Management Accounting Research and Practice

VerifiedAdded on 2020/06/06

|15

|4530

|49

AI Summary

This assignment delves into the world of management accounting research, examining various perspectives and contributions. It analyzes influential theories like contingency theory and explores topics such as cost management, sustainability reporting, and the impact of industry context on accounting practices. The assignment also considers the evolving role of management accounting in a dynamic business environment.

Contribute Materials

Your contribution can guide someone’s learning journey. Share your

documents today.

MANAGEMENT

ACCOUNTING

ACCOUNTING

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

Table of Contents

INTRODUCTION...........................................................................................................................1

SECTION I......................................................................................................................................1

LO 1.................................................................................................................................................1

P1 Importance of management accounting in the decision making process\.........................1

P2 Different types of management accounting systems.........................................................3

LO 2.................................................................................................................................................4

P3 Use of absorption and variable costing techniques in management accounting...............4

SECTION II.....................................................................................................................................7

LO 3.................................................................................................................................................7

P4 Advantages and disadvantages of different types of planning tools adopted for budgetary

control in Nero Ltd.................................................................................................................7

LO 4.................................................................................................................................................9

P5 Adaptation of management accounting systems to respond to financial problems..........9

CONCLUSION..............................................................................................................................11

REFERENCES..............................................................................................................................12

INTRODUCTION...........................................................................................................................1

SECTION I......................................................................................................................................1

LO 1.................................................................................................................................................1

P1 Importance of management accounting in the decision making process\.........................1

P2 Different types of management accounting systems.........................................................3

LO 2.................................................................................................................................................4

P3 Use of absorption and variable costing techniques in management accounting...............4

SECTION II.....................................................................................................................................7

LO 3.................................................................................................................................................7

P4 Advantages and disadvantages of different types of planning tools adopted for budgetary

control in Nero Ltd.................................................................................................................7

LO 4.................................................................................................................................................9

P5 Adaptation of management accounting systems to respond to financial problems..........9

CONCLUSION..............................................................................................................................11

REFERENCES..............................................................................................................................12

INTRODUCTION

The management accounting standards ensures the management team of an organisation

to undertake an effective decision making process in order to achieve well desired goals as well

as objectives of that venture. It assists an entity in its decision making process by providing that

firm with relevant financial as well as cost accounting details, which gives a clear picture of the

working of an organisation and identify the loopholes that are prevailing in the firm and thus,

leading to desired changes to overcome the same. The management accounting system enables

the mangers appointed in a venture to determine the availability as well as requirement of

various resources required to undertake the operational activities in that firm. Management

accounting keeps a record of sales made, the revenue generated, purchases made, profits earned,

the efficiencies improved, etc. , which are important to analyse as per the view point of

management.

SECTION I

LO 1

P1 Importance of management accounting in the decision making process\

The management accounting standards adopted enables the managers of an organisation

to determine decisions regarding the day to day functional activities of that venture. The small

business organisation taken into the report is Alara Wholefoods Ltd. The management

accounting standards adopted in present organisation assists the managers with its numerous day

to day functional activities, that they need to perform in the context of managing a business

(Schaltegger and Burritt, 2017). The benefits of various information that is collected by

undertaking effective management accounting system are listed as well as explained in detail as

under: Cost analysis: An effective management accounting records initiated in the cited

organisation enables the appointed managers to analyse the cost of input inculcated in

order to generate desired outputs. This cost analysis ensures the managers or leaders to

determine the price to be charged for the products that are being offered to customers, as

per the cost incurred, in order to generate efficient results or profits. Thus, management

accounting standards enables to analyse cost of manufacturing the products and thus,

undertake an important decision making mechanism regarding its prices to be charged.

1

The management accounting standards ensures the management team of an organisation

to undertake an effective decision making process in order to achieve well desired goals as well

as objectives of that venture. It assists an entity in its decision making process by providing that

firm with relevant financial as well as cost accounting details, which gives a clear picture of the

working of an organisation and identify the loopholes that are prevailing in the firm and thus,

leading to desired changes to overcome the same. The management accounting system enables

the mangers appointed in a venture to determine the availability as well as requirement of

various resources required to undertake the operational activities in that firm. Management

accounting keeps a record of sales made, the revenue generated, purchases made, profits earned,

the efficiencies improved, etc. , which are important to analyse as per the view point of

management.

SECTION I

LO 1

P1 Importance of management accounting in the decision making process\

The management accounting standards adopted enables the managers of an organisation

to determine decisions regarding the day to day functional activities of that venture. The small

business organisation taken into the report is Alara Wholefoods Ltd. The management

accounting standards adopted in present organisation assists the managers with its numerous day

to day functional activities, that they need to perform in the context of managing a business

(Schaltegger and Burritt, 2017). The benefits of various information that is collected by

undertaking effective management accounting system are listed as well as explained in detail as

under: Cost analysis: An effective management accounting records initiated in the cited

organisation enables the appointed managers to analyse the cost of input inculcated in

order to generate desired outputs. This cost analysis ensures the managers or leaders to

determine the price to be charged for the products that are being offered to customers, as

per the cost incurred, in order to generate efficient results or profits. Thus, management

accounting standards enables to analyse cost of manufacturing the products and thus,

undertake an important decision making mechanism regarding its prices to be charged.

1

Determining target market: The determination of target audience is of utmost

importance for an organisation, as the marketing activities of that venture is carried in

accordance with targeting those customers. This determination of target market is

undertaken by the appointed mangers of cited venture (Susilawati and Baridwan, 2016).

In order to determine target customers, the management accounting standards maintained

by that firm assist the managers or leaders. A major decision making process is involved

in defining the market market of a particular product. It should be decided as per the

offerings made by the present firm as well as demand patterns of customers. Thus, an

important decision making mechanism is needed to be undertaken to achieve the desired

goal of the venture to increase its market share. The management accounting standards

adopted gives a relevant data regarding the offerings made and applying it to generate

more customers leading to more share in the market, which further leads to long term

growth as well as development. Analysing purchases: The purchases made here, are in the context of purchasing various

resources required for undertaking operational activities of an organisation, in order to

generate desired output. The decisions regarding purchase of raw materials or inputs is

essential in order to avoid any emergent situation or any loss that may occur to the

inventory stocks maintained by the mentioned firm, i.e. Alara. The management

accounting standards keep a well maintained record of availability of raw materials,

finished goods, semi- finished goods and work in progress, while further enables the

mangers to make availability of these resources in a timely manner, in order to avoid any

disturbance in the production process (Höglund and Svärdsten, 2016). Thus, it can be

concluded that, management accounts assist the managers appointed at mentioned

organisation to undertake effective decisions regarding its purchases to be made.

Growth and developmental activities: Achieving growth as well s development is the

primary objective of every business organisation which operates in an economy. In

general terms, it is the base of various objects to be achieved by a venture. The

information included in the management accounting system is relevant to determine the

growth and development that has been achieved by mentioned venture in the long run.

Along with this, the mangers are required to undertake the function of planning the

resources in order to generate maximum results for future growth and development

2

importance for an organisation, as the marketing activities of that venture is carried in

accordance with targeting those customers. This determination of target market is

undertaken by the appointed mangers of cited venture (Susilawati and Baridwan, 2016).

In order to determine target customers, the management accounting standards maintained

by that firm assist the managers or leaders. A major decision making process is involved

in defining the market market of a particular product. It should be decided as per the

offerings made by the present firm as well as demand patterns of customers. Thus, an

important decision making mechanism is needed to be undertaken to achieve the desired

goal of the venture to increase its market share. The management accounting standards

adopted gives a relevant data regarding the offerings made and applying it to generate

more customers leading to more share in the market, which further leads to long term

growth as well as development. Analysing purchases: The purchases made here, are in the context of purchasing various

resources required for undertaking operational activities of an organisation, in order to

generate desired output. The decisions regarding purchase of raw materials or inputs is

essential in order to avoid any emergent situation or any loss that may occur to the

inventory stocks maintained by the mentioned firm, i.e. Alara. The management

accounting standards keep a well maintained record of availability of raw materials,

finished goods, semi- finished goods and work in progress, while further enables the

mangers to make availability of these resources in a timely manner, in order to avoid any

disturbance in the production process (Höglund and Svärdsten, 2016). Thus, it can be

concluded that, management accounts assist the managers appointed at mentioned

organisation to undertake effective decisions regarding its purchases to be made.

Growth and developmental activities: Achieving growth as well s development is the

primary objective of every business organisation which operates in an economy. In

general terms, it is the base of various objects to be achieved by a venture. The

information included in the management accounting system is relevant to determine the

growth and development that has been achieved by mentioned venture in the long run.

Along with this, the mangers are required to undertake the function of planning the

resources in order to generate maximum results for future growth and development

2

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

activities, which requires a range of financial and operational information of the venture

which is provided by the accounting standards of management (Hemmer and Labro,

2016). This important decision making mechanism of planning the activities of an

organisation for development is undertaken with respect to management accounts.

The above mentioned are the essential decision making processes that are undertaken by

the mangers appointed at mentioned organisation, in accordance with the management

accounting systems.

P2 Different types of management accounting systems

With reference to adopting an effective management accounting systems, the managers

or accountants appointed at Alara wholefoods, can adopt four systems of accounting, namely,

Cost accounting systems, Inventory management system of accounting, Job costing system and

Price optimising system. These systems of accounting enables the mangers to undertake an

effective as well as efficient management system for functioning of its activities (Otley, 2016). A

detailed evaluation of these accounting systems in the context of cited organisation is presented

as below: Cost accounting systems: The cost accounting system undertaken by present venture,

enables the managers appointed to determine the cost producing a particular level of

output. This cost calculated as per the cost accounting systems enables the manages to

determine the profits that have been generated and what measures are required to be

undertaken in order to generate or increase more profits. Inventory accounting systems: Inventory refers to the stock availability of a company

regarding its raw materials, semi finished goods, finished goods as well as work in

progress. Thus, inventory management refers to keeping a record as well as managing the

inventories available with the mentioned venture (Renz and Herman, 2016). A proper

accounting system is undertaken in order to manage the inventories, in respect of

avoiding any hindrances in the production process of the present entity and avoid any

damages for the inventories due to its overvaluation. In other words, inventory

management systems enables the appointed managers to maintain a balanced relationship

between the demand as well as supply of products offered by the organisation.

3

which is provided by the accounting standards of management (Hemmer and Labro,

2016). This important decision making mechanism of planning the activities of an

organisation for development is undertaken with respect to management accounts.

The above mentioned are the essential decision making processes that are undertaken by

the mangers appointed at mentioned organisation, in accordance with the management

accounting systems.

P2 Different types of management accounting systems

With reference to adopting an effective management accounting systems, the managers

or accountants appointed at Alara wholefoods, can adopt four systems of accounting, namely,

Cost accounting systems, Inventory management system of accounting, Job costing system and

Price optimising system. These systems of accounting enables the mangers to undertake an

effective as well as efficient management system for functioning of its activities (Otley, 2016). A

detailed evaluation of these accounting systems in the context of cited organisation is presented

as below: Cost accounting systems: The cost accounting system undertaken by present venture,

enables the managers appointed to determine the cost producing a particular level of

output. This cost calculated as per the cost accounting systems enables the manages to

determine the profits that have been generated and what measures are required to be

undertaken in order to generate or increase more profits. Inventory accounting systems: Inventory refers to the stock availability of a company

regarding its raw materials, semi finished goods, finished goods as well as work in

progress. Thus, inventory management refers to keeping a record as well as managing the

inventories available with the mentioned venture (Renz and Herman, 2016). A proper

accounting system is undertaken in order to manage the inventories, in respect of

avoiding any hindrances in the production process of the present entity and avoid any

damages for the inventories due to its overvaluation. In other words, inventory

management systems enables the appointed managers to maintain a balanced relationship

between the demand as well as supply of products offered by the organisation.

3

Job costing system: The job costing system of accounting enables the appointed

managers at cited firm to determine the costs incurred to undertake a particular job or

task in the process of production. It evaluates the significance as well as the costs that

have been involved by performing a particular activity, which further analyses the profits

that have been generated in the respect of that particular job performed. This technique of

accounting standards of management is provided to the customers as and whenever

demanded (Wouters and Maher, 2017). The numerous information included in this type

of accounting system are direct materials, direct labour and direct overheads.

Price optimising system: As per this system of accounting records of management, the

demand for the product at different price levels are recorded. There is an inverse

relationship between demand as well as price and a positive relation between supply as

well as price. The price where a producer is willing to sell maximum output coinciding

with the price which leads to maximum demand made by the customers, is taken into

consideration to charge for the products (Cooper and Qu, 2017). This different levels of

demand in accordance with different levels of prices, enables the appointed managers in

the cited organisation to charge an effective as well as reasonable and affordable prices

for its offerings, thus, generating more customers, leading towards more amount of

earnings.

This accounting standards adopted in assists the management accounting systems and

enables the manger to undertake an efficient decision making mechanism in respect of various

functions of management and different operational activities of the present company or business.

The major accounting system among the above mentioned system, which is useful in many ways

to Alara is Cost-accounting system of management, which would enable the firm determine the

cost of inputs used in respect of generating an output, which would be further used by the

managers to decide a price to attract more number of customers, leading to earning as well as

beneficial results (Eldenburg and Cook, 2016).

LO 2

P3 Use of absorption and variable costing techniques in management accounting

The absorption system or technique of costing and variable costing technique are two

different approaches that can be used by the managers appointed at cited firm to determine the

4

managers at cited firm to determine the costs incurred to undertake a particular job or

task in the process of production. It evaluates the significance as well as the costs that

have been involved by performing a particular activity, which further analyses the profits

that have been generated in the respect of that particular job performed. This technique of

accounting standards of management is provided to the customers as and whenever

demanded (Wouters and Maher, 2017). The numerous information included in this type

of accounting system are direct materials, direct labour and direct overheads.

Price optimising system: As per this system of accounting records of management, the

demand for the product at different price levels are recorded. There is an inverse

relationship between demand as well as price and a positive relation between supply as

well as price. The price where a producer is willing to sell maximum output coinciding

with the price which leads to maximum demand made by the customers, is taken into

consideration to charge for the products (Cooper and Qu, 2017). This different levels of

demand in accordance with different levels of prices, enables the appointed managers in

the cited organisation to charge an effective as well as reasonable and affordable prices

for its offerings, thus, generating more customers, leading towards more amount of

earnings.

This accounting standards adopted in assists the management accounting systems and

enables the manger to undertake an efficient decision making mechanism in respect of various

functions of management and different operational activities of the present company or business.

The major accounting system among the above mentioned system, which is useful in many ways

to Alara is Cost-accounting system of management, which would enable the firm determine the

cost of inputs used in respect of generating an output, which would be further used by the

managers to decide a price to attract more number of customers, leading to earning as well as

beneficial results (Eldenburg and Cook, 2016).

LO 2

P3 Use of absorption and variable costing techniques in management accounting

The absorption system or technique of costing and variable costing technique are two

different approaches that can be used by the managers appointed at cited firm to determine the

4

costs that have been incurred, in order to define the price making decision. As per the absorption

technique, the cost determined includes the fixed as well as variable costs, whereas, as per the

variable costing technique, only the variable costs are needed to be included. Although, both are

the techniques of recording costs, but, the application of both these methods is different in many

ways. The variable costing methods are included in the direct costing methods, whereas,

absorption costing technique is a full costing approach (Weetman, 2016). The difference

between the values generated from variable costing method as well as absorption costing

technique is due to the treatment of fixed cost or the value of fixed cost undertaken. Also, one of

the major differences between these costs along with the treatment of fixed overheads, is the

presentation of the income statement. These costs moves with the goods until they are sold and

then recorded in the income statement when they are sold, as cost of goods sold.

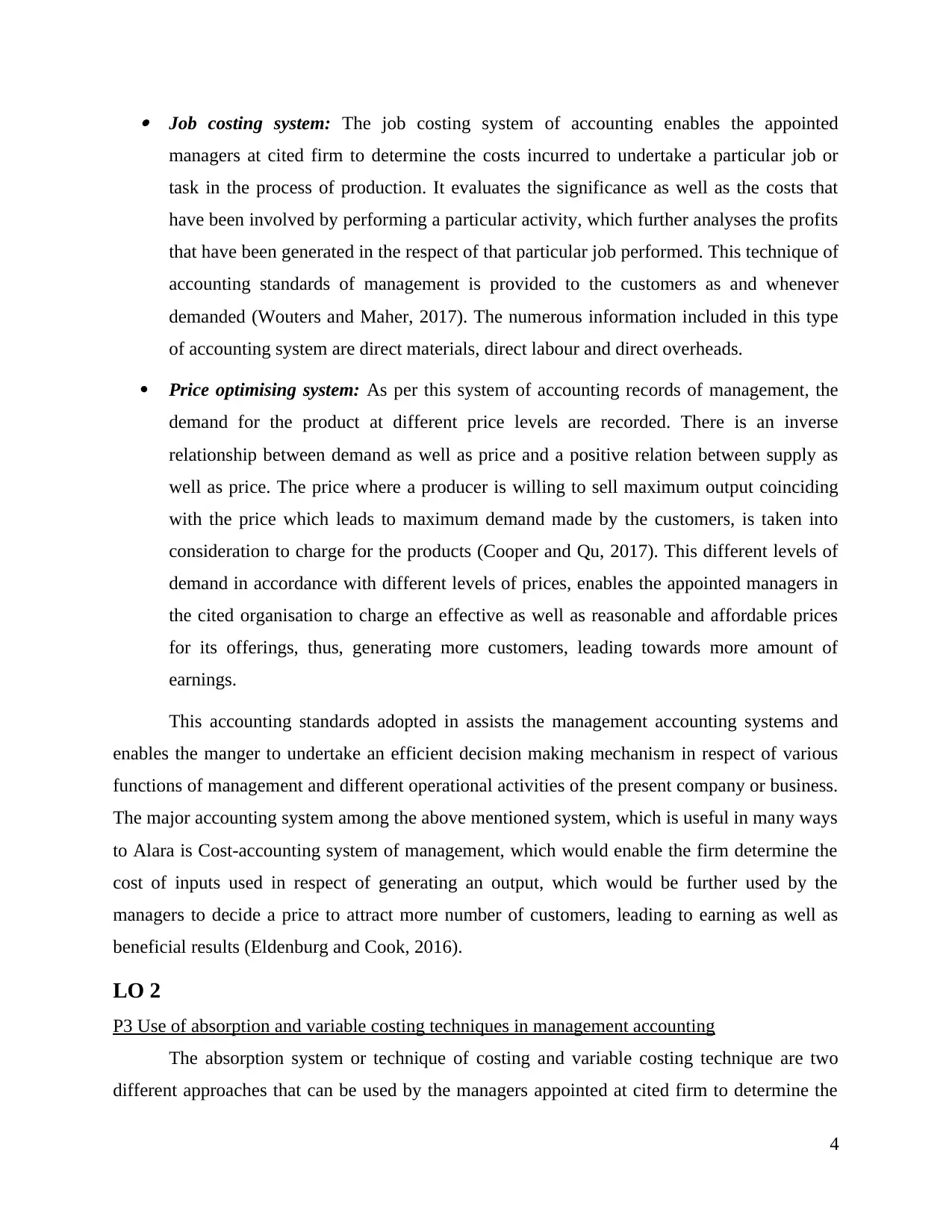

The above presented illustration evaluates the production costs of manufacturing

products by Alara Wholefoods, as per the absorption costing method as well as marginal costing

method. While calculating cost of each product produced or manufactured through absorption

technique, it can be concluded that the cost per unit is calculated as 0.85. whereas, while

calculating the production cost per unit as per the marginal approach of costing, the cost per unit

is recognised to be as 0.65. As mentioned earlier, the difference between both these costs is due

to the variation in the treatment of fixed overheads as per both the mentioned methods or

techniques of costing.

5

technique, the cost determined includes the fixed as well as variable costs, whereas, as per the

variable costing technique, only the variable costs are needed to be included. Although, both are

the techniques of recording costs, but, the application of both these methods is different in many

ways. The variable costing methods are included in the direct costing methods, whereas,

absorption costing technique is a full costing approach (Weetman, 2016). The difference

between the values generated from variable costing method as well as absorption costing

technique is due to the treatment of fixed cost or the value of fixed cost undertaken. Also, one of

the major differences between these costs along with the treatment of fixed overheads, is the

presentation of the income statement. These costs moves with the goods until they are sold and

then recorded in the income statement when they are sold, as cost of goods sold.

The above presented illustration evaluates the production costs of manufacturing

products by Alara Wholefoods, as per the absorption costing method as well as marginal costing

method. While calculating cost of each product produced or manufactured through absorption

technique, it can be concluded that the cost per unit is calculated as 0.85. whereas, while

calculating the production cost per unit as per the marginal approach of costing, the cost per unit

is recognised to be as 0.65. As mentioned earlier, the difference between both these costs is due

to the variation in the treatment of fixed overheads as per both the mentioned methods or

techniques of costing.

5

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

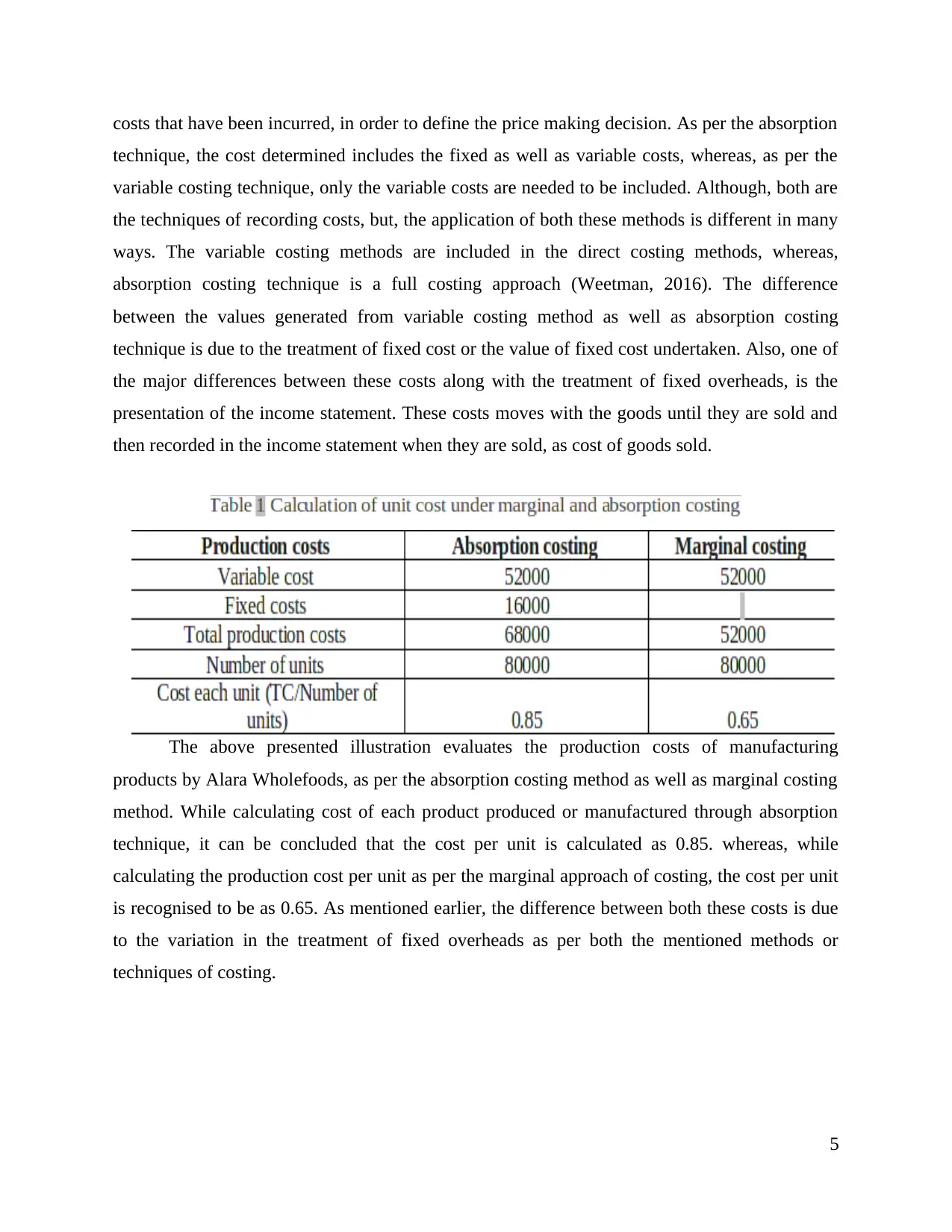

The above illustration represents the profitability statement of Alara Ltd, which states the

difference between the profits generated during the 1st quarter as well as 2nd quarter. As per the

absorption technique of undertaking cost per unit, the gross profit generated is 4700 during the

quarter 1, while during quarter 2 it has been increased due to the involvement of beginning

inventory value of the firm. The absorption technique includes fixed cost, thus, after the

deduction of fixed overheads incurred by the cited venture, the net profit generated by the firm is

recognised to be as 5900 during quarter 1 and 5900 as per the 2nd quarter.

6

difference between the profits generated during the 1st quarter as well as 2nd quarter. As per the

absorption technique of undertaking cost per unit, the gross profit generated is 4700 during the

quarter 1, while during quarter 2 it has been increased due to the involvement of beginning

inventory value of the firm. The absorption technique includes fixed cost, thus, after the

deduction of fixed overheads incurred by the cited venture, the net profit generated by the firm is

recognised to be as 5900 during quarter 1 and 5900 as per the 2nd quarter.

6

The above numerical illustration evaluates the profitability statement of Alara

wholefoods, which states its net profits generated as per the marginal or variable costing method

of management accounting. The numerical example states that during the quarter 1 period, the

net profits that has been generated by the firm is calculated as 1900, while in the 2nd quarter it is

calculated to be as 4700. there is no such difference recorded between net and gross profits, as

there is no involvement of fixed overheads in the costing approach as per marginal method.

The major difference between both the mentioned management accounting standards of

costing methods, i.e. absorption and marginal technique, is the difference between net profit

recorded as per both these approaches. The costs and the profits generated from both the

techniques varies from each other due to the valuation of fixed overheads undertaken. Along

with the differences in value of costs and profits, there is also a difference which can be noted,

that the absorption method evaluates difference between gross and net profits, while, the

marginal approach, dose not deals with the differentiation between gross and net profits, as it

only involves variable overheads.

SECTION II

LO 3

P4 Advantages and disadvantages of different types of planning tools adopted for budgetary

control in Nero Ltd.

In respect of undertaking the management function in an effective way, the mangers are

required to achieve a thorough information about the management accounting system. With the

objective of achieving the same by managers appointed at Nero Ltd., there is a need to undertake

or make use of different planning tools of management accounting standards. The present

venture in this topic is Nero Ltd., which is a London based coffee bar, which is a manufacturing

unit for coffees. The manger appointed at cited firm needs to utilise the planning tools in order to

perform his managerial functions in an effective way, towards the betterment of the organisation

(Jermias, 2017). These planning tools adopted ensures the managers appointed at mentioned

organisation to pioneer effective decision making process in the context of different managerial

function that need to be performed. It ensures management of organisational strategy, fuller

utilisation of available resources with the venture, generating a high range of satisfaction on the

7

wholefoods, which states its net profits generated as per the marginal or variable costing method

of management accounting. The numerical example states that during the quarter 1 period, the

net profits that has been generated by the firm is calculated as 1900, while in the 2nd quarter it is

calculated to be as 4700. there is no such difference recorded between net and gross profits, as

there is no involvement of fixed overheads in the costing approach as per marginal method.

The major difference between both the mentioned management accounting standards of

costing methods, i.e. absorption and marginal technique, is the difference between net profit

recorded as per both these approaches. The costs and the profits generated from both the

techniques varies from each other due to the valuation of fixed overheads undertaken. Along

with the differences in value of costs and profits, there is also a difference which can be noted,

that the absorption method evaluates difference between gross and net profits, while, the

marginal approach, dose not deals with the differentiation between gross and net profits, as it

only involves variable overheads.

SECTION II

LO 3

P4 Advantages and disadvantages of different types of planning tools adopted for budgetary

control in Nero Ltd.

In respect of undertaking the management function in an effective way, the mangers are

required to achieve a thorough information about the management accounting system. With the

objective of achieving the same by managers appointed at Nero Ltd., there is a need to undertake

or make use of different planning tools of management accounting standards. The present

venture in this topic is Nero Ltd., which is a London based coffee bar, which is a manufacturing

unit for coffees. The manger appointed at cited firm needs to utilise the planning tools in order to

perform his managerial functions in an effective way, towards the betterment of the organisation

(Jermias, 2017). These planning tools adopted ensures the managers appointed at mentioned

organisation to pioneer effective decision making process in the context of different managerial

function that need to be performed. It ensures management of organisational strategy, fuller

utilisation of available resources with the venture, generating a high range of satisfaction on the

7

part of customers through providing a qualified offerings at reasonable rates. Some of the

important tools that can be best sited for present organisation are explained in detail as under: Budget analysis: The budgetary analysis undertaken in a venture is useful in controlling

the financial activities of that firm by the managers. A budget shows pre determined

values or figures of investment to be made on a particular operational activity interpreted.

An effective budgetary analysis enables the mangers of mentioned organisation to keep

their functions in track of achieving growth and development, thus, leading towards

success. It ensures the managers to determine the difference between the potential

revenue that can be generated from a particular activity, from the actual returns that has

been generated. Higher returns indicates higher efficiencies of managers as well as the

concerned company (Messner, 2016). It enables the mangers to control the financial

activities prevailing in the business, in order to ensure sustainable growth with higher

earnings. This tool is associated with numerous advantages, but, it is just a mere

estimation of potentialities of a venture which are compared with actual performance

generated.

Ratio analysis: The managerial accounting standards adopted needed to be applied

effectively in order to generate efficient as well as beneficial results. In respect of

achieving this objective, the ratio analysis strategy of planning can be undertaken in an

effective way. As per this tool of planning, specific ratios are generated which acts as

informative sources for the managers in decision making process (Ax and Greve, 2017).

The numerous ratios that can be generated includes the following:

Profitability ratio, which determines the returns on the investment mechanism

confiscated.

Leverage ratio, which evaluates the risk factor of the firm.

Solvency ratio, which determines the potentiality of the venture to repay its debts

created. Liquidity ratio, which involves the nature of the firm regarding converting its assets

into monetary terms (Granlund and Lukka, 2017).

8

important tools that can be best sited for present organisation are explained in detail as under: Budget analysis: The budgetary analysis undertaken in a venture is useful in controlling

the financial activities of that firm by the managers. A budget shows pre determined

values or figures of investment to be made on a particular operational activity interpreted.

An effective budgetary analysis enables the mangers of mentioned organisation to keep

their functions in track of achieving growth and development, thus, leading towards

success. It ensures the managers to determine the difference between the potential

revenue that can be generated from a particular activity, from the actual returns that has

been generated. Higher returns indicates higher efficiencies of managers as well as the

concerned company (Messner, 2016). It enables the mangers to control the financial

activities prevailing in the business, in order to ensure sustainable growth with higher

earnings. This tool is associated with numerous advantages, but, it is just a mere

estimation of potentialities of a venture which are compared with actual performance

generated.

Ratio analysis: The managerial accounting standards adopted needed to be applied

effectively in order to generate efficient as well as beneficial results. In respect of

achieving this objective, the ratio analysis strategy of planning can be undertaken in an

effective way. As per this tool of planning, specific ratios are generated which acts as

informative sources for the managers in decision making process (Ax and Greve, 2017).

The numerous ratios that can be generated includes the following:

Profitability ratio, which determines the returns on the investment mechanism

confiscated.

Leverage ratio, which evaluates the risk factor of the firm.

Solvency ratio, which determines the potentiality of the venture to repay its debts

created. Liquidity ratio, which involves the nature of the firm regarding converting its assets

into monetary terms (Granlund and Lukka, 2017).

8

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

MIS: In respect of conducting the managerial activities in an efficient manner, there is a

need to perform effective communicational activities in an organisation. The

management information system (MIS) is an effective system, which ensures free flow of

information in the mentioned venture, i.e. Alara. Thus, the managers can undertake

decision making process in an effective way and communicate the decisions and the facts

regarding any changes that has been undertaken as a result of this decision making

mechanism to its subordinates or other individuals working in that entity (Chiwamit and

Scapens, 2017). The information generated through MIS, is useful for the managers as

well as organisation in many ways.

These are the major planning tools that can be used by cited company with a view if

adopting an effective management accounting standards, thus, leading that organisation towards

achievement of its goals as well as objectives. Quality decision making processes can be

undertaken in a firm in accordance with these tools or strategies adopted in management

accounting systems.

LO 4

P5 Adaptation of management accounting systems to respond to financial problems

In order to solve the various financial problems in an organisation, there is a need to

adopt an effective management standards, which would generate efficient enough solutions for

the managers. The numerous accounting systems in order to respond to prevailing finance

related problems are explained in detail as under: Identification of problems: In respect of solving a particular problem, there is a need to

identify the problems that needed to be solved overtime. The managers of the mentioned

venture, i.e. Nero Ltd., are required to identify the financial needs or problems and

provide solutions for that. This identification can be generated with the help of

management accounting standards that have been maintained by the organisation (Maas

and Crutzen, 2016). The financial problems that may occur in an organisation are relating

to its reduction in revenue as a result of reduction in sales, increase in the cost of inputs

required to generate desired outputs, decrease in the rates of earnings made by a firm

through its operational activities. Also, the managers are required to make availability of

9

need to perform effective communicational activities in an organisation. The

management information system (MIS) is an effective system, which ensures free flow of

information in the mentioned venture, i.e. Alara. Thus, the managers can undertake

decision making process in an effective way and communicate the decisions and the facts

regarding any changes that has been undertaken as a result of this decision making

mechanism to its subordinates or other individuals working in that entity (Chiwamit and

Scapens, 2017). The information generated through MIS, is useful for the managers as

well as organisation in many ways.

These are the major planning tools that can be used by cited company with a view if

adopting an effective management accounting standards, thus, leading that organisation towards

achievement of its goals as well as objectives. Quality decision making processes can be

undertaken in a firm in accordance with these tools or strategies adopted in management

accounting systems.

LO 4

P5 Adaptation of management accounting systems to respond to financial problems

In order to solve the various financial problems in an organisation, there is a need to

adopt an effective management standards, which would generate efficient enough solutions for

the managers. The numerous accounting systems in order to respond to prevailing finance

related problems are explained in detail as under: Identification of problems: In respect of solving a particular problem, there is a need to

identify the problems that needed to be solved overtime. The managers of the mentioned

venture, i.e. Nero Ltd., are required to identify the financial needs or problems and

provide solutions for that. This identification can be generated with the help of

management accounting standards that have been maintained by the organisation (Maas

and Crutzen, 2016). The financial problems that may occur in an organisation are relating

to its reduction in revenue as a result of reduction in sales, increase in the cost of inputs

required to generate desired outputs, decrease in the rates of earnings made by a firm

through its operational activities. Also, the managers are required to make availability of

9

funds or financial resources as and when required by an organisation, this requirement of

funds is realised through an evaluation of management accounts prepared. Variance analysis: This analysis evaluates the variations or differences in the financial

performance of a venture from time to time. This variations are evaluated in response to

the budgetary targets made by the managers on a pre determined basis. These values

which are determined on a prior basis are compared with actual results and the variations

generated are needed to be recognised, along with the reason behind those variances or

deviations (Bromwich and Scapens, 2016). With this recognition, the managers are

assigned with the responsibility of generating solutions regarding these problems. Benchmark scorecard: The benchmark scorecard is used by an organisation to evaluate

its various objectives by determining the target to be accomplished, aligning the day to

day activities that the employees are expected to perform, effective planning of projects

for production of goods as well as services and monitoring the performance of employees

as well as other personnel in the organisation, with a sloe view of achieving desired

strategic targets (Balance Scorecard, 2018). Appointing Qualitative human resource team: With respect of solving a particular

financial problems that may prevail in a firm, the managers appointed at the mentioned

organisation are required to hire or appointed qualified individuals in order to perform

various operational duties in favour of that company. The organisation with skilled as

well as expertise workforce brings efficient as well as earning results for that venture, as

human is considered to be as the driving source if an entity's performance and profits.

Qualified personnel would assist the managers in providing solutions to the various

financial problems that may occur in a business and lead to higher rate of flexibility

relating to undertake required changes in that firm (Hopper and Bui, 2016). Efficient strategies: The various tools or strategies of planning can be adopted in order to

solve a particular financial problem that may prevail in an organisation. These planning

tools are effective in generating solutions, as it assist the managers in maintenance of

proper management accounting standards.

Financial governance: A set of rules, regulations, practices and processes relating to the

financial activities that are needed to be undertaken in an organisation is termed as

10

funds is realised through an evaluation of management accounts prepared. Variance analysis: This analysis evaluates the variations or differences in the financial

performance of a venture from time to time. This variations are evaluated in response to

the budgetary targets made by the managers on a pre determined basis. These values

which are determined on a prior basis are compared with actual results and the variations

generated are needed to be recognised, along with the reason behind those variances or

deviations (Bromwich and Scapens, 2016). With this recognition, the managers are

assigned with the responsibility of generating solutions regarding these problems. Benchmark scorecard: The benchmark scorecard is used by an organisation to evaluate

its various objectives by determining the target to be accomplished, aligning the day to

day activities that the employees are expected to perform, effective planning of projects

for production of goods as well as services and monitoring the performance of employees

as well as other personnel in the organisation, with a sloe view of achieving desired

strategic targets (Balance Scorecard, 2018). Appointing Qualitative human resource team: With respect of solving a particular

financial problems that may prevail in a firm, the managers appointed at the mentioned

organisation are required to hire or appointed qualified individuals in order to perform

various operational duties in favour of that company. The organisation with skilled as

well as expertise workforce brings efficient as well as earning results for that venture, as

human is considered to be as the driving source if an entity's performance and profits.

Qualified personnel would assist the managers in providing solutions to the various

financial problems that may occur in a business and lead to higher rate of flexibility

relating to undertake required changes in that firm (Hopper and Bui, 2016). Efficient strategies: The various tools or strategies of planning can be adopted in order to

solve a particular financial problem that may prevail in an organisation. These planning

tools are effective in generating solutions, as it assist the managers in maintenance of

proper management accounting standards.

Financial governance: A set of rules, regulations, practices and processes relating to the

financial activities that are needed to be undertaken in an organisation is termed as

10

financial governance. In general terms, the financial governance provided acts as a

guiding principle or framework for performing finance related activities in a venture.

The managers of Nero Ltd., may resort to these guidelines issued in respect of solving a

particular financial problem in a firm (Dekker, , 2016).

All these can be recognised as the ways in which the management accounting standards

can be beneficial for an organisation, with a view of providing solutions by the managers to

solve finance related matter or issue.

CONCLUSION

The report presented in this project includes a detailed evaluation of management

accounting standards and its implications in the context of an organisation. It evaluates in detail

about the importance of management accounting systems to be adopted with reference to an

enterprise. It states that, there are four major accounting systems that can be undertaken in

management accounting namely, Cost accounting systems, Inventory management system of

accounting, Job costing system and Price optimising system. The present report includes a brief

evaluation of difference between absorption and variance or marginal costing techniques used in

the context of management accounting standards. This difference is presented with a numerical

example showing cost and profitability statement of a company. The section II of the report

represents various advantages as well as disadvantages of three major planning tools adopted inn

management accounting, viz. Budget analysis, Ratio analysis and MIS. The implication of

management accounting standards in identifying as well as solving a related financial problem of

a venture is explained in detail as in this report.

11

guiding principle or framework for performing finance related activities in a venture.

The managers of Nero Ltd., may resort to these guidelines issued in respect of solving a

particular financial problem in a firm (Dekker, , 2016).

All these can be recognised as the ways in which the management accounting standards

can be beneficial for an organisation, with a view of providing solutions by the managers to

solve finance related matter or issue.

CONCLUSION

The report presented in this project includes a detailed evaluation of management

accounting standards and its implications in the context of an organisation. It evaluates in detail

about the importance of management accounting systems to be adopted with reference to an

enterprise. It states that, there are four major accounting systems that can be undertaken in

management accounting namely, Cost accounting systems, Inventory management system of

accounting, Job costing system and Price optimising system. The present report includes a brief

evaluation of difference between absorption and variance or marginal costing techniques used in

the context of management accounting standards. This difference is presented with a numerical

example showing cost and profitability statement of a company. The section II of the report

represents various advantages as well as disadvantages of three major planning tools adopted inn

management accounting, viz. Budget analysis, Ratio analysis and MIS. The implication of

management accounting standards in identifying as well as solving a related financial problem of

a venture is explained in detail as in this report.

11

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

REFERENCES

Books and Journals

Ax, C. and Greve, J., 2017. Adoption of management accounting innovations: Organizational

culture compatibility and perceived outcomes. Management Accounting Research. 34.

pp.59-74.

Bromwich, M. and Scapens, R. W., 2016. Management accounting research: 25 years on.

Management Accounting Research. 31. pp.1-9.

Chiwamit, P. and Scapens, R. W., 2017. Regulation and adaptation of management accounting

innovations: The case of economic value added in Thai state-owned enterprises.

Management Accounting Research. 37. pp.30-48.

Cooper, D. J. and Qu, S.Q., 2017. Popularizing a management accounting idea: The case of the

balanced scorecard. Contemporary Accounting Research. 34(2). pp.991-1025.

Dekker, H. C., 2016. On the boundaries between intrafirm and interfirm management accounting

research. Management Accounting Research. 31. pp.86-99.

Eldenburg, L. G. and Cook, G., 2016. Cost management: Measuring, monitoring, and

motivating performance. Wiley Global Education.

Granlund, M. and Lukka, K., 2017. Investigating highly established research paradigms:

Reviving contextuality in contingency theory based management accounting research.

Critical Perspectives on Accounting. 45. pp.63-80.

Hemmer, T. and Labro, E., 2016. Productions and Operations Management & Management

Accounting.

Höglund, L. and Svärdsten, F., 2016. Management accounting of control practices: a matter of

and for strategy. In the 9TH INTERNATIONAL EIASM PUBLIC SECTOR

CONFERENCE, held in LISBON, PORTUGAL, SEPTEMBER 6-8, 2016..

Hopper, T. and Bui, B., 2016. Has management accounting research been critical?. Management

Accounting Research. 31. pp.10-30.

Jermias, J., 2017. Development of management accounting practices in Indonesia. The

Routledge Handbook of Accounting in Asia, p.104.

12

Books and Journals

Ax, C. and Greve, J., 2017. Adoption of management accounting innovations: Organizational

culture compatibility and perceived outcomes. Management Accounting Research. 34.

pp.59-74.

Bromwich, M. and Scapens, R. W., 2016. Management accounting research: 25 years on.

Management Accounting Research. 31. pp.1-9.

Chiwamit, P. and Scapens, R. W., 2017. Regulation and adaptation of management accounting

innovations: The case of economic value added in Thai state-owned enterprises.

Management Accounting Research. 37. pp.30-48.

Cooper, D. J. and Qu, S.Q., 2017. Popularizing a management accounting idea: The case of the

balanced scorecard. Contemporary Accounting Research. 34(2). pp.991-1025.

Dekker, H. C., 2016. On the boundaries between intrafirm and interfirm management accounting

research. Management Accounting Research. 31. pp.86-99.

Eldenburg, L. G. and Cook, G., 2016. Cost management: Measuring, monitoring, and

motivating performance. Wiley Global Education.

Granlund, M. and Lukka, K., 2017. Investigating highly established research paradigms:

Reviving contextuality in contingency theory based management accounting research.

Critical Perspectives on Accounting. 45. pp.63-80.

Hemmer, T. and Labro, E., 2016. Productions and Operations Management & Management

Accounting.

Höglund, L. and Svärdsten, F., 2016. Management accounting of control practices: a matter of

and for strategy. In the 9TH INTERNATIONAL EIASM PUBLIC SECTOR

CONFERENCE, held in LISBON, PORTUGAL, SEPTEMBER 6-8, 2016..

Hopper, T. and Bui, B., 2016. Has management accounting research been critical?. Management

Accounting Research. 31. pp.10-30.

Jermias, J., 2017. Development of management accounting practices in Indonesia. The

Routledge Handbook of Accounting in Asia, p.104.

12

Maas, K. and Crutzen, N., 2016. Integrating corporate sustainability assessment, management

accounting, control, and reporting. Journal of Cleaner Production. 136. pp.237-248.

Messner, M., 2016. Does industry matter? How industry context shapes management accounting

practice. Management Accounting Research. 31. pp.103-111.

Otley, D., 2016. The contingency theory of management accounting and control: 1980–2014.

Management accounting research. 31. pp.45-62.

Renz, D. O. and Herman, R. D. eds., 2016. The Jossey-Bass handbook of nonprofit leadership

and management. John Wiley & Sons.

Schaltegger, S. and Burritt, R., 2017. Contemporary environmental accounting: issues, concepts

and practice. Routledge.

Susilawati, M. and Baridwan, Z., 2016. Frame Value of Strategic Management Accounting

Based on The Balance of Tri Kaya Parisudha.

Weetman, P., 2016. Financial and Management Accounting with MyAccountingLab Access

Card. Pearson/Education.

Wouters, M. and Maher, M. W., 2017. T Course: Management Accounting 1 [T-WIWI-102800].

Module Handbook Industrial Engineering and Management (B. Sc.).

Online

Balance Scorecard. 2018 [online] Available through .<http://www.balancedscorecard.org/BSC-

Basics/About-the-Balanced-Scorecard>.

13

accounting, control, and reporting. Journal of Cleaner Production. 136. pp.237-248.

Messner, M., 2016. Does industry matter? How industry context shapes management accounting

practice. Management Accounting Research. 31. pp.103-111.

Otley, D., 2016. The contingency theory of management accounting and control: 1980–2014.

Management accounting research. 31. pp.45-62.

Renz, D. O. and Herman, R. D. eds., 2016. The Jossey-Bass handbook of nonprofit leadership

and management. John Wiley & Sons.

Schaltegger, S. and Burritt, R., 2017. Contemporary environmental accounting: issues, concepts

and practice. Routledge.

Susilawati, M. and Baridwan, Z., 2016. Frame Value of Strategic Management Accounting

Based on The Balance of Tri Kaya Parisudha.

Weetman, P., 2016. Financial and Management Accounting with MyAccountingLab Access

Card. Pearson/Education.

Wouters, M. and Maher, M. W., 2017. T Course: Management Accounting 1 [T-WIWI-102800].

Module Handbook Industrial Engineering and Management (B. Sc.).

Online

Balance Scorecard. 2018 [online] Available through .<http://www.balancedscorecard.org/BSC-

Basics/About-the-Balanced-Scorecard>.

13

1 out of 15

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

© 2024 | Zucol Services PVT LTD | All rights reserved.