Managerial Finance Portfolio 1: Financial Ratio Analysis Report

VerifiedAdded on 2023/01/17

|17

|3445

|22

Report

AI Summary

This report presents a comprehensive analysis of Managerial Finance Portfolio 1, focusing on ratio analysis and company performance. It begins with the computation of various financial ratios for Glaxo Smith and Reckitt Benckiser Group Plc, including current ratio, quick ratio, net profit margin, gross profit margin, gearing ratio, price-earnings ratio, earnings per share, return on capital employed, inventory turnover ratio, and dividend payout ratio. The report then assesses the performance of both companies based on these ratios, highlighting their strengths and weaknesses in terms of liquidity, profitability, solvency, and efficiency. Following the assessment, it offers specific recommendations for improving the financial ratios of each company. The report also discusses the limitations of using financial ratios in financial analysis.

Managerial Finance

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of Contents

Portfolio 1........................................................................................................................................3

a. computation of ratios ...............................................................................................................3

b. Assessing performance of both the companies .......................................................................5

c. Recommendations for improving the ratio of the company ....................................................7

d. Limitations of financial ratios..................................................................................................8

Portfolio 2........................................................................................................................................9

a. Advising the most suitable project that needs to be selected by top management................12

b. Limitations of using capital budgeting techniques in the longer period for the purpose of

decision making ........................................................................................................................12

REFERENCES................................................................................................................................1

Portfolio 1........................................................................................................................................3

a. computation of ratios ...............................................................................................................3

b. Assessing performance of both the companies .......................................................................5

c. Recommendations for improving the ratio of the company ....................................................7

d. Limitations of financial ratios..................................................................................................8

Portfolio 2........................................................................................................................................9

a. Advising the most suitable project that needs to be selected by top management................12

b. Limitations of using capital budgeting techniques in the longer period for the purpose of

decision making ........................................................................................................................12

REFERENCES................................................................................................................................1

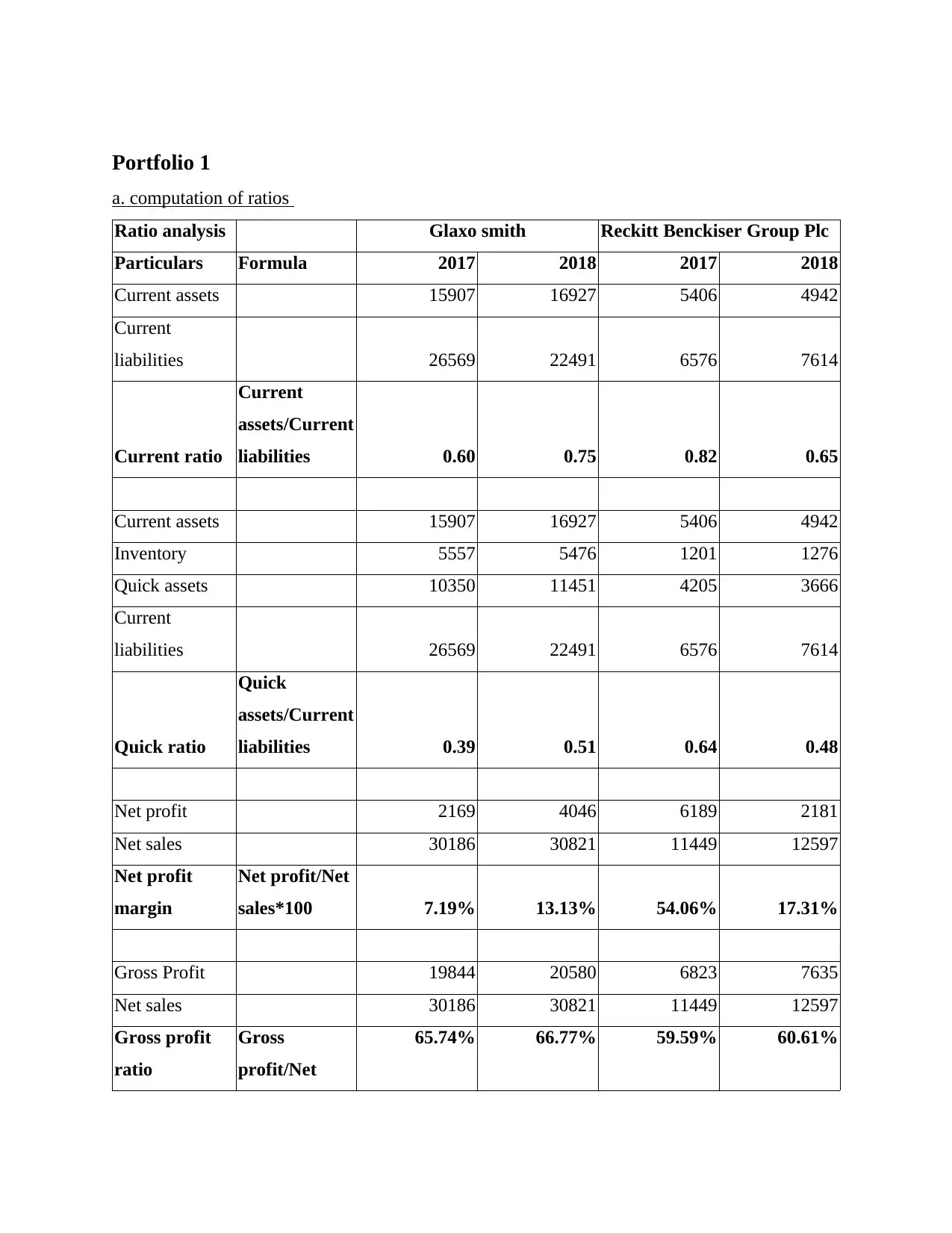

Portfolio 1

a. computation of ratios

Ratio analysis Glaxo smith Reckitt Benckiser Group Plc

Particulars Formula 2017 2018 2017 2018

Current assets 15907 16927 5406 4942

Current

liabilities 26569 22491 6576 7614

Current ratio

Current

assets/Current

liabilities 0.60 0.75 0.82 0.65

Current assets 15907 16927 5406 4942

Inventory 5557 5476 1201 1276

Quick assets 10350 11451 4205 3666

Current

liabilities 26569 22491 6576 7614

Quick ratio

Quick

assets/Current

liabilities 0.39 0.51 0.64 0.48

Net profit 2169 4046 6189 2181

Net sales 30186 30821 11449 12597

Net profit

margin

Net profit/Net

sales*100 7.19% 13.13% 54.06% 17.31%

Gross Profit 19844 20580 6823 7635

Net sales 30186 30821 11449 12597

Gross profit

ratio

Gross

profit/Net

65.74% 66.77% 59.59% 60.61%

a. computation of ratios

Ratio analysis Glaxo smith Reckitt Benckiser Group Plc

Particulars Formula 2017 2018 2017 2018

Current assets 15907 16927 5406 4942

Current

liabilities 26569 22491 6576 7614

Current ratio

Current

assets/Current

liabilities 0.60 0.75 0.82 0.65

Current assets 15907 16927 5406 4942

Inventory 5557 5476 1201 1276

Quick assets 10350 11451 4205 3666

Current

liabilities 26569 22491 6576 7614

Quick ratio

Quick

assets/Current

liabilities 0.39 0.51 0.64 0.48

Net profit 2169 4046 6189 2181

Net sales 30186 30821 11449 12597

Net profit

margin

Net profit/Net

sales*100 7.19% 13.13% 54.06% 17.31%

Gross Profit 19844 20580 6823 7635

Net sales 30186 30821 11449 12597

Gross profit

ratio

Gross

profit/Net

65.74% 66.77% 59.59% 60.61%

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

sales*100

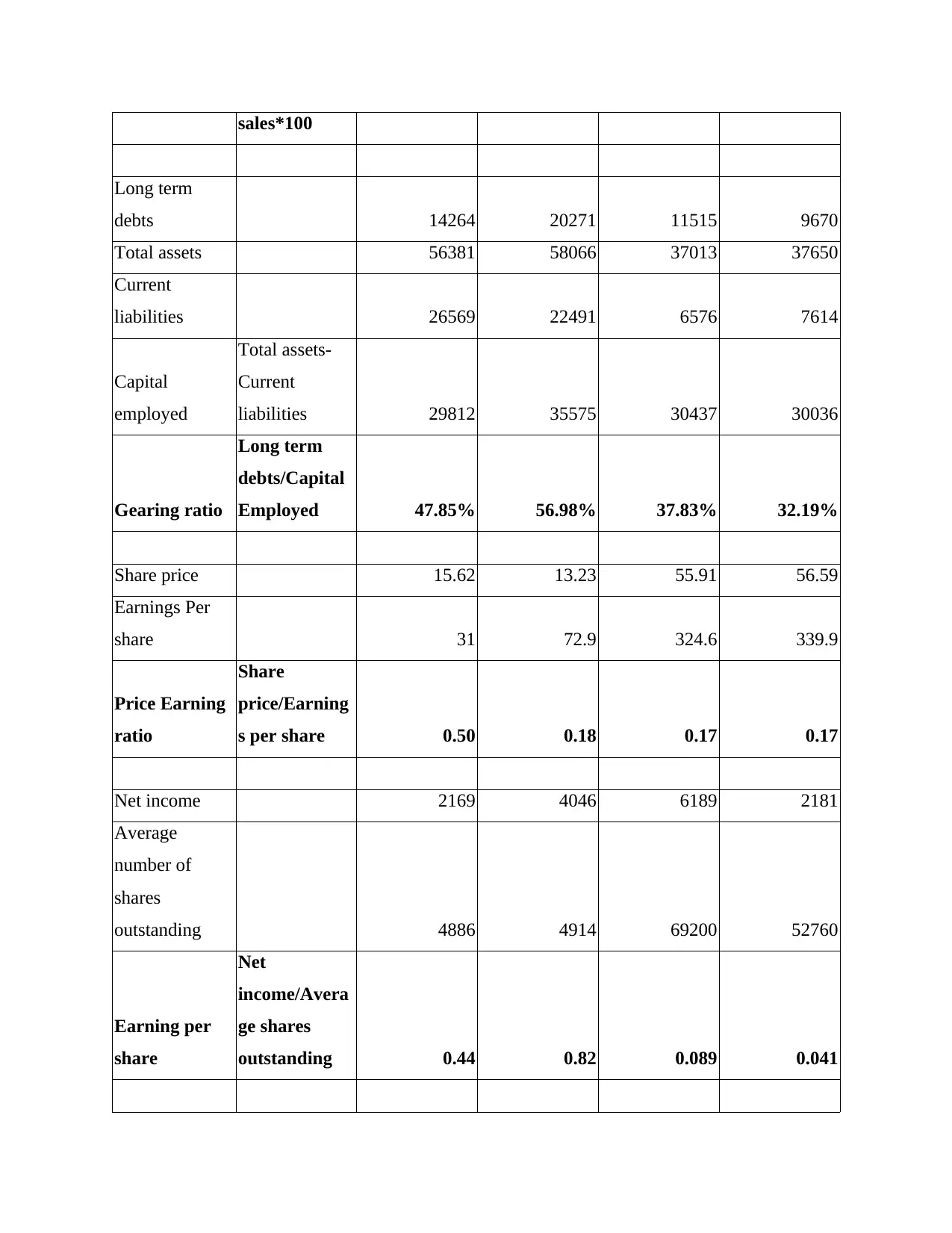

Long term

debts 14264 20271 11515 9670

Total assets 56381 58066 37013 37650

Current

liabilities 26569 22491 6576 7614

Capital

employed

Total assets-

Current

liabilities 29812 35575 30437 30036

Gearing ratio

Long term

debts/Capital

Employed 47.85% 56.98% 37.83% 32.19%

Share price 15.62 13.23 55.91 56.59

Earnings Per

share 31 72.9 324.6 339.9

Price Earning

ratio

Share

price/Earning

s per share 0.50 0.18 0.17 0.17

Net income 2169 4046 6189 2181

Average

number of

shares

outstanding 4886 4914 69200 52760

Earning per

share

Net

income/Avera

ge shares

outstanding 0.44 0.82 0.089 0.041

Long term

debts 14264 20271 11515 9670

Total assets 56381 58066 37013 37650

Current

liabilities 26569 22491 6576 7614

Capital

employed

Total assets-

Current

liabilities 29812 35575 30437 30036

Gearing ratio

Long term

debts/Capital

Employed 47.85% 56.98% 37.83% 32.19%

Share price 15.62 13.23 55.91 56.59

Earnings Per

share 31 72.9 324.6 339.9

Price Earning

ratio

Share

price/Earning

s per share 0.50 0.18 0.17 0.17

Net income 2169 4046 6189 2181

Average

number of

shares

outstanding 4886 4914 69200 52760

Earning per

share

Net

income/Avera

ge shares

outstanding 0.44 0.82 0.089 0.041

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

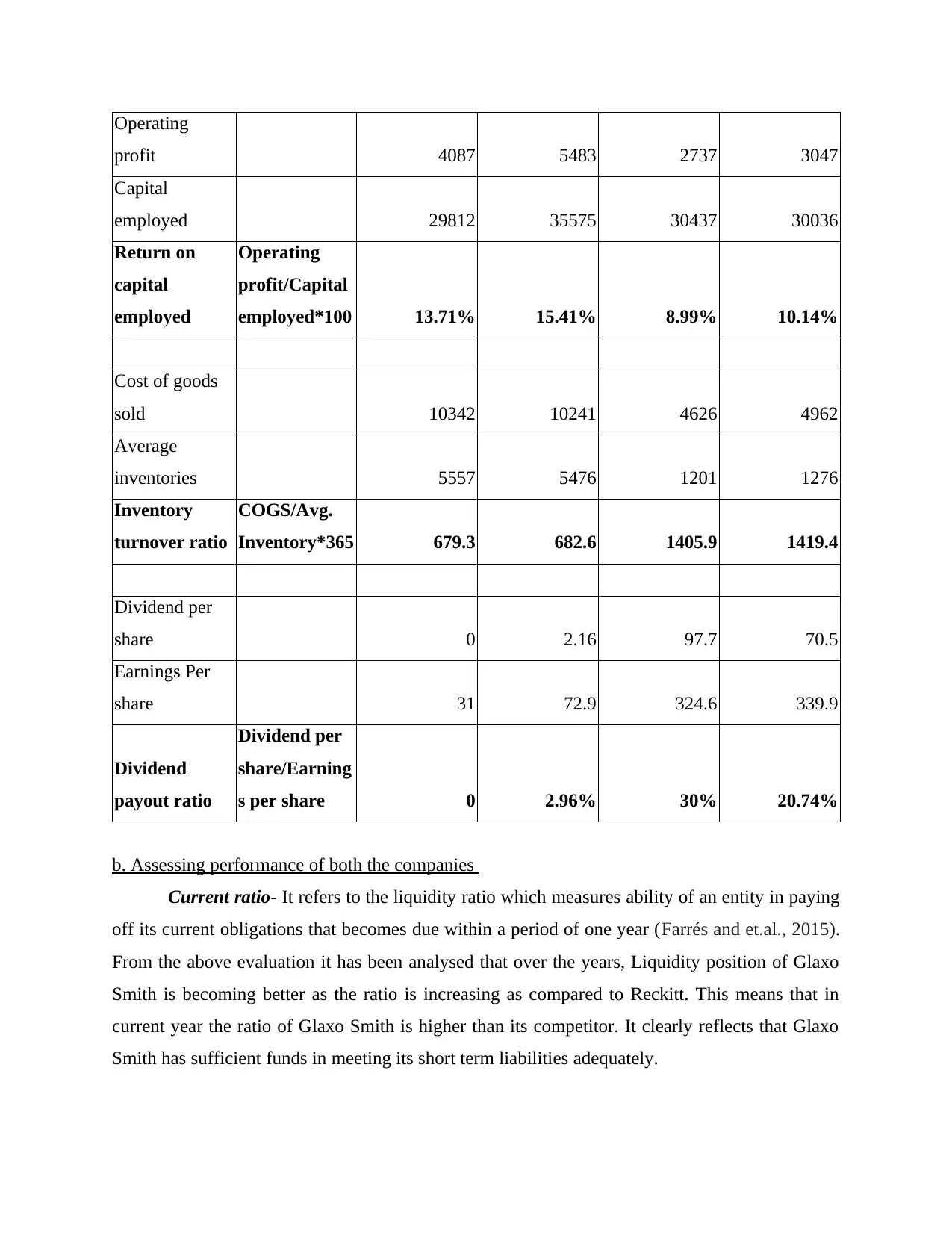

Operating

profit 4087 5483 2737 3047

Capital

employed 29812 35575 30437 30036

Return on

capital

employed

Operating

profit/Capital

employed*100 13.71% 15.41% 8.99% 10.14%

Cost of goods

sold 10342 10241 4626 4962

Average

inventories 5557 5476 1201 1276

Inventory

turnover ratio

COGS/Avg.

Inventory*365 679.3 682.6 1405.9 1419.4

Dividend per

share 0 2.16 97.7 70.5

Earnings Per

share 31 72.9 324.6 339.9

Dividend

payout ratio

Dividend per

share/Earning

s per share 0 2.96% 30% 20.74%

b. Assessing performance of both the companies

Current ratio- It refers to the liquidity ratio which measures ability of an entity in paying

off its current obligations that becomes due within a period of one year (Farrés and et.al., 2015).

From the above evaluation it has been analysed that over the years, Liquidity position of Glaxo

Smith is becoming better as the ratio is increasing as compared to Reckitt. This means that in

current year the ratio of Glaxo Smith is higher than its competitor. It clearly reflects that Glaxo

Smith has sufficient funds in meeting its short term liabilities adequately.

profit 4087 5483 2737 3047

Capital

employed 29812 35575 30437 30036

Return on

capital

employed

Operating

profit/Capital

employed*100 13.71% 15.41% 8.99% 10.14%

Cost of goods

sold 10342 10241 4626 4962

Average

inventories 5557 5476 1201 1276

Inventory

turnover ratio

COGS/Avg.

Inventory*365 679.3 682.6 1405.9 1419.4

Dividend per

share 0 2.16 97.7 70.5

Earnings Per

share 31 72.9 324.6 339.9

Dividend

payout ratio

Dividend per

share/Earning

s per share 0 2.96% 30% 20.74%

b. Assessing performance of both the companies

Current ratio- It refers to the liquidity ratio which measures ability of an entity in paying

off its current obligations that becomes due within a period of one year (Farrés and et.al., 2015).

From the above evaluation it has been analysed that over the years, Liquidity position of Glaxo

Smith is becoming better as the ratio is increasing as compared to Reckitt. This means that in

current year the ratio of Glaxo Smith is higher than its competitor. It clearly reflects that Glaxo

Smith has sufficient funds in meeting its short term liabilities adequately.

Quick ratio- It means the financial ratio that is been used for gauging liquidity and also

called as acid test ratio. It shows the capability of the company in respect to meet its liability

with immediate funds (Faello, 2015). This ratio compares sum of the cash and cash equivalent

along with marketable securities and account receivable with that of its short term liabilities. As

per the computation, it has been assessed that in the year 2017, the quick ratio of Reckitt is

higher that is 0.64 from Glaxo Smith resulted as 0.39 which indicates better liquidity of the

Reckitt. However, as the year passes the ratio of Glaxo Smith has increased and resulted as

greater than its rivalry which means that its immediate liquidity position has improved from one

period to another.

Net profit margin- It measures or reveals the profitability that an enterprise will earn

from that of its overall sales revenue (Mechler, 2016). In other words, it is the revenue

percentage that is left out after payment of all the expenses deducted or subtracted from the sales

(Sebastiani and et.al., 2017). The net profit ratio of Reckitt is seen as higher than Glaxo Smith in

both the years that is 2017 and 2018. This means that overall profitability performance of Reckitt

is better than its competitors. The resulted ratio in 2017 of Reckitt equated as 54.06% and Glaxo

Smith as 7.19% , this shows a larger difference in the profit earning of the companies after

meeting their expense, cost and tax liability. Similarly, In year 2018, the ratio of the Glaxo smith

accounted as 13.13% while of Reckitt attained as 17.31% (Financial statement of Reckitt, 2018).

Gross profit margin- It means that metric that is been sued for accessing financial health

and the business model of the company by way of revealing the amount of the money left with

that from the revenue after reducing the cost of sales (Maktoomi, Hashmi and Ghannouchi,

2017). This ratio is been expressed as sales percentage and is called as gross margin. From the

analysis it has been stated that the gross profit ratio of Glaxo Smith is better than Reckitt as it is

resulting a higher ratio. This shows that Glaxo Smith is generating large amount of profitability

after paying off its variable cost that occurs in relation to production of the goods and the

services.

Gearing ratio- It means the financial ratio that compares debt of the company towards

different or various financial metrics like total equity. It represents leverage position of the an

entity which reflects determination of the amount of funding is been made through the borrowed

funds against the owners funds (Alkaraan, 2017). A higher ratio presents the higher proportion

of the equity and the debt whereas the lower gearing ratio presents a small proportion of the debt

called as acid test ratio. It shows the capability of the company in respect to meet its liability

with immediate funds (Faello, 2015). This ratio compares sum of the cash and cash equivalent

along with marketable securities and account receivable with that of its short term liabilities. As

per the computation, it has been assessed that in the year 2017, the quick ratio of Reckitt is

higher that is 0.64 from Glaxo Smith resulted as 0.39 which indicates better liquidity of the

Reckitt. However, as the year passes the ratio of Glaxo Smith has increased and resulted as

greater than its rivalry which means that its immediate liquidity position has improved from one

period to another.

Net profit margin- It measures or reveals the profitability that an enterprise will earn

from that of its overall sales revenue (Mechler, 2016). In other words, it is the revenue

percentage that is left out after payment of all the expenses deducted or subtracted from the sales

(Sebastiani and et.al., 2017). The net profit ratio of Reckitt is seen as higher than Glaxo Smith in

both the years that is 2017 and 2018. This means that overall profitability performance of Reckitt

is better than its competitors. The resulted ratio in 2017 of Reckitt equated as 54.06% and Glaxo

Smith as 7.19% , this shows a larger difference in the profit earning of the companies after

meeting their expense, cost and tax liability. Similarly, In year 2018, the ratio of the Glaxo smith

accounted as 13.13% while of Reckitt attained as 17.31% (Financial statement of Reckitt, 2018).

Gross profit margin- It means that metric that is been sued for accessing financial health

and the business model of the company by way of revealing the amount of the money left with

that from the revenue after reducing the cost of sales (Maktoomi, Hashmi and Ghannouchi,

2017). This ratio is been expressed as sales percentage and is called as gross margin. From the

analysis it has been stated that the gross profit ratio of Glaxo Smith is better than Reckitt as it is

resulting a higher ratio. This shows that Glaxo Smith is generating large amount of profitability

after paying off its variable cost that occurs in relation to production of the goods and the

services.

Gearing ratio- It means the financial ratio that compares debt of the company towards

different or various financial metrics like total equity. It represents leverage position of the an

entity which reflects determination of the amount of funding is been made through the borrowed

funds against the owners funds (Alkaraan, 2017). A higher ratio presents the higher proportion

of the equity and the debt whereas the lower gearing ratio presents a small proportion of the debt

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

to an equity. As per the assessment, it has been identified that the solvency or leverage position

of Reckitt seems to be better or sound that Glaxo Smith as it results a lower ratio which clearly

indicates that it has made less use of borrowed funds fro funding its investment or projects over

its equities.

Price earning ratio- This ratio is the measure of present share price of an enterprise in

comparison to the earning per share. Higher ratio depicts that an investor is been willing to pay

more for gaining the profits. It indicates an expected price of the shares on the basis of its

earnings (Throsby, 2016). As earnings of the company is rising then its market value for per

share also increases. Higher P/E ratio reflects positive and better performance of the firm and in

turn depicts that an investor is ready to pay more for the company's shares. From computation, it

has been determined that the ratio of Glaxo Smith is greater than Reckitt which in turn shows

that the company will be performing better in the future periods.

Earnings per share- It means the profits that are earned by the company in respect of the

each and every share of their shares or stock. Higher EPS reflects greater value as investors will

have to pay more for the company which is generating higher amount of profits. The Earning per

share of Glaxo Smith resulted as high than Reckitt which mean that the former company is

earnings greater value towards its each and every shares. This in turn reflects sound financial

position of Glaxo Smith in comparison to Reckitt.

Return on capital employed- It is the profitability ratio which measures the ways in

which an entity can efficiently generate profits from that of its invested capital by making

comparison of the net operating margin to that of capital employed (Gülbahar and Tinmaz,

2016). Higher value of Return on capital employed depicts that the larger amount of the earnings

or profits could be plough back into the other projects of the firm for ensuring benefits to the

shareholders. In accordance to the ratio analysis it has been stated that ROCE of Glaxo Smith is

much better than Reckitt in the last 2 years that is 2017 and 2018 (Annual report of Glaxo Smith,

2018). This means that Glaxo Smith is making an efficient and effective use of its capital for

generating larger profitability as compared to its rivalry.

Inventory Turnover period- It referred as the ratio which shows the number of times an

entity has replaced and sold its inventory during the given period. Thereafter a company could

divide days within the period by the formula of inventory turnover for computing days that it

takes in selling an inventory on the hand. In other words, it states number of the days taken by

of Reckitt seems to be better or sound that Glaxo Smith as it results a lower ratio which clearly

indicates that it has made less use of borrowed funds fro funding its investment or projects over

its equities.

Price earning ratio- This ratio is the measure of present share price of an enterprise in

comparison to the earning per share. Higher ratio depicts that an investor is been willing to pay

more for gaining the profits. It indicates an expected price of the shares on the basis of its

earnings (Throsby, 2016). As earnings of the company is rising then its market value for per

share also increases. Higher P/E ratio reflects positive and better performance of the firm and in

turn depicts that an investor is ready to pay more for the company's shares. From computation, it

has been determined that the ratio of Glaxo Smith is greater than Reckitt which in turn shows

that the company will be performing better in the future periods.

Earnings per share- It means the profits that are earned by the company in respect of the

each and every share of their shares or stock. Higher EPS reflects greater value as investors will

have to pay more for the company which is generating higher amount of profits. The Earning per

share of Glaxo Smith resulted as high than Reckitt which mean that the former company is

earnings greater value towards its each and every shares. This in turn reflects sound financial

position of Glaxo Smith in comparison to Reckitt.

Return on capital employed- It is the profitability ratio which measures the ways in

which an entity can efficiently generate profits from that of its invested capital by making

comparison of the net operating margin to that of capital employed (Gülbahar and Tinmaz,

2016). Higher value of Return on capital employed depicts that the larger amount of the earnings

or profits could be plough back into the other projects of the firm for ensuring benefits to the

shareholders. In accordance to the ratio analysis it has been stated that ROCE of Glaxo Smith is

much better than Reckitt in the last 2 years that is 2017 and 2018 (Annual report of Glaxo Smith,

2018). This means that Glaxo Smith is making an efficient and effective use of its capital for

generating larger profitability as compared to its rivalry.

Inventory Turnover period- It referred as the ratio which shows the number of times an

entity has replaced and sold its inventory during the given period. Thereafter a company could

divide days within the period by the formula of inventory turnover for computing days that it

takes in selling an inventory on the hand. In other words, it states number of the days taken by

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

the firm on an average for turning its inventory into the sales. As seen in the analysis, it is been

viewed that ITR period of Glaxo Smith is efficient and better in comparison to Reckitt because it

is taking less time in converting its stock into the revenue than Reckitt.

Dividend payout ratio- This ratio means total amount of the dividend that is been paid to

the shareholders in respect to the net profit of an enterprise. It means the percentage of an

earnings paid to the shareholders in form of dividend (Mietzner and Reger, 2015). The

evaluation shows that the payout ratio of Reckitt is good in comparison to Glaxo Smith as it is

distributing higher percentage of the dividends to its shareholders than its rivalry which in turn

indicates that more profits are generated by an enterprise.

c. Recommendations for improving the ratio of the company

Overall it has been reviewed that profitability, solvency, liquidity and efficiency of Glaxo

Smith is seen as better than Reckitt. As the current ratio and quick ratio of Reckitt is falling, this

means that it needs to take corrective action for improving its liquidity position such as paying

off its current liabilities, selling off an unproductive assets, Improving its short term assets by

increasing the shareholders funds, ensuring fast conversion cycle of the debtors or an accounts

receivables. In order its gross profit margins, Reckitt must take appropriate measures like

increasing prices, enhancing sales, taking cash discounts from its suppliers, not competing on the

prices and preventing thefts. It should pay the dividends that could cause a rise in the price

earning ratio of the company. For the purpose of increasing an earning per share, Reckitt should

increase its revenues with rising the prices and volume of production along with it decrease or

keep control over the cost so that higher earnings can be generated in respect to each shares. The

return on capital employed ratio of Reckitt is also seen as lower so it should reduce value of its

capital employed in order maintain its operating profits that in turn helps in improving the ROCE

ratio. Lastly, for improving inventory turnover days, Reckitt should save the time, makes more

and more automation, better forecasting and optimizing the supply chain.

d. Limitations of financial ratios

Financial analysis through the use of ratio analysis tool as it highlights a relationships

between the items in the final reports. However, there are various limitations that should be kept

in the mind at the time of preparing or using it are as follows-

Ratios are mainly evaluated on the basis of the accounting figures that are given or

provided in the final reports. This reflects that accounting figures itself contains

viewed that ITR period of Glaxo Smith is efficient and better in comparison to Reckitt because it

is taking less time in converting its stock into the revenue than Reckitt.

Dividend payout ratio- This ratio means total amount of the dividend that is been paid to

the shareholders in respect to the net profit of an enterprise. It means the percentage of an

earnings paid to the shareholders in form of dividend (Mietzner and Reger, 2015). The

evaluation shows that the payout ratio of Reckitt is good in comparison to Glaxo Smith as it is

distributing higher percentage of the dividends to its shareholders than its rivalry which in turn

indicates that more profits are generated by an enterprise.

c. Recommendations for improving the ratio of the company

Overall it has been reviewed that profitability, solvency, liquidity and efficiency of Glaxo

Smith is seen as better than Reckitt. As the current ratio and quick ratio of Reckitt is falling, this

means that it needs to take corrective action for improving its liquidity position such as paying

off its current liabilities, selling off an unproductive assets, Improving its short term assets by

increasing the shareholders funds, ensuring fast conversion cycle of the debtors or an accounts

receivables. In order its gross profit margins, Reckitt must take appropriate measures like

increasing prices, enhancing sales, taking cash discounts from its suppliers, not competing on the

prices and preventing thefts. It should pay the dividends that could cause a rise in the price

earning ratio of the company. For the purpose of increasing an earning per share, Reckitt should

increase its revenues with rising the prices and volume of production along with it decrease or

keep control over the cost so that higher earnings can be generated in respect to each shares. The

return on capital employed ratio of Reckitt is also seen as lower so it should reduce value of its

capital employed in order maintain its operating profits that in turn helps in improving the ROCE

ratio. Lastly, for improving inventory turnover days, Reckitt should save the time, makes more

and more automation, better forecasting and optimizing the supply chain.

d. Limitations of financial ratios

Financial analysis through the use of ratio analysis tool as it highlights a relationships

between the items in the final reports. However, there are various limitations that should be kept

in the mind at the time of preparing or using it are as follows-

Ratios are mainly evaluated on the basis of the accounting figures that are given or

provided in the final reports. This reflects that accounting figures itself contains

deficiencies, estimations, diversity and manipulation up-to some extent. Thus, ratios are

not considered as helpful in drawing the reliable conclusions.

It comprises of inherent comparability problem as every company uses different methods

of accounting that could cause problems in respect of comparing key relationship

between them.

Inflation might limit utility of an accounting ratios because of inflation, historical cost

related final reports and an accounting figures that does not reflects present value figures,

specifically in case of purchasing an assets at the different dates by the different

enterprises. As final reports are not been adjusted in context of an inflation effect,

accounting ratios that contains distortions and in becoming deceptive.

Financial ratios are not entirely dependable and it must be used after facilitating due

weights to the general economic circumstances, situation of an industry, firm's position,

mode of an operations, product diversity that could make a business entity wholly

dissimilar and hence impacts calculation of an accounting ratios.

The different ways that is been adopted by the firm for computing results also influences

utility of an accounting ratios. There are several concepts which is been used for

identifying the numerator and the denominator in specific type of accounting ratio that

will not be helping in drawing the reliable conclusions in an identical situations.

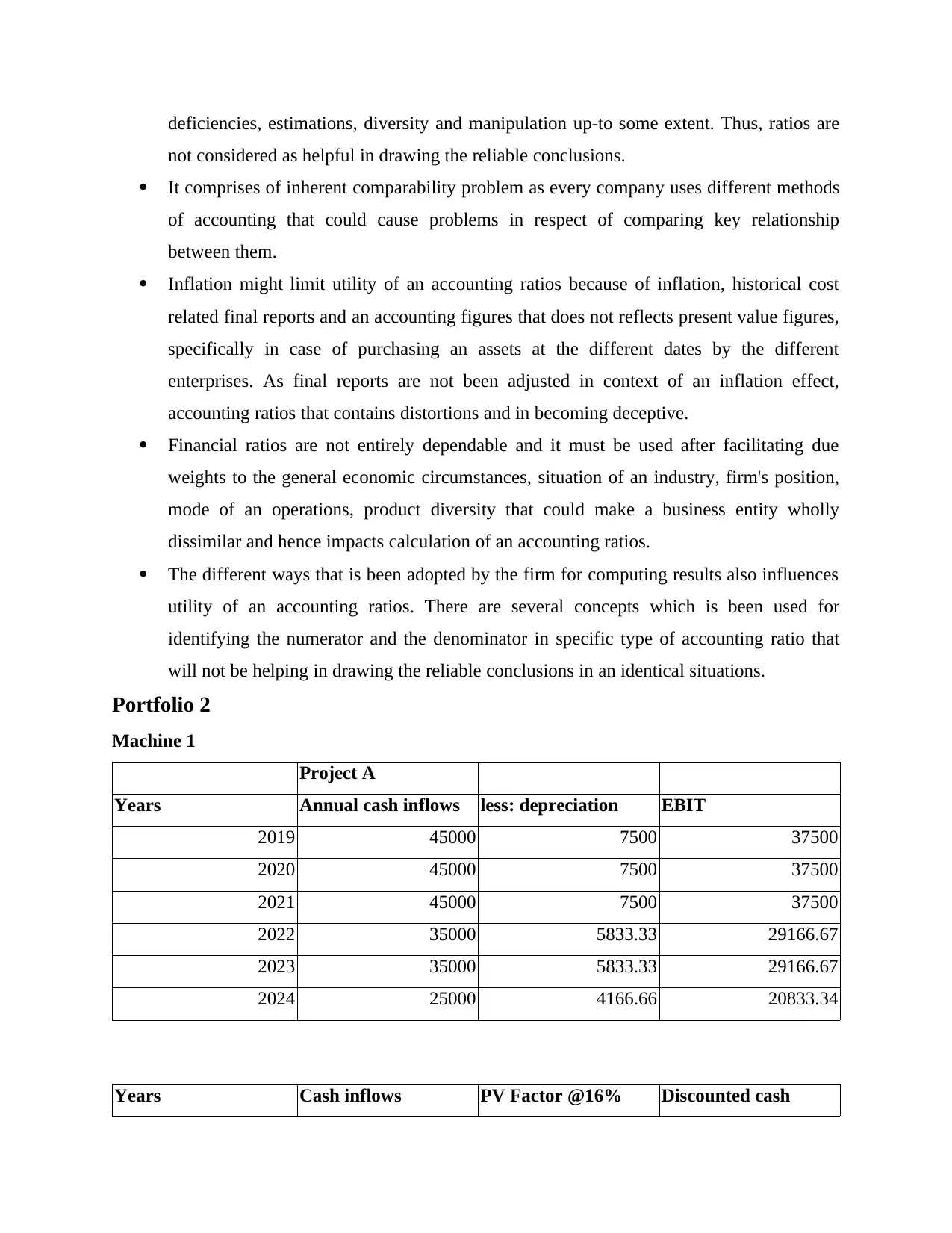

Portfolio 2

Machine 1

Project A

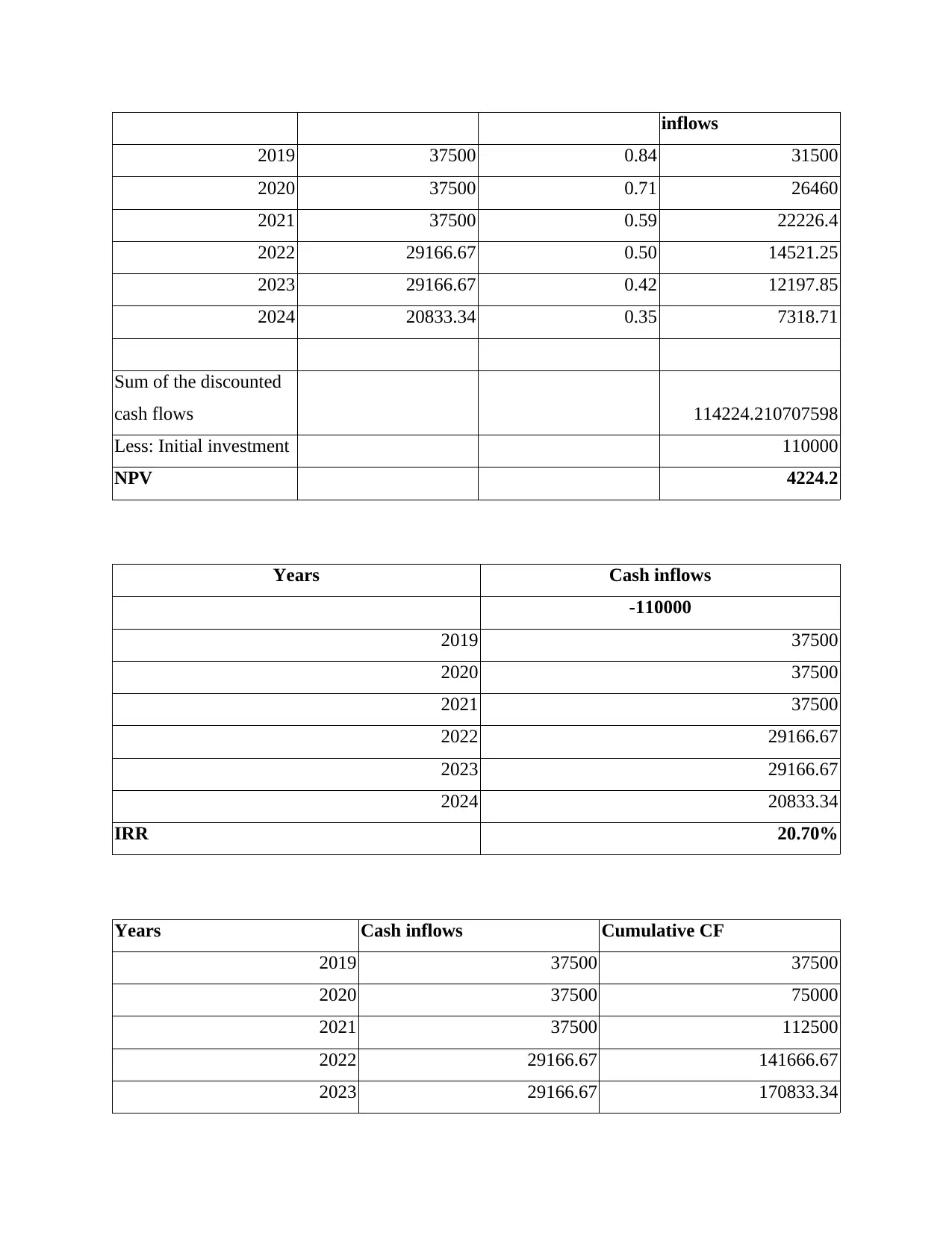

Years Annual cash inflows less: depreciation EBIT

2019 45000 7500 37500

2020 45000 7500 37500

2021 45000 7500 37500

2022 35000 5833.33 29166.67

2023 35000 5833.33 29166.67

2024 25000 4166.66 20833.34

Years Cash inflows PV Factor @16% Discounted cash

not considered as helpful in drawing the reliable conclusions.

It comprises of inherent comparability problem as every company uses different methods

of accounting that could cause problems in respect of comparing key relationship

between them.

Inflation might limit utility of an accounting ratios because of inflation, historical cost

related final reports and an accounting figures that does not reflects present value figures,

specifically in case of purchasing an assets at the different dates by the different

enterprises. As final reports are not been adjusted in context of an inflation effect,

accounting ratios that contains distortions and in becoming deceptive.

Financial ratios are not entirely dependable and it must be used after facilitating due

weights to the general economic circumstances, situation of an industry, firm's position,

mode of an operations, product diversity that could make a business entity wholly

dissimilar and hence impacts calculation of an accounting ratios.

The different ways that is been adopted by the firm for computing results also influences

utility of an accounting ratios. There are several concepts which is been used for

identifying the numerator and the denominator in specific type of accounting ratio that

will not be helping in drawing the reliable conclusions in an identical situations.

Portfolio 2

Machine 1

Project A

Years Annual cash inflows less: depreciation EBIT

2019 45000 7500 37500

2020 45000 7500 37500

2021 45000 7500 37500

2022 35000 5833.33 29166.67

2023 35000 5833.33 29166.67

2024 25000 4166.66 20833.34

Years Cash inflows PV Factor @16% Discounted cash

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

inflows

2019 37500 0.84 31500

2020 37500 0.71 26460

2021 37500 0.59 22226.4

2022 29166.67 0.50 14521.25

2023 29166.67 0.42 12197.85

2024 20833.34 0.35 7318.71

Sum of the discounted

cash flows 114224.210707598

Less: Initial investment 110000

NPV 4224.2

Years Cash inflows

-110000

2019 37500

2020 37500

2021 37500

2022 29166.67

2023 29166.67

2024 20833.34

IRR 20.70%

Years Cash inflows Cumulative CF

2019 37500 37500

2020 37500 75000

2021 37500 112500

2022 29166.67 141666.67

2023 29166.67 170833.34

2019 37500 0.84 31500

2020 37500 0.71 26460

2021 37500 0.59 22226.4

2022 29166.67 0.50 14521.25

2023 29166.67 0.42 12197.85

2024 20833.34 0.35 7318.71

Sum of the discounted

cash flows 114224.210707598

Less: Initial investment 110000

NPV 4224.2

Years Cash inflows

-110000

2019 37500

2020 37500

2021 37500

2022 29166.67

2023 29166.67

2024 20833.34

IRR 20.70%

Years Cash inflows Cumulative CF

2019 37500 37500

2020 37500 75000

2021 37500 112500

2022 29166.67 141666.67

2023 29166.67 170833.34

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

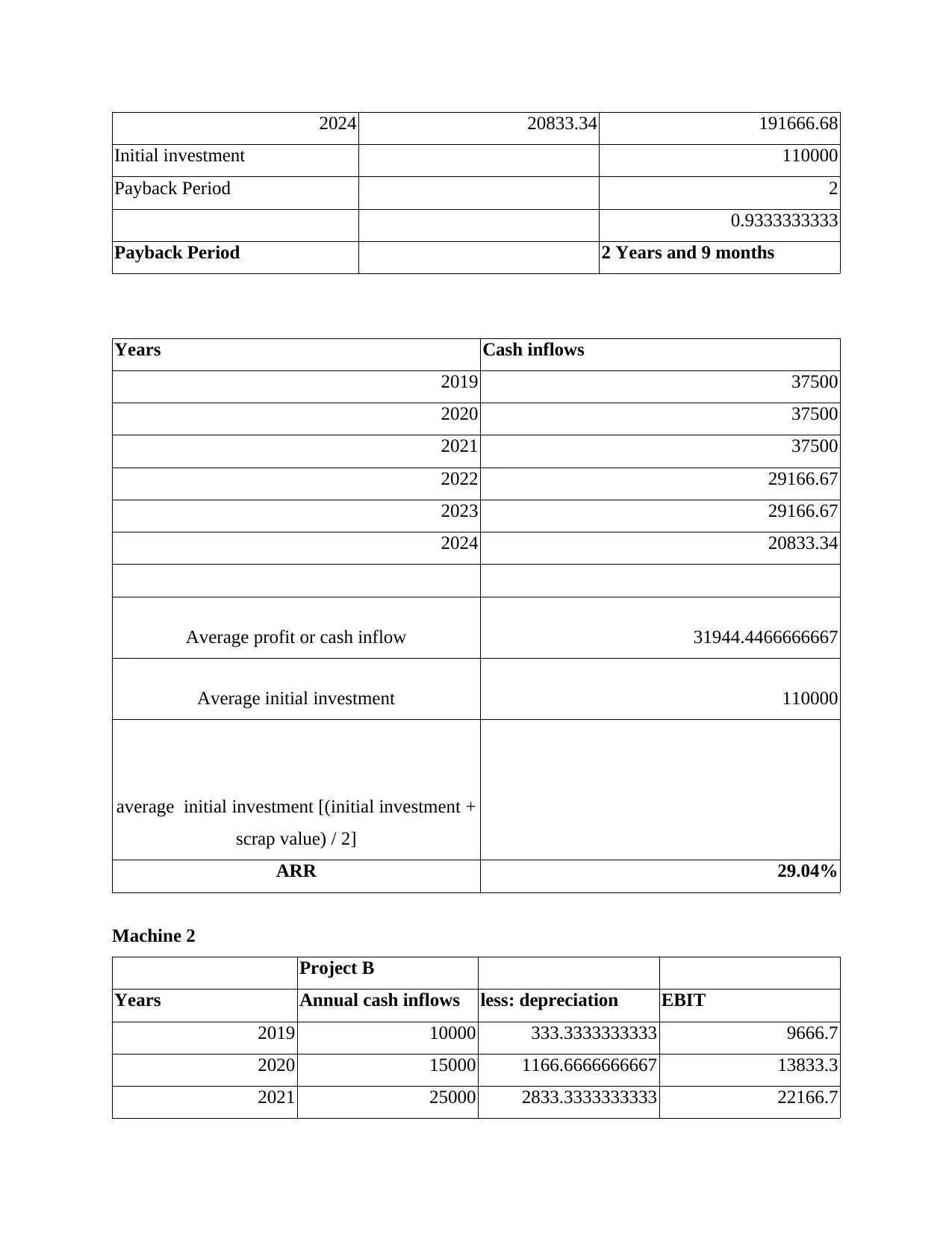

2024 20833.34 191666.68

Initial investment 110000

Payback Period 2

0.9333333333

Payback Period 2 Years and 9 months

Years Cash inflows

2019 37500

2020 37500

2021 37500

2022 29166.67

2023 29166.67

2024 20833.34

Average profit or cash inflow 31944.4466666667

Average initial investment 110000

average initial investment [(initial investment +

scrap value) / 2]

ARR 29.04%

Machine 2

Project B

Years Annual cash inflows less: depreciation EBIT

2019 10000 333.3333333333 9666.7

2020 15000 1166.6666666667 13833.3

2021 25000 2833.3333333333 22166.7

Initial investment 110000

Payback Period 2

0.9333333333

Payback Period 2 Years and 9 months

Years Cash inflows

2019 37500

2020 37500

2021 37500

2022 29166.67

2023 29166.67

2024 20833.34

Average profit or cash inflow 31944.4466666667

Average initial investment 110000

average initial investment [(initial investment +

scrap value) / 2]

ARR 29.04%

Machine 2

Project B

Years Annual cash inflows less: depreciation EBIT

2019 10000 333.3333333333 9666.7

2020 15000 1166.6666666667 13833.3

2021 25000 2833.3333333333 22166.7

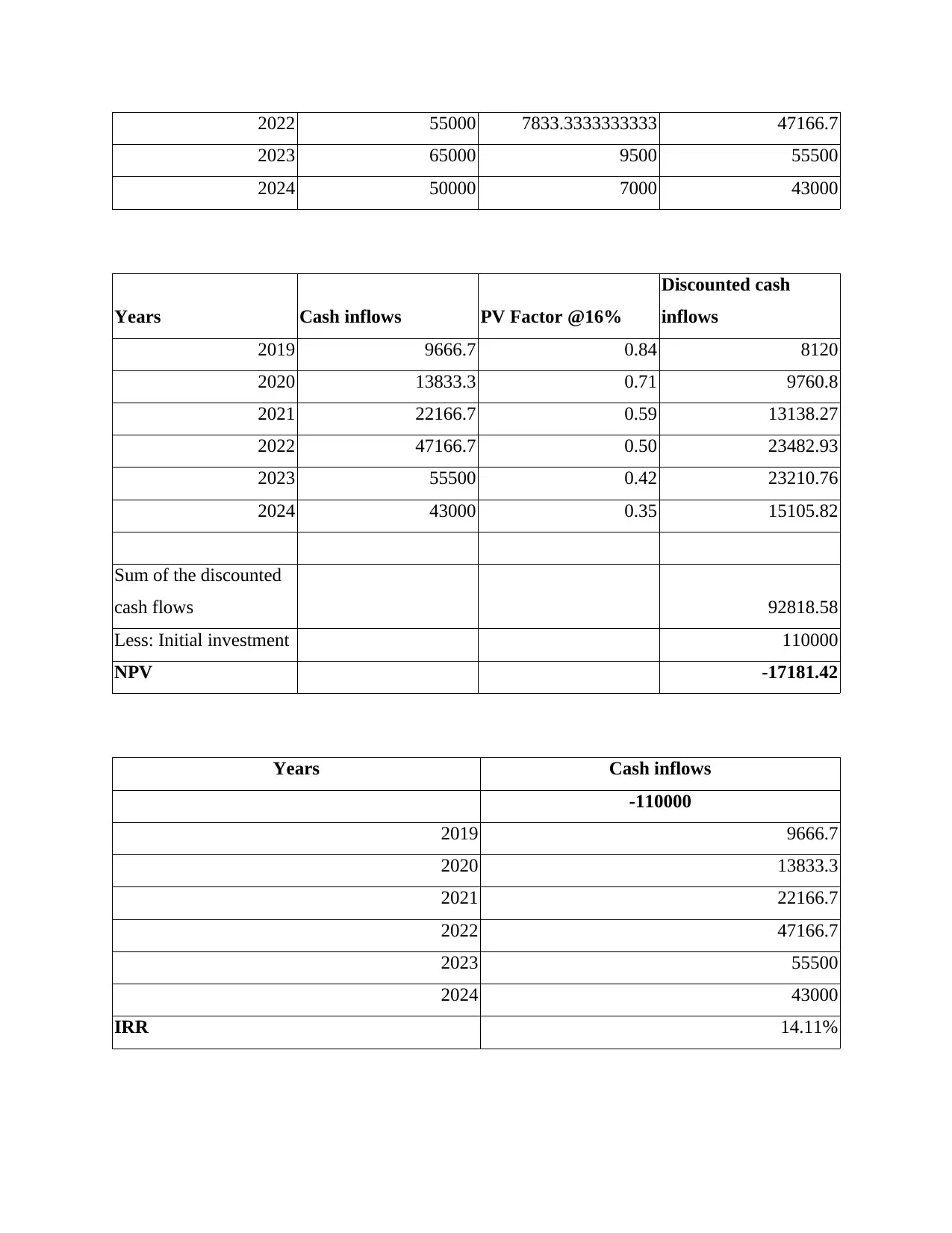

2022 55000 7833.3333333333 47166.7

2023 65000 9500 55500

2024 50000 7000 43000

Years Cash inflows PV Factor @16%

Discounted cash

inflows

2019 9666.7 0.84 8120

2020 13833.3 0.71 9760.8

2021 22166.7 0.59 13138.27

2022 47166.7 0.50 23482.93

2023 55500 0.42 23210.76

2024 43000 0.35 15105.82

Sum of the discounted

cash flows 92818.58

Less: Initial investment 110000

NPV -17181.42

Years Cash inflows

-110000

2019 9666.7

2020 13833.3

2021 22166.7

2022 47166.7

2023 55500

2024 43000

IRR 14.11%

2023 65000 9500 55500

2024 50000 7000 43000

Years Cash inflows PV Factor @16%

Discounted cash

inflows

2019 9666.7 0.84 8120

2020 13833.3 0.71 9760.8

2021 22166.7 0.59 13138.27

2022 47166.7 0.50 23482.93

2023 55500 0.42 23210.76

2024 43000 0.35 15105.82

Sum of the discounted

cash flows 92818.58

Less: Initial investment 110000

NPV -17181.42

Years Cash inflows

-110000

2019 9666.7

2020 13833.3

2021 22166.7

2022 47166.7

2023 55500

2024 43000

IRR 14.11%

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 17

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2025 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.