Calculate E-Surfboards' taxable income for the year ended 30 June 2015

12 Pages2054 Words89 Views

Added on 2023-02-01

About This Document

This document provides instructions and calculations for determining E-Surfboards' taxable income for the year ended 30 June 2015. It includes information on temporary differences, deferred tax liability and asset, and journal entries for recording current tax and deferred tax.

Calculate E-Surfboards' taxable income for the year ended 30 June 2015

Added on 2023-02-01

ShareRelated Documents

Module 6 Week 8

Assessment Type Written Examination

Unit Title: Prepare financial reports

for corporate entities

Student Declaration: I declare that this work has been

completed by me honestly and with integrity. I understand

that the Elite Education Vocation Institute’s Student

Assessment, Reassessment and Repeating Units of

Competency Guidelines apply to these assessment tasks.

Student Name:

Student Signature:

D

a

t

e

:

Assessment submission (new) requirements

Please save this file as PDF format (include your name to

the filename) before uploading onto Moodle.

Assessment/evidence gathering conditions

Each assessment component is recorded as either

Satisfactory (S) or Not Yet Satisfactory (NYS). A student can

only achieve competence when all assessment components

listed under procedures and specifications of the

assessment section are Satisfactory. Your trainer will give

you feedback after the completion of each assessment. A

student who is assessed as NYS is eligible for re-

assessment. Should the student fail to submit the

assessment, a result outcome of Did Not Submit (DNS) will

be recorded.

Principles of Assessment

V2018.T2. 1.1

FNS50215 - Diploma of Accounting / FNSACC504/ 2018/ T2/ Assessment Tool Page 1 of

12

Assessment Type Written Examination

Unit Title: Prepare financial reports

for corporate entities

Student Declaration: I declare that this work has been

completed by me honestly and with integrity. I understand

that the Elite Education Vocation Institute’s Student

Assessment, Reassessment and Repeating Units of

Competency Guidelines apply to these assessment tasks.

Student Name:

Student Signature:

D

a

t

e

:

Assessment submission (new) requirements

Please save this file as PDF format (include your name to

the filename) before uploading onto Moodle.

Assessment/evidence gathering conditions

Each assessment component is recorded as either

Satisfactory (S) or Not Yet Satisfactory (NYS). A student can

only achieve competence when all assessment components

listed under procedures and specifications of the

assessment section are Satisfactory. Your trainer will give

you feedback after the completion of each assessment. A

student who is assessed as NYS is eligible for re-

assessment. Should the student fail to submit the

assessment, a result outcome of Did Not Submit (DNS) will

be recorded.

Principles of Assessment

V2018.T2. 1.1

FNS50215 - Diploma of Accounting / FNSACC504/ 2018/ T2/ Assessment Tool Page 1 of

12

Based on Clauses 1.8 – 1.12 from the Australian Standards

Quality Assurance’s (ASQA) Standards for Registered

Training Organizations (RTO) 2015, the learner would be

assessed based on the following principles:

Fairness - (1) the individual learner’s needs are considered

in the assessment process, (2) where

appropriate, reasonable adjustments are applied

by the RTO to take into account the individual

leaner’s needs and, (3) the RTO informs the

leaner about the assessment process, and

provides the learner with the opportunity to

challenge the result of the assessment and be

reassessed if necessary.

Flexibility – assessment is flexible to the individual learner

by; (1) reflecting the learner’s needs, (2)

assessing competencies held by the learner no

matter how or where they have been acquired

and, (3) the unit of competency and associated

assessment requirements, and the individual.

Validity – (1) requires that assessment against the unit/s of

competency and the associated assessment

requirements covers the broad range of skills

and knowledge, (2) assessment of knowledge

and skills is integrated with their practical

application, (3) assessment to be based on

evidence that demonstrates tat a leaner could

demonstrate these skills and knowledge in other

similar situations and, (4) judgement of

competence is based on evidence of learner

performance that is aligned to the unit/s of

competency and associated assessment

requirements.

Reliability – evidence presented for assessment is

consistently interpreted and assessment results

are comparable irrespective of the assessor

conducting the assessment

Rules of Evidence

Validity – the assessor is assured that the learner has

the skills, knowledge and attributes, as

described in the module of unit of competency

and associated assessment requirements.

Sufficiency – the assessor is assured that the quality,

quantity and relevance of the assessment

evidence enables a judgement to be made of a

learner’s competency.

Authenticity – the assessor is assured that the evidence

presented for assessment is the learner’s own

work. This would mean that any form of

plagiarism or copying of other’s work may not

be permitted and would be deemed strictly as a

‘Not Yet Competent’ grading.

Currency – the assessor is assured that the assessment

evidence demonstrates current competency.

This requires the assessment evidence to be

from the present or the very recent past.

Resources required for this Assessment

V2018.T2. 1.1

FNS50215 - Diploma of Accounting / FNSACC504/ 2018/ T2/ Assessment Tool Page 2 of

12

Quality Assurance’s (ASQA) Standards for Registered

Training Organizations (RTO) 2015, the learner would be

assessed based on the following principles:

Fairness - (1) the individual learner’s needs are considered

in the assessment process, (2) where

appropriate, reasonable adjustments are applied

by the RTO to take into account the individual

leaner’s needs and, (3) the RTO informs the

leaner about the assessment process, and

provides the learner with the opportunity to

challenge the result of the assessment and be

reassessed if necessary.

Flexibility – assessment is flexible to the individual learner

by; (1) reflecting the learner’s needs, (2)

assessing competencies held by the learner no

matter how or where they have been acquired

and, (3) the unit of competency and associated

assessment requirements, and the individual.

Validity – (1) requires that assessment against the unit/s of

competency and the associated assessment

requirements covers the broad range of skills

and knowledge, (2) assessment of knowledge

and skills is integrated with their practical

application, (3) assessment to be based on

evidence that demonstrates tat a leaner could

demonstrate these skills and knowledge in other

similar situations and, (4) judgement of

competence is based on evidence of learner

performance that is aligned to the unit/s of

competency and associated assessment

requirements.

Reliability – evidence presented for assessment is

consistently interpreted and assessment results

are comparable irrespective of the assessor

conducting the assessment

Rules of Evidence

Validity – the assessor is assured that the learner has

the skills, knowledge and attributes, as

described in the module of unit of competency

and associated assessment requirements.

Sufficiency – the assessor is assured that the quality,

quantity and relevance of the assessment

evidence enables a judgement to be made of a

learner’s competency.

Authenticity – the assessor is assured that the evidence

presented for assessment is the learner’s own

work. This would mean that any form of

plagiarism or copying of other’s work may not

be permitted and would be deemed strictly as a

‘Not Yet Competent’ grading.

Currency – the assessor is assured that the assessment

evidence demonstrates current competency.

This requires the assessment evidence to be

from the present or the very recent past.

Resources required for this Assessment

V2018.T2. 1.1

FNS50215 - Diploma of Accounting / FNSACC504/ 2018/ T2/ Assessment Tool Page 2 of

12

All documents must be created using Microsoft

Office suites i.e., MS Word, Excel, PowerPoint

Upon completion, submit the assessment via the

student learning management system to your trainer

along with the completed assessment coversheet.

Refer the notes on eLearning to answer the tasks

Any additional material will be provided by Trainer

Instructions for Students

Please read the following instructions carefully

This assessment is to be completed according to the

instructions given by your assessor.

Students are allowed to take this assessment home.

Feedback on each task will be provided to enable you

to determine how your work could be improved. You will

be provided with feedback on your work within 2 weeks

of the assessment due date.

Should you not answer the questions correctly, you will

be given feedback on the results and your gaps in

knowledge. You will be given another opportunity to

demonstrate your knowledge and skills to be deemed

competent for this unit of competency.

If you are not sure about any aspect of this assessment,

please ask for clarification from your assessor.

Please refer to the College re-assessment and re-

enrolment policy for more information.

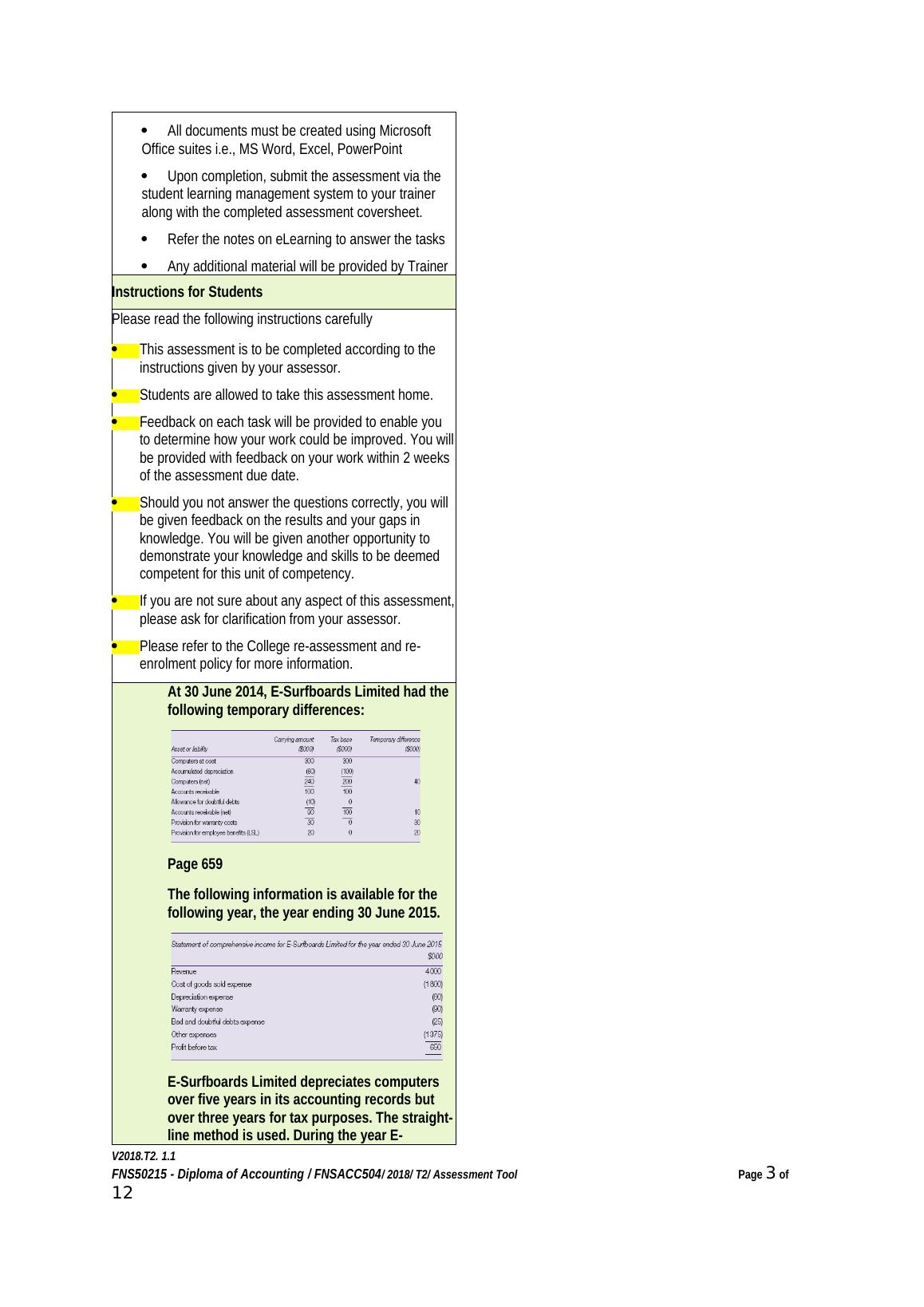

At 30 June 2014, E-Surfboards Limited had the

following temporary differences:

Page 659

The following information is available for the

following year, the year ending 30 June 2015.

E-Surfboards Limited depreciates computers

over five years in its accounting records but

over three years for tax purposes. The straight-

line method is used. During the year E-

V2018.T2. 1.1

FNS50215 - Diploma of Accounting / FNSACC504/ 2018/ T2/ Assessment Tool Page 3 of

12

Office suites i.e., MS Word, Excel, PowerPoint

Upon completion, submit the assessment via the

student learning management system to your trainer

along with the completed assessment coversheet.

Refer the notes on eLearning to answer the tasks

Any additional material will be provided by Trainer

Instructions for Students

Please read the following instructions carefully

This assessment is to be completed according to the

instructions given by your assessor.

Students are allowed to take this assessment home.

Feedback on each task will be provided to enable you

to determine how your work could be improved. You will

be provided with feedback on your work within 2 weeks

of the assessment due date.

Should you not answer the questions correctly, you will

be given feedback on the results and your gaps in

knowledge. You will be given another opportunity to

demonstrate your knowledge and skills to be deemed

competent for this unit of competency.

If you are not sure about any aspect of this assessment,

please ask for clarification from your assessor.

Please refer to the College re-assessment and re-

enrolment policy for more information.

At 30 June 2014, E-Surfboards Limited had the

following temporary differences:

Page 659

The following information is available for the

following year, the year ending 30 June 2015.

E-Surfboards Limited depreciates computers

over five years in its accounting records but

over three years for tax purposes. The straight-

line method is used. During the year E-

V2018.T2. 1.1

FNS50215 - Diploma of Accounting / FNSACC504/ 2018/ T2/ Assessment Tool Page 3 of

12

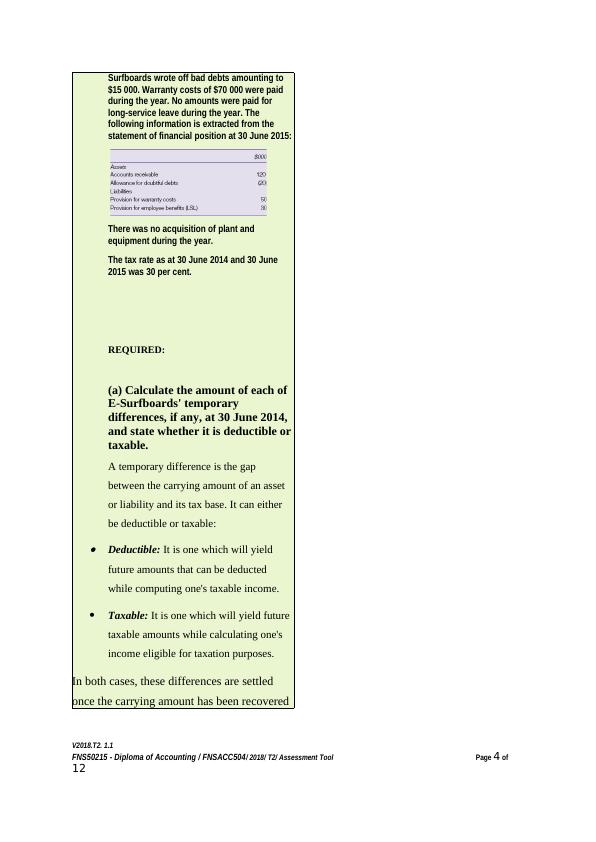

Surfboards wrote off bad debts amounting to

$15 000. Warranty costs of $70 000 were paid

during the year. No amounts were paid for

long-service leave during the year. The

following information is extracted from the

statement of financial position at 30 June 2015:

There was no acquisition of plant and

equipment during the year.

The tax rate as at 30 June 2014 and 30 June

2015 was 30 per cent.

REQUIRED:

(a) Calculate the amount of each of

E-Surfboards' temporary

differences, if any, at 30 June 2014,

and state whether it is deductible or

taxable.

A temporary difference is the gap

between the carrying amount of an asset

or liability and its tax base. It can either

be deductible or taxable: Deductible: It is one which will yield

future amounts that can be deducted

while computing one's taxable income.

Taxable: It is one which will yield future

taxable amounts while calculating one's

income eligible for taxation purposes.

In both cases, these differences are settled

once the carrying amount has been recovered

V2018.T2. 1.1

FNS50215 - Diploma of Accounting / FNSACC504/ 2018/ T2/ Assessment Tool Page 4 of

12

$15 000. Warranty costs of $70 000 were paid

during the year. No amounts were paid for

long-service leave during the year. The

following information is extracted from the

statement of financial position at 30 June 2015:

There was no acquisition of plant and

equipment during the year.

The tax rate as at 30 June 2014 and 30 June

2015 was 30 per cent.

REQUIRED:

(a) Calculate the amount of each of

E-Surfboards' temporary

differences, if any, at 30 June 2014,

and state whether it is deductible or

taxable.

A temporary difference is the gap

between the carrying amount of an asset

or liability and its tax base. It can either

be deductible or taxable: Deductible: It is one which will yield

future amounts that can be deducted

while computing one's taxable income.

Taxable: It is one which will yield future

taxable amounts while calculating one's

income eligible for taxation purposes.

In both cases, these differences are settled

once the carrying amount has been recovered

V2018.T2. 1.1

FNS50215 - Diploma of Accounting / FNSACC504/ 2018/ T2/ Assessment Tool Page 4 of

12

End of preview

Want to access all the pages? Upload your documents or become a member.

Related Documents

BSBMKG501 Identify And Evaluate Marketing Opportunities Assignmentlg...

|18

|3344

|202

BSBINN501 Establish Systems that Supports Innovationlg...

|16

|3395

|226

Report on Establish and Adjust the Marketing Mixlg...

|14

|3239

|52

BSBMKG606: Manage International Marketing Assignmentlg...

|16

|2993

|283

Term and Year 2017 Assessment Cover Sheetlg...

|15

|2950

|440

Financial Reports for Corporate Entities Assignmentlg...

|9

|1816

|269