Macquarie University ECON634: Econometrics and Statistics Take-home

VerifiedAdded on 2023/06/12

|15

|1572

|369

Homework Assignment

AI Summary

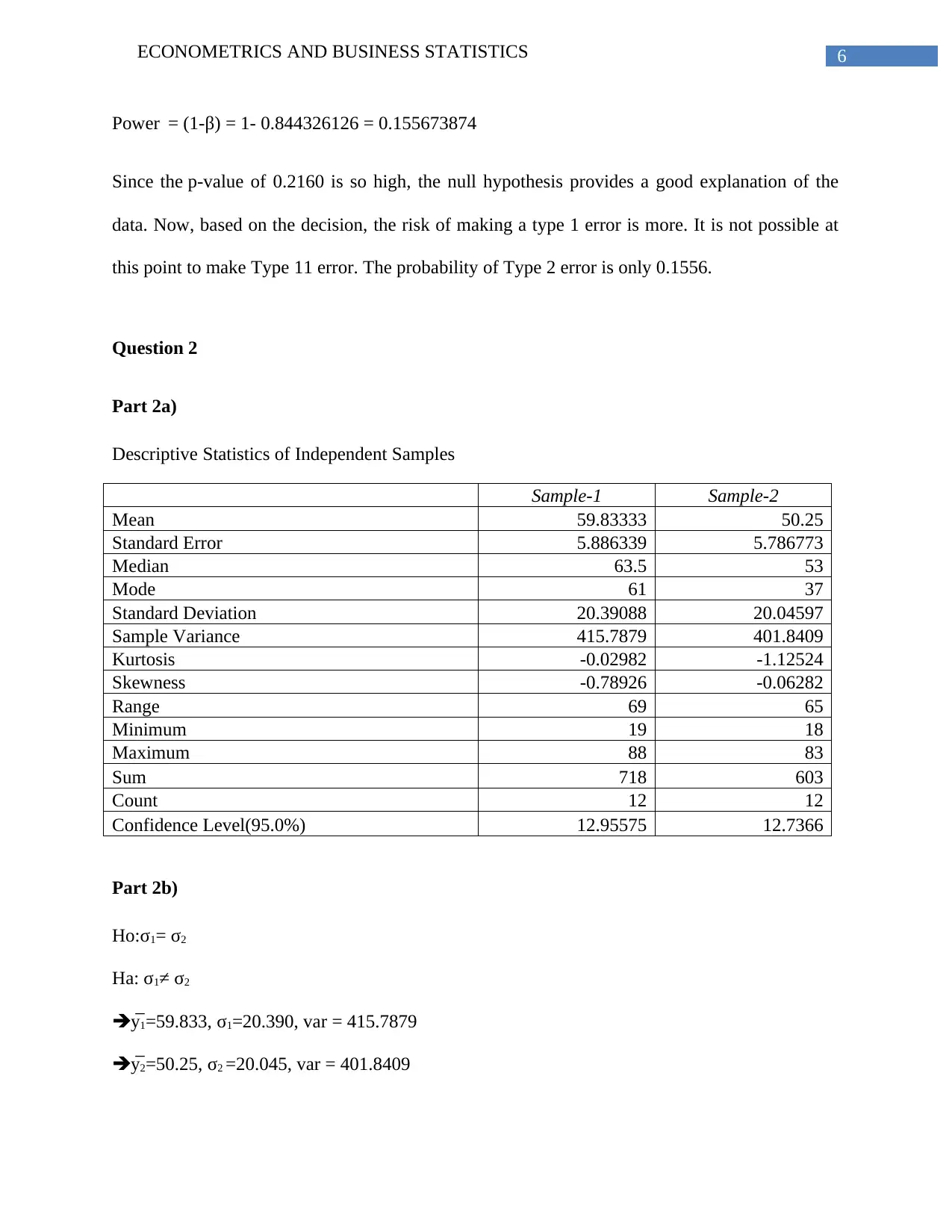

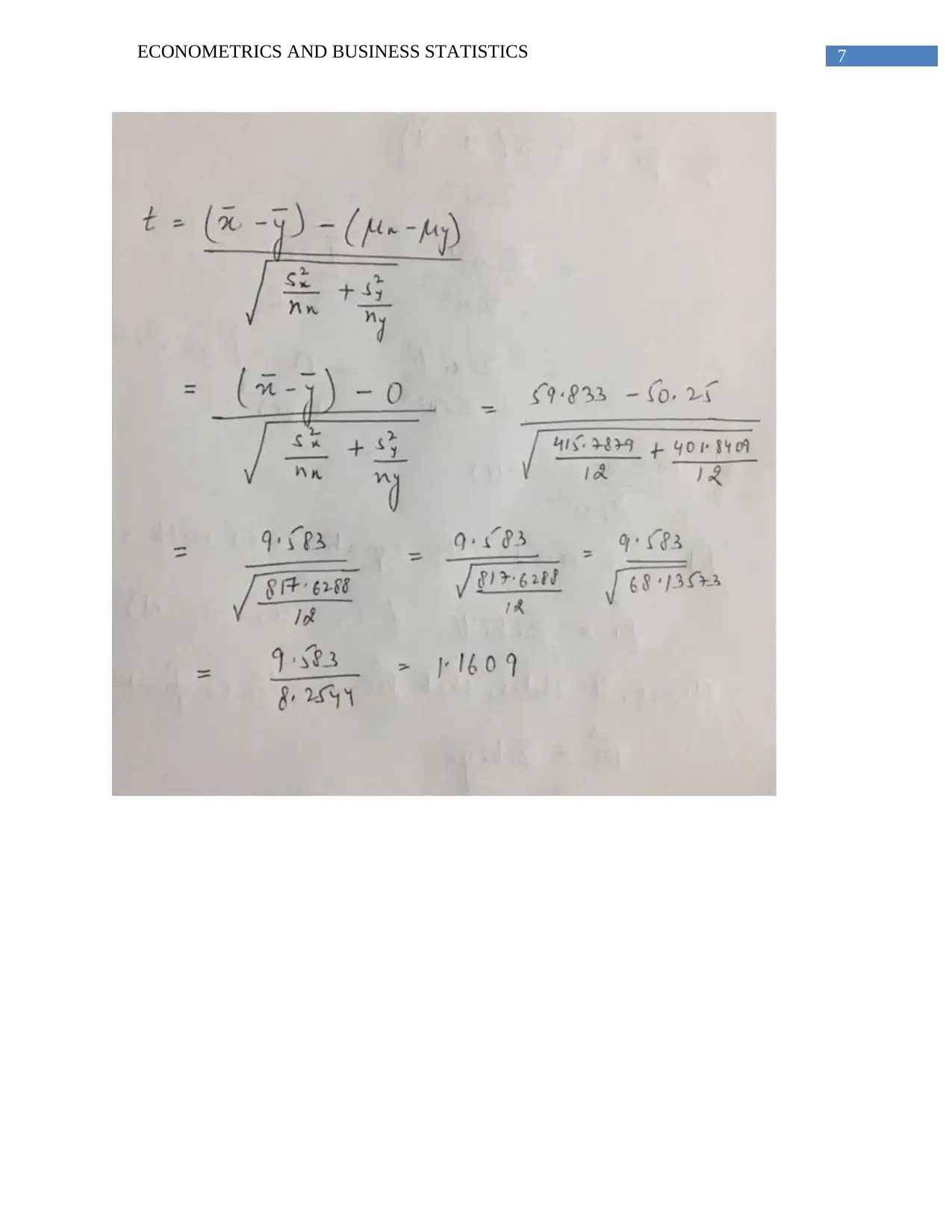

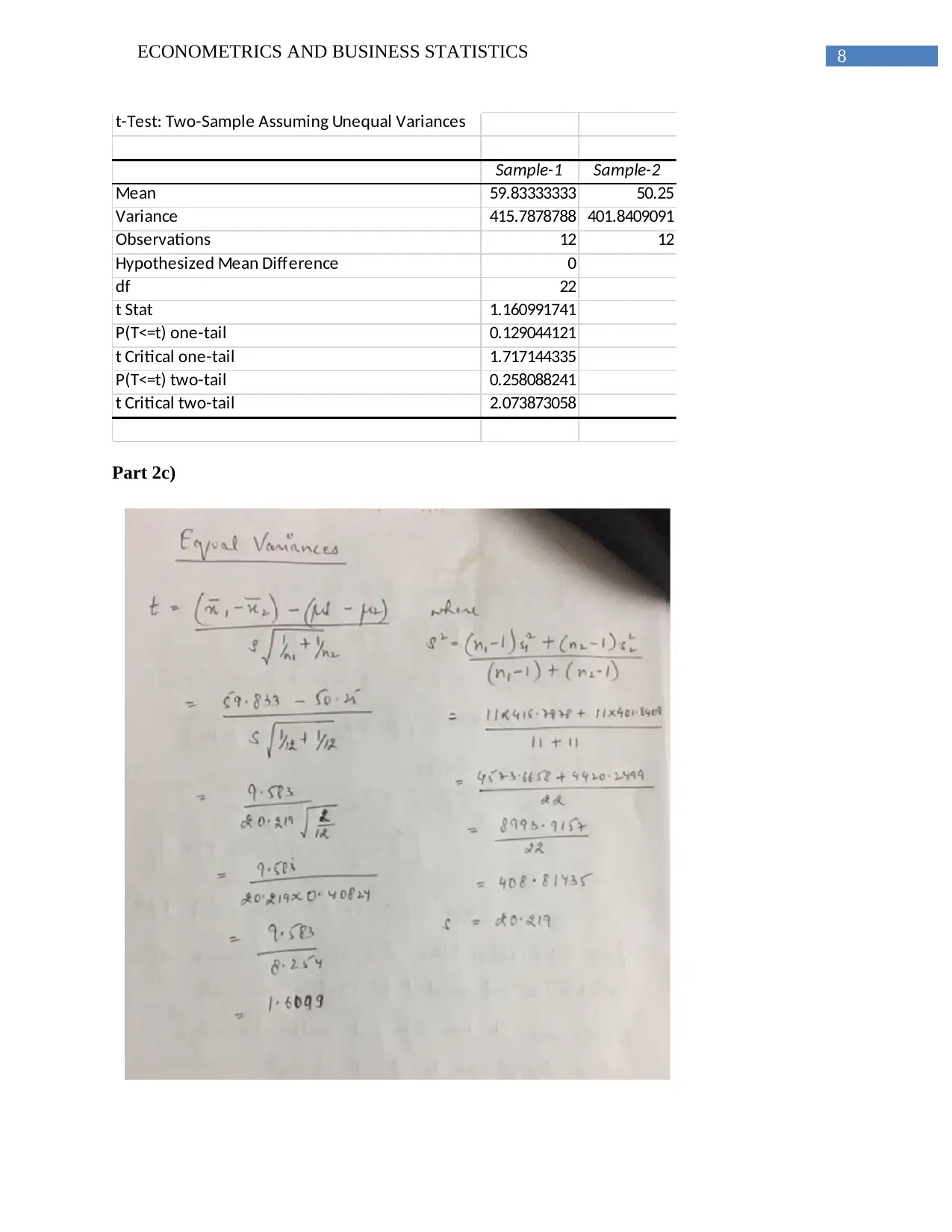

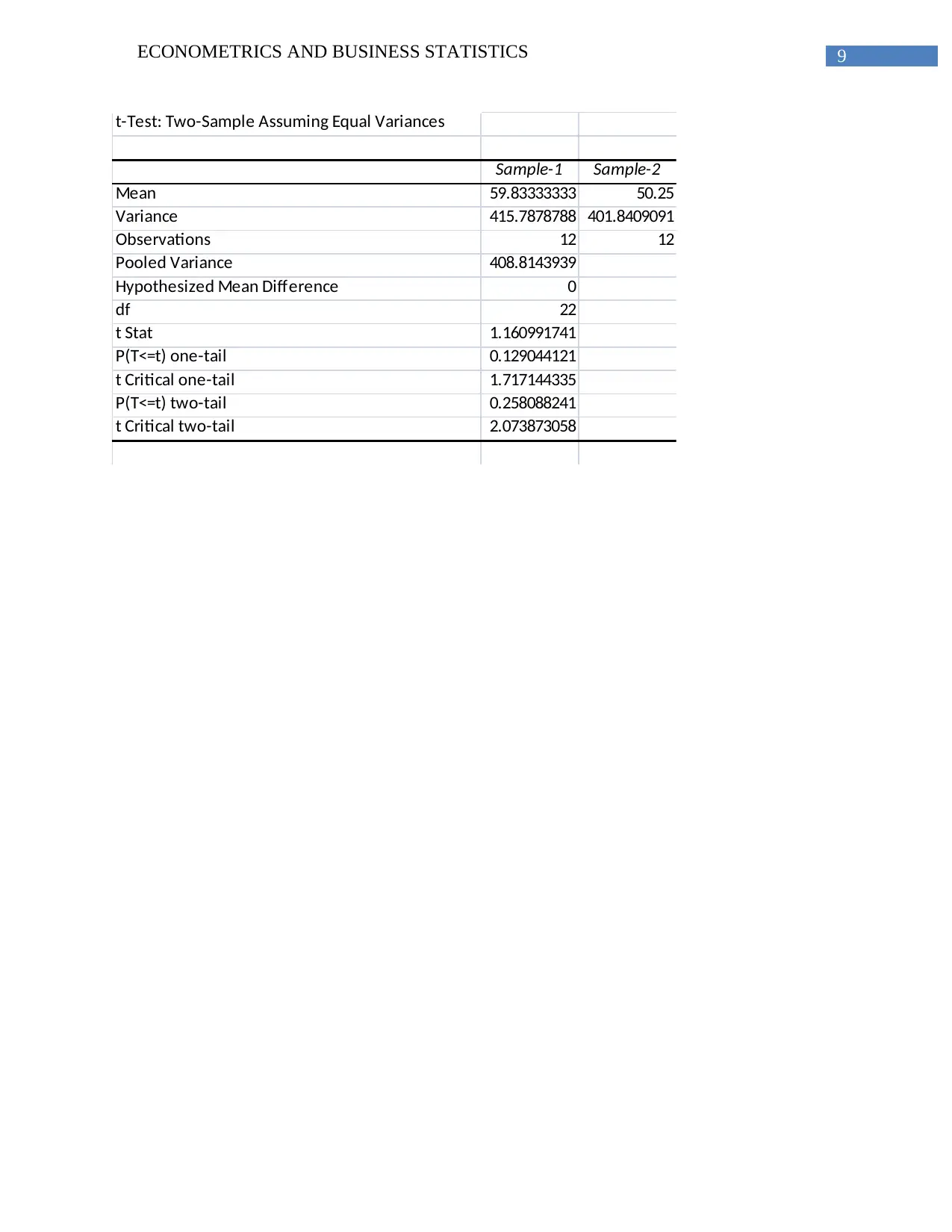

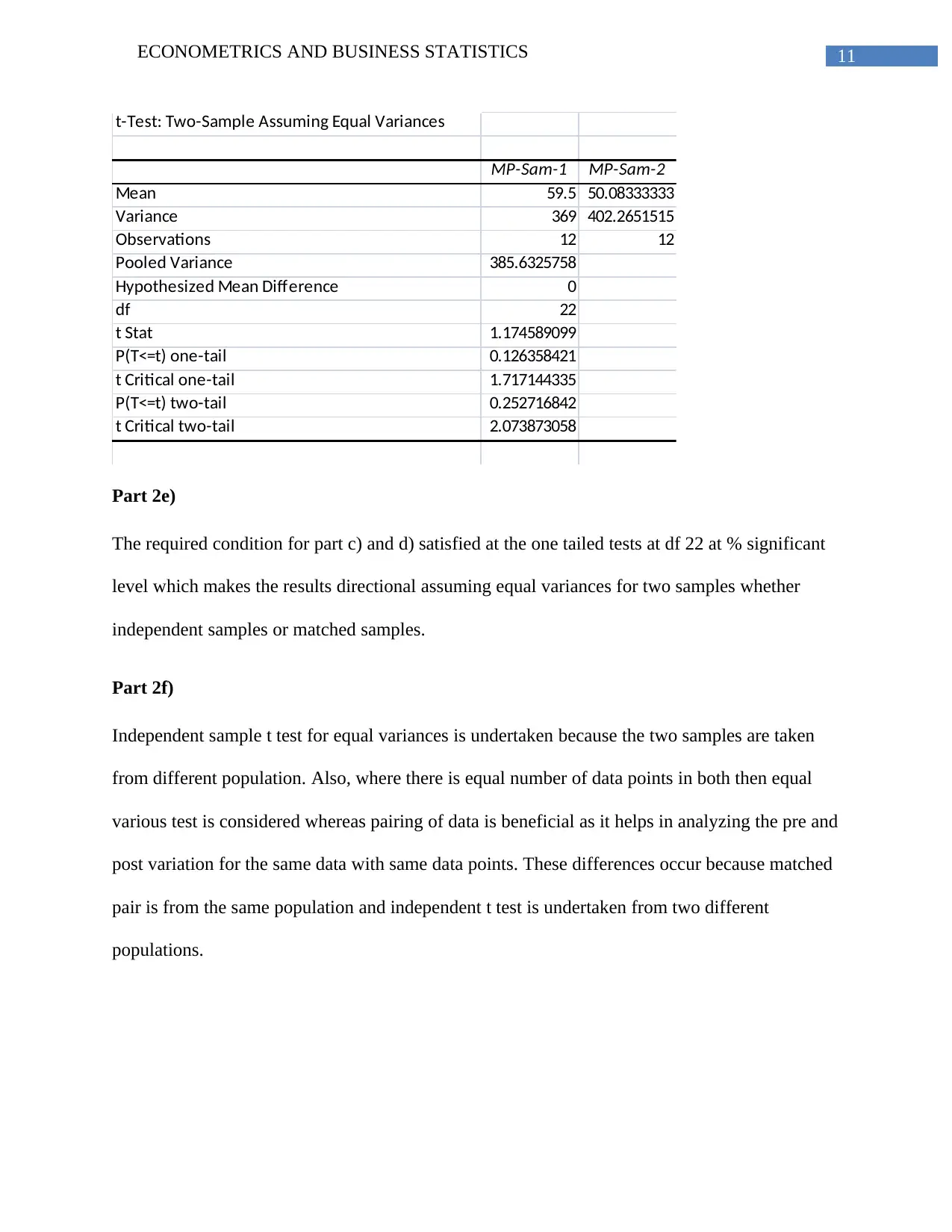

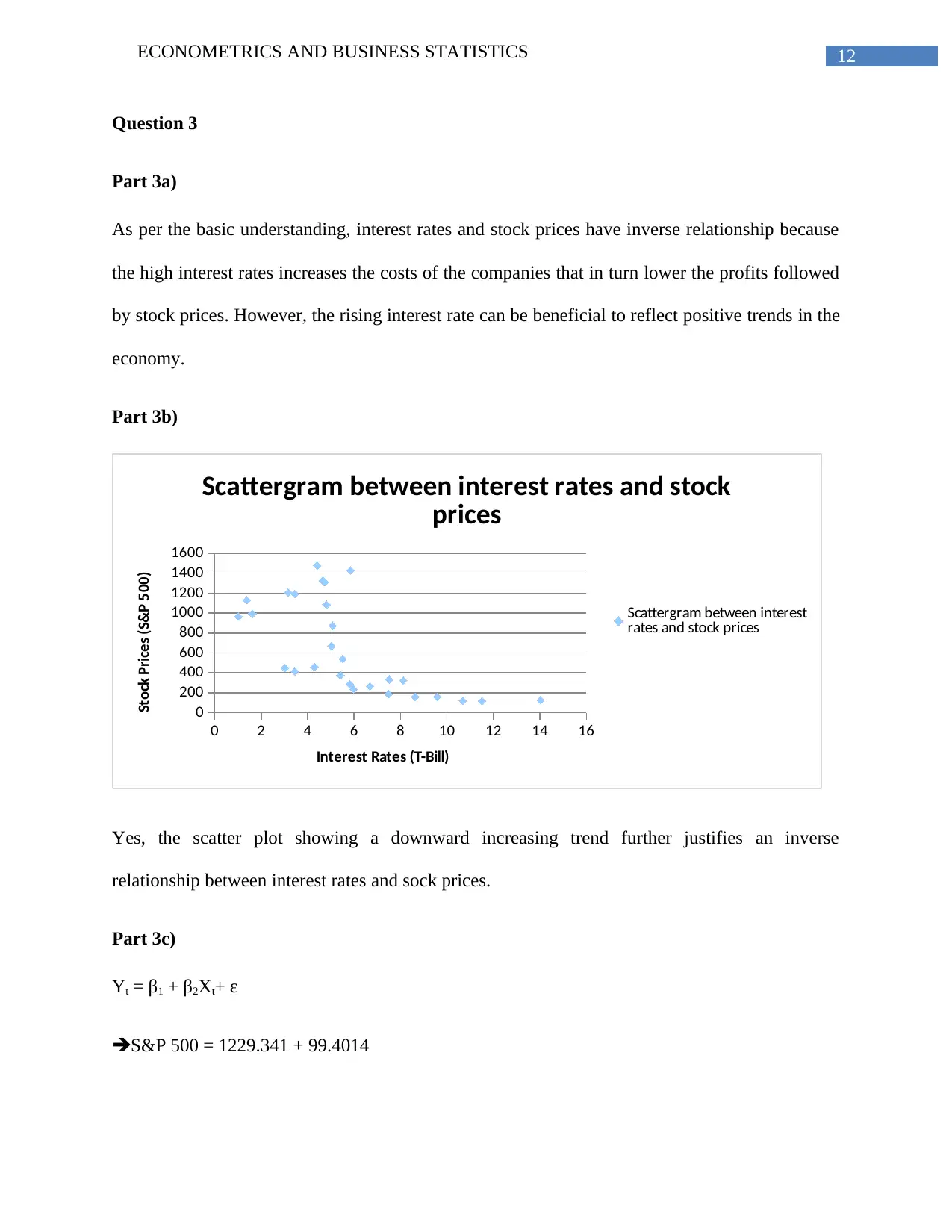

This document provides a detailed solution to a take-home test for the Econometrics and Business Statistics course (ECON634) at Macquarie University. The solution covers various topics, including confidence intervals, hypothesis testing (one-tailed and two-tailed tests), p-value calculations, and regression analysis. Specifically, it addresses questions related to weight loss data, comparing means and variances of independent samples, and analyzing the relationship between interest rates (T-Bill) and stock prices (S&P 500). The analysis includes descriptive statistics, t-tests (assuming equal and unequal variances), scatter plots, regression output interpretation (R-squared, t-statistics, p-values), and hypothesis testing for the significance of the relationship between interest rates and stock prices.

1 out of 15

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2025 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.