Financial Ratio Analysis

VerifiedAdded on 2020/02/24

|14

|2284

|120

AI Summary

This assignment provides a comprehensive financial ratio analysis for a company spanning the years 2013 to 2016. The analysis covers various key ratios across different categories, including profitability (Return on Total Assets), solvency (Debt-Equity Ratio, Interest Coverage Ratio), and efficiency (Receivable Turnover Ratio, Creditor Turnover Ratio, Inventory Turnover Ratio, Asset Turnover Ratio). Additionally, the document includes a calculation of Return on Capital Invested (ROCI) for each year.

Contribute Materials

Your contribution can guide someone’s learning journey. Share your

documents today.

Running head: BUSINESS VALUATION AND ANALYSIS

Business Valuation and Analysis

Name of the Student:

Name of the University:

Author Note:

Business Valuation and Analysis

Name of the Student:

Name of the University:

Author Note:

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

2BUSINESS VALUATION AND ANALYSIS

Table of Contents

Porter’s Five Forces Model of Qantas Airways Limited.................................................................2

SWOT Analysis of Qantas Airways Limited..................................................................................3

Corporate strategy of Qantas Airways Limited...............................................................................3

Accounting Policy...........................................................................................................................4

Financial Performance of Qantas Airways Limited at the end of 2013..........................................5

Financial Performance of Qantas Airways Limited for 2015 and 2016..........................................7

Analysis the data of 2013, 2015 and 2016.......................................................................................7

Recommendations and conclusion..................................................................................................8

Reference List..................................................................................................................................9

Appendix........................................................................................................................................10

Table of Contents

Porter’s Five Forces Model of Qantas Airways Limited.................................................................2

SWOT Analysis of Qantas Airways Limited..................................................................................3

Corporate strategy of Qantas Airways Limited...............................................................................3

Accounting Policy...........................................................................................................................4

Financial Performance of Qantas Airways Limited at the end of 2013..........................................5

Financial Performance of Qantas Airways Limited for 2015 and 2016..........................................7

Analysis the data of 2013, 2015 and 2016.......................................................................................7

Recommendations and conclusion..................................................................................................8

Reference List..................................................................................................................................9

Appendix........................................................................................................................................10

3BUSINESS VALUATION AND ANALYSIS

Porter’s Five Forces Model of Qantas Airways Limited

Rivalry from competitors- From the case study of Qantas Airways Limited, it is noted

that there is fewer firms in the Australian aviation industry and none of them can equalize

Qantas Airways Limited in terms of performance, profitability as well as market share

(Qantas.com 2017).

Threats from new entrants- From the case study of Qantas Airways Limited, it is noted

that different firms are trying to enter in the market to give a high level of competition to

the airline industry. Furthermore, threat from new entrants is quite less for Qantas

Airways Limited (Trugman 2016).

Threats of substitute products- From the case study of Qantas Airways Limited, it is

noted that different substitutes are available in the current marketplace. Threat from

substitute products is quite less to Qantas Airways Limited.

Bargaining power of suppliers- From the case study of Qantas Airways Limited, it is

noted that different war materials are needed, where fuel and aircrafts is the essential

element. Qantas Airways Limited is taking the product from one of the biggest supplier

in the marketplace that act as main strength of the company.

Bargaining power of buyers- The bargaining power of buyers shows about the buyer

power for influencing the price as well as other factors. From the case study of Qantas

Airways Limited, clients are available in the market and firms for serving them so that

buyers have the power to influence the price as well as operations of the company.

Porter’s Five Forces Model of Qantas Airways Limited

Rivalry from competitors- From the case study of Qantas Airways Limited, it is noted

that there is fewer firms in the Australian aviation industry and none of them can equalize

Qantas Airways Limited in terms of performance, profitability as well as market share

(Qantas.com 2017).

Threats from new entrants- From the case study of Qantas Airways Limited, it is noted

that different firms are trying to enter in the market to give a high level of competition to

the airline industry. Furthermore, threat from new entrants is quite less for Qantas

Airways Limited (Trugman 2016).

Threats of substitute products- From the case study of Qantas Airways Limited, it is

noted that different substitutes are available in the current marketplace. Threat from

substitute products is quite less to Qantas Airways Limited.

Bargaining power of suppliers- From the case study of Qantas Airways Limited, it is

noted that different war materials are needed, where fuel and aircrafts is the essential

element. Qantas Airways Limited is taking the product from one of the biggest supplier

in the marketplace that act as main strength of the company.

Bargaining power of buyers- The bargaining power of buyers shows about the buyer

power for influencing the price as well as other factors. From the case study of Qantas

Airways Limited, clients are available in the market and firms for serving them so that

buyers have the power to influence the price as well as operations of the company.

4BUSINESS VALUATION AND ANALYSIS

SWOT Analysis of Qantas Airways Limited

Strengths Weakness

Oldest airline in Australia

High market share in Australia

20 domestic and global destinations

Monopoly in airline sector

Huge Sponsorship

Advertising campaign

Strong backing of Australian Government

Issue with employee or human resources

Too much concentration around Australasia

Opportunities Threats

Investors attractiveness

Advancement of technology

Asian different tourist destination

Joint venture with international brands

High fuel prices

Intense competition in the market because of new

entrants

High labor cost

Corporate strategy of Qantas Airways Limited

From the case study of Qantas Airways Limited, it is noted that the company need to

investigate over the corporate strategy of the business. There are different factors that relates to

the corporate strategy of Qantas Airways Limited. Qantas Airways Limited has come into

existence in the year 1920 and plans for opting strategies for managing the business as well as

enhancing the growth (Sheth and Sisodia 2015).

SWOT Analysis of Qantas Airways Limited

Strengths Weakness

Oldest airline in Australia

High market share in Australia

20 domestic and global destinations

Monopoly in airline sector

Huge Sponsorship

Advertising campaign

Strong backing of Australian Government

Issue with employee or human resources

Too much concentration around Australasia

Opportunities Threats

Investors attractiveness

Advancement of technology

Asian different tourist destination

Joint venture with international brands

High fuel prices

Intense competition in the market because of new

entrants

High labor cost

Corporate strategy of Qantas Airways Limited

From the case study of Qantas Airways Limited, it is noted that the company need to

investigate over the corporate strategy of the business. There are different factors that relates to

the corporate strategy of Qantas Airways Limited. Qantas Airways Limited has come into

existence in the year 1920 and plans for opting strategies for managing the business as well as

enhancing the growth (Sheth and Sisodia 2015).

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

5BUSINESS VALUATION AND ANALYSIS

After 1992, Qantas Airways Limited has made many changes into its strategy,

functioning, operations as well as technology and sources for managing and enhancing the

performance and profitability of the business. It is noted that the company has adopted two

strategies for managing the performance as well as profitability of the business. The company

has used international expansion strategy as well as diversification strategy for the business

enterprise (Armstrong et al. 2015).

Till now, Qantas Airways Limited had already operated its business into 42 countries

with 173 offices and 35000 employees. Most of the business operations had started to

management the performance like budget airlines, Jetstar, Qantas holidays and Qantas catering

for evaluating the situation of the business firm (Sekaran and Bougie 2016).

Accounting Policy

From the case study of Qantas Airways Limited, it had been analyzed that the company is

peppering the final financial data at the time of analyzing the different point of view in relation

to the company for managing the reports based on accounting policies.

Revenue and expenses recognition

The rules of IFRS and US GAAP explain that an association needs to be identified in the

income and expenses based on market value in the income statement. In addition, revenue is

identified of an association that could be understood by the Business Corporation of trading of

products or services such as sales, interest income, long-term gains and short-term profits where

expense is calculated as loss of an association that can be paid by the Business Corporation at the

time of trading products and services such as labor, operational expenses and cost of goods sold

After 1992, Qantas Airways Limited has made many changes into its strategy,

functioning, operations as well as technology and sources for managing and enhancing the

performance and profitability of the business. It is noted that the company has adopted two

strategies for managing the performance as well as profitability of the business. The company

has used international expansion strategy as well as diversification strategy for the business

enterprise (Armstrong et al. 2015).

Till now, Qantas Airways Limited had already operated its business into 42 countries

with 173 offices and 35000 employees. Most of the business operations had started to

management the performance like budget airlines, Jetstar, Qantas holidays and Qantas catering

for evaluating the situation of the business firm (Sekaran and Bougie 2016).

Accounting Policy

From the case study of Qantas Airways Limited, it had been analyzed that the company is

peppering the final financial data at the time of analyzing the different point of view in relation

to the company for managing the reports based on accounting policies.

Revenue and expenses recognition

The rules of IFRS and US GAAP explain that an association needs to be identified in the

income and expenses based on market value in the income statement. In addition, revenue is

identified of an association that could be understood by the Business Corporation of trading of

products or services such as sales, interest income, long-term gains and short-term profits where

expense is calculated as loss of an association that can be paid by the Business Corporation at the

time of trading products and services such as labor, operational expenses and cost of goods sold

6BUSINESS VALUATION AND ANALYSIS

(Peñaloza, Toulouse and Visconti 2013). Therefore, the accounting rules show that the expenses

should be recorded in the debit column and income needs to be recorded in the credit column in

the income statement.

Asset and liability recording

The rule of IFRS and US GAAP show that an association should identify overall asset as

well as liabilities based on market value in the balance sheet, where assets is recognized as

economical profit of business that need to be converted by the Business Corporation based on

nature of assets (Meffert 2013). The short-term asset is that asset that can be converted in a year

and long-term asset need some time like plants and debtors. On the other hand, liability is

recorded as debt of an association can be converted by the Business Corporation based on the

nature of liability. Therefore, double entry accounting system is helpful where total asset equals

liability and capital of business enterprise.

Financial Performance of Qantas Airways Limited at the end of 2013

Liquidity ratio 2013

Current ratio 0.823390895

Quick ratio 0.709105181

Working capital -1,125.0

Profitability Ratios 2013

Operating Profit Margin 0.002182705

Net Profit Margin 0.000320986

Return on Capital Employed 0.0

Return on Equity 0.000841184

Return on Total assets 0.000247525

Capital structure ratio 2013

(Peñaloza, Toulouse and Visconti 2013). Therefore, the accounting rules show that the expenses

should be recorded in the debit column and income needs to be recorded in the credit column in

the income statement.

Asset and liability recording

The rule of IFRS and US GAAP show that an association should identify overall asset as

well as liabilities based on market value in the balance sheet, where assets is recognized as

economical profit of business that need to be converted by the Business Corporation based on

nature of assets (Meffert 2013). The short-term asset is that asset that can be converted in a year

and long-term asset need some time like plants and debtors. On the other hand, liability is

recorded as debt of an association can be converted by the Business Corporation based on the

nature of liability. Therefore, double entry accounting system is helpful where total asset equals

liability and capital of business enterprise.

Financial Performance of Qantas Airways Limited at the end of 2013

Liquidity ratio 2013

Current ratio 0.823390895

Quick ratio 0.709105181

Working capital -1,125.0

Profitability Ratios 2013

Operating Profit Margin 0.002182705

Net Profit Margin 0.000320986

Return on Capital Employed 0.0

Return on Equity 0.000841184

Return on Total assets 0.000247525

Capital structure ratio 2013

7BUSINESS VALUATION AND ANALYSIS

Debt- equity 2.398384926

Interest coverage ratio 0.057432432

Efficiency ratio 2013

Receivable turnover ratio

Creditor turnover ratio

Inventory turnover ratio

Assets turnover ratio

Particular 2013

ROCI

-

100.3846154

The financial data of the company for the year 2013 depict ways for identifying the level

of performance of the company based on finance. Most of the ratio had been calculated for

identifying liquidity, efficiency, profitability and solvency position of Qantas Airways Limited.

On analysis, it is noted that current ratio of Qantas Airways Limited depict a bad liquidity

position for the company that reveals the fact where company cannot repay their short-term debt

obligations for specified time. In addition, the quick ratio of Qantas Airways Limited shows a

bad position in the year 2013. Overall, the working capital of Qantas Airways Limited is

negative that show that company need to make some changes so that they can sustain in the long-

run (Keller and Kotler 2016).

Profitability ratio help in predicting the profitability position of any business enterprise.

On analysis, it is noted that Qantas Airways Limited is earning very less profit from the market

that restrict the company to work smoothly in the near future.

Debt- equity 2.398384926

Interest coverage ratio 0.057432432

Efficiency ratio 2013

Receivable turnover ratio

Creditor turnover ratio

Inventory turnover ratio

Assets turnover ratio

Particular 2013

ROCI

-

100.3846154

The financial data of the company for the year 2013 depict ways for identifying the level

of performance of the company based on finance. Most of the ratio had been calculated for

identifying liquidity, efficiency, profitability and solvency position of Qantas Airways Limited.

On analysis, it is noted that current ratio of Qantas Airways Limited depict a bad liquidity

position for the company that reveals the fact where company cannot repay their short-term debt

obligations for specified time. In addition, the quick ratio of Qantas Airways Limited shows a

bad position in the year 2013. Overall, the working capital of Qantas Airways Limited is

negative that show that company need to make some changes so that they can sustain in the long-

run (Keller and Kotler 2016).

Profitability ratio help in predicting the profitability position of any business enterprise.

On analysis, it is noted that Qantas Airways Limited is earning very less profit from the market

that restrict the company to work smoothly in the near future.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

8BUSINESS VALUATION AND ANALYSIS

Capital structure ratio reveals that debts of Qantas Airways Limited are quite higher than

the assets of the company that need changes. Efficiency ratio of Qantas Airways Limited shows

bad efficiency and it is suggested that the company should make some changes during the

recovery days for maintaining the working capital at accepted level (Hollensen 2015).

Financial Performance of Qantas Airways Limited for 2015 and 2016

Liquidity ratio 2016 2015

Current ratio 0.492031873 0.675903614

Quick ratio 0.396414343 0.589692102

Working capital -3,570.0 -2,421.0

Profitability Ratios 2016 2015

Operating Profit Margin 0.180435884 0.101596704

Net Profit Margin 0.0651926 0.035861447

Return on Capital Employed 0.3 0.2

Return on Equity 0.316615385 0.162059936

Return on Total assets 0.061598324 0.031774102

Capital structure ratio 2016 2015

Debt- equity 4.14 4.100378237

Interest coverage ratio 5.014084507 2.260744986

Efficiency ratio 2016 2015

Receivable turnover ratio 17.9977195 14.41484919

Creditor turnover ratio 5.214511041 12.28374893

Inventory turnover ratio 20.09726444 22.35680751

Assets turnover ratio 0.922097269 0.891414141

Computation of return on capital invested

Particular 2016 2015

ROCI

-

268.0327869

-

47.05372617

Capital structure ratio reveals that debts of Qantas Airways Limited are quite higher than

the assets of the company that need changes. Efficiency ratio of Qantas Airways Limited shows

bad efficiency and it is suggested that the company should make some changes during the

recovery days for maintaining the working capital at accepted level (Hollensen 2015).

Financial Performance of Qantas Airways Limited for 2015 and 2016

Liquidity ratio 2016 2015

Current ratio 0.492031873 0.675903614

Quick ratio 0.396414343 0.589692102

Working capital -3,570.0 -2,421.0

Profitability Ratios 2016 2015

Operating Profit Margin 0.180435884 0.101596704

Net Profit Margin 0.0651926 0.035861447

Return on Capital Employed 0.3 0.2

Return on Equity 0.316615385 0.162059936

Return on Total assets 0.061598324 0.031774102

Capital structure ratio 2016 2015

Debt- equity 4.14 4.100378237

Interest coverage ratio 5.014084507 2.260744986

Efficiency ratio 2016 2015

Receivable turnover ratio 17.9977195 14.41484919

Creditor turnover ratio 5.214511041 12.28374893

Inventory turnover ratio 20.09726444 22.35680751

Assets turnover ratio 0.922097269 0.891414141

Computation of return on capital invested

Particular 2016 2015

ROCI

-

268.0327869

-

47.05372617

9BUSINESS VALUATION AND ANALYSIS

The financial data of Qantas Airways Limited for the year 2015 and 2016 had been

analyzed for identifying the performance of the company based on finance (Foxall 2014).

Analysis the data of 2013, 2015 and 2016

By conducting the study of Qantas Airways Limited for the three years (2013, 2015 and

2016), it is noted that Qantas Airways Limited faced many issues in the last two years because of

internal and external factors. In addition, it is analyzed that different strategies have been adopted

by Qantas Airways Limited for enhancing the level of performance. The study shows that the

performance of Qantas Airways Limited is similar to that for year 2013 and 2015, 2016. It is

noted that the liquidity position of Qantas Airways Limited is even similar over the years. The

company is facing issue in meeting the short-term debt obligations. It is noted that Qantas

Airways Limited is still not able to enjoy high profits (Goworek and McGoldrick 2015).

Recommendations and conclusion

At the end of the case study, it is concluded that Qantas Airways Limited is required to

make some changes into the financial as well as non-financial figures for enhancing the level of

performance. Qantas Airways Limited operates in aviation industry but faces external and

internal issue that reveals that the performance of the company has been lowered. It is suggested

to Qantas Airways Limited to make some changes into the operations for enhancing the level of

performance.

The financial data of Qantas Airways Limited for the year 2015 and 2016 had been

analyzed for identifying the performance of the company based on finance (Foxall 2014).

Analysis the data of 2013, 2015 and 2016

By conducting the study of Qantas Airways Limited for the three years (2013, 2015 and

2016), it is noted that Qantas Airways Limited faced many issues in the last two years because of

internal and external factors. In addition, it is analyzed that different strategies have been adopted

by Qantas Airways Limited for enhancing the level of performance. The study shows that the

performance of Qantas Airways Limited is similar to that for year 2013 and 2015, 2016. It is

noted that the liquidity position of Qantas Airways Limited is even similar over the years. The

company is facing issue in meeting the short-term debt obligations. It is noted that Qantas

Airways Limited is still not able to enjoy high profits (Goworek and McGoldrick 2015).

Recommendations and conclusion

At the end of the case study, it is concluded that Qantas Airways Limited is required to

make some changes into the financial as well as non-financial figures for enhancing the level of

performance. Qantas Airways Limited operates in aviation industry but faces external and

internal issue that reveals that the performance of the company has been lowered. It is suggested

to Qantas Airways Limited to make some changes into the operations for enhancing the level of

performance.

10BUSINESS VALUATION AND ANALYSIS

Reference List

Armstrong, G., Kotler, P., Harker, M. and Brennan, R., 2015. Marketing: an introduction.

Pearson Education.

Foxall, G., 2014. Strategic Marketing Management (RLE Marketing) (Vol. 3). Routledge.

Goworek, H. and McGoldrick, P., 2015. Retail marketing management: Principles and practice.

Pearson Higher Ed.

Hollensen, S., 2015. Marketing management: A relationship approach. Pearson Education

Keller, K.L. and Kotler, P., 2016. Marketing management. Pearson.

Meffert, H., 2013. Marketing-Management: Analyse—Strategie—Implementierung. Springer-

Verlag.

Peñaloza, L., Toulouse, N. and Visconti, L.M. eds., 2013. Marketing management: A cultural

perspective. Routledge.

Qantas.com. 2017. Flights to Australia, New Zealand and Dubai | Qantas UK. [online] Available

at: http://www.qantas.com [Accessed 25 Aug. 2017].

Sekaran, U. and Bougie, R., 2016. Research methods for business: A skill building approach.

John Wiley & Sons.

Sheth, J.N. and Sisodia, R.S., 2015. Does marketing need reform?: Fresh perspectives on the

future. Routledge.

Reference List

Armstrong, G., Kotler, P., Harker, M. and Brennan, R., 2015. Marketing: an introduction.

Pearson Education.

Foxall, G., 2014. Strategic Marketing Management (RLE Marketing) (Vol. 3). Routledge.

Goworek, H. and McGoldrick, P., 2015. Retail marketing management: Principles and practice.

Pearson Higher Ed.

Hollensen, S., 2015. Marketing management: A relationship approach. Pearson Education

Keller, K.L. and Kotler, P., 2016. Marketing management. Pearson.

Meffert, H., 2013. Marketing-Management: Analyse—Strategie—Implementierung. Springer-

Verlag.

Peñaloza, L., Toulouse, N. and Visconti, L.M. eds., 2013. Marketing management: A cultural

perspective. Routledge.

Qantas.com. 2017. Flights to Australia, New Zealand and Dubai | Qantas UK. [online] Available

at: http://www.qantas.com [Accessed 25 Aug. 2017].

Sekaran, U. and Bougie, R., 2016. Research methods for business: A skill building approach.

John Wiley & Sons.

Sheth, J.N. and Sisodia, R.S., 2015. Does marketing need reform?: Fresh perspectives on the

future. Routledge.

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

11BUSINESS VALUATION AND ANALYSIS

Trugman, 2016. Understanding business valuation: A practical guide to valuing small to medium

sized businesses. John Wiley & Sons.

Trugman, 2016. Understanding business valuation: A practical guide to valuing small to medium

sized businesses. John Wiley & Sons.

12BUSINESS VALUATION AND ANALYSIS

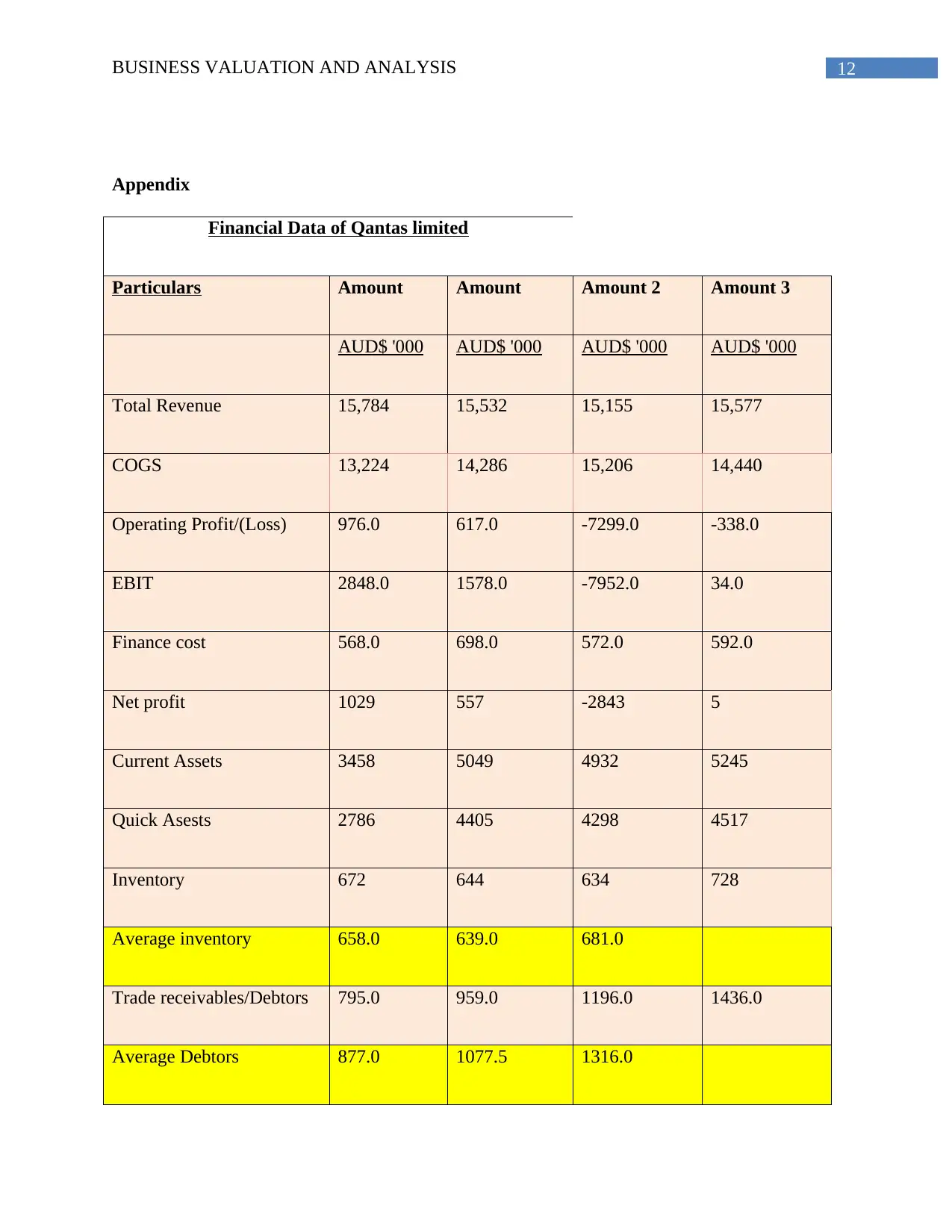

Appendix

Financial Data of Qantas limited

Particulars Amount Amount Amount 2 Amount 3

AUD$ '000 AUD$ '000 AUD$ '000 AUD$ '000

Total Revenue 15,784 15,532 15,155 15,577

COGS 13,224 14,286 15,206 14,440

Operating Profit/(Loss) 976.0 617.0 -7299.0 -338.0

EBIT 2848.0 1578.0 -7952.0 34.0

Finance cost 568.0 698.0 572.0 592.0

Net profit 1029 557 -2843 5

Current Assets 3458 5049 4932 5245

Quick Asests 2786 4405 4298 4517

Inventory 672 644 634 728

Average inventory 658.0 639.0 681.0

Trade receivables/Debtors 795.0 959.0 1196.0 1436.0

Average Debtors 877.0 1077.5 1316.0

Appendix

Financial Data of Qantas limited

Particulars Amount Amount Amount 2 Amount 3

AUD$ '000 AUD$ '000 AUD$ '000 AUD$ '000

Total Revenue 15,784 15,532 15,155 15,577

COGS 13,224 14,286 15,206 14,440

Operating Profit/(Loss) 976.0 617.0 -7299.0 -338.0

EBIT 2848.0 1578.0 -7952.0 34.0

Finance cost 568.0 698.0 572.0 592.0

Net profit 1029 557 -2843 5

Current Assets 3458 5049 4932 5245

Quick Asests 2786 4405 4298 4517

Inventory 672 644 634 728

Average inventory 658.0 639.0 681.0

Trade receivables/Debtors 795.0 959.0 1196.0 1436.0

Average Debtors 877.0 1077.5 1316.0

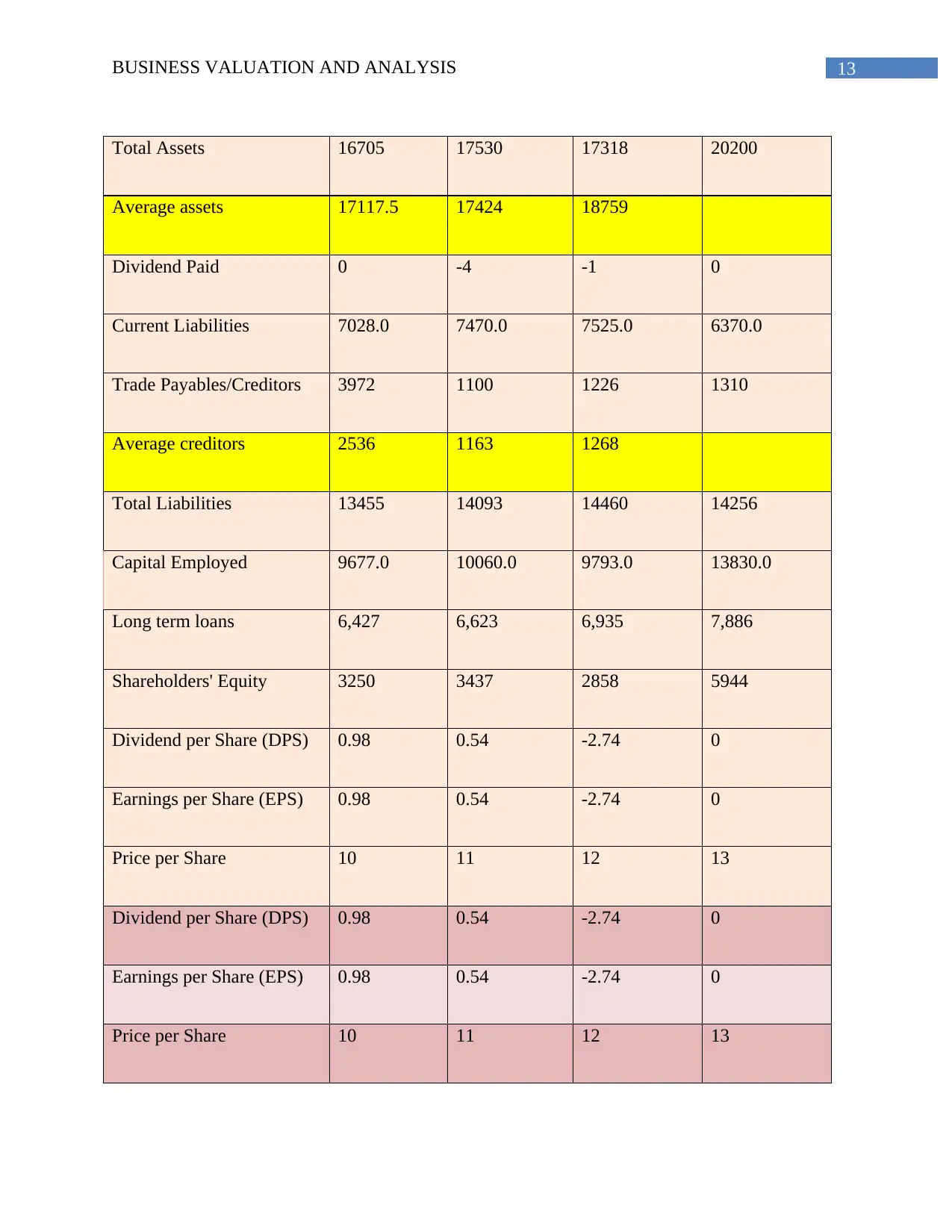

13BUSINESS VALUATION AND ANALYSIS

Total Assets 16705 17530 17318 20200

Average assets 17117.5 17424 18759

Dividend Paid 0 -4 -1 0

Current Liabilities 7028.0 7470.0 7525.0 6370.0

Trade Payables/Creditors 3972 1100 1226 1310

Average creditors 2536 1163 1268

Total Liabilities 13455 14093 14460 14256

Capital Employed 9677.0 10060.0 9793.0 13830.0

Long term loans 6,427 6,623 6,935 7,886

Shareholders' Equity 3250 3437 2858 5944

Dividend per Share (DPS) 0.98 0.54 -2.74 0

Earnings per Share (EPS) 0.98 0.54 -2.74 0

Price per Share 10 11 12 13

Dividend per Share (DPS) 0.98 0.54 -2.74 0

Earnings per Share (EPS) 0.98 0.54 -2.74 0

Price per Share 10 11 12 13

Total Assets 16705 17530 17318 20200

Average assets 17117.5 17424 18759

Dividend Paid 0 -4 -1 0

Current Liabilities 7028.0 7470.0 7525.0 6370.0

Trade Payables/Creditors 3972 1100 1226 1310

Average creditors 2536 1163 1268

Total Liabilities 13455 14093 14460 14256

Capital Employed 9677.0 10060.0 9793.0 13830.0

Long term loans 6,427 6,623 6,935 7,886

Shareholders' Equity 3250 3437 2858 5944

Dividend per Share (DPS) 0.98 0.54 -2.74 0

Earnings per Share (EPS) 0.98 0.54 -2.74 0

Price per Share 10 11 12 13

Dividend per Share (DPS) 0.98 0.54 -2.74 0

Earnings per Share (EPS) 0.98 0.54 -2.74 0

Price per Share 10 11 12 13

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

14BUSINESS VALUATION AND ANALYSIS

Computation of ratio analyis

Liquidity ratio 2016 2015 2014 2013

Current ratio 0.492031873 0.675903614 0.655415282 0.823390895

Quick ratio 0.396414343 0.589692102 0.571162791 0.709105181

Working capital -3,570.0 -2,421.0 -2,593.0 -1,125.0

Profitability Ratios 2016 2015 2014 2013

Operating Profit Margin 0.180435884 0.101596704 -0.524711316 0.002182705

Net Profit Margin 0.0651926 0.035861447 -0.187594853 0.000320986

Return on Capital

Employed 0.3 0.2 -0.8 0.0

Return on Equity 0.316615385 0.162059936 -0.994751575 0.000841184

Return on Total assets 0.061598324 0.031774102 -0.164164453 0.000247525

Debt equity ratio

Capital structure ratio 2016 2015 2014 2013

Debt- equity 4.14 4.100378237 5.059482155 2.398384926

Computation of ratio analyis

Liquidity ratio 2016 2015 2014 2013

Current ratio 0.492031873 0.675903614 0.655415282 0.823390895

Quick ratio 0.396414343 0.589692102 0.571162791 0.709105181

Working capital -3,570.0 -2,421.0 -2,593.0 -1,125.0

Profitability Ratios 2016 2015 2014 2013

Operating Profit Margin 0.180435884 0.101596704 -0.524711316 0.002182705

Net Profit Margin 0.0651926 0.035861447 -0.187594853 0.000320986

Return on Capital

Employed 0.3 0.2 -0.8 0.0

Return on Equity 0.316615385 0.162059936 -0.994751575 0.000841184

Return on Total assets 0.061598324 0.031774102 -0.164164453 0.000247525

Debt equity ratio

Capital structure ratio 2016 2015 2014 2013

Debt- equity 4.14 4.100378237 5.059482155 2.398384926

1 out of 14

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

© 2024 | Zucol Services PVT LTD | All rights reserved.