Evaluating M&C Plc Financial Performance: A Ratio Analysis (2015-2016)

VerifiedAdded on 2020/07/23

|12

|1744

|290

Report

AI Summary

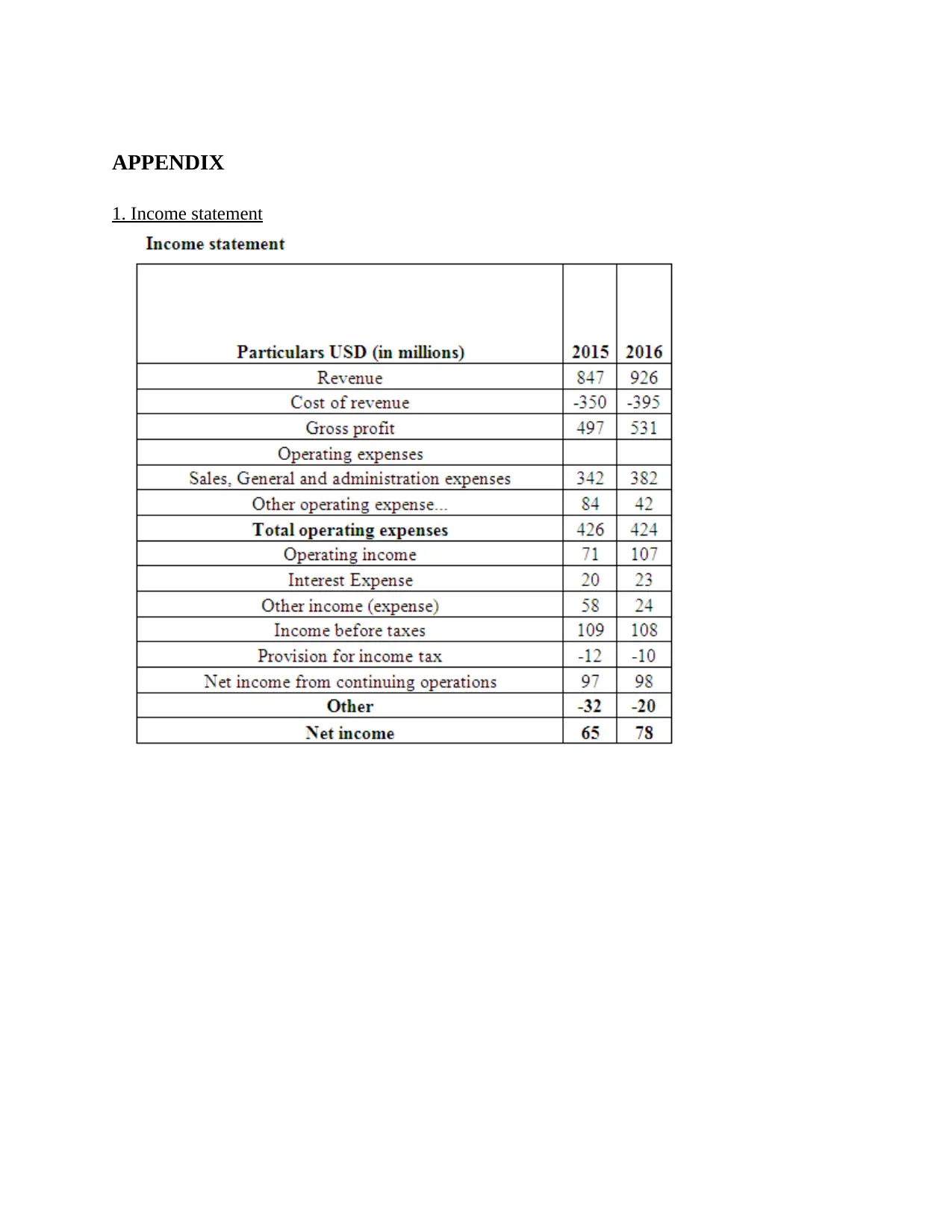

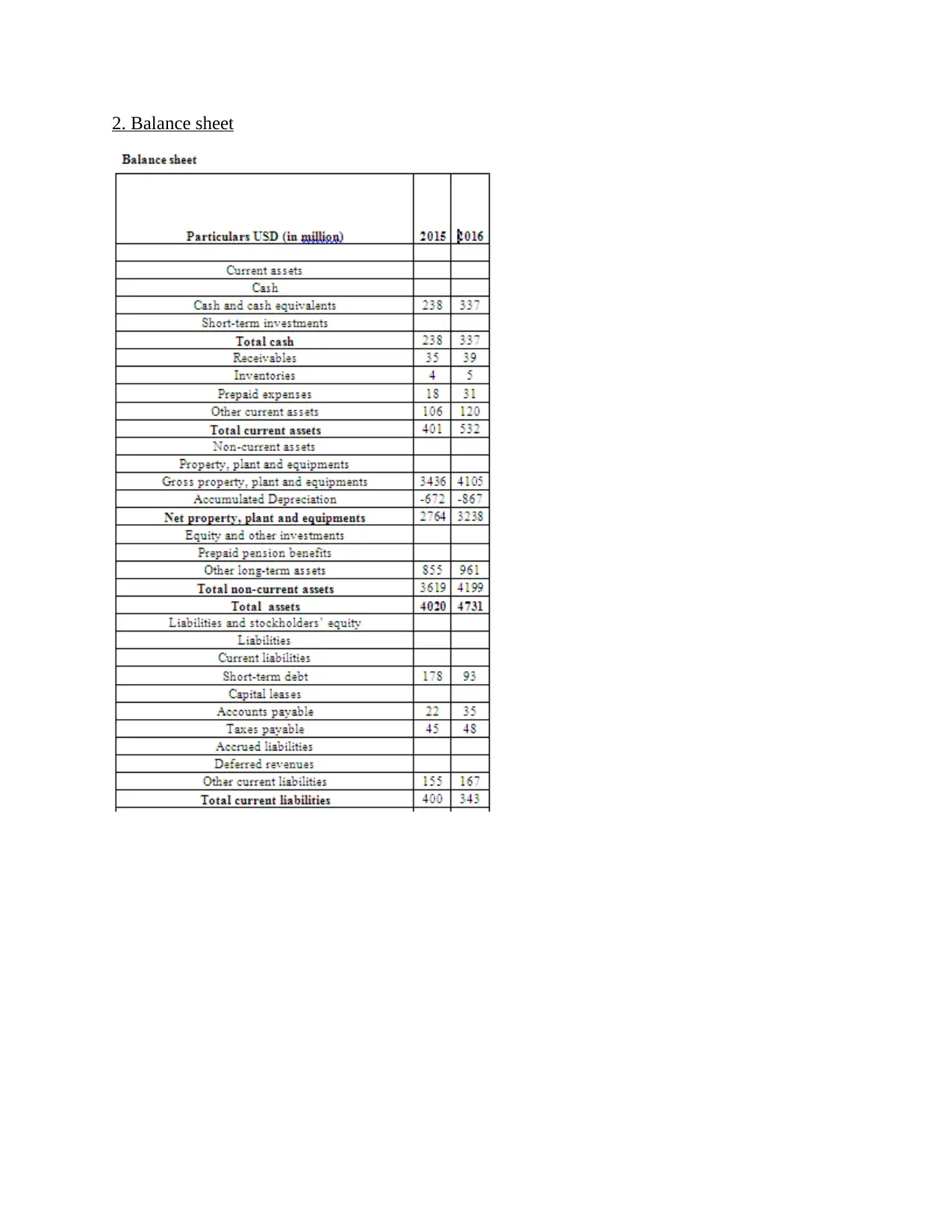

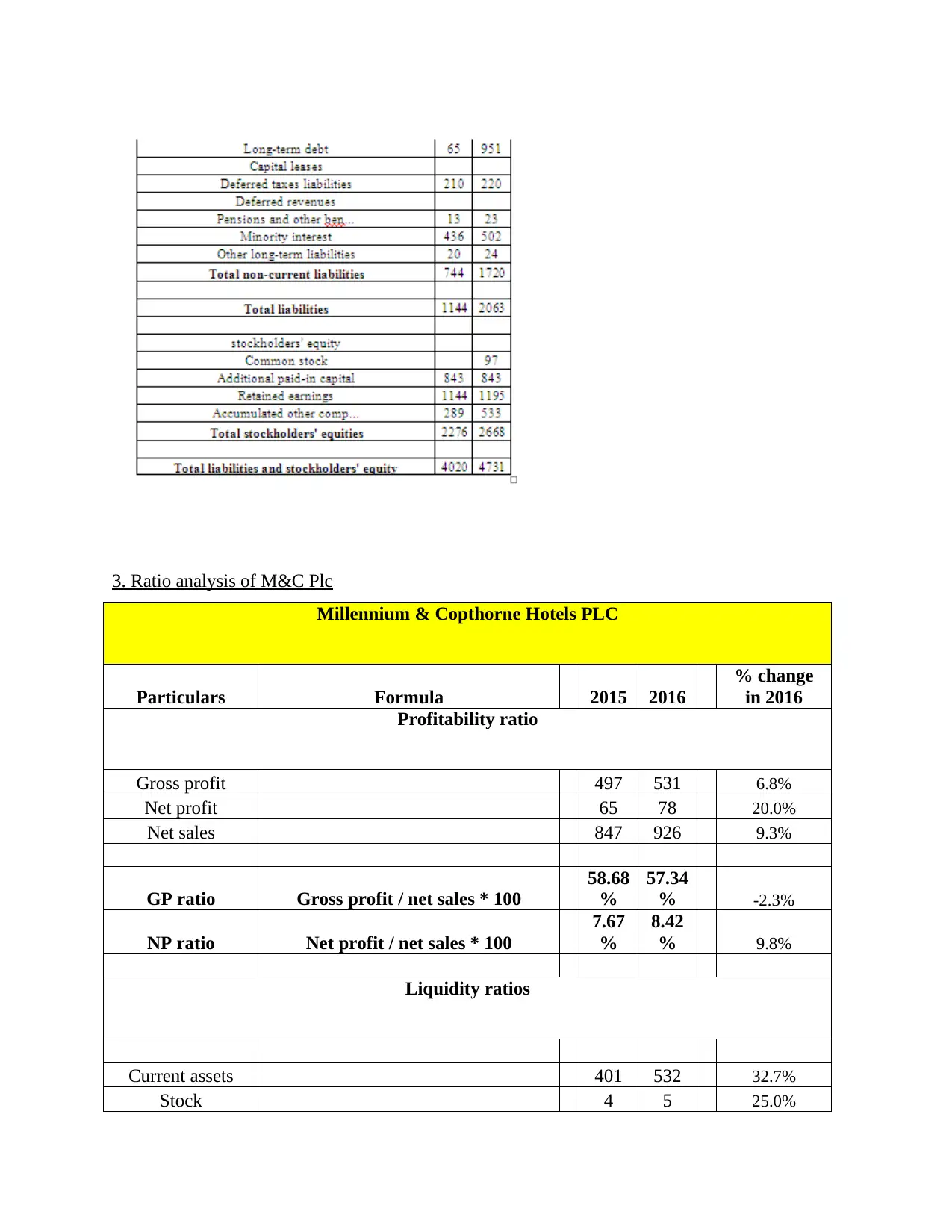

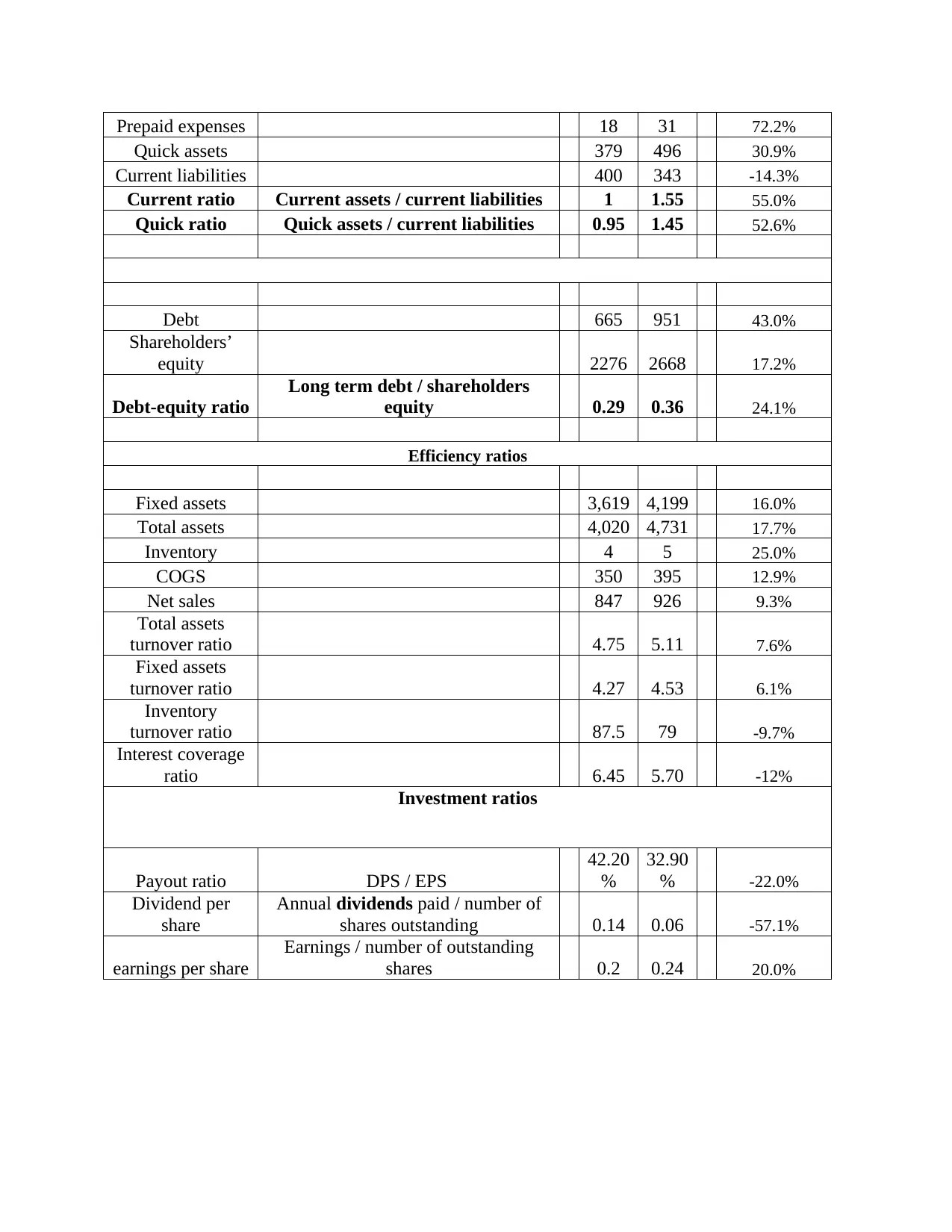

This report presents a financial analysis of Millennium & Copthorne Hotels PLC (M&C Plc) for the fiscal years 2015 and 2016. It evaluates the company's performance and financial position using ratio analysis, covering profitability (gross profit margin, net profit margin), liquidity (current ratio, quick ratio), solvency (debt-equity ratio), efficiency (inventory turnover, total assets turnover, fixed assets turnover), and investment ratios (payout ratio, dividend per share, earnings per share). The analysis reveals insights into M&C Plc's financial health, identifying trends and areas of improvement. The report also critically analyzes the views of Aerts and Walton (2017) on ratio analysis and its application in assessing a company's financial standing, while also considering the limitations of using past data to predict future performance. The report concludes with recommendations for strategic and policy frameworks to enhance M&C Plc's financial position and performance.

1 out of 12

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2025 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.