Detailed Financial Ratio Analysis Report of ASOS plc (2019-2020)

VerifiedAdded on 2023/06/12

|6

|1198

|195

Report

AI Summary

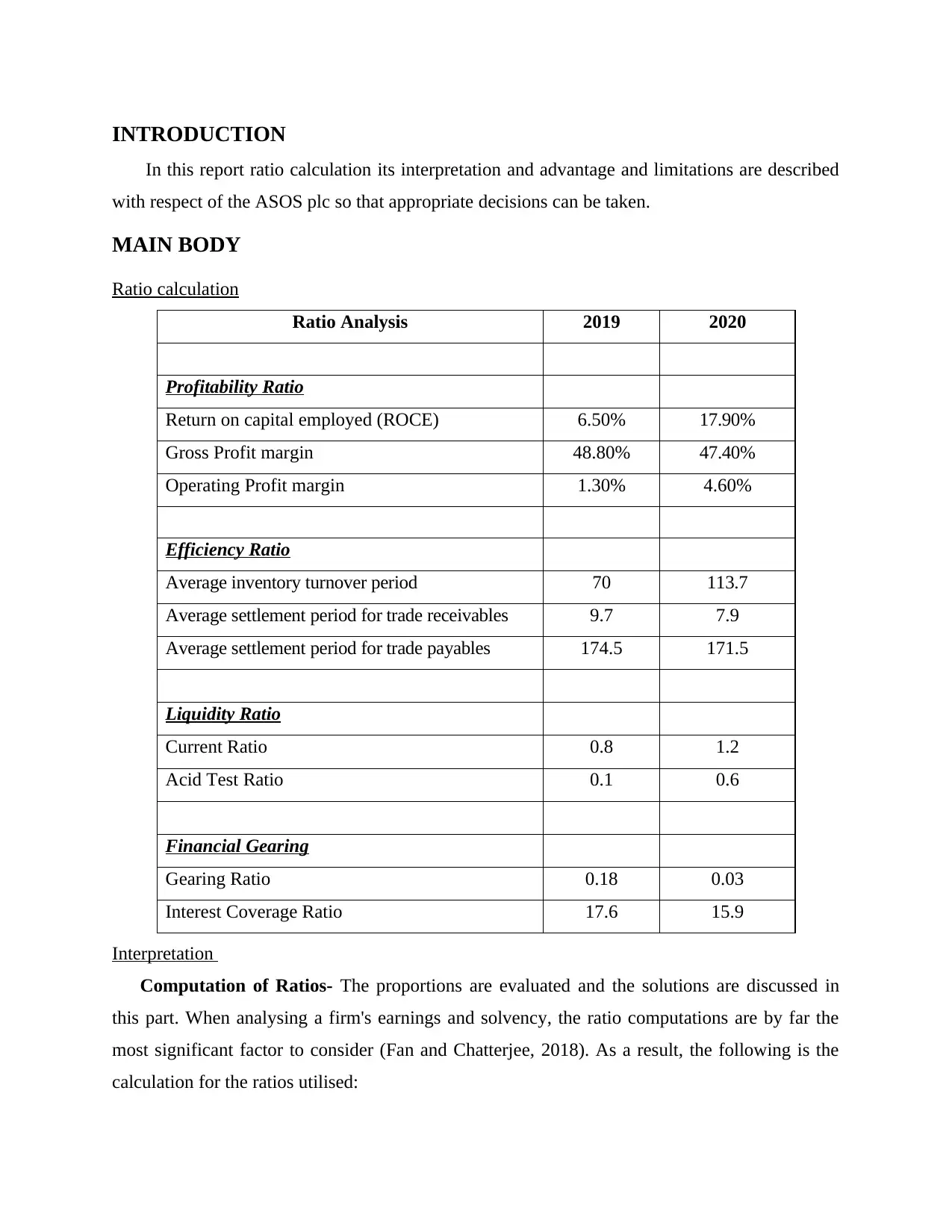

This report provides a financial ratio analysis of ASOS plc for the years 2019 and 2020. It includes calculations and interpretations of key ratios such as Return on Capital Employed (ROCE), Gross Profit Margin, Operating Profit Margin, Inventory Turnover Period, Average Settlement Periods for Trade Receivables and Payables, Current Ratio, Acid Test Ratio, Gearing Ratio, and Interest Coverage Ratio. The analysis indicates improvements in ROCE, Operating Profit Margin, and Current Ratio, suggesting better financial health. However, the Gross Profit Margin decreased slightly. The report also discusses the advantages and limitations of using financial ratios for decision-making, concluding that while ratios offer valuable insights, they should be used cautiously due to the unpredictable nature of future events. Desklib offers a platform to explore this and similar solved assignments.

1 out of 6

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2025 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.