Management Accounting and Accounting Systems

VerifiedAdded on 2023/01/19

|25

|5615

|25

AI Summary

This document provides an introduction to management accounting and the requirement of different accounting systems. It discusses various methods of accounting for management reporting and the advantages of management accounting systems. The document also includes the development of income statements using marginal and absorption costing.

Contribute Materials

Your contribution can guide someone’s learning journey. Share your

documents today.

Name:

Registration Number

Date:

Is this a First Submission or Second Submission ?

Word Count

Turnitin Score

Learner’s statement of authenticity

I certify that the work submitted for this project is my own. Where the work of others

has been used to support my work then credit has been acknowledged. I have

identified and acknowledged all sources used in this project and have referenced

according to the Harvard referencing system. I have read and understood the

Plagiarism and Collusion section provided with the project brief and understood the

consequences of plagiarising.

Signature: ___________________ Date: ___/___/_____

wor

ds %

Registration Number

Date:

Is this a First Submission or Second Submission ?

Word Count

Turnitin Score

Learner’s statement of authenticity

I certify that the work submitted for this project is my own. Where the work of others

has been used to support my work then credit has been acknowledged. I have

identified and acknowledged all sources used in this project and have referenced

according to the Harvard referencing system. I have read and understood the

Plagiarism and Collusion section provided with the project brief and understood the

consequences of plagiarising.

Signature: ___________________ Date: ___/___/_____

wor

ds %

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

Table of Contents

INTRODUCTION...........................................................................................................................1

TASK 1............................................................................................................................................1

P1. Management accounting and requirement of different accounting systems...................1

P2. Various method of accounting of management reporting...............................................3

M1. Advantages of management accounting systems and their application for context of

companies...............................................................................................................................5

D1 Management accounting system and reporting integrated with organisational process.. 6

TASK 2............................................................................................................................................6

P3. Development of income statements as per the marginal and absorption costing...........6

M2. Management accounting techniques to produce financial reports................................13

D2. Interpretation of produced financial statements............................................................13

TASK 3..........................................................................................................................................14

P4. Benefits and limitations of tools of planning ................................................................14

M3. Various types of planning tools and their application for developing and forecasting of

budget...................................................................................................................................15

TASK 4..........................................................................................................................................15

P5. Comparison of companies to solve the financial issues with the help of systems of

accounting.............................................................................................................................15

M4. Management accounting to solve the financial issues..................................................17

D3. Planning tools to solve the financial issues...................................................................17

CONCLUSION..............................................................................................................................18

REFERENCES..............................................................................................................................19

INTRODUCTION...........................................................................................................................1

TASK 1............................................................................................................................................1

P1. Management accounting and requirement of different accounting systems...................1

P2. Various method of accounting of management reporting...............................................3

M1. Advantages of management accounting systems and their application for context of

companies...............................................................................................................................5

D1 Management accounting system and reporting integrated with organisational process.. 6

TASK 2............................................................................................................................................6

P3. Development of income statements as per the marginal and absorption costing...........6

M2. Management accounting techniques to produce financial reports................................13

D2. Interpretation of produced financial statements............................................................13

TASK 3..........................................................................................................................................14

P4. Benefits and limitations of tools of planning ................................................................14

M3. Various types of planning tools and their application for developing and forecasting of

budget...................................................................................................................................15

TASK 4..........................................................................................................................................15

P5. Comparison of companies to solve the financial issues with the help of systems of

accounting.............................................................................................................................15

M4. Management accounting to solve the financial issues..................................................17

D3. Planning tools to solve the financial issues...................................................................17

CONCLUSION..............................................................................................................................18

REFERENCES..............................................................................................................................19

INTRODUCTION

Management Accounting can be explained as the procedure for maintaining all the

internal data of an organization through which better strategies can be formulated for achieving

organizational goals. It is necessary because it helps manager, directors, shareholder to analyse

about overall performance of the organization. Also, it gives idea to outsiders, whether they

should invest within the company or not. For this project, the chosen financial consultancy is

AstraZeneca. This company belongs to pharmaceutical and biotechnology industry. It offers

various types of pharmaceuticals products. It was founded in year 1999. Headquarter of company

is located in England, UK. Different planning tools in budgetary control will also be explained

with their pros and cons. Also, there will be explanation about how financial problem can be

resolved with the help of management accounting.

TASK 1

P1. Management accounting and requirement of different accounting systems.

As per the institute of Cost and Management Accountants, management accounting refers

to the use of professional skill and knowledge in prepartion of accounting information that helps

management in developing policies.

It involves methods and concepts that are essential for effectively plan for selecting among

alternative actions for interpretation of performance (Chenhall and Moers, 2015).

The role of management accounting includes recording, gathering and reporting financial

information from different units of firm and analysing the budget and suggesting allocation.

Its major role is to conduct budgeting. It guides company regarding all the expenditures (Jefrey,

ed., 2018).

It is the process of the system of accounting which helps directors of an organisation to

take any of the decision as per the situation arises in front of them. There are number of reports

which is being prepared by organization and all of those reports are directly related with

management accounting (Chenhall and Moers, 2015). In context of AstraZeneca, it has been

helpful for them because they are able to take any of the effective decision with the help of

management accounting. There are numbers of the system of management accounting and they

are:

1

Management Accounting can be explained as the procedure for maintaining all the

internal data of an organization through which better strategies can be formulated for achieving

organizational goals. It is necessary because it helps manager, directors, shareholder to analyse

about overall performance of the organization. Also, it gives idea to outsiders, whether they

should invest within the company or not. For this project, the chosen financial consultancy is

AstraZeneca. This company belongs to pharmaceutical and biotechnology industry. It offers

various types of pharmaceuticals products. It was founded in year 1999. Headquarter of company

is located in England, UK. Different planning tools in budgetary control will also be explained

with their pros and cons. Also, there will be explanation about how financial problem can be

resolved with the help of management accounting.

TASK 1

P1. Management accounting and requirement of different accounting systems.

As per the institute of Cost and Management Accountants, management accounting refers

to the use of professional skill and knowledge in prepartion of accounting information that helps

management in developing policies.

It involves methods and concepts that are essential for effectively plan for selecting among

alternative actions for interpretation of performance (Chenhall and Moers, 2015).

The role of management accounting includes recording, gathering and reporting financial

information from different units of firm and analysing the budget and suggesting allocation.

Its major role is to conduct budgeting. It guides company regarding all the expenditures (Jefrey,

ed., 2018).

It is the process of the system of accounting which helps directors of an organisation to

take any of the decision as per the situation arises in front of them. There are number of reports

which is being prepared by organization and all of those reports are directly related with

management accounting (Chenhall and Moers, 2015). In context of AstraZeneca, it has been

helpful for them because they are able to take any of the effective decision with the help of

management accounting. There are numbers of the system of management accounting and they

are:

1

Cost accounting system: In any of the organization, top-level management uses cost

accounting system for finding the actual price of any manufacturing products. It even helps them

to analyse any of the direct or indirect cost mainly occurs within business organization. In short,

it helps business organization to help collect all of relevant information related to expenses of a

company. It is being maintained by AstraZeneca, for the purpose of maintaining any of the

records which occurs during manufacturing process.

DIRECT COST- It refers to the expenditure that can be directly allocated to the production of

particular goods or services.

INDIRECT COST- These are those expenses that are incurred for proper working of the

business. They cannot be directly attributed to a cost object. It includes fixed cost that remain

fixed inspite of change in volume of sales. Variable cost that changes with a change in volume of

sales.

Inventory Management System: It is helpful for this company which are engaged

within manufacturing process. AstraZeneca applies IMS so that they can easily maintain all of

the records which are taken while conducting manufacturing process. (Englund and Gerdin,

2014). There are three types of Inventory management systems such as FIFO, LIFO & AVCO.

When it comes to FIFO, the products which where bough in beginning are needed to be used

whereas in case of LIFO, the products which are bough recently is needed to be used for

manufacturing process. In case of AVCO, production is needed to be done on the basis of

average cost. In case of AstraZeneca, they use FIFO for manufacturing process because that

helps them to maintain the data related to inventories and whole of the procedure can be

conducted in systematic manner.

EOQ- It is the proper quantity that should be purchased by firm to reduce cost of inventory like

shortage cost, holding cost, order cost etc.

ROP- Reorder point is the quantity that triggers the buying of a specific amount of

replenishment stock.

JIT- It is the strategy of management that integrate orders of raw material from suppliers directly

with schedule of production.

Price Optimisation System: The most important accounting system for management is

the system of price optimization because it helps to set the standard price of product which has

been manufactured. Also, it tries to find whether expectation of customers is meet or not with

2

accounting system for finding the actual price of any manufacturing products. It even helps them

to analyse any of the direct or indirect cost mainly occurs within business organization. In short,

it helps business organization to help collect all of relevant information related to expenses of a

company. It is being maintained by AstraZeneca, for the purpose of maintaining any of the

records which occurs during manufacturing process.

DIRECT COST- It refers to the expenditure that can be directly allocated to the production of

particular goods or services.

INDIRECT COST- These are those expenses that are incurred for proper working of the

business. They cannot be directly attributed to a cost object. It includes fixed cost that remain

fixed inspite of change in volume of sales. Variable cost that changes with a change in volume of

sales.

Inventory Management System: It is helpful for this company which are engaged

within manufacturing process. AstraZeneca applies IMS so that they can easily maintain all of

the records which are taken while conducting manufacturing process. (Englund and Gerdin,

2014). There are three types of Inventory management systems such as FIFO, LIFO & AVCO.

When it comes to FIFO, the products which where bough in beginning are needed to be used

whereas in case of LIFO, the products which are bough recently is needed to be used for

manufacturing process. In case of AVCO, production is needed to be done on the basis of

average cost. In case of AstraZeneca, they use FIFO for manufacturing process because that

helps them to maintain the data related to inventories and whole of the procedure can be

conducted in systematic manner.

EOQ- It is the proper quantity that should be purchased by firm to reduce cost of inventory like

shortage cost, holding cost, order cost etc.

ROP- Reorder point is the quantity that triggers the buying of a specific amount of

replenishment stock.

JIT- It is the strategy of management that integrate orders of raw material from suppliers directly

with schedule of production.

Price Optimisation System: The most important accounting system for management is

the system of price optimization because it helps to set the standard price of product which has

been manufactured. Also, it tries to find whether expectation of customers is meet or not with

2

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

price range which has been decided by organization. In context of AstraZeneca, they help to

select the price of the clothes so that it can be sold within the marketplace at reasonable price.

Job Order Costing System: It is the method of costing which is used by organisation in

the situation where products are manufactured on the basis of specific order by any of the

customers. It helps to determine accurate cost of product through which it can be easily found

whether company is having loss or profit in any of the job. In context of AstraZeneca, they uses

job order costing system because they manufacture different variety of product where price are

different and it can easily calculated with the help of this accounting system.

P2. Various method of accounting of management reporting.

Management accounting reporting can be explained as the procedure which delivers

different types of information regarding daily basis operation which is being managed within the

company (Maas, Schaltegger and Crutzen, 2016). Some of the management accounting reports

are explained below:

Inventory management report- This report contains any of the information which is

related with the stock available within the company and that helps organisation to

calculate that when they are required reorder raw material. Here, Production department

of AstraZeneca uses this report just to find actual amount of product which they have

manufactured and additional amount of raw material which they will require in future.

Account receivable ageing report- This management accounting is being prepared for

the purpose of finding the debtors who are unable to clear their account even after the

end of deadlines. This report is helpful in deciding whether organisation should allow for

future credit dealings or not (Melnyk and et. al., 2014). In short helps to determine the

relationship between organization and their customers who deals in credit facilities.

While talking about AstraZeneca, their finance department is responsible for this report

where they check which debtors is needed to pay debt amount to organization.

Cost accounting report- In this report it is being checked that what is the total expenses

that company has incurred while conducting any of the particular activity. It is helpful

for company because they can easily find the expenses incurred in conducting any of the

activity. AstraZeneca requires to prepare this particular report in order to manage the

overall cost while manufacturing clothing products.

3

select the price of the clothes so that it can be sold within the marketplace at reasonable price.

Job Order Costing System: It is the method of costing which is used by organisation in

the situation where products are manufactured on the basis of specific order by any of the

customers. It helps to determine accurate cost of product through which it can be easily found

whether company is having loss or profit in any of the job. In context of AstraZeneca, they uses

job order costing system because they manufacture different variety of product where price are

different and it can easily calculated with the help of this accounting system.

P2. Various method of accounting of management reporting.

Management accounting reporting can be explained as the procedure which delivers

different types of information regarding daily basis operation which is being managed within the

company (Maas, Schaltegger and Crutzen, 2016). Some of the management accounting reports

are explained below:

Inventory management report- This report contains any of the information which is

related with the stock available within the company and that helps organisation to

calculate that when they are required reorder raw material. Here, Production department

of AstraZeneca uses this report just to find actual amount of product which they have

manufactured and additional amount of raw material which they will require in future.

Account receivable ageing report- This management accounting is being prepared for

the purpose of finding the debtors who are unable to clear their account even after the

end of deadlines. This report is helpful in deciding whether organisation should allow for

future credit dealings or not (Melnyk and et. al., 2014). In short helps to determine the

relationship between organization and their customers who deals in credit facilities.

While talking about AstraZeneca, their finance department is responsible for this report

where they check which debtors is needed to pay debt amount to organization.

Cost accounting report- In this report it is being checked that what is the total expenses

that company has incurred while conducting any of the particular activity. It is helpful

for company because they can easily find the expenses incurred in conducting any of the

activity. AstraZeneca requires to prepare this particular report in order to manage the

overall cost while manufacturing clothing products.

3

Budget report- These reports are very important in measuring the performance of firm

and are generated for various departments. Every firm develop overall budget yto

understand the overall scheme of business.

Performance report- These reports are developed to review the performance of firm as

a whole and for individual employee's.

4

and are generated for various departments. Every firm develop overall budget yto

understand the overall scheme of business.

Performance report- These reports are developed to review the performance of firm as

a whole and for individual employee's.

4

M1. Advantages of management accounting systems and their application for context of

companies.

Cost accounting system-

This method allows managers to fluctuate the cost structure of products to manage the

customer base.

It enables AstraZeneca to evaluate its cost-effectiveness of its operations (Smith, 2017).

System of Price optimisation -

It often allows the entity to select the effective price for its products in order to maximize

its productivity.

The system will help AstraZeneca to assess the belief of users on distinct clothing

products.

It is used by business to analyse how the customer’s will respond when there is a change

in the price of goods or services.

Inventory management system-

5

companies.

Cost accounting system-

This method allows managers to fluctuate the cost structure of products to manage the

customer base.

It enables AstraZeneca to evaluate its cost-effectiveness of its operations (Smith, 2017).

System of Price optimisation -

It often allows the entity to select the effective price for its products in order to maximize

its productivity.

The system will help AstraZeneca to assess the belief of users on distinct clothing

products.

It is used by business to analyse how the customer’s will respond when there is a change

in the price of goods or services.

Inventory management system-

5

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

By depleting the stock, an organization can minimize its costs, maximize revenues, or

maximize benefit.

It is very useful system for organization because it will assist to preserve the records of

stock with accuracy.

It is used for by manufacturing firms to develop a work order, production related

documents and bill of materials.

D1 Management accounting system and reporting integrated with organisational process.

Most of the accounting monitoring system is connected with the managerial reporting. A

further example that works with both the regime of the cost measurement system to facilitate the

industry along with determining the exact cost of all its products (Tucker and Lowe, 2014). This

declaration could be comprehended using the instance as when the program introduced

throughout the enterprise of its stock management so all the operations linked to the inventory

could be acquired through coverage of inventory control.

TASK 2.

P3. Development of income statements as per the marginal and absorption costing.

Absorption costing- In these types of costing techniques, both variable & fixed cost are

assumed as cost of unit or even product too. This types of costing methods are mainly

used in this organisation who need to perform business activity at a greater platform

(Nitzl, 2016)(Quattrone, 2016).

Marginal costing- Here, it is necessary to take fixed cost as periodic cost whereas

variable cost is known as unit cost. Fixed cost does not change for certain period within

marginal costing.

6

maximize benefit.

It is very useful system for organization because it will assist to preserve the records of

stock with accuracy.

It is used for by manufacturing firms to develop a work order, production related

documents and bill of materials.

D1 Management accounting system and reporting integrated with organisational process.

Most of the accounting monitoring system is connected with the managerial reporting. A

further example that works with both the regime of the cost measurement system to facilitate the

industry along with determining the exact cost of all its products (Tucker and Lowe, 2014). This

declaration could be comprehended using the instance as when the program introduced

throughout the enterprise of its stock management so all the operations linked to the inventory

could be acquired through coverage of inventory control.

TASK 2.

P3. Development of income statements as per the marginal and absorption costing.

Absorption costing- In these types of costing techniques, both variable & fixed cost are

assumed as cost of unit or even product too. This types of costing methods are mainly

used in this organisation who need to perform business activity at a greater platform

(Nitzl, 2016)(Quattrone, 2016).

Marginal costing- Here, it is necessary to take fixed cost as periodic cost whereas

variable cost is known as unit cost. Fixed cost does not change for certain period within

marginal costing.

6

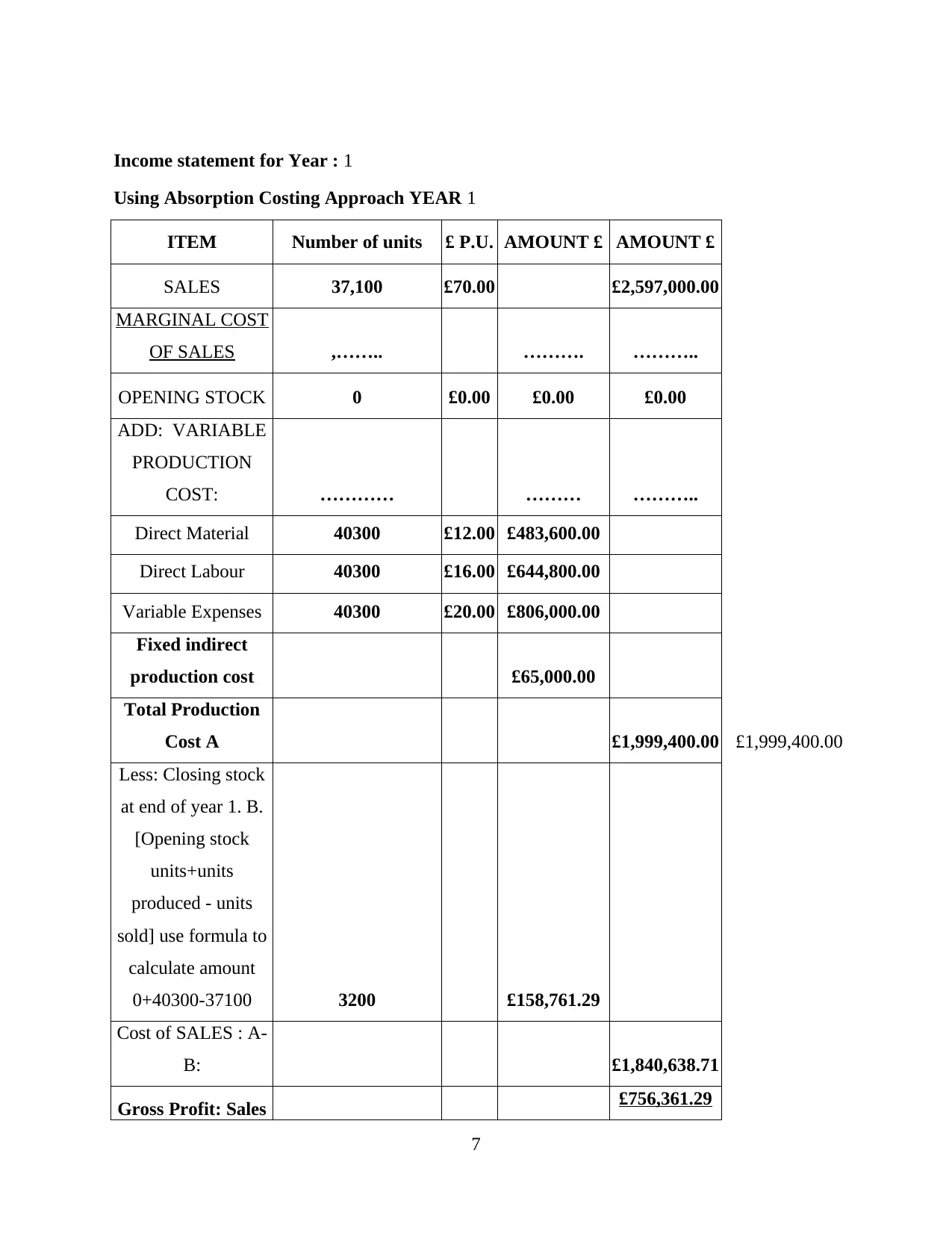

Income statement for Year : 1

Using Absorption Costing Approach YEAR 1

ITEM Number of units £ P.U. AMOUNT £ AMOUNT £

SALES 37,100 £70.00 £2,597,000.00

MARGINAL COST

OF SALES ,…….. ………. ………..

OPENING STOCK 0 £0.00 £0.00 £0.00

ADD: VARIABLE

PRODUCTION

COST: ………… ……… ………..

Direct Material 40300 £12.00 £483,600.00

Direct Labour 40300 £16.00 £644,800.00

Variable Expenses 40300 £20.00 £806,000.00

Fixed indirect

production cost £65,000.00

Total Production

Cost A £1,999,400.00 £1,999,400.00

Less: Closing stock

at end of year 1. B.

[Opening stock

units+units

produced - units

sold] use formula to

calculate amount

0+40300-37100 3200 £158,761.29

Cost of SALES : A-

B: £1,840,638.71

Gross Profit: Sales £756,361.29

7

Using Absorption Costing Approach YEAR 1

ITEM Number of units £ P.U. AMOUNT £ AMOUNT £

SALES 37,100 £70.00 £2,597,000.00

MARGINAL COST

OF SALES ,…….. ………. ………..

OPENING STOCK 0 £0.00 £0.00 £0.00

ADD: VARIABLE

PRODUCTION

COST: ………… ……… ………..

Direct Material 40300 £12.00 £483,600.00

Direct Labour 40300 £16.00 £644,800.00

Variable Expenses 40300 £20.00 £806,000.00

Fixed indirect

production cost £65,000.00

Total Production

Cost A £1,999,400.00 £1,999,400.00

Less: Closing stock

at end of year 1. B.

[Opening stock

units+units

produced - units

sold] use formula to

calculate amount

0+40300-37100 3200 £158,761.29

Cost of SALES : A-

B: £1,840,638.71

Gross Profit: Sales £756,361.29

7

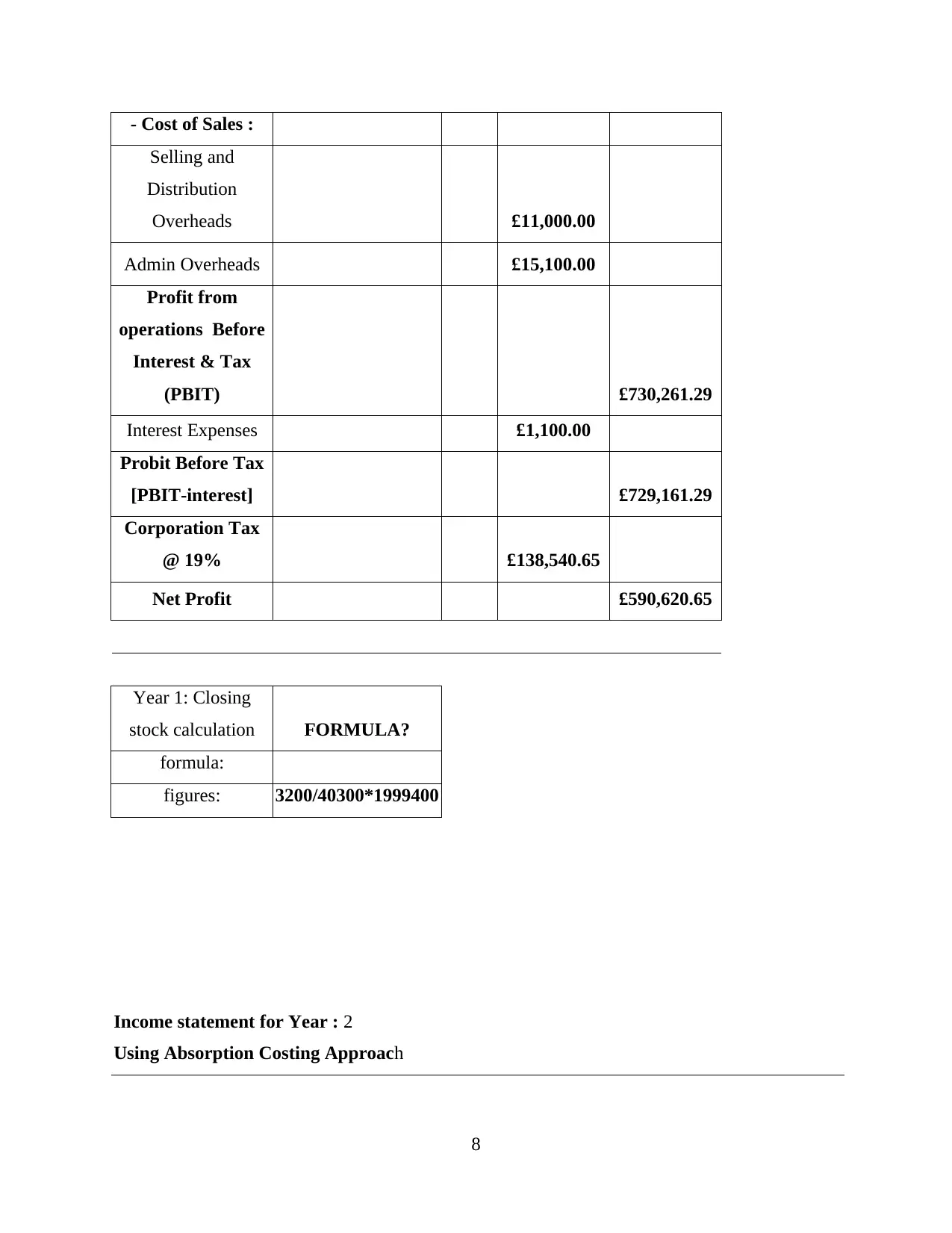

- Cost of Sales :

Selling and

Distribution

Overheads £11,000.00

Admin Overheads £15,100.00

Profit from

operations Before

Interest & Tax

(PBIT) £730,261.29

Interest Expenses £1,100.00

Probit Before Tax

[PBIT-interest] £729,161.29

Corporation Tax

@ 19% £138,540.65

Net Profit £590,620.65

Year 1: Closing

stock calculation FORMULA?

formula:

figures: 3200/40300*1999400

Income statement for Year : 2

Using Absorption Costing Approach

8

Selling and

Distribution

Overheads £11,000.00

Admin Overheads £15,100.00

Profit from

operations Before

Interest & Tax

(PBIT) £730,261.29

Interest Expenses £1,100.00

Probit Before Tax

[PBIT-interest] £729,161.29

Corporation Tax

@ 19% £138,540.65

Net Profit £590,620.65

Year 1: Closing

stock calculation FORMULA?

formula:

figures: 3200/40300*1999400

Income statement for Year : 2

Using Absorption Costing Approach

8

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

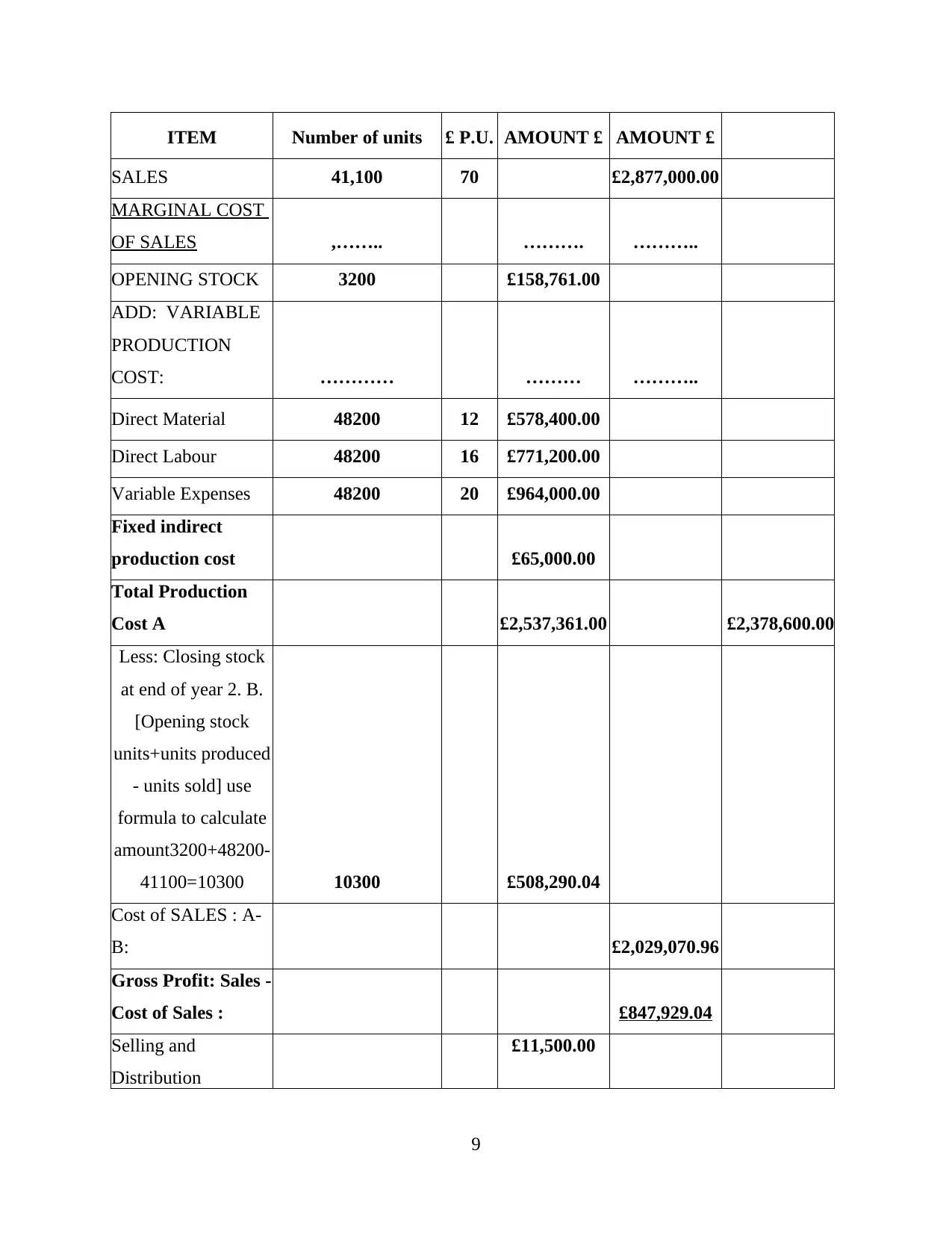

ITEM Number of units £ P.U. AMOUNT £ AMOUNT £

SALES 41,100 70 £2,877,000.00

MARGINAL COST

OF SALES ,…….. ………. ………..

OPENING STOCK 3200 £158,761.00

ADD: VARIABLE

PRODUCTION

COST: ………… ……… ………..

Direct Material 48200 12 £578,400.00

Direct Labour 48200 16 £771,200.00

Variable Expenses 48200 20 £964,000.00

Fixed indirect

production cost £65,000.00

Total Production

Cost A £2,537,361.00 £2,378,600.00

Less: Closing stock

at end of year 2. B.

[Opening stock

units+units produced

- units sold] use

formula to calculate

amount3200+48200-

41100=10300 10300 £508,290.04

Cost of SALES : A-

B: £2,029,070.96

Gross Profit: Sales -

Cost of Sales : £847,929.04

Selling and

Distribution

£11,500.00

9

SALES 41,100 70 £2,877,000.00

MARGINAL COST

OF SALES ,…….. ………. ………..

OPENING STOCK 3200 £158,761.00

ADD: VARIABLE

PRODUCTION

COST: ………… ……… ………..

Direct Material 48200 12 £578,400.00

Direct Labour 48200 16 £771,200.00

Variable Expenses 48200 20 £964,000.00

Fixed indirect

production cost £65,000.00

Total Production

Cost A £2,537,361.00 £2,378,600.00

Less: Closing stock

at end of year 2. B.

[Opening stock

units+units produced

- units sold] use

formula to calculate

amount3200+48200-

41100=10300 10300 £508,290.04

Cost of SALES : A-

B: £2,029,070.96

Gross Profit: Sales -

Cost of Sales : £847,929.04

Selling and

Distribution

£11,500.00

9

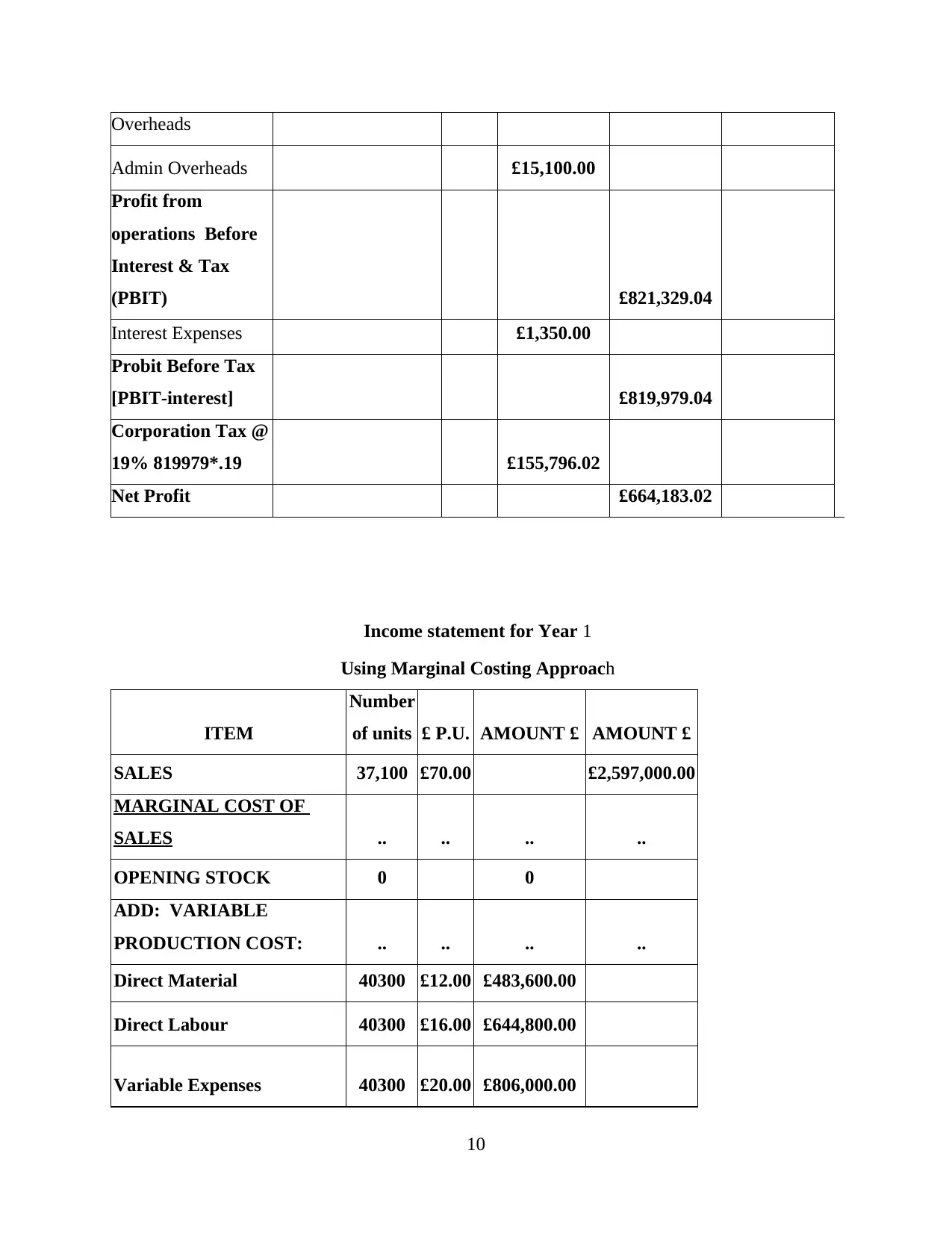

Overheads

Admin Overheads £15,100.00

Profit from

operations Before

Interest & Tax

(PBIT) £821,329.04

Interest Expenses £1,350.00

Probit Before Tax

[PBIT-interest] £819,979.04

Corporation Tax @

19% 819979*.19 £155,796.02

Net Profit £664,183.02

Income statement for Year 1

Using Marginal Costing Approach

ITEM

Number

of units £ P.U. AMOUNT £ AMOUNT £

SALES 37,100 £70.00 £2,597,000.00

MARGINAL COST OF

SALES .. .. .. ..

OPENING STOCK 0 0

ADD: VARIABLE

PRODUCTION COST: .. .. .. ..

Direct Material 40300 £12.00 £483,600.00

Direct Labour 40300 £16.00 £644,800.00

Variable Expenses 40300 £20.00 £806,000.00

10

Admin Overheads £15,100.00

Profit from

operations Before

Interest & Tax

(PBIT) £821,329.04

Interest Expenses £1,350.00

Probit Before Tax

[PBIT-interest] £819,979.04

Corporation Tax @

19% 819979*.19 £155,796.02

Net Profit £664,183.02

Income statement for Year 1

Using Marginal Costing Approach

ITEM

Number

of units £ P.U. AMOUNT £ AMOUNT £

SALES 37,100 £70.00 £2,597,000.00

MARGINAL COST OF

SALES .. .. .. ..

OPENING STOCK 0 0

ADD: VARIABLE

PRODUCTION COST: .. .. .. ..

Direct Material 40300 £12.00 £483,600.00

Direct Labour 40300 £16.00 £644,800.00

Variable Expenses 40300 £20.00 £806,000.00

10

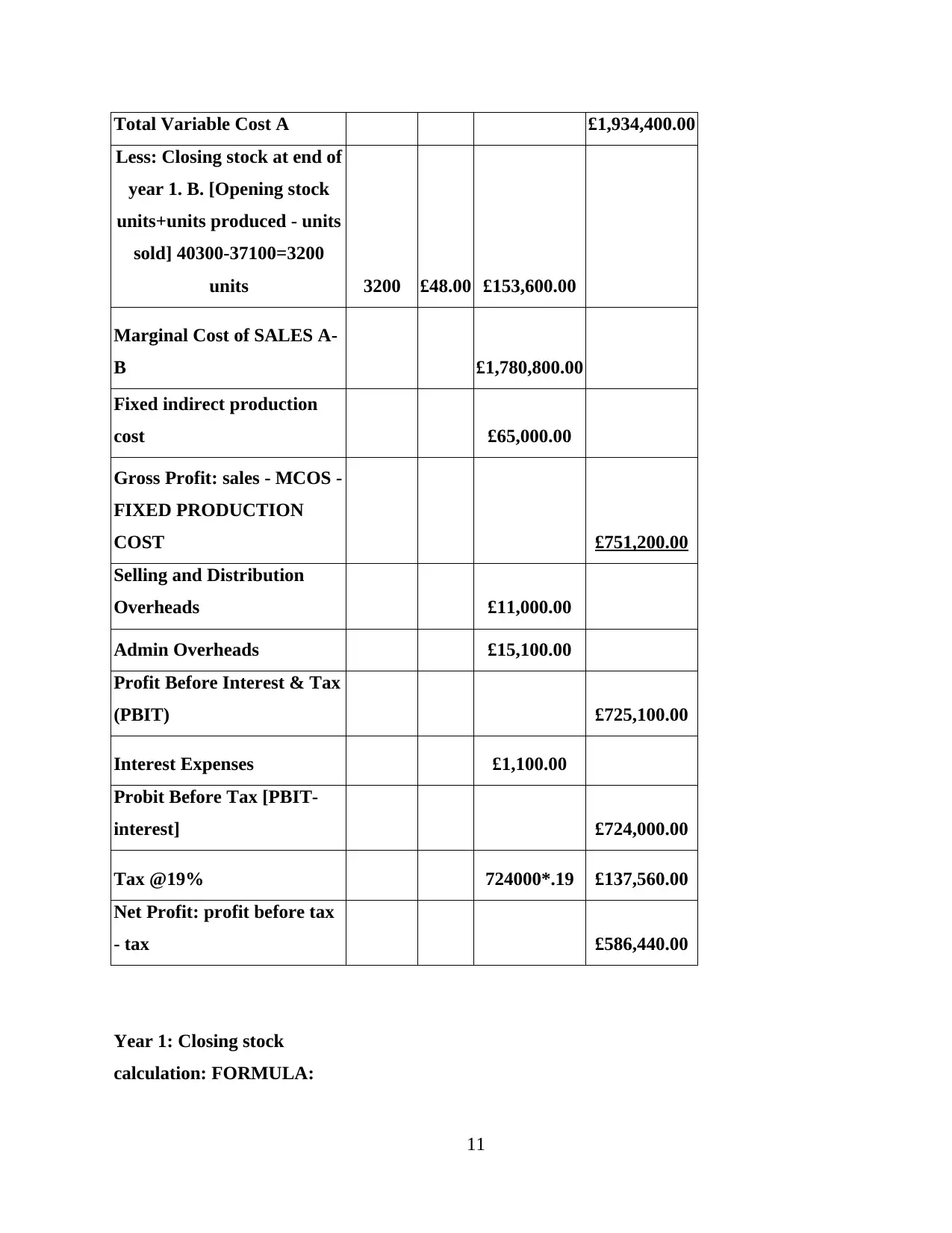

Total Variable Cost A £1,934,400.00

Less: Closing stock at end of

year 1. B. [Opening stock

units+units produced - units

sold] 40300-37100=3200

units 3200 £48.00 £153,600.00

Marginal Cost of SALES A-

B £1,780,800.00

Fixed indirect production

cost £65,000.00

Gross Profit: sales - MCOS -

FIXED PRODUCTION

COST £751,200.00

Selling and Distribution

Overheads £11,000.00

Admin Overheads £15,100.00

Profit Before Interest & Tax

(PBIT) £725,100.00

Interest Expenses £1,100.00

Probit Before Tax [PBIT-

interest] £724,000.00

Tax @19% 724000*.19 £137,560.00

Net Profit: profit before tax

- tax £586,440.00

Year 1: Closing stock

calculation: FORMULA:

11

Less: Closing stock at end of

year 1. B. [Opening stock

units+units produced - units

sold] 40300-37100=3200

units 3200 £48.00 £153,600.00

Marginal Cost of SALES A-

B £1,780,800.00

Fixed indirect production

cost £65,000.00

Gross Profit: sales - MCOS -

FIXED PRODUCTION

COST £751,200.00

Selling and Distribution

Overheads £11,000.00

Admin Overheads £15,100.00

Profit Before Interest & Tax

(PBIT) £725,100.00

Interest Expenses £1,100.00

Probit Before Tax [PBIT-

interest] £724,000.00

Tax @19% 724000*.19 £137,560.00

Net Profit: profit before tax

- tax £586,440.00

Year 1: Closing stock

calculation: FORMULA:

11

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

3200/40300*1934400=153600

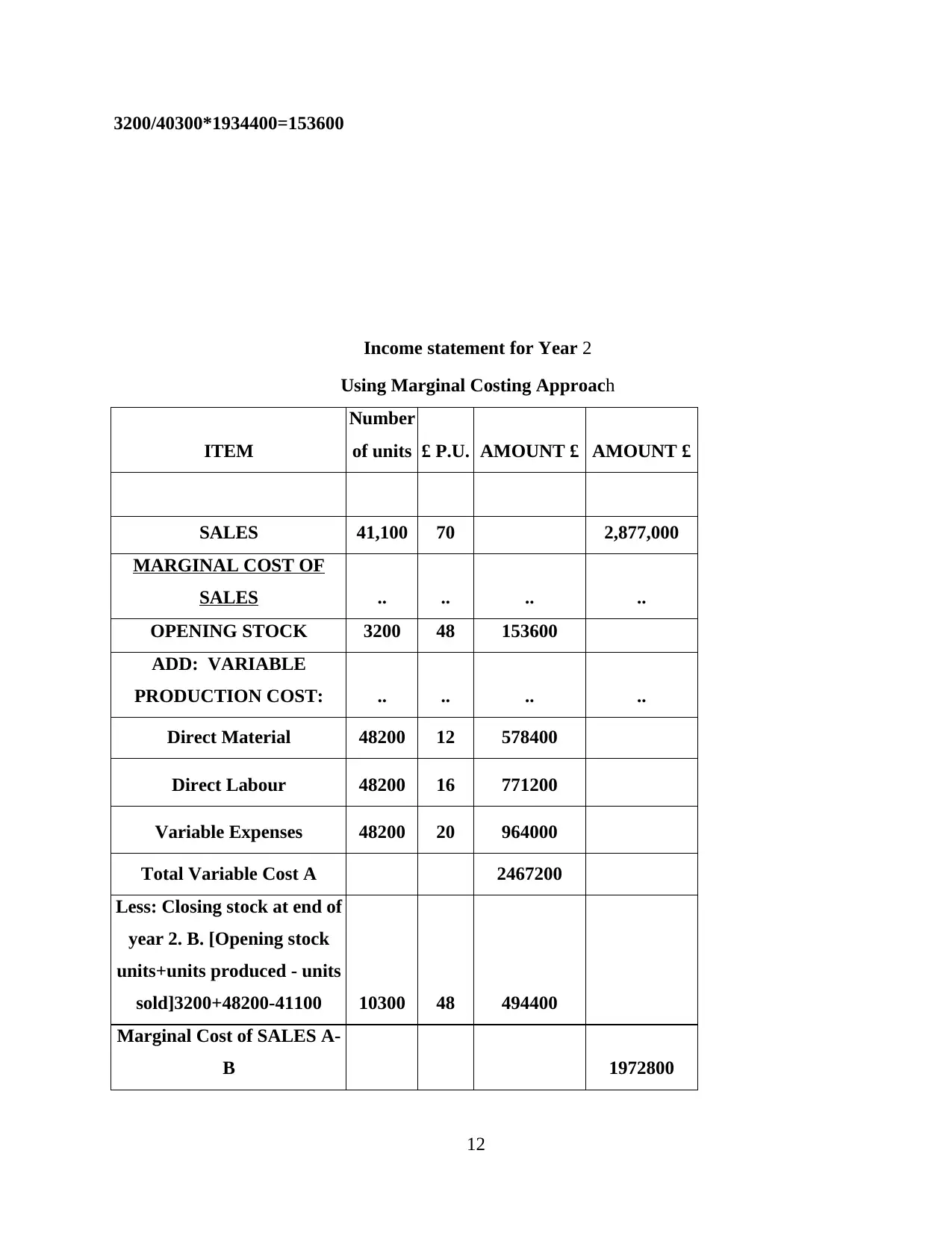

Income statement for Year 2

Using Marginal Costing Approach

ITEM

Number

of units £ P.U. AMOUNT £ AMOUNT £

SALES 41,100 70 2,877,000

MARGINAL COST OF

SALES .. .. .. ..

OPENING STOCK 3200 48 153600

ADD: VARIABLE

PRODUCTION COST: .. .. .. ..

Direct Material 48200 12 578400

Direct Labour 48200 16 771200

Variable Expenses 48200 20 964000

Total Variable Cost A 2467200

Less: Closing stock at end of

year 2. B. [Opening stock

units+units produced - units

sold]3200+48200-41100 10300 48 494400

Marginal Cost of SALES A-

B 1972800

12

Income statement for Year 2

Using Marginal Costing Approach

ITEM

Number

of units £ P.U. AMOUNT £ AMOUNT £

SALES 41,100 70 2,877,000

MARGINAL COST OF

SALES .. .. .. ..

OPENING STOCK 3200 48 153600

ADD: VARIABLE

PRODUCTION COST: .. .. .. ..

Direct Material 48200 12 578400

Direct Labour 48200 16 771200

Variable Expenses 48200 20 964000

Total Variable Cost A 2467200

Less: Closing stock at end of

year 2. B. [Opening stock

units+units produced - units

sold]3200+48200-41100 10300 48 494400

Marginal Cost of SALES A-

B 1972800

12

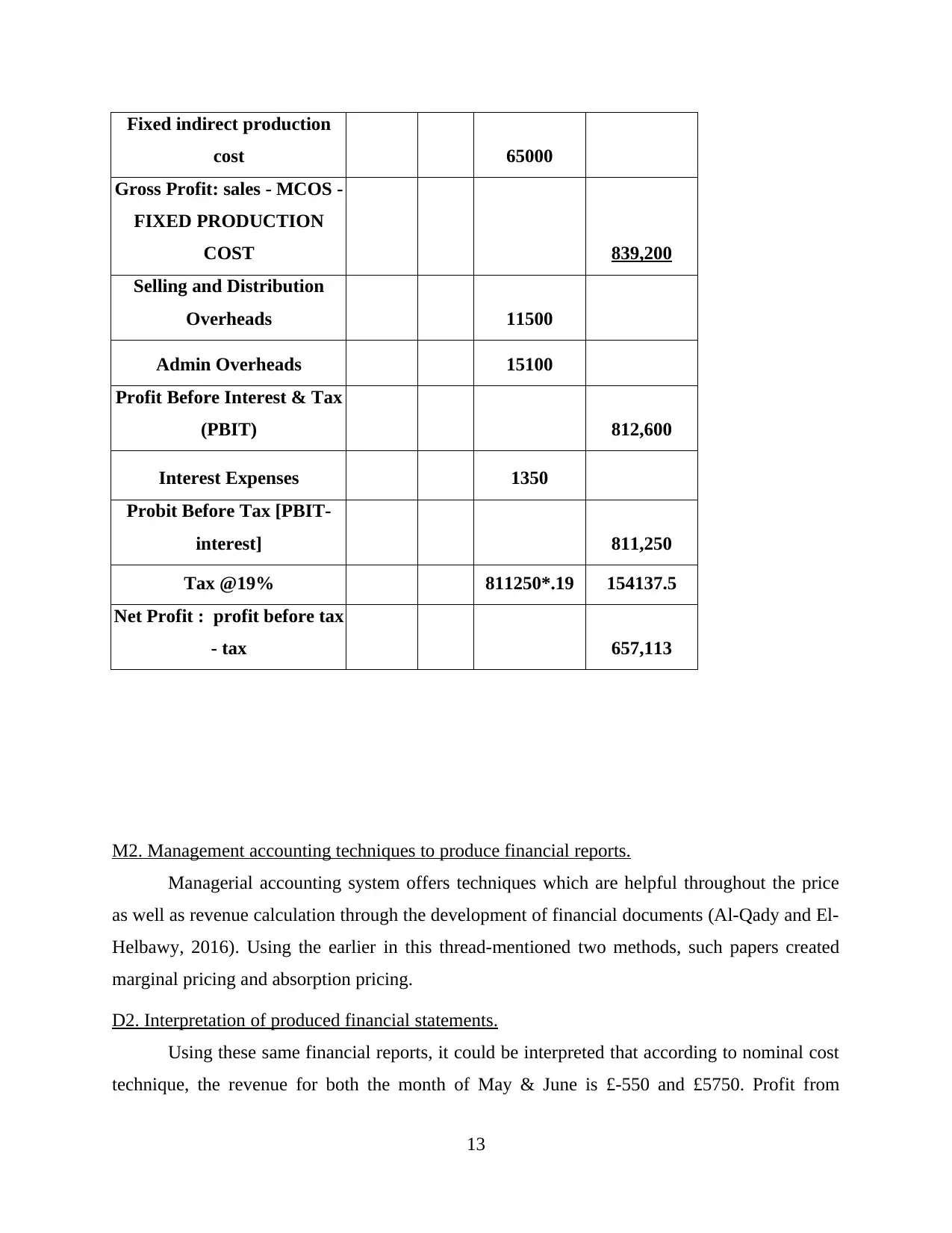

Fixed indirect production

cost 65000

Gross Profit: sales - MCOS -

FIXED PRODUCTION

COST 839,200

Selling and Distribution

Overheads 11500

Admin Overheads 15100

Profit Before Interest & Tax

(PBIT) 812,600

Interest Expenses 1350

Probit Before Tax [PBIT-

interest] 811,250

Tax @19% 811250*.19 154137.5

Net Profit : profit before tax

- tax 657,113

M2. Management accounting techniques to produce financial reports.

Managerial accounting system offers techniques which are helpful throughout the price

as well as revenue calculation through the development of financial documents (Al-Qady and El-

Helbawy, 2016). Using the earlier in this thread-mentioned two methods, such papers created

marginal pricing and absorption pricing.

D2. Interpretation of produced financial statements.

Using these same financial reports, it could be interpreted that according to nominal cost

technique, the revenue for both the month of May & June is £-550 and £5750. Profit from

13

cost 65000

Gross Profit: sales - MCOS -

FIXED PRODUCTION

COST 839,200

Selling and Distribution

Overheads 11500

Admin Overheads 15100

Profit Before Interest & Tax

(PBIT) 812,600

Interest Expenses 1350

Probit Before Tax [PBIT-

interest] 811,250

Tax @19% 811250*.19 154137.5

Net Profit : profit before tax

- tax 657,113

M2. Management accounting techniques to produce financial reports.

Managerial accounting system offers techniques which are helpful throughout the price

as well as revenue calculation through the development of financial documents (Al-Qady and El-

Helbawy, 2016). Using the earlier in this thread-mentioned two methods, such papers created

marginal pricing and absorption pricing.

D2. Interpretation of produced financial statements.

Using these same financial reports, it could be interpreted that according to nominal cost

technique, the revenue for both the month of May & June is £-550 and £5750. Profit from

13

absorption costing is calculated as £-630 and £4550. June profits is greater as retail earnings in

the month are greater. AstraZeneca is suggested which they embrace the absorption costing

technique instead of the marginal technique when they correctly distribute most of the internal

and external costs with such a technique. Such methods are helpful to both the business because

it will assist them to evaluate the commercial ' competitiveness.

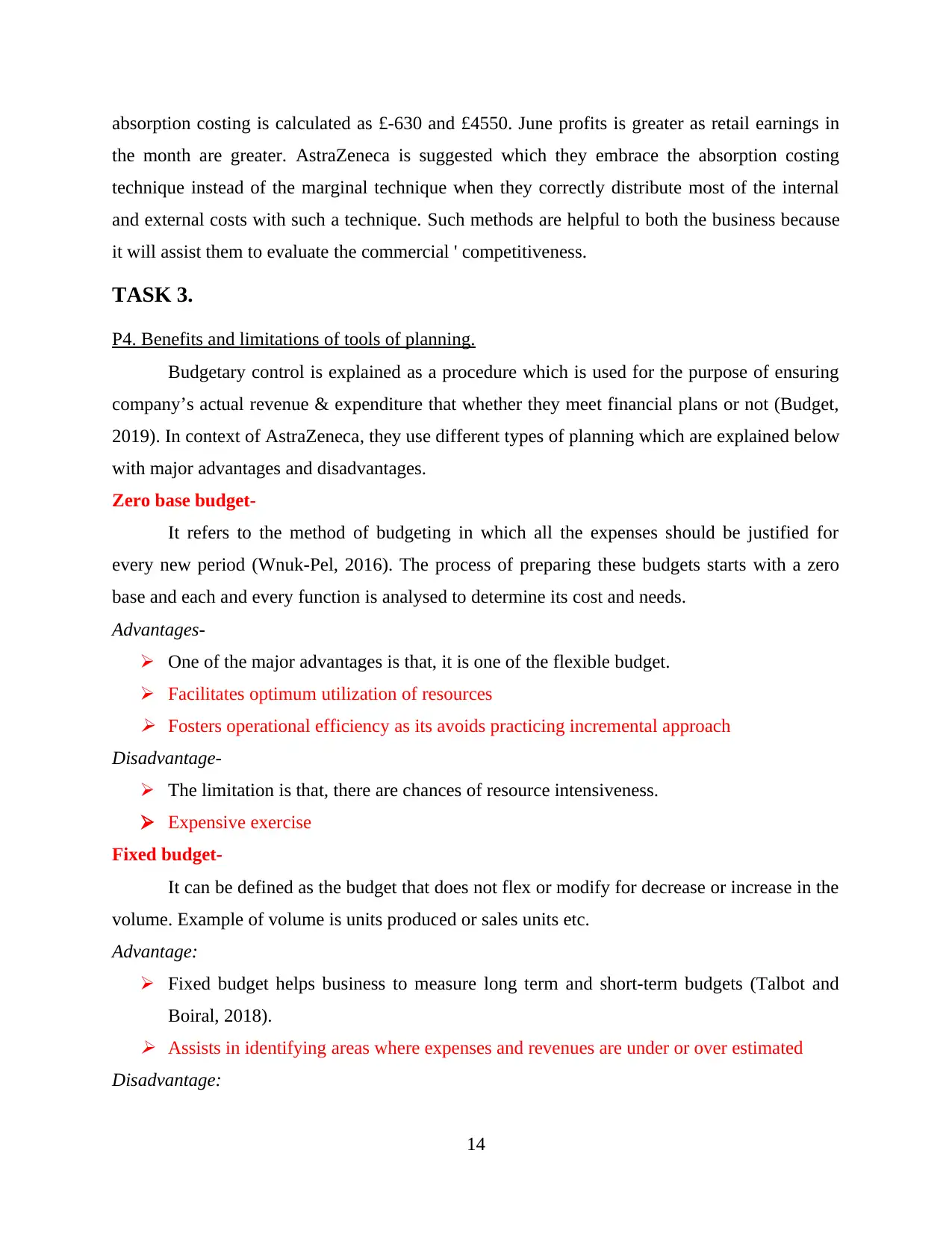

TASK 3.

P4. Benefits and limitations of tools of planning.

Budgetary control is explained as a procedure which is used for the purpose of ensuring

company’s actual revenue & expenditure that whether they meet financial plans or not (Budget,

2019). In context of AstraZeneca, they use different types of planning which are explained below

with major advantages and disadvantages.

Zero base budget-

It refers to the method of budgeting in which all the expenses should be justified for

every new period (Wnuk-Pel, 2016). The process of preparing these budgets starts with a zero

base and each and every function is analysed to determine its cost and needs.

Advantages-

One of the major advantages is that, it is one of the flexible budget.

Facilitates optimum utilization of resources Fosters operational efficiency as its avoids practicing incremental approach

Disadvantage-

The limitation is that, there are chances of resource intensiveness.

Expensive exercise

Fixed budget-

It can be defined as the budget that does not flex or modify for decrease or increase in the

volume. Example of volume is units produced or sales units etc.

Advantage:

Fixed budget helps business to measure long term and short-term budgets (Talbot and

Boiral, 2018). Assists in identifying areas where expenses and revenues are under or over estimated

Disadvantage:

14

the month are greater. AstraZeneca is suggested which they embrace the absorption costing

technique instead of the marginal technique when they correctly distribute most of the internal

and external costs with such a technique. Such methods are helpful to both the business because

it will assist them to evaluate the commercial ' competitiveness.

TASK 3.

P4. Benefits and limitations of tools of planning.

Budgetary control is explained as a procedure which is used for the purpose of ensuring

company’s actual revenue & expenditure that whether they meet financial plans or not (Budget,

2019). In context of AstraZeneca, they use different types of planning which are explained below

with major advantages and disadvantages.

Zero base budget-

It refers to the method of budgeting in which all the expenses should be justified for

every new period (Wnuk-Pel, 2016). The process of preparing these budgets starts with a zero

base and each and every function is analysed to determine its cost and needs.

Advantages-

One of the major advantages is that, it is one of the flexible budget.

Facilitates optimum utilization of resources Fosters operational efficiency as its avoids practicing incremental approach

Disadvantage-

The limitation is that, there are chances of resource intensiveness.

Expensive exercise

Fixed budget-

It can be defined as the budget that does not flex or modify for decrease or increase in the

volume. Example of volume is units produced or sales units etc.

Advantage:

Fixed budget helps business to measure long term and short-term budgets (Talbot and

Boiral, 2018). Assists in identifying areas where expenses and revenues are under or over estimated

Disadvantage:

14

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

Limitation is that, it does not consider unpredictable events.

This budget is lacking flexibility

Flexible Budget:

It refers to the budget that flexes or adjusts with the change in activity or volume. It is

more refined and useful as compared with static budget.

Advantage-

It helps to determine the amount or quantity of output to be produced by organisation to

attain desired level of profits.

Helps in developing appropriate budget for specific activities.

Disadvantage-

It is a time-consuming process.

These are some of the planning tools which are being used within AstraZeneca. It has

been giving them the idea that where they need to invest their capital within the organisation.

Variance Analysis

It is one of the most effectual planning tool that can be undertaken by Astra Zeneca for

planning purpose. Moreover, such tool clearly exhibits deviation that take place in organizational

performance along with the causes. Thus, by taking into account assessed causes manager of

Astra Zeneca can set suitable and realistic standards for the upcoming time period.

Advantage-

It helps to identify the reasons behind variance in expenses and income of the present

year from budgeted values.

Disadvantage-

It requires long time to evaluate the impact of variance.

Such budgeting tool highly relies on the assumption of continuity which in turn not

appropriate. This in turn limits significance of variance analysis tool to a great extent.

Ratio analysis

By doing analysis, it has been assessed that ratio analysis tool makes significant

contribution in the assessing the liquidity, profitability, solvency and the leverage position of the

company. Through this tool a company could compare its current results with the results of the

past period.

Advantage-

15

This budget is lacking flexibility

Flexible Budget:

It refers to the budget that flexes or adjusts with the change in activity or volume. It is

more refined and useful as compared with static budget.

Advantage-

It helps to determine the amount or quantity of output to be produced by organisation to

attain desired level of profits.

Helps in developing appropriate budget for specific activities.

Disadvantage-

It is a time-consuming process.

These are some of the planning tools which are being used within AstraZeneca. It has

been giving them the idea that where they need to invest their capital within the organisation.

Variance Analysis

It is one of the most effectual planning tool that can be undertaken by Astra Zeneca for

planning purpose. Moreover, such tool clearly exhibits deviation that take place in organizational

performance along with the causes. Thus, by taking into account assessed causes manager of

Astra Zeneca can set suitable and realistic standards for the upcoming time period.

Advantage-

It helps to identify the reasons behind variance in expenses and income of the present

year from budgeted values.

Disadvantage-

It requires long time to evaluate the impact of variance.

Such budgeting tool highly relies on the assumption of continuity which in turn not

appropriate. This in turn limits significance of variance analysis tool to a great extent.

Ratio analysis

By doing analysis, it has been assessed that ratio analysis tool makes significant

contribution in the assessing the liquidity, profitability, solvency and the leverage position of the

company. Through this tool a company could compare its current results with the results of the

past period.

Advantage-

15

It helps in forecasting, budgeting, measurement of operational efficiency.

Help in measuring performance and gives indication about areas where improvements are

needed.

Disadvantage-

The organisation can make improvements to improve their financial ratios. It is based on past performance whereas business unit is concerning about future.

Capital budgeting:

In addition to this, planning can also be done by business unit by taking into account capital

budgeting tools and techniques. Moreover, such tools offer opportunity in relation to identifying

whether proposed investment will aid in company’s growth in terms of both monetary and non-

monetary. Specifically, capital budgeting tool includes payback period, net present value,

average and internal rate of return. Hence, with the help of different tools manager of the firm

can identify programs, projects and other investment options which in turn proves to be more

beneficial in long run.

For example: Business unit is having two options for investment purpose. In this regard,

with the motive to prioritize projects according to profitability or monetary aspects capital

budgeting tools have been applied.

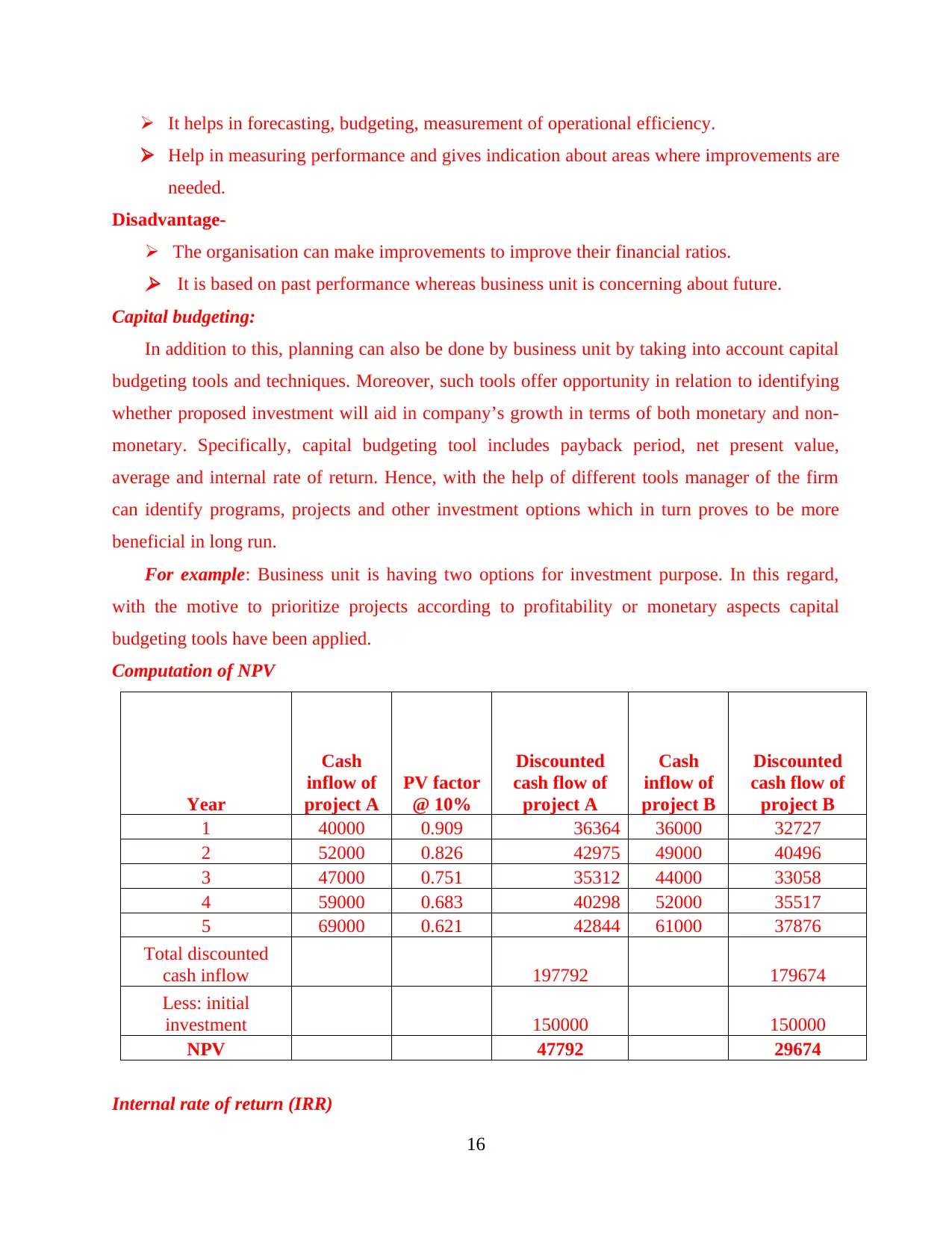

Computation of NPV

Year

Cash

inflow of

project A

PV factor

@ 10%

Discounted

cash flow of

project A

Cash

inflow of

project B

Discounted

cash flow of

project B

1 40000 0.909 36364 36000 32727

2 52000 0.826 42975 49000 40496

3 47000 0.751 35312 44000 33058

4 59000 0.683 40298 52000 35517

5 69000 0.621 42844 61000 37876

Total discounted

cash inflow 197792 179674

Less: initial

investment 150000 150000

NPV 47792 29674

Internal rate of return (IRR)

16

Help in measuring performance and gives indication about areas where improvements are

needed.

Disadvantage-

The organisation can make improvements to improve their financial ratios. It is based on past performance whereas business unit is concerning about future.

Capital budgeting:

In addition to this, planning can also be done by business unit by taking into account capital

budgeting tools and techniques. Moreover, such tools offer opportunity in relation to identifying

whether proposed investment will aid in company’s growth in terms of both monetary and non-

monetary. Specifically, capital budgeting tool includes payback period, net present value,

average and internal rate of return. Hence, with the help of different tools manager of the firm

can identify programs, projects and other investment options which in turn proves to be more

beneficial in long run.

For example: Business unit is having two options for investment purpose. In this regard,

with the motive to prioritize projects according to profitability or monetary aspects capital

budgeting tools have been applied.

Computation of NPV

Year

Cash

inflow of

project A

PV factor

@ 10%

Discounted

cash flow of

project A

Cash

inflow of

project B

Discounted

cash flow of

project B

1 40000 0.909 36364 36000 32727

2 52000 0.826 42975 49000 40496

3 47000 0.751 35312 44000 33058

4 59000 0.683 40298 52000 35517

5 69000 0.621 42844 61000 37876

Total discounted

cash inflow 197792 179674

Less: initial

investment 150000 150000

NPV 47792 29674

Internal rate of return (IRR)

16

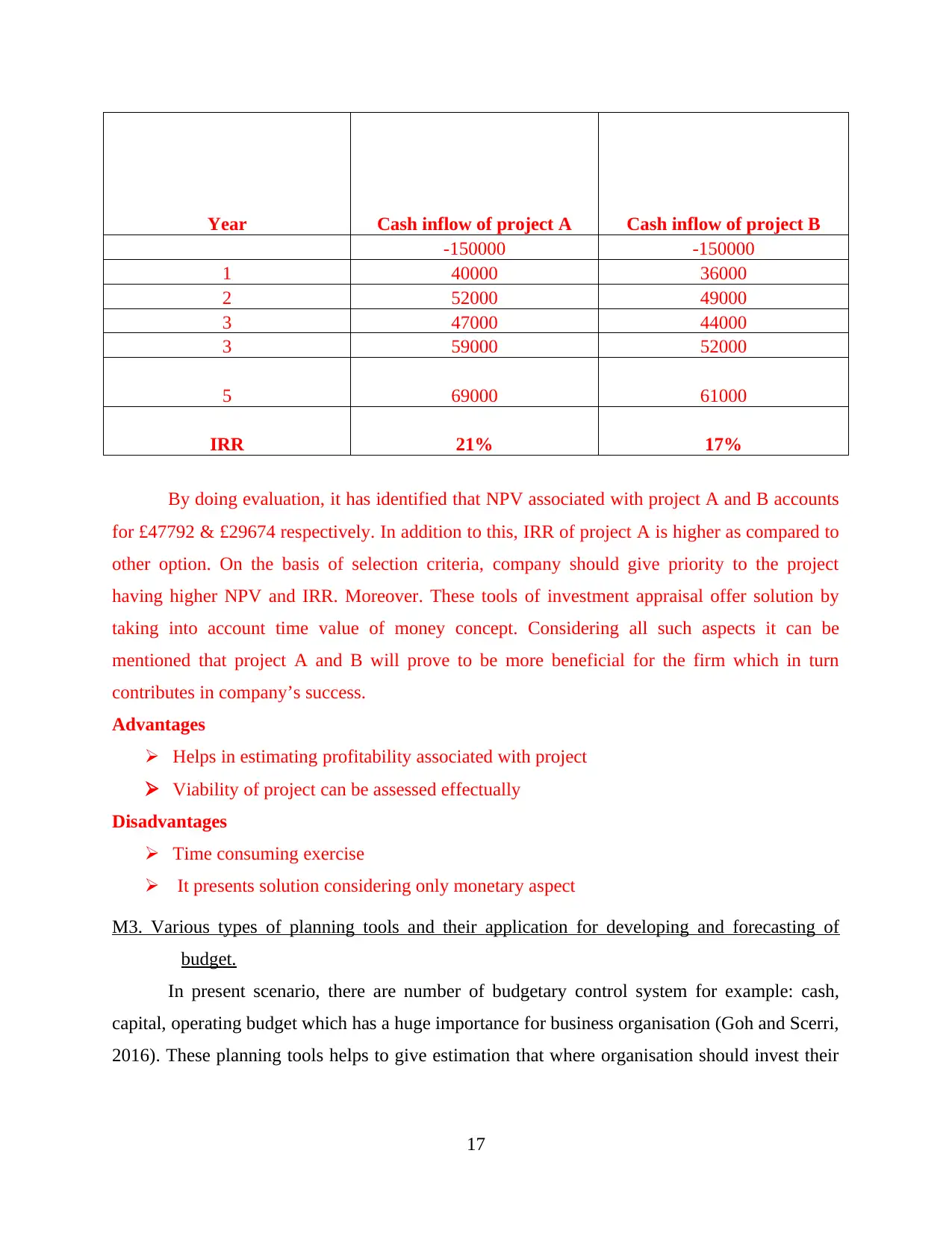

Year Cash inflow of project A Cash inflow of project B

-150000 -150000

1 40000 36000

2 52000 49000

3 47000 44000

3 59000 52000

5 69000 61000

IRR 21% 17%

By doing evaluation, it has identified that NPV associated with project A and B accounts

for £47792 & £29674 respectively. In addition to this, IRR of project A is higher as compared to

other option. On the basis of selection criteria, company should give priority to the project

having higher NPV and IRR. Moreover. These tools of investment appraisal offer solution by

taking into account time value of money concept. Considering all such aspects it can be

mentioned that project A and B will prove to be more beneficial for the firm which in turn

contributes in company’s success.

Advantages

Helps in estimating profitability associated with project

Viability of project can be assessed effectually

Disadvantages

Time consuming exercise

It presents solution considering only monetary aspect

M3. Various types of planning tools and their application for developing and forecasting of

budget.

In present scenario, there are number of budgetary control system for example: cash,

capital, operating budget which has a huge importance for business organisation (Goh and Scerri,

2016). These planning tools helps to give estimation that where organisation should invest their

17

-150000 -150000

1 40000 36000

2 52000 49000

3 47000 44000

3 59000 52000

5 69000 61000

IRR 21% 17%

By doing evaluation, it has identified that NPV associated with project A and B accounts

for £47792 & £29674 respectively. In addition to this, IRR of project A is higher as compared to

other option. On the basis of selection criteria, company should give priority to the project

having higher NPV and IRR. Moreover. These tools of investment appraisal offer solution by

taking into account time value of money concept. Considering all such aspects it can be

mentioned that project A and B will prove to be more beneficial for the firm which in turn

contributes in company’s success.

Advantages

Helps in estimating profitability associated with project

Viability of project can be assessed effectually

Disadvantages

Time consuming exercise

It presents solution considering only monetary aspect

M3. Various types of planning tools and their application for developing and forecasting of

budget.

In present scenario, there are number of budgetary control system for example: cash,

capital, operating budget which has a huge importance for business organisation (Goh and Scerri,

2016). These planning tools helps to give estimation that where organisation should invest their

17

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

money so that they can perform in a systematic manner. Company gets the idea that where they

should invest capital so that they can earn profit in future period of time.

TASK 4.

P5. Comparison of companies to solve the financial issues with the help of systems of

accounting.

Financial issue is explained as the condition where organisation have to suffer from

different problem just because of lack of fund available. (West, 2018). There are some of the

financial issues which are going on within AstraZeneca and they have been discussed below: Higher Expenses as Compared to Profit: In this type of financial issues company have

to suffer to suffer from losses as their expenses increases due to which profit reduces

automatically. Here, AstraZeneca is unable to work according to plan and policy due to

which their daily expenses have increases and company is unable to meet their targets.

Inconsistency in Sales: It is one of the financial issues where organization doesn't find

the way to sale their product due to which they have to suffer from losses. In context of

AstraZeneca, they are also facing the problem of inconsistency in sales and the major

reason is that price fluctuation of profit. It has been impacting on their profitability ratio

as well because it is decreasing at a higher speed. Financial Governance: It is referred as a situation where organisation needs to collect

manage, monitor & control all of the financial information and transaction of company. It

is helpful because it will give the idea that how organisation can sort out issues which

they are faced in company. In context of AstraZeneca Company, they are needed to

ensure that they use financial governance because it will give them the idea that how they

need to utilise the financial resources of a company.

Methods for deducting financial issues

Benchmarking: It can be explained as the method of comparison where top level

management need to compare whole of the plans and policies, strategies & other

operational performance with similar form of organization so that accurate reasons can be

obtained (Jefrey, 2018). According to this technique, by doing comparison of actual

performance in against to standard business unit can identify deficiencies. Thus, by

evaluating areas of deviations firm can take corrective measure for improvement.

18

should invest capital so that they can earn profit in future period of time.

TASK 4.

P5. Comparison of companies to solve the financial issues with the help of systems of

accounting.

Financial issue is explained as the condition where organisation have to suffer from

different problem just because of lack of fund available. (West, 2018). There are some of the

financial issues which are going on within AstraZeneca and they have been discussed below: Higher Expenses as Compared to Profit: In this type of financial issues company have

to suffer to suffer from losses as their expenses increases due to which profit reduces

automatically. Here, AstraZeneca is unable to work according to plan and policy due to

which their daily expenses have increases and company is unable to meet their targets.

Inconsistency in Sales: It is one of the financial issues where organization doesn't find

the way to sale their product due to which they have to suffer from losses. In context of

AstraZeneca, they are also facing the problem of inconsistency in sales and the major

reason is that price fluctuation of profit. It has been impacting on their profitability ratio

as well because it is decreasing at a higher speed. Financial Governance: It is referred as a situation where organisation needs to collect

manage, monitor & control all of the financial information and transaction of company. It

is helpful because it will give the idea that how organisation can sort out issues which

they are faced in company. In context of AstraZeneca Company, they are needed to

ensure that they use financial governance because it will give them the idea that how they

need to utilise the financial resources of a company.

Methods for deducting financial issues

Benchmarking: It can be explained as the method of comparison where top level

management need to compare whole of the plans and policies, strategies & other

operational performance with similar form of organization so that accurate reasons can be

obtained (Jefrey, 2018). According to this technique, by doing comparison of actual

performance in against to standard business unit can identify deficiencies. Thus, by

evaluating areas of deviations firm can take corrective measure for improvement.

18

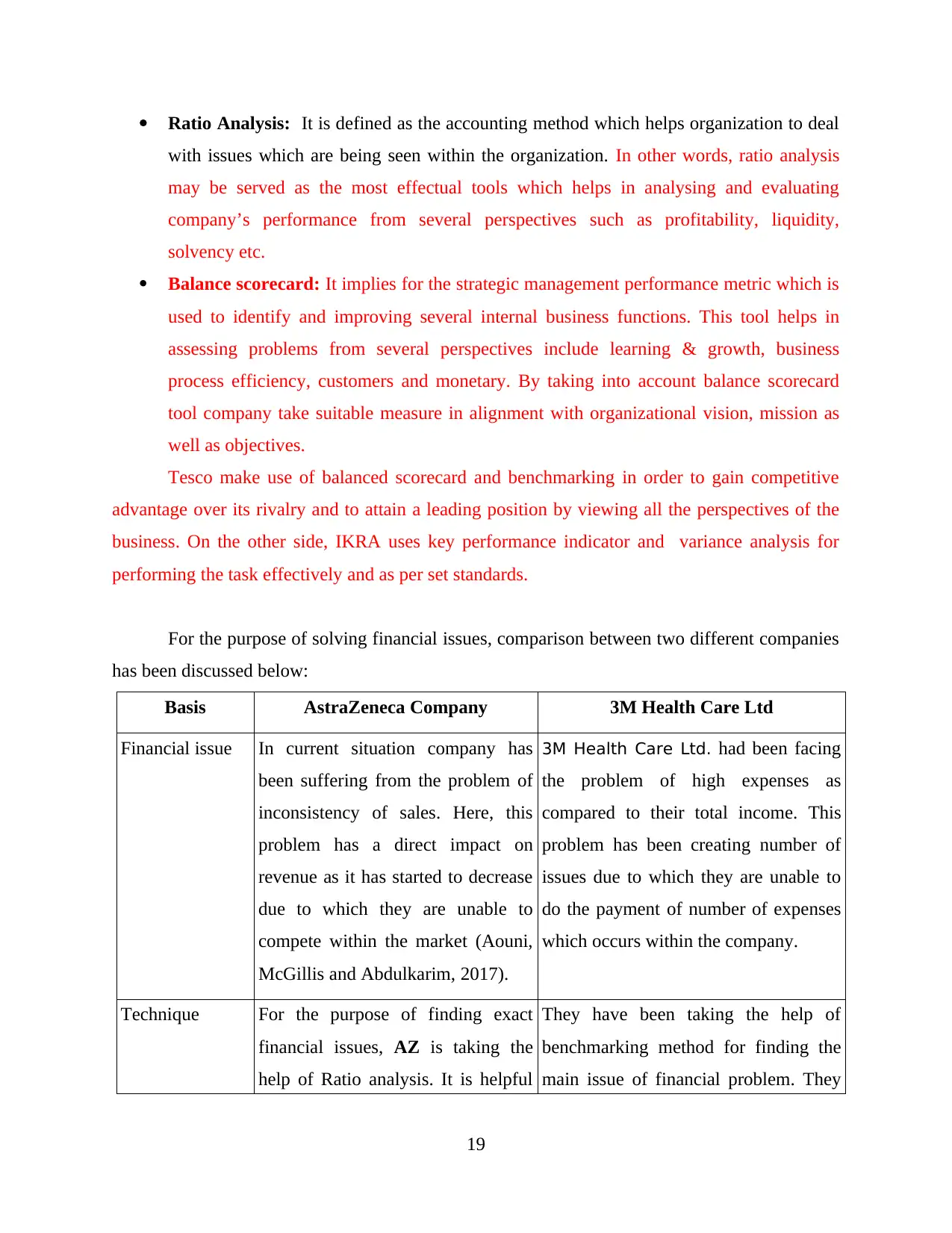

Ratio Analysis: It is defined as the accounting method which helps organization to deal

with issues which are being seen within the organization. In other words, ratio analysis

may be served as the most effectual tools which helps in analysing and evaluating

company’s performance from several perspectives such as profitability, liquidity,

solvency etc.

Balance scorecard: It implies for the strategic management performance metric which is

used to identify and improving several internal business functions. This tool helps in

assessing problems from several perspectives include learning & growth, business

process efficiency, customers and monetary. By taking into account balance scorecard

tool company take suitable measure in alignment with organizational vision, mission as

well as objectives.

Tesco make use of balanced scorecard and benchmarking in order to gain competitive

advantage over its rivalry and to attain a leading position by viewing all the perspectives of the

business. On the other side, IKRA uses key performance indicator and variance analysis for

performing the task effectively and as per set standards.

For the purpose of solving financial issues, comparison between two different companies

has been discussed below:

Basis AstraZeneca Company 3M Health Care Ltd

Financial issue In current situation company has

been suffering from the problem of

inconsistency of sales. Here, this

problem has a direct impact on

revenue as it has started to decrease

due to which they are unable to

compete within the market (Aouni,

McGillis and Abdulkarim, 2017).

3M Health Care Ltd. had been facing

the problem of high expenses as

compared to their total income. This

problem has been creating number of

issues due to which they are unable to

do the payment of number of expenses

which occurs within the company.

Technique For the purpose of finding exact

financial issues, AZ is taking the

help of Ratio analysis. It is helpful

They have been taking the help of

benchmarking method for finding the

main issue of financial problem. They

19

with issues which are being seen within the organization. In other words, ratio analysis

may be served as the most effectual tools which helps in analysing and evaluating

company’s performance from several perspectives such as profitability, liquidity,

solvency etc.

Balance scorecard: It implies for the strategic management performance metric which is

used to identify and improving several internal business functions. This tool helps in

assessing problems from several perspectives include learning & growth, business

process efficiency, customers and monetary. By taking into account balance scorecard

tool company take suitable measure in alignment with organizational vision, mission as

well as objectives.

Tesco make use of balanced scorecard and benchmarking in order to gain competitive

advantage over its rivalry and to attain a leading position by viewing all the perspectives of the

business. On the other side, IKRA uses key performance indicator and variance analysis for

performing the task effectively and as per set standards.

For the purpose of solving financial issues, comparison between two different companies

has been discussed below:

Basis AstraZeneca Company 3M Health Care Ltd

Financial issue In current situation company has

been suffering from the problem of

inconsistency of sales. Here, this

problem has a direct impact on

revenue as it has started to decrease

due to which they are unable to

compete within the market (Aouni,

McGillis and Abdulkarim, 2017).

3M Health Care Ltd. had been facing

the problem of high expenses as

compared to their total income. This

problem has been creating number of

issues due to which they are unable to

do the payment of number of expenses

which occurs within the company.

Technique For the purpose of finding exact

financial issues, AZ is taking the

help of Ratio analysis. It is helpful

They have been taking the help of

benchmarking method for finding the

main issue of financial problem. They

19

for them because it helps to

calculate all the ratios and according

to that it does analysis.

have been using this method because it

compares with another organisation

working in similar field.

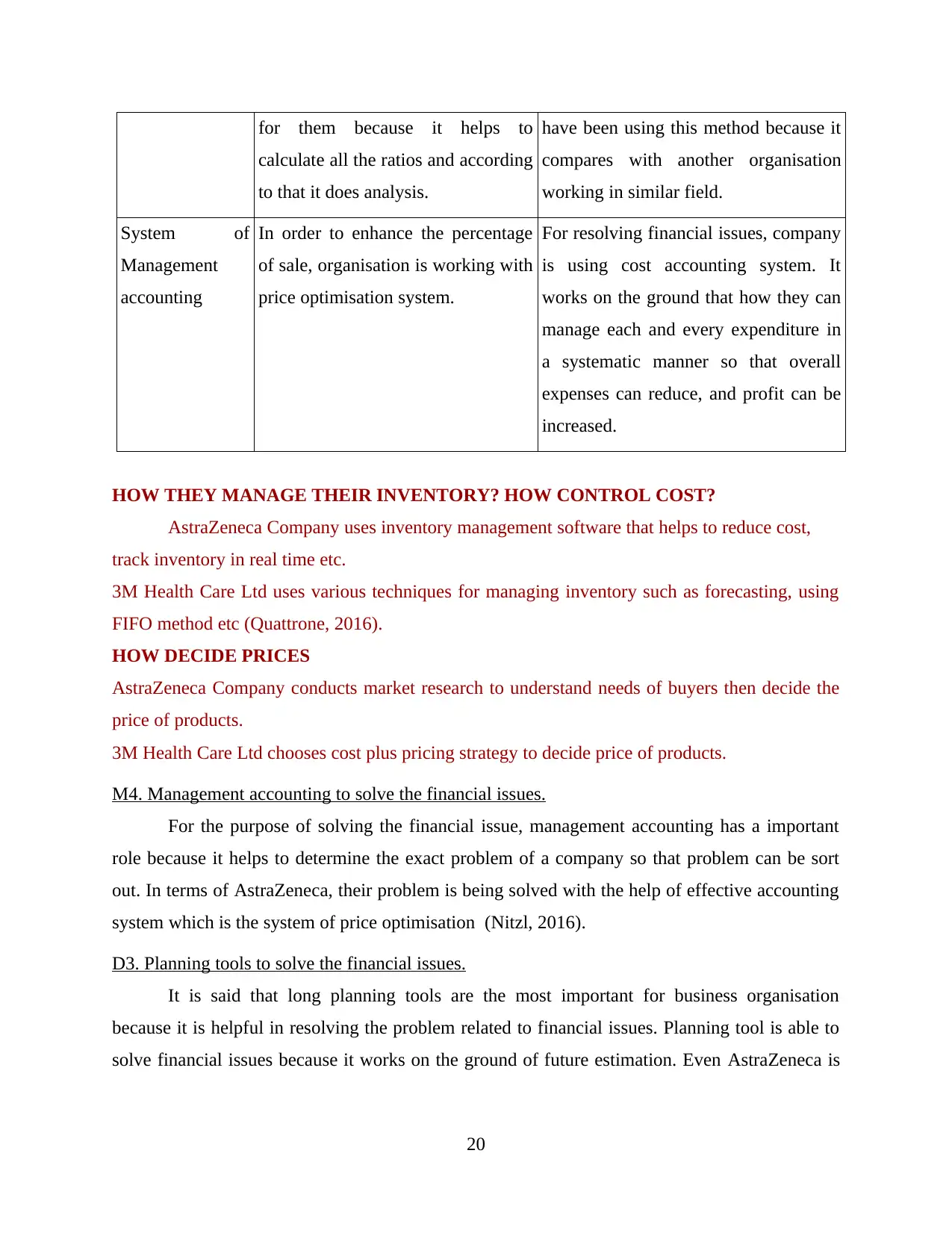

System of

Management

accounting

In order to enhance the percentage

of sale, organisation is working with

price optimisation system.

For resolving financial issues, company

is using cost accounting system. It

works on the ground that how they can

manage each and every expenditure in

a systematic manner so that overall

expenses can reduce, and profit can be

increased.

HOW THEY MANAGE THEIR INVENTORY? HOW CONTROL COST?

AstraZeneca Company uses inventory management software that helps to reduce cost,

track inventory in real time etc.

3M Health Care Ltd uses various techniques for managing inventory such as forecasting, using

FIFO method etc (Quattrone, 2016).

HOW DECIDE PRICES

AstraZeneca Company conducts market research to understand needs of buyers then decide the

price of products.

3M Health Care Ltd chooses cost plus pricing strategy to decide price of products.

M4. Management accounting to solve the financial issues.

For the purpose of solving the financial issue, management accounting has a important

role because it helps to determine the exact problem of a company so that problem can be sort

out. In terms of AstraZeneca, their problem is being solved with the help of effective accounting

system which is the system of price optimisation (Nitzl, 2016).

D3. Planning tools to solve the financial issues.

It is said that long planning tools are the most important for business organisation

because it is helpful in resolving the problem related to financial issues. Planning tool is able to

solve financial issues because it works on the ground of future estimation. Even AstraZeneca is

20

calculate all the ratios and according

to that it does analysis.

have been using this method because it

compares with another organisation

working in similar field.

System of

Management

accounting

In order to enhance the percentage

of sale, organisation is working with

price optimisation system.

For resolving financial issues, company

is using cost accounting system. It

works on the ground that how they can

manage each and every expenditure in

a systematic manner so that overall

expenses can reduce, and profit can be

increased.

HOW THEY MANAGE THEIR INVENTORY? HOW CONTROL COST?

AstraZeneca Company uses inventory management software that helps to reduce cost,

track inventory in real time etc.

3M Health Care Ltd uses various techniques for managing inventory such as forecasting, using

FIFO method etc (Quattrone, 2016).

HOW DECIDE PRICES

AstraZeneca Company conducts market research to understand needs of buyers then decide the

price of products.

3M Health Care Ltd chooses cost plus pricing strategy to decide price of products.

M4. Management accounting to solve the financial issues.

For the purpose of solving the financial issue, management accounting has a important

role because it helps to determine the exact problem of a company so that problem can be sort

out. In terms of AstraZeneca, their problem is being solved with the help of effective accounting

system which is the system of price optimisation (Nitzl, 2016).

D3. Planning tools to solve the financial issues.

It is said that long planning tools are the most important for business organisation

because it is helpful in resolving the problem related to financial issues. Planning tool is able to

solve financial issues because it works on the ground of future estimation. Even AstraZeneca is

20

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

also using the planning tools which has been helping them to do estimation which even reduces

their problem.

21

their problem.

21

CONCLUSION

As per understanding of above file, it is analysed that management accounting is the

important element of business organisation which help to proper analysis through which business

decisions can be easily taken. Different business organisation uses different types of accounting

system for the purpose of finding actual position of a company. Business organisation uses

various types of budgeting system for doing future planning within the organisation. Whenever

business faces problem they use different types of accounting techniques through which

problems can be easily resolved.

22

As per understanding of above file, it is analysed that management accounting is the

important element of business organisation which help to proper analysis through which business

decisions can be easily taken. Different business organisation uses different types of accounting

system for the purpose of finding actual position of a company. Business organisation uses

various types of budgeting system for doing future planning within the organisation. Whenever

business faces problem they use different types of accounting techniques through which

problems can be easily resolved.

22

REFERENCES

Books & Journals

Al-Qady, M. and El-Helbawy, S., 2016. Integrating Target Costing and Resource Consumption

Accounting. Journal of Applied Management Accounting Research. 14(1).

Aouni, B., McGillis, S. and Abdulkarim, M. E., 2017. Goal programming model for management

accounting and auditing: a new typology. Annals of Operations Research. 251(1-2).

pp.41-54.

Chenhall, R. H. and Moers, F., 2015. The role of innovation in the evolution of management

accounting and its integration into management control. Accounting, organizations and

society. 47. pp.1-13.

Englund, H. and Gerdin, J., 2014. Structuration theory in accounting research: Applications and

applicability. Critical Perspectives on Accounting. 25(2). pp.162-180.

Goh, E. and Scerri, M., 2016. “I study accounting because I have to”: An exploratory study of

hospitality students’ attitudes toward accounting education. Journal of Hospitality &

Tourism Education. 28(2). pp.85-94.

Jefrey, C. ed., 2018. Research on professional responsibility and ethics in accounting. Emerald

Publishing Limited.

Maas, K., Schaltegger, S. and Crutzen, N., 2016. Integrating corporate sustainability assessment,

management accounting, control, and reporting. Journal of Cleaner Production. 136.

pp.237-248.

Melnyk, S. A. and et.al., 2014. Is performance measurement and management fit for the

future?. Management Accounting Research. 25(2). pp.173-186.

Nitzl, C., 2016. The use of partial least squares structural equation modelling (PLS-SEM) in

management accounting research: Directions for future theory development. Journal of

Accounting Literature. 37. pp.19-35.

Quattrone, P., 2016. Management accounting goes digital: Will the move make it

wiser?. Management Accounting Research. 31. pp.118-122.

Smith, M., 2017. Research methods in accounting. Sage.

Talbot, D. and Boiral, O., 2018. GHG reporting and impression management: An assessment of

sustainability reports from the energy sector. Journal of Business Ethics. 147(2).

pp.367-383.

Tucker, B. P. and Lowe, A. D., 2014. Practitioners are from Mars; academics are from Venus?:

An investigation of the research-practice gap in management accounting. Accounting,

Auditing & Accountability Journal. 27(3). pp.394-425.

West, A., 2018. After virtue and accounting ethics. Journal of Business Ethics. 148(1). pp.21-

36.

Wnuk-Pel, T., 2016. MANAGEMENT ACCOUNTING SYSTEMS AND LEAN

MANAGEMENT: A SERVICE COMPANY PERSPECTIVE. Transformations in

Business & Economics. 15(1).

Online

Budget. 2019. [Online]. Available through:

<https://www.mymoneycoach.ca/budgeting/what-is-a-budget-planning-forecasting/>

23

Books & Journals

Al-Qady, M. and El-Helbawy, S., 2016. Integrating Target Costing and Resource Consumption

Accounting. Journal of Applied Management Accounting Research. 14(1).

Aouni, B., McGillis, S. and Abdulkarim, M. E., 2017. Goal programming model for management

accounting and auditing: a new typology. Annals of Operations Research. 251(1-2).

pp.41-54.

Chenhall, R. H. and Moers, F., 2015. The role of innovation in the evolution of management

accounting and its integration into management control. Accounting, organizations and

society. 47. pp.1-13.

Englund, H. and Gerdin, J., 2014. Structuration theory in accounting research: Applications and

applicability. Critical Perspectives on Accounting. 25(2). pp.162-180.

Goh, E. and Scerri, M., 2016. “I study accounting because I have to”: An exploratory study of

hospitality students’ attitudes toward accounting education. Journal of Hospitality &

Tourism Education. 28(2). pp.85-94.

Jefrey, C. ed., 2018. Research on professional responsibility and ethics in accounting. Emerald

Publishing Limited.

Maas, K., Schaltegger, S. and Crutzen, N., 2016. Integrating corporate sustainability assessment,

management accounting, control, and reporting. Journal of Cleaner Production. 136.

pp.237-248.

Melnyk, S. A. and et.al., 2014. Is performance measurement and management fit for the

future?. Management Accounting Research. 25(2). pp.173-186.

Nitzl, C., 2016. The use of partial least squares structural equation modelling (PLS-SEM) in

management accounting research: Directions for future theory development. Journal of

Accounting Literature. 37. pp.19-35.

Quattrone, P., 2016. Management accounting goes digital: Will the move make it

wiser?. Management Accounting Research. 31. pp.118-122.

Smith, M., 2017. Research methods in accounting. Sage.

Talbot, D. and Boiral, O., 2018. GHG reporting and impression management: An assessment of

sustainability reports from the energy sector. Journal of Business Ethics. 147(2).

pp.367-383.

Tucker, B. P. and Lowe, A. D., 2014. Practitioners are from Mars; academics are from Venus?:

An investigation of the research-practice gap in management accounting. Accounting,

Auditing & Accountability Journal. 27(3). pp.394-425.

West, A., 2018. After virtue and accounting ethics. Journal of Business Ethics. 148(1). pp.21-

36.

Wnuk-Pel, T., 2016. MANAGEMENT ACCOUNTING SYSTEMS AND LEAN

MANAGEMENT: A SERVICE COMPANY PERSPECTIVE. Transformations in

Business & Economics. 15(1).

Online

Budget. 2019. [Online]. Available through:

<https://www.mymoneycoach.ca/budgeting/what-is-a-budget-planning-forecasting/>

23

1 out of 25

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

© 2024 | Zucol Services PVT LTD | All rights reserved.