrual basis: record transaction pertaining to a business as and when they occur

irrespective of the fact of actual cash flow. This means a revenue when earned shall be booked

in books of business though amount related with it will be received on a later date or is received

in advance, same is case with expenses. Book a transaction as when it happens though cash is

received or paid in the future.

6. Matching principle: this principle states that a dual accounting system has to be

followed by a business. This means for every income there shall be an expense and vice a versa.

This means for expenses incurred income generation shall be showed.

7. Accounting period: Accounting period means a particular time period for which

financial accounts of an organisation are prepared. This preparation can be monthly, quarterly

or annually. Generally, time frame which is followed is annual. All statements reflecting

financial position of business are for a year which can start from either January, March or

September.

8. Relevance and reliability: all data and information recorded in books of accounts

must be relevant and reliable. Relevancy can be determined as all financial transaction books

must belong to that particular year and involves cash flow. Reliability of a transaction can be

checked to prove its authenticity all documentary evidences are available.

9. Conservatism: sometimes accounting transactions and other events are uncertain

and for maintaining relevancy they have to be reported in time. Estimation are made for

making judgement to deal with such uncertainty.

10. Comparability: this is a key quality which must be possessed by accounting

information. A comparison of such data can be carried out when accounting-standards and

polices are applied consistently from one period to other.

4 Convention and concepts of financial accounting

Consistency: once a method is adopted for recording financial transaction it must be

4

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

applied in future consistently. Same methods techniques for calculations, presentation and

evaluation shall be followed every year (Warren and Jones, 2018). This principle refrains a

business from shuffling from one accounting policy to another. It is mandatory for a firm to

stick to one policy until there is valid and relevant reason to change accounting policy. Reasons

and intention behind such change must be disclosed along with a nature on such change and its

impact of financial reporting.

Material disclosure: according to this principle all material information shall be

disclosed in financial statements either on face or in notes. Material information means all those

information which can reasonably effect decision of user of these statements. All such related

information are inserted in financial records which are considerable after judgements. Some of

them are easily known as sales, purchase, plant and machinery etc. for some reasonable

consideration is required.

CLIENT 1

Sole trader: A business carried on by an individual is termed as sole proprietorship and

that person is called a sole trader. That person is fully liable for carrying out all business

operations. With this capital is invested by him/her solely and have a complete control over

revenue and right on profits earned. Sole trader is responsible for meeting all liabilities and

expenses of business. This type of entrepreneurship is considered as easiest structure for setting

up a new business.

Capital: The sum which is required in establishing and running a new or existing

business. The sum is generated from public, owners or partners. Then this raised amount is also

further invested in order to generate more income (Jaggi, 2015). It can be defined as net worth of

a business organisation. Calculation of net worth is carried out as total liabilities are deducted

from overall assets. Various forms of capital present in organisation are- equity, debt, trading and

working capital.

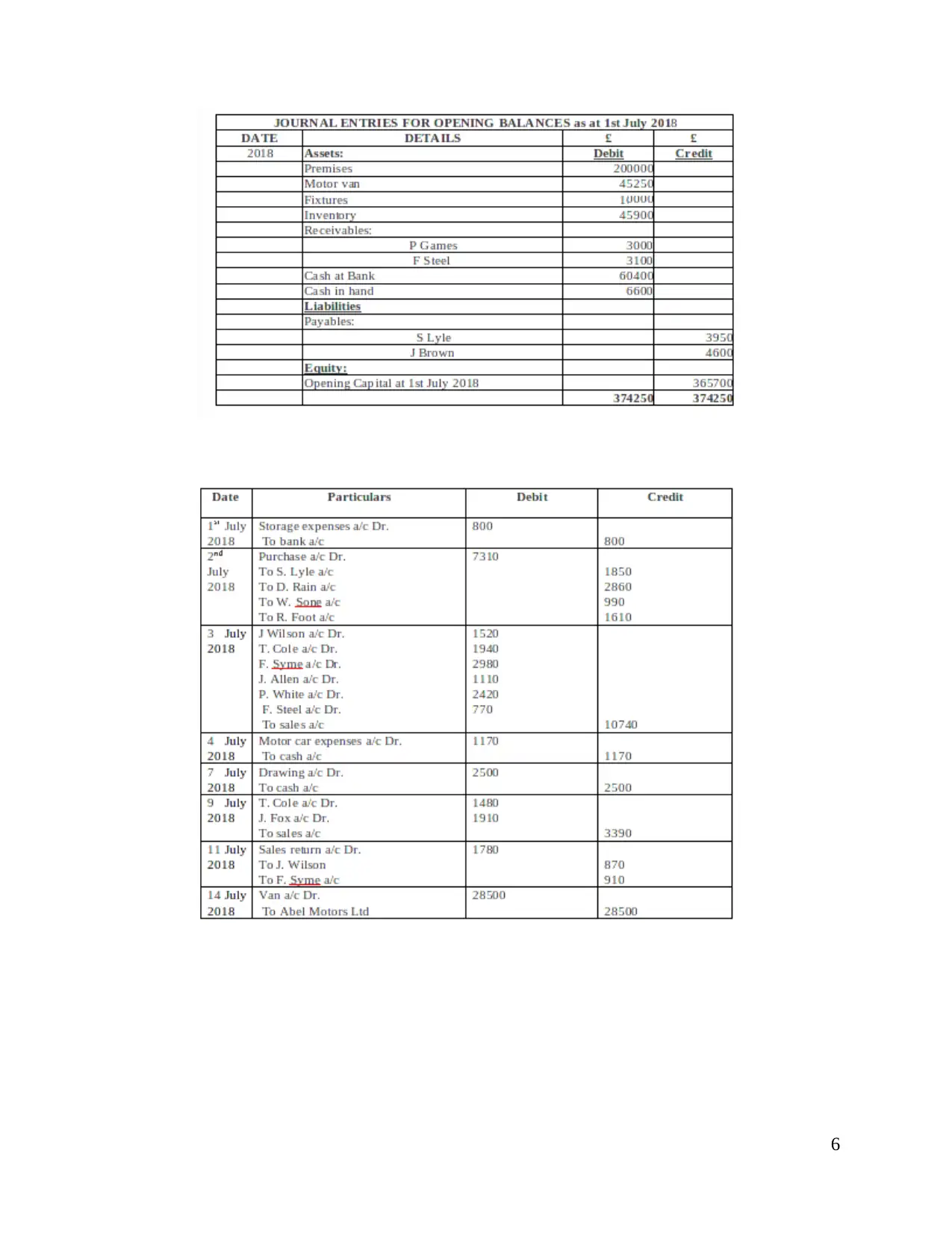

A. Journals entries

5

evaluation shall be followed every year (Warren and Jones, 2018). This principle refrains a

business from shuffling from one accounting policy to another. It is mandatory for a firm to

stick to one policy until there is valid and relevant reason to change accounting policy. Reasons

and intention behind such change must be disclosed along with a nature on such change and its

impact of financial reporting.

Material disclosure: according to this principle all material information shall be

disclosed in financial statements either on face or in notes. Material information means all those

information which can reasonably effect decision of user of these statements. All such related

information are inserted in financial records which are considerable after judgements. Some of

them are easily known as sales, purchase, plant and machinery etc. for some reasonable

consideration is required.

CLIENT 1

Sole trader: A business carried on by an individual is termed as sole proprietorship and

that person is called a sole trader. That person is fully liable for carrying out all business

operations. With this capital is invested by him/her solely and have a complete control over

revenue and right on profits earned. Sole trader is responsible for meeting all liabilities and

expenses of business. This type of entrepreneurship is considered as easiest structure for setting

up a new business.

Capital: The sum which is required in establishing and running a new or existing

business. The sum is generated from public, owners or partners. Then this raised amount is also

further invested in order to generate more income (Jaggi, 2015). It can be defined as net worth of

a business organisation. Calculation of net worth is carried out as total liabilities are deducted

from overall assets. Various forms of capital present in organisation are- equity, debt, trading and

working capital.

A. Journals entries

5

6

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

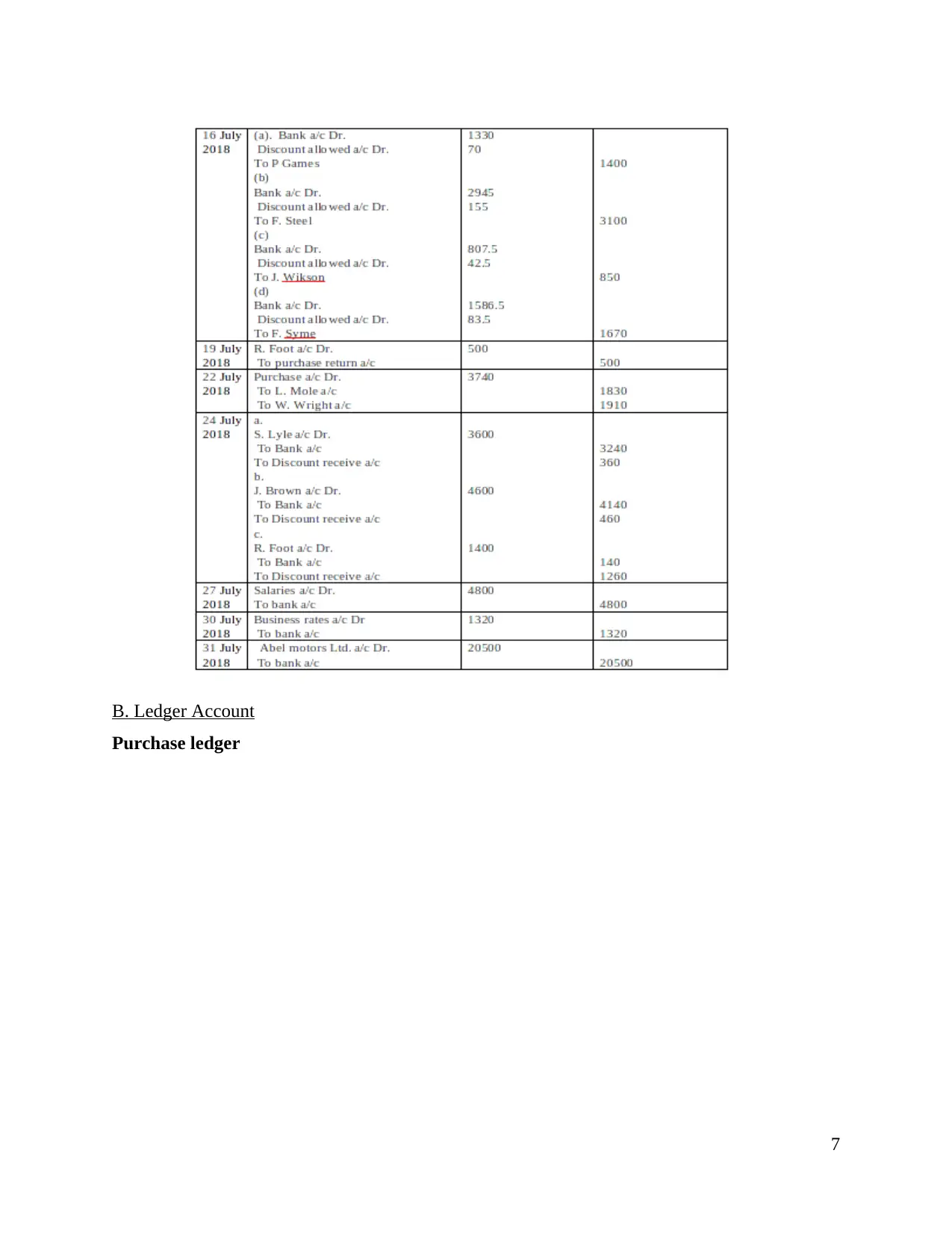

B. Ledger Account

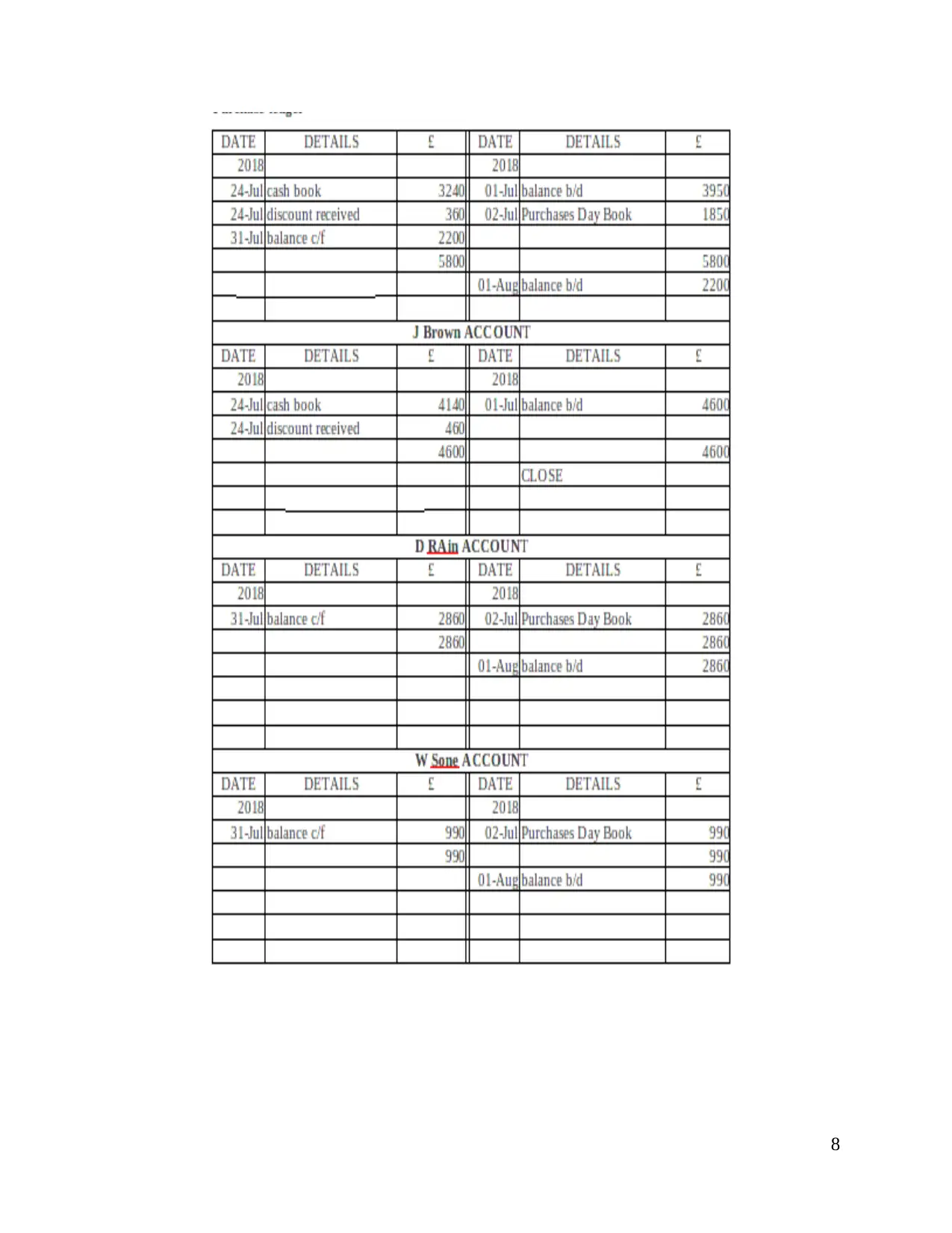

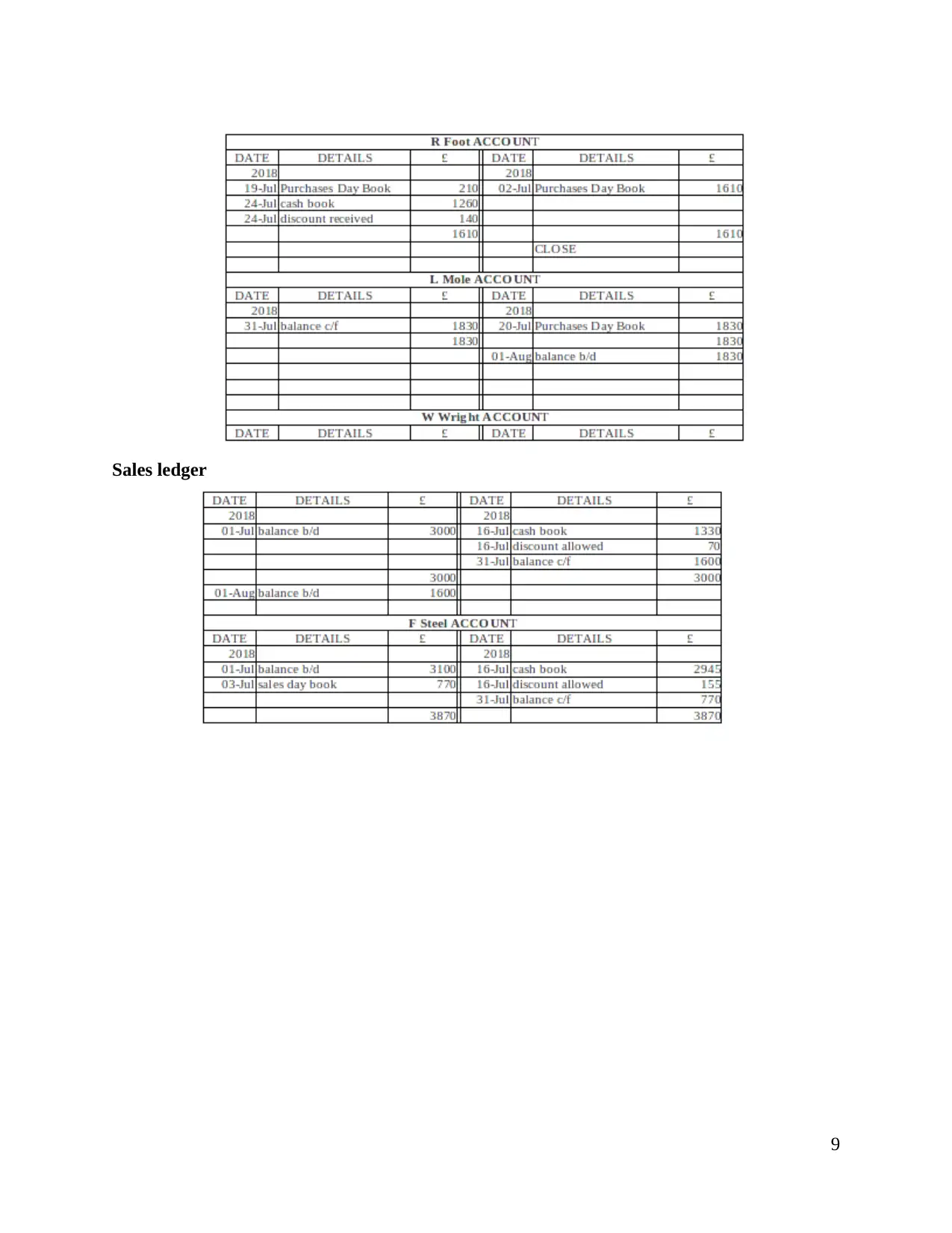

Purchase ledger

7

Purchase ledger

7

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

8

Sales ledger

9

9

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 29

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2025 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.