FNSACC507 Provide Management Accounting Information Solutions

VerifiedAdded on 2023/06/11

|8

|2079

|431

Homework Assignment

AI Summary

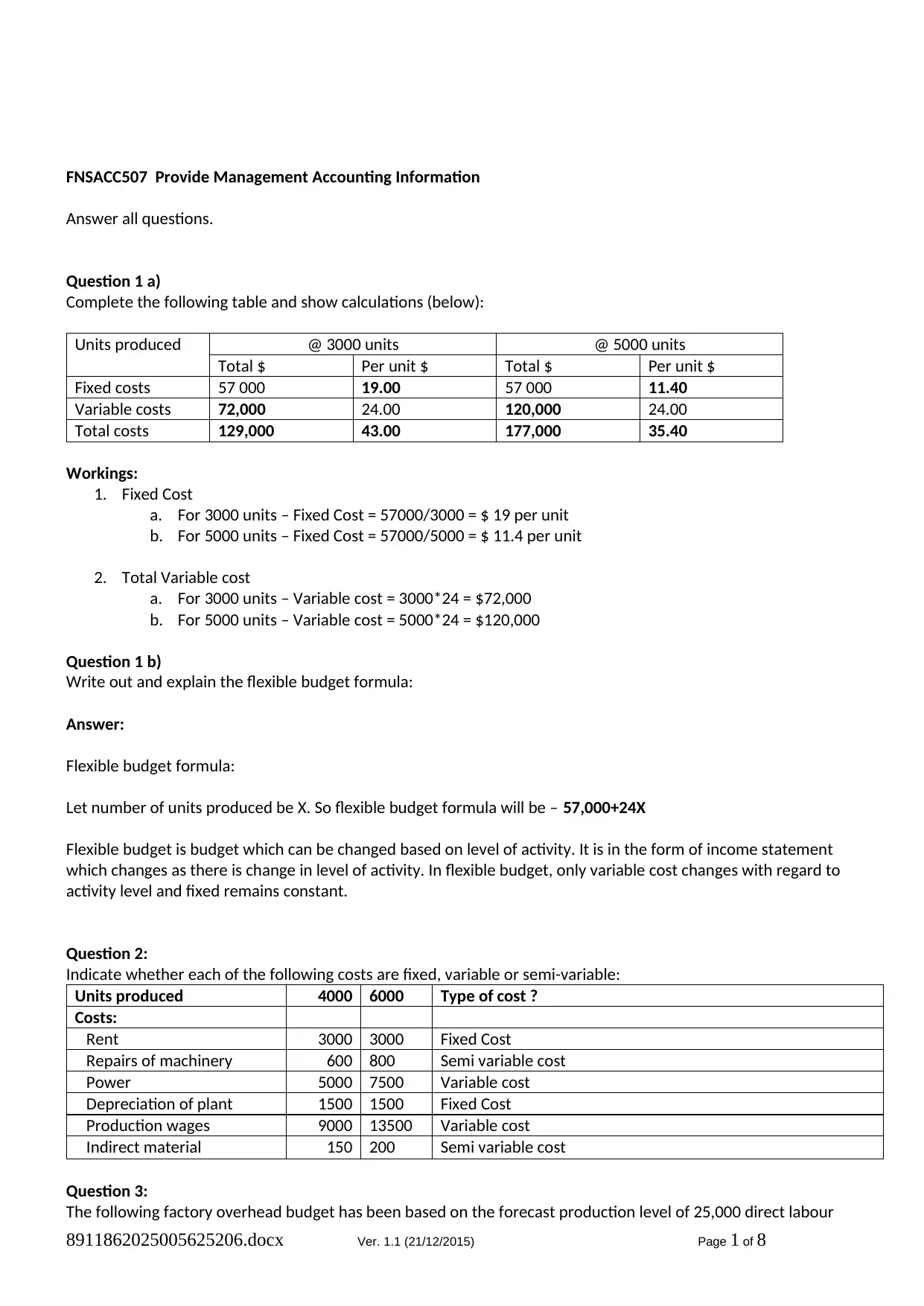

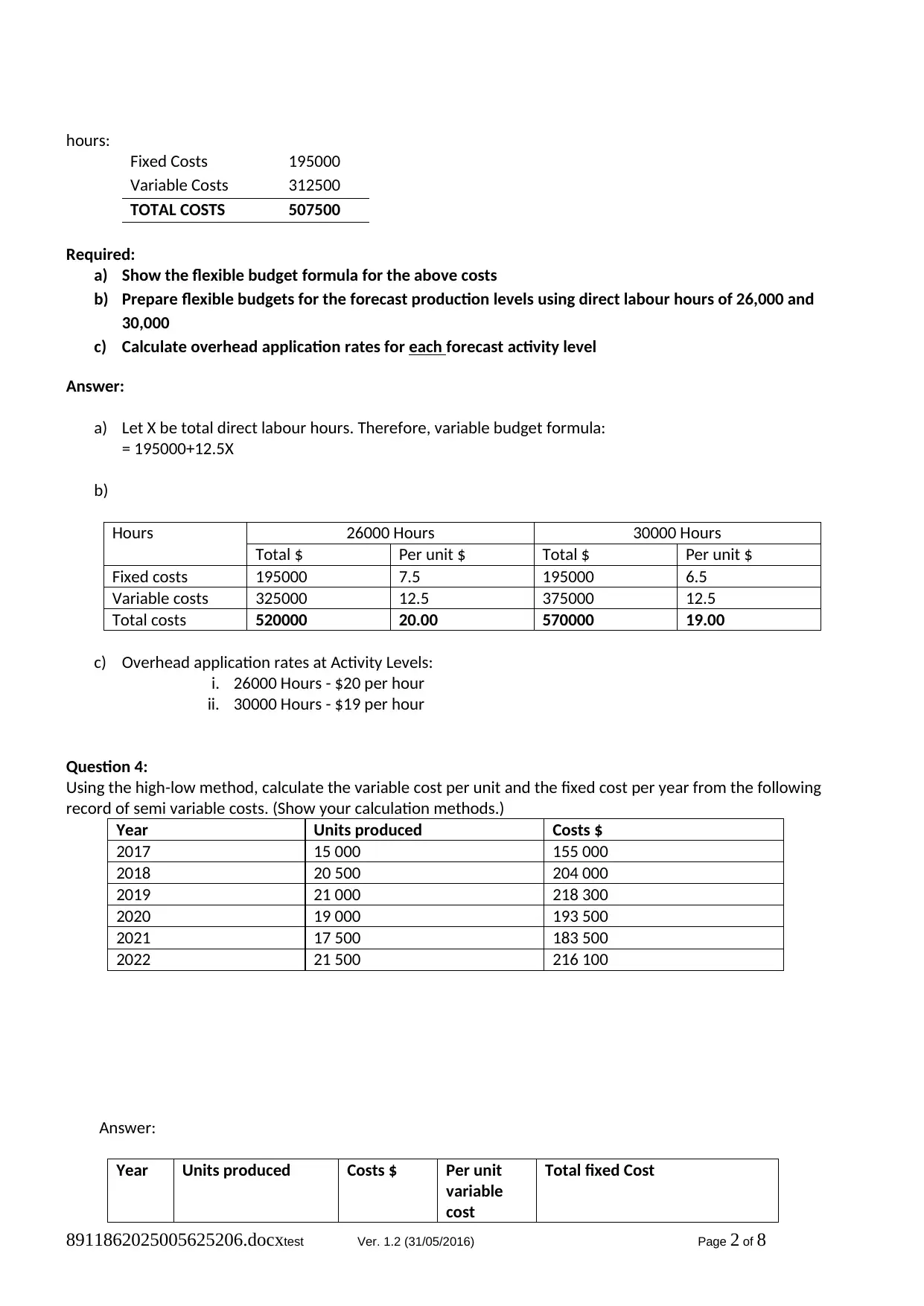

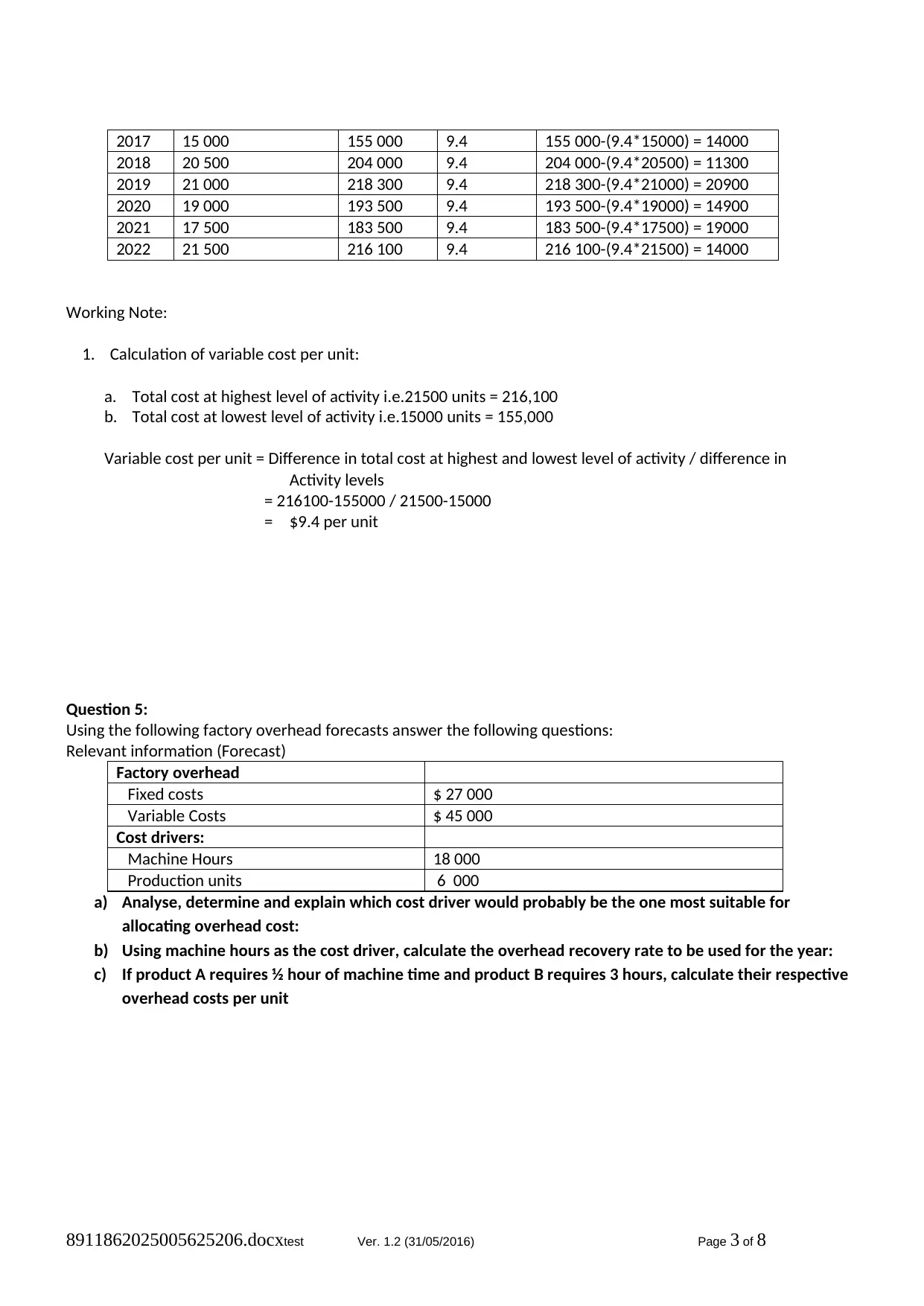

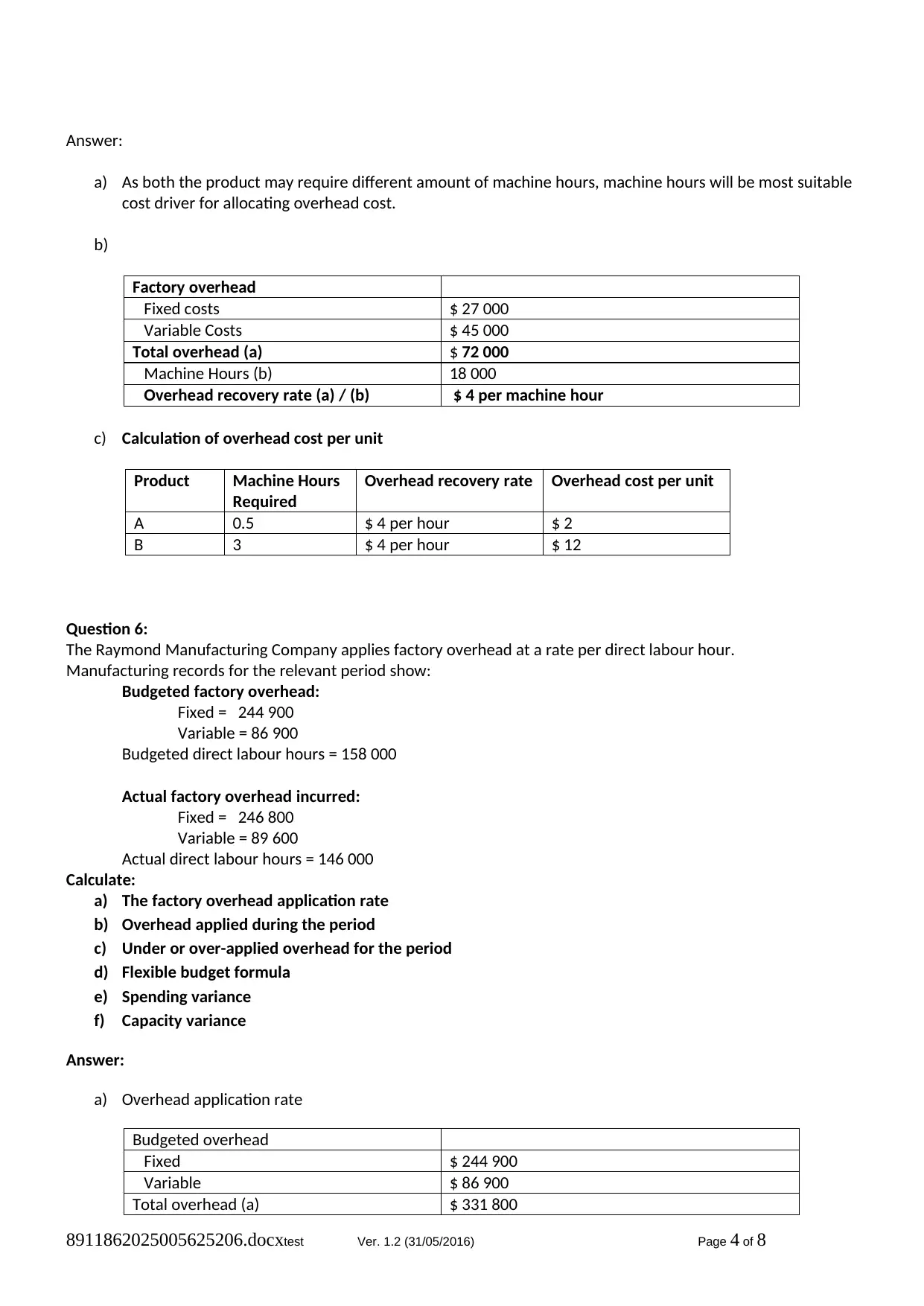

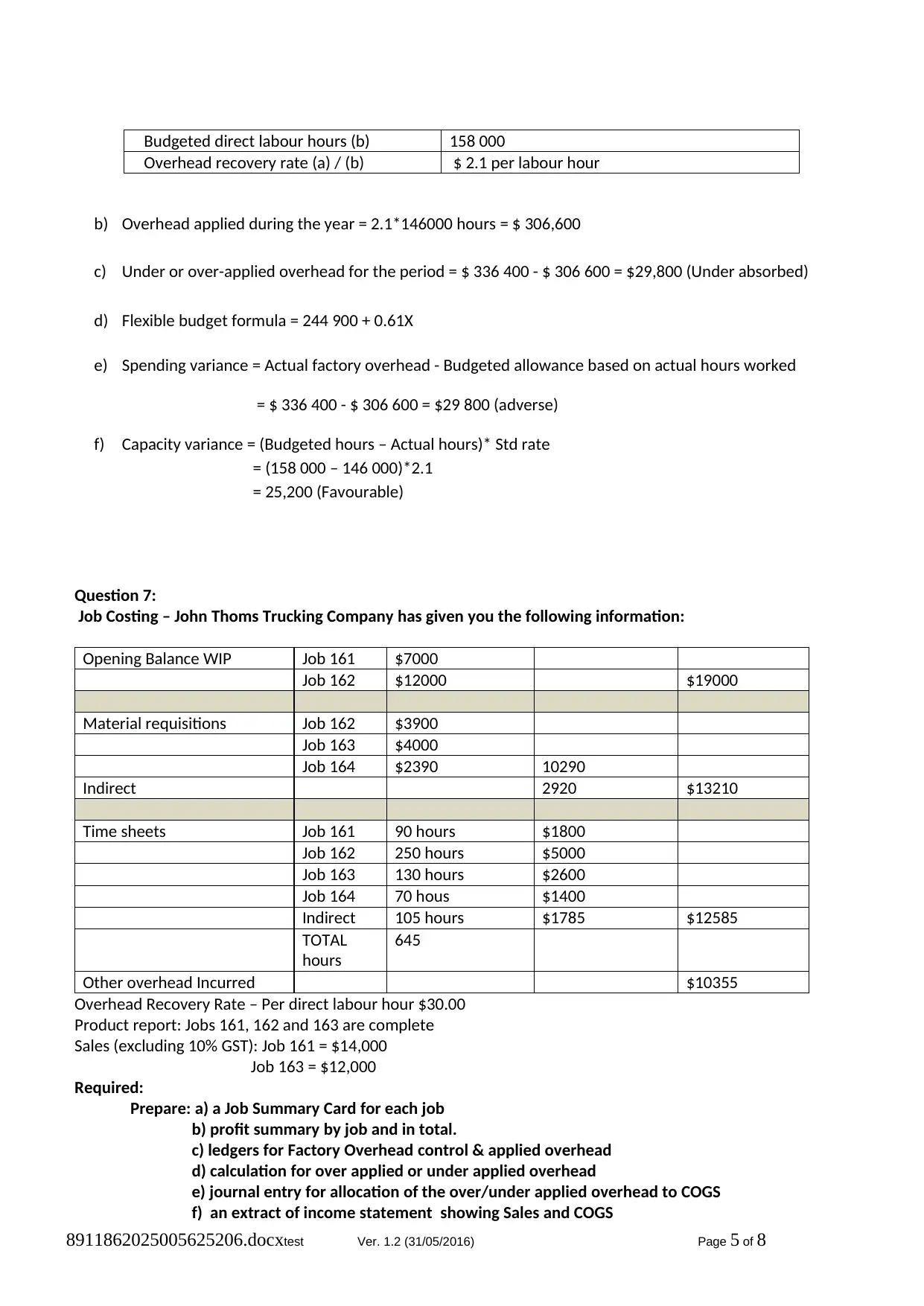

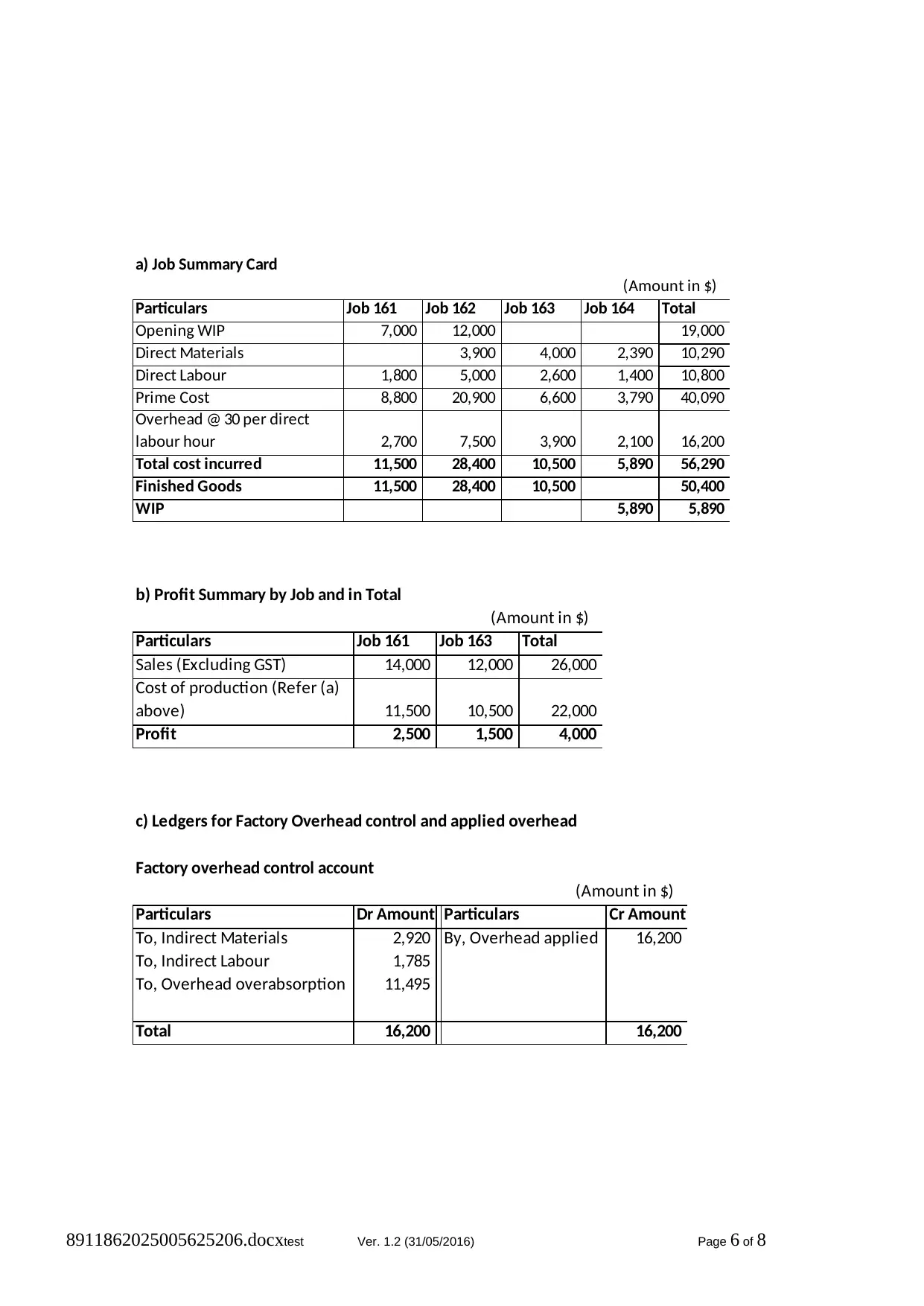

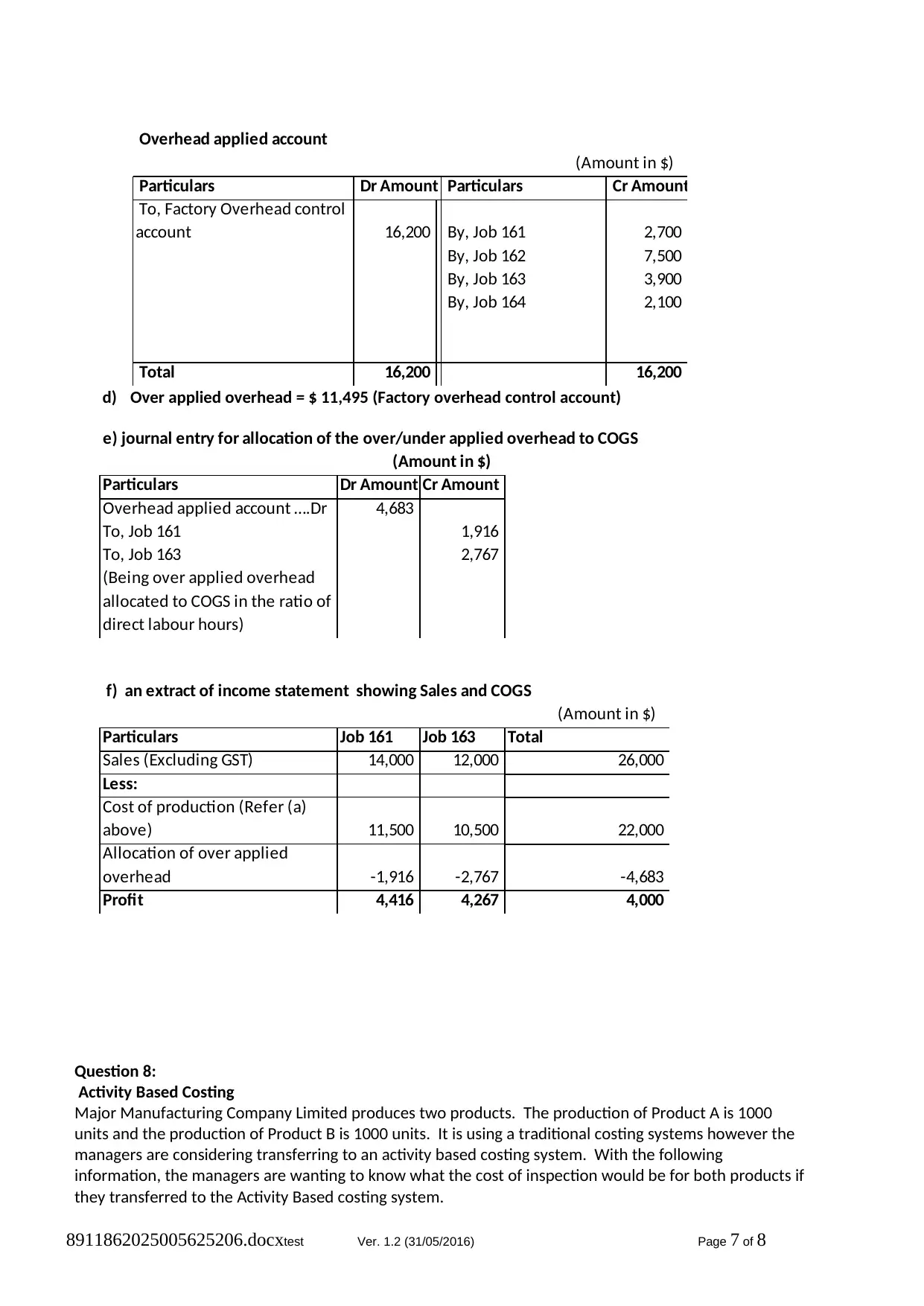

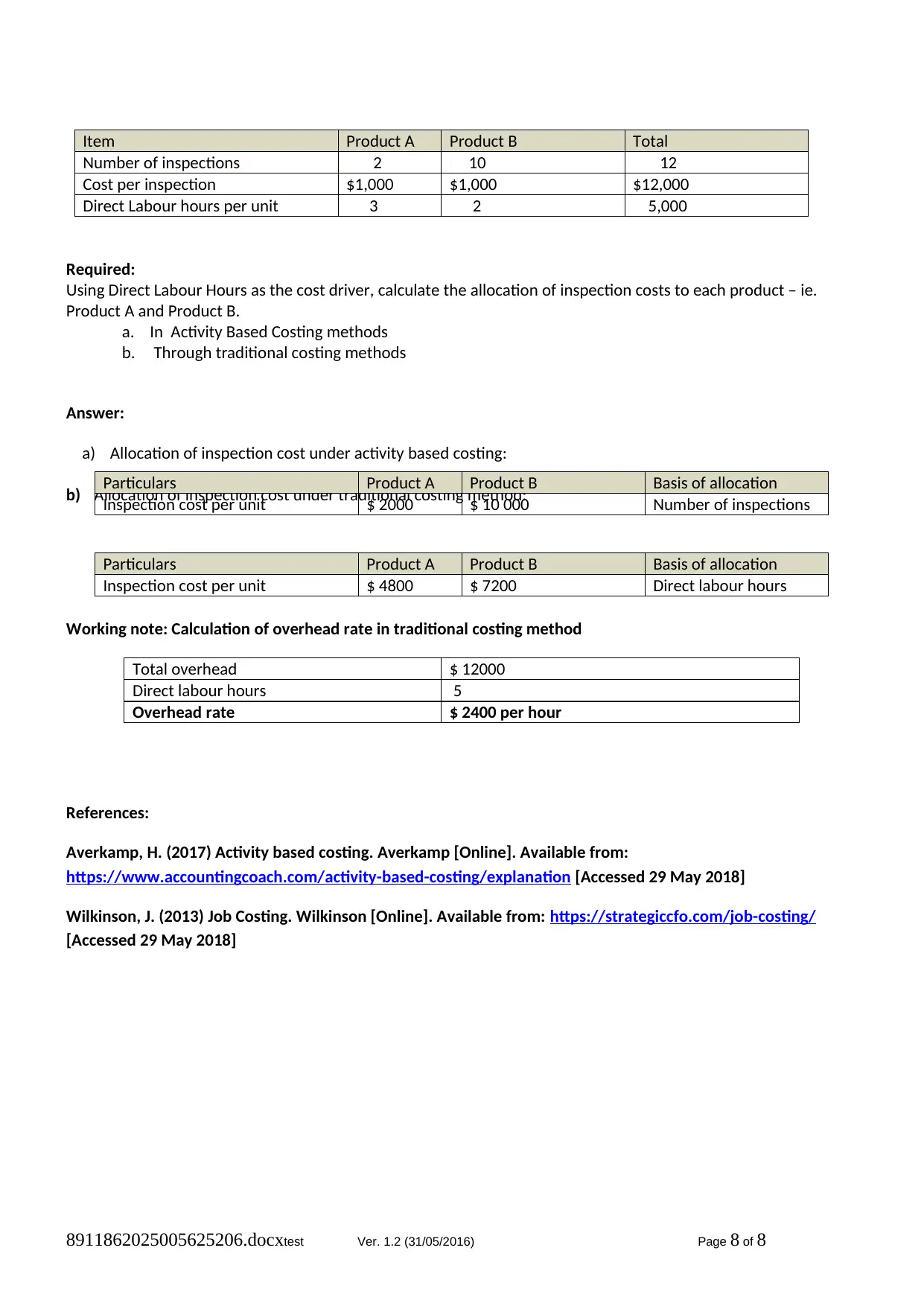

This document provides a comprehensive solution to an FNSACC507 assignment focused on management accounting information. It includes detailed calculations and explanations for various concepts such as flexible budgeting, fixed, variable and semi-variable costs, overhead application, high-low method, job costing, and activity-based costing (ABC). The solution covers calculations for fixed and variable costs at different production levels, flexible budget formulas, overhead application rates, variable cost per unit and fixed cost calculations using the high-low method. Furthermore, the assignment solution provides job summary cards, profit summaries, ledger entries for factory overhead, and income statement extracts. Finally, it includes detailed explanations of activity-based costing versus traditional costing methods.

1 out of 8

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2025 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.