Variance Analysis in Management Accounting

VerifiedAdded on 2023/01/07

|12

|3140

|31

AI Summary

This document discusses variance analysis in management accounting, specifically focusing on sales price variance, sales volume contribution variance, material price planning variance, and material price operational variance. It also critically analyzes the merits and demerits of using variances in assessing managers' performance. Additionally, it explores the competitive advantage provided by FamaQ, the demand for chemical X and Y, and the final decision on whether to make or buy the raw material famaQ.

Contribute Materials

Your contribution can guide someone’s learning journey. Share your

documents today.

Management Accounting-2

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

Table of Contents

Introduction......................................................................................................................................3

PART A...........................................................................................................................................3

i) The sales price variance and sales volume contribution variance............................................3

ii) The material price planning variance and material price operational variance.......................5

iii. Critically analyze the merits and demerits of using variances in assessing managers

performance.................................................................................................................................5

PART B...........................................................................................................................................9

a) FamaQ gives XLG competitive advantage..............................................................................9

b) Demand for chemical X and Y................................................................................................9

c) Final decision whether to buy or make famaQ......................................................................10

Conclusion.....................................................................................................................................11

References......................................................................................................................................12

Introduction......................................................................................................................................3

PART A...........................................................................................................................................3

i) The sales price variance and sales volume contribution variance............................................3

ii) The material price planning variance and material price operational variance.......................5

iii. Critically analyze the merits and demerits of using variances in assessing managers

performance.................................................................................................................................5

PART B...........................................................................................................................................9

a) FamaQ gives XLG competitive advantage..............................................................................9

b) Demand for chemical X and Y................................................................................................9

c) Final decision whether to buy or make famaQ......................................................................10

Conclusion.....................................................................................................................................11

References......................................................................................................................................12

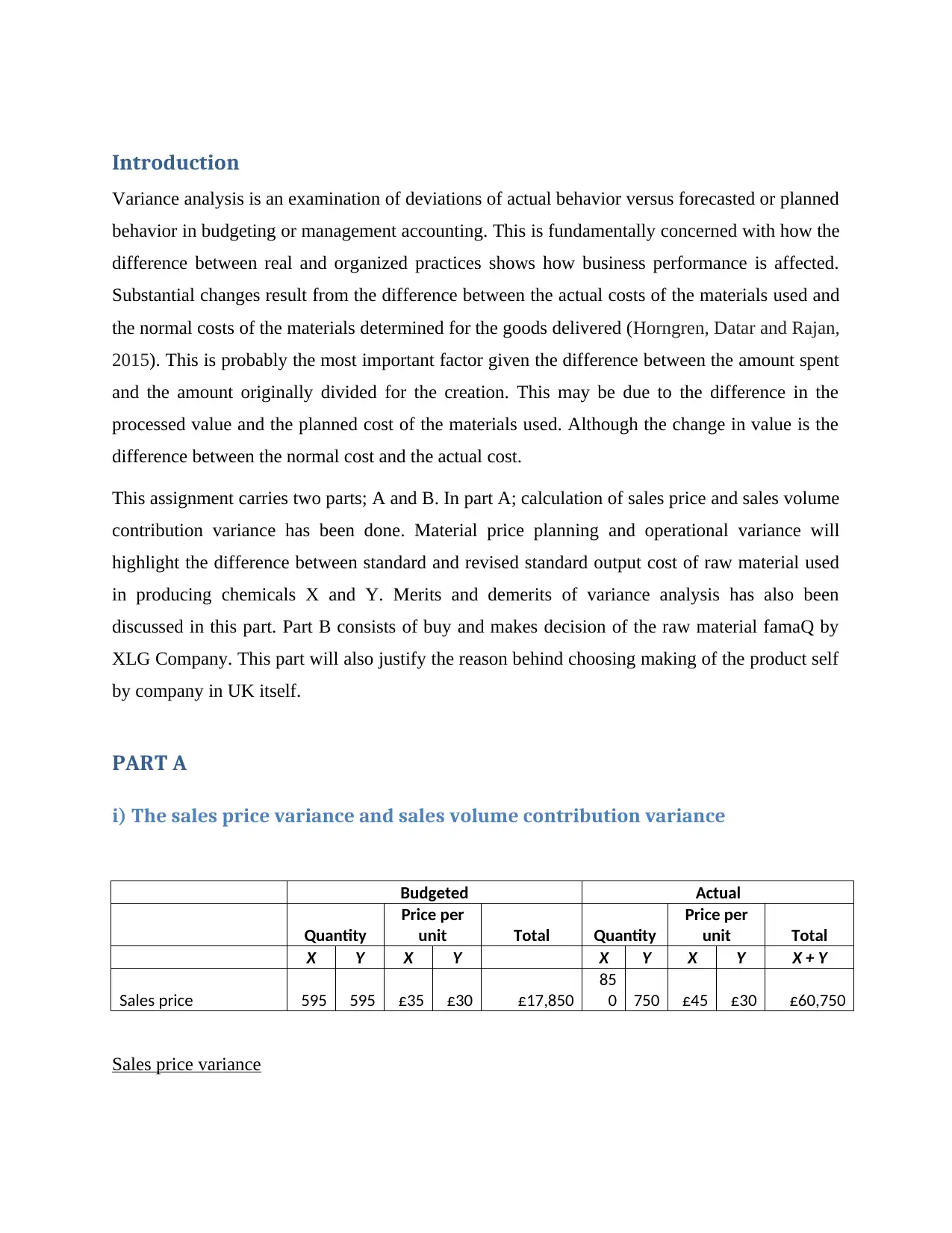

Introduction

Variance analysis is an examination of deviations of actual behavior versus forecasted or planned

behavior in budgeting or management accounting. This is fundamentally concerned with how the

difference between real and organized practices shows how business performance is affected.

Substantial changes result from the difference between the actual costs of the materials used and

the normal costs of the materials determined for the goods delivered (Horngren, Datar and Rajan,

2015). This is probably the most important factor given the difference between the amount spent

and the amount originally divided for the creation. This may be due to the difference in the

processed value and the planned cost of the materials used. Although the change in value is the

difference between the normal cost and the actual cost.

This assignment carries two parts; A and B. In part A; calculation of sales price and sales volume

contribution variance has been done. Material price planning and operational variance will

highlight the difference between standard and revised standard output cost of raw material used

in producing chemicals X and Y. Merits and demerits of variance analysis has also been

discussed in this part. Part B consists of buy and makes decision of the raw material famaQ by

XLG Company. This part will also justify the reason behind choosing making of the product self

by company in UK itself.

PART A

i) The sales price variance and sales volume contribution variance

Budgeted Actual

Quantity

Price per

unit Total Quantity

Price per

unit Total

X Y X Y X Y X Y X + Y

Sales price 595 595 £35 £30 £17,850

85

0 750 £45 £30 £60,750

Sales price variance

Variance analysis is an examination of deviations of actual behavior versus forecasted or planned

behavior in budgeting or management accounting. This is fundamentally concerned with how the

difference between real and organized practices shows how business performance is affected.

Substantial changes result from the difference between the actual costs of the materials used and

the normal costs of the materials determined for the goods delivered (Horngren, Datar and Rajan,

2015). This is probably the most important factor given the difference between the amount spent

and the amount originally divided for the creation. This may be due to the difference in the

processed value and the planned cost of the materials used. Although the change in value is the

difference between the normal cost and the actual cost.

This assignment carries two parts; A and B. In part A; calculation of sales price and sales volume

contribution variance has been done. Material price planning and operational variance will

highlight the difference between standard and revised standard output cost of raw material used

in producing chemicals X and Y. Merits and demerits of variance analysis has also been

discussed in this part. Part B consists of buy and makes decision of the raw material famaQ by

XLG Company. This part will also justify the reason behind choosing making of the product self

by company in UK itself.

PART A

i) The sales price variance and sales volume contribution variance

Budgeted Actual

Quantity

Price per

unit Total Quantity

Price per

unit Total

X Y X Y X Y X Y X + Y

Sales price 595 595 £35 £30 £17,850

85

0 750 £45 £30 £60,750

Sales price variance

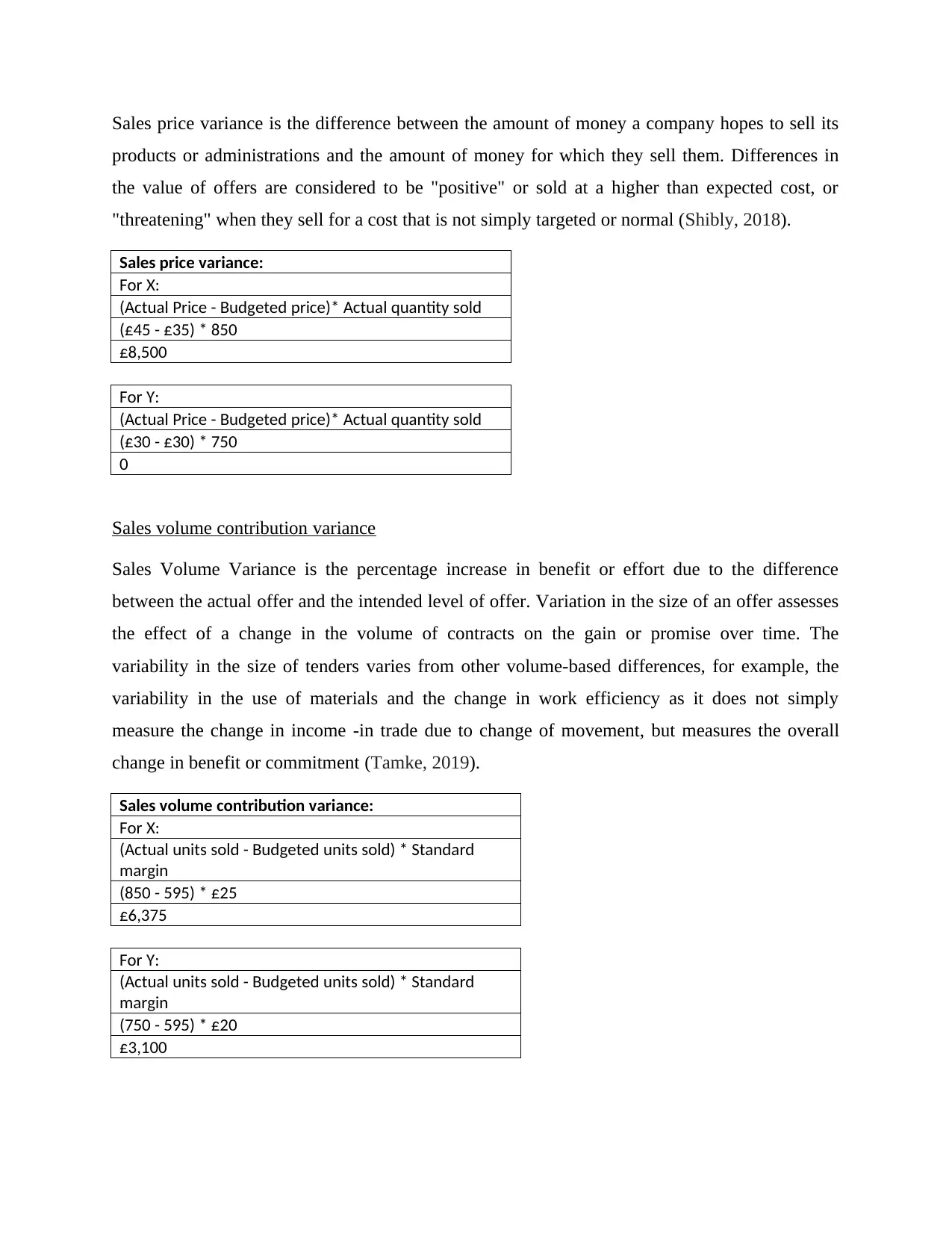

Sales price variance is the difference between the amount of money a company hopes to sell its

products or administrations and the amount of money for which they sell them. Differences in

the value of offers are considered to be "positive" or sold at a higher than expected cost, or

"threatening" when they sell for a cost that is not simply targeted or normal (Shibly, 2018).

Sales price variance:

For X:

(Actual Price - Budgeted price)* Actual quantity sold

(£45 - £35) * 850

£8,500

For Y:

(Actual Price - Budgeted price)* Actual quantity sold

(£30 - £30) * 750

0

Sales volume contribution variance

Sales Volume Variance is the percentage increase in benefit or effort due to the difference

between the actual offer and the intended level of offer. Variation in the size of an offer assesses

the effect of a change in the volume of contracts on the gain or promise over time. The

variability in the size of tenders varies from other volume-based differences, for example, the

variability in the use of materials and the change in work efficiency as it does not simply

measure the change in income -in trade due to change of movement, but measures the overall

change in benefit or commitment (Tamke, 2019).

Sales volume contribution variance:

For X:

(Actual units sold - Budgeted units sold) * Standard

margin

(850 - 595) * £25

£6,375

For Y:

(Actual units sold - Budgeted units sold) * Standard

margin

(750 - 595) * £20

£3,100

products or administrations and the amount of money for which they sell them. Differences in

the value of offers are considered to be "positive" or sold at a higher than expected cost, or

"threatening" when they sell for a cost that is not simply targeted or normal (Shibly, 2018).

Sales price variance:

For X:

(Actual Price - Budgeted price)* Actual quantity sold

(£45 - £35) * 850

£8,500

For Y:

(Actual Price - Budgeted price)* Actual quantity sold

(£30 - £30) * 750

0

Sales volume contribution variance

Sales Volume Variance is the percentage increase in benefit or effort due to the difference

between the actual offer and the intended level of offer. Variation in the size of an offer assesses

the effect of a change in the volume of contracts on the gain or promise over time. The

variability in the size of tenders varies from other volume-based differences, for example, the

variability in the use of materials and the change in work efficiency as it does not simply

measure the change in income -in trade due to change of movement, but measures the overall

change in benefit or commitment (Tamke, 2019).

Sales volume contribution variance:

For X:

(Actual units sold - Budgeted units sold) * Standard

margin

(850 - 595) * £25

£6,375

For Y:

(Actual units sold - Budgeted units sold) * Standard

margin

(750 - 595) * £20

£3,100

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

ii) The material price planning variance and material price operational

variance

Planning and operational analysis

For materials and labor, planning and operational variances can be determined by comparing

unprecedented and reconsidered (reconciled) spending plans with updated financial plans with

actual (operational) results. A material price planning variance is a very useful value proposition

to give you an idea of how talented leaders are in evaluating future costs. The operational

difference is more important because it measures the efficiency of a purchasing department with

the winning economic conditions in that period. Ignore the factors that cannot be avoided by

buying an office (Hout, 2017).

Planning variances seek to reflect the extent to which the initial level should be balanced to

reflect changes in working conditions between the current situation and those created when the

status was first determined, to fact means that the first level has been raised so far and so it is a

practical goal that can be achieved under the current conditions (Hout, 2017).

Operating variables reflect the extent to which achievable goals (i.e. fair guidelines) are

achieved. The job differences would be determined after the organizational changes have been

set and are therefore a reasonable way to achieve the finding.

The use of this approach challenges the notion that the current models are full of predictions that

there will not be enough work and that the organization supporting the predetermined guidance

was correct.

Material price planning variance = Original standard cost – Revised standard cost

= £2.50 - £4.50 = £2 Adverse

Material price operational variance = Revised standard cost – Cost actually paid

= £4.50 - £3.70 = £0.80 F

iii. Critically analyze the merits and demerits of using variances in assessing

managers performance

Variance Analysis

variance

Planning and operational analysis

For materials and labor, planning and operational variances can be determined by comparing

unprecedented and reconsidered (reconciled) spending plans with updated financial plans with

actual (operational) results. A material price planning variance is a very useful value proposition

to give you an idea of how talented leaders are in evaluating future costs. The operational

difference is more important because it measures the efficiency of a purchasing department with

the winning economic conditions in that period. Ignore the factors that cannot be avoided by

buying an office (Hout, 2017).

Planning variances seek to reflect the extent to which the initial level should be balanced to

reflect changes in working conditions between the current situation and those created when the

status was first determined, to fact means that the first level has been raised so far and so it is a

practical goal that can be achieved under the current conditions (Hout, 2017).

Operating variables reflect the extent to which achievable goals (i.e. fair guidelines) are

achieved. The job differences would be determined after the organizational changes have been

set and are therefore a reasonable way to achieve the finding.

The use of this approach challenges the notion that the current models are full of predictions that

there will not be enough work and that the organization supporting the predetermined guidance

was correct.

Material price planning variance = Original standard cost – Revised standard cost

= £2.50 - £4.50 = £2 Adverse

Material price operational variance = Revised standard cost – Cost actually paid

= £4.50 - £3.70 = £0.80 F

iii. Critically analyze the merits and demerits of using variances in assessing

managers performance

Variance Analysis

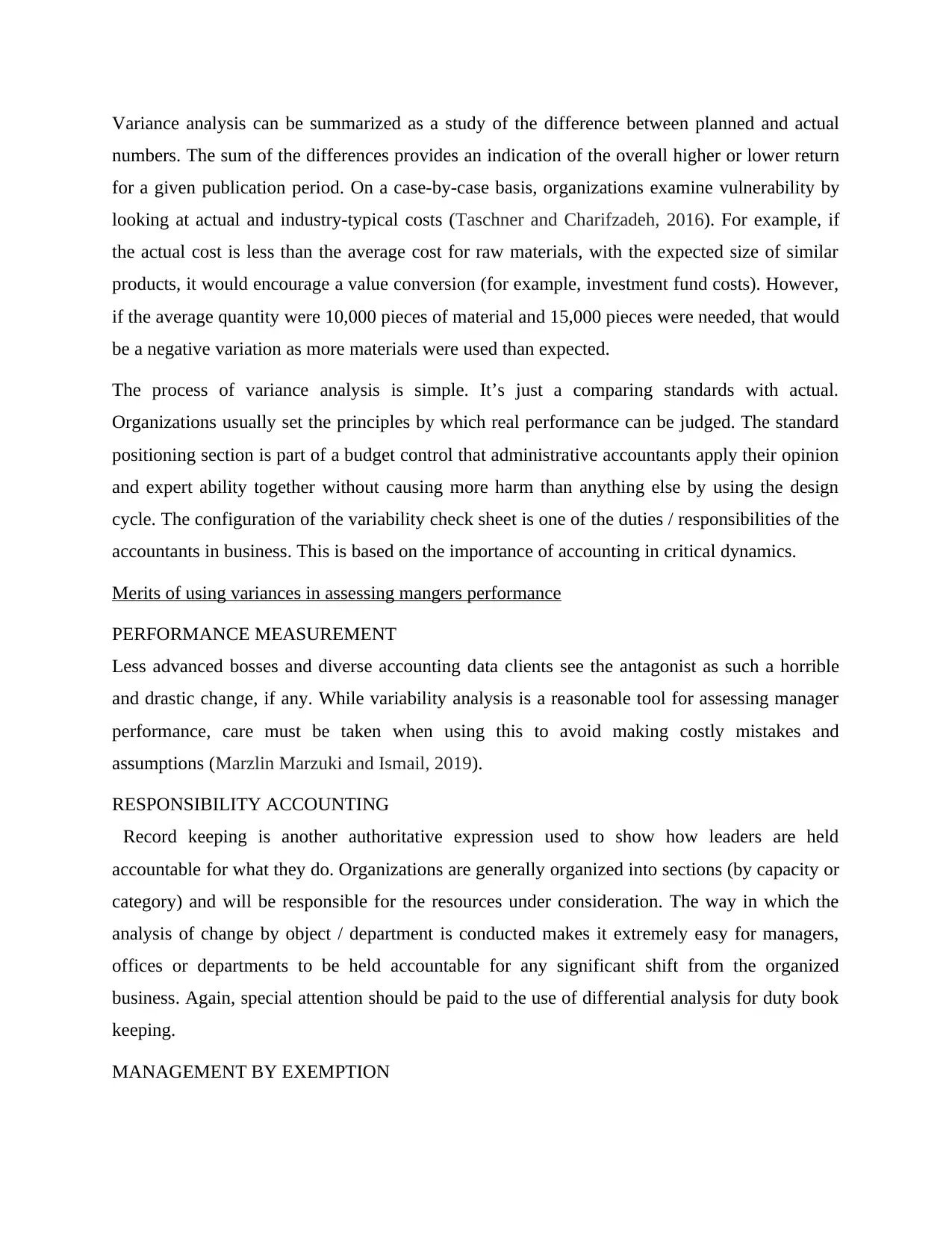

Variance analysis can be summarized as a study of the difference between planned and actual

numbers. The sum of the differences provides an indication of the overall higher or lower return

for a given publication period. On a case-by-case basis, organizations examine vulnerability by

looking at actual and industry-typical costs (Taschner and Charifzadeh, 2016). For example, if

the actual cost is less than the average cost for raw materials, with the expected size of similar

products, it would encourage a value conversion (for example, investment fund costs). However,

if the average quantity were 10,000 pieces of material and 15,000 pieces were needed, that would

be a negative variation as more materials were used than expected.

The process of variance analysis is simple. It’s just a comparing standards with actual.

Organizations usually set the principles by which real performance can be judged. The standard

positioning section is part of a budget control that administrative accountants apply their opinion

and expert ability together without causing more harm than anything else by using the design

cycle. The configuration of the variability check sheet is one of the duties / responsibilities of the

accountants in business. This is based on the importance of accounting in critical dynamics.

Merits of using variances in assessing mangers performance

PERFORMANCE MEASUREMENT

Less advanced bosses and diverse accounting data clients see the antagonist as such a horrible

and drastic change, if any. While variability analysis is a reasonable tool for assessing manager

performance, care must be taken when using this to avoid making costly mistakes and

assumptions (Marzlin Marzuki and Ismail, 2019).

RESPONSIBILITY ACCOUNTING

Record keeping is another authoritative expression used to show how leaders are held

accountable for what they do. Organizations are generally organized into sections (by capacity or

category) and will be responsible for the resources under consideration. The way in which the

analysis of change by object / department is conducted makes it extremely easy for managers,

offices or departments to be held accountable for any significant shift from the organized

business. Again, special attention should be paid to the use of differential analysis for duty book

keeping.

MANAGEMENT BY EXEMPTION

numbers. The sum of the differences provides an indication of the overall higher or lower return

for a given publication period. On a case-by-case basis, organizations examine vulnerability by

looking at actual and industry-typical costs (Taschner and Charifzadeh, 2016). For example, if

the actual cost is less than the average cost for raw materials, with the expected size of similar

products, it would encourage a value conversion (for example, investment fund costs). However,

if the average quantity were 10,000 pieces of material and 15,000 pieces were needed, that would

be a negative variation as more materials were used than expected.

The process of variance analysis is simple. It’s just a comparing standards with actual.

Organizations usually set the principles by which real performance can be judged. The standard

positioning section is part of a budget control that administrative accountants apply their opinion

and expert ability together without causing more harm than anything else by using the design

cycle. The configuration of the variability check sheet is one of the duties / responsibilities of the

accountants in business. This is based on the importance of accounting in critical dynamics.

Merits of using variances in assessing mangers performance

PERFORMANCE MEASUREMENT

Less advanced bosses and diverse accounting data clients see the antagonist as such a horrible

and drastic change, if any. While variability analysis is a reasonable tool for assessing manager

performance, care must be taken when using this to avoid making costly mistakes and

assumptions (Marzlin Marzuki and Ismail, 2019).

RESPONSIBILITY ACCOUNTING

Record keeping is another authoritative expression used to show how leaders are held

accountable for what they do. Organizations are generally organized into sections (by capacity or

category) and will be responsible for the resources under consideration. The way in which the

analysis of change by object / department is conducted makes it extremely easy for managers,

offices or departments to be held accountable for any significant shift from the organized

business. Again, special attention should be paid to the use of differential analysis for duty book

keeping.

MANAGEMENT BY EXEMPTION

A significant or significant variability calls the administrations to consider areas in which the

organized exercises do not coincide with the actual results.

INDICATE DEPARTURE

The first favorable scenario of differentiation or variance tests is a sign of deviation from the

norm or expectation. This acceptance is subject to test consideration. The board is very confident

about this flight, especially for taking off or changing variability (the cost is higher than

expected).

CONTROLLING EXPENDITURE

The second room for shifting variables is its role in controlling consumption. The board makes

appropriate disciplinary action in the event of hostile discrimination. In the leadership situation,

clarification of hostile change is investigated, if appropriate clarification is not offered, and then

an appropriate control move is made (Marzlin Marzuki and Ismail, 2019).

ADJUST BUDGET ESTIMATES

The third part of the room for the movement of the variability or variance tests is the change of

future cost indicators. When there is no appropriate explanation behind a change but the wrong

consumption signal, the planned signal for the future is balanced or adjusted.

EVALUATE PERFORMANCE

The fourth favorable setting of the variability or variability tests to evaluate the performance of

the individual and in particular the control controller. A large difference is characterized by a

large office run or depression, while an unfavorable change is a sign of poor vision.

ROLES & RESPONSIBILITY

A fifth benefit of the study of variability or variability is the definition of a configuration of

functions and responsibilities within the association. As a result of the definition of jobs and

activities, productivity and controls within society improve.

ACCOUNTABILITY

Variance calculation or variables establish an agreement of liability within the association.

Everyone is responsible for the results of antagonistic differences (the cost of materials or labor

is greater than expected).

Demerits of using variances in assessing mangers performance

organized exercises do not coincide with the actual results.

INDICATE DEPARTURE

The first favorable scenario of differentiation or variance tests is a sign of deviation from the

norm or expectation. This acceptance is subject to test consideration. The board is very confident

about this flight, especially for taking off or changing variability (the cost is higher than

expected).

CONTROLLING EXPENDITURE

The second room for shifting variables is its role in controlling consumption. The board makes

appropriate disciplinary action in the event of hostile discrimination. In the leadership situation,

clarification of hostile change is investigated, if appropriate clarification is not offered, and then

an appropriate control move is made (Marzlin Marzuki and Ismail, 2019).

ADJUST BUDGET ESTIMATES

The third part of the room for the movement of the variability or variance tests is the change of

future cost indicators. When there is no appropriate explanation behind a change but the wrong

consumption signal, the planned signal for the future is balanced or adjusted.

EVALUATE PERFORMANCE

The fourth favorable setting of the variability or variability tests to evaluate the performance of

the individual and in particular the control controller. A large difference is characterized by a

large office run or depression, while an unfavorable change is a sign of poor vision.

ROLES & RESPONSIBILITY

A fifth benefit of the study of variability or variability is the definition of a configuration of

functions and responsibilities within the association. As a result of the definition of jobs and

activities, productivity and controls within society improve.

ACCOUNTABILITY

Variance calculation or variables establish an agreement of liability within the association.

Everyone is responsible for the results of antagonistic differences (the cost of materials or labor

is greater than expected).

Demerits of using variances in assessing mangers performance

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

NON STANDARDIZED PRODUCTION

General Costs are generally applicable to organizations involved in the production of standard

materials under large-scale production conditions. There are problems where the cost of creating

printed records of small items of material is regularly reduced due to the lack of validation

criteria for existing new products. While it is possible to create new routines for each new

custom article browser, the amount of time it takes to handle the entire cycle for articles with

such a short lifecycle may not make it accessible fundamentally (Marzlin Marzuki and Ismail,

2019).

SERVICE ORGANIZATIONS

It is more difficult to apply a standard cost and variability analysis to support sub-companies

because much of their cost is included with respect to creation costs (eg direct labor cost,

material cost only, and so on). Although routine cost variance analysis of regular costs may not

provide very useful data for over-control purposes, the use of more conventional methods of

addressing conventional costs (e.g. the use of action-based costs) may provide a useful basis for

the analysis of variance on administrative costs in the field of association administration,

however, can require a significant amount of time and interest to implement an appropriate

administrative data framework for the transport of such data.

ASSIGNING RESPONSIBILITIES

Responsible accounting is a great potential for routine cost and difference analysis. Changes can

arise for a number of reasons ranging from rusty directions (e.g. neglecting to consider a normal

increase in wage rates) to operational reasons (e.g. an increase in material use just as a result of

hiring more talented workers). Defining deficiencies that can cause significant changes due to

faulty routines can be managed by carefully implementing changes and operational changes. It

may be more difficult, at least, to uncover the exact causes and assign operational variability

tasks to a particular person, office, or skill within a company. It could at least be argued that,

despite the fact that the reasons and responsibilities for variables may be obscured from time to

time; a study of change provides a basis for control, which could lead to a better understanding

of the operational situation among membership administrations (Marzlin Marzuki and Ismail,

2019).

General Costs are generally applicable to organizations involved in the production of standard

materials under large-scale production conditions. There are problems where the cost of creating

printed records of small items of material is regularly reduced due to the lack of validation

criteria for existing new products. While it is possible to create new routines for each new

custom article browser, the amount of time it takes to handle the entire cycle for articles with

such a short lifecycle may not make it accessible fundamentally (Marzlin Marzuki and Ismail,

2019).

SERVICE ORGANIZATIONS

It is more difficult to apply a standard cost and variability analysis to support sub-companies

because much of their cost is included with respect to creation costs (eg direct labor cost,

material cost only, and so on). Although routine cost variance analysis of regular costs may not

provide very useful data for over-control purposes, the use of more conventional methods of

addressing conventional costs (e.g. the use of action-based costs) may provide a useful basis for

the analysis of variance on administrative costs in the field of association administration,

however, can require a significant amount of time and interest to implement an appropriate

administrative data framework for the transport of such data.

ASSIGNING RESPONSIBILITIES

Responsible accounting is a great potential for routine cost and difference analysis. Changes can

arise for a number of reasons ranging from rusty directions (e.g. neglecting to consider a normal

increase in wage rates) to operational reasons (e.g. an increase in material use just as a result of

hiring more talented workers). Defining deficiencies that can cause significant changes due to

faulty routines can be managed by carefully implementing changes and operational changes. It

may be more difficult, at least, to uncover the exact causes and assign operational variability

tasks to a particular person, office, or skill within a company. It could at least be argued that,

despite the fact that the reasons and responsibilities for variables may be obscured from time to

time; a study of change provides a basis for control, which could lead to a better understanding

of the operational situation among membership administrations (Marzlin Marzuki and Ismail,

2019).

PART B

a) FamaQ gives XLG competitive advantage

Competitive advantage refers to factors that allow an organization to create products or

administrations that are better or much cheaper than its opponents. These variables allow the

profit element to achieve more business or better margins than its market competitors. At the

opportunity that an organization could not use economies of scale and extract items at a lower

cost than its competitors, the organization is then ready to build sales value that cannot be

duplicated by different organizations. As a result, an organization that adopts a cost authority

system would be able to recoup the benefits of its cost advantage over its competitors. Benefit

recognizes an organization from its competitors. It contributes to higher spending, more

customers, and brand stability. One of the most important goals of any organization is to

establish such a path (Jiambalvo, 2019).

One of the competitive advantages given by FamaQ is having capacity of superior cleaning agent

and another benefit is no competitor can manufacture cleaning agent by using famaQ material

due to patent rights hold by XLG. Through this company can only manufacture cleaning

products using famaQ which is very much effective in terms of results. This gives XLG a

competitive advantage over other firms in the market.

b) Demand for chemical X and Y

In this COVID-19 pandemic outbreak; demand for chemical X and Y has been increased by

45%. It is also researched that demand for both of these chemicals will be stable over long period

of time. X and Y chemicals required 1 unit of raw material named famaQ; hence demand for

famaQ will also simultaneously increased by 45%. Hence, company could be stable in this

business for more than year and it could also take risk to manufacture the raw material famaQ

which it earlier acquired from Brazil @ £2.50 per unit.

a) FamaQ gives XLG competitive advantage

Competitive advantage refers to factors that allow an organization to create products or

administrations that are better or much cheaper than its opponents. These variables allow the

profit element to achieve more business or better margins than its market competitors. At the

opportunity that an organization could not use economies of scale and extract items at a lower

cost than its competitors, the organization is then ready to build sales value that cannot be

duplicated by different organizations. As a result, an organization that adopts a cost authority

system would be able to recoup the benefits of its cost advantage over its competitors. Benefit

recognizes an organization from its competitors. It contributes to higher spending, more

customers, and brand stability. One of the most important goals of any organization is to

establish such a path (Jiambalvo, 2019).

One of the competitive advantages given by FamaQ is having capacity of superior cleaning agent

and another benefit is no competitor can manufacture cleaning agent by using famaQ material

due to patent rights hold by XLG. Through this company can only manufacture cleaning

products using famaQ which is very much effective in terms of results. This gives XLG a

competitive advantage over other firms in the market.

b) Demand for chemical X and Y

In this COVID-19 pandemic outbreak; demand for chemical X and Y has been increased by

45%. It is also researched that demand for both of these chemicals will be stable over long period

of time. X and Y chemicals required 1 unit of raw material named famaQ; hence demand for

famaQ will also simultaneously increased by 45%. Hence, company could be stable in this

business for more than year and it could also take risk to manufacture the raw material famaQ

which it earlier acquired from Brazil @ £2.50 per unit.

c) Final decision whether to buy or make famaQ

Make or buy decisions:

The make or buy decision refers to the problem that an association feels when choosing whether

to purchase or manage an item or administration from outside sources. Amazingly, everything

that is currently purchased from an external supplier is constantly competing for inbound

production and everything is as it is now making the inside of the house a valid refueling

opportunity (Datar and Rajan, 2018).

Most make or buy decisions are made on the basis of price. However, this is only one of the

models, to be evaluated in this crucial choice. A number of non-cost factors support long-range

contracts with suppliers to help meet creativity and quality standards and enhance interests in

responding to innovative resources and ideas (Datar and Rajan, 2018).

To reach at some conclusion, cost analysis has been done below:

The cost of manufacturing the product is £3 per unit while if it is ordered from Brazil than actual

paid cost is £3.70 per unit (during lockdown). But if there’s no lockdown and no barrier on trade

through ship than the actual paid cost will be £2.50 per unit at reduced demand. Based on market

research; it is assumed that lockdown will be stay for longer period of time. Thus, cost of

importing famaQ has been calculated below:

Total cost = Total units * Cost per unit

= 1,600 * £3.70 = £5,920

Total cost bear by XLG if units are produced at UK:

Total cost of manufacturing = Total units sold * Cost per unit

= 1,600 * £3 = £4,800

Hence, overall cost is lesser than importing cost of femaQ by £1,120; if company has sales

around 1,600 units. It is clear that XLG could save up to £0.70 on each unit, if it decides to self

manufacturing the units.

Make or buy decisions:

The make or buy decision refers to the problem that an association feels when choosing whether

to purchase or manage an item or administration from outside sources. Amazingly, everything

that is currently purchased from an external supplier is constantly competing for inbound

production and everything is as it is now making the inside of the house a valid refueling

opportunity (Datar and Rajan, 2018).

Most make or buy decisions are made on the basis of price. However, this is only one of the

models, to be evaluated in this crucial choice. A number of non-cost factors support long-range

contracts with suppliers to help meet creativity and quality standards and enhance interests in

responding to innovative resources and ideas (Datar and Rajan, 2018).

To reach at some conclusion, cost analysis has been done below:

The cost of manufacturing the product is £3 per unit while if it is ordered from Brazil than actual

paid cost is £3.70 per unit (during lockdown). But if there’s no lockdown and no barrier on trade

through ship than the actual paid cost will be £2.50 per unit at reduced demand. Based on market

research; it is assumed that lockdown will be stay for longer period of time. Thus, cost of

importing famaQ has been calculated below:

Total cost = Total units * Cost per unit

= 1,600 * £3.70 = £5,920

Total cost bear by XLG if units are produced at UK:

Total cost of manufacturing = Total units sold * Cost per unit

= 1,600 * £3 = £4,800

Hence, overall cost is lesser than importing cost of femaQ by £1,120; if company has sales

around 1,600 units. It is clear that XLG could save up to £0.70 on each unit, if it decides to self

manufacturing the units.

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

Additional to this; company has another advantage, which is delivery time reduced by 15 days.

This will help XLG in reducing holding cost of inventories at warehouse and also support in

fulfilling demands on time without any risk of delay in delivery (Demski and Kreps, 1982).

Recommendation

After analyzing all facts and calculations; it is recommended that XLG should go for

manufacturing product itself; as company has an opportunity to meet increase demand and the

difference between import and manufacturing cost will increase the profit of company by £0.70

at each unit of cleansing agent sold in market (Demski and Kreps, 1982).

Conclusion

After evaluation of all aspects of given assignment; it can be concluded that COVID-19 has raise

the opportunity for the company to choose to build the product itself and reduce the price

variance through minimizing the cost of production.

This will help XLG in reducing holding cost of inventories at warehouse and also support in

fulfilling demands on time without any risk of delay in delivery (Demski and Kreps, 1982).

Recommendation

After analyzing all facts and calculations; it is recommended that XLG should go for

manufacturing product itself; as company has an opportunity to meet increase demand and the

difference between import and manufacturing cost will increase the profit of company by £0.70

at each unit of cleansing agent sold in market (Demski and Kreps, 1982).

Conclusion

After evaluation of all aspects of given assignment; it can be concluded that COVID-19 has raise

the opportunity for the company to choose to build the product itself and reduce the price

variance through minimizing the cost of production.

References

Datar, S.M. and Rajan, M., 2018. Horngren's cost accounting: A managerial emphasis.

Demski, J.S. and Kreps, D.M., 1982. Models in managerial accounting. Journal of Accounting

Research, pp.117-148.

Horngren, C.T., Datar, S.M. and Rajan, M.V., 2015. Cost accounting: A managerial emphasis.

Hout, B., 2017. Cost accounting approaches: The lean success. SAGE Publications: SAGE

Business Cases Originals.

Jiambalvo, J., 2019. Managerial accounting. John Wiley & Sons.

Marzlin Marzuki, N.A.R. and Ismail, J., 2019. Benefits and limitations of variance analysis in

management accounting. ACCOUNTING BULLETIN, p.15.

Shibly, F.B., 2018. Advanced Managerial Accounting.

Tamke, W., 2019. ACCT 215-003: Managerial Accounting.

Taschner, A. and Charifzadeh, M., 2016. Management and Cost Accounting. John Wiley &

Sons.

Datar, S.M. and Rajan, M., 2018. Horngren's cost accounting: A managerial emphasis.

Demski, J.S. and Kreps, D.M., 1982. Models in managerial accounting. Journal of Accounting

Research, pp.117-148.

Horngren, C.T., Datar, S.M. and Rajan, M.V., 2015. Cost accounting: A managerial emphasis.

Hout, B., 2017. Cost accounting approaches: The lean success. SAGE Publications: SAGE

Business Cases Originals.

Jiambalvo, J., 2019. Managerial accounting. John Wiley & Sons.

Marzlin Marzuki, N.A.R. and Ismail, J., 2019. Benefits and limitations of variance analysis in

management accounting. ACCOUNTING BULLETIN, p.15.

Shibly, F.B., 2018. Advanced Managerial Accounting.

Tamke, W., 2019. ACCT 215-003: Managerial Accounting.

Taschner, A. and Charifzadeh, M., 2016. Management and Cost Accounting. John Wiley &

Sons.

1 out of 12

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

© 2024 | Zucol Services PVT LTD | All rights reserved.