Variance Analysis in Management Accounting

Added on 2023-01-07

12 Pages3140 Words31 Views

Management Accounting-2

Table of Contents

Introduction......................................................................................................................................3

PART A...........................................................................................................................................3

i) The sales price variance and sales volume contribution variance............................................3

ii) The material price planning variance and material price operational variance.......................5

iii. Critically analyze the merits and demerits of using variances in assessing managers

performance.................................................................................................................................5

PART B...........................................................................................................................................9

a) FamaQ gives XLG competitive advantage..............................................................................9

b) Demand for chemical X and Y................................................................................................9

c) Final decision whether to buy or make famaQ......................................................................10

Conclusion.....................................................................................................................................11

References......................................................................................................................................12

Introduction......................................................................................................................................3

PART A...........................................................................................................................................3

i) The sales price variance and sales volume contribution variance............................................3

ii) The material price planning variance and material price operational variance.......................5

iii. Critically analyze the merits and demerits of using variances in assessing managers

performance.................................................................................................................................5

PART B...........................................................................................................................................9

a) FamaQ gives XLG competitive advantage..............................................................................9

b) Demand for chemical X and Y................................................................................................9

c) Final decision whether to buy or make famaQ......................................................................10

Conclusion.....................................................................................................................................11

References......................................................................................................................................12

Introduction

Variance analysis is an examination of deviations of actual behavior versus forecasted or planned

behavior in budgeting or management accounting. This is fundamentally concerned with how the

difference between real and organized practices shows how business performance is affected.

Substantial changes result from the difference between the actual costs of the materials used and

the normal costs of the materials determined for the goods delivered (Horngren, Datar and Rajan,

2015). This is probably the most important factor given the difference between the amount spent

and the amount originally divided for the creation. This may be due to the difference in the

processed value and the planned cost of the materials used. Although the change in value is the

difference between the normal cost and the actual cost.

This assignment carries two parts; A and B. In part A; calculation of sales price and sales volume

contribution variance has been done. Material price planning and operational variance will

highlight the difference between standard and revised standard output cost of raw material used

in producing chemicals X and Y. Merits and demerits of variance analysis has also been

discussed in this part. Part B consists of buy and makes decision of the raw material famaQ by

XLG Company. This part will also justify the reason behind choosing making of the product self

by company in UK itself.

PART A

i) The sales price variance and sales volume contribution variance

Budgeted Actual

Quantity

Price per

unit Total Quantity

Price per

unit Total

X Y X Y X Y X Y X + Y

Sales price 595 595 £35 £30 £17,850

85

0 750 £45 £30 £60,750

Sales price variance

Variance analysis is an examination of deviations of actual behavior versus forecasted or planned

behavior in budgeting or management accounting. This is fundamentally concerned with how the

difference between real and organized practices shows how business performance is affected.

Substantial changes result from the difference between the actual costs of the materials used and

the normal costs of the materials determined for the goods delivered (Horngren, Datar and Rajan,

2015). This is probably the most important factor given the difference between the amount spent

and the amount originally divided for the creation. This may be due to the difference in the

processed value and the planned cost of the materials used. Although the change in value is the

difference between the normal cost and the actual cost.

This assignment carries two parts; A and B. In part A; calculation of sales price and sales volume

contribution variance has been done. Material price planning and operational variance will

highlight the difference between standard and revised standard output cost of raw material used

in producing chemicals X and Y. Merits and demerits of variance analysis has also been

discussed in this part. Part B consists of buy and makes decision of the raw material famaQ by

XLG Company. This part will also justify the reason behind choosing making of the product self

by company in UK itself.

PART A

i) The sales price variance and sales volume contribution variance

Budgeted Actual

Quantity

Price per

unit Total Quantity

Price per

unit Total

X Y X Y X Y X Y X + Y

Sales price 595 595 £35 £30 £17,850

85

0 750 £45 £30 £60,750

Sales price variance

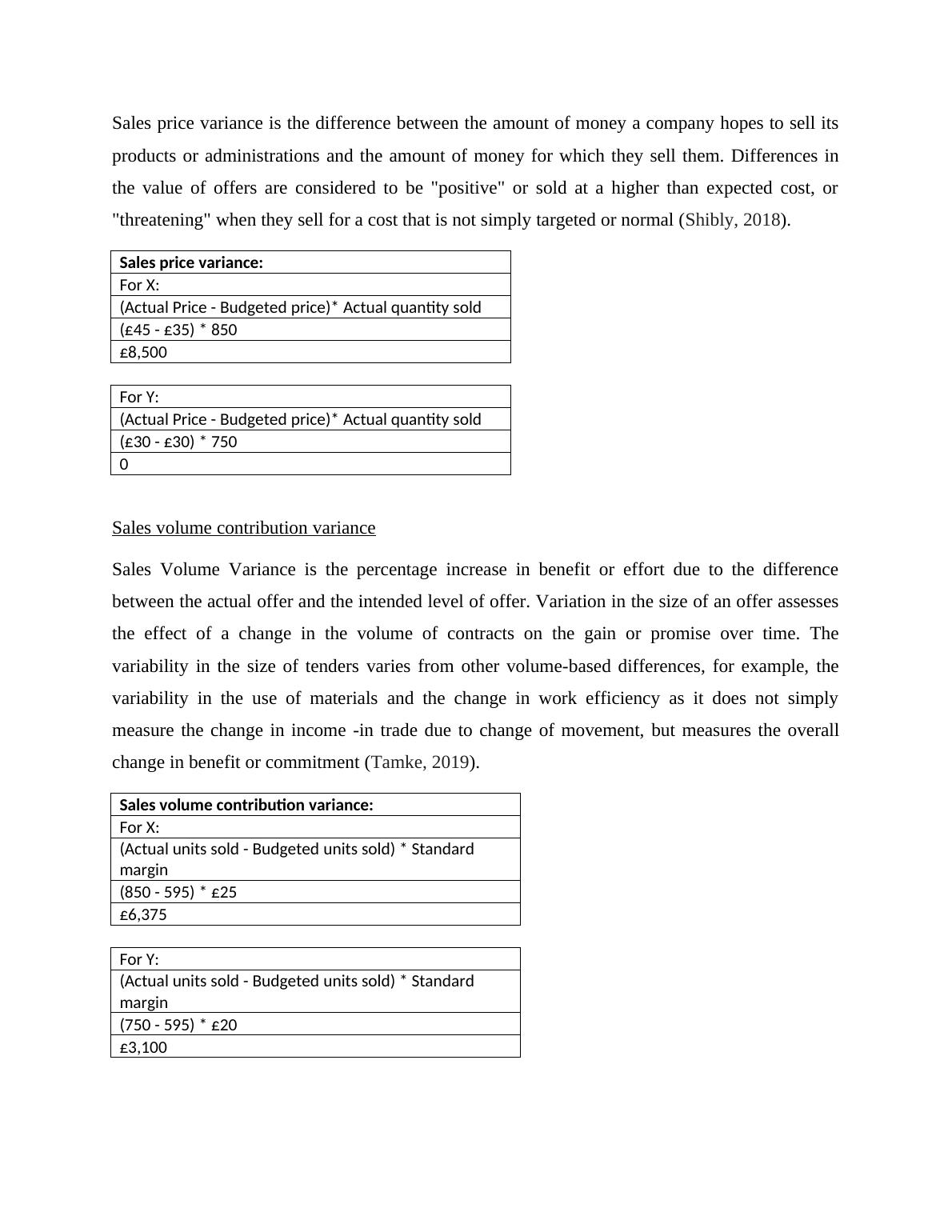

Sales price variance is the difference between the amount of money a company hopes to sell its

products or administrations and the amount of money for which they sell them. Differences in

the value of offers are considered to be "positive" or sold at a higher than expected cost, or

"threatening" when they sell for a cost that is not simply targeted or normal (Shibly, 2018).

Sales price variance:

For X:

(Actual Price - Budgeted price)* Actual quantity sold

(£45 - £35) * 850

£8,500

For Y:

(Actual Price - Budgeted price)* Actual quantity sold

(£30 - £30) * 750

0

Sales volume contribution variance

Sales Volume Variance is the percentage increase in benefit or effort due to the difference

between the actual offer and the intended level of offer. Variation in the size of an offer assesses

the effect of a change in the volume of contracts on the gain or promise over time. The

variability in the size of tenders varies from other volume-based differences, for example, the

variability in the use of materials and the change in work efficiency as it does not simply

measure the change in income -in trade due to change of movement, but measures the overall

change in benefit or commitment (Tamke, 2019).

Sales volume contribution variance:

For X:

(Actual units sold - Budgeted units sold) * Standard

margin

(850 - 595) * £25

£6,375

For Y:

(Actual units sold - Budgeted units sold) * Standard

margin

(750 - 595) * £20

£3,100

products or administrations and the amount of money for which they sell them. Differences in

the value of offers are considered to be "positive" or sold at a higher than expected cost, or

"threatening" when they sell for a cost that is not simply targeted or normal (Shibly, 2018).

Sales price variance:

For X:

(Actual Price - Budgeted price)* Actual quantity sold

(£45 - £35) * 850

£8,500

For Y:

(Actual Price - Budgeted price)* Actual quantity sold

(£30 - £30) * 750

0

Sales volume contribution variance

Sales Volume Variance is the percentage increase in benefit or effort due to the difference

between the actual offer and the intended level of offer. Variation in the size of an offer assesses

the effect of a change in the volume of contracts on the gain or promise over time. The

variability in the size of tenders varies from other volume-based differences, for example, the

variability in the use of materials and the change in work efficiency as it does not simply

measure the change in income -in trade due to change of movement, but measures the overall

change in benefit or commitment (Tamke, 2019).

Sales volume contribution variance:

For X:

(Actual units sold - Budgeted units sold) * Standard

margin

(850 - 595) * £25

£6,375

For Y:

(Actual units sold - Budgeted units sold) * Standard

margin

(750 - 595) * £20

£3,100

End of preview

Want to access all the pages? Upload your documents or become a member.

Related Documents

Management Accounting: Sales Variance, Material Variance, and Performance Evaluationlg...

|14

|3460

|98

MANAGEMENT ACCOUNTING - REPORTlg...

|12

|3134

|71

Variance in Assessing Performance and Decision Makinglg...

|15

|3344

|66

Management Accounting: Sales Price Variance, Material Price Variance, and Performance Evaluationlg...

|15

|3285

|47

Variance Analysis for Assessing Manager Performance in Management Accountinglg...

|11

|3061

|98

Variance Analysis in Management Accountinglg...

|12

|3302

|69