Detailed Analysis of VAT Regulations, Compliance, and Financial Impact

VerifiedAdded on 2020/12/23

|14

|3988

|90

Report

AI Summary

This report provides a comprehensive overview of Value Added Tax (VAT) regulations. It begins with an introduction to indirect taxes and VAT, explaining its sources and how organizations interact with government agencies like HMRC. The report details VAT registration requirements, the information needed on business documentation, and various implemented schemes for VAT-registered businesses, including flat-rate, cash accounting, annual accounting, and retail/margin schemes. It emphasizes the importance of staying updated on changes to codes of practice, regulations, and legislation to avoid penalties. The report includes examples of data analysis from accounting systems, the calculation of input and output VAT, and VAT return processes. It also discusses the implications and penalties for non-compliance with VAT regulations, making declarations and adjustments for errors, and informing managers about the impact of changes in VAT laws on an organization's finances. Finally, the report covers how to advise relevant people of changes in VAT legislation, and concludes with references to support the information presented.

Indirect Tax

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of Contents

INTRODUCTION...........................................................................................................................1

1.1 Source of information on VAT.............................................................................................1

1.2 How organisation interact with government agency.............................................................1

1.3 Value added tax registration requirement.............................................................................2

1.4 Information which needs to included on business documentation of VAT registered

businesses....................................................................................................................................2

1.5 Implemented schemes for VAT registered businesses..........................................................3

1.6 Maintaining an up-to-date knowledge of changes to codes of practice, regulation or

legislation....................................................................................................................................4

2.1 Relevant data for a specific period from accounting system................................................5

2.2 Calculation of inputs and outputs using the VAT classification...........................................5

2.3 Calculation of VAT due to / from relevant tax authority......................................................6

2.4 VAT return and any associated payment within the statutory time limit.............................7

3.1 Implications and Penalties for an organisation resulting from failure to abide by VAT

Regulations..................................................................................................................................7

3.2 Making Declarations and Adjustments on the Previously Occurred Errors and Rectifying

them.............................................................................................................................................8

4.1 Informing Managers about the Impact of Change in the VAT Laws on Organisation's Cash

Flows and Financial Forecasts....................................................................................................8

4.2 Advise Relevant People of Changes in VAT Legislation which would have an Effect on

an.................................................................................................................................................9

CONCLUSION................................................................................................................................9

REFERENCES..............................................................................................................................11

INTRODUCTION...........................................................................................................................1

1.1 Source of information on VAT.............................................................................................1

1.2 How organisation interact with government agency.............................................................1

1.3 Value added tax registration requirement.............................................................................2

1.4 Information which needs to included on business documentation of VAT registered

businesses....................................................................................................................................2

1.5 Implemented schemes for VAT registered businesses..........................................................3

1.6 Maintaining an up-to-date knowledge of changes to codes of practice, regulation or

legislation....................................................................................................................................4

2.1 Relevant data for a specific period from accounting system................................................5

2.2 Calculation of inputs and outputs using the VAT classification...........................................5

2.3 Calculation of VAT due to / from relevant tax authority......................................................6

2.4 VAT return and any associated payment within the statutory time limit.............................7

3.1 Implications and Penalties for an organisation resulting from failure to abide by VAT

Regulations..................................................................................................................................7

3.2 Making Declarations and Adjustments on the Previously Occurred Errors and Rectifying

them.............................................................................................................................................8

4.1 Informing Managers about the Impact of Change in the VAT Laws on Organisation's Cash

Flows and Financial Forecasts....................................................................................................8

4.2 Advise Relevant People of Changes in VAT Legislation which would have an Effect on

an.................................................................................................................................................9

CONCLUSION................................................................................................................................9

REFERENCES..............................................................................................................................11

INTRODUCTION

Indirect tax is a source of revenues for the government from the producer or retailer. This

amount is passed on consumers as part of their purchasing goods and services. Basically there

are two types of taxes which is levied on consumers direct and indirect tax. Direct tax includes

income tax and indirect tax includes sales tax, custom duties on import, excise duty on

production and value added tax (VAT). The main aim of this report is to understand various

VAT regulations. Apart from this the report discuss about accurate value added tax returns

within a given time period. The different penalties on value added tax and adjustments for

previous errors is being discussed in this report. There can great impact of indirect tax on cash

flows and financial forecasts of an organisation which is also discussed in this report.

1.1 Source of information on VAT

Value added tax is an indirect tax which is implied by the government on consumption of

goods and services by end consumers. The tax is levied on producer or retailer and than they

charge it from customers in order to pay to the government. This is a liability for retailer and

producers which is imposed by government (Littlewood, Murphy and Wang, 2013). This tax is

not applicable on all cities however some cities are exempted from this tax. The VAT payable by

a person is calculated by deducting inputs used for production of goods and services from cost of

products. There different sources for getting VAT information but reliable information can be

availed through federal government sites. Apart from this, HM revenue and customs portal

which is liable for collecting tax across UK. The different sources are discussed as below:

HMRC VAT – Traders registered for VAT purposes with HMRC

HMRC PAYE – Employers operating a PAYE scheme registered with HMRC

Companies house – Incorporated businesses registered at companies house

These are sources through which one can avail the information regarding VAT and its

compliances and can get benefit out of this.

1.2 How organisation interact with government agency

There are various government departments which circulate the laws and legislation for

organisations according to their nature. The organisations have to comply with these laws in

order to maintain their business in smooth way. While comply with these laws, organisations

faces various complication which can be solved by the government agencies. For example

1

Indirect tax is a source of revenues for the government from the producer or retailer. This

amount is passed on consumers as part of their purchasing goods and services. Basically there

are two types of taxes which is levied on consumers direct and indirect tax. Direct tax includes

income tax and indirect tax includes sales tax, custom duties on import, excise duty on

production and value added tax (VAT). The main aim of this report is to understand various

VAT regulations. Apart from this the report discuss about accurate value added tax returns

within a given time period. The different penalties on value added tax and adjustments for

previous errors is being discussed in this report. There can great impact of indirect tax on cash

flows and financial forecasts of an organisation which is also discussed in this report.

1.1 Source of information on VAT

Value added tax is an indirect tax which is implied by the government on consumption of

goods and services by end consumers. The tax is levied on producer or retailer and than they

charge it from customers in order to pay to the government. This is a liability for retailer and

producers which is imposed by government (Littlewood, Murphy and Wang, 2013). This tax is

not applicable on all cities however some cities are exempted from this tax. The VAT payable by

a person is calculated by deducting inputs used for production of goods and services from cost of

products. There different sources for getting VAT information but reliable information can be

availed through federal government sites. Apart from this, HM revenue and customs portal

which is liable for collecting tax across UK. The different sources are discussed as below:

HMRC VAT – Traders registered for VAT purposes with HMRC

HMRC PAYE – Employers operating a PAYE scheme registered with HMRC

Companies house – Incorporated businesses registered at companies house

These are sources through which one can avail the information regarding VAT and its

compliances and can get benefit out of this.

1.2 How organisation interact with government agency

There are various government departments which circulate the laws and legislation for

organisations according to their nature. The organisations have to comply with these laws in

order to maintain their business in smooth way. While comply with these laws, organisations

faces various complication which can be solved by the government agencies. For example

1

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

companies are facing issue in filling VAT returns than they have to communicate with HMRC.

So to communicate with related organisation company can use internet communication such as

E-mail and other social media where agencies are active. Beside this organisations can

communicate with government agency by going to their respective offices in order to solve the

queries. The interaction between government and organisations are very important for

sustainable for long term period in marketplace. As leader of the specific industry can also meet

personally with government agencies for issues which are faced by companies (LandWhalley,

2012).

1.3 Value added tax registration requirement

VAT is a source of revenue for government which is imposed by administration on the

various kinds of goods and services in a country. In UK if company or firm has the more than

GBP 85000 taxable turnover than they are obliged to register for value added tax (VAT

Registration. 2019). The registration of this indirect tax in not a tough task but it is mandatory

for all those who falls under category which limit is set by government. If firm has not this

turnover than they can also register as voluntarily. For register themselves as VAT company are

required to apply to HMRC. There is an online portal also for organisation which helps them

apply for registration online. The organisation can register with help of an accountant or an agent

also as they have better knowledge for registration. Company have to use VAT1 form for

registered as exception . This case also applied when firm wants to apply for Agricultural flat

rate. Company needs file VAT1A if there business is in Europe and is in distance selling and

company has to file VAT1B if there taxable turnover is more than GBP 85000 from another

country. The last form which is available is VAT1C if company is disposing asset in which 8th or

13th directive refunds have been claimed. After receiving VAT numbers from HMRC the

organisation can submit returns.

1.4 Information which needs to included on business documentation of VAT registered

businesses.

There are various documents which are required for registration and trading as a

registered firm. The companies and businesses are obliges to give the VAT number written sales

invoice to their customers. The company has to follow regulation 16 which gives them the some

points that are to be followed by organisations while issuing invoice to the customers. These are

as follows:

2

So to communicate with related organisation company can use internet communication such as

E-mail and other social media where agencies are active. Beside this organisations can

communicate with government agency by going to their respective offices in order to solve the

queries. The interaction between government and organisations are very important for

sustainable for long term period in marketplace. As leader of the specific industry can also meet

personally with government agencies for issues which are faced by companies (LandWhalley,

2012).

1.3 Value added tax registration requirement

VAT is a source of revenue for government which is imposed by administration on the

various kinds of goods and services in a country. In UK if company or firm has the more than

GBP 85000 taxable turnover than they are obliged to register for value added tax (VAT

Registration. 2019). The registration of this indirect tax in not a tough task but it is mandatory

for all those who falls under category which limit is set by government. If firm has not this

turnover than they can also register as voluntarily. For register themselves as VAT company are

required to apply to HMRC. There is an online portal also for organisation which helps them

apply for registration online. The organisation can register with help of an accountant or an agent

also as they have better knowledge for registration. Company have to use VAT1 form for

registered as exception . This case also applied when firm wants to apply for Agricultural flat

rate. Company needs file VAT1A if there business is in Europe and is in distance selling and

company has to file VAT1B if there taxable turnover is more than GBP 85000 from another

country. The last form which is available is VAT1C if company is disposing asset in which 8th or

13th directive refunds have been claimed. After receiving VAT numbers from HMRC the

organisation can submit returns.

1.4 Information which needs to included on business documentation of VAT registered

businesses.

There are various documents which are required for registration and trading as a

registered firm. The companies and businesses are obliges to give the VAT number written sales

invoice to their customers. The company has to follow regulation 16 which gives them the some

points that are to be followed by organisations while issuing invoice to the customers. These are

as follows:

2

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

A recognised number

There should be time of supply of goods on invoice.

The date of issue of documents must be included on invoice

As name, address and registration number of supplier should be on the top of invoice.

For authentication of buyer, there should be buyer name, address and registration and if

there is no registration number than it should be left as blank.

Invoice must comprise a type of supply which may be categorised as:

The supply by sale

Supply on hire purchase

The loan supply

A supply with help of exchange

As supply which is made through the customer material

When there is supply by sale on commission (Lam and Ravussin, 2017).

1. As invoice must includes the recognition of products and services which are supplied.

2. There should be tax rate for every item which needs to be include in the separate column.

3. In the separate column MRP and amount of VAT should be entered so value can be

determined individually.

4. The cash discount needs to shown separately if it is offered to supplier.

Organisation can maintain some books of accounts also which helps them to file VAT

return and needs to furnish these books and accounts to authoriy.

1.5 Implemented schemes for VAT registered businesses

HM Revenue and Customs department has provided four schemes that cover different

registered businesses under its scope to meet the different needs such as governing principles

applicable to an organization's accounting and financial systems and disclosure under governing

laws. These schemes have been mentioned below:

Flat Rate VAT Accounting Scheme:

Flat rate VAT scheme says that a registered VAT business needs to pay a fixed rate of

VAT to the department of HM Revenue and Customs with no eligibilty on reclaims except when

a particular capital asset is valued more than £2,000. In order for a business to join this scheme, a

business must have a VAT turnover of £150,000 or less. The Flat rate VAT scheme, unlike other

3

There should be time of supply of goods on invoice.

The date of issue of documents must be included on invoice

As name, address and registration number of supplier should be on the top of invoice.

For authentication of buyer, there should be buyer name, address and registration and if

there is no registration number than it should be left as blank.

Invoice must comprise a type of supply which may be categorised as:

The supply by sale

Supply on hire purchase

The loan supply

A supply with help of exchange

As supply which is made through the customer material

When there is supply by sale on commission (Lam and Ravussin, 2017).

1. As invoice must includes the recognition of products and services which are supplied.

2. There should be tax rate for every item which needs to be include in the separate column.

3. In the separate column MRP and amount of VAT should be entered so value can be

determined individually.

4. The cash discount needs to shown separately if it is offered to supplier.

Organisation can maintain some books of accounts also which helps them to file VAT

return and needs to furnish these books and accounts to authoriy.

1.5 Implemented schemes for VAT registered businesses

HM Revenue and Customs department has provided four schemes that cover different

registered businesses under its scope to meet the different needs such as governing principles

applicable to an organization's accounting and financial systems and disclosure under governing

laws. These schemes have been mentioned below:

Flat Rate VAT Accounting Scheme:

Flat rate VAT scheme says that a registered VAT business needs to pay a fixed rate of

VAT to the department of HM Revenue and Customs with no eligibilty on reclaims except when

a particular capital asset is valued more than £2,000. In order for a business to join this scheme, a

business must have a VAT turnover of £150,000 or less. The Flat rate VAT scheme, unlike other

3

schemes, cannot be combined with other applicable schemes to avail multiple benefits by the

organisations.

VAT Cash Accounting Scheme:

VAT Cash Accounting Scheme demands that the taxable person needs to pay the

difference of purchase and sale invoices to the tax authorities as their VAT returns in a given

accounting period. This is generally applicable on firms that have a VAT taxable turnover of

£1.35 million or less. To avail benefits under multiple sections, this scheme can be clubbed with

accounting or retail and margin schemes accordingly (Kenyon, Langley and Paquin, 2012).

Annual Accounting Scheme:

Annual Accounting scheme requires a registered VAT business to pay returns on three

quarterly basis to the department of HM Revenue and Customs. Through this scheme, advance

VAT payments can be made and are eligible for a refund in case of any overpayment of bill. It is

not suitable for a business that reclaims regularly on its filings.

Retail and Margin Scheme:

Retail and Margin Schemes are organisation specific schemes that can be clubbed with

Cash accounting and Annual Accounting schemes to avail multiple benefits by organisations.

1.6 Maintaining an up-to-date knowledge of changes to codes of practice, regulation or

legislation

The taxable persons are liable to pay their due amounts within statutory time limits that

are in line with the codes, rules, regulations or legislations in effect. Hence, it is important for a

business or individual to maintain an up-to-date knowledge of any changes being made in these

areas. Any kind of lack or error discovered in the VAT returns due to negligence or deliberate

dismissal of invoices from tax filing can prove to be harmful to the reputation as well as they

may attract heavy penalties and interests from the tax authorities ranging between 15% to 100%

of amount due (Keen, 2013).

For instance, if an organisation does not file its VAT return on quarterly basis and due to

change in legislations it is now asked to file the returns on quarter-wise, any kind of error or

negligence in filing the VAT within the aforementioned time limit would hamper the operational

efficacies of the organisation since it would be charged a penalty that would require reduction in

cash-flows freely available to a business for meeting working capital requirements. Thus, it is

4

organisations.

VAT Cash Accounting Scheme:

VAT Cash Accounting Scheme demands that the taxable person needs to pay the

difference of purchase and sale invoices to the tax authorities as their VAT returns in a given

accounting period. This is generally applicable on firms that have a VAT taxable turnover of

£1.35 million or less. To avail benefits under multiple sections, this scheme can be clubbed with

accounting or retail and margin schemes accordingly (Kenyon, Langley and Paquin, 2012).

Annual Accounting Scheme:

Annual Accounting scheme requires a registered VAT business to pay returns on three

quarterly basis to the department of HM Revenue and Customs. Through this scheme, advance

VAT payments can be made and are eligible for a refund in case of any overpayment of bill. It is

not suitable for a business that reclaims regularly on its filings.

Retail and Margin Scheme:

Retail and Margin Schemes are organisation specific schemes that can be clubbed with

Cash accounting and Annual Accounting schemes to avail multiple benefits by organisations.

1.6 Maintaining an up-to-date knowledge of changes to codes of practice, regulation or

legislation

The taxable persons are liable to pay their due amounts within statutory time limits that

are in line with the codes, rules, regulations or legislations in effect. Hence, it is important for a

business or individual to maintain an up-to-date knowledge of any changes being made in these

areas. Any kind of lack or error discovered in the VAT returns due to negligence or deliberate

dismissal of invoices from tax filing can prove to be harmful to the reputation as well as they

may attract heavy penalties and interests from the tax authorities ranging between 15% to 100%

of amount due (Keen, 2013).

For instance, if an organisation does not file its VAT return on quarterly basis and due to

change in legislations it is now asked to file the returns on quarter-wise, any kind of error or

negligence in filing the VAT within the aforementioned time limit would hamper the operational

efficacies of the organisation since it would be charged a penalty that would require reduction in

cash-flows freely available to a business for meeting working capital requirements. Thus, it is

4

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

important to make sure that any legislation change is duly complied with to make sure no amount

is paid in excess or less by the business to tax authorities.

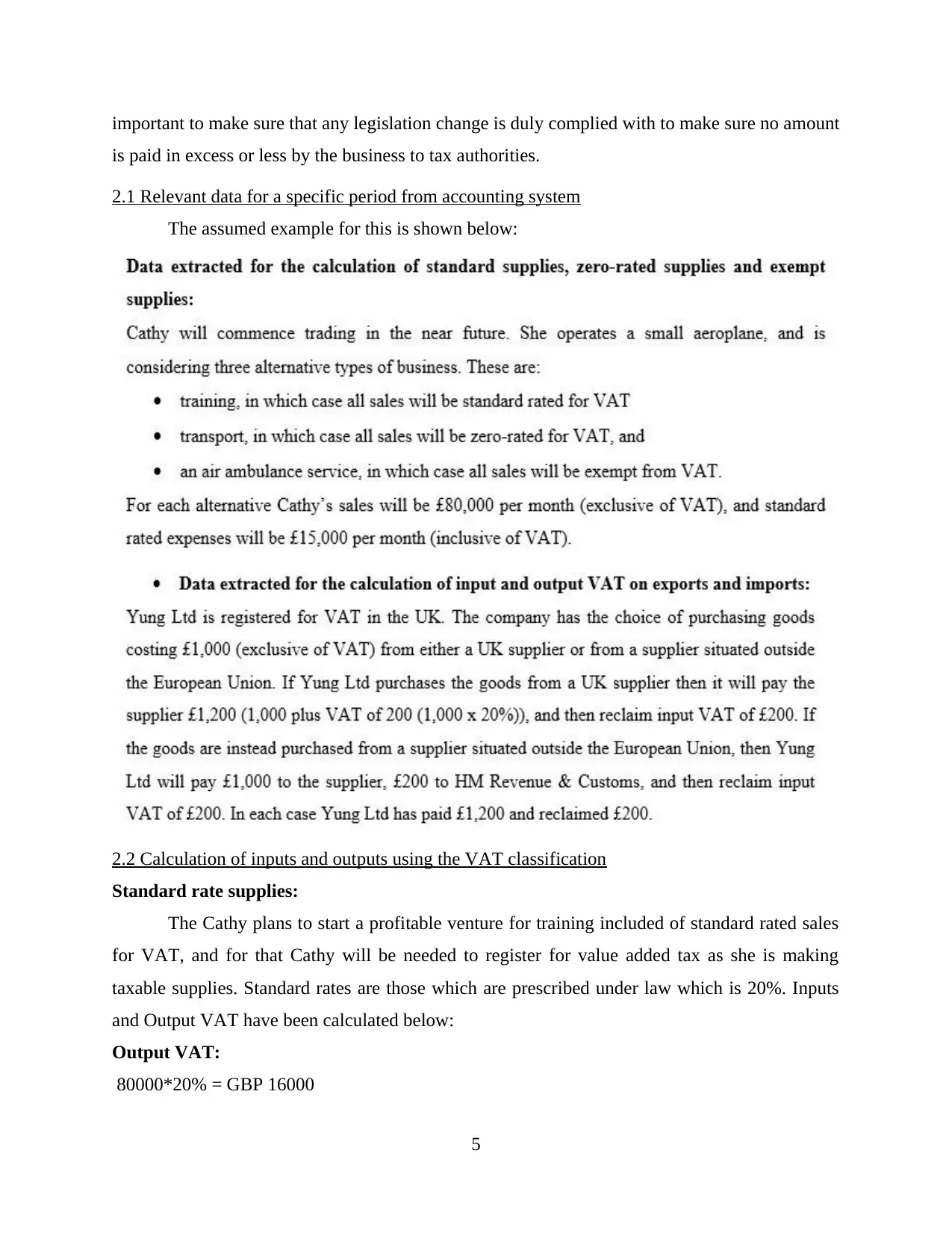

2.1 Relevant data for a specific period from accounting system

The assumed example for this is shown below:

2.2 Calculation of inputs and outputs using the VAT classification

Standard rate supplies:

The Cathy plans to start a profitable venture for training included of standard rated sales

for VAT, and for that Cathy will be needed to register for value added tax as she is making

taxable supplies. Standard rates are those which are prescribed under law which is 20%. Inputs

and Output VAT have been calculated below:

Output VAT:

80000*20% = GBP 16000

5

is paid in excess or less by the business to tax authorities.

2.1 Relevant data for a specific period from accounting system

The assumed example for this is shown below:

2.2 Calculation of inputs and outputs using the VAT classification

Standard rate supplies:

The Cathy plans to start a profitable venture for training included of standard rated sales

for VAT, and for that Cathy will be needed to register for value added tax as she is making

taxable supplies. Standard rates are those which are prescribed under law which is 20%. Inputs

and Output VAT have been calculated below:

Output VAT:

80000*20% = GBP 16000

5

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Input VAT = 15000*20% = GBP 3000

Zero rated supplies:

The zero rated supplies are those which comes under exemption and on that items there

will be nil percent rate of tax.

Output VAT will not be due in this case.

The amount of input VAT will be approx GBP 2500 per month and will be recoverable.

Exempt supplies:

Under this case Cathy will not be required or permitted to register for tax as she is not

doing any kind of taxable supplies.

No output will be due and no input will be recoverable.

Calculation of input and output VAT on export and import:

Rule:

When a VAT registered organisation imports goods to the UK from outside the European

Union than VAT has to be paid at time of importation. Therefore, it can be reclaimed as input

Vat on the VAT return for period during which goods were imported.

For example, if Chang ltd. Choose to purchase goods of worth amount of GBP 1000 from a

supplier, standard rate of 20% will be applicable. Apart from this if Chang ltd. Choose to buy the

goods from a supplier outside European Union, they can postpone payment of VAT on

importation by setting up an account with HMRC. There should be a bank guarantee also.

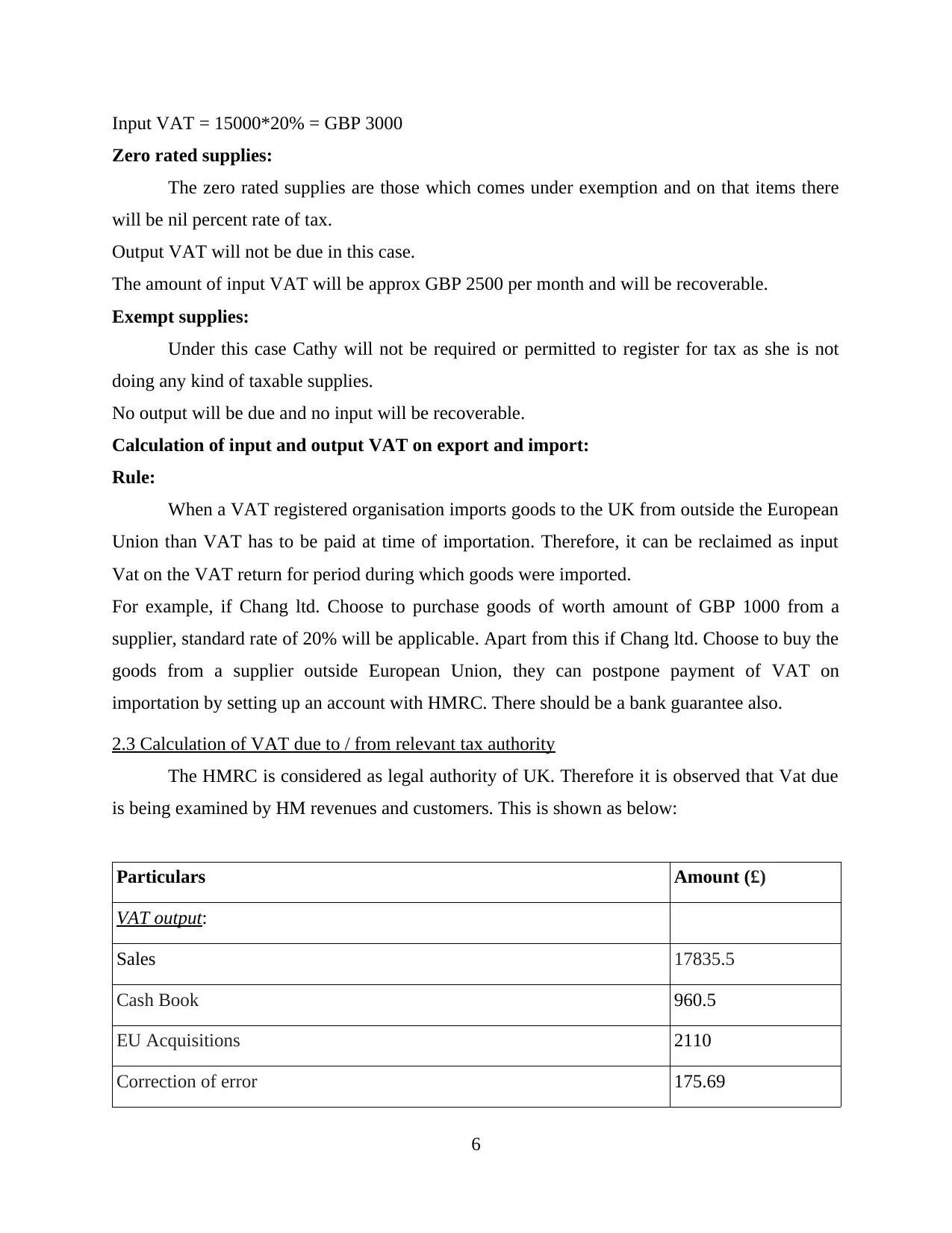

2.3 Calculation of VAT due to / from relevant tax authority

The HMRC is considered as legal authority of UK. Therefore it is observed that Vat due

is being examined by HM revenues and customers. This is shown as below:

Particulars Amount (£)

VAT output:

Sales 17835.5

Cash Book 960.5

EU Acquisitions 2110

Correction of error 175.69

6

Zero rated supplies:

The zero rated supplies are those which comes under exemption and on that items there

will be nil percent rate of tax.

Output VAT will not be due in this case.

The amount of input VAT will be approx GBP 2500 per month and will be recoverable.

Exempt supplies:

Under this case Cathy will not be required or permitted to register for tax as she is not

doing any kind of taxable supplies.

No output will be due and no input will be recoverable.

Calculation of input and output VAT on export and import:

Rule:

When a VAT registered organisation imports goods to the UK from outside the European

Union than VAT has to be paid at time of importation. Therefore, it can be reclaimed as input

Vat on the VAT return for period during which goods were imported.

For example, if Chang ltd. Choose to purchase goods of worth amount of GBP 1000 from a

supplier, standard rate of 20% will be applicable. Apart from this if Chang ltd. Choose to buy the

goods from a supplier outside European Union, they can postpone payment of VAT on

importation by setting up an account with HMRC. There should be a bank guarantee also.

2.3 Calculation of VAT due to / from relevant tax authority

The HMRC is considered as legal authority of UK. Therefore it is observed that Vat due

is being examined by HM revenues and customers. This is shown as below:

Particulars Amount (£)

VAT output:

Sales 17835.5

Cash Book 960.5

EU Acquisitions 2110

Correction of error 175.69

6

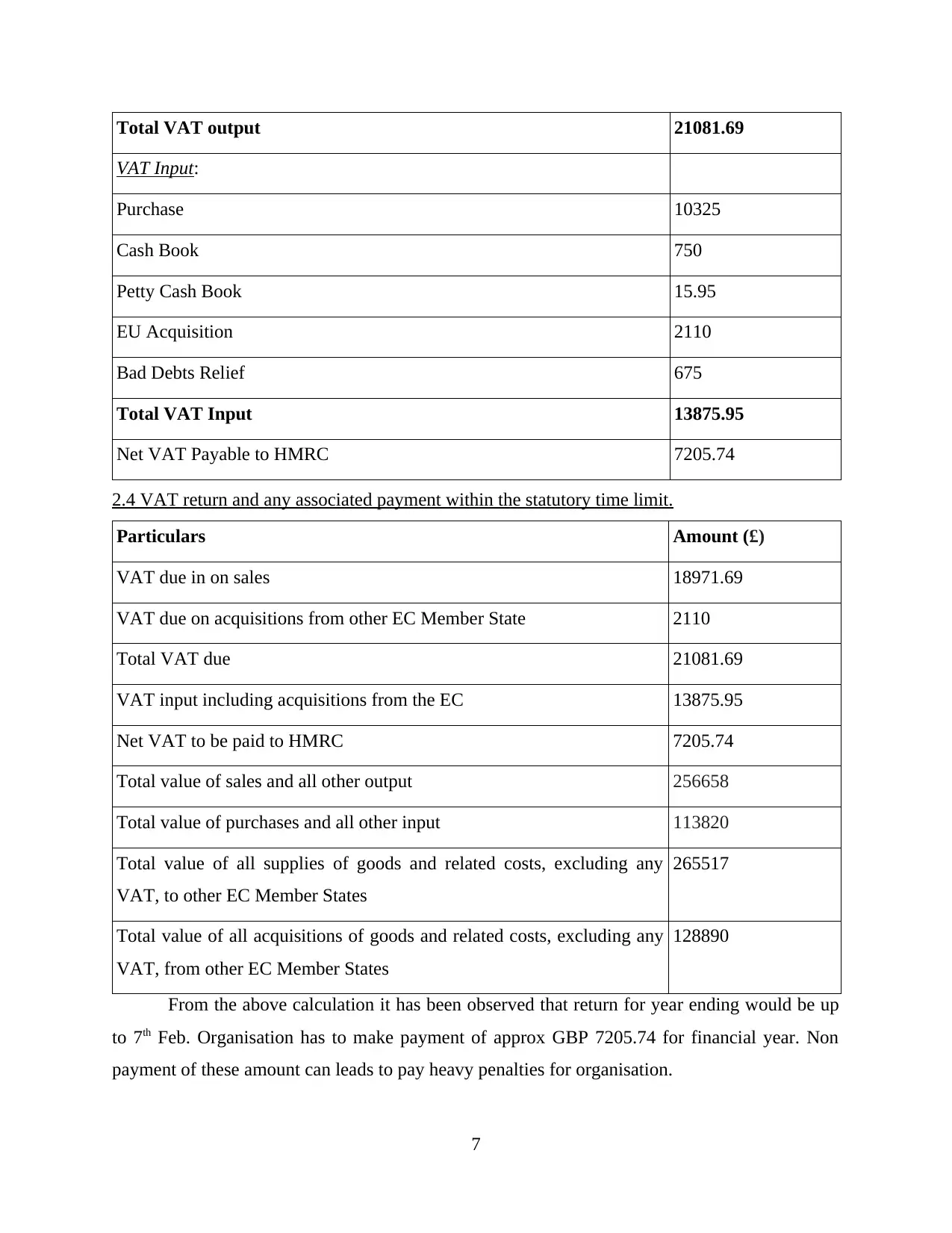

Total VAT output 21081.69

VAT Input:

Purchase 10325

Cash Book 750

Petty Cash Book 15.95

EU Acquisition 2110

Bad Debts Relief 675

Total VAT Input 13875.95

Net VAT Payable to HMRC 7205.74

2.4 VAT return and any associated payment within the statutory time limit.

Particulars Amount (£)

VAT due in on sales 18971.69

VAT due on acquisitions from other EC Member State 2110

Total VAT due 21081.69

VAT input including acquisitions from the EC 13875.95

Net VAT to be paid to HMRC 7205.74

Total value of sales and all other output 256658

Total value of purchases and all other input 113820

Total value of all supplies of goods and related costs, excluding any

VAT, to other EC Member States

265517

Total value of all acquisitions of goods and related costs, excluding any

VAT, from other EC Member States

128890

From the above calculation it has been observed that return for year ending would be up

to 7th Feb. Organisation has to make payment of approx GBP 7205.74 for financial year. Non

payment of these amount can leads to pay heavy penalties for organisation.

7

VAT Input:

Purchase 10325

Cash Book 750

Petty Cash Book 15.95

EU Acquisition 2110

Bad Debts Relief 675

Total VAT Input 13875.95

Net VAT Payable to HMRC 7205.74

2.4 VAT return and any associated payment within the statutory time limit.

Particulars Amount (£)

VAT due in on sales 18971.69

VAT due on acquisitions from other EC Member State 2110

Total VAT due 21081.69

VAT input including acquisitions from the EC 13875.95

Net VAT to be paid to HMRC 7205.74

Total value of sales and all other output 256658

Total value of purchases and all other input 113820

Total value of all supplies of goods and related costs, excluding any

VAT, to other EC Member States

265517

Total value of all acquisitions of goods and related costs, excluding any

VAT, from other EC Member States

128890

From the above calculation it has been observed that return for year ending would be up

to 7th Feb. Organisation has to make payment of approx GBP 7205.74 for financial year. Non

payment of these amount can leads to pay heavy penalties for organisation.

7

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

3.1 Implications and Penalties for an organisation resulting from failure to abide by VAT

Regulations

The Penalties for the non compliance of the laws related to the VAT are made by the

HMRC Department (Delgado, Lago‐Peñas and Mayor, 2015). All the penalties and implications

of possible crimes related to the non fulfilment of VAT Laws are different and are decided by

this department. The foremost is the misrepresentation of records of the payment of VAT Return

to HMRC Department. The Department charges penalty for the late payment interest and

repayment interest on VAT, for those who had applied for corporation tax. Also, it depends upon

the lateness of the payment made by the taxpayer company that how much interest is to be

charged from them. When VAT is paid late by 15 days by the companies, then they have to pay a

penalty of 2.5% to the amount. And in case when the payment is made late by 30 days then the

penalty charged will be 5%. The department has also revised its charge in case of late payments

of taxes by the taxpayer companies. Due to the revision of these charges, it had made companies

for their first mistake which is related to working according to the change made in the policies.

These charges also increases as the frequency of doing these mistakes are repeated again and

again by the company.

3.2 Making Declarations and Adjustments on the Previously Occurred Errors and Rectifying

them

HMRC Department also provides some relaxation to the companies so that they may

cover up their mistakes which they made unknowingly in their accounts. The companies which

declare their mistakes themselves at their own are not charged anything by the Department and

they can simply rectify their errors they had made. They have to submit the remaining amount of

the new calculation they had made and also they have to proof it that the new calculation id right.

Any amount which the companies have to pay or take back from the department will be settled

with the next year's payment of VAT. The Department provides the companies to make an

adjustment in their accounts if the amount of errors in their accounts are not more than £10,000

or less. In that case, companies can rectify their error by informing the department priorly. For

doing this also, the company has to make the calculation again about the actual amount of VAT

that it has to pay and after that any difference arises will be settled in full and final by the

department. In the accounts of company, it can make adjustments by keeping the details of

inaccuracy and the reason how it occurred. In case, the error was a deliberate error than penalty

8

Regulations

The Penalties for the non compliance of the laws related to the VAT are made by the

HMRC Department (Delgado, Lago‐Peñas and Mayor, 2015). All the penalties and implications

of possible crimes related to the non fulfilment of VAT Laws are different and are decided by

this department. The foremost is the misrepresentation of records of the payment of VAT Return

to HMRC Department. The Department charges penalty for the late payment interest and

repayment interest on VAT, for those who had applied for corporation tax. Also, it depends upon

the lateness of the payment made by the taxpayer company that how much interest is to be

charged from them. When VAT is paid late by 15 days by the companies, then they have to pay a

penalty of 2.5% to the amount. And in case when the payment is made late by 30 days then the

penalty charged will be 5%. The department has also revised its charge in case of late payments

of taxes by the taxpayer companies. Due to the revision of these charges, it had made companies

for their first mistake which is related to working according to the change made in the policies.

These charges also increases as the frequency of doing these mistakes are repeated again and

again by the company.

3.2 Making Declarations and Adjustments on the Previously Occurred Errors and Rectifying

them

HMRC Department also provides some relaxation to the companies so that they may

cover up their mistakes which they made unknowingly in their accounts. The companies which

declare their mistakes themselves at their own are not charged anything by the Department and

they can simply rectify their errors they had made. They have to submit the remaining amount of

the new calculation they had made and also they have to proof it that the new calculation id right.

Any amount which the companies have to pay or take back from the department will be settled

with the next year's payment of VAT. The Department provides the companies to make an

adjustment in their accounts if the amount of errors in their accounts are not more than £10,000

or less. In that case, companies can rectify their error by informing the department priorly. For

doing this also, the company has to make the calculation again about the actual amount of VAT

that it has to pay and after that any difference arises will be settled in full and final by the

department. In the accounts of company, it can make adjustments by keeping the details of

inaccuracy and the reason how it occurred. In case, the error was a deliberate error than penalty

8

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

will be charged by the department. The process of making the errors correct is also done by

following the guidelines and rules of the relevant EU member state. The companies must also

address the mistakes they had made in time of less than four years. It can be done by filing up the

form VAT652 and submitting it to the VAT Error Correction Team (Bahl, 2018).

4.1 Informing Managers about the Impact of Change in the VAT Laws on Organisation's Cash

Flows and Financial Forecasts

The changes in the VAT Laws affects the profitability of an organisation. It is because as

the dividend paid to the shareholders of a company are also paid after the prior calculation of

interest and tax upon them. The change in these tax rates will also make affect on the amount of

dividend to be distributed among the shareholders of a company. One major point of difference

is also that some companies also provide goods on credit to their customers so the time at they

give goods and invoices to their customers and receiving the payment for those goods both are

different so there may arise a change in the VAT Rates and the price of the goods may change.

The manager of a company must be aware about these changes and make policies according to

them so that they may make good the relationship between the customers and them. Also the

managers must adopt those policies which indicate that the both type of VAT such as the

treatment of capital goods and the inclusion and exclusion of exports have significant effects on

the revenue generated while making collection for the goods. However, in case of some goods

whose price changes very rapidly, in that case the companies are exempted a little bit but have to

select the same on going VAT Rate at the time of sale of goods or services (Albayrak, 2017).

4.2 Advise Relevant People of Changes in VAT Legislation which would have an Effect on an

Organisation’s Recording Systems

The changes in the record keeping has been made due to the amendments made by the

HMRC Department in their rules and policies related to the VAT Legislation. As one of them

explains about the way of record keeping. The HMRC Department has provided new ways of

record keeping which is the digital record keeping instead of manual record keeping. In Digital

Record Keeping, the company has to make and prepare their records in spreadsheets format and

also have to submit them to HMRC Department. These all proceedings are done with the help of

network system. The companies now have to use different software so as to make the records as

per the requirements of HMRC Department. The companies are directly connected with the

HMRC Department and they can transfer these data directly. It has improved the way of working

9

following the guidelines and rules of the relevant EU member state. The companies must also

address the mistakes they had made in time of less than four years. It can be done by filing up the

form VAT652 and submitting it to the VAT Error Correction Team (Bahl, 2018).

4.1 Informing Managers about the Impact of Change in the VAT Laws on Organisation's Cash

Flows and Financial Forecasts

The changes in the VAT Laws affects the profitability of an organisation. It is because as

the dividend paid to the shareholders of a company are also paid after the prior calculation of

interest and tax upon them. The change in these tax rates will also make affect on the amount of

dividend to be distributed among the shareholders of a company. One major point of difference

is also that some companies also provide goods on credit to their customers so the time at they

give goods and invoices to their customers and receiving the payment for those goods both are

different so there may arise a change in the VAT Rates and the price of the goods may change.

The manager of a company must be aware about these changes and make policies according to

them so that they may make good the relationship between the customers and them. Also the

managers must adopt those policies which indicate that the both type of VAT such as the

treatment of capital goods and the inclusion and exclusion of exports have significant effects on

the revenue generated while making collection for the goods. However, in case of some goods

whose price changes very rapidly, in that case the companies are exempted a little bit but have to

select the same on going VAT Rate at the time of sale of goods or services (Albayrak, 2017).

4.2 Advise Relevant People of Changes in VAT Legislation which would have an Effect on an

Organisation’s Recording Systems

The changes in the record keeping has been made due to the amendments made by the

HMRC Department in their rules and policies related to the VAT Legislation. As one of them

explains about the way of record keeping. The HMRC Department has provided new ways of

record keeping which is the digital record keeping instead of manual record keeping. In Digital

Record Keeping, the company has to make and prepare their records in spreadsheets format and

also have to submit them to HMRC Department. These all proceedings are done with the help of

network system. The companies now have to use different software so as to make the records as

per the requirements of HMRC Department. The companies are directly connected with the

HMRC Department and they can transfer these data directly. It has improved the way of working

9

of the companies and also provided them new ways of working. The companies are now able to

maintain their records in more amount and the office area can be used for other purposes. Also it

has reduced the keeping of manual records where there are chances of damaging and losing the

data. The new way has eliminated all these problems.

CONCLUSION

In the conclusion it can be said that tax is major source of revenue for organisation

whether it is direct or indirect. There are various VAT regulations which needs to be understand

and applied by organisations for smooth process of business operations. The companies are

required to fulfil their VAT returns in timely manner. The non payment or late payment of VAT

can impose heavy penalties on the organisations. The value added tax information should be

communicated within organisations.

10

maintain their records in more amount and the office area can be used for other purposes. Also it

has reduced the keeping of manual records where there are chances of damaging and losing the

data. The new way has eliminated all these problems.

CONCLUSION

In the conclusion it can be said that tax is major source of revenue for organisation

whether it is direct or indirect. There are various VAT regulations which needs to be understand

and applied by organisations for smooth process of business operations. The companies are

required to fulfil their VAT returns in timely manner. The non payment or late payment of VAT

can impose heavy penalties on the organisations. The value added tax information should be

communicated within organisations.

10

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 14

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.