Financial Statement Analysis and Performance of Kellogg's Company

VerifiedAdded on 2019/12/03

|14

|3227

|337

Report

AI Summary

This report presents a comprehensive financial analysis of Kellogg's, a major player in the food manufacturing industry. It begins with an introduction to the company, its historical background, operational aspects, and competitive landscape, including market share and concentration. The analysis delves into the market price per share and prevailing market conditions, such as political, economic, social, technological, environmental, and legal factors (PESTLE analysis) influencing the company's performance. A thorough financial analysis follows, incorporating key financial ratios like profitability, liquidity, activity, and solvency ratios from 2010 to 2014. Each ratio is calculated, and its implications for Kellogg's financial health are interpreted. The report highlights strengths, weaknesses, opportunities, and threats (SWOT analysis), providing insights into the company's financial standing and potential areas for improvement. The conclusion summarizes the key findings, and recommendations are offered to enhance Kellogg's financial performance, supported by relevant references.

FINANCIAL

STATEMENT

ANALYSIS

STATEMENT

ANALYSIS

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

TABLE OF CONTENTS

FINANCIAL STATEMENT ANALYSIS......................................................................................1

Introduction......................................................................................................................................1

Brief history.................................................................................................................................1

Company operations....................................................................................................................1

Competitors..................................................................................................................................2

Market concentration...................................................................................................................3

Analysis...........................................................................................................................................4

Market price per share.................................................................................................................4

Market Conditions.......................................................................................................................4

Financial Analysis...........................................................................................................................6

Interpretation................................................................................................................................9

Conclusion.......................................................................................................................................9

Recommendations..........................................................................................................................10

References......................................................................................................................................11

FINANCIAL STATEMENT ANALYSIS......................................................................................1

Introduction......................................................................................................................................1

Brief history.................................................................................................................................1

Company operations....................................................................................................................1

Competitors..................................................................................................................................2

Market concentration...................................................................................................................3

Analysis...........................................................................................................................................4

Market price per share.................................................................................................................4

Market Conditions.......................................................................................................................4

Financial Analysis...........................................................................................................................6

Interpretation................................................................................................................................9

Conclusion.......................................................................................................................................9

Recommendations..........................................................................................................................10

References......................................................................................................................................11

Introduction

Financial information produced from the statements is of great importance for the

company and its various stakeholders. All of them fulfil their respective financial goals and

objectives. The purpose of this research report is to analyse the financial performance of an

organization named Kellog. It will analyse the impact of market conditions on the business

performance. At last the report will also do the ratio analysis for the business.

Brief history

Kellogg’s is an American multinational food manufacturing organization headquartered

in Battle Creek, Michigan in United States. The brand was founded as the Battle Creek Toasted

Corn Flake Company in the year 1906. From 1969 to 1977, it acquired various small businesses

including Salada Foods, Eggo, Fearn International, Pure Packed Food etc. In the year 2001 it

made its largest acquisition over the Keebler Company (Kellogs, Investors relations, 2014). In

the year 2012 the brand became the world’s largest snack food organization by acquiring the

Pringles potato chips brand from Procter & Gamble.

Company operations

Kellogg’s produced cereal, convenience foods, cookies, crackers, toaster pastries and

many other items. Some of the famous brands of the company are Froot Loops, Corn Flakes,

Rice Krispes, Eggo, Nutri-Grain etc. The products are manufactured in 18 countries and are

marketed in over 180 countries (Kellogs, Annual Reports, 2014). The largest factor for Kellogg’s

is at Trafford Park in Manchester, United Kingdom. The factory produces more cornflakes than

any other company’s factory across the world.

1

Financial information produced from the statements is of great importance for the

company and its various stakeholders. All of them fulfil their respective financial goals and

objectives. The purpose of this research report is to analyse the financial performance of an

organization named Kellog. It will analyse the impact of market conditions on the business

performance. At last the report will also do the ratio analysis for the business.

Brief history

Kellogg’s is an American multinational food manufacturing organization headquartered

in Battle Creek, Michigan in United States. The brand was founded as the Battle Creek Toasted

Corn Flake Company in the year 1906. From 1969 to 1977, it acquired various small businesses

including Salada Foods, Eggo, Fearn International, Pure Packed Food etc. In the year 2001 it

made its largest acquisition over the Keebler Company (Kellogs, Investors relations, 2014). In

the year 2012 the brand became the world’s largest snack food organization by acquiring the

Pringles potato chips brand from Procter & Gamble.

Company operations

Kellogg’s produced cereal, convenience foods, cookies, crackers, toaster pastries and

many other items. Some of the famous brands of the company are Froot Loops, Corn Flakes,

Rice Krispes, Eggo, Nutri-Grain etc. The products are manufactured in 18 countries and are

marketed in over 180 countries (Kellogs, Annual Reports, 2014). The largest factor for Kellogg’s

is at Trafford Park in Manchester, United Kingdom. The factory produces more cornflakes than

any other company’s factory across the world.

1

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

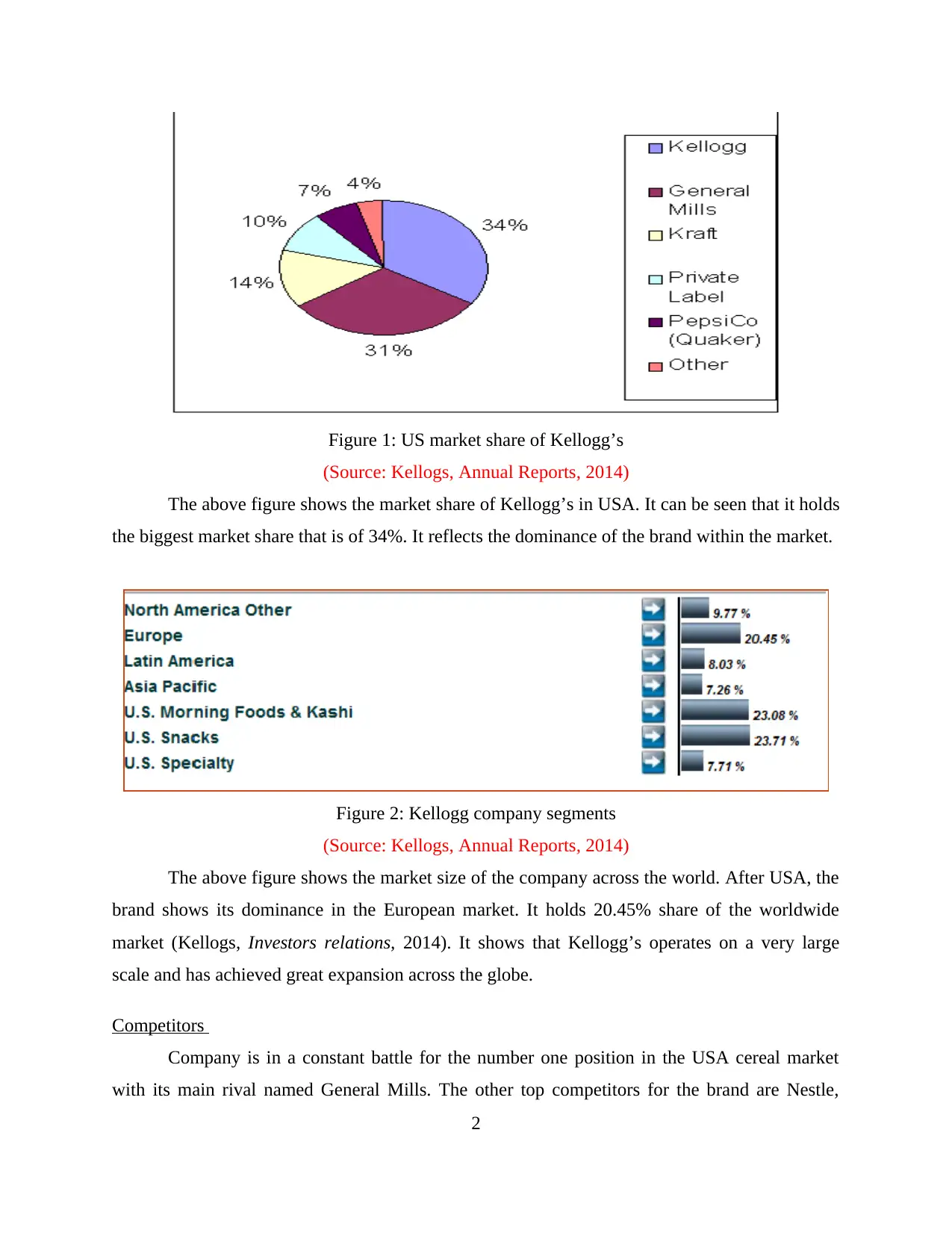

Figure 1: US market share of Kellogg’s

(Source: Kellogs, Annual Reports, 2014)

The above figure shows the market share of Kellogg’s in USA. It can be seen that it holds

the biggest market share that is of 34%. It reflects the dominance of the brand within the market.

Figure 2: Kellogg company segments

(Source: Kellogs, Annual Reports, 2014)

The above figure shows the market size of the company across the world. After USA, the

brand shows its dominance in the European market. It holds 20.45% share of the worldwide

market (Kellogs, Investors relations, 2014). It shows that Kellogg’s operates on a very large

scale and has achieved great expansion across the globe.

Competitors

Company is in a constant battle for the number one position in the USA cereal market

with its main rival named General Mills. The other top competitors for the brand are Nestle,

2

(Source: Kellogs, Annual Reports, 2014)

The above figure shows the market share of Kellogg’s in USA. It can be seen that it holds

the biggest market share that is of 34%. It reflects the dominance of the brand within the market.

Figure 2: Kellogg company segments

(Source: Kellogs, Annual Reports, 2014)

The above figure shows the market size of the company across the world. After USA, the

brand shows its dominance in the European market. It holds 20.45% share of the worldwide

market (Kellogs, Investors relations, 2014). It shows that Kellogg’s operates on a very large

scale and has achieved great expansion across the globe.

Competitors

Company is in a constant battle for the number one position in the USA cereal market

with its main rival named General Mills. The other top competitors for the brand are Nestle,

2

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Ralcorp Holdings and many others (Gordon, 2008). The competition for Kellogg’s is very high

because it is operating under the FMCG industry. In this industry, large number and variety of

food items are produced at constant intervals.

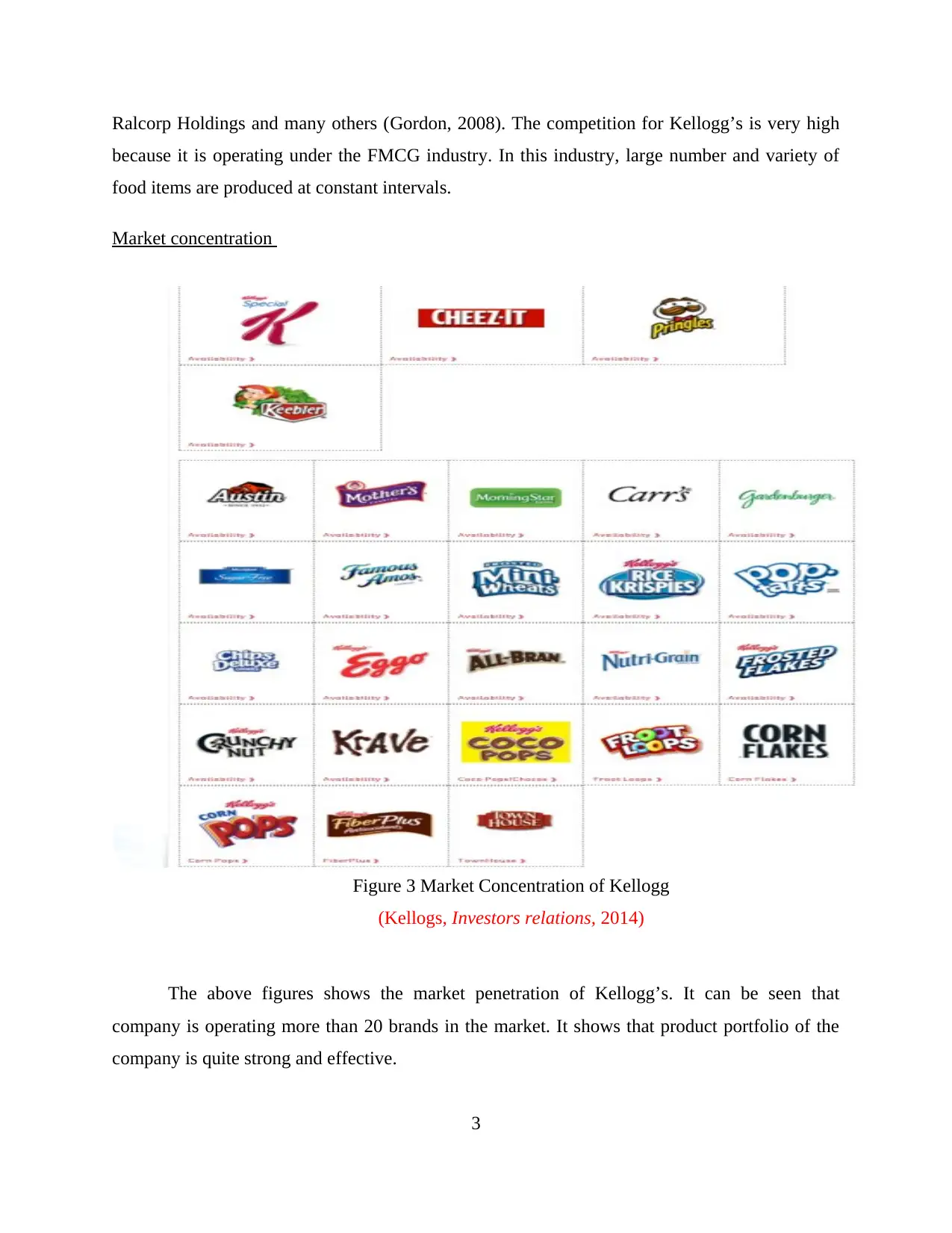

Market concentration

The above figures shows the market penetration of Kellogg’s. It can be seen that

company is operating more than 20 brands in the market. It shows that product portfolio of the

company is quite strong and effective.

3

Figure 3 Market Concentration of Kellogg

(Kellogs, Investors relations, 2014)

because it is operating under the FMCG industry. In this industry, large number and variety of

food items are produced at constant intervals.

Market concentration

The above figures shows the market penetration of Kellogg’s. It can be seen that

company is operating more than 20 brands in the market. It shows that product portfolio of the

company is quite strong and effective.

3

Figure 3 Market Concentration of Kellogg

(Kellogs, Investors relations, 2014)

Analysis

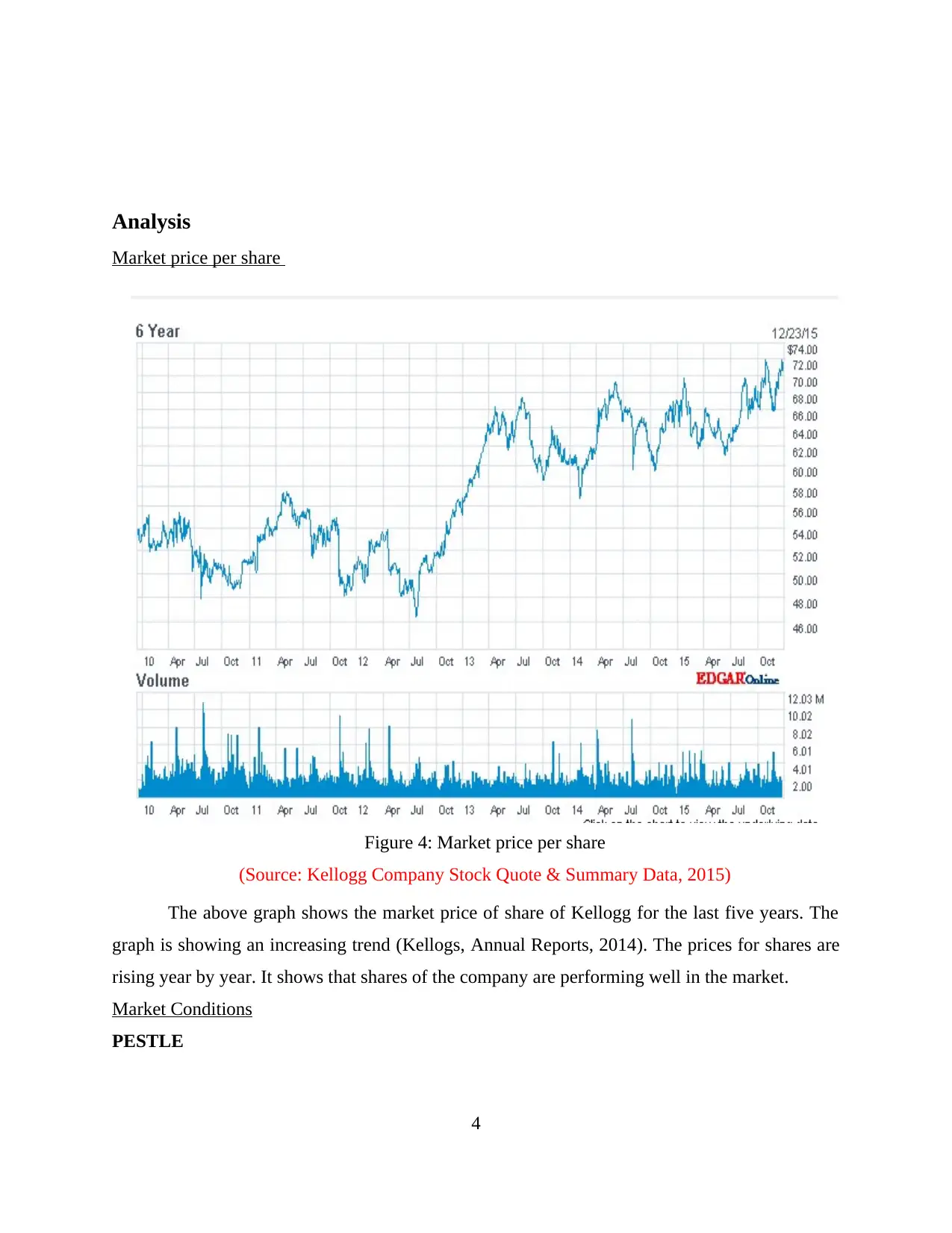

Market price per share

The above graph shows the market price of share of Kellogg for the last five years. The

graph is showing an increasing trend (Kellogs, Annual Reports, 2014). The prices for shares are

rising year by year. It shows that shares of the company are performing well in the market.

Market Conditions

PESTLE

4

Figure 4: Market price per share

(Source: Kellogg Company Stock Quote & Summary Data, 2015)

Market price per share

The above graph shows the market price of share of Kellogg for the last five years. The

graph is showing an increasing trend (Kellogs, Annual Reports, 2014). The prices for shares are

rising year by year. It shows that shares of the company are performing well in the market.

Market Conditions

PESTLE

4

Figure 4: Market price per share

(Source: Kellogg Company Stock Quote & Summary Data, 2015)

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Political factors – Government has food acts and there is also an association called

ACFM (Association of Cereal Food Manufacturers). It deals particularly on the cereal

issues (Jara, Ebrero and Zapata, 2011).

Economic – Company has seen success due to high usage of the products but still it is

threatened by the traditional breakfast. There are still many growth opportunities.

Social – Earlier the product was targeted on school students but later on it covered the

whole family members (Keller, 2013). A new eating habit has been evolved.

Technological factors – The production process has become highly automated. Online

shopping has also increased the sale of products.

Environment – Environmental stewardship has been a major element of Kellogg

Company’s CSR strategy (Leung, 2011). Constant efforts are made to improve the

environmental performance and to conserve the natural resources.

Legal – EU legislation related to health, ingredients, labelling, storage etc affects the

business practices of the company. Some of the legislations are Food Labelling

Regulations, ACFM, and CEEREAL etc.

Strengths Weaknesses

Company’s flexibility and adaptability

towards the customer needs

Customization of products

Holds the history of changing food

habits (Murty Kopparthi and Kagabo,

2012)

Despite of liking of taste from the

customers, the products are expensive

(Price, 2015)

There is no much room left for

expansion because Kellogg’s has

entered already in nearly every market

around the world

High dependence on cereal segment

(Menifield, 2013)

Opportunities Threats

Acquiring of Pringles potato crisps

from Procter and Gamble (Noor,

2013)

Product innovation is a greater part of

Rising food pricing are increasing the

cost for the company

Presence of extreme level of

competition in the FMCG world

5

ACFM (Association of Cereal Food Manufacturers). It deals particularly on the cereal

issues (Jara, Ebrero and Zapata, 2011).

Economic – Company has seen success due to high usage of the products but still it is

threatened by the traditional breakfast. There are still many growth opportunities.

Social – Earlier the product was targeted on school students but later on it covered the

whole family members (Keller, 2013). A new eating habit has been evolved.

Technological factors – The production process has become highly automated. Online

shopping has also increased the sale of products.

Environment – Environmental stewardship has been a major element of Kellogg

Company’s CSR strategy (Leung, 2011). Constant efforts are made to improve the

environmental performance and to conserve the natural resources.

Legal – EU legislation related to health, ingredients, labelling, storage etc affects the

business practices of the company. Some of the legislations are Food Labelling

Regulations, ACFM, and CEEREAL etc.

Strengths Weaknesses

Company’s flexibility and adaptability

towards the customer needs

Customization of products

Holds the history of changing food

habits (Murty Kopparthi and Kagabo,

2012)

Despite of liking of taste from the

customers, the products are expensive

(Price, 2015)

There is no much room left for

expansion because Kellogg’s has

entered already in nearly every market

around the world

High dependence on cereal segment

(Menifield, 2013)

Opportunities Threats

Acquiring of Pringles potato crisps

from Procter and Gamble (Noor,

2013)

Product innovation is a greater part of

Rising food pricing are increasing the

cost for the company

Presence of extreme level of

competition in the FMCG world

5

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

the corporate strategies

Selling of some of the brands for cash

helps the company in paying its debts.

(Petch, 2012)

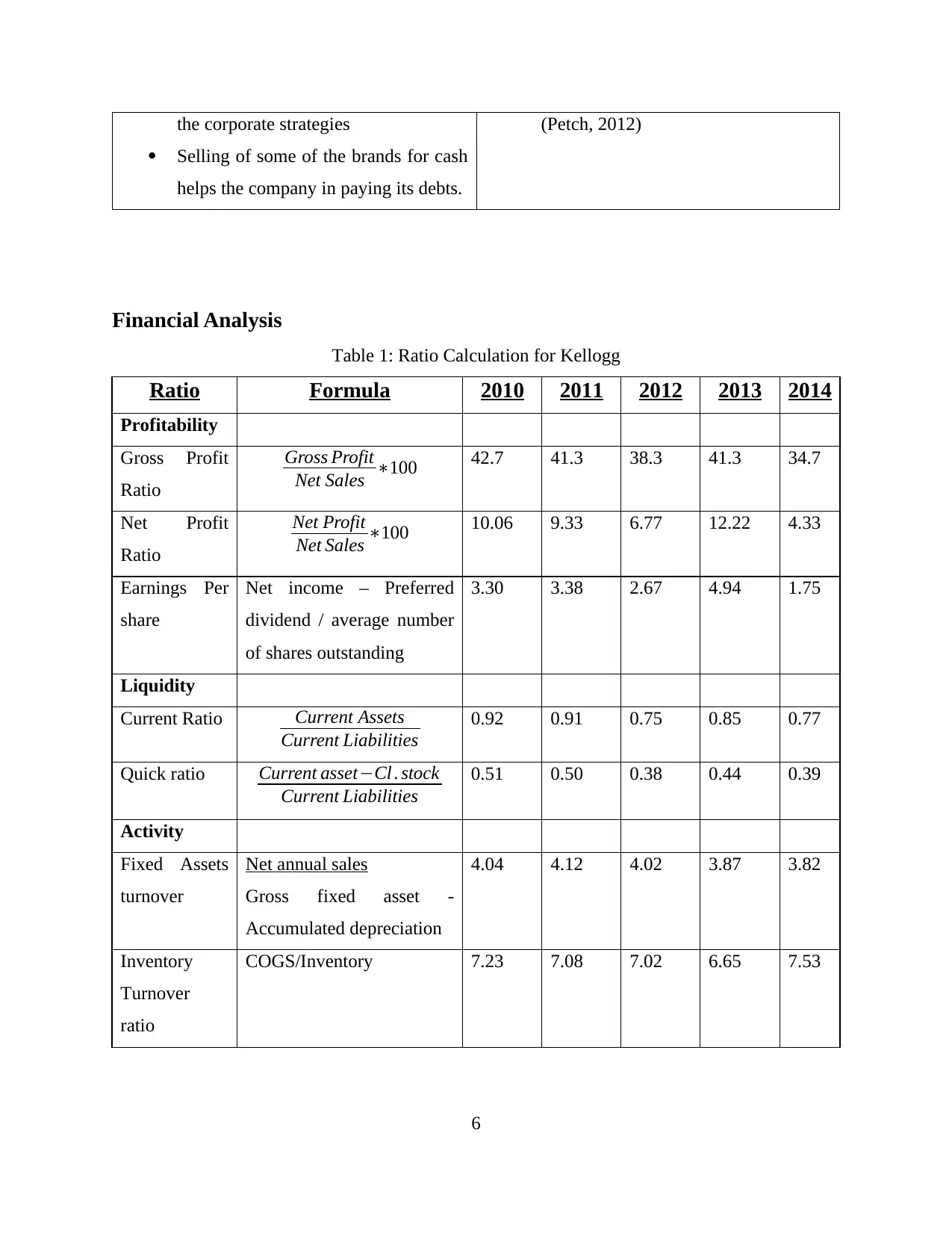

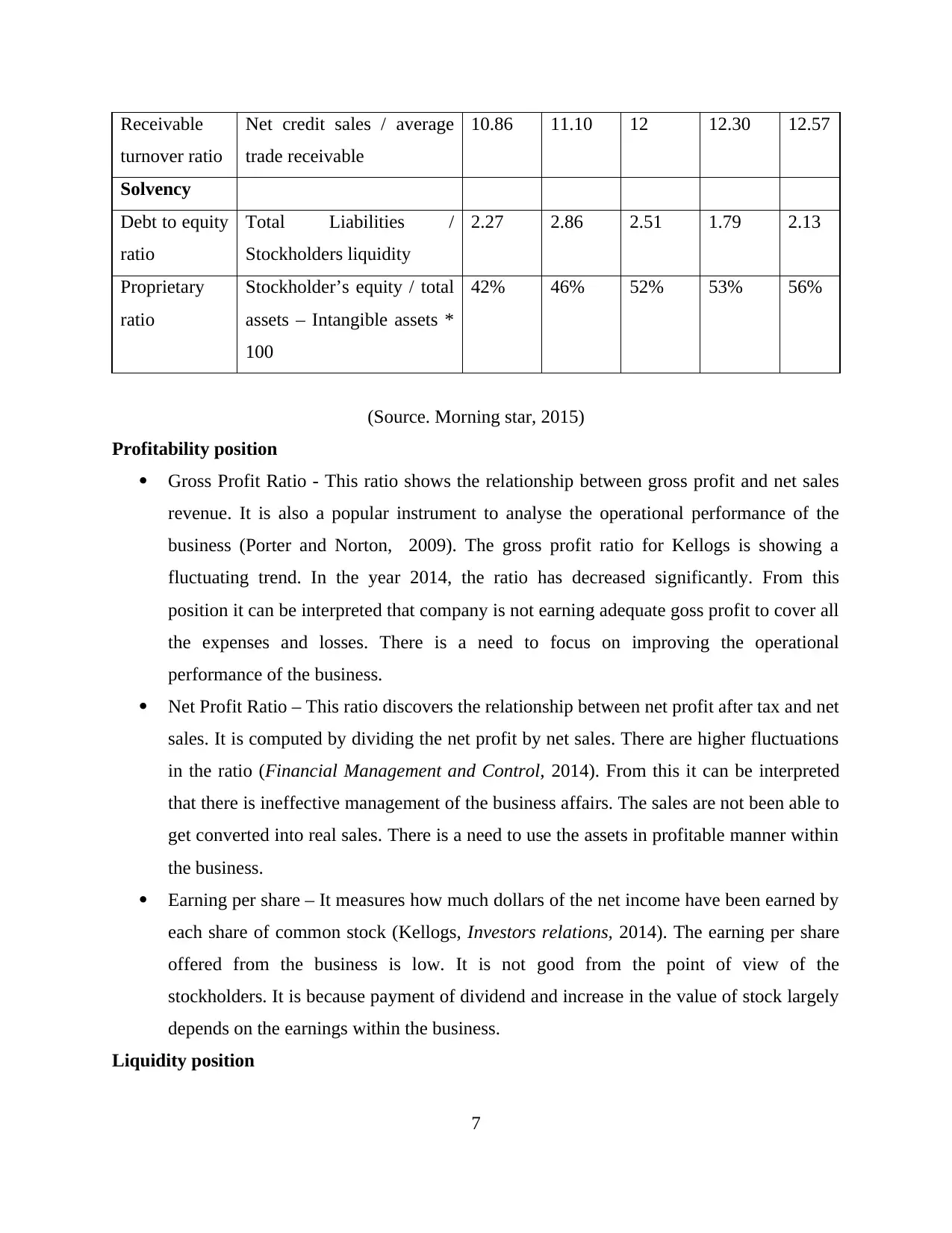

Financial Analysis

Table 1: Ratio Calculation for Kellogg

Ratio Formula 2010 2011 2012 2013 2014

Profitability

Gross Profit

Ratio

Gross Profit

Net Sales ∗100 42.7 41.3 38.3 41.3 34.7

Net Profit

Ratio

Net Profit

Net Sales ∗100 10.06 9.33 6.77 12.22 4.33

Earnings Per

share

Net income – Preferred

dividend / average number

of shares outstanding

3.30 3.38 2.67 4.94 1.75

Liquidity

Current Ratio Current Assets

Current Liabilities

0.92 0.91 0.75 0.85 0.77

Quick ratio Current asset−Cl . stock

Current Liabilities

0.51 0.50 0.38 0.44 0.39

Activity

Fixed Assets

turnover

Net annual sales

Gross fixed asset -

Accumulated depreciation

4.04 4.12 4.02 3.87 3.82

Inventory

Turnover

ratio

COGS/Inventory 7.23 7.08 7.02 6.65 7.53

6

Selling of some of the brands for cash

helps the company in paying its debts.

(Petch, 2012)

Financial Analysis

Table 1: Ratio Calculation for Kellogg

Ratio Formula 2010 2011 2012 2013 2014

Profitability

Gross Profit

Ratio

Gross Profit

Net Sales ∗100 42.7 41.3 38.3 41.3 34.7

Net Profit

Ratio

Net Profit

Net Sales ∗100 10.06 9.33 6.77 12.22 4.33

Earnings Per

share

Net income – Preferred

dividend / average number

of shares outstanding

3.30 3.38 2.67 4.94 1.75

Liquidity

Current Ratio Current Assets

Current Liabilities

0.92 0.91 0.75 0.85 0.77

Quick ratio Current asset−Cl . stock

Current Liabilities

0.51 0.50 0.38 0.44 0.39

Activity

Fixed Assets

turnover

Net annual sales

Gross fixed asset -

Accumulated depreciation

4.04 4.12 4.02 3.87 3.82

Inventory

Turnover

ratio

COGS/Inventory 7.23 7.08 7.02 6.65 7.53

6

Receivable

turnover ratio

Net credit sales / average

trade receivable

10.86 11.10 12 12.30 12.57

Solvency

Debt to equity

ratio

Total Liabilities /

Stockholders liquidity

2.27 2.86 2.51 1.79 2.13

Proprietary

ratio

Stockholder’s equity / total

assets – Intangible assets *

100

42% 46% 52% 53% 56%

(Source. Morning star, 2015)

Profitability position

Gross Profit Ratio - This ratio shows the relationship between gross profit and net sales

revenue. It is also a popular instrument to analyse the operational performance of the

business (Porter and Norton, 2009). The gross profit ratio for Kellogs is showing a

fluctuating trend. In the year 2014, the ratio has decreased significantly. From this

position it can be interpreted that company is not earning adequate goss profit to cover all

the expenses and losses. There is a need to focus on improving the operational

performance of the business.

Net Profit Ratio – This ratio discovers the relationship between net profit after tax and net

sales. It is computed by dividing the net profit by net sales. There are higher fluctuations

in the ratio (Financial Management and Control, 2014). From this it can be interpreted

that there is ineffective management of the business affairs. The sales are not been able to

get converted into real sales. There is a need to use the assets in profitable manner within

the business.

Earning per share – It measures how much dollars of the net income have been earned by

each share of common stock (Kellogs, Investors relations, 2014). The earning per share

offered from the business is low. It is not good from the point of view of the

stockholders. It is because payment of dividend and increase in the value of stock largely

depends on the earnings within the business.

Liquidity position

7

turnover ratio

Net credit sales / average

trade receivable

10.86 11.10 12 12.30 12.57

Solvency

Debt to equity

ratio

Total Liabilities /

Stockholders liquidity

2.27 2.86 2.51 1.79 2.13

Proprietary

ratio

Stockholder’s equity / total

assets – Intangible assets *

100

42% 46% 52% 53% 56%

(Source. Morning star, 2015)

Profitability position

Gross Profit Ratio - This ratio shows the relationship between gross profit and net sales

revenue. It is also a popular instrument to analyse the operational performance of the

business (Porter and Norton, 2009). The gross profit ratio for Kellogs is showing a

fluctuating trend. In the year 2014, the ratio has decreased significantly. From this

position it can be interpreted that company is not earning adequate goss profit to cover all

the expenses and losses. There is a need to focus on improving the operational

performance of the business.

Net Profit Ratio – This ratio discovers the relationship between net profit after tax and net

sales. It is computed by dividing the net profit by net sales. There are higher fluctuations

in the ratio (Financial Management and Control, 2014). From this it can be interpreted

that there is ineffective management of the business affairs. The sales are not been able to

get converted into real sales. There is a need to use the assets in profitable manner within

the business.

Earning per share – It measures how much dollars of the net income have been earned by

each share of common stock (Kellogs, Investors relations, 2014). The earning per share

offered from the business is low. It is not good from the point of view of the

stockholders. It is because payment of dividend and increase in the value of stock largely

depends on the earnings within the business.

Liquidity position

7

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Current ratio - This ratio measures the short term solvency position of the company. It

reflects the ability of the firm to pay its short term obligations. The ratio is lesser than the

ideal ratio which is 2:1. This shows that business is facing issues in meeting its short term

obligations and making its current debt payments (Kellogs, Annual Reports, 2014). The

business is not making enough from the operations to support activities.

Quick ratio – It shows the ability of the organization to pay its short term debts. The

relationship between liquid assets and current liabilities. Quick ratio is also showing a

fluctuating trend (Abraham, Deo and Irvine, 2008). Low quick ratio is sometimes good

for the business because it shows that company may have fast moving inventories. There

is a need to have a hard look on the nature of the individual assets.

Activity position

Fixed Assets turnover – It measures the efficiency through which company uses its fixed

assets to generate the sales revenue. Decreasing trend can be noticed in the fixed assets

ratio (Ball, Jayaraman and Shivakumar, 2012). It shows that there is ineffective

utilization of fixed assets. The assets are not been able to generate effective sales and this

is not a good sign for the financial position.

Inventory Turnover ratio - This ratio evaluates the liquidity of inventories of an

organization. It measures how many times the company has sold and replaced the

inventory during a certain period of time (Broadbent and Cullen, 2012). The ratio for

Kellogs is showing a positive trend. It is a sign of fast moving inventories. It means there

is no wastage of the resources and the stocks are maintained in appropriate manner.

Receivable turnover ratio – It is calculated by dividing the net credit sales by average

receivables. The ratio is very useful when it is used in combination with short term

solvency ratios that are current ratio and quick ratio (Goldman and Carrier, 2010). The

ratio is showing a very stagnant trend. It indicates that receivable in the company are

more liquid and are being collected in prompt manner.

Solvency

Debt to equity ratio - This ratio shows the soundness of long term financial policies of the

organization (Ittelson, 2009). A relationship is reflected between the portion of assets

offered from the stockholders and the portion of assets offered from the creditors. The

ratio for all the five years appears to be higher than 1. This indicates that portion of assets

8

reflects the ability of the firm to pay its short term obligations. The ratio is lesser than the

ideal ratio which is 2:1. This shows that business is facing issues in meeting its short term

obligations and making its current debt payments (Kellogs, Annual Reports, 2014). The

business is not making enough from the operations to support activities.

Quick ratio – It shows the ability of the organization to pay its short term debts. The

relationship between liquid assets and current liabilities. Quick ratio is also showing a

fluctuating trend (Abraham, Deo and Irvine, 2008). Low quick ratio is sometimes good

for the business because it shows that company may have fast moving inventories. There

is a need to have a hard look on the nature of the individual assets.

Activity position

Fixed Assets turnover – It measures the efficiency through which company uses its fixed

assets to generate the sales revenue. Decreasing trend can be noticed in the fixed assets

ratio (Ball, Jayaraman and Shivakumar, 2012). It shows that there is ineffective

utilization of fixed assets. The assets are not been able to generate effective sales and this

is not a good sign for the financial position.

Inventory Turnover ratio - This ratio evaluates the liquidity of inventories of an

organization. It measures how many times the company has sold and replaced the

inventory during a certain period of time (Broadbent and Cullen, 2012). The ratio for

Kellogs is showing a positive trend. It is a sign of fast moving inventories. It means there

is no wastage of the resources and the stocks are maintained in appropriate manner.

Receivable turnover ratio – It is calculated by dividing the net credit sales by average

receivables. The ratio is very useful when it is used in combination with short term

solvency ratios that are current ratio and quick ratio (Goldman and Carrier, 2010). The

ratio is showing a very stagnant trend. It indicates that receivable in the company are

more liquid and are being collected in prompt manner.

Solvency

Debt to equity ratio - This ratio shows the soundness of long term financial policies of the

organization (Ittelson, 2009). A relationship is reflected between the portion of assets

offered from the stockholders and the portion of assets offered from the creditors. The

ratio for all the five years appears to be higher than 1. This indicates that portion of assets

8

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

provided by the creditors is higher than the portion of assets provided by the

stockholders. However Kellogs is a very bigger brand in the FMCG industry and it has

the potential to maintain a high debt to equity ratio (Jara, Ebrero and Zapata, 2011).

Proprietary ratio – This ratio helps in evaluating the soundness of the capital structure of

the organization. It is calculated by dividing the stockholders equity by the total number

of assets. Consistency can be seen in the Proprietary ratio of the company for the last

three years (Murty, Kopparthi and Kagabo, 2012). This indicates a strong financial

position of the business and a greater security for the creditors. This shows that

organization is not dependent on debts for its operations.

Interpretation

From the above ratio analysis it can be interpreted that Kellogg’s is performing well in

terms of activity and solvency. In terms of activity the organization is capable of generating the

revenues through converting the production into cash or sales. It shows fast movement of cash

and sales in the business (Financial Management and Control, 2014). In terms of solvency,

company has the potential to survive for a long period of time. It shows that firm’s internal and

external equities are in right proportion. However there is a need to focus on profitability and

liquidity position. Constant improvements are needed in the profits to survive and thrive after all

achieving profits is the ultimate objective of any business. The business resources are to be used

in effective manner (Ball, Jayaraman and Shivakumar, 2012). With regard to liquidity, Kellogg’s

is required to increase its potential in terms of paying the short term obligations. Currently they

are having insufficient current and liquid assets. It is a sign of weak liquidity position. Hence

improvements are needed in maintaining long term liquidity.

Conclusion

From the above study it can be concluded that product portfolio of Kellogg’s is quite

strong and effective because it is operating more than 20 brands in the market. Environmental

stewardship has been a major component of Kellogg Company’s CSR strategy (Kellogs,

Investors relations, 2014.). EU legislation related to health, ingredients, labelling, storage etc

affects the business practices of the company. It was realized that despite of liking of taste from

the customers, the products are expensive. There are no expansion opportunities left for the

9

stockholders. However Kellogs is a very bigger brand in the FMCG industry and it has

the potential to maintain a high debt to equity ratio (Jara, Ebrero and Zapata, 2011).

Proprietary ratio – This ratio helps in evaluating the soundness of the capital structure of

the organization. It is calculated by dividing the stockholders equity by the total number

of assets. Consistency can be seen in the Proprietary ratio of the company for the last

three years (Murty, Kopparthi and Kagabo, 2012). This indicates a strong financial

position of the business and a greater security for the creditors. This shows that

organization is not dependent on debts for its operations.

Interpretation

From the above ratio analysis it can be interpreted that Kellogg’s is performing well in

terms of activity and solvency. In terms of activity the organization is capable of generating the

revenues through converting the production into cash or sales. It shows fast movement of cash

and sales in the business (Financial Management and Control, 2014). In terms of solvency,

company has the potential to survive for a long period of time. It shows that firm’s internal and

external equities are in right proportion. However there is a need to focus on profitability and

liquidity position. Constant improvements are needed in the profits to survive and thrive after all

achieving profits is the ultimate objective of any business. The business resources are to be used

in effective manner (Ball, Jayaraman and Shivakumar, 2012). With regard to liquidity, Kellogg’s

is required to increase its potential in terms of paying the short term obligations. Currently they

are having insufficient current and liquid assets. It is a sign of weak liquidity position. Hence

improvements are needed in maintaining long term liquidity.

Conclusion

From the above study it can be concluded that product portfolio of Kellogg’s is quite

strong and effective because it is operating more than 20 brands in the market. Environmental

stewardship has been a major component of Kellogg Company’s CSR strategy (Kellogs,

Investors relations, 2014.). EU legislation related to health, ingredients, labelling, storage etc

affects the business practices of the company. It was realized that despite of liking of taste from

the customers, the products are expensive. There are no expansion opportunities left for the

9

company because of presence in every country. High dependence is there on cereal segment

which is a biggest drawback for them.

The financial analysis showed that Kellogg’s is performing well in terms of activity and

solvency, however improvements are needed in profitability and liquidity position. Business has

the potential to survive for a long period of time and firm’s internal and external equities are in

right proportion. However the brand has succeeded in maintaining a good financial position

within the industry. Due to increasing competition it has become difficult to retain high share in

the market.

Recommendations

Following recommendations can be made regarding the business of Kellogg:

Focus is to be paid on maintaining long term liquidity and profitability.

More focus is to be paid on the markets where the products are achieving success.

In order to face the competition, differentiation is needed to be achieved in terms of

products and services (Kellogs, Investors relations, 2014)

Liquidity can be improved by doing effective management of the liquid cash.

Market share can be gained by adopting strategies such as new product development,

expansion into new markets and acquisition.

The high dependence on the cereal segment is needed to be removed and emphasis is to

be paid on launching new categories of FMCG products.

10

which is a biggest drawback for them.

The financial analysis showed that Kellogg’s is performing well in terms of activity and

solvency, however improvements are needed in profitability and liquidity position. Business has

the potential to survive for a long period of time and firm’s internal and external equities are in

right proportion. However the brand has succeeded in maintaining a good financial position

within the industry. Due to increasing competition it has become difficult to retain high share in

the market.

Recommendations

Following recommendations can be made regarding the business of Kellogg:

Focus is to be paid on maintaining long term liquidity and profitability.

More focus is to be paid on the markets where the products are achieving success.

In order to face the competition, differentiation is needed to be achieved in terms of

products and services (Kellogs, Investors relations, 2014)

Liquidity can be improved by doing effective management of the liquid cash.

Market share can be gained by adopting strategies such as new product development,

expansion into new markets and acquisition.

The high dependence on the cereal segment is needed to be removed and emphasis is to

be paid on launching new categories of FMCG products.

10

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 14

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.