Detailed Financial Analysis of JB Hi-Fi: Performance and Ratios

VerifiedAdded on 2019/11/08

|11

|3051

|213

Report

AI Summary

This report presents a comprehensive financial analysis of JB Hi-Fi, a major Australian retailer, from 2013 to 2017. The analysis includes an overview of the company's industry situation, future plans, and key financial statements such as the statement of financial performance, statement of financial position, and statement of cash flows. The report also performs horizontal and vertical analyses to identify trends and significant accounting policies. Furthermore, the report delves into ratio analysis, covering liquidity, solvency, profitability, cash flow adequacy, and market strength ratios. The findings highlight the company's increasing gross profit, income from operation, and net income, while also pointing out potential inconsistencies in the financial statements. The report concludes with recommendations and a final decision based on the financial data and industry insights.

Running head: INTRODUCTION TO ACCOUNTING AND FINANCE

Introduction to accounting and finance

Name of the student

Name of the university

Author note

Introduction to accounting and finance

Name of the student

Name of the university

Author note

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

1INTRODUCTION TO ACCOUNTING AND FINANCE

Table of Contents

Part I – Introduction...................................................................................................................2

Part II – Industry situation and company plans..........................................................................2

Industry situation....................................................................................................................2

Future plans of the company..................................................................................................3

Part III – Financial statement analysis.......................................................................................3

Statement of financial performance.......................................................................................3

Statement of financial position...............................................................................................5

Statement of cash flows.........................................................................................................6

Part IV – Ratio analysis..............................................................................................................7

Part V – Conclusion...................................................................................................................8

Findings..................................................................................................................................8

Recommendation....................................................................................................................8

Decision and rational..............................................................................................................9

Reference..................................................................................................................................10

Table of Contents

Part I – Introduction...................................................................................................................2

Part II – Industry situation and company plans..........................................................................2

Industry situation....................................................................................................................2

Future plans of the company..................................................................................................3

Part III – Financial statement analysis.......................................................................................3

Statement of financial performance.......................................................................................3

Statement of financial position...............................................................................................5

Statement of cash flows.........................................................................................................6

Part IV – Ratio analysis..............................................................................................................7

Part V – Conclusion...................................................................................................................8

Findings..................................................................................................................................8

Recommendation....................................................................................................................8

Decision and rational..............................................................................................................9

Reference..................................................................................................................................10

2INTRODUCTION TO ACCOUNTING AND FINANCE

Part I – Introduction

JB Hi-Fi is the largest retailer for home entertainment that established in Australia.

They are the market leader due to the competitive price, big brands and wide range of

products like headphones, iPads, wireless speakers, home theatre, mobile phones, laptops and

televisions. The company identifies the significance of environmental, social and governance

related matters towards the shareholders, customers and suppliers. Other details related to the

company are as follows –

Name of the CEO – Mr Richard Murray since 1st July 2014

Home office – Chadstone, Australia

Closing date of the latest fiscal year – 30th June 2017

Primary service and products – the company is the speciality retailer for the products

related to home entertainment like headphones, iPads, wireless speakers, home

theatre, mobile phones, laptops and televisions.

Primary geographic area of activity – Australia and New Zealand

Name of independent auditor – Deloitte Touche Tohmatsu

Auditor’s opinion on financial statement – as per the opinion of the independent

auditor the financial report of the company is in compliance with Corporation act

2001 and includes –

The financial statement of the company presents the true and fair view of the financial

position of the company as on 30th June 2017 and the financial performance of the

company for the year ended on the mentioned date (JB Hi-Fi | JB Hi-Fi - Australia's

Largest Home Entertainment Retailer, 2017)

Complies with the AAS (Australian Accounting Standards) and Corporation

Regulation act 2001.

Most recent share price of the company - $ 23.37 as on 30th June 2017.

Dividend per share –

Final dividend as on 25th August 2017 – 46 cents

Interim dividend as on 24th February 2017 – 72 cents

Part I – Introduction

JB Hi-Fi is the largest retailer for home entertainment that established in Australia.

They are the market leader due to the competitive price, big brands and wide range of

products like headphones, iPads, wireless speakers, home theatre, mobile phones, laptops and

televisions. The company identifies the significance of environmental, social and governance

related matters towards the shareholders, customers and suppliers. Other details related to the

company are as follows –

Name of the CEO – Mr Richard Murray since 1st July 2014

Home office – Chadstone, Australia

Closing date of the latest fiscal year – 30th June 2017

Primary service and products – the company is the speciality retailer for the products

related to home entertainment like headphones, iPads, wireless speakers, home

theatre, mobile phones, laptops and televisions.

Primary geographic area of activity – Australia and New Zealand

Name of independent auditor – Deloitte Touche Tohmatsu

Auditor’s opinion on financial statement – as per the opinion of the independent

auditor the financial report of the company is in compliance with Corporation act

2001 and includes –

The financial statement of the company presents the true and fair view of the financial

position of the company as on 30th June 2017 and the financial performance of the

company for the year ended on the mentioned date (JB Hi-Fi | JB Hi-Fi - Australia's

Largest Home Entertainment Retailer, 2017)

Complies with the AAS (Australian Accounting Standards) and Corporation

Regulation act 2001.

Most recent share price of the company - $ 23.37 as on 30th June 2017.

Dividend per share –

Final dividend as on 25th August 2017 – 46 cents

Interim dividend as on 24th February 2017 – 72 cents

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

3INTRODUCTION TO ACCOUNTING AND FINANCE

Part II – Industry situation and company plans

Industry situation

JB Hi-Fi Limited belongs to the retail industry in Australia and though the retail

industry is becoming stronger as compared to the past years. Retailing sector in Australia

increased by 3% during 2016 with regard to the current value terms that is the growth line

recognized during the period. Though the growth is positive, it is slower as compared to the

year 2015 as the country became cautious regarding its discretionary spending owing to the

low growth in income (Post & Byron, 2015). Wesfarmers was the biggest retailer during

2016 along with it being the leader over all the multiple categories for retailing. Their value

growth was mainly driven by strong performance in home related products. Therefore, JB Hi-

Fi will continue to have a strong competition with Wesfarmers during the current year as well

as in the future years.

Further, retail industry in Australia is expected to grow at the value CAGR for 3% at

constant rate. This growth will mainly driven by the home entertainment, garden specialist

and internet retailing that are expected to grow owing to the increase in demand for new

home related products and new technologies adoption.

Future plans of the company

The solution from JB Hi-Fi is the key driver for their success. They will continue with

the plan of aggressive recruitment along with the expansion of the services and products they

offer. They are planning to set up the play in the integrating related products and the services

towards the education sector, government and business sectors through the JB Hi-Fi solutions

arm. Further, it is expected to provide $ 500 million per year with regard to sales through the

strategic acquisitions and organic growth (Hunjra & Bashir, 2014). Moreover, the company

has a plan to expand their store with regard to home branded to 75 from 43 outlets. Each new

outlet for JB Hi-Fi store contributes towards the growth of the customer awareness, supplier

support and market share. As per the CEO, Mr Murray, in association with the ongoing

investment towards the store wages, supply chain and staff training put the company in strong

position so that they can continue with the expansion.

Part II – Industry situation and company plans

Industry situation

JB Hi-Fi Limited belongs to the retail industry in Australia and though the retail

industry is becoming stronger as compared to the past years. Retailing sector in Australia

increased by 3% during 2016 with regard to the current value terms that is the growth line

recognized during the period. Though the growth is positive, it is slower as compared to the

year 2015 as the country became cautious regarding its discretionary spending owing to the

low growth in income (Post & Byron, 2015). Wesfarmers was the biggest retailer during

2016 along with it being the leader over all the multiple categories for retailing. Their value

growth was mainly driven by strong performance in home related products. Therefore, JB Hi-

Fi will continue to have a strong competition with Wesfarmers during the current year as well

as in the future years.

Further, retail industry in Australia is expected to grow at the value CAGR for 3% at

constant rate. This growth will mainly driven by the home entertainment, garden specialist

and internet retailing that are expected to grow owing to the increase in demand for new

home related products and new technologies adoption.

Future plans of the company

The solution from JB Hi-Fi is the key driver for their success. They will continue with

the plan of aggressive recruitment along with the expansion of the services and products they

offer. They are planning to set up the play in the integrating related products and the services

towards the education sector, government and business sectors through the JB Hi-Fi solutions

arm. Further, it is expected to provide $ 500 million per year with regard to sales through the

strategic acquisitions and organic growth (Hunjra & Bashir, 2014). Moreover, the company

has a plan to expand their store with regard to home branded to 75 from 43 outlets. Each new

outlet for JB Hi-Fi store contributes towards the growth of the customer awareness, supplier

support and market share. As per the CEO, Mr Murray, in association with the ongoing

investment towards the store wages, supply chain and staff training put the company in strong

position so that they can continue with the expansion.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

4INTRODUCTION TO ACCOUNTING AND FINANCE

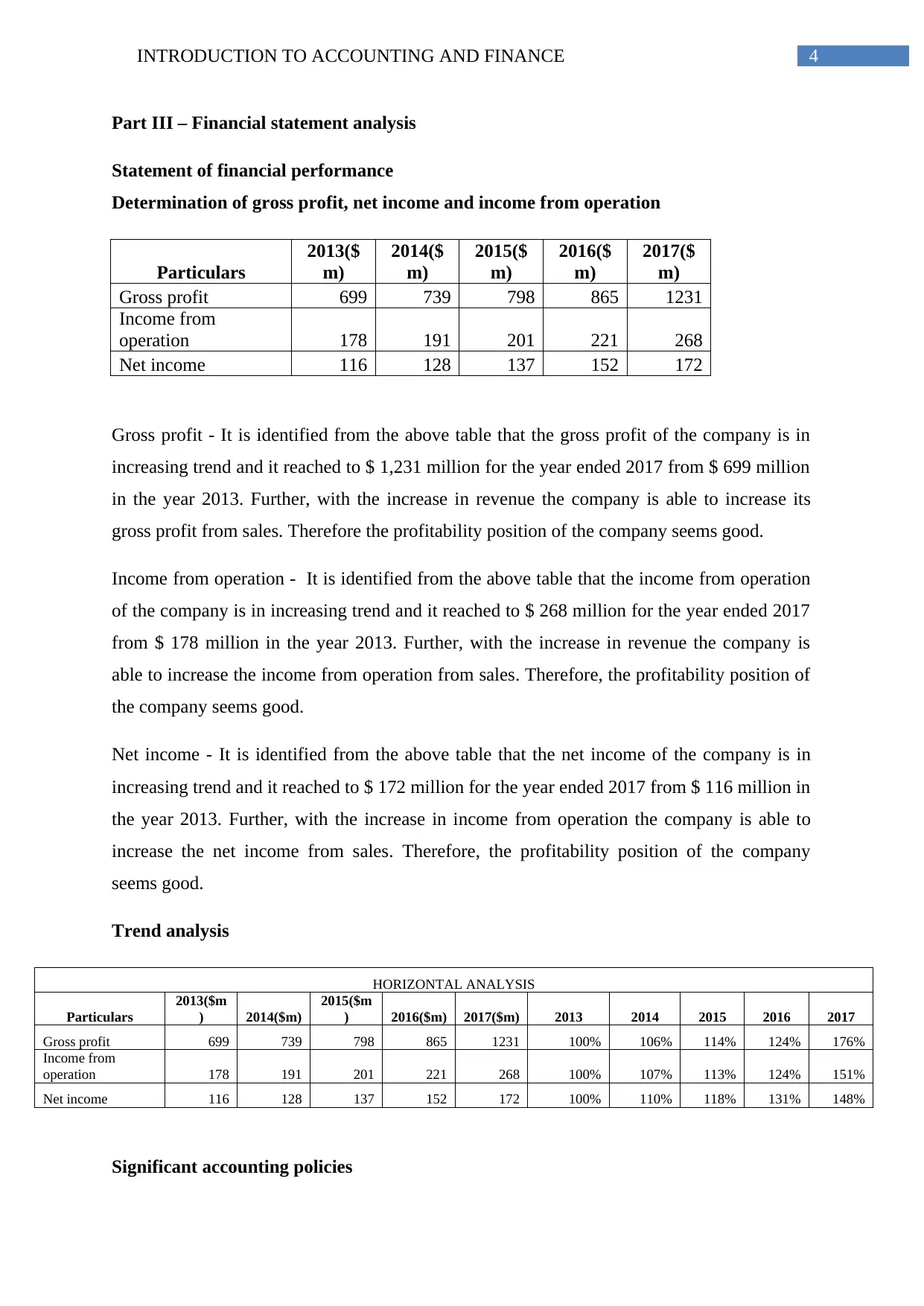

Part III – Financial statement analysis

Statement of financial performance

Determination of gross profit, net income and income from operation

Particulars

2013($

m)

2014($

m)

2015($

m)

2016($

m)

2017($

m)

Gross profit 699 739 798 865 1231

Income from

operation 178 191 201 221 268

Net income 116 128 137 152 172

Gross profit - It is identified from the above table that the gross profit of the company is in

increasing trend and it reached to $ 1,231 million for the year ended 2017 from $ 699 million

in the year 2013. Further, with the increase in revenue the company is able to increase its

gross profit from sales. Therefore the profitability position of the company seems good.

Income from operation - It is identified from the above table that the income from operation

of the company is in increasing trend and it reached to $ 268 million for the year ended 2017

from $ 178 million in the year 2013. Further, with the increase in revenue the company is

able to increase the income from operation from sales. Therefore, the profitability position of

the company seems good.

Net income - It is identified from the above table that the net income of the company is in

increasing trend and it reached to $ 172 million for the year ended 2017 from $ 116 million in

the year 2013. Further, with the increase in income from operation the company is able to

increase the net income from sales. Therefore, the profitability position of the company

seems good.

Trend analysis

HORIZONTAL ANALYSIS

Particulars

2013($m

) 2014($m)

2015($m

) 2016($m) 2017($m) 2013 2014 2015 2016 2017

Gross profit 699 739 798 865 1231 100% 106% 114% 124% 176%

Income from

operation 178 191 201 221 268 100% 107% 113% 124% 151%

Net income 116 128 137 152 172 100% 110% 118% 131% 148%

Significant accounting policies

Part III – Financial statement analysis

Statement of financial performance

Determination of gross profit, net income and income from operation

Particulars

2013($

m)

2014($

m)

2015($

m)

2016($

m)

2017($

m)

Gross profit 699 739 798 865 1231

Income from

operation 178 191 201 221 268

Net income 116 128 137 152 172

Gross profit - It is identified from the above table that the gross profit of the company is in

increasing trend and it reached to $ 1,231 million for the year ended 2017 from $ 699 million

in the year 2013. Further, with the increase in revenue the company is able to increase its

gross profit from sales. Therefore the profitability position of the company seems good.

Income from operation - It is identified from the above table that the income from operation

of the company is in increasing trend and it reached to $ 268 million for the year ended 2017

from $ 178 million in the year 2013. Further, with the increase in revenue the company is

able to increase the income from operation from sales. Therefore, the profitability position of

the company seems good.

Net income - It is identified from the above table that the net income of the company is in

increasing trend and it reached to $ 172 million for the year ended 2017 from $ 116 million in

the year 2013. Further, with the increase in income from operation the company is able to

increase the net income from sales. Therefore, the profitability position of the company

seems good.

Trend analysis

HORIZONTAL ANALYSIS

Particulars

2013($m

) 2014($m)

2015($m

) 2016($m) 2017($m) 2013 2014 2015 2016 2017

Gross profit 699 739 798 865 1231 100% 106% 114% 124% 176%

Income from

operation 178 191 201 221 268 100% 107% 113% 124% 151%

Net income 116 128 137 152 172 100% 110% 118% 131% 148%

Significant accounting policies

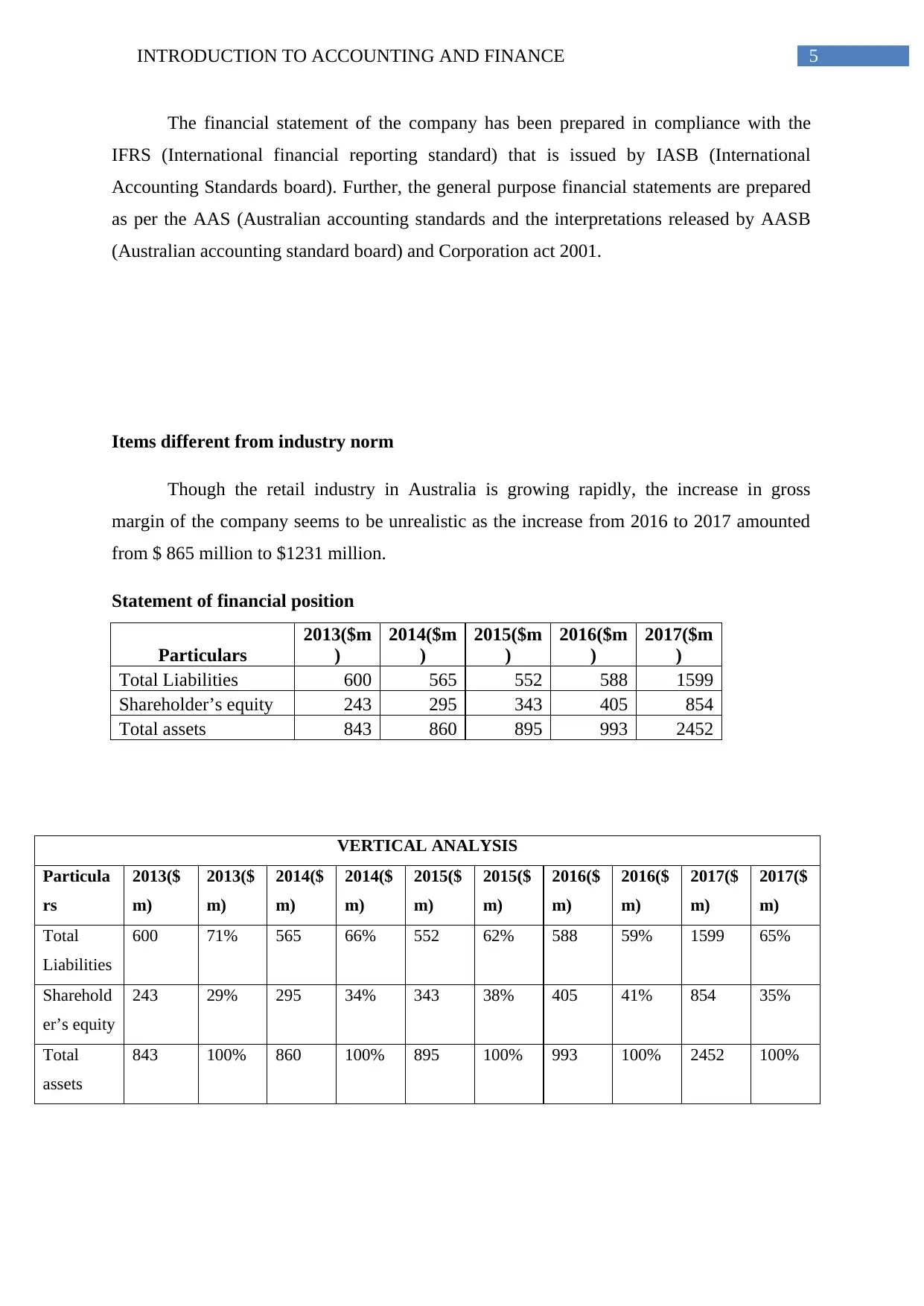

5INTRODUCTION TO ACCOUNTING AND FINANCE

The financial statement of the company has been prepared in compliance with the

IFRS (International financial reporting standard) that is issued by IASB (International

Accounting Standards board). Further, the general purpose financial statements are prepared

as per the AAS (Australian accounting standards and the interpretations released by AASB

(Australian accounting standard board) and Corporation act 2001.

Items different from industry norm

Though the retail industry in Australia is growing rapidly, the increase in gross

margin of the company seems to be unrealistic as the increase from 2016 to 2017 amounted

from $ 865 million to $1231 million.

Statement of financial position

Particulars

2013($m

)

2014($m

)

2015($m

)

2016($m

)

2017($m

)

Total Liabilities 600 565 552 588 1599

Shareholder’s equity 243 295 343 405 854

Total assets 843 860 895 993 2452

VERTICAL ANALYSIS

Particula

rs

2013($

m)

2013($

m)

2014($

m)

2014($

m)

2015($

m)

2015($

m)

2016($

m)

2016($

m)

2017($

m)

2017($

m)

Total

Liabilities

600 71% 565 66% 552 62% 588 59% 1599 65%

Sharehold

er’s equity

243 29% 295 34% 343 38% 405 41% 854 35%

Total

assets

843 100% 860 100% 895 100% 993 100% 2452 100%

The financial statement of the company has been prepared in compliance with the

IFRS (International financial reporting standard) that is issued by IASB (International

Accounting Standards board). Further, the general purpose financial statements are prepared

as per the AAS (Australian accounting standards and the interpretations released by AASB

(Australian accounting standard board) and Corporation act 2001.

Items different from industry norm

Though the retail industry in Australia is growing rapidly, the increase in gross

margin of the company seems to be unrealistic as the increase from 2016 to 2017 amounted

from $ 865 million to $1231 million.

Statement of financial position

Particulars

2013($m

)

2014($m

)

2015($m

)

2016($m

)

2017($m

)

Total Liabilities 600 565 552 588 1599

Shareholder’s equity 243 295 343 405 854

Total assets 843 860 895 993 2452

VERTICAL ANALYSIS

Particula

rs

2013($

m)

2013($

m)

2014($

m)

2014($

m)

2015($

m)

2015($

m)

2016($

m)

2016($

m)

2017($

m)

2017($

m)

Total

Liabilities

600 71% 565 66% 552 62% 588 59% 1599 65%

Sharehold

er’s equity

243 29% 295 34% 343 38% 405 41% 854 35%

Total

assets

843 100% 860 100% 895 100% 993 100% 2452 100%

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

6INTRODUCTION TO ACCOUNTING AND FINANCE

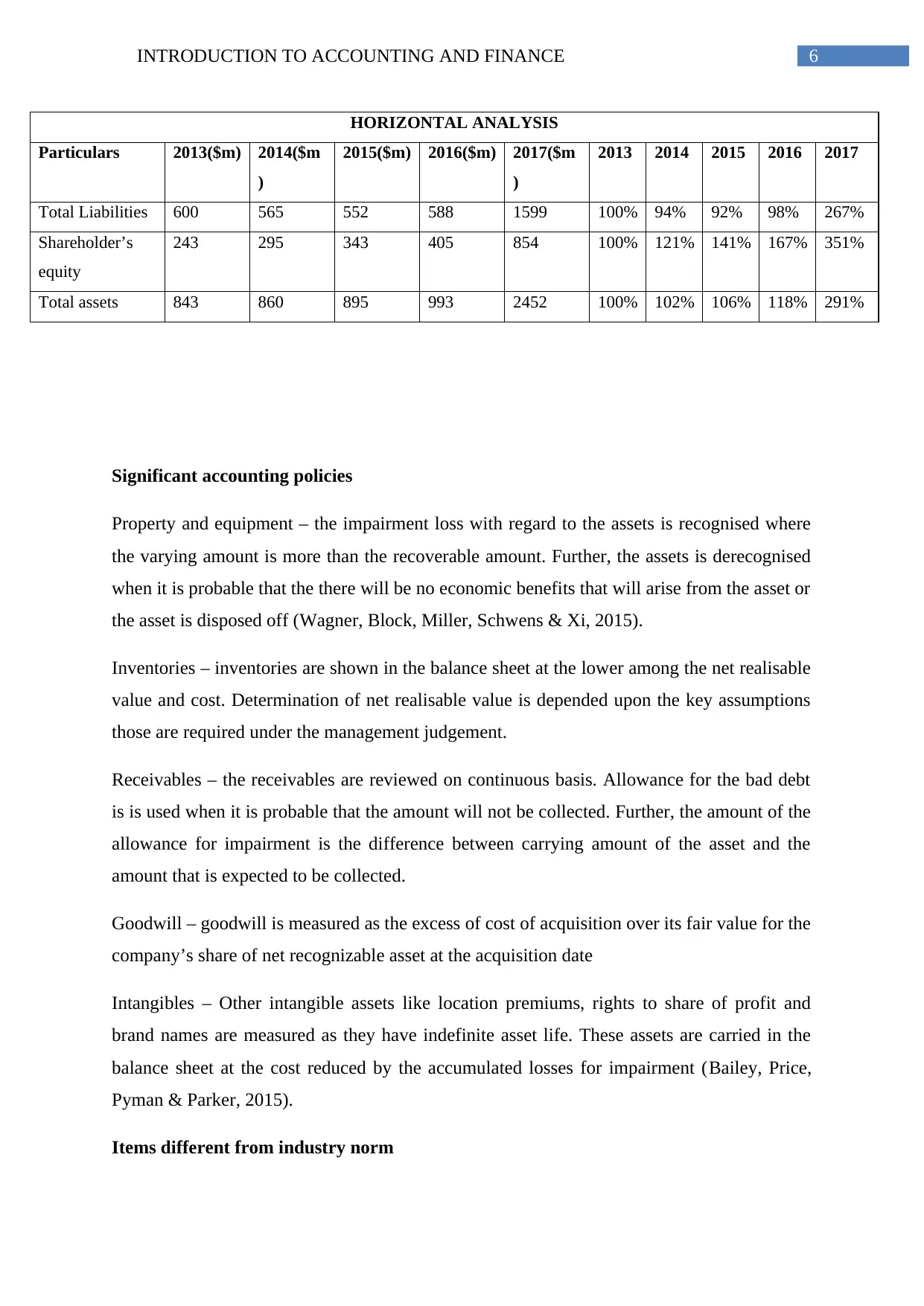

HORIZONTAL ANALYSIS

Particulars 2013($m) 2014($m

)

2015($m) 2016($m) 2017($m

)

2013 2014 2015 2016 2017

Total Liabilities 600 565 552 588 1599 100% 94% 92% 98% 267%

Shareholder’s

equity

243 295 343 405 854 100% 121% 141% 167% 351%

Total assets 843 860 895 993 2452 100% 102% 106% 118% 291%

Significant accounting policies

Property and equipment – the impairment loss with regard to the assets is recognised where

the varying amount is more than the recoverable amount. Further, the assets is derecognised

when it is probable that the there will be no economic benefits that will arise from the asset or

the asset is disposed off (Wagner, Block, Miller, Schwens & Xi, 2015).

Inventories – inventories are shown in the balance sheet at the lower among the net realisable

value and cost. Determination of net realisable value is depended upon the key assumptions

those are required under the management judgement.

Receivables – the receivables are reviewed on continuous basis. Allowance for the bad debt

is is used when it is probable that the amount will not be collected. Further, the amount of the

allowance for impairment is the difference between carrying amount of the asset and the

amount that is expected to be collected.

Goodwill – goodwill is measured as the excess of cost of acquisition over its fair value for the

company’s share of net recognizable asset at the acquisition date

Intangibles – Other intangible assets like location premiums, rights to share of profit and

brand names are measured as they have indefinite asset life. These assets are carried in the

balance sheet at the cost reduced by the accumulated losses for impairment (Bailey, Price,

Pyman & Parker, 2015).

Items different from industry norm

HORIZONTAL ANALYSIS

Particulars 2013($m) 2014($m

)

2015($m) 2016($m) 2017($m

)

2013 2014 2015 2016 2017

Total Liabilities 600 565 552 588 1599 100% 94% 92% 98% 267%

Shareholder’s

equity

243 295 343 405 854 100% 121% 141% 167% 351%

Total assets 843 860 895 993 2452 100% 102% 106% 118% 291%

Significant accounting policies

Property and equipment – the impairment loss with regard to the assets is recognised where

the varying amount is more than the recoverable amount. Further, the assets is derecognised

when it is probable that the there will be no economic benefits that will arise from the asset or

the asset is disposed off (Wagner, Block, Miller, Schwens & Xi, 2015).

Inventories – inventories are shown in the balance sheet at the lower among the net realisable

value and cost. Determination of net realisable value is depended upon the key assumptions

those are required under the management judgement.

Receivables – the receivables are reviewed on continuous basis. Allowance for the bad debt

is is used when it is probable that the amount will not be collected. Further, the amount of the

allowance for impairment is the difference between carrying amount of the asset and the

amount that is expected to be collected.

Goodwill – goodwill is measured as the excess of cost of acquisition over its fair value for the

company’s share of net recognizable asset at the acquisition date

Intangibles – Other intangible assets like location premiums, rights to share of profit and

brand names are measured as they have indefinite asset life. These assets are carried in the

balance sheet at the cost reduced by the accumulated losses for impairment (Bailey, Price,

Pyman & Parker, 2015).

Items different from industry norm

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

7INTRODUCTION TO ACCOUNTING AND FINANCE

Though the retail industry in Australia is growing rapidly, the increase in total assets

of the company seems to be unrealistic as the increase from 2016 to 2017 amounted from $

993 million to $2452 million.

Statement of cash flows

Particulars

2013($m

)

2014($m

)

2015($m

)

2016($m

)

2017($m

)

Operating cash flow 178 191 201 221 268

Net income 116 128 137 152 172

Net income % 65% 67% 68% 69% 64%

It can be identified that the net income percentage after deducting the expenses from

operating cash flows are in increasing trend. Therefore, it can be said that the profitability

position of the company is improving along with the increase in operating cash flow of the

company (Graves & Shan, 2014).

It is recognized that the company is sufficiently expanding though the investing

activities and it increased from $38 million in 2013 to $ 886 million in 2017. However, the

increase from the year 2016 to 2017 was significant as the increase was from $ 52 million to

$ 886 million seems unrealistic.

The most important source of financing for the company is through equity as more

percentage of finance is raised through equity as compared to raising through debt. During

the year ended 30th June 2016, shareholder’s equity represents the amount of $854 million

whereas, the amount of debt amounted to $ 559 million.

Item 2013($m) 2014($m) 2015($m) 2016($m) 2017 ($m)

Cash 67 43 49 52 73

It can be identified from the above table that there is no specific trend for the cash of

the company over the past five years. During 2013, the amount of cash under balance sheet

was amounted to $ 67 million and started decreasing and reached to $ 52 million in 2016.

However, during 2017 it again increased and reached to $ 73 million.

The major points of interest regarding the above findings concerning the cash flow

statement is that with regard to investing activities, the increase from the year 2016 to 2017

was significant as the increase was from $ 52 million to $ 886 million seems unrealistic.

Though the retail industry in Australia is growing rapidly, the increase in total assets

of the company seems to be unrealistic as the increase from 2016 to 2017 amounted from $

993 million to $2452 million.

Statement of cash flows

Particulars

2013($m

)

2014($m

)

2015($m

)

2016($m

)

2017($m

)

Operating cash flow 178 191 201 221 268

Net income 116 128 137 152 172

Net income % 65% 67% 68% 69% 64%

It can be identified that the net income percentage after deducting the expenses from

operating cash flows are in increasing trend. Therefore, it can be said that the profitability

position of the company is improving along with the increase in operating cash flow of the

company (Graves & Shan, 2014).

It is recognized that the company is sufficiently expanding though the investing

activities and it increased from $38 million in 2013 to $ 886 million in 2017. However, the

increase from the year 2016 to 2017 was significant as the increase was from $ 52 million to

$ 886 million seems unrealistic.

The most important source of financing for the company is through equity as more

percentage of finance is raised through equity as compared to raising through debt. During

the year ended 30th June 2016, shareholder’s equity represents the amount of $854 million

whereas, the amount of debt amounted to $ 559 million.

Item 2013($m) 2014($m) 2015($m) 2016($m) 2017 ($m)

Cash 67 43 49 52 73

It can be identified from the above table that there is no specific trend for the cash of

the company over the past five years. During 2013, the amount of cash under balance sheet

was amounted to $ 67 million and started decreasing and reached to $ 52 million in 2016.

However, during 2017 it again increased and reached to $ 73 million.

The major points of interest regarding the above findings concerning the cash flow

statement is that with regard to investing activities, the increase from the year 2016 to 2017

was significant as the increase was from $ 52 million to $ 886 million seems unrealistic.

8INTRODUCTION TO ACCOUNTING AND FINANCE

Further, the net cash provided from financing activities were in negative till the year 2015.

However, it went up to $716 million at the closing of the period 30th June 2017. The reason

behind this must be found out.

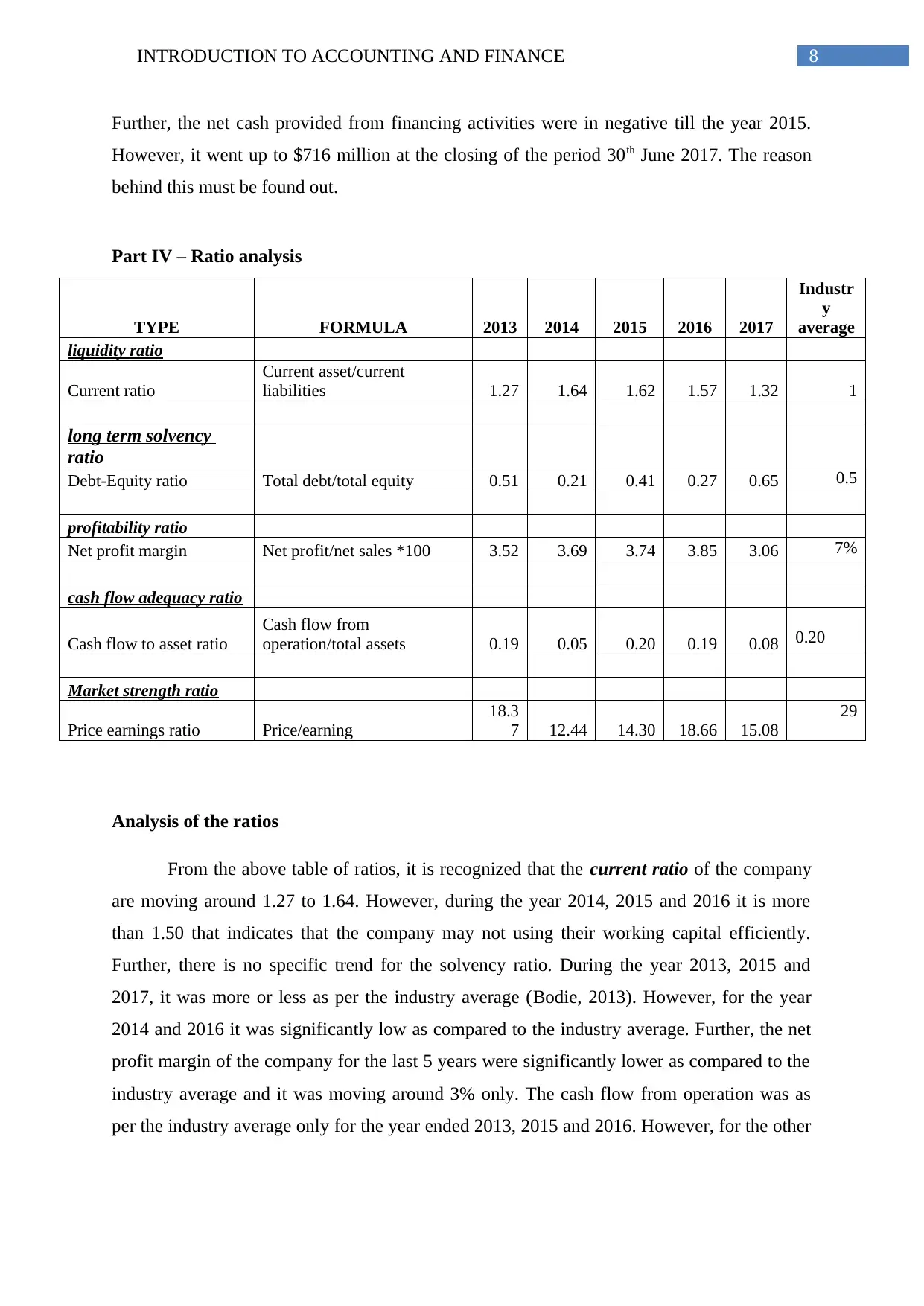

Part IV – Ratio analysis

TYPE FORMULA 2013 2014 2015 2016 2017

Industr

y

average

liquidity ratio

Current ratio

Current asset/current

liabilities 1.27 1.64 1.62 1.57 1.32 1

long term solvency

ratio

Debt-Equity ratio Total debt/total equity 0.51 0.21 0.41 0.27 0.65 0.5

profitability ratio

Net profit margin Net profit/net sales *100 3.52 3.69 3.74 3.85 3.06 7%

cash flow adequacy ratio

Cash flow to asset ratio

Cash flow from

operation/total assets 0.19 0.05 0.20 0.19 0.08 0.20

Market strength ratio

Price earnings ratio Price/earning

18.3

7 12.44 14.30 18.66 15.08

29

Analysis of the ratios

From the above table of ratios, it is recognized that the current ratio of the company

are moving around 1.27 to 1.64. However, during the year 2014, 2015 and 2016 it is more

than 1.50 that indicates that the company may not using their working capital efficiently.

Further, there is no specific trend for the solvency ratio. During the year 2013, 2015 and

2017, it was more or less as per the industry average (Bodie, 2013). However, for the year

2014 and 2016 it was significantly low as compared to the industry average. Further, the net

profit margin of the company for the last 5 years were significantly lower as compared to the

industry average and it was moving around 3% only. The cash flow from operation was as

per the industry average only for the year ended 2013, 2015 and 2016. However, for the other

Further, the net cash provided from financing activities were in negative till the year 2015.

However, it went up to $716 million at the closing of the period 30th June 2017. The reason

behind this must be found out.

Part IV – Ratio analysis

TYPE FORMULA 2013 2014 2015 2016 2017

Industr

y

average

liquidity ratio

Current ratio

Current asset/current

liabilities 1.27 1.64 1.62 1.57 1.32 1

long term solvency

ratio

Debt-Equity ratio Total debt/total equity 0.51 0.21 0.41 0.27 0.65 0.5

profitability ratio

Net profit margin Net profit/net sales *100 3.52 3.69 3.74 3.85 3.06 7%

cash flow adequacy ratio

Cash flow to asset ratio

Cash flow from

operation/total assets 0.19 0.05 0.20 0.19 0.08 0.20

Market strength ratio

Price earnings ratio Price/earning

18.3

7 12.44 14.30 18.66 15.08

29

Analysis of the ratios

From the above table of ratios, it is recognized that the current ratio of the company

are moving around 1.27 to 1.64. However, during the year 2014, 2015 and 2016 it is more

than 1.50 that indicates that the company may not using their working capital efficiently.

Further, there is no specific trend for the solvency ratio. During the year 2013, 2015 and

2017, it was more or less as per the industry average (Bodie, 2013). However, for the year

2014 and 2016 it was significantly low as compared to the industry average. Further, the net

profit margin of the company for the last 5 years were significantly lower as compared to the

industry average and it was moving around 3% only. The cash flow from operation was as

per the industry average only for the year ended 2013, 2015 and 2016. However, for the other

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

9INTRODUCTION TO ACCOUNTING AND FINANCE

years the ratio was significantly low. Moreover, the price earnings ratio of the company

almost half for all the years as compared to the industry average.

Part V – Conclusion

Findings

It is found from the above analysis that the company is performing steadily. However,

the net profit margin of the company of the company for the last 5 years was significantly

lower as compared to the industry average of 7% and it was moving around 3% only. Further,

the price earnings ratio of the company for all the years under consideration is considerably

low as compared to the industry average of 29.

Recommendation

As the net profit margin of the company is significantly low as compared to the

industry average, the company shall find out the areas of wastages and minimize the expenses

as far as possible. Further, the company shall try to create shareholder’s value through

generating income from sales and increasing the shareholders value.

Decision and rational

As it is identified that the company’ performance with respect to all aspect are in

increasing trend and company is regular in payment of dividend to the shareholders. Though

the price earnings ratio is lower as compared to the industry average, it is found that the

company is able to provide positive return to the shareholders throughout the period of 5

years that is under consideration. Therefore, it will be a good decision to invest in JB Hi-Fi

Limited.

years the ratio was significantly low. Moreover, the price earnings ratio of the company

almost half for all the years as compared to the industry average.

Part V – Conclusion

Findings

It is found from the above analysis that the company is performing steadily. However,

the net profit margin of the company of the company for the last 5 years was significantly

lower as compared to the industry average of 7% and it was moving around 3% only. Further,

the price earnings ratio of the company for all the years under consideration is considerably

low as compared to the industry average of 29.

Recommendation

As the net profit margin of the company is significantly low as compared to the

industry average, the company shall find out the areas of wastages and minimize the expenses

as far as possible. Further, the company shall try to create shareholder’s value through

generating income from sales and increasing the shareholders value.

Decision and rational

As it is identified that the company’ performance with respect to all aspect are in

increasing trend and company is regular in payment of dividend to the shareholders. Though

the price earnings ratio is lower as compared to the industry average, it is found that the

company is able to provide positive return to the shareholders throughout the period of 5

years that is under consideration. Therefore, it will be a good decision to invest in JB Hi-Fi

Limited.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

10INTRODUCTION TO ACCOUNTING AND FINANCE

Reference

Bailey, J., Price, R., Pyman, A., & Parker, J. (2015). Union power in retail: contrasting cases

in Australia and New Zealand. New Zealand Journal of Employment Relations

(Online), 40(1), 1.

Bodie, Z. (2013). Investments. McGraw-Hill.

Graves, C., & Shan, Y. G. (2014). An empirical analysis of the effect of internationalization

on the performance of unlisted family and nonfamily firms in Australia. Family

Business Review, 27(2), 142-160.

Hunjra, A. I., & Bashir, A. (2014). Comparative Financial Performance Analysis of

Conventional and Islamic Banks in Pakistan. Bulletin of Business and Economics

(BBE), 3(4), 196-206.

JB Hi-Fi | JB Hi-Fi - Australia's Largest Home Entertainment Retailer. (2017). Jbhifi.com.au.

Retrieved 13 September 2017, from https://www.jbhifi.com.au/

Post, C., & Byron, K. (2015). Women on boards and firm financial performance: A meta-

analysis. Academy of Management Journal, 58(5), 1546-1571.

Wagner, D., Block, J. H., Miller, D., Schwens, C., & Xi, G. (2015). A meta-analysis of the

financial performance of family firms: Another attempt. Journal of Family Business

Strategy, 6(1), 3-13.

Reference

Bailey, J., Price, R., Pyman, A., & Parker, J. (2015). Union power in retail: contrasting cases

in Australia and New Zealand. New Zealand Journal of Employment Relations

(Online), 40(1), 1.

Bodie, Z. (2013). Investments. McGraw-Hill.

Graves, C., & Shan, Y. G. (2014). An empirical analysis of the effect of internationalization

on the performance of unlisted family and nonfamily firms in Australia. Family

Business Review, 27(2), 142-160.

Hunjra, A. I., & Bashir, A. (2014). Comparative Financial Performance Analysis of

Conventional and Islamic Banks in Pakistan. Bulletin of Business and Economics

(BBE), 3(4), 196-206.

JB Hi-Fi | JB Hi-Fi - Australia's Largest Home Entertainment Retailer. (2017). Jbhifi.com.au.

Retrieved 13 September 2017, from https://www.jbhifi.com.au/

Post, C., & Byron, K. (2015). Women on boards and firm financial performance: A meta-

analysis. Academy of Management Journal, 58(5), 1546-1571.

Wagner, D., Block, J. H., Miller, D., Schwens, C., & Xi, G. (2015). A meta-analysis of the

financial performance of family firms: Another attempt. Journal of Family Business

Strategy, 6(1), 3-13.

1 out of 11

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.