Tax Deductions and Income Calculation

VerifiedAdded on 2020/04/01

|10

|1743

|33

AI Summary

The assignment focuses on calculating a business's taxable income by identifying allowable deductions against total income. It presents a detailed financial record with various income sources and expenses, including legal fees, interest payments, and business lunches. The student is tasked with determining the tax implications of specific deductions based on relevant sections of the Australian Income Tax Assessment Act 1997.

Contribute Materials

Your contribution can guide someone’s learning journey. Share your

documents today.

HI3042 Taxation Law

T2 2017 Individual Assignment

T2 2017 Individual Assignment

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

TABLE OF CONTENTS

Solution 1.................................................................................................................... 3

Issue........................................................................................................................ 3

Legal provisions.......................................................................................................3

Application on cited transactions.............................................................................4

Solution 2.................................................................................................................... 5

Issue........................................................................................................................ 5

Legal provisions.......................................................................................................5

Application on cited transactions.............................................................................5

Conclusion...............................................................................................................6

Solution 3.................................................................................................................... 6

Issue........................................................................................................................ 6

Legal provisions.......................................................................................................6

Calculations.............................................................................................................6

Solution 4.................................................................................................................... 8

Issue........................................................................................................................ 8

Legal provisions and Calculations...........................................................................8

References................................................................................................................10

Solution 1.................................................................................................................... 3

Issue........................................................................................................................ 3

Legal provisions.......................................................................................................3

Application on cited transactions.............................................................................4

Solution 2.................................................................................................................... 5

Issue........................................................................................................................ 5

Legal provisions.......................................................................................................5

Application on cited transactions.............................................................................5

Conclusion...............................................................................................................6

Solution 3.................................................................................................................... 6

Issue........................................................................................................................ 6

Legal provisions.......................................................................................................6

Calculations.............................................................................................................6

Solution 4.................................................................................................................... 8

Issue........................................................................................................................ 8

Legal provisions and Calculations...........................................................................8

References................................................................................................................10

SOLUTION 1

Issue

The issue is to determine whether the following cited expense are allowable as

general deductions under section 8.1 ITAA 1997.

Expense 1 The cost of moving machinery to a new site

Expense 2 The cost of revaluing assets to effect insurance cover

Expense 3 Legal Expenses incurred by a company opposing a petition for

winding up

Expense 4 Legal Expenses incurred for services of a solicitor in respect of a

number of matters

Legal provisions

Calculation of income tax is done according to the taxable income of taxpayer.

Further the taxable income is computed by subtracting general and specific

deductions from the total assessable income of taxpayer (Somers and Eynaud,

2015).

In accordance with ITAA97 s 8-1, a general deduction is loss/expense that contains

an applicable relation with the income generating activities, such as personal efforts,

investment or operating activities, but it is not of capital and neither of domestic

nature.

SECTION 8-1 (General deductions)

One can make deduction from their assessable income if any loss/outgoing satisfies

one of the following two provisions:

If the loss/outgoing is incurred while producing or gaining assessable income

It is automatically incurred in carrying a business with the intention of

producing or gaining assessable income (SECTION 8-1 General deductions,

2017).

Under s 8-1(2), one the other hand one cannot make deductions from their

assessable income if any loss/expense if following cited aspect is satisfied as Act

does not allow to make deduction:

Issue

The issue is to determine whether the following cited expense are allowable as

general deductions under section 8.1 ITAA 1997.

Expense 1 The cost of moving machinery to a new site

Expense 2 The cost of revaluing assets to effect insurance cover

Expense 3 Legal Expenses incurred by a company opposing a petition for

winding up

Expense 4 Legal Expenses incurred for services of a solicitor in respect of a

number of matters

Legal provisions

Calculation of income tax is done according to the taxable income of taxpayer.

Further the taxable income is computed by subtracting general and specific

deductions from the total assessable income of taxpayer (Somers and Eynaud,

2015).

In accordance with ITAA97 s 8-1, a general deduction is loss/expense that contains

an applicable relation with the income generating activities, such as personal efforts,

investment or operating activities, but it is not of capital and neither of domestic

nature.

SECTION 8-1 (General deductions)

One can make deduction from their assessable income if any loss/outgoing satisfies

one of the following two provisions:

If the loss/outgoing is incurred while producing or gaining assessable income

It is automatically incurred in carrying a business with the intention of

producing or gaining assessable income (SECTION 8-1 General deductions,

2017).

Under s 8-1(2), one the other hand one cannot make deductions from their

assessable income if any loss/expense if following cited aspect is satisfied as Act

does not allow to make deduction:

If it is held as a loss/expense of a capital nature

If it is held as a loss/ expense of private nature

If it is incurred regarding the producing or gaining of non-assessable income

or exempt income

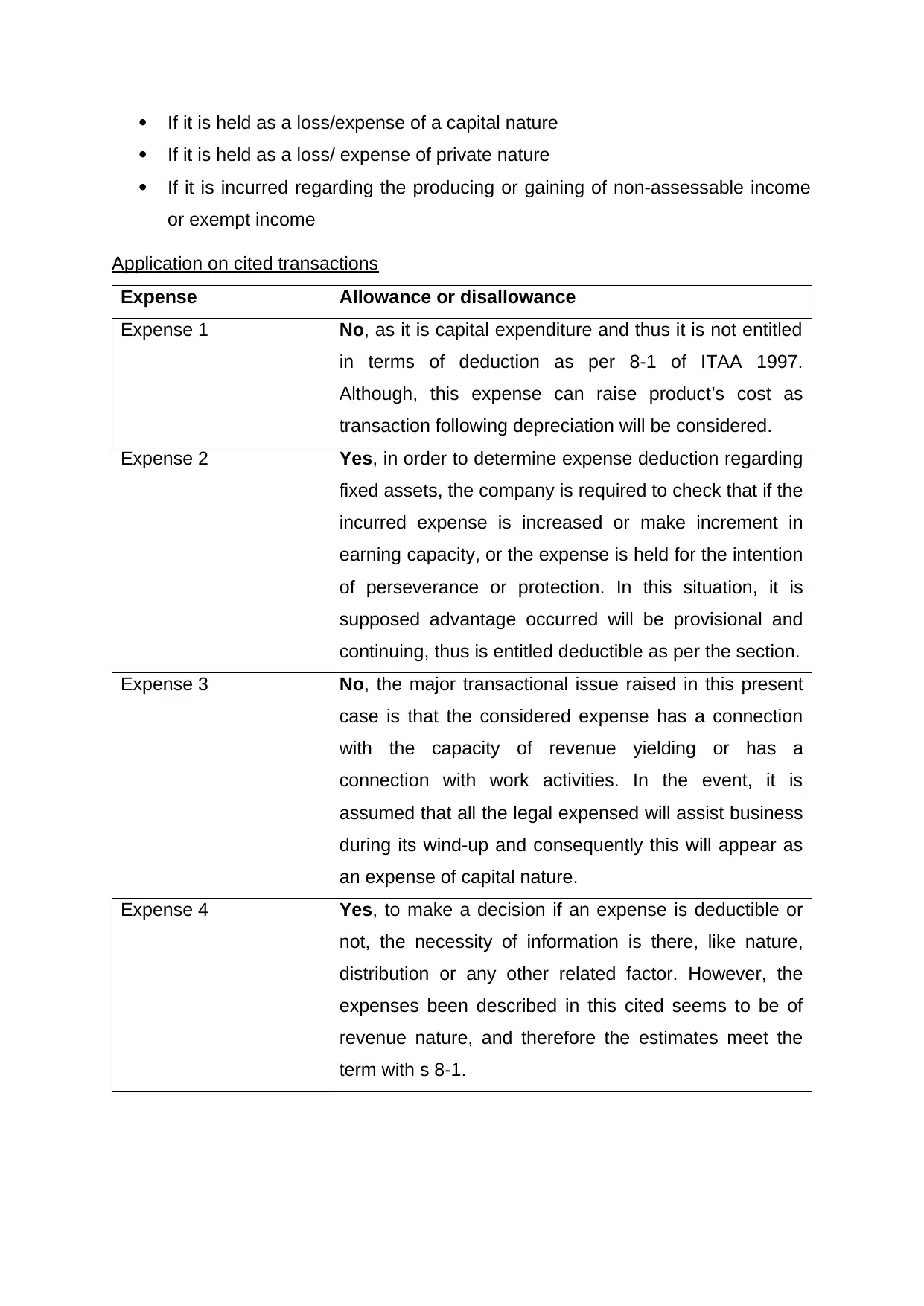

Application on cited transactions

Expense Allowance or disallowance

Expense 1 No, as it is capital expenditure and thus it is not entitled

in terms of deduction as per 8-1 of ITAA 1997.

Although, this expense can raise product’s cost as

transaction following depreciation will be considered.

Expense 2 Yes, in order to determine expense deduction regarding

fixed assets, the company is required to check that if the

incurred expense is increased or make increment in

earning capacity, or the expense is held for the intention

of perseverance or protection. In this situation, it is

supposed advantage occurred will be provisional and

continuing, thus is entitled deductible as per the section.

Expense 3 No, the major transactional issue raised in this present

case is that the considered expense has a connection

with the capacity of revenue yielding or has a

connection with work activities. In the event, it is

assumed that all the legal expensed will assist business

during its wind-up and consequently this will appear as

an expense of capital nature.

Expense 4 Yes, to make a decision if an expense is deductible or

not, the necessity of information is there, like nature,

distribution or any other related factor. However, the

expenses been described in this cited seems to be of

revenue nature, and therefore the estimates meet the

term with s 8-1.

If it is held as a loss/ expense of private nature

If it is incurred regarding the producing or gaining of non-assessable income

or exempt income

Application on cited transactions

Expense Allowance or disallowance

Expense 1 No, as it is capital expenditure and thus it is not entitled

in terms of deduction as per 8-1 of ITAA 1997.

Although, this expense can raise product’s cost as

transaction following depreciation will be considered.

Expense 2 Yes, in order to determine expense deduction regarding

fixed assets, the company is required to check that if the

incurred expense is increased or make increment in

earning capacity, or the expense is held for the intention

of perseverance or protection. In this situation, it is

supposed advantage occurred will be provisional and

continuing, thus is entitled deductible as per the section.

Expense 3 No, the major transactional issue raised in this present

case is that the considered expense has a connection

with the capacity of revenue yielding or has a

connection with work activities. In the event, it is

assumed that all the legal expensed will assist business

during its wind-up and consequently this will appear as

an expense of capital nature.

Expense 4 Yes, to make a decision if an expense is deductible or

not, the necessity of information is there, like nature,

distribution or any other related factor. However, the

expenses been described in this cited seems to be of

revenue nature, and therefore the estimates meet the

term with s 8-1.

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

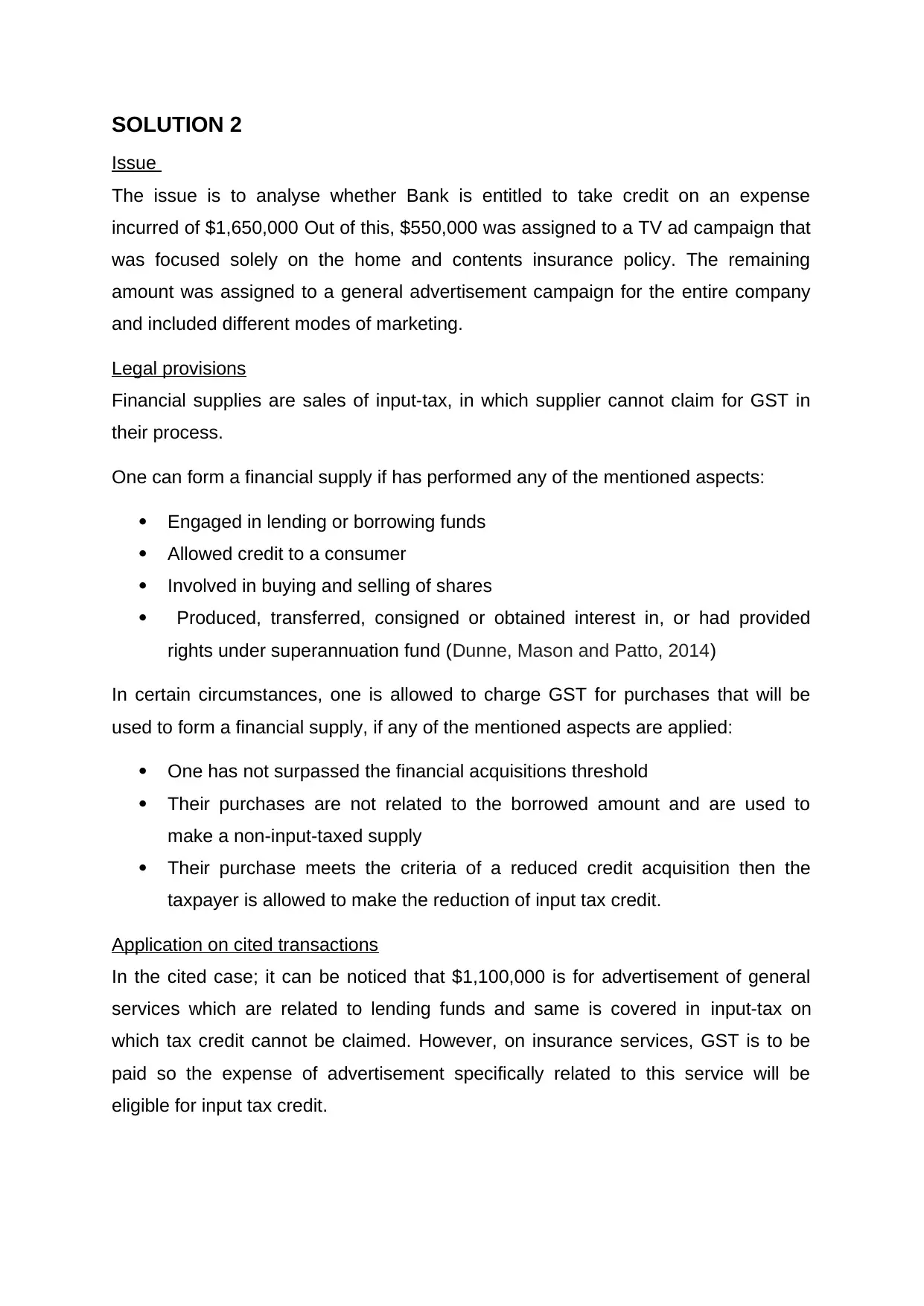

SOLUTION 2

Issue

The issue is to analyse whether Bank is entitled to take credit on an expense

incurred of $1,650,000 Out of this, $550,000 was assigned to a TV ad campaign that

was focused solely on the home and contents insurance policy. The remaining

amount was assigned to a general advertisement campaign for the entire company

and included different modes of marketing.

Legal provisions

Financial supplies are sales of input-tax, in which supplier cannot claim for GST in

their process.

One can form a financial supply if has performed any of the mentioned aspects:

Engaged in lending or borrowing funds

Allowed credit to a consumer

Involved in buying and selling of shares

Produced, transferred, consigned or obtained interest in, or had provided

rights under superannuation fund (Dunne, Mason and Patto, 2014)

In certain circumstances, one is allowed to charge GST for purchases that will be

used to form a financial supply, if any of the mentioned aspects are applied:

One has not surpassed the financial acquisitions threshold

Their purchases are not related to the borrowed amount and are used to

make a non-input-taxed supply

Their purchase meets the criteria of a reduced credit acquisition then the

taxpayer is allowed to make the reduction of input tax credit.

Application on cited transactions

In the cited case; it can be noticed that $1,100,000 is for advertisement of general

services which are related to lending funds and same is covered in input-tax on

which tax credit cannot be claimed. However, on insurance services, GST is to be

paid so the expense of advertisement specifically related to this service will be

eligible for input tax credit.

Issue

The issue is to analyse whether Bank is entitled to take credit on an expense

incurred of $1,650,000 Out of this, $550,000 was assigned to a TV ad campaign that

was focused solely on the home and contents insurance policy. The remaining

amount was assigned to a general advertisement campaign for the entire company

and included different modes of marketing.

Legal provisions

Financial supplies are sales of input-tax, in which supplier cannot claim for GST in

their process.

One can form a financial supply if has performed any of the mentioned aspects:

Engaged in lending or borrowing funds

Allowed credit to a consumer

Involved in buying and selling of shares

Produced, transferred, consigned or obtained interest in, or had provided

rights under superannuation fund (Dunne, Mason and Patto, 2014)

In certain circumstances, one is allowed to charge GST for purchases that will be

used to form a financial supply, if any of the mentioned aspects are applied:

One has not surpassed the financial acquisitions threshold

Their purchases are not related to the borrowed amount and are used to

make a non-input-taxed supply

Their purchase meets the criteria of a reduced credit acquisition then the

taxpayer is allowed to make the reduction of input tax credit.

Application on cited transactions

In the cited case; it can be noticed that $1,100,000 is for advertisement of general

services which are related to lending funds and same is covered in input-tax on

which tax credit cannot be claimed. However, on insurance services, GST is to be

paid so the expense of advertisement specifically related to this service will be

eligible for input tax credit.

Conclusion

Credit can only be availed for the amount of $550,000, as it was to be paid to a

campaign of television advertising for the promotion of Big Bank home and contents

insurance policies.

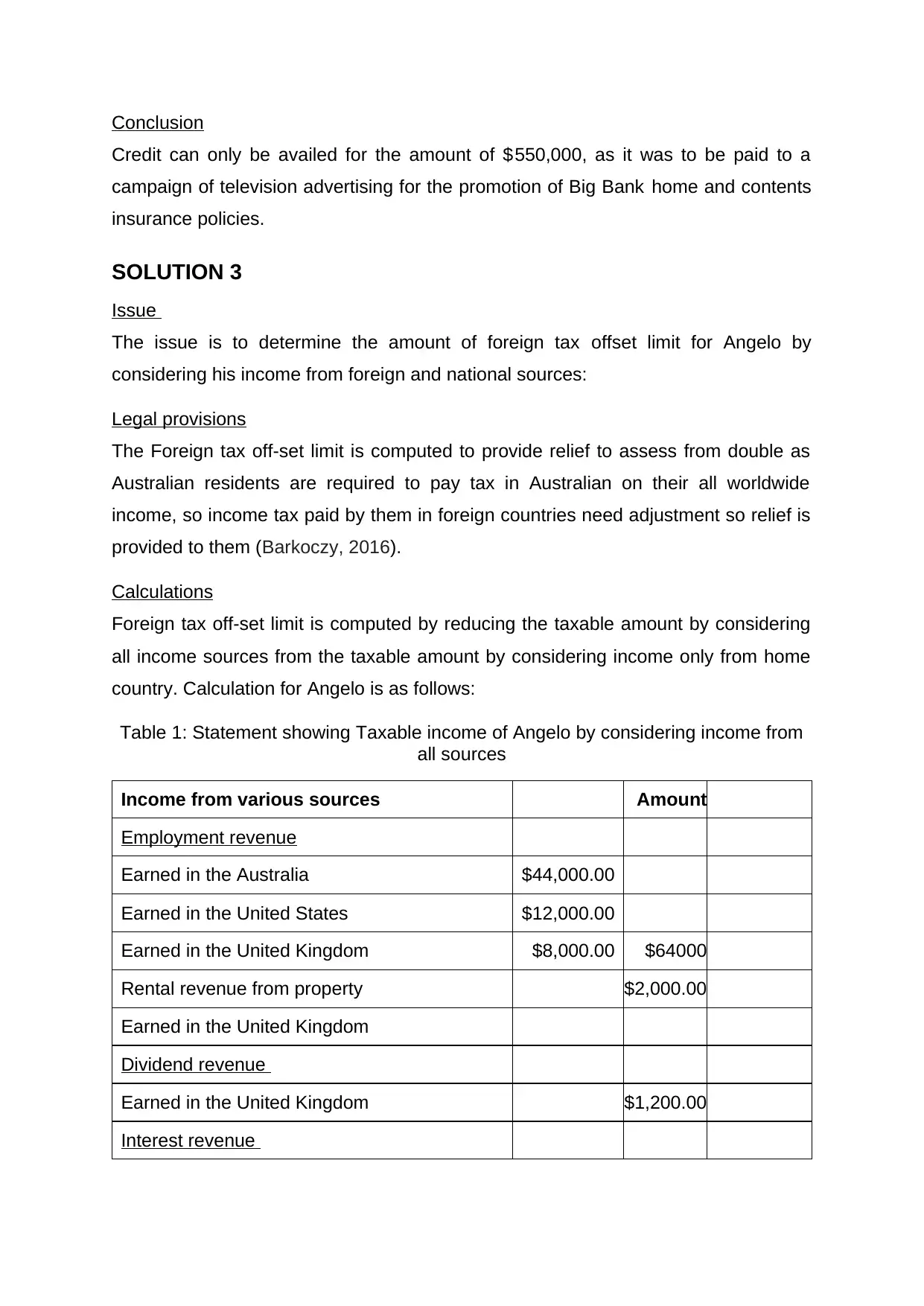

SOLUTION 3

Issue

The issue is to determine the amount of foreign tax offset limit for Angelo by

considering his income from foreign and national sources:

Legal provisions

The Foreign tax off-set limit is computed to provide relief to assess from double as

Australian residents are required to pay tax in Australian on their all worldwide

income, so income tax paid by them in foreign countries need adjustment so relief is

provided to them (Barkoczy, 2016).

Calculations

Foreign tax off-set limit is computed by reducing the taxable amount by considering

all income sources from the taxable amount by considering income only from home

country. Calculation for Angelo is as follows:

Table 1: Statement showing Taxable income of Angelo by considering income from

all sources

Income from various sources Amount

Employment revenue

Earned in the Australia $44,000.00

Earned in the United States $12,000.00

Earned in the United Kingdom $8,000.00 $64000

Rental revenue from property $2,000.00

Earned in the United Kingdom

Dividend revenue

Earned in the United Kingdom $1,200.00

Interest revenue

Credit can only be availed for the amount of $550,000, as it was to be paid to a

campaign of television advertising for the promotion of Big Bank home and contents

insurance policies.

SOLUTION 3

Issue

The issue is to determine the amount of foreign tax offset limit for Angelo by

considering his income from foreign and national sources:

Legal provisions

The Foreign tax off-set limit is computed to provide relief to assess from double as

Australian residents are required to pay tax in Australian on their all worldwide

income, so income tax paid by them in foreign countries need adjustment so relief is

provided to them (Barkoczy, 2016).

Calculations

Foreign tax off-set limit is computed by reducing the taxable amount by considering

all income sources from the taxable amount by considering income only from home

country. Calculation for Angelo is as follows:

Table 1: Statement showing Taxable income of Angelo by considering income from

all sources

Income from various sources Amount

Employment revenue

Earned in the Australia $44,000.00

Earned in the United States $12,000.00

Earned in the United Kingdom $8,000.00 $64000

Rental revenue from property $2,000.00

Earned in the United Kingdom

Dividend revenue

Earned in the United Kingdom $1,200.00

Interest revenue

Earned in the United Kingdom $800.00

Total gross income $68000.00

Allowable deductions

Expenses incurred for earning employment

income

From the Australia $4,000.00

From the United States $900.00 $4900

Expenses incurred for earning rental income

From the United Kingdom $500.00

Gift to a deductible gift recipient $400.00

Interest paid to obtain dividend income $140.00

Expenses incurred to earn interest income $60.00

Total allowable deductions $6000.00

Taxable income $62000.00

Total tax payable** $12937.00*

*Low-income off tax is not considered

** (Tax on income + Medicare levy)

Table 2: Statement showing Taxable amount for Angelo by considering income of

Australia

Income from various sources Amount

Employment income $44,000.00

Allowable deductions

Expenses incurred for earning employment income $4,000.00

Gift to a deductible gift recipient $400.00

Interest paid to obtain dividend income $140.00

Expenses incurred to earn interest income $60.00

Total allowable deductions $4600.00

Taxable income $39400.00

Total gross income $68000.00

Allowable deductions

Expenses incurred for earning employment

income

From the Australia $4,000.00

From the United States $900.00 $4900

Expenses incurred for earning rental income

From the United Kingdom $500.00

Gift to a deductible gift recipient $400.00

Interest paid to obtain dividend income $140.00

Expenses incurred to earn interest income $60.00

Total allowable deductions $6000.00

Taxable income $62000.00

Total tax payable** $12937.00*

*Low-income off tax is not considered

** (Tax on income + Medicare levy)

Table 2: Statement showing Taxable amount for Angelo by considering income of

Australia

Income from various sources Amount

Employment income $44,000.00

Allowable deductions

Expenses incurred for earning employment income $4,000.00

Gift to a deductible gift recipient $400.00

Interest paid to obtain dividend income $140.00

Expenses incurred to earn interest income $60.00

Total allowable deductions $4600.00

Taxable income $39400.00

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

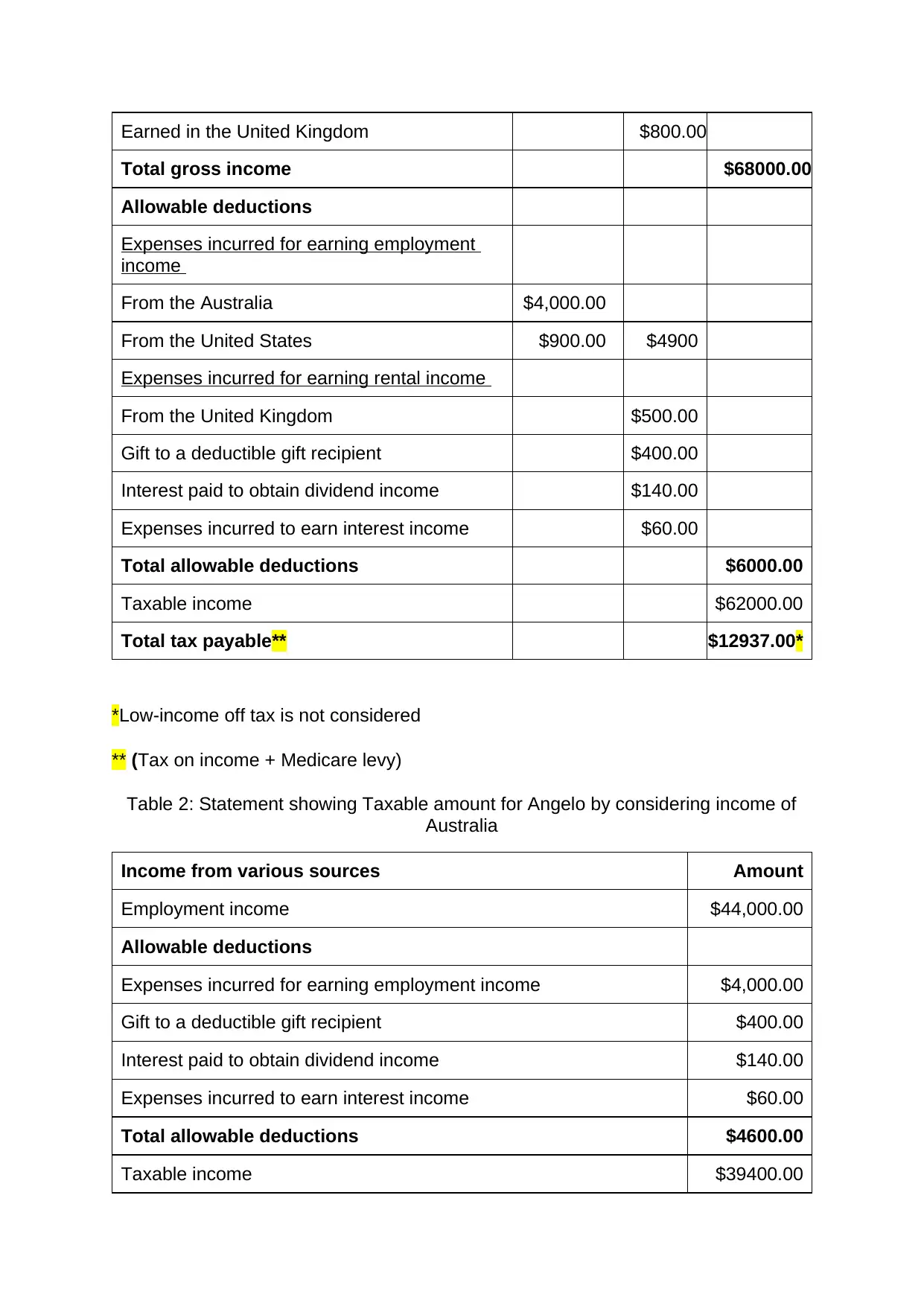

Total tax payable (Tax on income + Medicare levy) $5140.00*

*Low-income off tax is not considered

** (Tax on income + Medicare levy)

Table 3: Statement showing offset limit

Taxable income of Angelo by considering income from all sources $12937.00

Taxable amount for Angelo by considering income of Australia $5140.00

Offset limit $7797.00

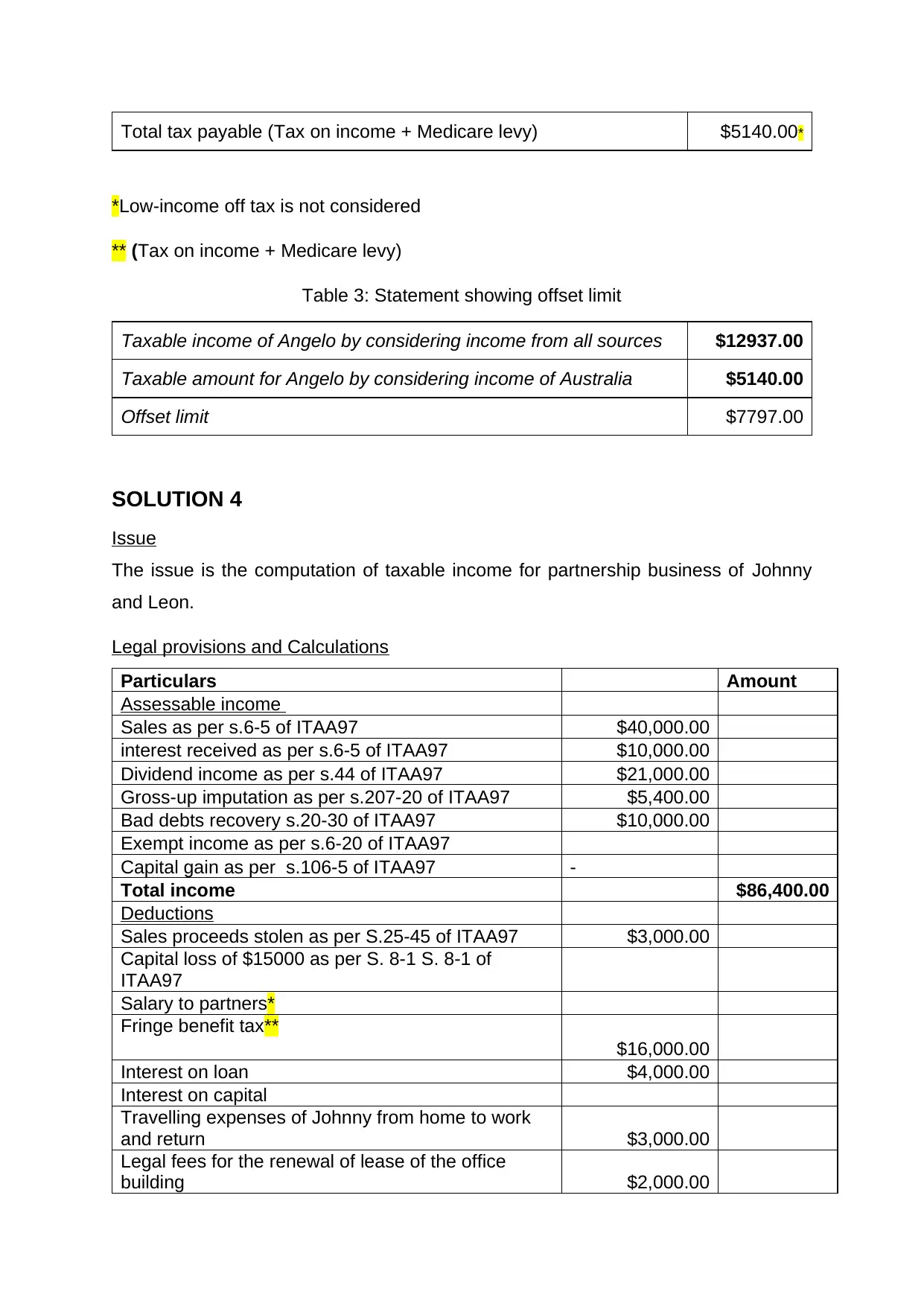

SOLUTION 4

Issue

The issue is the computation of taxable income for partnership business of Johnny

and Leon.

Legal provisions and Calculations

Particulars Amount

Assessable income

Sales as per s.6-5 of ITAA97 $40,000.00

interest received as per s.6-5 of ITAA97 $10,000.00

Dividend income as per s.44 of ITAA97 $21,000.00

Gross-up imputation as per s.207-20 of ITAA97 $5,400.00

Bad debts recovery s.20-30 of ITAA97 $10,000.00

Exempt income as per s.6-20 of ITAA97

Capital gain as per s.106-5 of ITAA97 -

Total income $86,400.00

Deductions

Sales proceeds stolen as per S.25-45 of ITAA97 $3,000.00

Capital loss of $15000 as per S. 8-1 S. 8-1 of

ITAA97

Salary to partners*

Fringe benefit tax**

$16,000.00

Interest on loan $4,000.00

Interest on capital

Travelling expenses of Johnny from home to work

and return $3,000.00

Legal fees for the renewal of lease of the office

building $2,000.00

*Low-income off tax is not considered

** (Tax on income + Medicare levy)

Table 3: Statement showing offset limit

Taxable income of Angelo by considering income from all sources $12937.00

Taxable amount for Angelo by considering income of Australia $5140.00

Offset limit $7797.00

SOLUTION 4

Issue

The issue is the computation of taxable income for partnership business of Johnny

and Leon.

Legal provisions and Calculations

Particulars Amount

Assessable income

Sales as per s.6-5 of ITAA97 $40,000.00

interest received as per s.6-5 of ITAA97 $10,000.00

Dividend income as per s.44 of ITAA97 $21,000.00

Gross-up imputation as per s.207-20 of ITAA97 $5,400.00

Bad debts recovery s.20-30 of ITAA97 $10,000.00

Exempt income as per s.6-20 of ITAA97

Capital gain as per s.106-5 of ITAA97 -

Total income $86,400.00

Deductions

Sales proceeds stolen as per S.25-45 of ITAA97 $3,000.00

Capital loss of $15000 as per S. 8-1 S. 8-1 of

ITAA97

Salary to partners*

Fringe benefit tax**

$16,000.00

Interest on loan $4,000.00

Interest on capital

Travelling expenses of Johnny from home to work

and return $3,000.00

Legal fees for the renewal of lease of the office

building $2,000.00

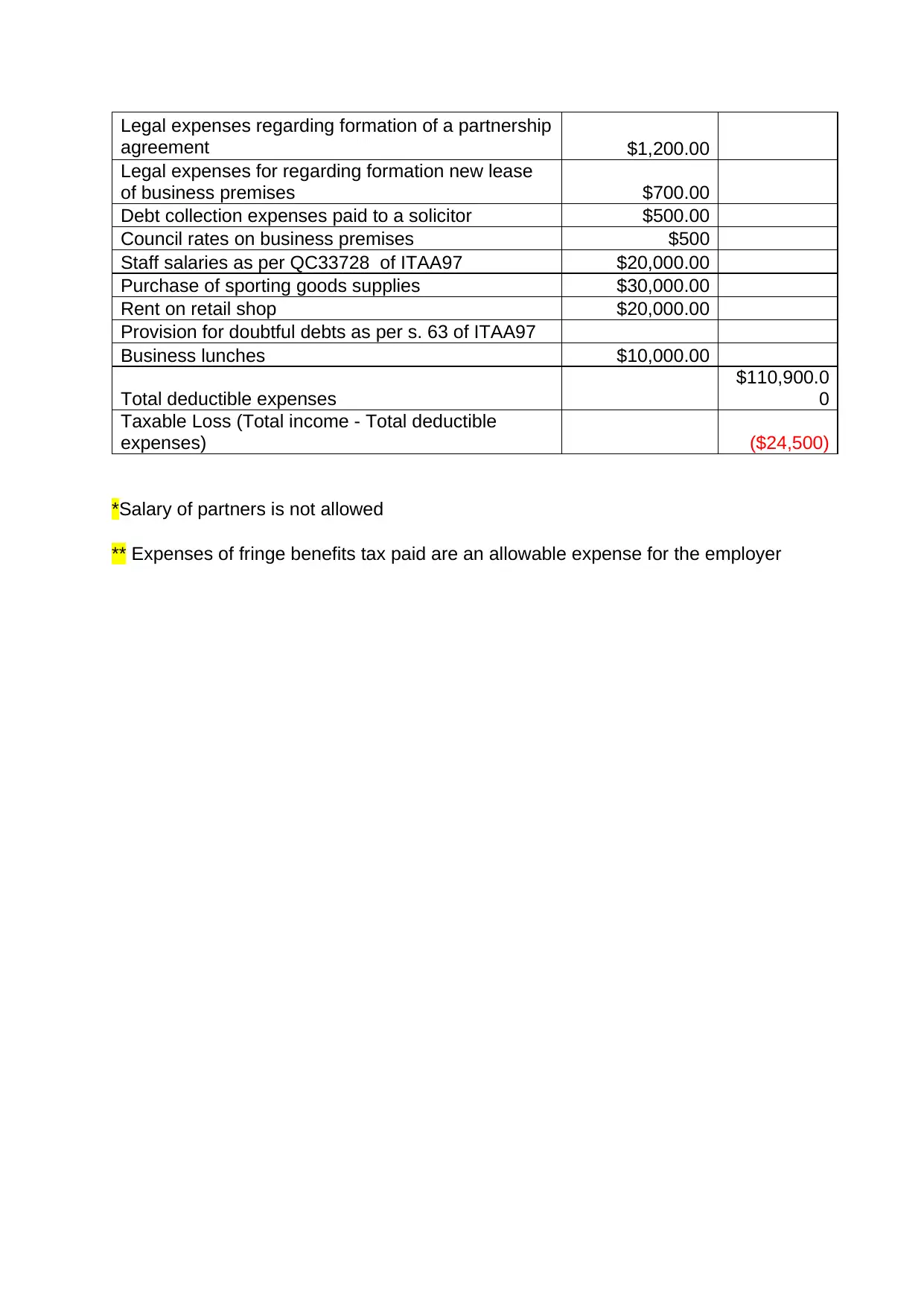

Legal expenses regarding formation of a partnership

agreement $1,200.00

Legal expenses for regarding formation new lease

of business premises $700.00

Debt collection expenses paid to a solicitor $500.00

Council rates on business premises $500

Staff salaries as per QC33728 of ITAA97 $20,000.00

Purchase of sporting goods supplies $30,000.00

Rent on retail shop $20,000.00

Provision for doubtful debts as per s. 63 of ITAA97

Business lunches $10,000.00

Total deductible expenses

$110,900.0

0

Taxable Loss (Total income - Total deductible

expenses) ($24,500)

*Salary of partners is not allowed

** Expenses of fringe benefits tax paid are an allowable expense for the employer

agreement $1,200.00

Legal expenses for regarding formation new lease

of business premises $700.00

Debt collection expenses paid to a solicitor $500.00

Council rates on business premises $500

Staff salaries as per QC33728 of ITAA97 $20,000.00

Purchase of sporting goods supplies $30,000.00

Rent on retail shop $20,000.00

Provision for doubtful debts as per s. 63 of ITAA97

Business lunches $10,000.00

Total deductible expenses

$110,900.0

0

Taxable Loss (Total income - Total deductible

expenses) ($24,500)

*Salary of partners is not allowed

** Expenses of fringe benefits tax paid are an allowable expense for the employer

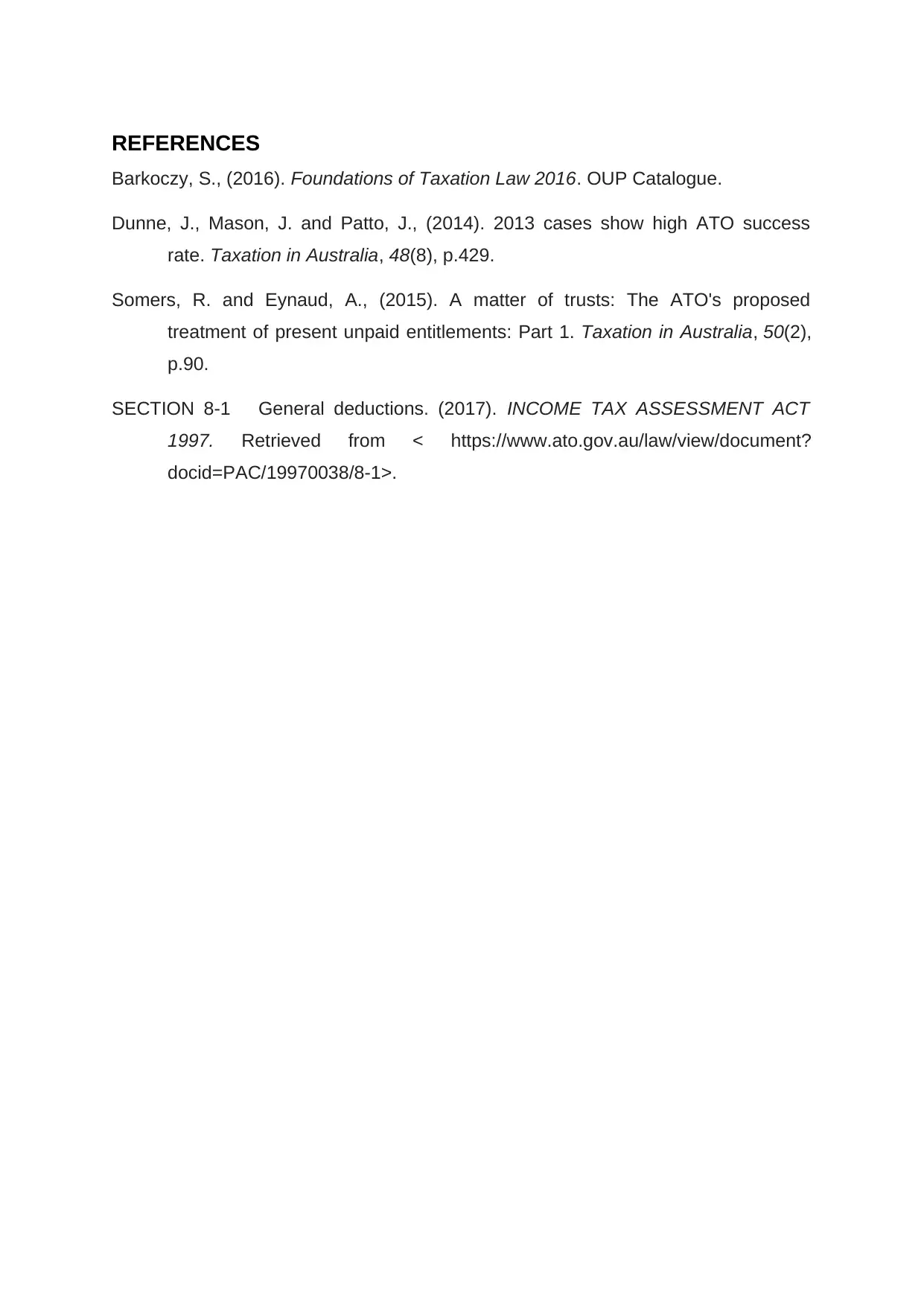

REFERENCES

Barkoczy, S., (2016). Foundations of Taxation Law 2016. OUP Catalogue.

Dunne, J., Mason, J. and Patto, J., (2014). 2013 cases show high ATO success

rate. Taxation in Australia, 48(8), p.429.

Somers, R. and Eynaud, A., (2015). A matter of trusts: The ATO's proposed

treatment of present unpaid entitlements: Part 1. Taxation in Australia, 50(2),

p.90.

SECTION 8-1 General deductions. (2017). INCOME TAX ASSESSMENT ACT

1997. Retrieved from < https://www.ato.gov.au/law/view/document?

docid=PAC/19970038/8-1>.

Barkoczy, S., (2016). Foundations of Taxation Law 2016. OUP Catalogue.

Dunne, J., Mason, J. and Patto, J., (2014). 2013 cases show high ATO success

rate. Taxation in Australia, 48(8), p.429.

Somers, R. and Eynaud, A., (2015). A matter of trusts: The ATO's proposed

treatment of present unpaid entitlements: Part 1. Taxation in Australia, 50(2),

p.90.

SECTION 8-1 General deductions. (2017). INCOME TAX ASSESSMENT ACT

1997. Retrieved from < https://www.ato.gov.au/law/view/document?

docid=PAC/19970038/8-1>.

1 out of 10

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

© 2024 | Zucol Services PVT LTD | All rights reserved.