Introduction to Financial Accounting

VerifiedAdded on 2023/01/07

|14

|3070

|53

AI Summary

This document provides an introduction to financial accounting, covering topics such as trading accounts, profit and loss accounts, and statement of position. It also discusses the main features of financial statements and their importance in decision making. Additionally, it includes examples and calculations for profitability ratios and liquidity ratios.

Contribute Materials

Your contribution can guide someone’s learning journey. Share your

documents today.

Introduction to Financial

Accounting

Accounting

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

TABLE OF CONTENTS

Question 1a)...............................................................................................................................3

Question 1b)...............................................................................................................................4

Question 2 a)..............................................................................................................................6

Question 2 b)..............................................................................................................................8

Question 2 c)............................................................................................................................10

REFERENCES.........................................................................................................................14

Question 1a)...............................................................................................................................3

Question 1b)...............................................................................................................................4

Question 2 a)..............................................................................................................................6

Question 2 b)..............................................................................................................................8

Question 2 c)............................................................................................................................10

REFERENCES.........................................................................................................................14

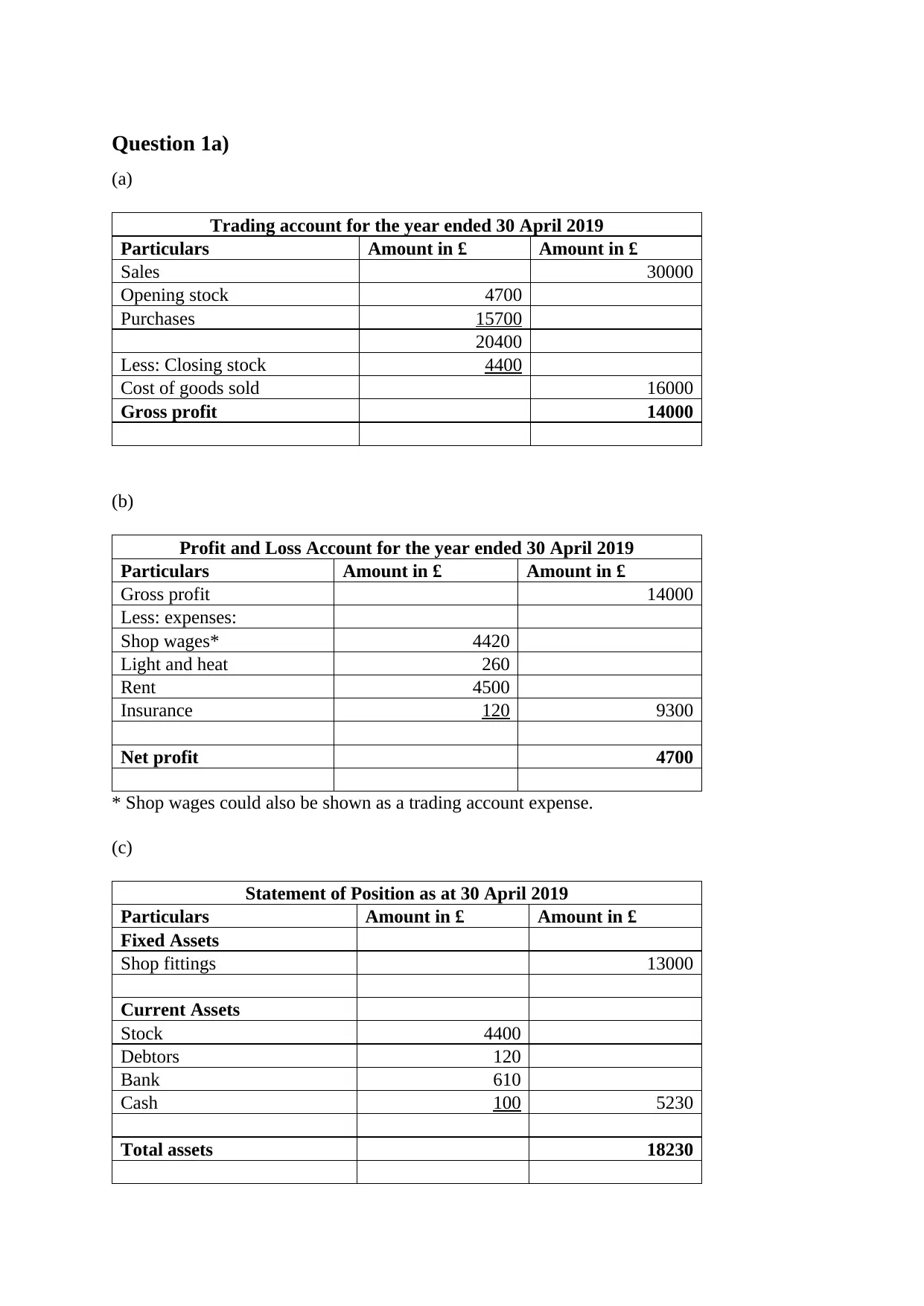

Question 1a)

(a)

Trading account for the year ended 30 April 2019

Particulars Amount in £ Amount in £

Sales 30000

Opening stock 4700

Purchases 15700

20400

Less: Closing stock 4400

Cost of goods sold 16000

Gross profit 14000

(b)

Profit and Loss Account for the year ended 30 April 2019

Particulars Amount in £ Amount in £

Gross profit 14000

Less: expenses:

Shop wages* 4420

Light and heat 260

Rent 4500

Insurance 120 9300

Net profit 4700

* Shop wages could also be shown as a trading account expense.

(c)

Statement of Position as at 30 April 2019

Particulars Amount in £ Amount in £

Fixed Assets

Shop fittings 13000

Current Assets

Stock 4400

Debtors 120

Bank 610

Cash 100 5230

Total assets 18230

(a)

Trading account for the year ended 30 April 2019

Particulars Amount in £ Amount in £

Sales 30000

Opening stock 4700

Purchases 15700

20400

Less: Closing stock 4400

Cost of goods sold 16000

Gross profit 14000

(b)

Profit and Loss Account for the year ended 30 April 2019

Particulars Amount in £ Amount in £

Gross profit 14000

Less: expenses:

Shop wages* 4420

Light and heat 260

Rent 4500

Insurance 120 9300

Net profit 4700

* Shop wages could also be shown as a trading account expense.

(c)

Statement of Position as at 30 April 2019

Particulars Amount in £ Amount in £

Fixed Assets

Shop fittings 13000

Current Assets

Stock 4400

Debtors 120

Bank 610

Cash 100 5230

Total assets 18230

Capital

Opening capital 15000

Add: profit 4700

Less: Drawings 3500 16200

Current Liabilities

Creditors 2030

Total liabilities 18230

Question 1b)

There are six main features of information provided by the financial statements are stated

below.

Relevance: This feature represents how much useful and supportive the information

for the purpose of taking important business decisions. For making the accounting data to be

relevant, it must have:

Confirmation value – Provides information in respect to the past occasions

Predictive value – Provides predictive value in regards to conceivable future events.

Accordingly, accounting information is applicable on the off chance that it can give

supportive data about past events and help in foreseeing future events or in making a move to

manage conceivable future events (Pirayesh, Forouzandeh and Louie, 2018). For instance, an

organization encountering a solid quarter and introducing these improved outcomes to the

lenders or investors is very relevant for the banks or investors in the decision making process

to stretch out or broaden credit accessible to the organization.

Representational Faithfulness: This is another feature of information which is also

called reliability, is the degree to which data precisely mirrors an organization's assets,

obligations, exchanges, and so on. To help, think about a pictorial portrayal of something, all

things considered – how precisely does the image speak to what you find, in actuality? For

bookkeeping information to have authentic faithfulness, it must be:

Complete – Financial statements ought not prohibit any transaction.

Neutral – how much data is liberated from biasness. It is important to note that there

are subjectivity and estimation engaged with fiscal summaries, in this way data can't

be truly "neutral." However, in the event that an organization surveyed 1,000

Opening capital 15000

Add: profit 4700

Less: Drawings 3500 16200

Current Liabilities

Creditors 2030

Total liabilities 18230

Question 1b)

There are six main features of information provided by the financial statements are stated

below.

Relevance: This feature represents how much useful and supportive the information

for the purpose of taking important business decisions. For making the accounting data to be

relevant, it must have:

Confirmation value – Provides information in respect to the past occasions

Predictive value – Provides predictive value in regards to conceivable future events.

Accordingly, accounting information is applicable on the off chance that it can give

supportive data about past events and help in foreseeing future events or in making a move to

manage conceivable future events (Pirayesh, Forouzandeh and Louie, 2018). For instance, an

organization encountering a solid quarter and introducing these improved outcomes to the

lenders or investors is very relevant for the banks or investors in the decision making process

to stretch out or broaden credit accessible to the organization.

Representational Faithfulness: This is another feature of information which is also

called reliability, is the degree to which data precisely mirrors an organization's assets,

obligations, exchanges, and so on. To help, think about a pictorial portrayal of something, all

things considered – how precisely does the image speak to what you find, in actuality? For

bookkeeping information to have authentic faithfulness, it must be:

Complete – Financial statements ought not prohibit any transaction.

Neutral – how much data is liberated from biasness. It is important to note that there

are subjectivity and estimation engaged with fiscal summaries, in this way data can't

be truly "neutral." However, in the event that an organization surveyed 1,000

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

bookkeepers and took the average of their answers, that would be viewed as unbiased

and liberated from errors.

Free from mistake – the level to which how much data is free from blunders or errors.

Verifiability: It is the degree to which data is reproducible with the given similar

information and the assumptions. For instance, if an organization possesses hardware worth

$1,000 and told a bookkeeper the buying cost, salvage value, method of depreciation, and life

of the asset, the accountant ought to have the option to imitate a similar outcome. In the event

that they can't, the data is considered not unquestionable.

Timeliness: It refers to how rapidly the data is accessible to clients of accounting

information (Floştoiu, 2019). The less timely (in this way bringing about an older data), the

less valuable data is for purpose of decision making. Timeliness matters for bookkeeping data

since it contends with other data. For instance, if an organization gives its fiscal reports a year

after its bookkeeping period, clients of budget summaries would think that it’s hard to decide

how well the organization is getting along in the present.

Understandability: This feature refers to as how much data is effectively comprehended.

In the present society, corporate yearly reports are more than 100 pages, with noteworthy

subjective data. Data that is understandable to the normal client of financial reports is

exceptionally desirable. It is regular for inadequately performing organizations to utilize a

great deal of language and troublesome phrasing in its financial report in order to trying to

mask the underperformance.

Comparability: It is the degree to how much accounting guidelines and approaches are

reliably applied starting with one period then onto the next. Annual summaries that are

comparable, with consistent bookkeeping guidelines and approaches applied all through each

bookkeeping period, empower clients to reach insightful conclusion about the patterns and

execution of the organization over the period of time. Furthermore, comparability

additionally alludes to the ability to handily compare and contrast an organization's fiscal

summaries with those of different organizations within the same industry.

Benefits and importance of features of information to its users

These features of the accounting information are very crucial as it make it very easy

for the management along with the investors in effectively utilizing the organization’s

financial information provided in the reports in order to make an informed and better

and liberated from errors.

Free from mistake – the level to which how much data is free from blunders or errors.

Verifiability: It is the degree to which data is reproducible with the given similar

information and the assumptions. For instance, if an organization possesses hardware worth

$1,000 and told a bookkeeper the buying cost, salvage value, method of depreciation, and life

of the asset, the accountant ought to have the option to imitate a similar outcome. In the event

that they can't, the data is considered not unquestionable.

Timeliness: It refers to how rapidly the data is accessible to clients of accounting

information (Floştoiu, 2019). The less timely (in this way bringing about an older data), the

less valuable data is for purpose of decision making. Timeliness matters for bookkeeping data

since it contends with other data. For instance, if an organization gives its fiscal reports a year

after its bookkeeping period, clients of budget summaries would think that it’s hard to decide

how well the organization is getting along in the present.

Understandability: This feature refers to as how much data is effectively comprehended.

In the present society, corporate yearly reports are more than 100 pages, with noteworthy

subjective data. Data that is understandable to the normal client of financial reports is

exceptionally desirable. It is regular for inadequately performing organizations to utilize a

great deal of language and troublesome phrasing in its financial report in order to trying to

mask the underperformance.

Comparability: It is the degree to how much accounting guidelines and approaches are

reliably applied starting with one period then onto the next. Annual summaries that are

comparable, with consistent bookkeeping guidelines and approaches applied all through each

bookkeeping period, empower clients to reach insightful conclusion about the patterns and

execution of the organization over the period of time. Furthermore, comparability

additionally alludes to the ability to handily compare and contrast an organization's fiscal

summaries with those of different organizations within the same industry.

Benefits and importance of features of information to its users

These features of the accounting information are very crucial as it make it very easy

for the management along with the investors in effectively utilizing the organization’s

financial information provided in the reports in order to make an informed and better

decisions. For making the right decision, it is very important to comply with the above stated

characteristics of information which leads to true and fair presentation of the financial

information of the company leading to meaningful decision making.

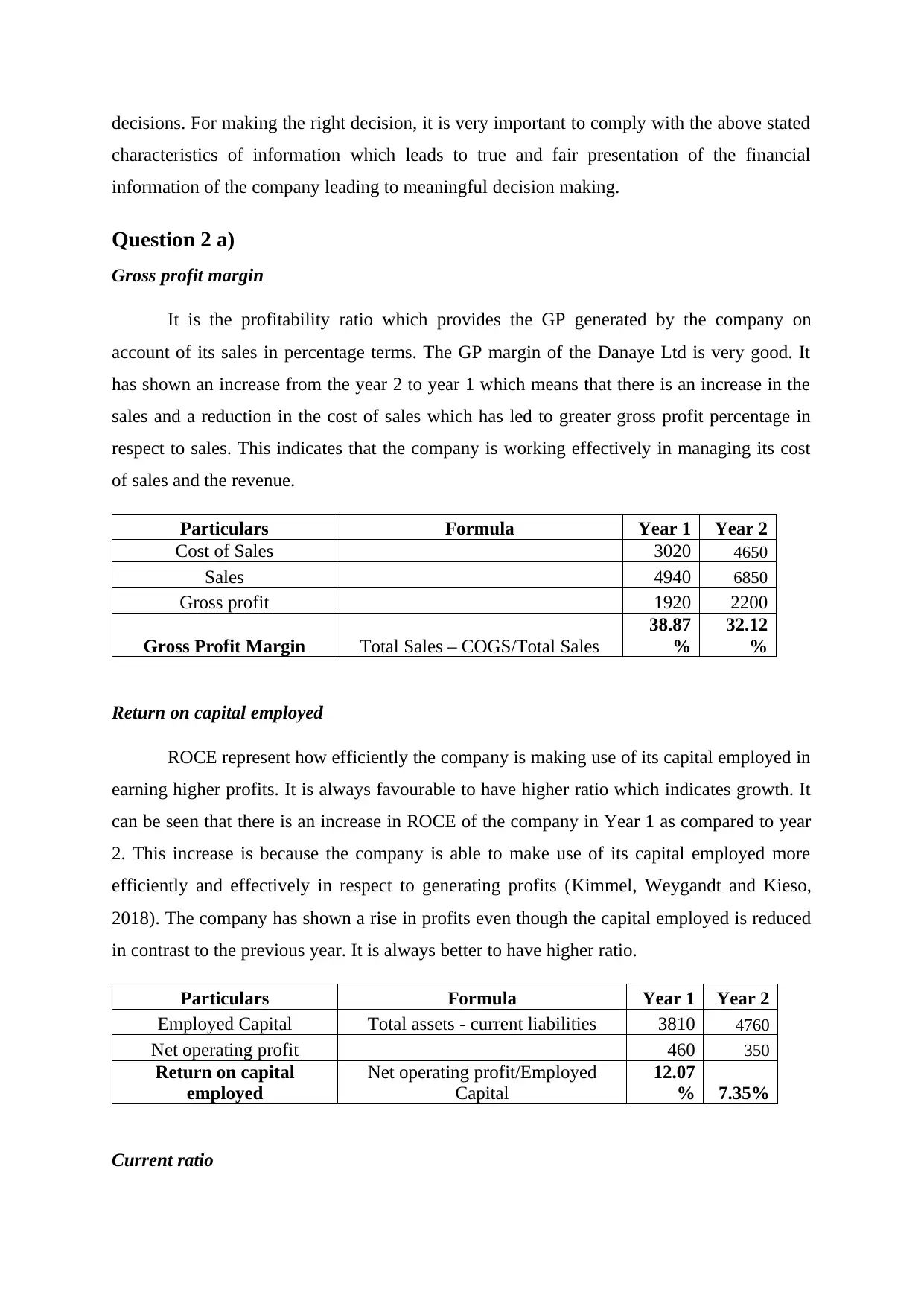

Question 2 a)

Gross profit margin

It is the profitability ratio which provides the GP generated by the company on

account of its sales in percentage terms. The GP margin of the Danaye Ltd is very good. It

has shown an increase from the year 2 to year 1 which means that there is an increase in the

sales and a reduction in the cost of sales which has led to greater gross profit percentage in

respect to sales. This indicates that the company is working effectively in managing its cost

of sales and the revenue.

Particulars Formula Year 1 Year 2

Cost of Sales 3020 4650

Sales 4940 6850

Gross profit 1920 2200

Gross Profit Margin Total Sales – COGS/Total Sales

38.87

%

32.12

%

Return on capital employed

ROCE represent how efficiently the company is making use of its capital employed in

earning higher profits. It is always favourable to have higher ratio which indicates growth. It

can be seen that there is an increase in ROCE of the company in Year 1 as compared to year

2. This increase is because the company is able to make use of its capital employed more

efficiently and effectively in respect to generating profits (Kimmel, Weygandt and Kieso,

2018). The company has shown a rise in profits even though the capital employed is reduced

in contrast to the previous year. It is always better to have higher ratio.

Particulars Formula Year 1 Year 2

Employed Capital Total assets - current liabilities 3810 4760

Net operating profit 460 350

Return on capital

employed

Net operating profit/Employed

Capital

12.07

% 7.35%

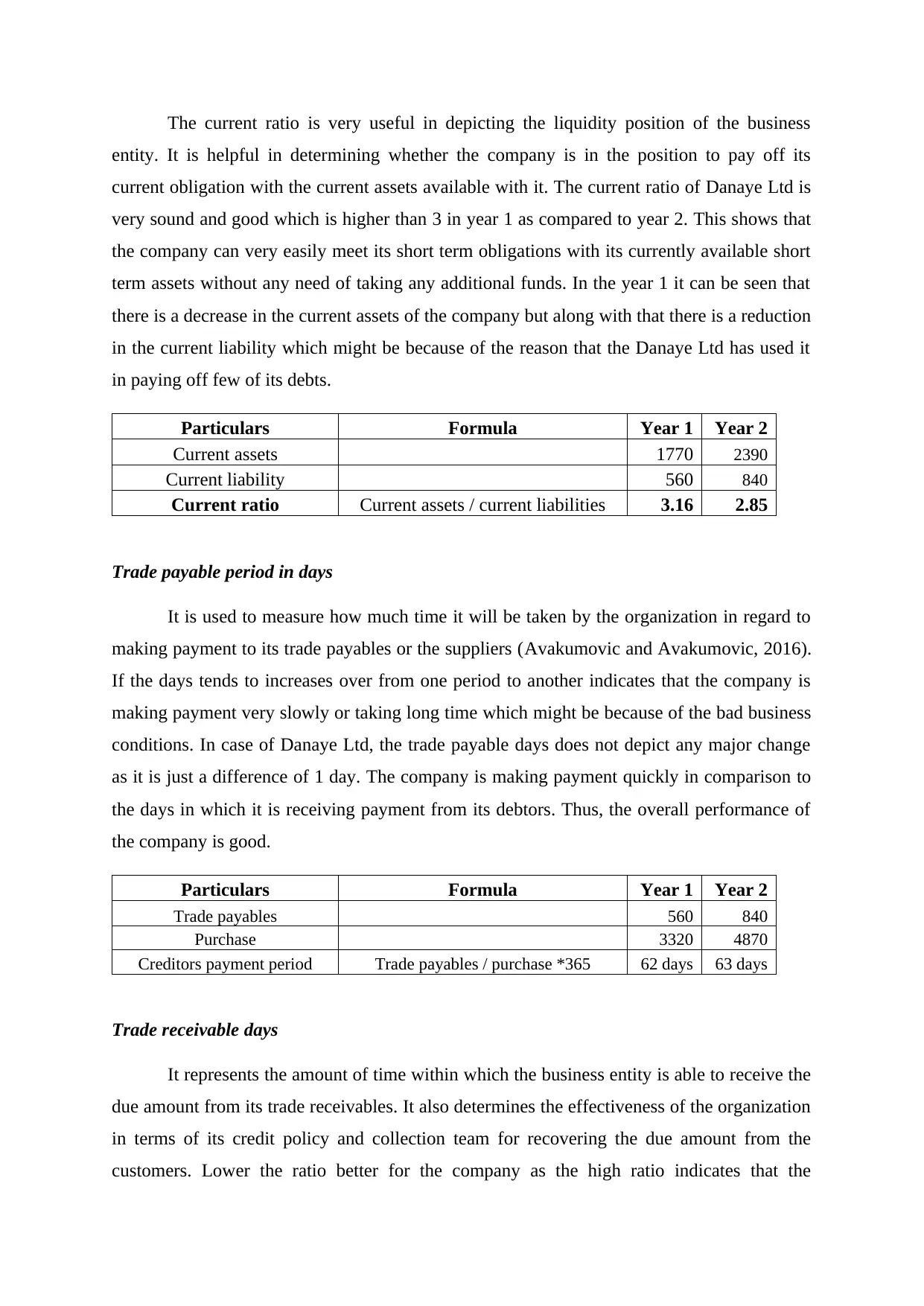

Current ratio

characteristics of information which leads to true and fair presentation of the financial

information of the company leading to meaningful decision making.

Question 2 a)

Gross profit margin

It is the profitability ratio which provides the GP generated by the company on

account of its sales in percentage terms. The GP margin of the Danaye Ltd is very good. It

has shown an increase from the year 2 to year 1 which means that there is an increase in the

sales and a reduction in the cost of sales which has led to greater gross profit percentage in

respect to sales. This indicates that the company is working effectively in managing its cost

of sales and the revenue.

Particulars Formula Year 1 Year 2

Cost of Sales 3020 4650

Sales 4940 6850

Gross profit 1920 2200

Gross Profit Margin Total Sales – COGS/Total Sales

38.87

%

32.12

%

Return on capital employed

ROCE represent how efficiently the company is making use of its capital employed in

earning higher profits. It is always favourable to have higher ratio which indicates growth. It

can be seen that there is an increase in ROCE of the company in Year 1 as compared to year

2. This increase is because the company is able to make use of its capital employed more

efficiently and effectively in respect to generating profits (Kimmel, Weygandt and Kieso,

2018). The company has shown a rise in profits even though the capital employed is reduced

in contrast to the previous year. It is always better to have higher ratio.

Particulars Formula Year 1 Year 2

Employed Capital Total assets - current liabilities 3810 4760

Net operating profit 460 350

Return on capital

employed

Net operating profit/Employed

Capital

12.07

% 7.35%

Current ratio

The current ratio is very useful in depicting the liquidity position of the business

entity. It is helpful in determining whether the company is in the position to pay off its

current obligation with the current assets available with it. The current ratio of Danaye Ltd is

very sound and good which is higher than 3 in year 1 as compared to year 2. This shows that

the company can very easily meet its short term obligations with its currently available short

term assets without any need of taking any additional funds. In the year 1 it can be seen that

there is a decrease in the current assets of the company but along with that there is a reduction

in the current liability which might be because of the reason that the Danaye Ltd has used it

in paying off few of its debts.

Particulars Formula Year 1 Year 2

Current assets 1770 2390

Current liability 560 840

Current ratio Current assets / current liabilities 3.16 2.85

Trade payable period in days

It is used to measure how much time it will be taken by the organization in regard to

making payment to its trade payables or the suppliers (Avakumovic and Avakumovic, 2016).

If the days tends to increases over from one period to another indicates that the company is

making payment very slowly or taking long time which might be because of the bad business

conditions. In case of Danaye Ltd, the trade payable days does not depict any major change

as it is just a difference of 1 day. The company is making payment quickly in comparison to

the days in which it is receiving payment from its debtors. Thus, the overall performance of

the company is good.

Particulars Formula Year 1 Year 2

Trade payables 560 840

Purchase 3320 4870

Creditors payment period Trade payables / purchase *365 62 days 63 days

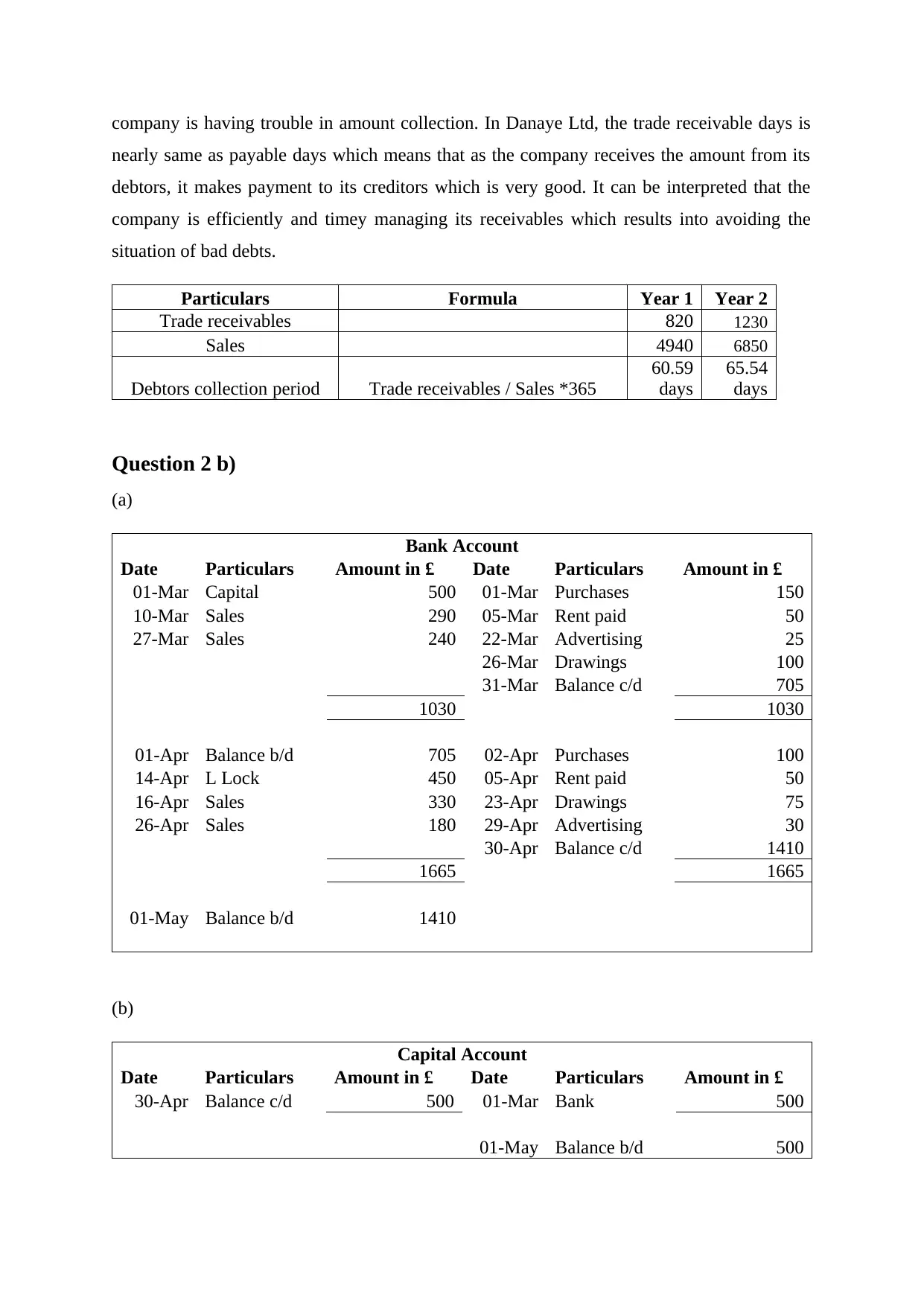

Trade receivable days

It represents the amount of time within which the business entity is able to receive the

due amount from its trade receivables. It also determines the effectiveness of the organization

in terms of its credit policy and collection team for recovering the due amount from the

customers. Lower the ratio better for the company as the high ratio indicates that the

entity. It is helpful in determining whether the company is in the position to pay off its

current obligation with the current assets available with it. The current ratio of Danaye Ltd is

very sound and good which is higher than 3 in year 1 as compared to year 2. This shows that

the company can very easily meet its short term obligations with its currently available short

term assets without any need of taking any additional funds. In the year 1 it can be seen that

there is a decrease in the current assets of the company but along with that there is a reduction

in the current liability which might be because of the reason that the Danaye Ltd has used it

in paying off few of its debts.

Particulars Formula Year 1 Year 2

Current assets 1770 2390

Current liability 560 840

Current ratio Current assets / current liabilities 3.16 2.85

Trade payable period in days

It is used to measure how much time it will be taken by the organization in regard to

making payment to its trade payables or the suppliers (Avakumovic and Avakumovic, 2016).

If the days tends to increases over from one period to another indicates that the company is

making payment very slowly or taking long time which might be because of the bad business

conditions. In case of Danaye Ltd, the trade payable days does not depict any major change

as it is just a difference of 1 day. The company is making payment quickly in comparison to

the days in which it is receiving payment from its debtors. Thus, the overall performance of

the company is good.

Particulars Formula Year 1 Year 2

Trade payables 560 840

Purchase 3320 4870

Creditors payment period Trade payables / purchase *365 62 days 63 days

Trade receivable days

It represents the amount of time within which the business entity is able to receive the

due amount from its trade receivables. It also determines the effectiveness of the organization

in terms of its credit policy and collection team for recovering the due amount from the

customers. Lower the ratio better for the company as the high ratio indicates that the

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

company is having trouble in amount collection. In Danaye Ltd, the trade receivable days is

nearly same as payable days which means that as the company receives the amount from its

debtors, it makes payment to its creditors which is very good. It can be interpreted that the

company is efficiently and timey managing its receivables which results into avoiding the

situation of bad debts.

Particulars Formula Year 1 Year 2

Trade receivables 820 1230

Sales 4940 6850

Debtors collection period Trade receivables / Sales *365

60.59

days

65.54

days

Question 2 b)

(a)

Bank Account

Date Particulars Amount in £ Date Particulars Amount in £

01-Mar Capital 500 01-Mar Purchases 150

10-Mar Sales 290 05-Mar Rent paid 50

27-Mar Sales 240 22-Mar Advertising 25

26-Mar Drawings 100

31-Mar Balance c/d 705

1030 1030

01-Apr Balance b/d 705 02-Apr Purchases 100

14-Apr L Lock 450 05-Apr Rent paid 50

16-Apr Sales 330 23-Apr Drawings 75

26-Apr Sales 180 29-Apr Advertising 30

30-Apr Balance c/d 1410

1665 1665

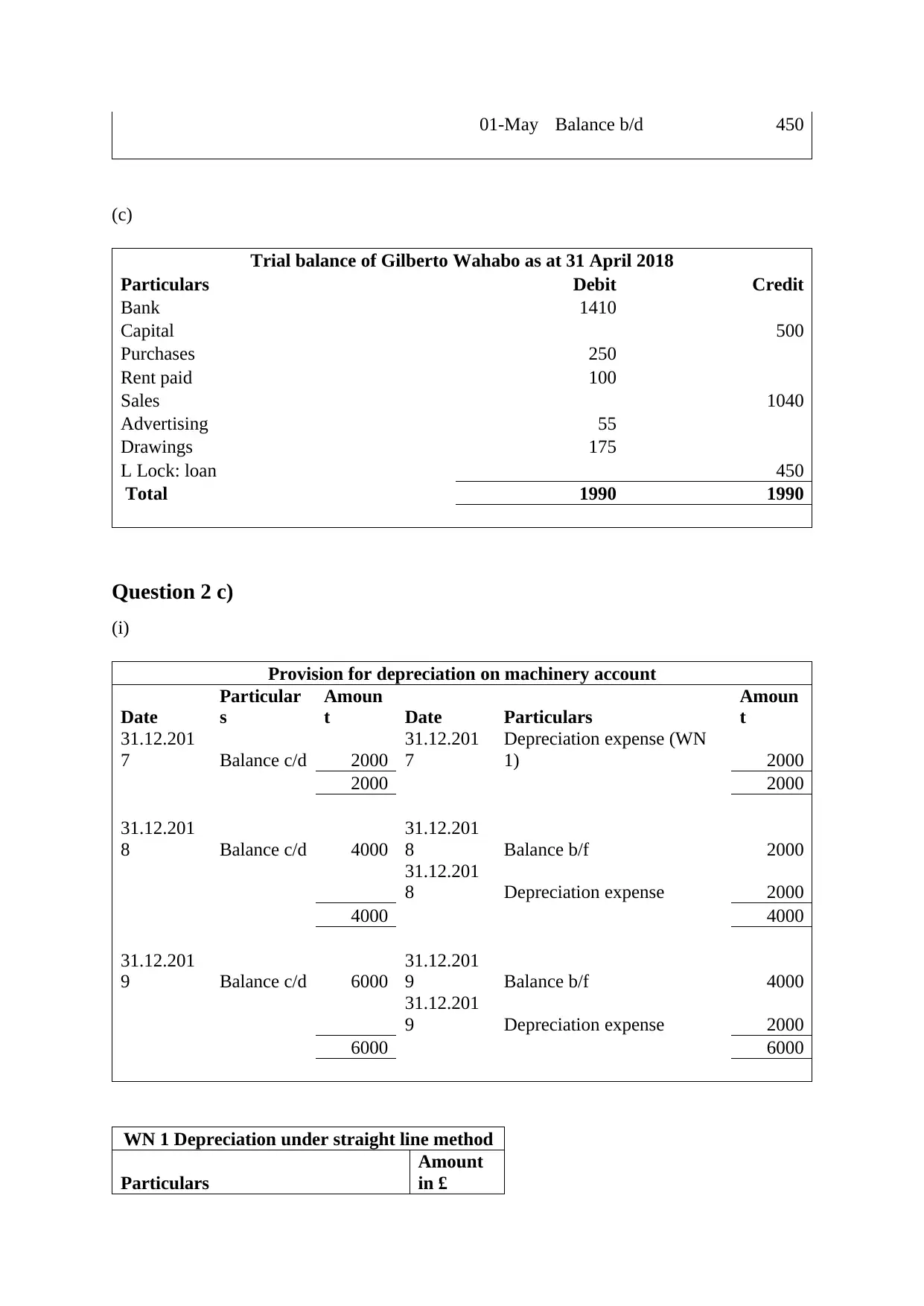

01-May Balance b/d 1410

(b)

Capital Account

Date Particulars Amount in £ Date Particulars Amount in £

30-Apr Balance c/d 500 01-Mar Bank 500

01-May Balance b/d 500

nearly same as payable days which means that as the company receives the amount from its

debtors, it makes payment to its creditors which is very good. It can be interpreted that the

company is efficiently and timey managing its receivables which results into avoiding the

situation of bad debts.

Particulars Formula Year 1 Year 2

Trade receivables 820 1230

Sales 4940 6850

Debtors collection period Trade receivables / Sales *365

60.59

days

65.54

days

Question 2 b)

(a)

Bank Account

Date Particulars Amount in £ Date Particulars Amount in £

01-Mar Capital 500 01-Mar Purchases 150

10-Mar Sales 290 05-Mar Rent paid 50

27-Mar Sales 240 22-Mar Advertising 25

26-Mar Drawings 100

31-Mar Balance c/d 705

1030 1030

01-Apr Balance b/d 705 02-Apr Purchases 100

14-Apr L Lock 450 05-Apr Rent paid 50

16-Apr Sales 330 23-Apr Drawings 75

26-Apr Sales 180 29-Apr Advertising 30

30-Apr Balance c/d 1410

1665 1665

01-May Balance b/d 1410

(b)

Capital Account

Date Particulars Amount in £ Date Particulars Amount in £

30-Apr Balance c/d 500 01-Mar Bank 500

01-May Balance b/d 500

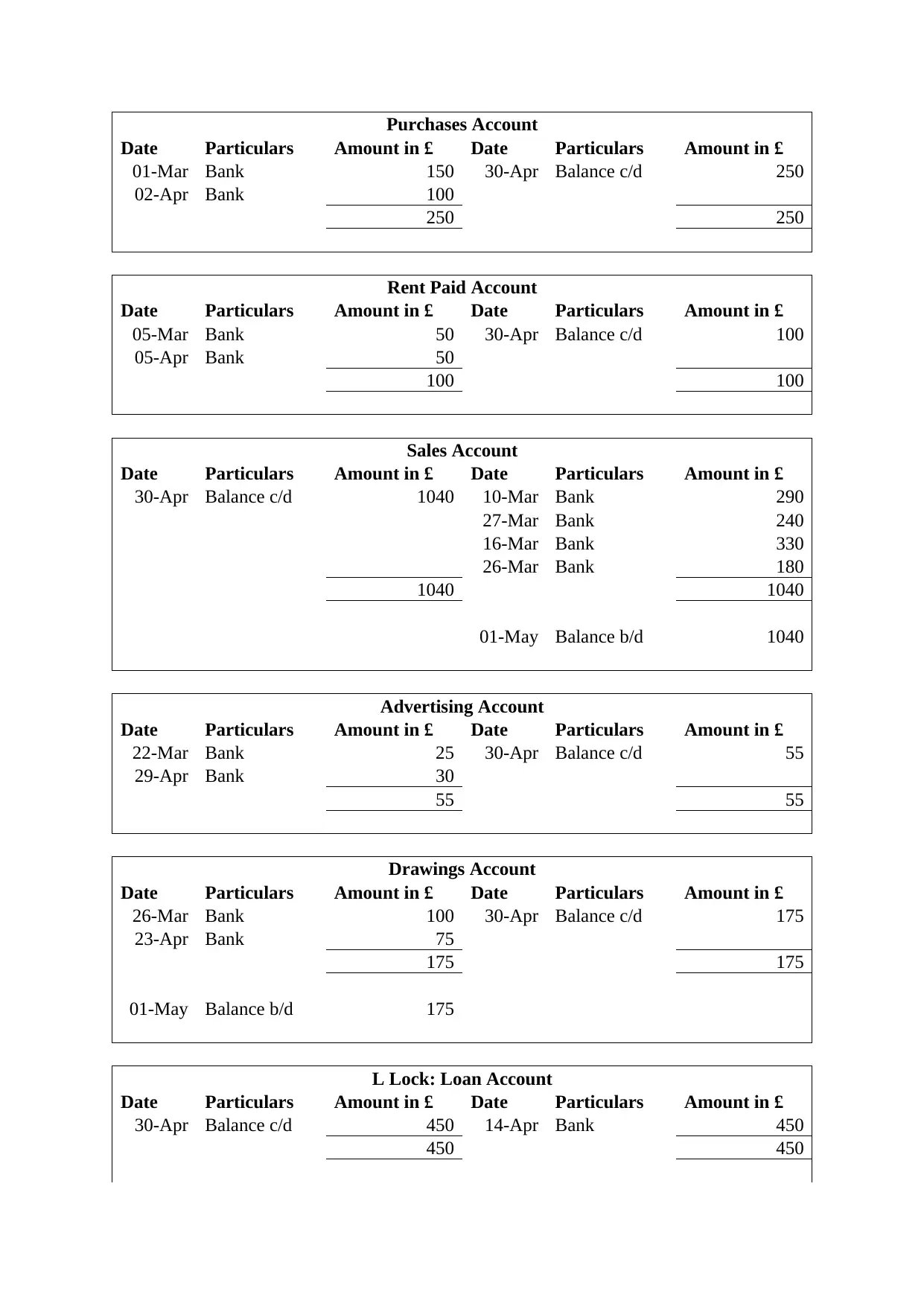

Purchases Account

Date Particulars Amount in £ Date Particulars Amount in £

01-Mar Bank 150 30-Apr Balance c/d 250

02-Apr Bank 100

250 250

Rent Paid Account

Date Particulars Amount in £ Date Particulars Amount in £

05-Mar Bank 50 30-Apr Balance c/d 100

05-Apr Bank 50

100 100

Sales Account

Date Particulars Amount in £ Date Particulars Amount in £

30-Apr Balance c/d 1040 10-Mar Bank 290

27-Mar Bank 240

16-Mar Bank 330

26-Mar Bank 180

1040 1040

01-May Balance b/d 1040

Advertising Account

Date Particulars Amount in £ Date Particulars Amount in £

22-Mar Bank 25 30-Apr Balance c/d 55

29-Apr Bank 30

55 55

Drawings Account

Date Particulars Amount in £ Date Particulars Amount in £

26-Mar Bank 100 30-Apr Balance c/d 175

23-Apr Bank 75

175 175

01-May Balance b/d 175

L Lock: Loan Account

Date Particulars Amount in £ Date Particulars Amount in £

30-Apr Balance c/d 450 14-Apr Bank 450

450 450

Date Particulars Amount in £ Date Particulars Amount in £

01-Mar Bank 150 30-Apr Balance c/d 250

02-Apr Bank 100

250 250

Rent Paid Account

Date Particulars Amount in £ Date Particulars Amount in £

05-Mar Bank 50 30-Apr Balance c/d 100

05-Apr Bank 50

100 100

Sales Account

Date Particulars Amount in £ Date Particulars Amount in £

30-Apr Balance c/d 1040 10-Mar Bank 290

27-Mar Bank 240

16-Mar Bank 330

26-Mar Bank 180

1040 1040

01-May Balance b/d 1040

Advertising Account

Date Particulars Amount in £ Date Particulars Amount in £

22-Mar Bank 25 30-Apr Balance c/d 55

29-Apr Bank 30

55 55

Drawings Account

Date Particulars Amount in £ Date Particulars Amount in £

26-Mar Bank 100 30-Apr Balance c/d 175

23-Apr Bank 75

175 175

01-May Balance b/d 175

L Lock: Loan Account

Date Particulars Amount in £ Date Particulars Amount in £

30-Apr Balance c/d 450 14-Apr Bank 450

450 450

01-May Balance b/d 450

(c)

Trial balance of Gilberto Wahabo as at 31 April 2018

Particulars Debit Credit

Bank 1410

Capital 500

Purchases 250

Rent paid 100

Sales 1040

Advertising 55

Drawings 175

L Lock: loan 450

Total 1990 1990

Question 2 c)

(i)

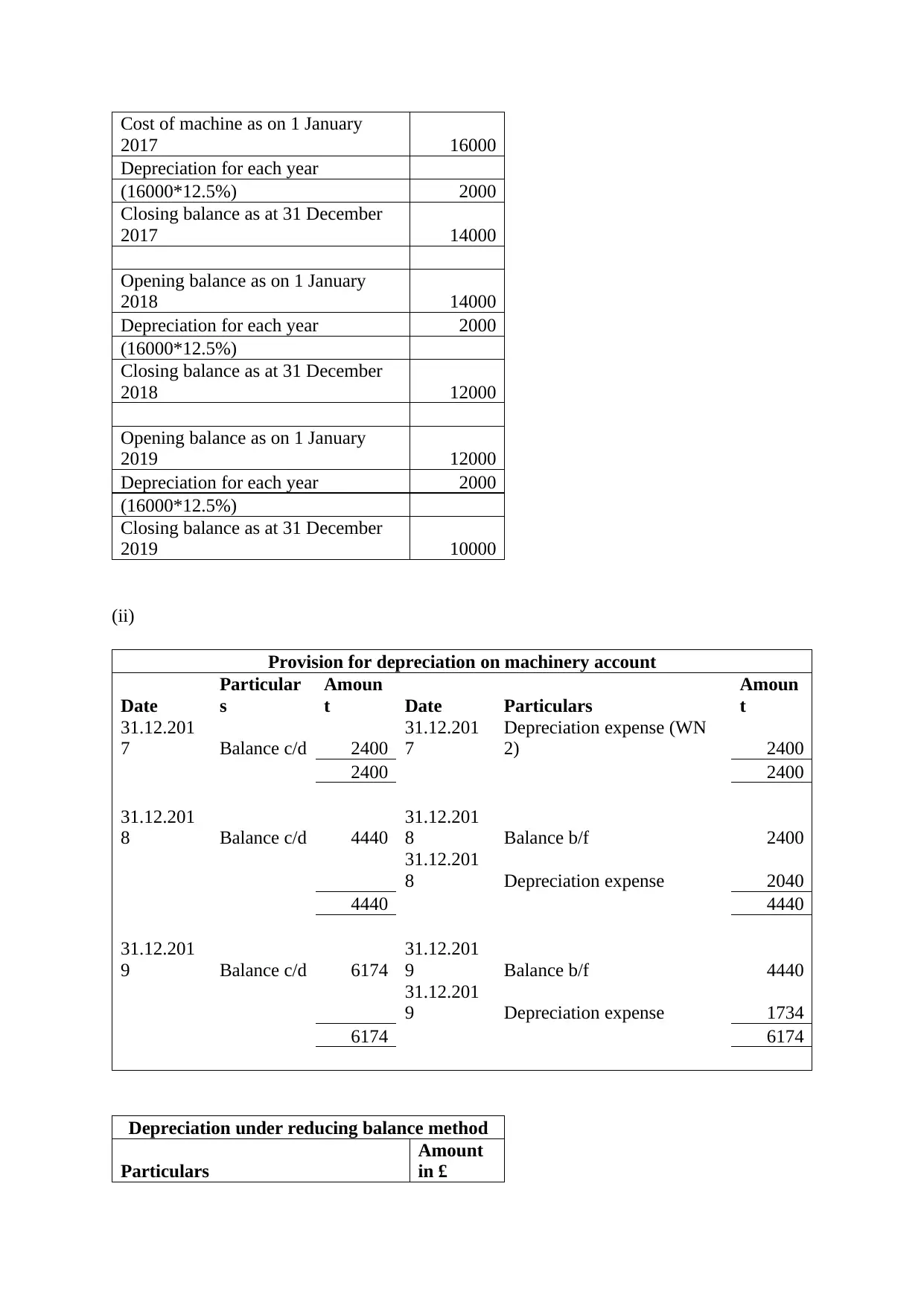

Provision for depreciation on machinery account

Date

Particular

s

Amoun

t Date Particulars

Amoun

t

31.12.201

7 Balance c/d 2000

31.12.201

7

Depreciation expense (WN

1) 2000

2000 2000

31.12.201

8 Balance c/d 4000

31.12.201

8 Balance b/f 2000

31.12.201

8 Depreciation expense 2000

4000 4000

31.12.201

9 Balance c/d 6000

31.12.201

9 Balance b/f 4000

31.12.201

9 Depreciation expense 2000

6000 6000

WN 1 Depreciation under straight line method

Particulars

Amount

in £

(c)

Trial balance of Gilberto Wahabo as at 31 April 2018

Particulars Debit Credit

Bank 1410

Capital 500

Purchases 250

Rent paid 100

Sales 1040

Advertising 55

Drawings 175

L Lock: loan 450

Total 1990 1990

Question 2 c)

(i)

Provision for depreciation on machinery account

Date

Particular

s

Amoun

t Date Particulars

Amoun

t

31.12.201

7 Balance c/d 2000

31.12.201

7

Depreciation expense (WN

1) 2000

2000 2000

31.12.201

8 Balance c/d 4000

31.12.201

8 Balance b/f 2000

31.12.201

8 Depreciation expense 2000

4000 4000

31.12.201

9 Balance c/d 6000

31.12.201

9 Balance b/f 4000

31.12.201

9 Depreciation expense 2000

6000 6000

WN 1 Depreciation under straight line method

Particulars

Amount

in £

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

Cost of machine as on 1 January

2017 16000

Depreciation for each year

(16000*12.5%) 2000

Closing balance as at 31 December

2017 14000

Opening balance as on 1 January

2018 14000

Depreciation for each year 2000

(16000*12.5%)

Closing balance as at 31 December

2018 12000

Opening balance as on 1 January

2019 12000

Depreciation for each year 2000

(16000*12.5%)

Closing balance as at 31 December

2019 10000

(ii)

Provision for depreciation on machinery account

Date

Particular

s

Amoun

t Date Particulars

Amoun

t

31.12.201

7 Balance c/d 2400

31.12.201

7

Depreciation expense (WN

2) 2400

2400 2400

31.12.201

8 Balance c/d 4440

31.12.201

8 Balance b/f 2400

31.12.201

8 Depreciation expense 2040

4440 4440

31.12.201

9 Balance c/d 6174

31.12.201

9 Balance b/f 4440

31.12.201

9 Depreciation expense 1734

6174 6174

Depreciation under reducing balance method

Particulars

Amount

in £

2017 16000

Depreciation for each year

(16000*12.5%) 2000

Closing balance as at 31 December

2017 14000

Opening balance as on 1 January

2018 14000

Depreciation for each year 2000

(16000*12.5%)

Closing balance as at 31 December

2018 12000

Opening balance as on 1 January

2019 12000

Depreciation for each year 2000

(16000*12.5%)

Closing balance as at 31 December

2019 10000

(ii)

Provision for depreciation on machinery account

Date

Particular

s

Amoun

t Date Particulars

Amoun

t

31.12.201

7 Balance c/d 2400

31.12.201

7

Depreciation expense (WN

2) 2400

2400 2400

31.12.201

8 Balance c/d 4440

31.12.201

8 Balance b/f 2400

31.12.201

8 Depreciation expense 2040

4440 4440

31.12.201

9 Balance c/d 6174

31.12.201

9 Balance b/f 4440

31.12.201

9 Depreciation expense 1734

6174 6174

Depreciation under reducing balance method

Particulars

Amount

in £

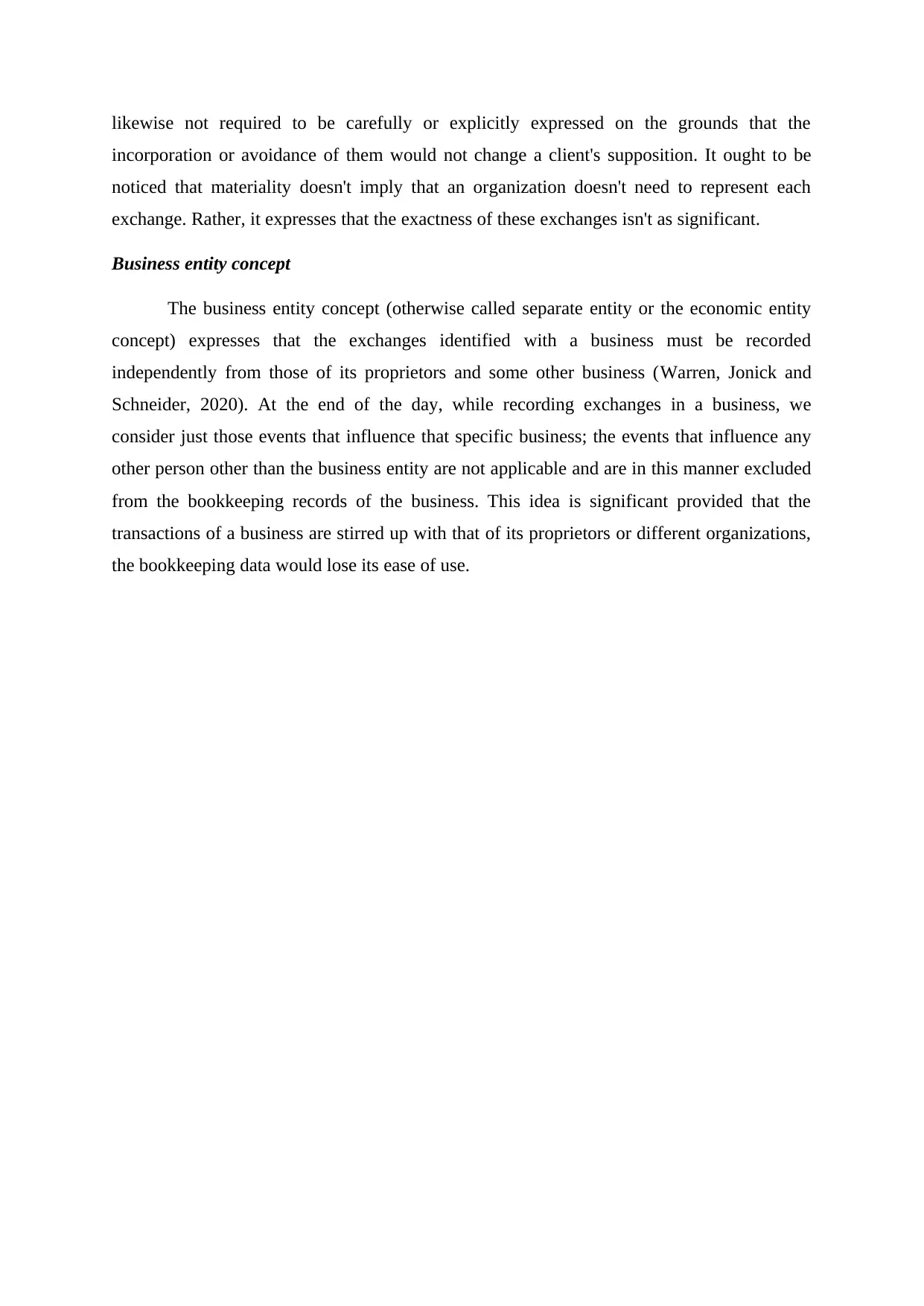

Cost of machine as on 1 January

2017 16000

Depreciation for each year

(16000*15%) 2400

Closing balance as at 31 December

2017 13600

Opening balance as on 1 January

2018 13600

Depreciation for each year 2040

(13600*15%)

Closing balance as at 31 December

2018 11560

Opening balance as on 1 January

2019 11560

Depreciation for each year 1734

(11560*15%)

Closing balance as at 31 December

2019 9826

(iii)

Going Concern Concept

Otherwise called the continuity concept, the going concern basically expresses that a

business organization will proceed to exist and stay in business in the unforeseeable future.

Picture a business that stops to exist anymore. At the point when this occurs, the business

needs to exchange or auction the resources for take care of the liabilities first. At that point

the business circulates any outstanding incentive to the equity holders (Kumor and

Poniatowska, 2017). This is then a proportion of the current worth. Be that as it may, in the

event that the business keeps on developing and stay in business, at that point the business

may not be able to measure the actual worth and it turns into a going concern. It is considered

that there is no intention of the business to shut down or cease its business in the future and if

the situation arises of the same, then it has to disclose it in the financial reports.

Materiality

The materiality concept basically expresses that an organization should carefully state

records and exchanges that are huge to the association's activities. A record or exchange is

material if it's consideration in the financial summaries were to alter the final decision of the

users. Irrelevant things are insignificant (Beske, Haustein and Lorson, 2019). They are

2017 16000

Depreciation for each year

(16000*15%) 2400

Closing balance as at 31 December

2017 13600

Opening balance as on 1 January

2018 13600

Depreciation for each year 2040

(13600*15%)

Closing balance as at 31 December

2018 11560

Opening balance as on 1 January

2019 11560

Depreciation for each year 1734

(11560*15%)

Closing balance as at 31 December

2019 9826

(iii)

Going Concern Concept

Otherwise called the continuity concept, the going concern basically expresses that a

business organization will proceed to exist and stay in business in the unforeseeable future.

Picture a business that stops to exist anymore. At the point when this occurs, the business

needs to exchange or auction the resources for take care of the liabilities first. At that point

the business circulates any outstanding incentive to the equity holders (Kumor and

Poniatowska, 2017). This is then a proportion of the current worth. Be that as it may, in the

event that the business keeps on developing and stay in business, at that point the business

may not be able to measure the actual worth and it turns into a going concern. It is considered

that there is no intention of the business to shut down or cease its business in the future and if

the situation arises of the same, then it has to disclose it in the financial reports.

Materiality

The materiality concept basically expresses that an organization should carefully state

records and exchanges that are huge to the association's activities. A record or exchange is

material if it's consideration in the financial summaries were to alter the final decision of the

users. Irrelevant things are insignificant (Beske, Haustein and Lorson, 2019). They are

likewise not required to be carefully or explicitly expressed on the grounds that the

incorporation or avoidance of them would not change a client's supposition. It ought to be

noticed that materiality doesn't imply that an organization doesn't need to represent each

exchange. Rather, it expresses that the exactness of these exchanges isn't as significant.

Business entity concept

The business entity concept (otherwise called separate entity or the economic entity

concept) expresses that the exchanges identified with a business must be recorded

independently from those of its proprietors and some other business (Warren, Jonick and

Schneider, 2020). At the end of the day, while recording exchanges in a business, we

consider just those events that influence that specific business; the events that influence any

other person other than the business entity are not applicable and are in this manner excluded

from the bookkeeping records of the business. This idea is significant provided that the

transactions of a business are stirred up with that of its proprietors or different organizations,

the bookkeeping data would lose its ease of use.

incorporation or avoidance of them would not change a client's supposition. It ought to be

noticed that materiality doesn't imply that an organization doesn't need to represent each

exchange. Rather, it expresses that the exactness of these exchanges isn't as significant.

Business entity concept

The business entity concept (otherwise called separate entity or the economic entity

concept) expresses that the exchanges identified with a business must be recorded

independently from those of its proprietors and some other business (Warren, Jonick and

Schneider, 2020). At the end of the day, while recording exchanges in a business, we

consider just those events that influence that specific business; the events that influence any

other person other than the business entity are not applicable and are in this manner excluded

from the bookkeeping records of the business. This idea is significant provided that the

transactions of a business are stirred up with that of its proprietors or different organizations,

the bookkeeping data would lose its ease of use.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

REFERENCES

Books and Journals

Avakumovic, J. and Avakumovic, J., 2016. Method Financial Analysis and Impact on the

Quality of Decision Making. EuroEconomica. 35(2).

Beske, F., Haustein, E. and Lorson, P. C., 2019. Materiality analysis in sustainability and

integrated reports. Sustainability Accounting, Management and Policy Journal.

Floştoiu, S., 2019, June. The Role and Place of Accounting Information in the Decision-

Making System. In International conference KNOWLEDGE-BASED

ORGANIZATION (Vol. 25, No. 2, pp. 46-51). Sciendo.

Kimmel, P. D., Weygandt, J. J. and Kieso, D. E., 2018. Financial accounting: Tools for

business decision making. John Wiley & Sons.

Kumor, I. and Poniatowska, L., 2017. The going-concern assumption in the assessment of

management and auditors. Economic and Social Development: Book of Proceedings.

pp.804-812.

Pirayesh, R., Forouzandeh, M. and Louie, S. I., 2018. Examining the effect of computerized

accounting information system on managers' decision making process. Revista

Publicando. 5(14 (1)). pp.68-82.

Warren, C., Jonick, C. and Schneider, J., 2020. Accounting. Cengage Learning.

Books and Journals

Avakumovic, J. and Avakumovic, J., 2016. Method Financial Analysis and Impact on the

Quality of Decision Making. EuroEconomica. 35(2).

Beske, F., Haustein, E. and Lorson, P. C., 2019. Materiality analysis in sustainability and

integrated reports. Sustainability Accounting, Management and Policy Journal.

Floştoiu, S., 2019, June. The Role and Place of Accounting Information in the Decision-

Making System. In International conference KNOWLEDGE-BASED

ORGANIZATION (Vol. 25, No. 2, pp. 46-51). Sciendo.

Kimmel, P. D., Weygandt, J. J. and Kieso, D. E., 2018. Financial accounting: Tools for

business decision making. John Wiley & Sons.

Kumor, I. and Poniatowska, L., 2017. The going-concern assumption in the assessment of

management and auditors. Economic and Social Development: Book of Proceedings.

pp.804-812.

Pirayesh, R., Forouzandeh, M. and Louie, S. I., 2018. Examining the effect of computerized

accounting information system on managers' decision making process. Revista

Publicando. 5(14 (1)). pp.68-82.

Warren, C., Jonick, C. and Schneider, J., 2020. Accounting. Cengage Learning.

1 out of 14

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

© 2024 | Zucol Services PVT LTD | All rights reserved.